During the last two years, Colombia, the world’s second most biodiverse country, has seen rapidly increasing deforestation. This report discusses the political changes that led to this surge in deforestation. It then focuses on the cattle supply chain, the most important sector exposing investors to deforestation risk in Colombia. In this report, CRR discusses the economic role of the cattle sector in Colombia and maps the key supply chain actors in the beef and dairy sectors. Some of these actors are listed companies that might expose investors to deforestation risk.

Download the PDF here: Deforestation Risk in Colombia: Beef and Dairy Sectors May Expose Investors

Key Findings

- Colombia’s recent surge in deforestation coincided with the peace deal between the government and the FARC rebels. FARC rebels exited previously controlled land, most of which was located in the Amazon region. Government efforts to establish its presence in the abandoned area were insufficient. Thus, the area became a target of different actors seeking to take control over the land.

- In April 2018, the Colombian Supreme Court of Justice ordered the protection of the Colombian Amazon from deforestation. However, current deforestation rates and lack of change so far from government measures signal that it will take a long time for anti-deforestation programs and commitments to have an impact.

- Key economic deforestation drivers in the Colombian Amazon include cattle ranching, land hoarding, coca cultivation and infrastructure. Land hoarding in the Amazon is either conducted with the intent to expand cattle ranches or to seize land with the intention to make a legal claim to it and/or to increase its value.

- Investor exposure to deforestation risk in Colombia is limited and mainly connected to the beef and dairy sectors. Other important drivers such as land hoarding and coca cultivation are mostly financed through illegal markets and therefore do not expose investors to deforestation risk.

- The largest investor exposure to the beef sector is via listed companies Grupo Nutresa (CO) and Minerva (BR). Grupo Nutresa accounts for 16.8 percent of the beef processing sector market share, followed by Minerva Foods with 3.5 percent.

- In the dairy sector, listed companies Grupo Nutresa and Parmalat (IT) have significant market shares. Grupo Nutresa accounts for 4.8 percent of the diary processing sector market and Parmalat accounts for 4.4 percent.

- Investors might also have exposure to the beef and dairy supply chains through listed food retailers Groupe Casino (FR) and Cencosud (CL). Groupe Casino, through its subsidiary Grupo Éxito, is the most important food retailer in Colombia, making up 71 percent of the market. Chilean Cencosud accounts for 5 percent of the market share.

Deforestation rapidly increases since FARC exit

Colombia is the world’s second most biodiverse country, with forest covering more than half of its territory. However, the last two years it has seen rapidly increasing deforestation. According to the Institute of Hydrology, Meteorology, and Environmental Studies (IDEAM), Colombia lost 178,597 hectares of virgin forest in 2016, a 44 percent increase since 2015. Of the forests lost in 2016, 70,074 ha (39 percent) were cleared from the Colombian part of the Amazon. For 2017, IDEAM reported the amount of deforested area increased by 23 percent since 2016, totalling 219,973 hectares of deforested land. In 2018, deforestation was mainly concentrated in the Amazon, which accounted for 66 percent of the total deforested area. The remaining deforested area was located in the following natural regions of Colombia (see Figure 1): the Andes (17 percent) , the Caribbean (7.1 percent), the Pacific (6.1 percent), and the Orinoquia (4.5 percent). Almost half of the country’s 2017 forest loss was concentrated in only seven Amazonian municipalities, all of which showed an increase in deforested area of more than 100 percent compared to what was detected in 2016. The latest report from IDEAM detected that in the first three months of 2018, deforestation increased at a higher rate than registered in previous years. It also highlighted eight active deforestation sites, six of them situated in the Amazon.

Figure 1: Natural regions of Colombia

The surge in deforestation coincided with the historic peace deal between the Revolutionary Armed Forces of Colombia (FARC) and the Colombian Government. In anticipation of this deal, signed in November 2016, the left-wing FARC rebels began to move towards demobilization of vast areas of the country they controlled for over half a century. The government wanted to quickly establish its presence in the places historically affected by armed conflict. However, that did not happen and as a result a power vacuum occurred. The abondoned area became a shelter of criminal activities by dissidents of the now-defunct FARC, criminal gangs and political and economic actors seeking to take control over those lands.

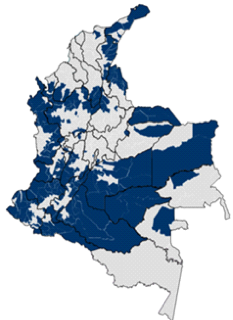

Figure 2: FARC controlled area, 2012

Source: El Instituto de Estudios para el Desarrollo y la Paz, 2012

The peace agreement included measures such as the formalization of seven million hectares of land. This increased the prospects of land titling, particularly in protected forests. As seen in Figure 2, the majority of the area previously controlled by the FARC is located in the Amazon. In this region, the increase in deforestation since the exit of the FARC has been most severe. It should be noted that the FARC itself did not completely halt deforestation. Between 1991 and 2013, 58 percent of the deforestation in Colombia occurred in conflict areas. However, the FARC did de facto regulate the activity in its controlled regions, limiting logging in certain areas and driving out smallholder farmers. This restraint ceased with the exit of the FARC from the conflict areas.

Court ruling orders protection of Amazon, efforts so far insufficient

In April 2018, the Colombian Supreme Court of Justice ordered the protection of the Colombian Amazon from deforestation, ruling in favor of a group of 25 children and youth who sued the Colombian government for failing to protect their right to life and a healthy environment. The court recognized Colombia’s Amazon as an “entity subject of rights.” The ruling granted the rainforest the same legal rights as a human being. The court said that despite numerous international commitments and regulations the Colombian government has not efficiently addressed the problem of deforestation in the Amazon. Therefore, the court ordered the government along with the environment and agriculture ministries and environmental authorities to develop action plans within four months to combat deforestation in the Amazon.

Before the court ruling, Colombia already made several commitments to reduce deforestation. In 2017, it became the first country to agree to a public-private partnership under the Tropical Forest Alliance 2020. This partnership seeks to reduce tropical deforestation associated with the supply of products such as palm oil, soybeans, beef, and pulp and paper. It is aiming for zero net deforestation by 2020 and an end to loss of natural forests by 2030. It thereby combines earlier pledges made by Colombia.

In order to achieve zero net deforestation in the region by 2020, the national government created the Amazon Vision Program in 2016, which is currently supported by Norway, Germany and the United Kingdom. The program aims to address deforestation by establishing appropriate incentives for communities and sectors to protect and sustainably use the Amazon’s resources. Its goal is to improve Colombia’s governance and capacity to manage forests sustainably. Under the UN-REDD Progam, Colombia supported several other initiatives to combat deforestation, such as the Forest and Carbon Monitoring System, the Climate and Forests program of the GIZ and the Forest Carbon Partnership Facility between the World Bank and the Colombian NGO Fondo Acción.

However, current deforestation rates and lack of change so far from government measures signal that it will take a long time for anti-deforestation programs and commitments to have an impact. Moreover, it is unlikely for such programs and commitments to work by themselves. Insufficient governance and governmental capacity within municipalities and departments to design and implement regional plans to eliminate deforestation remains an important issue. The same goes for insufficient technical support and financial incentives for producers to convert dominant land uses to sustainable production systems. Weak incentives for the private sector to invest in sustainable production systems due to insufficient competitiveness of products and high investment risk also make rapid progress unlikely.

Land hoarding, illicit crops, cattle ranching and infrastructure are main deforestation drivers

During 2017, the main drivers of deforestation in Colombia included land hoarding, extensive cattle ranching, illicit crops, development of road infrastructure, illegal extraction of minerals and the extraction of wood. Land hoarding occurs when armed groups, or people from outside a certain territory, systematically take over a protected or forested area. New paramilitary groups, including former factions of the FARC, the ELN guerrillas, criminal gangs and drug-trafficking enterprises typically hoard land, but it can also be executed by individual farmers. In the Amazon, where 66 percent of the 2017 deforestation took place, land hoarding and the expansion of road infrastructure were the main factors. Land hoarding in the Amazon was either conducted with the intent to expand cattle ranches or to seize land with the intention to make a legal claim to it and/or to increase its value. These trends correspond with the overall reality that cattle ranching is the single most important use of cleared land in the Amazon as a whole, with pastures occupying 80 percent of deforested areas.

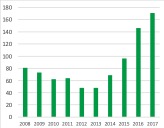

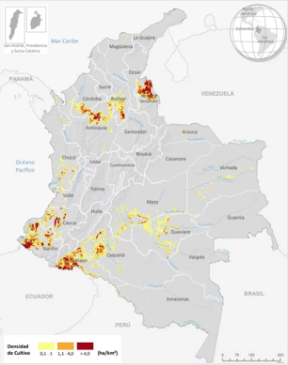

The development of illicit crops, and more specifically coca cultivation (in order to produce cocaine), is on the rise. As seen in Figure 3, from 2015 to 2017, coca cultivation in Colombia increased by 78 percent. Figure 4 shows the areas most affected by coca cultivation in 2017. Besides the obvious clearing of land that accompanies coca cultivation, the wealth increase of narcotics traders (‘narcos’) as a result of huge cocaine profits is another indirect, and significant, cause of deforestation related to coca cultivation. Drug traffickers can be seen as ‘“narco-bourgeoisie”, important actors in changing rural areas by acquiring, transforming, and holding rural landed property. They use cocaine profits to establish and extend private property holdings into communal and protected lands previously unavailable for capital accumulation. Thus, narcos and their acquired illicit capital could play an important role in the land hoarding that is considered the most important driver of deforestation in Colombia.

Figure 3: Coca cultivation in Colombia, 2008-2017 (in thousand hectares)

Source: United Nations’ Office on Drugs and Crime (UNODC), Colombia Reports

Figure 4: Coca cultivation density in Colombia, 2017

Source: United Nations’ Office on Drugs and Crime (UNODC), Colombia Reports

Cattle ranching for beef and diary is main deforestation driver that exposes investors to deforestation risk

The cattle ranching sector is a key driver of deforestation in the Colombian Amazon. Other important deforestation drivers, such as land hoarding, could also clear the way for cattle ranching. Against this backdrop, cattle-ranching is the sector to which investors are most exposed in Colombia. Given the illicit character of land hoarding and coca cultivation, the involvement of investors in these deforestation drivers is less likely.

In 2017, cattle ranching accounted for 21.8 percent of Colombia’s agribusiness GDP and 1.4 percent of its total GDP. This is equivalent to 2.1 times the poultry sector, 4.4 times the swine sector and 8 times the palm oil sector. The cattle sector generated 810,000 direct jobs, accounting for 19 percent of the country’s agricultural employment and 6 percent of total employment. In 2016, livestock accounted for 37.5 million ha of land, which is nearly 80 percent of the agricultural area in Colombia. Over 60 percent of this livestock area consists of pasture. Since only a little over 20 million ha are adequate for cattle ranching, the country is currently overusing its capacity.

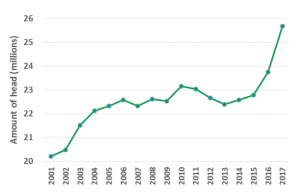

In 2017, the Colombian cattle herd totaled 25.7 million head, which corresponds to 2.6 percent of the global cattle stock. As seen in Figure 5, over the period 2001-2017, the cattle herd has been steadily increasing, reaching its highest level so far in 2017. Since 2015, the herd has rapidly increased, showing a 13 percent expansion in two years.

Figure 5: Cattle herd 2001-2017

Source: FEDEGAN, 2018

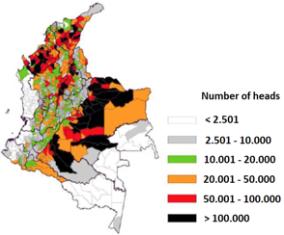

Figure 6 shows the location and density of the cattle herd within the country as of 2016. In 2016, there were 494,402 cattle farms. Most extensive cattle ranching takes place in the natural regions of the Amazon and Orinoquía. The departments of Antioquia, Caqueta, Casanare, Cesar, Cordoba, Meta and Santander accounted for more than 50 percent of the Colombian cattle herd. Caqueta is located in the Amazon.

Figure 6: Location of cattle herd, 2016

Source: FEDEGAN, 2018

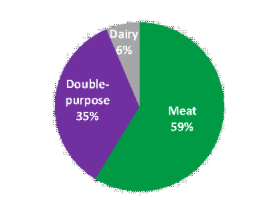

Figure 7 shows what the Colombian cattle herd is used for, as of 2017. On the national level, 58.5 percent of cattle is devoted to meat production, 34.7 percent is dual purpose production and 6.4 percent is specialized dairy. Dairy cattle herds are mainly located on high Andean forests and moors, plateaus and low moorland; double purpose cattle breeds for meat and milk productions are mainly found in tropical areas.

Figure 7: Purpose of cattle, 2017

Source: FEDEGAN, 2018

97 percent of Colombia’s beef consumed domestically

The beef supply chain consists of the following actors:

- Input suppliers (live animals, feed, salts, seeds, breeders, drugs and vaccines, machinery);

- Farmers;

- Cattle traders participating in auctions, brokers, or underwriters;

- Slaughterhouses (public and private);

- Wholesalers (specialist butchers, traders, wholesalers, dealers);

- Food processing industry;

- Meat retailers (butchers, shops, domestic and regional supermarkets);

- Final consumers (restaurants, households).

Generally, the same traders bringing animals for slaughter will also move animal products from slaughterhouses to wholesalers and retailers. Product differentiation within Colombia’s beef value chain is based solely on storage temperature and bone content (carcass/side, cut with bone, boneless, etc.).

In 2017, the Colombian beef market reported total revenue of USD 3.6 billion. In that same year, the amount of cattle slaughtered was 4.1 million head, which equaled production of 910,000 metric tons of beef carcass equivalent. This puts Colombia as the fourth largest beef producer in Latin America. Most of the beef is sold unprocessed. Since 2013, when the Colombian count stood at 4.4 million slaughtered heads, the amount of cattle slaughtered has steadily decreased. DANE, Colombia’s National Statistics Office, reported 3.4 million heads slaughtered in 2017, indicating that illegal clandestine slaughtering and animal smuggling continue to play a critical role in the Colombian beef sector.

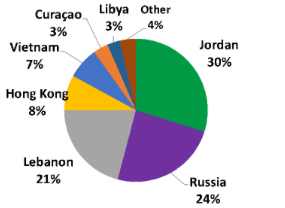

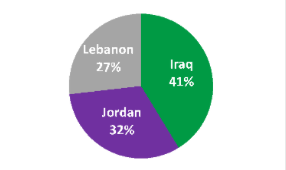

Of the 3.4 million heads that were legally slaughtered, 3.3 million (97 percent) were used for domestic consumption. Figure 8 shows the export destinations of the remaining 0.1 million heads slaughtered. The largest volumes went to Jordan (5,146 tons), Russia (4,182 tons) and Lebanon (3,593 tons). The value of the 2017 beef exports totaled USD 67.4 million. This amount made up 56 percent of the total export value of the beef sector and was mainly concentrated on frozen deboned beef. The remaining 44 percent (USD 52.1 million) of the 2017 export value came from livestock exports. As seen in Figure 8, a total of 87,134 exported living animals were shipped to Iraq (35,924), Jordan (27,844) and Lebanon (23,366). In 2015 and 2016, the reported revenue through beef exports was lower than the 2017 reported revenue.

Figure 8: Beef and livestock export destinations, 2017

Beef exports

Livestock exports

Source: DANE, FEDEGAN, 2018

Although Colombia is one of the countries with the lowest costs to raise cattle, the sector suffers from a lack of productivity and competitiveness. Most cattle ranchers own too few animals and meat loses its competitiveness in the cold supply chain and slaughterhouses, making it costly to export. Therefore, Colombia can export to only countries that accept lower sanitary standards. As of December 2017, eighteen countries bought beef from Colombia.

Per capita beef consumption in Colombia has fluctuated over the years but has decreased since 1990. However, due to a growing population, overall demand for meat in Colombia has increased significantly, mainly caused by an increased consumption of poultry, porcine and fish.

428 companies active in Colombia’s beef sector

In 2015, there were 428 companies in Colombia’s beef sector, with more than half of them located in the departments of Bogota, Antioquia, Valle, Atlantico, Santander and Cundinamarca. At the end of 2017, there were 524 authorized slaughterhouses and 70 authorized meat cutting and packing establishments. The total amount of closures for breaching new sanitary regulations stood at 174 at the end of 2017. Of these 174 closures, 20 clandestine unauthorized slaughterhouses have been closed in 2017, indicating that informal cattle slaughter is still an important part of the beef supply chain. In the Amazon region, slaughtering facilities are underdeveloped. While there are also reports about illegal slaughtering in the Amazon, the majority of cattle is transported to larger slaughterhouses outside the Amazon. Out of the in total 486 slaughterhouses that meet the Colombian sanitary requirements or have provisional sanitary authorization, 17 are located within departments that belong to the Amazon natural region.

Figure 9 shows the market share of the top 10 companies operating in the beef processing industry of Colombia, grouping companies that belong to the same parent. The market shares are based upon sales data for the year 2017. The total beef market value of USD 3,640 million reported by FEDEGAN is used as an indicator for the aggregated market revenue.

Grupo Nutresa is the most dominant company in the beef market, with a market share of 16.8 percent, mainly through its subsidiary Alimentos Carnicos. Grupo Nutresa is the leading processed foods company in Colombia, holding a 60 percent market share in the aggregated processed foods market. It is listed on the Colombia Stock Exchange. The Brazilian Minerva Foods, one of the leaders in the South American beef sector, is the second most important company. However, its market share accounts for only 3.5 percent of the total market. The other companies making up the top 10 are all private Colombian companies.

Figure 9: Market share of top 10 companies in beef sector, 2017

| Rank | Company name | Parent | Country | Ownership | Market share beef (2017) |

| Alimentos Carnicos | Grupo Nutresa | Colombia | Public | 15.83% | |

| Industria de Alimentos Zenú | Grupo Nutresa | Colombia | Public | 0.96% | |

| 1 | Grupo Nutresa | 16.79% | |||

| Red Cárnica | Minerva Foods | Brazil | Public | 3.34% | |

| Minerva Colombia | Minerva Foods | Brazil | Public | 0.14% | |

| 2 | Minvera Foods | 3.48% | |||

| 3 | Camagüey | – | Colombia | Private | 1.77% |

| Comestibles Dan | – | Colombia | Private | 1.23% | |

| Comestibles Dan Zona Franca | Comestibles Dan | Colombia | Private | 0.06% | |

| 4 | Comestibles Dan | 1.29% | |||

| 5 | Carnes Casablanca | Industrias Casablanca | Colombia | Private | 1.28% |

| 6 | Expoganados Internacional | – | Colombia | Private | 1.22% |

| 7 | Cialta | – | Colombia | Private | 0.88% |

| 8 | Alimentos Carbel | – | Colombia | Private | 0.75% |

| 9 | Carnes Santa Cruz | – | Colombia | Private | 0.73% |

| Frigorifico Guadalupe | – | Colombia | Private | 0.53% | |

| Carnes Finas Guadalupe | Frigorifico Guadalupe | Colombia | Private | 0.20% | |

| 10 | Frigorifico Guadalupe | 0.73% | |||

| Total top 10 companies | 28.92% | ||||

Source: LaNota, FEDEGAN, 2018

Colombian dairy sector accounts for USD 3.1 billion in revenue

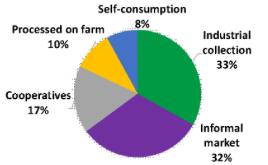

In 2017, the Colombian market for raw milk reported a total revenue of USD 2.1 billion, while the 78 largest dairy companies in Colombia accounted for a total revenue of USD 3.1 billion. In that same year, raw milk production stood at 7.1 billion liters, making Colombia the fourth largest milk producer in Latin America. Figure 10 shows the destination of the produced milk. Most of the milk either ends up at industrial companies (33 percent) or in the informal market (32 percent). Unlike the decreasing trend in cattle slaughtering since 2013, milk production has increased by 7 percent over the 2013-2017 period. Since 1990, when milk production stood at 3.9 billion liters, the production of milk reached an all-time high in 2017. However, the country lacks competitiveness, having high cost of production compared with its competitors. This difference can be explained by the fact that Colombia’s dairy producers rely on concentrate-based animal nutrition products made from imported corn and soy, which is hindering the industry’s growth. A lack of processing efficiency at the end of the dairy chain for products like cheese and milk powder adds to Colombia’s lack of competitiveness.

Figure 10: Destination of produced milk, 2017

Source: DANE, FEDEGAN, 2018

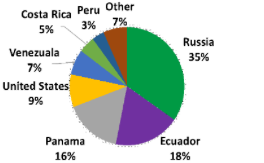

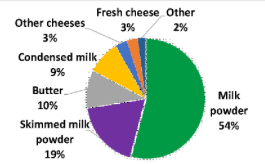

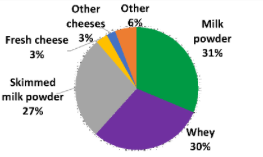

Ninety-two percent of the Colombian milk production was consumed domestically in 2017. In that same year, 556.1 million liters of dairy products were exported. The exports were valued (FOB, Free On Board) at USD 22.0 million and corresponded to 8 percent of that year’s total milk production. Most of the dairy exports went to Russia (35 percent), Ecuador (18 percent) and Panama (16 percent) (Figure 11a). Milk powder, both whole and skimmed, accounted for 73 percent of the total dairy exports, while butter (10 percent) and condensed milk (9 percent) were the most important other dairy export products (Figure 11b).

Figure 11a: Dairy export, 2017

Export destinations

Source: Consejo Nacional Lácteo (CNL), 2018

Figure 11b: Dairy exports, 2017

Types of dairy products

Source: CNL, 2018

Compared to 2016, when dairy exports stood at an all-time low, the 2017 dairy exports grew by almost 600 percent. However, these export numbers are still far away from the peak levels in 2008, when 31.6 million liters were sold abroad. The most important reason for the free fall of Colombian dairy exports between 2008 and 2012 was the reduction of trade with Venezuela. The trade agreement with Venezuela faltered. In 2011, a new agreement helped exports rise in 2012. However, difficulties in the last couple of years to exploit Free Trade Agreements with other countries due to the absence of strong institutions are the main reason for a lack of competitiveness. This has led to a trade imbalance in several sectors, including the dairy sector.

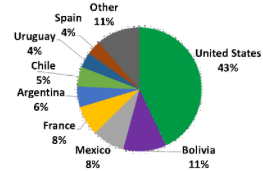

The dairy trade imbalance of Colombia is apparent when looking at the 2017 dairy imports, which amounted to 4.4 billion liters and represented a total value (CIF, Cost Insurance and Freight) of USD 109.3 million. These imports equal 62 percent of the total domestic production of 2017. Compared to 2016, when 58.2 billion liters were imported, the amount of imports have decreased by 25 percent. However, when comparing 2017 imports with the average imports of 0.9 billion liters for 2003-2011, imports in 2017 were still relatively high. Most dairy imports originated from the United States (43 percent), Bolivia (11 percent), Mexico and France (both 8 percent) (Figure 12). Milk powder (58 percent, whole and skimmed), whey (30 percent) and cheese (6 percent, fresh and other) are the top imported dairy products.

Figure 12: Dairy imports, 2017

Countries of origin

Types of dairy products

Source: Consejo Nacional Lácteo, 2018

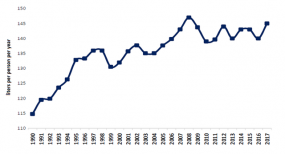

Since 1990, the yearly per capita milk consumption in Colombia has increased, from 115 liters in 1990 to 145 liter per year in 2017 (Figure 13). From 2016 to 2017, the per capita milk consumption increased by 4 percent. In 2017, per capital milk consumption was more than three times the average consumption of developed countries.

Figure 13: Yearly per capita milk consumption, 1990-2017

Source: FEDEGAN, 2018

80 companies in Colombia’s dairy sector

In 2015, there were over 80 companies in Colombia’s dairy sector, with more than half located in the departments of Bogota and Antioquia. Figure 14 shows the market share of top 10 companies operating in the dairy industry of Colombia, grouping companies that belong to the same parent. The market shares are based upon sales data for the year 2017. The total market value of USD 3,074 million reported by LaNota as aggregated sales for the 78 largest companies was used as an indicator for the aggregated market revenue.

Colanta, a cooperative of producers and workers, is the most dominant company in the dairy market, with a market share of 23 percent. The private Colombian companies Alpina Group and Alquería are the other two important players on the dairy market, accounting for market shares of 19.9 percent and 11.3 percent respectively. Colombian Grupo Nutresa (4.8 percent) and Italian Parmalat (4.4 percent), companies in the top 10, are listed on a stock exchange.

Figure 14: Market share of top 10 companies in dairy sector, 2017

| Rank | Company name | Parent | Country | Ownership | Market share dairy (2017) |

| 1 | Colanta | – | Colombia | Cooperative | 22.95% |

| Alipna Productos Alimenticios | Alpina Group | Colombia | Private | 19.80% | |

| Alpina Cauca Zona Franca | Alpina Group | Colombia | Private | 0.10% | |

| 2 | Alpina Group | 19.90% | |||

| Alquería | – | Colombia | Private | 7.90% | |

| Freskaleche | Alquería | Colombia | Private | 2.11% | |

| Dasa de Colombia | Alquería | Colombia | Private | 0.87% | |

| CPNS | Alquería | Colombia | Private | 0.41% | |

| 3 | Alquería | 11.29% | |||

| Meals de Colombia | Grupo Nutresa | Colombia | Public | 4.50% | |

| Quesos del Vecchio | Grupo Nutresa | Colombia | Public | 0.29% | |

| 4 | Grupo Nutresa | 4.79% | |||

| Parmalat Colombia | Parmalat | Italy | Public | 2.91% | |

| Proleche | Parmalat | Italy | Public | 1.49% | |

| 5 | Parmalat | 4.40% | |||

| 6 | Gloria Colombia (Algarra) | Grupo Gloria | Peru | Semi-private | 3.53% |

| 7 | Coolechera | – | Colombia | Cooperative | 2.10% |

| 8 | Lácteos Betania | – | Colombia | Private | 2.08% |

| 9 | Alival | – | Colombia | Private | 1.88% |

| 10 | Lácteos El Recreo | – | Colombia | Private | 1.73% |

| Total top 10 companies | 74.65% | ||||

Source: LaNota, 2018

Minerva Foods only listed company that has specific Amazon deforestation policy in place

Minerva Foods is the only company of its sector in Latin America to be recognized by the International Finance Corporation of the World Bank Group for acting with sustainable practices and generating value for an entire productive chain. The company’s raw material origination criteria, amongst others, claims that farm and supplier partners are not related to deforestation in the Amazon. Grupo Nutresa and Parmalat have no specific policies in place regarding deforestation in the Amazon. Grupo Nutresa, an important player in both the beef and dairy sector, does have a general sustainable sourcing policy in place. In its guidelines for suppliers, Grupo Nutresa also describes specific audit forms for cattle production, livestock and milk.

Grupo Éxito dominant force in Colombian food retail sector

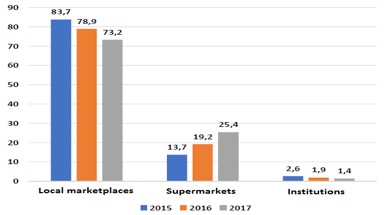

In 2017, some 73 percent of Colombian consumers bought beef at local marketplaces such as market squares and neighborhood stores, whereas supermarkets accounted for only 25 percent of the sales locations. Institutions such as prisons and community kitchens accounted for 1 percent of total beef sales locations. Figure 15 shows that supermarkets are becoming more important sales locations, increasing their market share by 11.7 percent for the period 2015-17. This increase comes mainly at the expense of local marketplaces, which lost 10.5 percent of their market share during the same period.

Figure 15: Where consumers buy beef, 2015-2017

Source: FEDEGAN, 2018

Grupo Éxito, part of the listed French Groupe Casino, is the most important food retailer in Colombia, representing 71 percent of the 2017 sales of the top 10 food retailers (figure 16). Colombian private companies Olimpica and Alkosto rank second and third, representing seven and six percent of the top 10 aggregated sales respectively. Cencosud Colombia, which accounts for five percent of the top 10 aggregated sales, is a subsidiary of the listed Chilean Cencosud. CRR recently published a report on Cencosud, showing the company’s links to high-risk Brazilian Amazon slaughterhouses.

Figure 16: Top 10 food retailers in Colombia, 2017

| Rank | Company name | Parent | Country | Ownership | Sales 2017 (USD million) |

| 1 | Grupo Éxito | Groupe Casino | France | Listed | 18,626 |

| 2 | Olimpica | – | Colombia | Private | 1,884 |

| 3 | Alkosto | – | Colombia | Private | 1,606 |

| 4 | Cencosud Colombia | Cencosud | Chile | Listed | 1,267 |

| 5 | D1 | Grupo Santo Domingo | Colombia | Private | 1,025 |

| 6 | La 14 | – | Colombia | Private | 495 |

| 7 | Ara | Jerónimo Martins | Colombia | Listed | 475 |

| 8 | Makro | SHV Holdings | Netherlands | Private | 364 |

| 9 | PriceSmart Colombia | PriceSmart | United States | Listed | 348 |

| 10 | Justo y Bueno | Mercadería | Colombia | Private | 254 |

| Total top 10 retailers | 26,344 | ||||

Source: Superintendencia de Sociedades, La Republica, Global Agricultural Information Network, 2018

According to rainforest rating agency Forest 500, Groupe Casino, the listed company with the highest sales in Colombia, scores two out of five on its overall forest policy and three out of five on its specific cattle policy. Cencosud, the second largest listed food retailer, scores zero out of five on both overall forest policy and cattle specific policy.