Summary

- BrasilAgro might face the risk of losing access to clients and an overvaluation of its land portfolio because of its sustainability impacts.

- Investors with forest policies might have most leverage through engagement with BrasilAgro’s parent company Cresud.

- BrasilAgro can course correct by addressing deforestation risks while improving returns via traceable products from farm to manufacturer.

BrasilAgro is a Brazilian rural real estate firm. It focuses on acquiring ‘underutilized and non-productive land’. It generates revenues by clearing and developing land and subsequently selling these rural properties. In addition, BrasilAgro produces soy, sugarcane, corn and livestock. BrasilAgro has 11 properties in its portfolio. The majority of its farms are in the Cerrado, a wooded grassland savanna and an environmentally sensitive area that sees high rates of deforestation since 2000. Most of the soy expansion has occurred by clearing native vegetation in the Matopiba region. The Matopiba region includes the Cerrado states of Maranhão, Tocantins, Piauí, and Bahia. The Cerrado is home to rich biodiversity, with 12,070 native plant species. It is also where many traditional communities reside, and it is an important source of water for all Brazilian regions. BrasilAgro’s activities in the Cerrado expose the company to deforestation-related business risks.

Key Findings

- BrasilAgro’s business model focuses on acquisition and transformation of Cerrado savanna into farmland. Its model relies on adding value to land by transforming underutilized or unproductive lands. This process of transforming land requires it to deforest native Cerrado vegetation. The value of BrasilAgro’s farmland portfolio increased by 146 percent in the last 10 years.

- Between 2012-2017, BrasilAgro has deforested 21,690 hectare (ha) of Cerrado vegetation. Most of the clearings took place at four of its farms:

- – 12,672 ha at Fazenda Chaparral, Bahia

- – 3,754 ha at Fazenda Preferencia, Bahia

- – 4,213 ha at Fazenda Jatoba, Bahia

- – 319 ha at Parceria II, Piauí.

- BrasilAgro might face the risk of losing access to clients and an overvaluation of its land portfolio because of its sustainability impacts. The soy market is moving towards zero-deforestation. In October 2017, a group of 23 consumer companies stated their support for the Cerrado Manifesto. Soy from recently deforested land might soon be barred from the supply chains of these companies. Recently deforested farms might also see less buyer interest.

- BrasilAgro’s investors could face an equity value loss of 21 percent. 26 percent of BrasilAgro’s agricultural commodity sales are to its top two customers in soy and corn, each of which have made zero-deforestation commitments. Losing access to these clients would result in a 4 percent equity loss. If the recently deforested farms were to lose 25 percent of their value, the value loss would amount to Real 125 million (USD 39 million) which would be equal to 17 percent of its current equity value, as of November 17, 2017.

- Investors with forest policies might have most leverage through engagement with BrasilAgro’s parent company Cresud. BrasilAgro is financed by USD 10 million through investors with policies on deforestation. Cresud is financed by USD 52 million in debt and USD 80 million in equity.

BrasilAgro’s Business Model Drives Deforestation

BrasilAgro is a publicly traded real estate company. Its headquarters are in São Paulo, Brazil. In 2006, CRESUD S.A.C.I.F., an Argentinean real estate firm, founded BrasilAgro in order to expand its rural land portfolio in Brazil. Cresud holds 40.7 percent of shares in BrasilAgro.

Land Transformation Drives Real Estate Value Appreciation

BrasilAgro’s business strategy is to acquire, develop, operate, and sell farmland. Core to its business strategy is the transformation of “underutilized and non-productive” land. The transformation of this land consists of clearing native vegetation, investing in infrastructure and developing agricultural activities. BrasilAgro’s website states:

“We believe that agricultural activity is fundamental not only to our non-real estate operating income, but also as a vector of appreciation of real estate value of properties.”

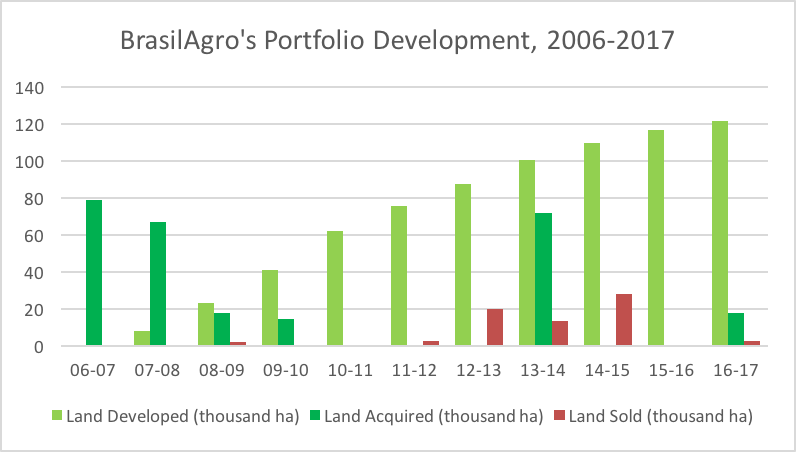

BrasilAgro also develops agricultural and livestock activities on these properties. As shown in Figure 1 (below), since 2006, it has acquired 266,599 ha of land, of which it has developed 121,371 ha. It uses 80,000 ha to produce soy, corn, sugarcane, and livestock. In crop year 2016/2016, it produced 50,920 metric tons of soy on its farms. In 2016, three large companies formed 75 percent of its client base. These companies were Brenco, Cargill, and Bunge.

After BrasilAgro acquires land, it invests in infrastructure and technology for efficient agricultural production. BrasilAgro then divests of a farm when it reaches its optimal value to capture capital gains. The company combines the returns generated from land value appreciation and agricultural production.

Figure 1: BrasilAgro’s land portfolio development. Source: BrasilAgro’s 2017 institutional presentation.

BrasilAgro is Active in Environmentally Sensitive Cerrado

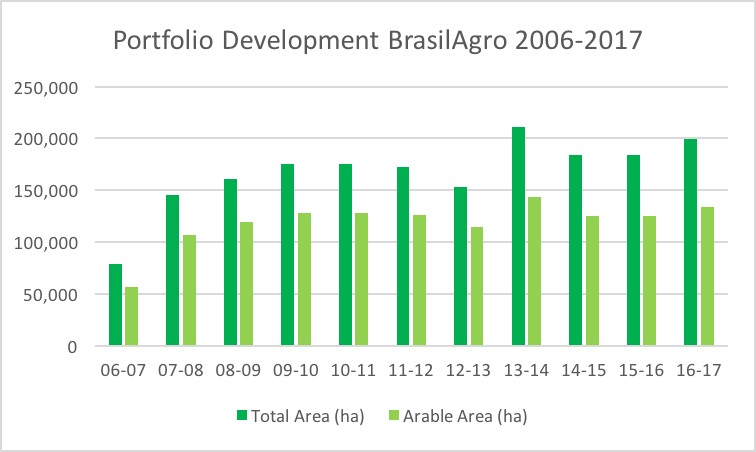

As of Q4 2017, BrasilAgro owns 225,832 ha in its portfolio spread over 11 properties. Ten of its properties are in the Brazilian states of Maranhão, Piauí, Bahia, Minas Gerais, Goiás, and Mato Grosso. One farm is in Paraguay. As shown in Figure 2 (below), BrasilAgro’s farms in Brazil are in the Cerrado Biome, which is one out of six Brazilian continental regions with unique biological diversity.

Figure 2: BrasilAgro’s property portfolio in Brazil located in Cerrado Biome. Source: BrasilAgro’s website, Brazilian Ministry of Environment (MMA) and the Brazilian Institute of Geography and Statistics (IBGE), 2004.

BrasilAgro wholly owns eight farms, while it leases an additional three farms. All owned farms are appraised on an annual basis. As shown in Figure 3 (below), its farmland portfolio has appreciated by 146 percent since the purchase of the first farm in 2007.

Figure 3: BrasilAgro’s Current Farmland Portfolio. Source: BrasilAgro’s 2017 institutional presentation.

| Farm name | Location | Acquisition Year | Total Area (HA) |

Acquisition & Capex (R$ MM) |

Internal Valuation (R$ MM) |

| Jatobá | Bahia | 2007 | 31,606 | 65.2 | 303.5 |

| Araucária | Goiás | 2007 | 6,490 | 50.5 | 141.9 |

| Alto Taquari | Mato Grosso | 2007 | 5,186 | 33.3 | 120.6 |

| Chaparral | Bahia | 2007 | 37,182 | 61.8 | 262.7 |

| Nova Buriti | Minas Gerais | 2007 | 24,.247 | 22.0 | 32.0 |

| Prefêrencia | Bahia | 2008 | 17,799 | 29.8 | 56.6 |

| São José | Maranhão | 2017 | 17,566 | 100.0 | – |

| Palmeiras | Paraguay | 2013 | 59,.490 | 72.0 | 154.8 |

| Sub-total | 199,566 | 434.6 | 1072.1 |

Since its inception in 2006, the company has sold 10 farms, for a total net profit of BRL 350.6 million (USD 108.7 at today’s exchange rate). In its largest sale to date, BrasilAgro sold its 27,745 ha Cremaq farm in Piauí in 2015 for USD 81.6 million (BRL 270 million), equivalent to USD 3,000 per ha. This equals seven times the original purchase price per ha nine years earlier.

Figure 4: BrasilAgro’s Farmland Sales. Source: BrasilAgro’s 2017 institutional presentation.

| Farms sold |

Location |

Acq. Date | Total Area (HA) | Acq. Capex

(BRL MM) |

Sale Value (BRL MM) |

Sale

Date |

| Engenho | Mato Grosso do Sul | 2007 | 2,022 | 10.1 | 22.0 | 2008 |

| São Pedro | Goiás | 2006 | 2,447 | 10.3 | 26.0 | 2011 |

| Horizontina | Maranhão | 2010 | 14,358 | 52.9 | 75.0 | 2012 |

| Araucária | Goiás | 2007 | 394 | 3.8 | 10.3 | 2013 |

| Cremaq | Piauí | 2006 | 4,957 | 11.0 | 38.0 | 2014 |

| Cresca S.A. | Paraguay | 2013 | 12,312 | 10.0 | 17.2 | 2014 |

| Araucária | Goiás | 2007 | 1,164 | 107 | 41.3 | 2014 |

| Cremaq | Piauí | 2006 | 27,745 | 63.5 | 270.0 | 2015 |

| Auracária | Goiás | 2007 | 274 | 3.0 | 13.2 | 2017 |

| Auracária | Goiás | 2007 | 1,360 | 4.0 | 16.9 | 2017 |

| Sub-total | 67,033 | 179.3 | 529.9 | |||

| Total | 266,599 | 613.9 | 1,602.0 |

Chain Reaction Research has identified farmland investment as a major driver of deforestation, land grabbing, and adverse social, economic, and environmental impacts in the Cerrado. 62 percent of the agricultural expansion in the Matopiba region in the Cerrado has replaced occurred while natural vegetation between 2007 and 2014. The Matopiba region is known as Brazil’s newest agricultural frontier. It has seen increasing deforestation rates mostly due to agribusiness expansion, and has lost half of its natural vegetation cover to date. Some of the sustainability risks associated with farmland acquisition, land development and soy production in the Cerrado are the loss of biodiversity due to large scale deforestation, social and environmental impacts on local communities that involve land grabbing and associated violence, and diminishing water resources.

Sustainability Impacts

Since 2011, BrasilAgro has expanded its landbank with 116,118 ha.This includes the purchase of the Palmeiras (2013) and São José (2017) farms and the expansion of the Parceria Farms. In the same period, the company sold 64,900 ha. The current properties cover 226,284 ha of land, of which it owns 199,556 ha. The rest is leased as part of agricultural partnerships. The total cultivated area in 2016/2017 harvest year was 88,873 ha.

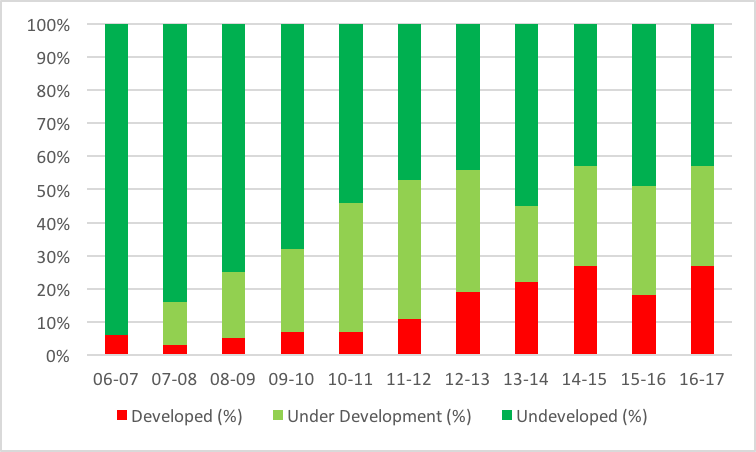

At the time of acquisition, some farms were already partially developed, but farms also contained large strands of undeveloped Cerrado forests. Since 2011, BrasilAgro has transformed 59,600 ha of undeveloped land and pasture into cropland. The transformation includes clearing of native Cerrado vegetation. BrasilAgro states that currently, 30 percent (38,859 ha) of its portfolio is under development (see Figure 5). As of 2017, 43 percent of the portfolio remained undeveloped, consisting of land with native vegetation and unproductive land.

Figure 5: Portfolio Development since 2006. Source: BrasilAgro’s 2017 institutional presentation.

The ongoing expansion and development of BrasilAgro’s landbank has a major impact on native Cerrado forest and savanna habitats. Landsat and Sentinel-2 satellite analysis on four BrasilAgro farms shows that 21,690 ha of Cerrado vegetation was cleared from January 2012 toOctober 2017. As shown in Figure 6 (below), the cleared area consists of 20,572 ha (95 percent) Cerrado forest and 1,119 ha (5 percent) of Cerrado grassland. Clearing of original vegetation is an ongoing process on BrasilAgro’s farms. Satellite observations show that since January 2017, significant areas of Cerrado forest were cleared on BrasilAgro’s Araucária (sugarcane) and Chaparral (soy, corn, and pasture) farms.

As shown in Figure 6 (below), three of BrasilAgro’s farms in Bahia have seen the most significant natural vegetation transformation since 2011. Vegetation has been cleared on one of the leased agricultural partnership farms in Piauí as well.

Figure 6: Cleared vegetation at BrasilAgro farms 2012-2017. Source: Aidenvironment Landsat and Sentinel-2 satellite analyses.

| Farm | Property since | Property size [ha] | Development 2012 to 2017 [ha] | Percent Cerrado forest cleared | Percent Cerrado grassland cleared |

| Chaparral | September 11, 2008 | 37,182 | 12,672 | 100% | 0% |

| Preferencia | November 30, 2007 | 17,799* | 3,754 | 95% | 5% |

| Jatoba | March 5, 2007 | 31,606 | 4,213 | 78% | 22% |

| Sub-total | 20,639 | ||||

| Parceira II | November 2013 | 7,455 | 1,051** | 100% | 0% |

| Total | 21,690 | 95% | 5% |

*As of Q4 2017

** Of which 732 ha by third parties (2012-2013) and 319 ha by BrasilAgro (2014-2016)

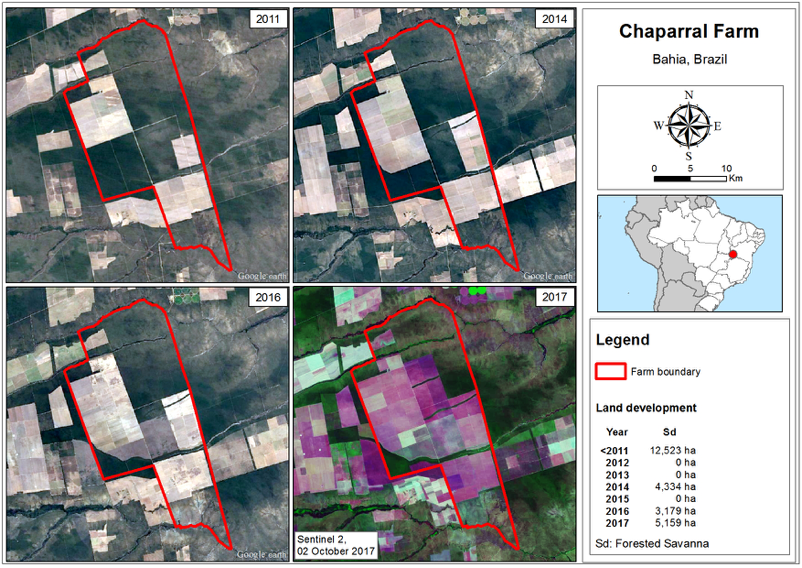

Fazenda Chaparral

Fazenda Chaparral is in Correntina (Bahia) and was purchased November 30, 2007. The farm is used to produce soy, corn, and pasture. As of 2017, the total farm area was 37,182 ha. Between 2014 and 2017, the appraised valuation of the farm increased by 28 percent to BRL 352 million. 40 percent of the farm is developed, while another 40 percent of the farm still is under development. Between 2012 and 2017, BrasilAgro cleared 12,672 ha of its original vegetation on Fazenda Chaparral. Satellite images from October 2017 indicate that vegetation clearing took place throughout 2017 as well.

Figure 7: Deforestation at Fazenda Chaparral between 2011 and 2016. Source: Aidenvironment Landsat and Sentinel-2 satellite analysis.

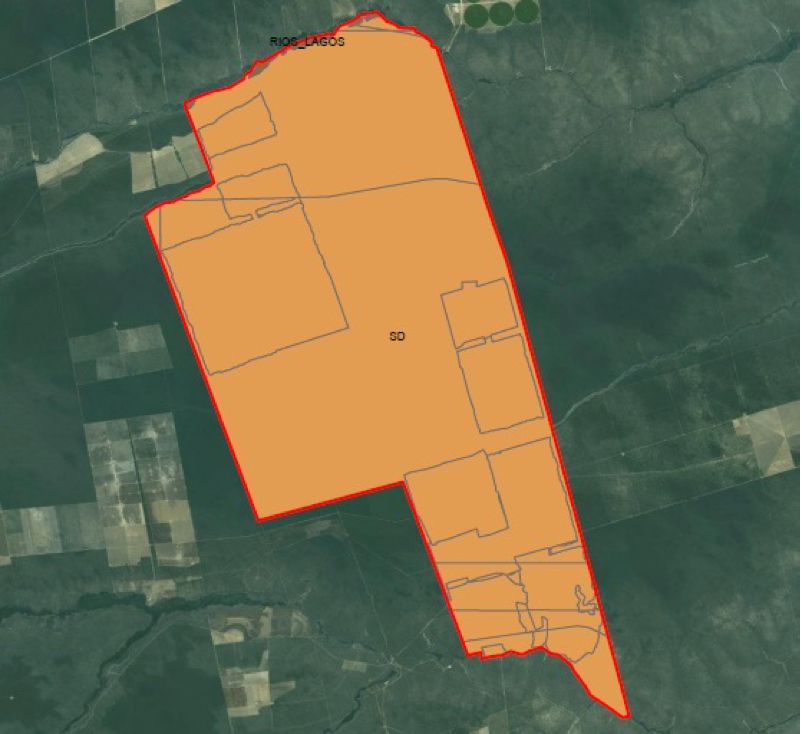

Vegetation maps of the Cerrado Biome were produced as part of Brazil’s Forest Reference Emissions Level (FREL) program, by the Brazilian Ministry of Environment and Ministry of Science, Technology and Innovation. As shown in Figure 7 (above) and 8 (below), the FREL categorized all cleared vegetation on Fazenda Chaparral as Forested Savanna. This means all development since 2012 has taken place on forested land. The Roundtable on Responsible Soy (RTRS) identified the cleared lands on Fazenda Chaparral as biodiversity hotspots, where ‘stakeholders agree there should be no conversion of native vegetation to responsible soy production’.

Figure 8: Original vegetation cover at Fazenda Chaparral. SD = forested savanna. Source: MMA and MCTI, 2014.

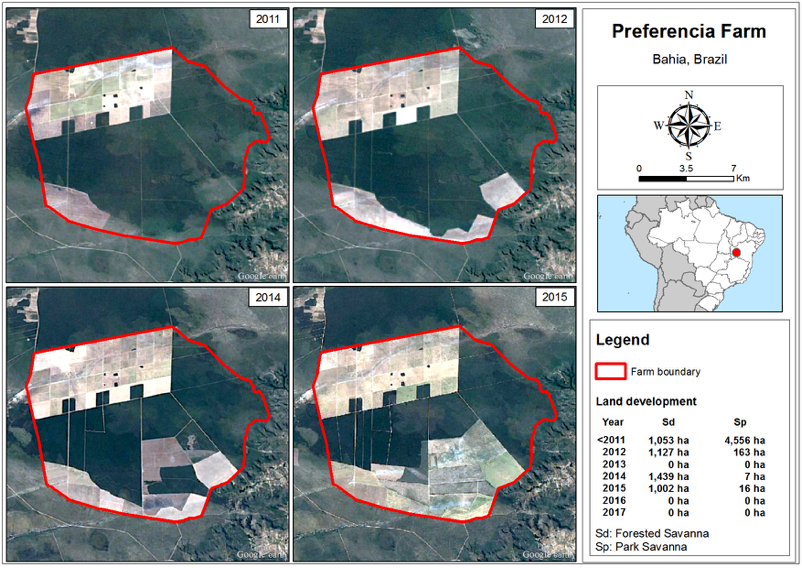

Fazenda Preferencia

Fazenda Preferencia is a 17,799 ha farm located in Baianópolis (Bahia). BrasilAgro purchased it on September 11, 2008. The farm is used for cattle farming and the production of soy and corn. 80 percent of the farm is under development, according to BrasilAgro’s Q4 2017 results.

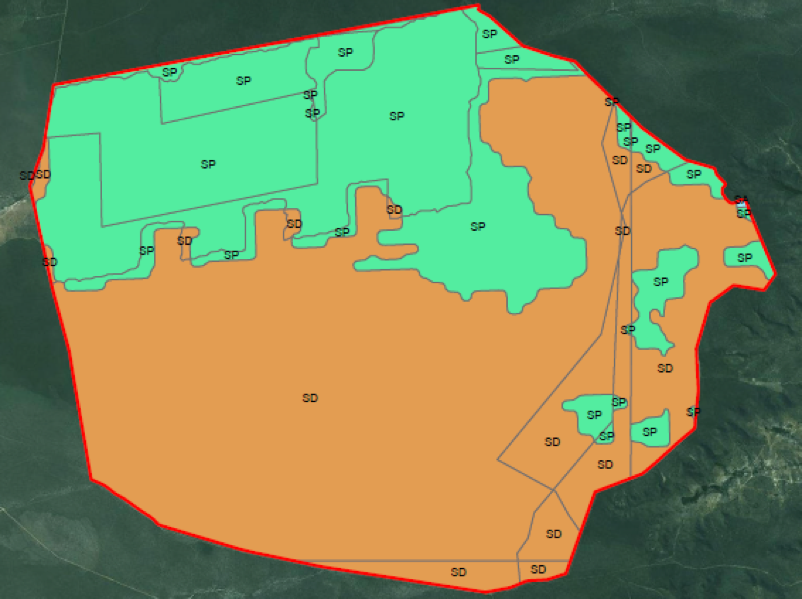

Between 2012 and 2017, BrasilAgro cleared 3,754 ha of its original vegetation on Fazenda Preferencia. Vegetation maps produced as part of Brazil’s Forest Reference Emissions Level (FREL) in the Cerrado Biome categorize the cleared vegetation as Forested Savanna (95 percent), a forest category, and Park Savanna (5 percent), a grassland category (Figure 9 and 10 below). The RTRS identified the cleared lands as biodiversity hotspots, where ‘stakeholders agree there should be no conversion of native vegetation to responsible soy production‘.

Figure 9: Deforestation at Fazenda Preferencia between 2012 and 2016, including vegetation types. Source: Aidenvironment Landsat and Sentinel-2 satellite analysis.

Figure 10: Original vegetation at Fazenda Preferencia. SD = Forested Savanna, SP = Park Savanna. Source: MMA and MCTI, 2014.

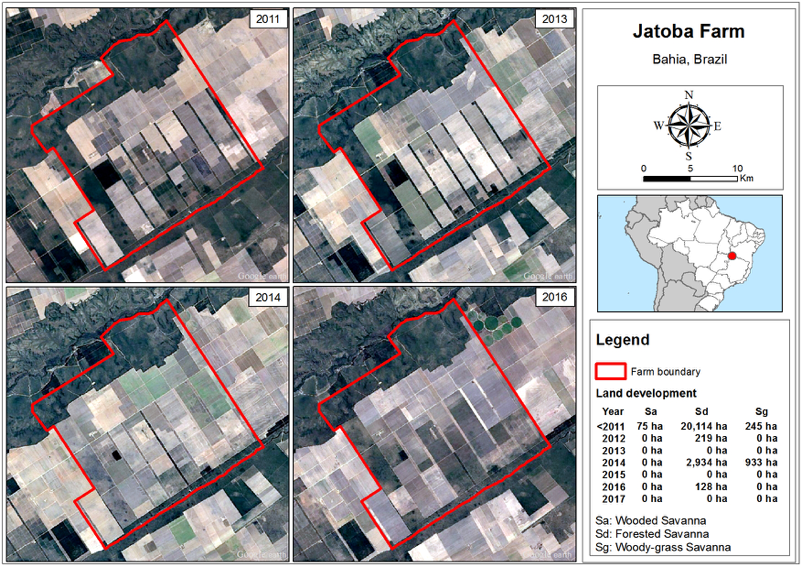

Fazenda Jatoba

Fazenda Jatoba is in Jaborandi (Bahia) and was purchased on March 5, 2007. The farm is used for the production of soy, corn, other commodities, and cattle farming. As of 2017, the total farm area contains 31,606 ha of land. Market valuation of the farm by Deloitte increased by 14.7 percent between 2014 and 2017. 30 percent of the farm is still under development. Part of the farm (625 ha) was sold in June 2017.

Figure 11: Deforestation at Fazenda Jatoba between 2011 and 2016. Source: Aidenvironment Landsat and Sentinel-2 satellite analysis.

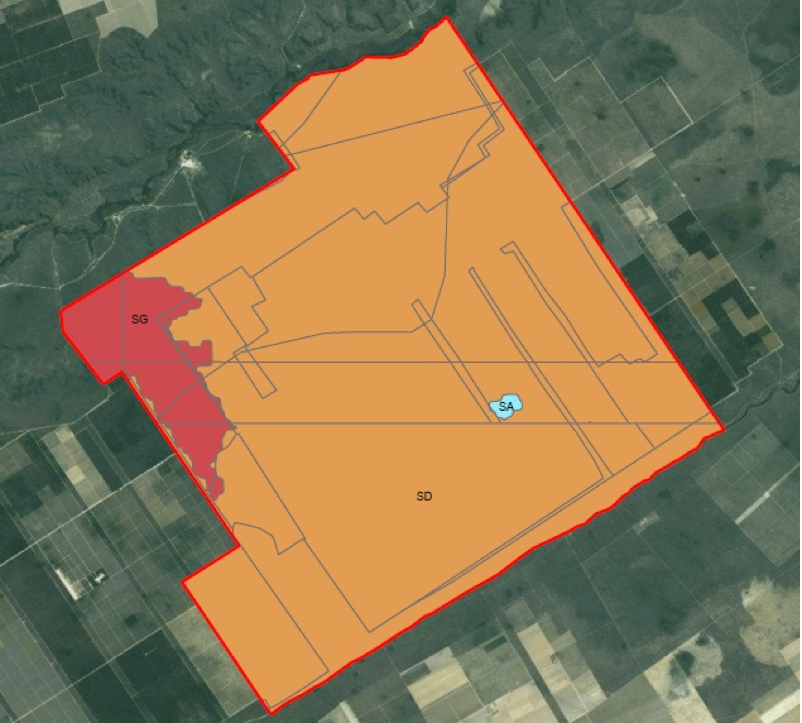

Figure 12: Original vegetation at Fazenda Jatobal. SD = Forested Savanna, SG = Woody-Grass Savana, SA = Wooded Savanna. Source: MMA and MCTI, 2014.

Between 2012 and 2017, BrasilAgro cleared 4,213 ha of its original vegetation on Fazenda Jatoba. Vegetation maps produced as part of Brazil’s Forest Reference Emissions Level (FREL) in the Cerrado Biome categorize the cleared vegetation as Forested Savanna and Woody-Grass Savanna, a grassland formation. 78 percent of the development since 2012 has taken place on forested land, according to Chain Reaction Research analysis. The RTRS identified the cleared lands as areas with ‘stakeholders agree there should be no conversion of native vegetation to responsible soy production‘.

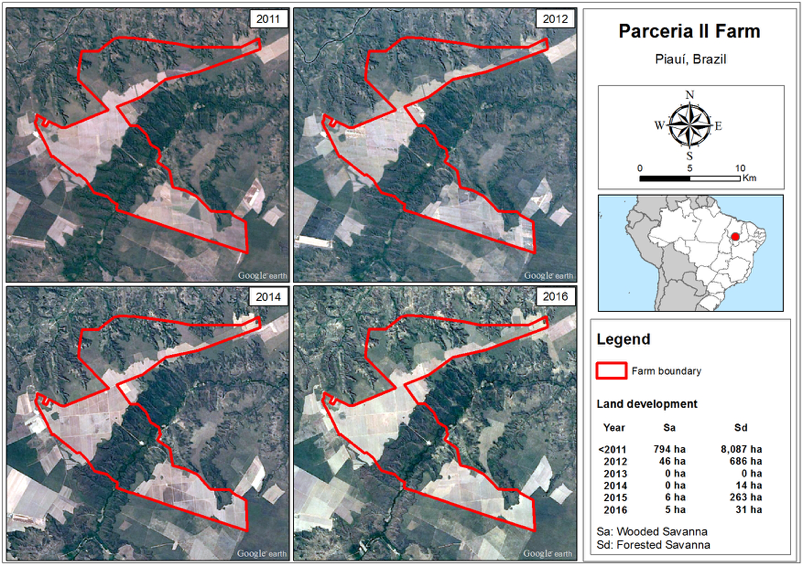

Fazenda Parceria II

Fazenda Parceria II, located in Ribeiro Gonçalves (Piauí), is a farm that BrasilAgro has leased since November 2013. The leasing period allows agricultural production by BrasilAgro for up to 11 harvests. As of 2017, the total farm area contains 7,455 ha of arable land, primarily used to produce soy. The total farm concession area contains 18,774 ha of land.

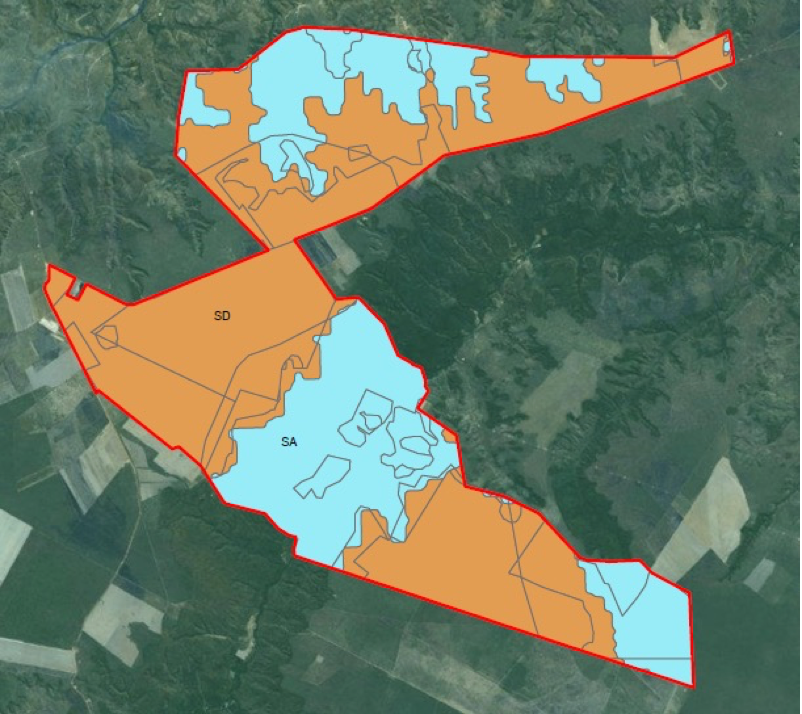

As shown in Figure 13 (below), since 2013, BrasilAgro cleared 319 ha of its original vegetation on Parceria II farm. Just before the acquisition of the farm in 2012, 732 ha of land was cleared by third parties. As shown in Figure 14 (below), vegetation maps produced as part of Brazil’s Forest Reference Emissions Level (FREL) in the Cerrado Biome categorize the cleared vegetation as Wooded Savanna and Forested Savanna. This means all development on Parceria II since 2011 has taken place on forested land.

Local media report that neighboring communities of Parceria II were directly affected by the removal of natural vegetation by BrasilAgro. After the clearing took place, rainwater was no longer captured by the natural vegetation on the higher plateaus of the farm. This resulted in rapid discharge of water, destroying community pastures and cornfields in the valley. In response, BrasilAgro agreed to restore contours around their farm to retain rainwater.

Figure 13: Deforestation at Fazenda Parceira II between 2011 and 2016. Source: Aidenvironment Landsat and Sentinel-2 satellite analysis.

Figure 14: Original vegetation at Fazenda Parceira II. SD = Forested Savanna, SA = Wooded Savanna. Source: MMA and MCTI, 2014.

BrasilAgro Faces Deforestation-Related Business Risks

The deforestation that has taken place in the farms described above could materialize in a number of operational business risks.

Supply Chain Risks

There is increasing pressure from civil society and the soy market to eliminate deforestation in the Cerrado. In September 2017, a group of civil society organizations, including WWF, adopted the Cerrado Manifesto. The Cerrado Manifesto highlights the destruction of native vegetation in the Cerrado. It calls for immediate action by companies that source soy and beef from the Biome, as well as from investors who invest in these companies and their supply chains. In October 2017, a group of 23 global companies stated their support for the Manifesto, committing themselves to halting soy-driven deforestation and native vegetation loss in the Cerrado. As shown in the growth of zero-deforestation commitments in the palm oil sector, the move towards zero-deforestation can lead to companies being excluded from supply chains when they do not comply with these policies.

Bunge, ADM, Amaggi and Cargill, some of BrasilAgro’s main soy and corn clients, are stepping up their commitments to zero-deforestation in their supply chains. They have recently made soy production in Cerrado a policy focus. This means that BrasilAgro’s soy production, land expansion, and deforestation in the Cerrado may fall under increasing scrutiny, resulting in a business risk to the company.

Bunge and Cargill were both in the top 3 of BrasilAgro’s main agricultural clients in 2016. If trading relationships are suspended due to the violation of deforestation commitments, the company risks losing half of its client base.

Overvaluation of Farmland Portfolio

Forests within BrasilAgro’s farmland portfolio might become stranded. Stranded land is a form of stranded assets that have suffered from unanticipated or premature write-downs, devaluations, or conversion to liabilities before the end of their useful economic lives.

BrasilAgro’s business strategy relies on the sale of newly transformed farmland to commodity producers. In earlier research on farmland investment in the Cerrado, Chain Reaction Research showed that land prices in the Cerrado have nearly quadrupled between 2002 and 2011. This research also explained that there are signs that the farmland real estate market is overheated. Should the soy market make zero-deforestation a requirement for market access – as has previously occurred in the palm oil industry – BrasilAgro might face difficulties finding buyers for recently deforested farmland.

Other concerns, such as social impacts of land expansion, diminishing water sources and volatile weather patterns in Matopiba might also deter potential buyers, and affect the value of land. BrasilAgro already recognized these volatile weather conditions and increasing droughts in 2013.

Legal Risks

BrasilAgro is aware that environmental impacts in the Cerrado might pose risks to its business. They state that as environmental laws and their applications are becoming “highly stringent,” their compliance with environmental requirements should increase in the future. This could lead to an increase in their environmental preservation expenditures compared to current estimates or costs.

BrasilAgro is also involved in court cases at the Brazilian state-level Agrarian Justice Courts. In Bahia, the real estate company Imobiliária Cajueiro Ltda that sold part of the land of Fazenda Chaparral, has been accused of illegally obtaining the land. If these land rights are cancelled as part of this case, it could affect 2,561 ha of BrasilAgro’s portfolio, or 6.9 percent of the total size of the farm.

Financial Risk Analysis

BrasilAgro faces four key financial issues:

- How can BrasilAgro be affected if buyers/customers react on BrasilAgro’s sustainability and deforestation violations?

- Are the potentially stranded assets substantial in size and could this impact the value of the company significantly?

- Who is financing BrasilAgro’s debt and equity and how will non-compliance related to deforestation in the Cerrado impact this?

- How much can the value of debt and equity be affected by the impact of the non-compliance on deforestation or by the impacted of ‘stranded land’, i.e. land owned by BrasilAgro that will not be taken into production?

Financial Analysis: Volatility

As shown in Figure 15 (below), in the six-year period FY2012 to FY2017 with year-ending June 30, BrasilAgro’s net revenues were volatile as they fluctuated between USD 37 million (2016) and USD 142 million (2015). In FY2017, its revenue was USD 57 million. Its EBITDA has also been volatile. In the last six years, it ranged from negative USD 2 million to positive USD 70 million. In Q1 FY2018, the company had a strong start mainly due to better production on more land with net revenue of USD 31 million and EBITDA of USD 10 million.

Figure 15: Key figures of BrasilAgro. Fiscal year ends June 30. Source: Bloomberg.

| USD million | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| Net revenues | 82.1 | 120.0 | 66.6 | 141.5 | 36.7 | 57.2 |

| Gross profit | 5.5 | 36.2 | 6.0 | 77.1 | 0.1 | 14.9 |

| EBITDA | 2.4 | 27.0 | -2.3 | 69.7 | -1.8 | 6.2 |

| Depreciation/Amortization | -15.4 | -13.8 | -9.4 | -8.4 | -5.9 | -4.7 |

| EBIT | -13.0 | 13.2 | -11.7 | 61.3 | -7.7 | 1.5 |

| Financial income/costs | 3.9 | 4.0 | 0.6 | 0.0 | 7.3 | 2.7 |

| Net profit | -3.1 | 14.1 | -5.8 | 68.3 | 2.2 | 8.6 |

| EPS (USD) | -0.15 | 0.24 | -0.10 | 1.17 | 0.03 | 0.15 |

| Free Cash Flow after capex | -9.1 | 15.8 | 8.9 | -4.9 | -5.1 | 12.3 |

An important explanation of the volatility of both revenue and EBITDA is related to a) how profits are accounted for when land is sold, which is included in the net revenues, and b) in the movement of agricultural prices. The company’s business model and its financial returns are mainly based on the price appreciation of land.

In FY2017, 20 percent of net revenues were generated from ‘Farm Sale’. The rest of revenue (80 percent) was mainly generated in sugar cane (50 percent of farming revenue), soybeans (43 percent) and corn (4 percent). The cost of goods sold for the agricultural products production is relatively high, leading to a low EBITDA margin if no land is sold. In the last six years, 27 percent of BrasilAgro’s agricultural revenues were generated through ‘Farm Sale’.

The company’s free cash flow generation (operating cash flow minus capital expenditures) was on average USD 3 million (annually) in the last six-year period. The large investments in land were made in 2010 and in the years before. In 2017, BrasilAgro acquired 17,566 ha for an average of BRL 5,693 (USD 1,779) per ha. At the same time, the company sold 2,259 ha for BRL 17,840 (USD 5,575) per ha.

Losing Bunge and Cargill as Customers affects Equity Value by Four Percent

BrasilAgro’s top three buyers are responsible for 65 percent of its net revenue. In its 20-F for FY2017 (page 9), the top-two were 58 percent of BrasilAgro’s net revenue. The largest customer in FY2017 was Brenco/ETH Bioenergia with 39.3% of sales (all sugar). The number 2 and 3 which generated 26% of net revenue, according to the 20-F. Although no names are mentioned, these were probably again Bunge and Cargill, like in 2016. Both Bunge and Cargill have introduced zero-deforestation policies. Other large customers in soybeans and corn are Amaggi and ADM.

If Bunge and Cargill stop buying from BrasilAgro, this could have a serious impact on the company’s net revenues. Losing 26 percent of the revenue from two of BrasilAgro’s top three customers would decrease annual revenues by USD 16 million. With a gross margin for only agricultural sales at 5 percent, the loss of gross profit and the impact on EBITDA would be USD 0.8 million. If these revenues would not ‘leak’ to new customers, the value of this would be USD 8 million in a discounted cash flow calculation which would impact its current Enterprise Value (Figure 17) by a negative 3.8 percent and its equity value (Figure 17) by a negative 4.1 percent. These numbers are relatively low as BrasilAgro’s enterprise value and equity value is mainly based on the value of the land.

Losing Brenco as a Sugar Customer Affects Equity Value by Eight Percent

BrasilAgro’s largest customer is Brenco/ETH Bioenergia (they merged in 2010), a subsidiary of Odebrecht with 39.3% of net revenues in FY2017 and 55.3% in FY2016, all sugarcane. Moreover, BrasilAgro entered into a supply contract in 2013 and a leasing contract (on 4,263 ha until 2026) with Brenco (Companhia Brasileira de Energia Renovável), controlled by Odebrecht SA. In this contract, 100 percent of the sugarcane production from Alto Taquari and Araucaria and Partnership III farms is involved, with two annual crop cycles until 2021/22. Although this contract does not relate to the soy/meat value chain and the deforestation on the four farms described above, investors should be aware of the potential financial risks.

BrasilAgro’s main risk is related to Odebrecht’s current financial position. Odebrecht is currently being investigated in Operation Car Wash – a nationwide corruption scandal. Odebrecht’s business has been affected by difficulties to access the credit markets. Consequently, it needs to cut costs which might also affect Brenco.

Despite the absence of policies on deforestation, Odebrecht and Brenco may use the ‘deforestation’ argument versus BrasilAgro to get out of the 2026 land lease contract. The value of this 10-year lease contract we estimate on USD 4.5 million, based on a 3 percent lease rate per year on the value of the land (USD 2,780 per ha) and then multiplied by 10 (years) and 4,263 ha. This would decrease another 2 percent BrasilAgro’s enterprise value and equity value.

Additionally, if the Brenco/Odebrecht would get into financial trouble, BrasilAgro could lose an additional 39 percent net revenue. Based on a 5 percent gross margin, the loss of gross profit and EBITDA would amount to USD 1.1 million, and the DCF is valued at USD 11 million. This could impact the company’s enterprise value by 5.6 percent. However, we believe BrasilAgro could easily redirect this sugar output into the fragmented global sugar market and reduce the loss of enterprise value.

Stranded Land Could Dramatically Affect BrasilAgro’s Equity Value

The starting point to calculate the value impact on BrasilAgro’s land portfolio is as follows. As discussed above, BrasilAgro has deforested Cerrado vegetation at four of its farms. Three of them are owned by BrasilAgro and are instrumental in its business/earnings model of ‘land value appreciation’. These three farms have a book value, made up of acquisition price plus capital expenditures, and a calculated market value based on estimates by Deloitte. Based on assumptions of reduction of expected market price, we calculate the impact on BrasilAgro’s equity value, assuming a 20 percent tax rate.

As shown in Figure 16 (below), this impact could be material on BrasilAgro’s net asset value. If the farms lose all their value (last column), the net asset value per share would decline by BRL 8.2 from BRL 25.96 (USD 8.1) to BRL 17.76 (USD 5.6). Assuming a reduction of 25 percent against the Deloitte estimate, this has an impact of negative 8 percent on the company’s net asset value and 17% versus equity value. If tax rates in certain areas are much lower than the 20 percent, the net value impact will be significantly higher.

Figure 16: Calculation of value loss due to stranded assets. Source: Chain Reaction Research, Deloitte.

| Three farms: Jatoba, Preferencia, Chaparral | Book value (A) | Deloitte value (B) | 75% of B | 50% of B | 0% of B |

| Value of farms (Real million) | 156.8 | 622.8 | 467.1 | 311.4 | 0 |

| Remaining Book gain | 466.0 | 310.3 | 154.6 | -156.8 | |

| Reduction versus B (net asset value) | 155.7 | 311.4 | 622.8 | ||

| -/- taxes (20% on book gain) | -31.1 | -31.4 | -155.9 | ||

| Net reduction of value | 124.6 | 280.0 | 466.9 | ||

| Number of shares (M) | 56.9 | 56.9 | 56.9 | ||

| Reduction in Value/share (Real) | 2.2 | 4.9 | 8.2 | ||

| As % of net asset value of Real 25.96 | 8.4% | 19.0% | 31.6% | ||

| As % of share price of Real 12.73 | 17.2% | 38.7% | 64.5% |

Is BrasilAgro able to accommodate investors which would become worried by the potential value reduction, as shown in Figure 16 (above)?

As stated above in the section on Legal Risks, BrasilAgro is aware of increasing environmental regulation. Although restoration policies, as exist in SE Asia, currently do not exist in Brazil, if these were replicated from SE Asia, the cost per ha might amount to USD 2,500 to USD 3,000, as it is under the Roundtable on Sustainable Palm Oil.

If BrasilAgro would choose this solution, the costs for the 20,639 ha cleared in the Cerrado, as shown in Figure 6 (above), would amount to USD 56.8 million. This equals to 29% of equity value.

BrasilAgro risks substantial value losses from ‘stranded assets’, which could easily add up to substantial losses on the net asset value per share. Although restoration policies are not yet practiced, this could be a remedy to protect value for shareholders and create a win-win with climate change mitigation.

Cresud’s Investors Could Impact BrasilAgro

BrasilAgro is financed with USD 13 million in net debt. In the last 6-year period, BrasilAgro, on average, had a net cash position of USD 13 million. Its low level of debt since FY2012 was accompanied by a relatively low level of the EBITDA.

Figure 17: Division of financing of BrasilAgro; Equity versus Debt. Source Bloomberg, Chain Reaction Research.

| USD Million | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| Enterprise Value | 229.9 | 290.7 | 252.1 | 131.6 | 178.6 | 211.1 |

| Market capitalization | 216.5 | 291.2 | 253.0 | 208.9 | 206.3 | 197.7 |

| Gross debt | 46.9 | 45.9 | 54.4 | 35.4 | 31.3 | 33.9 |

| Cash | 33.6 | 46.4 | 55.3 | 112.7 | 59.0 | 20.5 |

| Net-debt | 13.3 | -0.5 | -0.9 | -77.3 | -27.7 | 13.4 |

| Net debt/EBITDA | 5.5 | 0.0 | 0.4 | 2.2 |

According to BrasilAgro’s 20-F for FY2017, development banks and government agencies own most of its debt, including loans and credit facilities. Beyond this, its major creditors include: Itau, the Banco do Nordeste Brasil, Banco Safra, HSBC, Rabobank, and Santander. These banks have zero-deforestation and forest policies. BrasilAgro has not issued listed notes/bonds.

BrasilAgro’s founder Cresud controls 41 percent of its shares. Cresud is the largest landowner in Argentina. It is listed on the stock exchange of Buenos Aires. Recently, Autonomy Capital from Jersey has reduced its stake in Cresud to under 10 percent from 15 percent. There are many smaller shareholders which have stakes below 2 percent each.

As shown in Figure 18 (below), BrasilAgro’s four largest shareholders do have no or weak policies on deforestation and/or do not have a rating from the Forest 500. Its smaller shareholders, such as CSHG (Credit Suisse (NYSE:CS)) and Deutsche Bank (NYSE:DB) have high Forest 500 scores. They respectively own 1.8 percent and 1.5 percent in BrasilAgro. Also, JPMorgan (NYSE:JPM) and Citibank (NYSE:C) have investment positions.

Ruane Cunniff owns USD 11 million in BrasilAgro depository receipts listed on exchanges in New York, London, and Frankfurt. Northern Trust (NASDAQ:NTRS), Citigroup, Bank of America (NYSE:BAC), and UBS (NYSE:UBS) all hold positions below USD 0.6 million. These five firms have deforestation policies.

In conclusion, USD 10 million in BrasilAgro’s equity and depository are owned by institutions that have deforestation policies. These investment firms may choose to engage directly with BrasilAgro regarding the company’s deforestation.

Figure 18: Main shareholders of BrasilAgro; Source Bloomberg.

| October 30, 2017 | % | Forest 500 | Policies |

| Cresud | 40.7% | – | Weak |

| Autonomy Capital (Jersey) | 9.6% | – | No |

| BrasilAgro | 5.4% | – | Yes |

| Cape Town LLC | 4.6% | – | No |

| CSHG AM | 1.8% | 4 out of 5 | No |

| Deutsche Bank | 1.5% | 5 out of 5 | Yes |

| Kopernik Global Investors | 1.2% | – | No |

| Horn Elie | 1.1% | – | No |

| Dimensional Fund Advisors | 0.8% | 1 out of 5 | ESG, UNPRI |

| JP Morgan Chase | 0.18% | 3 out of 5 | Weak |

| Banco Citibank | 0.03% | 3 out of 5 | Yes |

Cresud is listed on the Bolsa de Comercio de Buenos Aires. Cresud’s equity also trades in the U.S. as American Depository Receipts (ADR). Cresud has business located in Argentina, Brazil, Bolivia, and Paraguay. Cresud is also active in real estate. 20% of the (agricultural) land is in Brazil, completely through BrasilAgro, and 7% in Paraguay (through BrasilAgro).

Cresud Lacks Either a Deforestation Policy or Zero-Deforestation Commitment

Cresud’s net debt is USD 6,247 million (ARS 109.9 billion). Most of its debt is listed in ARS and USD. This debt is mainly held by investors without policies on deforestation. Still, T. Rowe Price (NASDAQ:TROW) (USD 27 million), Fidelity (USD 10 million), MetLife (NYSE:MET), Deutsche Bank, and Nordea Bank (OTCPK:NRDEF), which all have Forest 500 rankings of one or more, have smaller positions. In total, this adds up to USD 52 million.

As shown in Figure 19 (below), it is interesting to list the shareholders of Cresud. There are some smaller shareholders that have policies on deforestation, such as Santander, BNP Paribas (OTCQX:BNPQF), and HSBC (NYSE:HSBC). This adds up to a USD 9 million position.

| Figure 19: Main shareholders Cresud SA. Source Bloomberg, Forest 500. |

| October 30, 2017 | % | Forest 500 |

| Ifisa | 30.57% | – |

| Anses | 3.56% | – |

| Elsztain Alejandro Gust | 1.27% | – |

| Zang Saul | 0.80% | – |

| Santander Rio AM | 0.45% | 3 out of 5 |

| BNP Paribas | 0.34% | 5 out of 5 |

| Standard Investments SA SGFCI | 0.22% | – |

| HSBC Roberts Administradora | 0.09% | 5 out of 5 |

| Schroders SASGFCI | 0.06% | – |

As shown in Figure 20 (below), its ADR reflect opportunity for engagement. Cresud’s enterprise value is dominated by debt, the equity value is only USD 1 billion. The holders of ADRs that have policies on deforestation hold 7.2 percent of its equity. Including the holders of the normal shares, this adds up to 8 percent of equity could be engaged.

| Figure 20: Cresud’s main shareholders of ADRs. Source Bloomberg. |

| November 2, 2017 | USD million | Forest 500 |

| Macquarie | 57.4 | 2 |

| Newfoundland CM | 44.8 | – |

| Senvest Management | 28.9 | – |

| 683 CM | 22.6 | – |

| Ruane Cunniff & Goldfarb | 13.9 | – |

| Warburg Invest Kap | 13.3 | – |

| Caisse de Depot et Placement | 12.6 | 2 |

| Russell Investment Group | 12.6 | – |

| Finepoint Capital | 11.4 | – |

| Bienville CM | 11.3 | – |

| Carmignac Gestion | 10.4 | – |

| Serengeti AM | 9.0 | – |

| Credit Suisse Group | 4.6 | 4 |

| BlackRock | 4.5 | 2 |

| London Stock Exchange Group | 4.3 | – |

| 261.6 |

In conclusion, BrasilAgro has USD 10 million of shareholders/ADRs owners that have policies related to deforestation. Cresud has USD 52 million in debt that is owned by institutions that have policies related to deforestation. Cresud also has USD 80 million equity/ADRs that is owned by investors with deforestation policies. This means that in total USD 142 million of investments could engage.

Valuation and Risks

In the last 5 years to 1 November 2017, BrasilAgro outperformed its Brazilian peer SLC Agricola, and it outperformed the Brazilian stock market index Ibovespa. However, it has been a meager investment in US Dollar terms.

| Figure 21: Five-Year Share Returns Comparison (USD) to 1 Nov 2017. Source Bloomberg, Chain Reaction Research. |

| Price Change | Total Return | |

| BrasilAgro | -13.4% | 5.7% |

| SLC Agricola | -32.5% | -19.1% |

| Ibovespa Brasil Index | -21.3% | -21.3% |

| Cresud | 96.6% | 110.5% |

In its peer group comparison, BrasilAgro’s current P/E and P/B are low. Its EV/EBITDA is relatively high. Versus its Latin American peers SLC Agricola and Cresud, BrasilAgro has the highest valuation.

The P/B ratio is the most important to look at because BrasilAgro’s business model is based on land value appreciation. At a share price of BRL 12.71, its P/B is 1.0X. Its book value is based on acquisition price plus investments. However, its share price as well as the book value per share is only half of the net Asset value (NAV) per share (BRL 25.69). This NAV per share is based on land value estimates by Deloitte (ca USD 3,000 or ca BRL 10,000 per arable ha, 70 percent of the total ha -30 percent is not allowed to be cultivated).

| Figure 22: Peer group valuation. Source Bloomberg, Chain Reaction Research. |

November 1, 2017 |

Price | P/E | EV/EBITDA | P/BV | Activity |

| Adecoagro S.A. | 10.33 | 13.9 | 6.2 | 1.8 | Crop farming Latin America |

| BF Holding/Bonifiche Ferraresi SpA | 26.02 | 54.2 | 29.3 | 1.3 | Crops farming Italy |

| BrasilAgro | 12.71 | 16.3 | 18.0 | 1.0 | Crops farming/real estate |

| Cresud | 39.25 | 5.6 | 10.2 | 1.2 | Crops farming/real estate |

| Heilongjiang Agriculture | 11.67 | 25.2 | 17.1 | 3.4 | Crops farming, fertilizers, paper China |

| Limoneira Company | 22.49 | 42.2 | 19.9 | 4.4 | Fruits cultivation and marketing USA |

| SLC Agricola | 21.49 | 10.0 | 7.6 | 0.8 | Crops farming and real estate Latin America |

| Average | 23.9 | 15.5 | 2.0 | ||

| Average excluding high-low | 21.5 | 14.6 | 1.7 | ||

| Premium/discount BrasilAgro (%) vs average excluding high-low | -24% | 24% | -41% | ||

| Idem vs Latin American peers | 109% | 102% | 3% |

In conclusion:

- If BrasilAgro’s top 3 customers would apply zero-deforestation commitments to their purchases from BrasilAgro, then the value impact should be a decrease in USD 24 million, or 12 percent of BrasilAgro’s current equity value given a share price of BRL 12.70. If only Bunge and Cargill would halt purchases, the impact would be 4 percent.

- If BrasilAgro found it difficult to sell its three wholly-owned farms, the potential discounts versus the Deloitte estimated values would lead to value-at-risk for shareholders. These equal to 17 percent of the current equity value in case of a 25 percent discount, to 65 percent in case of a 100 percent discount. Although restoration costs are not yet practiced in Latin America, the costs for the deforested 20,639 hectares would amount to a value of USD 57 million, equal to 24 percent of BrasilAgro’s current equity valuation.

- Investors with a forest policy have invested USD 10m in BrasilAgro’s equity. Cresud’s debt and equity investors with forest policies own respectively USD 52 million and USD 80 million.

If BrasilAgro does not develop a zero-deforestation business model and it loses its top three clients, the company could report a net loss and would face a P/B increase to greater than 1.2X. However, if BrasilAgro does develop a zero-deforestation business model, including forest restoration, it could record a net profit with an EV/EBITDA of 129X and, more relevant to investors, a P/B less than 1.2X.