Summary

- There is risk of more expensive commercial financing, which accounts for around 53 percent of all rural financing.

- Some engagement from concerned investors may also address the weak ESG scores of their soy investees.

- Risk from more expensive barter-based financing is limited.

The large-scale expansion of soybean cultivation in Brazil has been identified as one of the key drivers of deforestation in the last 20 years. The Cerrado, which is a particularly biodiverse and carbon-rich biome, has been rapidly converted. Prior analyses by Chain Reaction Research have found that soy producers face financial risks from ongoing involvement in this Cerrado deforestation. This report builds upon two previously-identified key trends:

- At least 49 percent of soy traders have committed to make their supply chains deforestation-free. The share as well as the strength of commitments are expected to further increase in the mid-term future. This creates market access risk for producers with weak sustainability performance.

- High ESG-performers are perceived as less risky due to their association with highperformance. This likely gives them to access to cheaper green finance. Some rural financing programs are also cheaper for producers with higher sustainability standards.

This paper looks in detail at the financing relations between nine key soy producers and their investors, scrutinizing any mismatches between the ESG performance of the two. They are scored from 0 to 100 on a set of sustainability and policy indicators. The paper also explores whether soy producers face the risk of more expensive financing due to weak sustainability commitments and scores.

Key findings:

- There is risk of more expensive commercial financing, which accounts for around 53 percent of all rural financing. The risk stems from a significant discrepancy between the ESG policy scores of some large soy growers (averaging 18 out of 100), compared with the average scores of their major investors (31 out of 100). Producers with low ESG scores are more than 80 percent credit financed and their major creditors have an average policy score of 45. Some investors provide cheaper green financing alternatives, likely disadvantaging low-scoring soy producers.

- Some engagement from concerned investors may also address the weak ESG scores of their soy investees. This may raise awareness among the producers and lead to better ESG policies, or may result in worse financial conditions for ESG policy laggards. The subsidized rural credit system, accounting for 30 percent of rural financing, already offers cheaper options for sustainability improvements.

- Risk from more expensive barter-based financing is limited. This type of financing accounts for 17 percent of rural financing and is provided by agri-traders, processors or manufacturers, who often have high ESG standards in place. Some risk stems from the stark contrast between soy producers with weak environmental standards, as opposed to 49 percent of the traders having some form of zero deforestation commitment. Traders may impose ESG requirements over their supply chains, which may also result in severed financing ties with non- compliant parties. Nevertheless, such developments are too early in implementation stages to infer direct risk.

- Soy growers might risk worse financial terms, such are increased cost of debt and equity, reduced net profits, reduced present value of free cash flows, lower return on investments, hampered growth and ultimately, potentially lower share prices. It may eventually be cheaper for low-scoring soy growers to adopt better ESG policies than to risk these impacts.

Brazil is a Global Leader in Soybean Cultivation

The global soybean cultivation area has more than doubled during the last 25 years and is projected to further increase. Brazil produced 114.1 million tons from 33.9 million ha in market year 2016/17. Its share in the global soybean surface increased from 18 percent (9.7 million ha) in 1991/92 to 28 percent in 2016/17 . Meat consumption and biodiesel are the major drivers of growing global soy demand in the form of vegetable oil and animal feed. Demand is projected to further increase, particularly in the emerging Asian economies. Domestic consumption in Brazil as one of the major soy producers is also expected to increase in response to growing poultry and pork production, as well as biodiesel.

The distribution of farmland in Brazil is fragmented, with many small and few large producers. According to the last agricultural census (2006), 98.5 percent of Brazilian farms have less than 1,000 ha and account for 54.8 percent of farmland, while farms with more than 1,000 ha account for 1.5 percent of farms but 45.2 percent of total farmland (Figure 2). It is likely that this trend continued over the past decade, as financial conditions favor larger producers. Thus, the production of soy is highly dispersed between a comparatively small number of large producers, and many medium- and small-sized producers. This paper is concerned with the average large producer.

Soybean Expansion is Driving Deforestation in Carbon-rich Areas

Soybean production has been one of the key drivers of deforestation in Brazil in the last two decades, but the Amazon moratorium was an effective mitigating factor. Soy growth is still leading to significant deforestation and biodiversity loss, as well as substantial greenhouse gas emissions. While Amazon deforestation remains a concern, the interrelation between Amazon deforestation and soy expansion has been substantially weakened by the 2006 Amazon Soy Moratorium. While in 2004, up to 30 percent of soybean cultivation in the Amazon came from recent deforestation, this share dropped to 1.3 percent in 2016. Soy expansion has shifted to the Cerrado.

The Cerrado is an environmentally sensitive and carbon-rich forested savannah, which has been converted for agricultural products including soy, corn, and cotton during the last decades. The remaining forested area is largely unprotected and under threat. Ongoing conversion leads to biodiversity loss and release of large carbon stocks. Land speculation contributes to the problem, as it produces value from land appreciation through clearing its native vegetation, transforming it into farmland and selling it off.

Mounting pressure to halt deforestation from key stakeholders including investors and key soy buyers may change the way land is converted in the Cerrado. This may disrupt the anticipated increase of over six million ha in Brazilian soybean area until 2025. i.e. planned land expansions may not be realized. This creates a risky environment, where violation of procurement and ESG policies may result in increased financing costs, divestment pressure or severed business relationships.

Financing of Brazilian Soy Producers May Become More Expensive

Within the different types of rural financing provided, commercial banks and institutional investors play a key role in enabling the operations and expansion of the soy industry since they provide more than half of the financing. There are three key sources of rural financing in Brazil:

- commercial financial institutions and other sources, accounting for approximately 53 percent.

- subsidized rural credit which accounted for approximately 30 percent of financing in the last 5 to 10 years,

- barter from traders and input providers accounting for around 17 percent.

Pillar 1 – Commercial Financial Institutions may impose higher interest rates

Commercial banks, international asset managers and sources like self-funding form the core type of financing available for agricultural activities. Domestic lending is connected to high costs, as private sector banks are hesitant to provide long-term credit due to concerns over unpredictable risks in the agricultural sector. (Therefore, the rationale of the governmental rural credit system has been to offer financing at more affordable rates.) The further tightened borrowing requirements of commercial banks are also a reaction to rising default rates in Brazil’s ongoing recession. This has stimulated the strong return of barter-based financing in recent years. Nevertheless, commercial finance is more transparent than the other types of financing and a link can be established between individual producers and the majority of their investors.

Because of the mounting global attention to higher sustainability, many of these investors are likely to subscribe to high ESG standards and to impose them on their investees. Discrepancies in ESG performance may result in reputational damage for investors. Furthermore, ESG-low-scoring producers are missing out on numerous opportunities for cheaper sustainable finance. Rabobank, JPMorgan Chase, ING, Itau Unibanco and more higher scoring investors, have large sustainable programs which remain unavailable for the low-scoring soy producers.

With high interest rates and bank reluctance to service a high-risk sector, corporate farms also started to look for backing from foreign investment funds in recent years. Foreign ownership in land has been limited since 2010, but minority investments took place. For example, UK-based hedge fund Altima Partners and U.S.-based Capital Group hold stakes in privately-owned O Telhar Agropecuaria, a major soy producer in Mato Grosso State. A similar example is the Valiance (NASDAQ:UK) stake in SLC LandCo, a subsidiary of SLC Agricola.

Pillar 2 – Rural Credit System – unsustainable practices may hamper access

Government-supported rural credit is disbursed through the National System of Rural Credit (NASDAQ:SNCR) at controlled interest rates. Rural credit is disbursed through various programs via the Brazilian Development Bank (Banco Nacional de Desenvolvimento Econômico e Social (BNDES)) as well as its intermediaries, including other public banks (Central Bank of Brazil, Banco do Brasil, Banco da Amazônia, Banco do Nordeste), as well as accredited private-sector banks (e.g. Rabobank, Santander, JPMorgan). Rural credit mostly benefits large commercial farmers. In 2016/17, more than 50 percent of the subsidized credit lines was for working capital investments in commercial farms, 21 percent for investments by large producers and about 12 percent for investments in family farms.

The Brazilian government increased the available rural credit in 2015/16 while also hiking up interest rates of the previously heavily subsidized credit. At the same time, commercial banks tightened borrowing requirements as a reaction to increasing default rates in economically difficult times with falling crop prices and a volatile Brazilian currency. The period 2016/17 saw a slight decline in credit volumes.

The Brazilian government increased the rural credits again in the 2017/18 season, and reduced the interest rate on several priority programs. The Inovagro program that finances investments related to technological improvements and better agricultural practices became cheaper. Another rural credit line – ABC program (Agricultura de Baixo Carbono) aims to reduce the emission of greenhouse gases from agricultural activities, including a reduction of deforestation. These programs imply that rural credit may be more easily accessible for companies abiding to higher sustainability standards. The technological eligibility criteria of these innovative credit programs make them more easily accessible for larger producers. Nevertheless, there is already a trend of rewarding higher ESG performance with lower interest rate and continued program support.

Pillar 3 – Barter-based financing – might impose worse financing terms

Agricultural processors, traders and input manufacturers provide barter-based financing. Given their difficulties accessing traditional financing, under-capitalized farmers have increasingly sought barter-based financing in the past decade. For processors and traders, such as Bunge, Cargill, or Louis Dreyfus, this provides an opportunity to secure physical commodity supplies for trading, and reduce payment risks as part of the crop is designated as collateral. At the same time, the traders receive soy from the producers, and provide financing and price risk management, thus also collecting interest fees. However, by servicing more of the producers’ financing needs, traders also expose themselves to the inherent risks of agricultural production, such as unforeseen harvest losses through unfavorable weather conditions and the potential of farmers defaulting on crop delivery. These risks can nevertheless be hedged.

Traders have strengthened their commitments to eliminate deforestation from their supply chains and may impose these on their barter-investees. Calls by leading consumer goods companies and retailers to preserve the remaining natural vegetation of the Cerrado can further strengthen traders’ commitments. This may also result in banning legal deforestation. Traders who do not live up to their pledges to fulfill the market demand for zero-deforestation soy could put their reputation and market at risk. Thus, soy producers involved in deforestation may lose access to clients. This may also result in limited barter-based financing, and make it more expensive. Nevertheless, there is often a simultaneous financing and a trade relationship between these parties, which makes changes of the terms of either less likely.

ESG Policies of Soy Producers are Weak, Lack Environmental Commitments

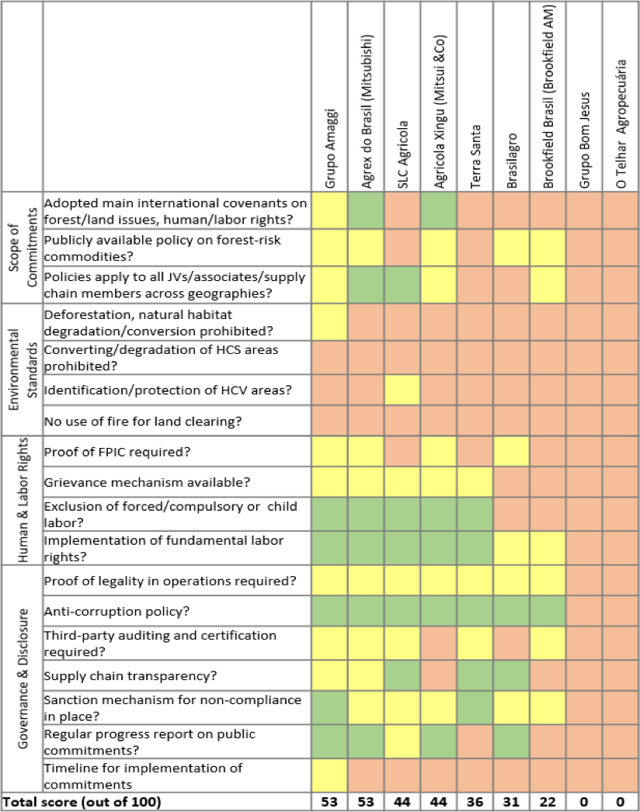

The nine producers analyzed have an average policy score of 31 out of 100, suggesting a lagging industry development (Figure 3). These ESG policies were evaluated against a set of 18 criteria (the Appendix provides a detailed description of the methodological approach and the selection of the companies.)

The key issues and findings covered in the analysis are:

- Scope of commitments: the overall presence and scope of ESG policies and alignment with international covenants on forest, land, human and labor rights issues. Half of the soy growers perform well and have some ESG policies in place.

- Environmental standards: the exclusion of deforestation and other environmentally destructive practices. All analyzed companies are deficient in environmental standards, with only two companies showing some awareness in relation to deforestation and conservation.

- Human & labor rights: adherence to key criteria on human and labor rights. Most of the soy producers score comparatively high on this pillar.

- Governance & disclosure: performance on transparency and good governance practices. More than half of the companies perform well on this issue.

The results show that the existing scores are driven by policies on governance and disclosure, human and labor rights and the overall scope of the commitments, not by environmental standards.

Figure 3: Soy producers ESG policy scores. Source: CRR. Note: The website of O Telhar Agropecuaria has been down for maintenance during the research period.

Soy producers show a lack of environmental awareness and commitments to zero- deforestation, even while this trend is quickly taking off among key buyers and investors. As the only company with a tangible statement on the conversion of natural habitats, producer and trader Grupo Amaggi (Amaggi) states that “[…] it does not carry out conversions of native forests for the agricultural use.[…] projects and partnerships to encourage responsible production by producers are signed annually to promote the Business Principles for Food and Agriculture, of the United Nations Global Compact, as well as the fight against illegal deforestation.” It does not specify whether its own commitment covers the conversion of secondary forests and other valuable natural habitats, and does not exclude legal deforestation by suppliers. Identification and protection of High Carbon Stock (HCS) and High Conservation Value (HCV) areas is largely absent from these policies.

The low-scoring soy sector is exposed to risk of divestment or divestment pressure, as on average its investors hold stronger sustainability policies.

| Top Investors in low scoring producers, with scores > 18 | Policy score |

| Rabobank | 83 |

| JPMorgan Chase | 58 |

| ING Group | 58 |

| Itaú Unibanco | 42 |

| Banco do Nordeste do Brasil | 39 |

| Scotiabank | 33 |

| CIBC | 33 |

| Royal Bank of Canada | 33 |

| BTG Pactual | 28 |

| Banco Paulista | 22 |

Deficient ESG policies may result in loss of clients for the producers. The above findings for upstream producers are in stark contrast to the deforestation-related ESG commitments of the leading traders, processors and exporters of soy from Brazil. A recent analysis by Chain Reaction Research has found that at least 49 percent of the Brazilian soy export market are covered by a type of zero deforestation commitment. This awareness of the issue among soy traders and processors appears to be further developed than among producers. Traders are likely to demand compliance from their suppliers, and may threaten to sever business relations due to the risks they otherwise experience.

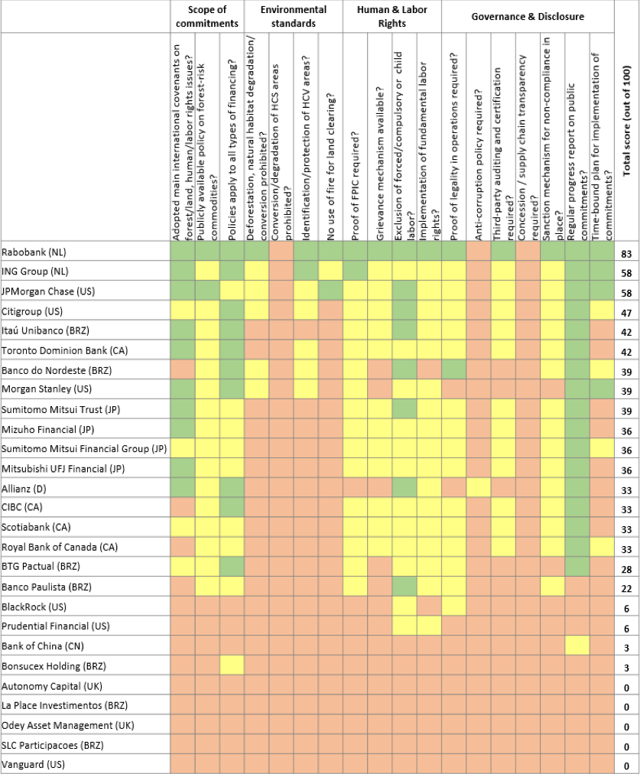

Producers ranged between low and medium scoring on ESG policies; the low scoring risk more expensive finance. The larger producers, or the ones which are part of a large conglomerate, have developed stronger policies, although only two growers score above 50 out of 100. Still, the average policy score of the medium scoring producer group is 49, while the laggards achieve an average policy score of 18. On the other hand, investors tend to have average and median scores around 32. The investors with the largest funds reach a score of 45, which aligns them with the ESG policy performance of the mid-scoring soy producers. Therefore, a conflict and risk related to financing exists primarily between the low-scoring soy producers and their investors, if the latter score higher.

|

Figure 4: Average ESG policy scores, as of Dec 2017. Source: CRR.

Low-scoring soy producers may be facing more expensive financing and shareholder activism. This is because investors financing soy producers with low sustainability standards have higher sustainability policy scores, averaging a third higher or 32 out of 100, compared to the low-scoring growers, who average 18. Medium-scoring producers, in fact, tend to have better policies than their investors (simple averages have been used).

Creditors Have Higher Policy Scores Than Their Investees

Among the low-scoring producers, 80 percent of financing comes from loans from companies with an average ESG policy score of 45, as opposed to an average policy of 18 for the producers. This drives a conclusion that investors may require their investees to develop better ESG policies and comply with them. Alternatively, creditors could demand higher interest rates to compensate for increased risk exposure, which can translate into higher financing costs for the growers.

Two top creditors – scoring 58 and 83 – on policy assessments are likely to engage with and possibly pressure the low scoring soy producers on ESG policies. ING and Rabobank are the third and the fourth largest credit investors in the low-scoring soy producers. Both Rabobank and ING have sustainable products with better terms for high-performing companies. The top two investors in the low-scoring soy producers also score higher on sustainability, but may exert less pressure on their Brazilian investees. These are Banco do Nordeste do Brazil and Itau Unibanco. They each have medium to low- scoring sustainability policies and are unlikely to be leveraged against unsustainable soy production. Nevertheless, they may be exposed to financial risks related to poor sustainability.

| Rank | Top 5 Creditors,

2012 -2017 |

Investor country | USD million | Policy score |

| 1 | Banco do Nordeste do Brasil | Brazil | 117.0 | 39 |

| 2 | Itaú Unibanco | Brazil | 64.0 | 42 |

| 3 | ING Group | Netherlands | 41.9 | 58 |

| 4 | Rabobank | Netherlands | 36.9 | 83 |

| 5 | Bank of China | China | 36.2 | 3 |

| Simple average policy score, max 100 | 45 | |||

Figure 5: Top 5 creditors of low scoring soy producers. Source: Thomson Reuters, Bloomberg, CRR, values adjusted to soy-related investments only.

Shareholders Also Have Higher Policy Scores Than Their Investees

Majority shareholdings are international. Given that on average these investors have higher sustainability standards, they may exert positive pressure on their Brazilian investees and drive change in their policies. Nevertheless, this represents only around 12 percent of all the funding going to the producers. Compared to the creditors, this minor stake limits the leverage that shareholders have over low-scoring investees.

Two top shareholders have considerably higher policy scores than their low-scoring investees and might engage. The third largest equity investor in the low-scoring producers is JPMorgan Chase, with a relatively high sustainability score of 58. This is followed by Banco Paulista, a Brazilian investor, which has a better sustainability policy than some of its local peers, but still a low score of 22. While these investors may react to the policy score discrepancy, their stake each is less than one percent of all investments, so their influence is limited.

On average, shareholders in the low-scoring soy producers have lower sustainability scores – averaging 17 – than the creditors with 45. Nevertheless, the investors are exposed to the risk of volatile share prices related to unsustainable production. Therefore, they can be reasonably expected to engage with, or divest from, their investees. Given JPMorgan’s exposure and high score, it may be the first shareholder to act upon sustainability issues.

| Rank | Shareholdings, Nov 2017 | Investor country | USD Million | Policy score |

| 1 | Laplace Investimentos e Gestao de Recursos | Brazil | 13.7 | 0 |

| 2 | Bonsucex Holding | Brazil | 9.5 | 3 |

| 3 | JPMorgan Chase | United States | 9.0 | 58 |

| 4 | Banco Paulista | Brazil | 7.1 | 22 |

| 5 | Autonomy Capital | United Kingdom | 6.7 | 0 |

| Simple average policy score | 17 | |||

Figure 6: Largest shareholders in the low-scoring soy producers, Brazil. Source: Thomson Reuters, Bloomberg, CRR, values adjusted to soy-related investments only.

The majority of the underwriters of low-scoring soy producers have high policy scores. Brazilian banks provided 78 percent of all underwriting of share and bond issuances by low-scoring soy producers during the period from 2012 to 2017.

Canadian banks provided 16 percent of the services. Underwriters average an ESG policy score of 34, 16 higher than the average of the low-scoring soy producers. This might give underwriters grounds for engaging with their clients. However, the provision of underwriting services is the most remote in terms of responsibility and reputation. Thus, there are limited expectations that these banks might leverage the growers.

|

||||||||||||||||||||||||||||||||||||

Figure 7: Underwriting services provided between 2012 – 2017. Source: Bloomberg, Thomson Reuters, CRR.

Investors in mid-scoring soy producers are not likely to leverage them towards better policies

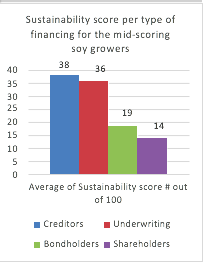

Four of the nine analyzed Brazilian soy producers have moderate policy scores, averaging 49. These are Amaggi, Agrex do Brasil (Mitsubishi Corp), SLC Agricola and Agricola Xingu (Mitsui & Co). Compared to the low-scoring soy producers, this group includes two soy-focused businesses – Amaggi and SCL Agricola – and two large investment institutions with diverse portfolios and only slight exposure to soy. To allow for this, the investments considered are adjusted for the relative size of the Brazilian soy segment of the producers. However, the different nature of these corporations suggests that their top investors may be different from the top investors of the low-scoring soy growers. Still the mid-scoring growers have higher policy scores then all of their top investors. This suggests that they may have improved their policies due to factors other than investor engagement or pressure.

Key financial relationships with conflicting policy scores

The tables below present investments going from a relatively higher scoring investor to a low scoring soy-producer. This policy score discrepancy may form grounds for engagement by the investors with their investees. Alternatively, rolling over some of the credits below may become more expensive, while some shareholdings may be reconsidered because of reputational damage. The investors are ordered by size of total exposure to the select group of low-scoring soy producers. A ranking based on the policy scores of the investors is provided in Figure 15 in the appendix. (These investments are assumed to all fall under Pillar 1 of rural financing, as explained above.)

| Producers

Creditors |

Bom Jesus | BrasilAgro | Brookfield | El Tejar | Terra Santa

Agro |

Total |

| Banco do Nordeste | 25.7 | 91.3 | 117.0 | |||

| do Brasil | ||||||

| Itaú Unibanco | 33.1 | 0.4 | 30.5 | 64.0 | ||

| ING Group | 0.1 | 41.8 | 41.9 | |||

| Rabobank | 3.3 | 33.6 | 36.9 | |||

| Royal Bank of | 0.9 | 0.9 | ||||

| Canada | ||||||

| CIBC | 0.7 | 0.7 | ||||

| JPMorgan Chase | 0.5 | 0.5 | ||||

| Scotiabank | 0.0 | 0.0 | ||||

| Grand Total | 25.7 | 124.4 | 2.2 | 45.5 | 64.1 | 261.9 |

Figure 8: Credit provided between 2012 – 2017 in USD. Source: Bloomberg, Thomson Reuters, CRR.

The figures are a sum of credit provided over the period 2012 – 2017, and current bondholdings, as of November 2017. They are adjusted to funds going to soy operations only.

| Producers

Shareholders |

BrasilAgro | Brookfield Asset Management | Terra Santa Agro

SA |

Total |

| JPMorgan Chase | 0.1 | 0.0 | 8.9 | 9.1 |

| Banco Paulista | 7.1 | 7.1 | ||

| BTG Pactual | 0.0 | 4.4 | 4.4 | |

| Royal Bank of Canada | 2.4 | 2.4 | ||

| CIBC | 0.7 | 0.7 | ||

| Scotiabank | 0.5 | 0.5 | ||

| Itaú Unibanco | 0.1 | 0.00 | 0.1 | |

| Grand Total | 0.2 | 3.6 | 20.4 | 24.2 |

Figure 9: Shareholding in USD mln, as of Nov 2017. Source: Bloomberg, Thomson Reuters, CRR. Figures are adjusted to funds going to soy operations only.

Low-Scoring Soy Producers: Worse Credit Conditions Lead to Financial Risks

Our analysis shows that there are key investors who have relatively strong policies, with investees who have contrastingly weak ones. This situation entails risks for each stakeholder:

- may pool investments to protect their own reputations and mitigate risks arising from any associated unsustainable soy production.

- The low-scoring companies may be engaged by their investors to change policies and practices, or financing may become more expensive.

- The low-scoring companies may be engaged with by their customers, which may also be providing barter financing and may threaten to leave. This could cause revenue reduction and a loss of financing.

- Financiers who do not act on policy controversies may in turn face risks arising in their own financial relations. For example, investors in the banks financing unsustainable soy also are exposed indirectly to sustainability risks and thus have grounds to reconsider investment relations.

The major risk for the low-scoring growers is worse credit conditions, which can have multiple material adverse effects. A producer with low sustainability performance has to renegotiate the terms of its credit financing and sits together with its key bankers: the banks have analyzed the above-mentioned scenarios and therefore perceive the soy grower as a riskier investment and therefore demand higher compensation for any loans they provide. They can also request more pledged collateral. This is a likely scenario, as the low-scoring soy producers are clearly identifiable as laggards versus their higher scoring peers. Multiple studies support that conclusion.

Financial Impacts of Worse Credit Conditions

- Increased financing costs: if credit investors perceive unsustainable companies as riskier, which is warranted in the scenarios described above, they may increase their required interest rates, or cost of debt. An example is Terra Santa Agro, which has received USD 34 million from Rabobank. Rabobank has an ESG policy score more than four times higher than its investee and may address that in different ways. One of these is to demand a higher interest rate, another is to divest from Terra Santa. In the latter case, the soy producer may have to find another banker on a short notice, and may receive worse borrowing conditions. This represents investor pressure that the likes of Terra Santa and El Tejar may experience.

- Reduced net profit: an increase in financing costs would result in immediate profit suppression, as interest expense increases. (Several palm oil companies have experienced losses in similar circumstances.) This in turn negatively impacts return on assets and return on equity.

- Reduced Free Cash Flows: the present value of cash flows is a function of several factors, one of which cost of debt. This cost of debt is used in a discount factor to value any future cash flows in today’s terms. Higher cost of debt can therefore ultimately mean lower present value of the business.

- Reduced return on investment (NYSE:ROI) and difficult growth: any projects a grower decides to undertake are evaluated with the cost of capital the grower can secure. If this is driven higher because the cost of debt was increased, any investment would have lower ROI and may be abandoned. This can therefore hamper the growth of unsustainable soy producers.

- Lower share price: increased financing costs, volatile profits and reduced present value of free cash flows would reduce the intrinsic equity value of soy growers. This is what happened to southeast Asian palm oil producers Sawit Sumbermas Sarana and Provident Agro. It is a plausible scenario for BrasilAgro, too.

Risks for the Investors in Low-Scoring Soy Producers

To a very large extent, the risks to credit and equity investors in soy are contingent on the risks and opportunities that soy producers and traders face. Some examples include:

- Non-performing loans and reduced interest income: if cost of debt is increased, or barter-based financing is no longer available, commercial financial lenders may experience delays in collecting their debt. Such delays lead to underutilized bank funds and risk unearned revenues, which would translate to reduced interest income. Furthermore, it is possible that a bank is underpricing the loans it gives to unsustainable companies, due to not being fully aware of their risk exposure.

- Reduced access to funds and reduced solvency position: Each bank is not only an investor but also an investee, needing international finance to function. Banks in developing countries often seek funding from developed countries’ banks. The latter are more likely to have high sustainability policies and practices in place and can therefore disengage with a bank investing in controversial practices. This may drive up the cost of capital for conflicting banks. Although small, this could have negative impact on a bank’s solvency ratios. Compliance with regulatory requirements regarding solvency may also be at risk.

- High risk – Lost value for equity investors: the stock market reacts more and more to news related to sustainability, as it can substantially define reputation and brand value. (One example is a recent New Global Collaboration between Ceres and PRI to target beef, soy, timber and palm oil companies.) Poor sustainability is perceived as a signal of a potentially outdated and stagnating managerial position, or an inability to address risks. Equity investors could therefore expect share price volatility, and under-performance of low-scoring soy producers. This has been the case for palm oil companies and multiple other studies confirmed the trend (one is a German metastudy of 2250 academic studies that found positive correlation between sustainability and performance in 63 percent of the studies, negative in only 10 percent; another further example is here.).

Financial Benefits of Stronger ESG Performance

The first benefit of improved sustainability in soy production will be the avoidance of the negative financial consequences discussed above. Additional benefits can also include:

- Premium for certified products: while the share of soy that is certified under a recognized scheme for more responsible production is still low, this share may increase more quickly in the light of increased awareness of the environmental and social impacts of soy production. Certified products are sold at a premium.

- Subsidies or cost savings: with the increase of sustainability initiatives from various stakeholders (like the ‘Statement of Support For The Objectives Of TheCerrado Manifesto’ or the Chinese Sustainable Meat Declaration) it is very likely that more subsidies and other stimuli will be offered to produce zero-deforestation soy. At present, there are already initiatives offering services like knowhow and training regarding sustainable production, for free or a reduced fee (this includes the Round Table of Responsible Soy, RTRS).

- Brand value can be enhanced: research in the developing countries produced results showing that the millennial generation is seeking more sustainable products and is ready to choose its service providers based on their sustainability and climate awareness. This suggests that consumer goods companies could benefit by demanding more sustainable products. Other research has also shown that companies can enjoy a wider and more loyal customer base by developing a sustainable image. Retention of clients was also improved.

- Access to green finance: insurance of green bonds and access to cheaper green finance can be granted through the adoption of sustainable soy. This in turn can enable more externally-financed projects, greater transparency and engagement with socially responsible investors which have “high appetite for green bonds, as seen because of multiple over subscriptions.”

- Lower cost of debt and cost of equity: other commodities show that there is a positive correlation between levels of sustainability and better finance terms. It is likely that the soy market will develop in a similar way.

- Leadership position: access to green finance as well as a better reputation can establish the early adopters of sustainability as leaders in the market.

- Higher stock price returns: studies have shown that sustainability indices perform statistically better than conventional (Morningstar’s study showed that 16 out of 20 sustainable indices outperformed conventional). The difference of share price return is material. SLC Agricola as an example, might “increase the institutional investors’ confidence in its management and actually reduce the company’sequity price discount vs its NAV per share” by complying with zero deforestation.

Appendix: Sample selection producers

The selected producers are sufficiently diversified to represent the wide spectrum of large soy producers (of land ownership above 1,000 ha), holding a minimum of 23,000 ha, Brasilagro, and a maximum of 267,000 ha soy area, Grupo Bom Futuro, and thus form a small sample of relevant companies in which to draw some preliminary conclusions.

Together, the ten companies have an estimated 2.1 million ha of land under management and plant soy on an estimated surface of 1.1 million ha. As a large part of that is located in Cerrado states, these ten producers could amount to more than 1 percent of the Cerrado-based soy cultivation. This comparatively small share of the overall surface dedicated to soybean production illustrates the fragmented production base. Bom Futuro had to be excluded from further analysis as no financial relationships could be identified for this privately-owned company.

| Soy producera | Soy cultivation Statesb | Parent country | Land under management (1,000ha)c | Soy area Brazil (1,000ha)c |

| Grupo Bom Futuro | Mato Grosso | Brazil | >340 | 267 |

| SLC Agricola | Mato Grosso, Píaui, Bahia, | Brazil | 393 | 230 |

| Goiás; Maranhão, Mato | ||||

| Grosso do Sul | ||||

| Grupo André Maggi | Mato Grosso | Brazil | 252 | 164 |

| Grupo Bom Jesus | Mato Grosso, Bahia | Brazil | >200 | 122 |

| Terra Santa | Mato Grosso | Brazil | 158 | 104 |

| O Telhar | Mato Grosso | Brazil | 77 | 74 |

| Agrex do Brasil | Maranhão, Piauí, | Japan | 74 | 53 |

| (Mitsubishi) | Tocantins, Goiás. | |||

| Brookfield Brasil | São Paulo; Minas Gerais; | Canada | 240 | 49 |

| (Brookfield Asset | Mato Grosso; Mato | |||

| Management) | Grosso do Sul; Tocantins; | |||

| Goiás; Maranhão | ||||

| Agrícola Xingu | Minas Gerais, Bahia, | Japan | 116 | 35 |

| (Mitsui) | Maranhão, Mato Grosso | |||

| Brasilagro | Maranhão, Piauí, | Brazil | 226 | 23 |

| Tocantins, Goiás |

Figure 10: Large Brazilian soy producers with operations in Cerrado States. Source: company data.

a list does not represent a ranking, inclusion is partly based on data availability. Inclusion does not imply recent deforestation activities.

b The Cerrado States include notably Mato Grosso, Goiás, Maranhão, Tocantins, Piauí, and Bahia, as well as expanding into Mato Grosso do Sul, Minas Gerais, Rondônia, Paraná, São Paulo and the Federal District.

c Estimates (partly due to figures only available from previous years) in italics.

Selection of Investors Subset

The ESG policies of the key financiers of the soy producers have been evaluated in relation to the requirements on social and environmental performance that they impose on their investees. The top five investors by type of funding provided (loans, bonds, shares, underwriting) were chosen for analysis for the two groups of low- scoring and mid-scoring producers. Thus, the top 40 investors were selected.

However, the top five bondholders in the low-scoring producer group provided an insignificant amount of financing, and were therefore not analyzed in detail. This left the top 35 investors, among them 26 individual/unique investors. These have provided the majority of the financing, and for the lower scoring producers represent 73 percent of the funding, while for the medium-scoring producers, the selected top 20 financiers have provided approximately 60 percent of the total identified funding. As they are considerably exposed, these investors are likely in a position to pressure their investees.

Methodology Financing Analysis

An analysis was conducted of loans, equity and debt underwriting for the period from January 2012 to June 2017, as well as share and bond holdings at most recent filing dates. Data was gathered from Bloomberg, Thomson Reuters and company annual reports. No financial information could be identified for privately-owned Grupo Bom Futuro, the largest soybean producer in Brazil. Also for other privately-owned companies included in the analysis only very limited information on financial relationships could be identified. This means that the findings on financial relationships may be somewhat distorted towards the larger, publicly traded companies.

To make an accurate representation of the investments considered, several adjustments were made:

- Loans and underwriting services provided to the soy companies are often not reported on a per-bank or per-investor value, therefore, an adjuster was applied to estimate individual contributions. This estimation is based on the ratio of non- bookrunners to total bookrunners:In deals with a bookratio equal to more than 3, a formula is used which gradually lowers the commitment assigned to the bookrunners as the bookratio increases. The formula is:

These two formulas allow for a more accurate value attribution to each investor participating in the financing provided. - In order to account for the fact that some of the producers operate as subsidiaries of larger foreign corporates, namely Agrex do Brasil (part of Mitsubishi Corp (Japan), Agricola Xingu (part of Mitsui & Co, Japan) and Brookfield Brasil (part of Brookfield Asset Management, Canada), values for financial relationships have been adjusted according to the relative role of the Brazilian soy activities in the overall business activities of the companies. A soy segment adjuster was calculated as the fraction of the assets involved in the Brazilian soy production, or if such information was lacking, it was based on the fraction of revenue generated by soy. Estimates were made following a similar logic when specific data was not available.

A more detailed description of the methodology can be found here.

Top 20 Investors in the Mid-Scoring Producers

The financing presented consists of loans, bondholdings, shareholdings and underwriting services provided to the mid-scoring soy producers.

| Rank | Loans | Investor Parent Country | USD million | Policy score |

| 1 | Sumitomo Mitsui Financial Group | Japan | 376.2 | 36 |

| 2 | Mitsubishi UFJ Financial | Japan | 255.6 | 36 |

| 3 | Citigroup | United States | 102.5 | 47 |

| 4 | Mizuho Financial | Japan | 92.1 | 36 |

| 5 | Sumitomo Mitsui Trust | Japan | 77.0 | 39 |

| Avg | 39 |

Figure 11: Top creditors in mid-scoring soy producers, 2012-2017.

| Rank | Underwriting | Investor Parent Country | USD million | Sustainability score #

out of 100 |

| 1

2 3 4 5 |

Mitsubishi UFJ Financial

Mizuho Financial Sumitomo Mitsui Financial Group Citigroup Morgan Stanley |

Japan

Japan Japan United States United States |

45.9

14.4 7.8 7.3 7.1 |

36

36 36 47 39 |

| Avg | 39 |

Figure 12: Top underwriters in mid- scoring soy producers, 2012-2017.

| Rank | Shareholdings | Investor Parent Country | USD million | Sustainability score #

out of 100 |

| 1

2 3 4 5 |

SLC Participações

Mitsubishi UFJ Financial Odey Asset Management Mizuho Financial Vanguard |

Brazil

Japan United Kingdom Japan United States |

203.8

79.5 60.1 38.2 27.7 |

0

36 0 36 0 |

| Avg | 14 |

Figure 13: Top shareholders in mid- scoring soy producers, 2012-2017.

|

Figure 14: Top bondholders in mid- scoring soy producers, November 2017.

ESG policy scores of the top investors in the selected soy producers

The scoring of the sustainability policies of the top financiers of selected soy producers in Brazil is based on publicly available company documents. Information was accessed online in November/December 2017. Figure 15 below shows the scoring results. The assessment specifically focused on commitments and requirements for investees relating to the soy supply chain. No points were assigned

e.g. for commitments solely applying to the palm oil or forestry sector. Inadvertent omissions of statements or commitments cannot be fully precluded. Please contact us in case of comments or corrections.

Figure 15: ESG policy scores of soy financiers.

Figure 16 shows the detailed scoring criteria for the policy assessment of financial institutions (NYSE:FI). An overview of the criteria applied for the soy producers is available in the recent CRR report on ‘Deforestation in Brazilian Soy Supply Chain: Market Access Risk from a Growing Share of Sourcing Commitments’.

|

| Fundamental labor rights as stipulated by the ILO upheld by investee, including: freedom of association, the effective recognition of the right to collective bargaining, and freedom

from discrimination. |

No such policy | Yes, but very general/vague or with exceptions or applied to part of business activities | Explicitly described in the policy, or referring to adoption of related standards/initiatives applicable to all

business |

| Score – Human & Labor Rights | |||

| Governance & Disclosure | |||

| Investee must provide proof of legality in operations and sourcing.5 | Not explicitly described | Yes, but with exceptions or implicitly through certifications

requirements |

Explicitly described in policy |

| Investee must have a policy addressing

corruption. |

No such policy | Yes, but very

general/vague |

Explicitly described in

the policy |

| Compliance with ESG criteria must be demonstrated across all operations and relevant supply chains of investee through independent third-party auditing and compliance with credible

certification scheme standards.6 |

No such policy | Yes, but only part of activities | Explicitly have such policy |

| Investee must provide supply chain transparency up to farm level. | No such policy | Yes, but very general/vague or limited to only part of the

business |

Full transparency on supply chain |

| Sanction mechanism defined to apply in case of non-compliance, defining thresholds for suspension of relationship with supplier in case of breach. | No such policy | Yes, but very general/vague or limited to only part of the business | Sanction mechanism defined that applies in case of breaches of standards, leads to suspension in case of

non-compliance |

| FI publishes evidence of progress achieved against public commitments,

reported within established frequency. |

None | ad-hoc | Established frequency |

| Timebound plan for implementation of no deforestation & no exploitation? | No timebound plan | Timebound plan but only with partial

coverage |

Timebound plan for NDE7 |

Figure 16: Criteria analyzed in ESG policy analysis.

Footnotes:

- Relevant covenants include Equator Principles, Natural Capital Declaration, UNEP Finance Initiative, UN PRI, UN Guiding Principles for Business & Human Rights, OECD Guidelines for Multinational Enterprises, UN Global Compact, IFC Performance Standards, The 8 ILO Core Conventions, UN Declaration on the Rights of Indigenous Peoples (UNDRIP), UN Forest Principles, Soft Commodity Compact, New York Declaration on Forests. Specific for Brazil: Amazon Soy Moratorium, Pact for the Eradication of Slave Work in Brazil. (1 point for 2 or 3 adoptions; 2 points if at least 4).

- Natural habitats refer to natural forests, encompassing primary forests as well as naturally regenerated secondary forests (FAO), as well as other regions identified as valuable eco-regions due to high biodiversity and carbon storage.

- For more information on HCV and HCS forests, see: The High Conservation Value (HCV) Resource Network;The High Carbon Stock (HCS) Approach.

- No resettlement of people who are dependent for their livelihoods on land affected by the operations without their FPIC. Relevant guidelines include UN Declaration on the Rights of Indigenous Peoples (UNDRIP); Convention on Indigenous and Tribal Peoples (ILO-169).

- This may entail verifying legal title to the land and acquisition of all relevant permits and approvals, exclusion of Ibama-embargoed areas.

- Considered are RTRS and Proterra certification standards.

- No Deforestation, No Exploitation.