Grupo Palmas, including Palmas del Espino and subsidiaries, is specialized in the cultivation and processing of palm oil in the Peruvian Amazon. Grupo Palmas is 100 percent owned by the Peruvian conglomerate Grupo Romero. Grupo Palmas is Peru’s largest producer, refiner and exporter of palm oil.

After past controversies, Grupo Palmas is now shifting to a zero-deforestation approach. On April 4, 2017 Grupo Palmas published its No Deforestation, No Peat, No Exploitation (NDPE) policy that covers palm oil and cocoa. This creates new business opportunities, while also stranding its past expansion plans. These undeveloped concessions would be financially risky to develop.

Key Findings

- Grupo Palmas is working towards a zero-deforestation supply chain. RSPO certification processes are underway, and it recently joined The Forest Trust. Grupo Palmas published its NDPE policy April 4, 2017. It also says it is pursuing growth strategies based on smallholder engagement.

- The adoption of a NDPE policy gives Grupo Palmas a competitive advantage over its main competitors by becoming the market leader for zero-deforestation in Peru. Benefits include maintaining and expanding an international customer base, strengthening relationships with smallholders and improving brand reputation.

- Given Grupo Palmas’ published NDPE policy and current market conditions, four planned projects with a total landbank of 25,000 ha are no longer feasible for development of large-scale palm oil plantations. This land can be considered stranded, and the company needs to pursue alternative ways to create value that does not require any land clearing.

- If, at any point in the future, Grupo Palmas does proceed with the development of any of the four planned projects, it could expose itself to a number of business risks. This could result in loss of clients, significant reputational damage and exposure to regulatory measures. The first can reduce margins, and the second can increase debt costs, and both can lead to a solvency and liquidity crisis in the company as debt and debt service are both high.

- Grupo Palmas has a Net Debt to EBITDA ratio of 7x, and so the company needs to generate cash flow and growth to meet their financial requirements. To generate the sufficient cash flow Palmas should work in keeping their client base, both in Peru and internationally, and if possible work to expand it. The growth should be achieved while taking sustainability policies into account. Expanding the agriculture frontier, without taking deforestation into account can create reputational risks and loss of clients, amplifying Grupo Palmas financial problems.

Grupo Palmas: Business Lines and Segments

Grupo Palmas has two business segments.

- The Plantations segment includes the palm oil and cocoa plantations. In FY2015, the group had 23,346 ha of planted area with 21,420 ha of oil palm and 1,926 ha of cocoa.

- The Industrial segment includes palm oil mills and refineries, a chocolate frosting factory, production and marketing of cooking oils, margarine and other products. All output of the Plantations segment is processed in the Industrial segment mills and refineries. In addition, input is purchased from smallholders. Smallholders represent 10 percent of the total supply of Fresh Fruit Bunches (FFB) to mills and refineries.

In FY2015, Grupo Palmas’ total revenues were USD 136 million (PEN 462 million). Its operating income margin was 12 percent. Grupo Palmas reported a net loss of USD 24 million (PEN 82 million) based on operating income of USD 16 million (PEN 56 million). Its USD 14 million (PEN 48 million) currency exposure loss and its 40 percent increase in financial costs from debt servicing drove this loss.

65 percent of Grupo Palmas’ sales are of consumer goods. 20 percent of sale are from CPO sales. 15 percent of sales are from industrial goods’ sales. Grupo Palmas accounts for almost all Peruvian palm oil exports. Its three cooking oil brands – Tondero, Soi and Pamerola – have a combined 12 percent domestic market share. Its two margarines brands – Tropical and Manpan – have a combined 24 percent domestic market share. Grupo Palmas sells Popeye laundry soap and Spa personal care soap. They have a 14 percent and 6 percent domestic market share respectively.

Consumer goods company Alicorp is the Peruvian market leader in all these segments. They control 51 percent of the cooking oils market, 66 percent of the margarine market and 82 percent of the laundry soap market. Grupo Romero also owns 46 percent of Alicorp. This makes Alicorp both a competitor and affiliate of Grupo Palmas.

Grupo Palmas: Structure and Governance

Family-owned Grupo Romero owns 100 percent of Grupo Palmas. In 1979, Grupo Palmas established Palmas del Espino in Uchiza, San Martín, as a cocoa and palm oil plantation company. In 1992, Grupo Palmas established Industrias del Espino to extract and process CPO.

In 2006, Palmas del Espino invested USD 39.8 million to establish the Shanusi project to increase oil palm cultivation in San Martin and Loreto. Palmas del Espino also invested USD 11.5 million in a palm oil biodiesel refinery. In 2012, Grupo Palmas invested USD 18 million in the first stage of developing the Industrias del Shanusi palm oil extraction plant. In 2015, they financed the construction of both a special oils refinery and a biogas electricity generation plant. The financiers of these projects are unknown.

In 2014, new senior management entered Grupo Palmas. This resulted in a new sustainability value proposition within the company. Grupo Palmas’s April 4, 2017 NDPE policy is a culmination of these efforts.Some of its subsidiaries are also obtaining RSPO certification, while the company also recently joined The Forest Trust.

Grupo Palmas has interlocking executives with Alicorp, the consumer goods company that is both an affiliate and a direct competitor for B2B customers:

- Dionisio Romero is the Chairman on the Board of Directors of Grupo Palmas and Alicorp.

- José Antonio Onrubia is on the Board of Directors of Grupo Palmas and Alicorp.

- Calixto Romero is on the Board of Directors of Grupo Palmas and Alicorp.

- Javier Onrubia was a director at Alicorp until 2001, when he became a Palmas del Espino director.

- Ángel Irazola Arribas is on the Board of Directors of Grupo Plamas and Grupo Chira. Grupo Chira is a former subsidiary of Grupo Palmas that is still 100 percent owned by Grupo Romero.

Grupo Palmas: Deforestation Risks and NDPE Opportunities

Past Deforestation Allegations

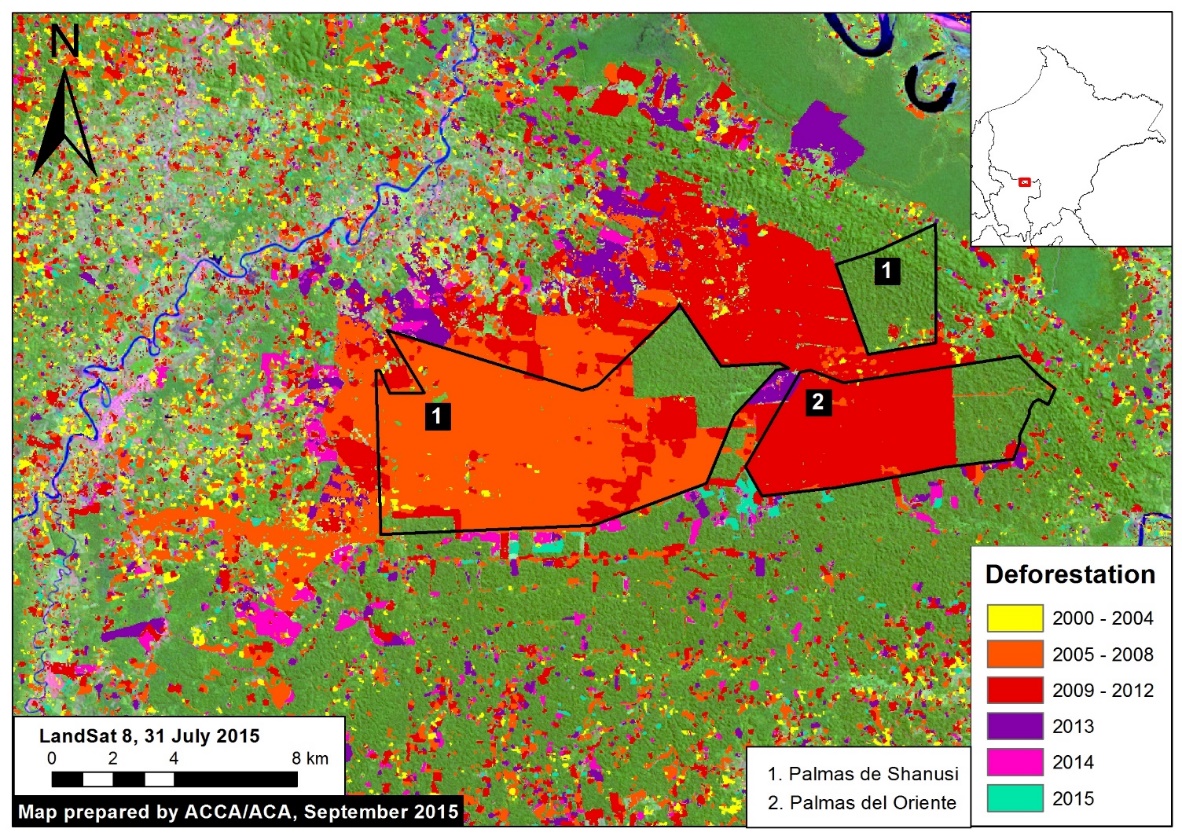

In 2015, the Environmental Investigation Agency (EIA) documented how Grupo Palmas’ palm oil expansion threatened the Peruvian Amazon. EIA showed that Grupo Palmas’ two existing plantations Palmas del Shanusi and Palmas del Oriente caused deforestation and created land disputes.

Figure 1: Deforestation at and around Palmas del Shanusi and Palmas del Oriente. Source: Finer & Novoa (2015).

As shown above in Figure 2, the Monitoring of the Andean Amazon Project (MAAP) reported that between 2006 and 2011, 16,800 ha of primary forest was cleared in and around Palmas del Shanusi and Palmas del Oriente. Local communities, civil society and various government agencies contested these deforestation activities. Both Grupo Palmas’ projects faced community protests, regional strikes and legal cases. Grupo Palmas faced court cases focused on illegal land clearings, trespassing, destruction of property and irregular land acquisition.

In 2015, Grupo Palmas was criticized for its plans to develop four new palm oil projects in Loreto. These four potential projects are shown in Figure 2 below.

| Project | Location | Land for palm oil (HA) | Reserve Land |

| Tierra Blanca | Sarayacu District | 7,002 | 2,996 |

| Santa Catalina | Sarayacu District | 7,003 | 3,001 |

| Manití | Indiana District | 6,440 | 1,631 |

| Santa Cecilia | Indiana District | 4,610 | 1,612 |

| Total | 25,055 | 9,240 |

Figure 2: Potential Grupo Palmas projects. Source: EIA 2015.

These projects could result in material deforestation supply chain risks. According to EIA, 92 percent of this land consists of primary forest. Full development of these projects into palm oil concessions would result in more than 25,000 ha being deforested. EIA reported that Manití’s and Santa Cecilia’s Environmental Impact Assessments included discrepancies regarding their legally required 30 percent forest reserve. AutoCAD data showed that the legally required 30 percent was not adhered to. Grupo Palmas denies any violations.

Stranded Land Risks

Grupo Palmas’ four planned projects may no longer be feasible for palm oil plantation development, as a result of the company’s recent NDPE policy. As such, this land may be stranded land. Stranded land is a stranded asset. Stranded assets are assets that have suffered from unanticipated or premature write-downs, devaluations, or conversion to liabilities before the end of their useful economic life.

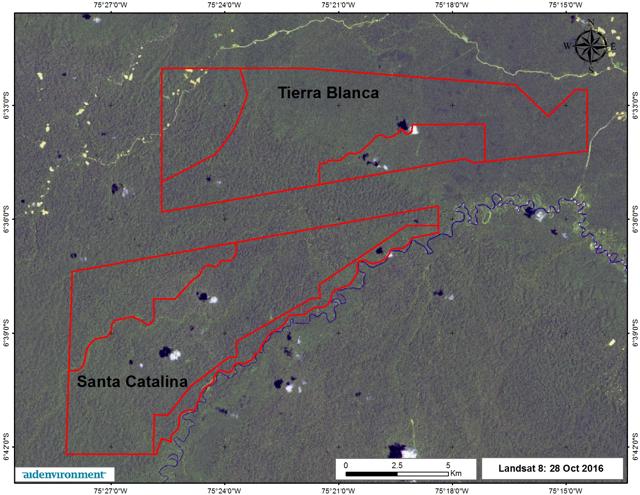

As shown below in Figures 3 and 4, since July 2015, satellite footage confirms that no development has occurred in the four projects. The only exception is minor deforestation of 28 ha at the Tierra Blanca concession.

Figure 3: Satellite images of the proposed Tierra Blanca and Santa Catalina project. Source: Aidenvironment, EIA.

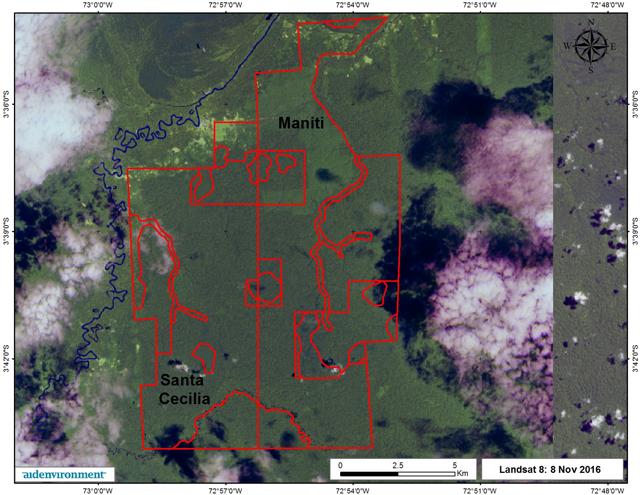

Figure 4: Satellite images of the proposed Santa Cecilia and Maniti projects. Source: Aidenvironment, EIA.

It is unlikely that these projects will be politically, socially or economically viable in the future. The global palm oil market is moving towards NDPE as a market access requirement. At the same time, the Peruvian government is prioritizing stopping deforestation. Deforesting these properties may also violate Grupo Palmas’ pending NDPE policy. This would result in reputational risks.

Stranded land may have different effects at Manití and Santa Cecilia compared to Tierra Blanca and Santa Catalina. This is because Grupo Palmas has obtained all licenses for Manití and Santa Cecilia, but not for Tiera Blanca and Santa Catalina.

- Manití and Santa Cecilia: Grupo Palmas needs to create value from its licenses without deforesting the properties. Grupo Palmas stated it is in a multi-stakeholder process to develop alternatives to deforestation for these properties.

- Tierra Blanca and Santa Catalina: Because Grupo Palmas does not have the required licenses to deforest these properties, they have not yet developed alternative land use plans. These projects are currently in the assessment phase. Grupo Palmas said they might not further develop the projects.

With these four projects, Grupo Palmas stranded land risk is 25,000 ha. This equals 107 percent of their currently planted area. This illustrates the material risk from stranded land facing Grupo Palmas. For 11,050 ha (Maniti and Santa Cecilia), the company might be able to find alternative value in forest conservation and sustainable land use.

Stranded land risk increases operational and financial risks. Examples include land purchases, costs incurred for obtaining permits, and for conducting environmental impact assessments and other evaluations. There are also possible costs for the preparation of related infrastructure, such as the planned road from Santa Catalina to Pongo Isla. Stranded land can also increase Grupo Palmas’ future net income variability.

Stranded land risk may furthermore decrease Grupo Palmas’ mills utilization rates. The two suspended projects – Santa Catalina and Tierra Blanca – are located 100 km from the Planta de Shanusi mill. The suspended projects would have supplied 45MT/hour to the mill. Grupo Palmas’ mills combined utilization rate is 60 percent. This means that the lack of FFB from these projects might decrease overall mill utilization rates. This might be partially offset by an increase of sourcing from smallholder farmers.

NDPE Business Opportunities

Grupo Palmas is working towards a NDPE supply chain with the publication of its April 2017 NDPE policy. The company is an ordinary member of the RSPO. Its Industrias del Espino and Palmas del Espino operations are in the process of becoming RSPO certified. The policy includes High Carbon Stock (HCS) and High Conservation Value (HCV) measures. The policy also includes a no exploitation clause, a commitment to ‘good agricultural practices’ and transparency measures.

Grupo Palmas has indicated that its growth strategy is based on intensifying relations with smallholder farmers. The company aims to increase smallholder productivity and identify suitable non-forested land where smallholders can expand. According to its general manager, Grupo Palmas wants to become Peru’s preferred supplier to companies with zero-deforestation and NDPE policies. They intend to do so through a smallholder deforestation-free supply chain model.

For Grupo Palmas, the benefits of a public and fully implemented NDPE policy include:

- Maintaining market access to international clients and investors with NDPE policies.

- Increasing potential customer base.

- Strengthening relationships with smallholders and suppliers.

- Improving brand reputation.

Grupo Palmas is the first Peruvian company with a NDPE policy. Grupo Palmas has a first-mover advantage over its competitors by becoming the Peruvian NDPE market leader. Grupo Palmas can build on this first-mover advantage by executing a smallholder strategy combined with an immediate moratorium on any further clearing. Grupo Palmas’ market leadership gives it the advantage that it can refrain from developing its plantations in Manití and Santa Catalina. Instead, Grupo Palmas can grow through the expansion of its smallholder base. Simultaneously, it can market its products to its domestic and international markets as deforestation-free.

Grupo Palmas is now aligned with other Peruvian deforestation-free agriculture initiatives. The Peruvian government officially committed to net zero deforestation by 2021. Peru’s National Forestry and Climate Change Strategy (ENBCC) is the primary framework for this target. ENBCC proposes an integrated landscape approach to forest conservation and restoration. Peru is pursuing investment in smallholder agriculture, monitoring and formalizing forests and strengthening conservation efforts. Peru wants to do this by improving production on existing and degraded land.

The“ National Plan for Sustainable Development of Palm Oil 2016 – 2021” ( PNDS 2016), a joint initiative by the government, palm oil associations and civil society. It comprises of legislative proposals, potential public-private partnerships, mechanisms to increase yields and financial mechanisms. This initiative seeks to ensure sustainable supply matches demand by 2025. To match demand, either cultivation areas must be expanded or productivity must be improved. PNDS has identified suitable non-forested or degraded areas for palm oil cultivation. Stakeholders in this initiative are developing deforestation-free business models. Key models center on improving local outgrower and smallholder association models.

Grupo Romero’s centralized corporate structure provides opportunities for firm-wide adoption and implementation of NDPE policies. Grupo Palmas’ lessons learned can inform other Grupo Romero companies’ future NDPE policies. None of the Grupo Romero firms today have a public NDPE policy. Grupo Romero’s affiliated firms including Alicorp and Credicorp might also be exposed to material deforestation risks. If all of Grupo Romero’s affiliated companies had NDPE policies, they could benefit from the previously described competitive advantages.

Future Deforestation Increases Grupo Palmas’ Business Risks

But if Grupo Palmas proceeds with the development of its four planned projects, it is exposed to material business risks. These risks include a loss of market access, reputation and regulatory risks.

Grupo Palmas palm oil production

| 2013 | 2014 | 2015 | |

| Planted area | 18,541 | 21,004 | 21,420 |

| FFB/ha (T) | 19.02 | 19.19 | 20.93 |

| CPO/ha | 4.7 | 4.89 | 7.51 |

Any further deforestation jeopardizes Grupo Palmas’ expansion to international markets. 15 percent of its total sales in 2014 were to international markets. Further expansion to international markets would require compliance with NDPE policies. In 2015, 61 percent of companies active in the palm oil value chain has made a public commitment to zero deforestation. Although these commitments differ in their details, key actors in the palm oil value chain all made such commitments. Sustainability policies are becoming broader, and recently are also including social impacts on palm oil plantations, such as child labor, community conflicts, and occupational health and safety. SE Asian examples like IOI Corporation show that companies involved in deforestation can quickly lose their corporate customer base and face immediate financial consequences.

In the Peruvian domestic market, deforestation concerns appear to be less of a factor to date. However, growing international and domestic efforts to halt climate change, and the increasing recognition of zero-deforestation as a means to that end, might bring additional revenue risks.

Continuing deforestation would contradict Grupo Palmas deforestation commitments, thereby creating material reputational risk. The availability of high quality and near real-time satellite images allows analysts to expose deforestation, including in remote areas. Companies therefore face increasing risks exposure with consequent damage to reputation.

Grupo Palmas capacity utilization in 2015

| Business | Capacity | Usage |

| Palm oil | 1,440 T FFB/Day | 60.5% |

| Refinery | 450 T CPO/Day | 60.4% |

| Fractionation | 280 T/ Day | 74.1% |

| Butter | 110 T/Day | 82.1% |

| Oils | 180 T/ Day | 82.4% |

| Soap | 44 T/ Day | 60.4% |

| Biodiesel | 150 T/ Day | 0.1% |

Where the legality of land clearing and deforestation is challenged, Grupo Palmas could face regulatory risks in the form of fines and stop-work orders. The Peruvian government has been strengthening environmental regulations. Illegal land clearing and deforestation in Peru are punishable with fines, stop-work orders and revoking of licenses. The Constitutional Tribunal is the highest legal authority in Peru. It has set precedents to the importance of preserving natural resources. While enforcement of deforestation legislation remains an issue, legal cases have been filed. Palmas del Shanusi is currently facing three legal cases concerning its deforestation activities.

Grupo Palmas: Financial Analysis

Grupo Palmas’ weak financials are a concern. Its high Net Debt to EBITDA of 7.3x gives the company little room to fund new initiatives. Grupo Palmas’ focus should be on generating cash to pay their creditors. This will assist them in reducing their interest expenses.

Its FY2015 revenues were USD 136 million (PEN 462 million). This was a 9.4 percent increase year-over-year. The increase was largely due to greater volume in the agricultural and industrial production segments. This offset the fall in the price of goods sold. The increase in sales was accompanied by a 22 percent increase in expenses. This negatively affected their gross margin.

In 2015, the company experienced an increase in sales of raw materials, oils and special butter. Those gains were partially offset by the reduction in sales of regular butter, processed products and biodiesel. Biodiesel was discontinued due to dumping from Argentina. In January 2016, the I NDECOPI Dumping and Subsidies Commission established countervailing duties. In the future, the company might restart its biodiesel production.

List of banks that in March 2016 loaned PEN 529 million to Grupo Palmas in a syndicated loan

- Banco de Crédito del Perú

- Banco Internacional del Perú – Interbank

- Bancolombia Puertorico Internacional

- Scotiabank Perú

The decrease in price of goods sold occurred because palm oil prices declined in 2015. This was due to the increased supply of palm oil from SE Asia and substitute oils. In 2016, El Niño effects reduced SE Asian palm oil production and prices rose. In H12017, palm oil are expected to remain high. This is despite the La Niña effect. Domestically, prices have been impacted by the strengthening of the PEN against the USD.

In 2015, operating income decreased 50 percent. This is explained by the lower fair value of biological assets. These assets value decreased due to lower FFB prices and higher discount rates. In 2014, its adjusted EBITDA (not adjusted for the change in fair value of biological asset) was USD 48 million (PEN 145 million). In 2015, its adjusted EBITDA was USD 24 million (PEN 91.8 million). This created an adjusted EBITDA margin of 20 percent.

This generated debt service coverage of 0.84 times EBITDA. This result also was negatively impacted by higher financial expenses of USD 12 million (PEN 41 million). This is due to an increase of debt in 2015. Debt grew as a result of the spin-off of the Agrícola del Chira assets. Debt also grew from an increase in working capital requirements. Finally, debt increased due to a synthetic hedge that involved borrowing in PEN with the proceeds invested in USD.

The company had a USD 11 million (PEN 39 million) loss due to its discontinued operations and spin-off of assets of Agrícola del Chira. It had a net loss of USD 14 million (PEN 48 million) from exchange rates mainly due to its foreign currency liabilities. In Q1 2016, Grupo Palmas increased its debt USD 100 million. As shown below in Figure 5, the company had an overall net loss of USD 24 million (PEN 83 million).

Palmas del Espino debt metrics compared to a peer group of Latin American agribusiness companies

| Metrics | Peer Group | Grupo Palmas |

| Total Debt / EBITDA | 4.7 | 8.4 |

| EBITDA / Tot Interest Expense | 11 | 2.1 |

| Net Debt / EBITDA | 3.3 | 7.3 |

Figure 5: Cash flow indicators. Source: Equilibrium.

| Indicator (PEN million) | 2012 | 2013 | 2014 | 2015 |

| Revenue | 388 | 399 | 422 | 461 |

| Cost of Goods Sold | 195 | 199 | 220 | 269 |

| Profit Margin | 50% | 50% | 48% | 42% |

| EBITDA | 144 | 122 | 110 | 87 |

| EBIT | 93 | 90 | 76 | 51 |

| Net Income | 184 | 195 | 4 | -83 |

| Net Debt/EBITDA | 1.46 | 3.52 | 4.28 | 7.27 |

In FY2015, its assets were USD 491 million (PEN 1,670 million). This reflected a decrease of 32.1 percent compared to year-over-year. This is from the spin-off of assets of Agrícola del Chira. The current assets to total assets ratio rose from 4.8 percent to 11.7 percent. This is due to the decision to accumulate assets in USD to offsets its USD liabilities. This reduced their USD net liability position.

FY2015 current liabilities increased by USD 73 million (PEN 249 million) to USD 38 million (PEN 129 million) due to an increase short-term bank loans. Grupo Palmas’ current liquidity ratio has declined from 1.5x to 0.6x in 2015.

Grupo Palmas finances its assets with 50.1 percent equity and 49.9 percent debt. Its liabilities have increased due to the spin-off of its Agrícola del Chira assets. Liabilities also increased as working capital expanded as the company has grown. The debt increase was also influenced by synthetic hedging used to mitigate exchange losses. Its net debt to EBITDA increased from 3.4x in 2014 to 8x. in 2015, which is a worryingly high number.

Credit Analysis

The Peruvian credit agency Equilibrium current AA.pe rating reflects Grupo Palmas’ current financial condition, its future, and expansion into Peru’s agricultural frontier. Equilibrium also considered Grupo Romero ownership of Palmas del Espino in its analysis.

Grupo Palmas needs to work on improving the debt service coverage. The debt in local currency for hedging reasons can be positive for the company, however this requires close monitoring. Grupo Romero Net Debt/ EBITDA should be monitored closely, as this indicator is associated with the company’s ability to reduce its debt. To generate the sufficient cash flow Palmas should work in keeping their client base, both in Peru and internationally, and if possible work to expend their buyers.

How Grupo Palmas chooses to address the stranded land risk will be crucial for the company investors. The stranded land can reduce the asset value and deteriorate the total debt to assets ratio. This could also work to increase the cost of capital and the cost of debt, what can deteriorate the EBITDA/total interest expense ratio even further.

For the company generating growth is key. However, expanding the agriculture frontier, without taking deforestation into account can create, reputational risks and loss of clients. The first can increase debt costs, the second can reduce margins and both can lead to a solvency and liquidity crisis in the company as debt and debt service are both high. All additional land development needs to be in line with the RSPO regulation, and with the sustainability policies of Grupo Palmas buyers and lenders.

Strengths

- Vertical integration in the palm oil supply chain.

- Diversification of products and leadership position in Peru

- Financial support from Grupo Romero.

- Agricultural business knowledge.

- Willingness to adopt global sustainability palm oil policies.

Weaknesses

- Weak balance sheet ratios and a high net debt / EBITDA.

- Three litigation cases could increase Grupo Palmas’ liabilities and decrease their credit rating.

- Cost of transportation because refineries are located in challenging locations.

- High turnover and personnel shortage in agricultural activities

- General Agricultural development risks (e.g. commodity price volatility and climate circumstances).

- Operational risks from deforestation by Grupo Palmas and its suppliers could increase cost of capital. Risks caused by the company’s third party suppliers or by themselves can increase cost of capital.

Opportunities

- Becoming the market leader in zero-deforestation palm oil in Peru.

- Issuing a NDPE policy to gain accesses to international markets and investors with NDPE policies.

- Opening of new domestic and foreign markets to zero-deforestation products.

- Expanding development of oil palm plantations in Peru.

- Peru imports oils and fats.

Threats

- Loss of clients due to unmatched NDPE policies.

- Potential write-down of stranded land can reduce equity.

- World economy deceleration dampens palm oil prices.

- Changes in tax laws, land rights regulations and forests protection could slow expansion plans.

- Competition of substitute oils based on soy, sunflower and cotton.

- Competition of imported biodiesel with subsidized prices.

- Deforestation and other practices can increase the company’s litigation expenses and government fines.