Summary

- Operational Risks: Hazards to investments can threaten the economic viability of projects when key risk management lessons are not applied in frontier markets.

- Stranded Assets Risk: Contested land bank reduces future growth and impacts investor value.

- Financial Risks: Failure to obtain free, prior, and informed consent (FPIC) from local communities can result in cash flow disruption.

- Reputational Risk: Violations of procurement policies and ESG criteria imposed by investors, buyers, and certification standards can damage companies’ reputation.

- Regulatory and Procurement Risks: Companies relying on land conversion for large-scale plantations may no longer be compliant with corporate buyers’ procurement policies.

SE Asian corporations – Golden Agri-Resources, Kuala Lumpur Kepong, Sime Darby, Olam International, Wilmar International, and Felda Global Ventures – are seeking to expand their palm oil business in West and Central Africa. Palm oil has been identified as a driver of both tropical deforestation and climate change, and this expansion also often has financial risks due to concerns about negligence of communities’ rights and environmental impacts. At the same time, countries supporting palm oil expansion are often post-conflict, fragile states seeking development and investments, dealing with weak governance and legal systems and lack instruments to stimulate and regulate responsible management practices.

Investments in Africa since 2008 illustrate both systemic and company-specific material financial risks. For example, the experiences of investors and corporations expanding into Liberia illustrate that it is important to absorb lessons from previous SE Asian investments regarding specific social and environmental risks and opportunities.

Companies analyzed:

- Felda Global Ventures (FGV:MK)Sime Darby (SIME:MK)

- Golden Agri-Resources

- Kuala Lumpur Kepong (KLK:MK)

- Wilmar International

- Olam International

- Golden Veroleum

- Equatorial Palm Oil

Key Findings

- Operational Risks:Hazards to investments can threaten the economic viability of projects when key risk management lessons are not applied in frontier markets. For example, relying on government assurances has proven to be insufficient in securing title when land banks are contested.

- Stranded Assets Risk:Contested land bank reduces future growth and impacts investor value. Key drivers are difficulty in forecasting public policies, governance risk, land-tenure disputes resulting from unclear customary and legal ownership, and international deforestation policy commitments and regulatory changes to halt climate change.

- Financial Risks:Failure to obtain free, prior, and informed consent (FPIC) from local communities can result in cash flow disruption. For example, every SE Asian investment in Liberia has been subject to delays, community conflicts, and complaints filed with the Roundtable on Sustainable Palm Oil (RSPO).

- Reputational Risk:Violations of procurement policies and ESG criteria imposed by investors, buyers, and certification standards can damage companies’ reputation. This increases revenue-at-risk and earnings volatility, and may increase the cost of capital as lenders price risks more accurately. For example, civil society has had success in monitoring current and proposed corporate actions in Liberia.

- Regulatory and Procurement Risks:Companies relying on land conversion for large-scale plantations may no longer be compliant with corporate buyers’ procurement policies regarding environmental and social risks, and international deforestation policy commitments.

- Palm Oil in Africa Can Succeed:Effective financial risk management aligned with investors’ expectations and local communities’ requirements and avoiding deforestation and biodiversity impacts can drive long-term financial returns. Large-scale concession models may become obsolete. Schemes that integrate smallholders and respect customary land rights are a precondition to create mutual benefits for both sides and value creation.

SE Asia Palm Oil Social and Environmental Impacts: Lessons Learned

- Indonesia is one of the world’s leading emitters of greenhouse gases. Deforestation causes 85 percent of Indonesia’s emissions.

From Africa to the World: Originating from Africa, the oil palm was harvested by subsistence smallholders in West and Central Africa from wild or semi-wild trees for centuries. After full domestication was achieved in the early 1900s, large plantation companies introduced new varieties to colonial Central Africa, first to Cameroon and today’s Democratic Republic of Congo (DRC). In the post-colonial years, as mineral mining and petroleum exploitation generated greater government revenue, interest in palm oil waned.

SE Asia Leads: In the 1960s, Malaysia pioneered large-scale industrial cultivation of oil palm trees. With a comparative advantage from low production costs, high productivity, and palm oil’s versatility of use in food and non-food, global demand caused production to quickly expand to Indonesia. The two countries today are responsible for 85 percent of global palm oil production. Currently, a large share of SE Asian palm oil production is in the hands of private enterprises. A comparatively small share of production is managed by smallholder farmers.

Deforestation and Greenhouse Gas Emissions: Emissions from tropical deforestation and forest degradation are responsible for 7 percent to 14 percent of the total global greenhouse gas emissions from human activities. Indonesia’s plantations have been predominantly established in carbon-rich tropical forests and peatlands, where clearing and draining for palm oil cultivation, often with the illegal but widely practiced slash-and-burn method, releases significant greenhouse gas emissions. Tropical peatlands can burn for many months, which has led to severe regional haze problems. It has been connected to thousands of deaths in SE Asia in recent years.

Indonesia is one of the world’s largest producers of greenhouse gases. 85 percent of the country’s emissions come from forest destruction and degradation. During 2015, Indonesia’s average emissions repeatedly exceeded those of China and the U.S. Indonesia’s primary forest loss totaled more than 6 million ha from 2000-12. In 2012, Indonesia lost 840,000 ha of primary forest, the largest loss globally for any country.

Human Rights Violations: The rapid expansion of palm oil production in SE Asia has also been connected to serious human rights violations, including child and forced labor. Migrant workers, whom are often discriminated against and exploited, are widely involved in palm oil production. Jobs available on palm oil plantations are often casual and seasonal. When compared to smallholder cocoa, rubber, rice and agroforestry, industrial palm oil creates fewer jobs per ha. Smallholders owning and managing their own estates tend to have higher earnings than laborers on corporate palm oil estates.

Value Appropriation vs. Value Creation: The full potential benefits from palm oil production for the economy and livelihoods of people in SE Asia have not been realized. This is due to the lack of a strong regulatory framework and policies that often favor extraction and value appropriation over investment and value creation. At the same time, smallholder cultivation – which currently accounts for one-third of production in SE Asia – has long been prevented from further expansion by disregard of land rights and lack of access to quality inputs and affordable finance.

Persistent Production Rise Despite Volatile Crude Palm Oil Prices

- Global palm oil production is expected to increase 29% from 2016 to 2025.

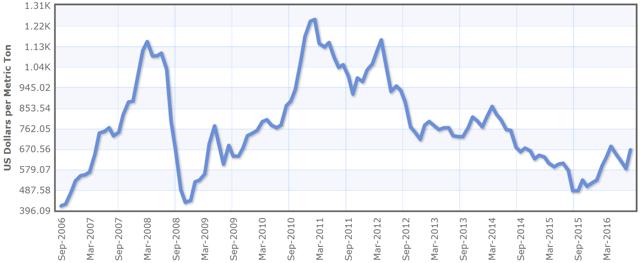

Volatile Markets: As shown below in Figure 1, after a sharp decline during the 2007-09 global credit crises, palm oil prices tripled and then collapsed. Since 2011, crude palm oil (CPO) prices declined about 50 percent caused in part by shifting buyer preference and a decrease in demand for biofuels caused by low petroleum prices.

Continuing Demand for Food and Fuel: In the 2015/16 agriculture season, palm oil and palm kernel oil accounted for 37 percent of world vegetable oil supply, followed by soybean oil at 29 percent and rapeseed oil at 16 percent. Rising global food demand – currently accounting for an estimated 68 percent of global palm oil production – and the expectation of biofuel demand picking up are likely to expand palm oil production in the foreseeable future.

From 2016-25, palm oil production is forecasted to increase 29 percent. Indonesian output is forecast to grow by an additional 2.5 percent annually over the same period. This is lower than Indonesia’ 8.1 percent annual growth over the previous decade. Malaysian growth is forecast to grow over the same period by 2.1 percent annually compared with 2.4 percent annually over the previous decade.

Figure 1: Palm oil monthly price – $ per metric ton (08/06 to 08/16) Source: Index Mundi

Palm oil biofuels demand in Europe is forecast to decrease over the mid-term, while SE Asian demand is forecast to expand due to domestic SE Asianmandates. Faced with falling global prices, SE Asian governments have recently boosted domestic demand for palm oil by increasing biofuels mandates. Indonesia’s 2016 biofuels mandate requires a 20 percent blending of palm oil biodiesel into petroleum for vehicle use. Under regulations released in 2015, the country’s electric power industry is also mandated to use B30 biodiesel blend (which includes 30 percent palm oil-based biofuels) starting in 2016. Malaysia is currently expected to increase its biofuels mandate from 7 percent to 10 percent in Q4 2016.

Distribution of global palm oil production in 2015

- SE Asia: 89%, of which 53% Indonesia and 32% Malaysia.

- Latin America: 6%, largest production in Colombia, Ecuador, and Honduras.

- Africa: 4%, largest production in Nigeria, Ghana, and Côte d’Ivoire.

SE Asian Corporations Need New Frontiers

Little Arable Land Remains in Indonesia and Malaysia: In the established palm oil production centers of SE Asia, little arable land remains. In addition, companies have recently been faced with improved environmental and land acquisition regulations as a consequence of increasing awareness of the negative effects caused by palm oil expansion. Since 2011, Indonesia has had a primary forest deforestation moratorium in place resulting in a temporary halt to the granting of new permits to clear forests and peatlands. However, many companies still have large land banks that are partially planted, enabling expansion despite the moratorium. There have been repeated reports of moratorium breaches. Nonetheless, the moratorium has succeeded in limiting the scale of expansion of Indonesia’s palm oil plantations.

These developments have triggered leading SE Asian corporations to search for new frontiers. Apart from consideration of agricultural growing conditions, the choice of regions for expansion is driven by a range of variables. These include supportive government policies, available cheap labor, affordable and available land concessions, and available finance. Issues related to direct state land ownership and perceived weak environmental and social oversight are also contributing factors.

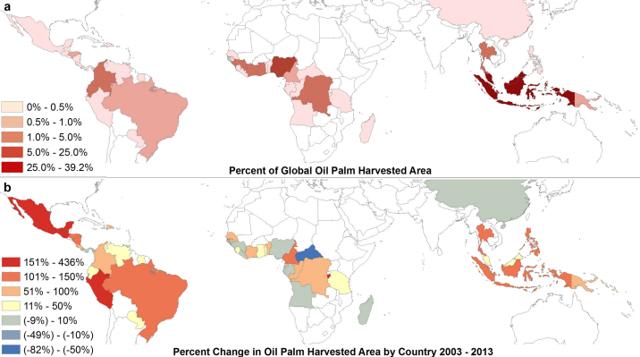

Figure 2: New Frontiers of palm oil expansion, 2003-13. Source: Vijay, V., Pimm, S.L., Jenkins, C.N. and S.J. Smith (2016, July 27), “The impacts of oil palm on recent deforestation and biodiversity loss”, PLoS ONE, 11 (7): e0159668.

Agriculture Frontiers in Africa and Latin America: As shown above in Figure 2, the new frontiers for palm oil expansion are located in West and Central Africa and in Central and South America. While land cultivated and tons produced are still significantly smaller than in SE Asia, relative expansion rates in these regions from 2003-13 show a different picture. High growth rates are observed in Cameroon, the DRC, Republic of the Congo, Benin, Côte d’Ivoire, and Senegal in Africa; and in Peru, Mexico, Guatemala, Brazil, and Colombia in South America. It is important to note that large areas of land that have already been granted as large-scale concessions especially in Africa are not planted yet, and thus not included in Figure 2.

Several of these West and Central African countries are considered to be‘ fragile states’. This includes both the DRC, a country that has been struggling with extreme poverty and ongoing civil unrest for many years; and Liberia, which emerged from a civil war in 2003 and then was hit by the Ebola crisis in 2014.

- A large share of the currently designated land for palm oil concessions is covered with ‘vulnerable forests’ in danger of deforestation.

West and Central Africa: Regionally, palm oil has long been produced as a subsistence crop in mixed systems on small-scale farms. Millions of small farmers, many of them women, depend on palm oil for both their food and livelihoods. Depending on the country, smallholders account for up to 90 percent of current regional palm oil production. They mostly cultivate the Duravariety, which has a lower oil content and thus oil extraction rate and productivity, but is nutritionally preferable to the higher yielding Teneravariety preferred by industry. While smallholders still dominate production in Africa, a new wave of international palm oil cultivators has arrived in recent years – among them large-scale producers and traders from SE Asia.

These countries boast attractive features: large areas of uncultivated arable land, favorable soil and climatic conditions, the proximity of key markets in Europe and Africa, governments providing easy access to land, low cost of concessions, weak governance and poor environmental and social oversight due to a recent history of political unrest and violent conflict. At the same time, rising incomes are expected to sustain growing demand for food products in the coming years.

In total, an estimated 1.8 million ha of land for palm oil plantations have been made available in West and Central Africa in the past decade, and more is being sought. Around 25 companies are investing directly in palm oil production in Africa, including some of the largest SE Asian and European producers targeting Liberia, Gabon, Nigeria, Sierra Leone, Cameroon, and Côte d’Ivoire in particular. The percentage of palm area harvested in West and Central Africa could increase significantly if all designated concessions became fully developed. For example, FAO estimates that Liberia has 17,000 ha under palm oil cultivation while its total capacity awarded is 500,000 ha.

Much of the land designated but not yet developed for palm oil production in Africa is forested. Consequently, it is in danger of deforestation. This land often contains high-levels of biodiversity and High Carbon Stock (HCS) forests. Almost 60 percent of African oil palm concessions overlap with the habitats of gorillas and chimpanzees, and about 40 percent of areas suitable for oil palm overlap with areas where apes live but are currently unprotected. This does not yet consider that concessions should recognize ‘buffer zones’ for food cultivation around villages, as well as leaving sacred sites and burial grounds untouched.

| Company | Plantation activities in SE Asia | Plantation activities in new frontiers |

| Felda Global Ventures (FGV:MK) | Largest plantation company in Malaysia. 431,000 ha of plantation land bank in 2015 with oil palm planted on:

327,343 ha in Malaysia 5,243 ha in Indonesia |

In 2012, FGV’s IPO raised$3.1 billion, with proceeds also earmarked for expansion. FGV seeksupstream expansion, reviews M&A options in SE Asia and Africa.

Existing African activities include providing plantation advice to planters in Sierra Leone and training of smallholders in Gabon with Olam International. |

| Golden Agri-Resources | Largest plantation company in Indonesia, executing agri-business activities of Sinar Mas Group (Indonesia).

In 2015, oil palm in SE Asia was planted on 485,606 ha in Indonesia. |

Lead investor in the private equity Verdant Fund(NASDAQ:UK).

2010: Verdant’s subsidiary, Golden Veroleum (Liberia) (GVL), signed a 65-year concession with the government of Liberia for oil palm plantation of 220,000 ha located within a total concession area of 350,000 ha. In addition, an outgrowers’ program of 40,000 ha. GGR announced that the government of Liberia and GVL plan to invest $1.6 billion in oil palm plantations in Liberia. 2015: 12,269 ha planted, with 4,684 ha newly planted. |

| Kuala Lumpur Kepong (KLK:MK) | KLK has a total land bank of 270,000, with palm oil in SE Asia in 2015 planted on:

90,897 ha in Malaysia 109,251 ha in Indonesia In addition, rubber planted on 13,916 ha. |

KLK holds a majority stake (62.9 percent) in UK-based Equatorial Palm Oil . Via its subsidiary KLK Agro Plantations, KLK has a 50/50 JV with PAL in Liberia, Liberian Palm Development (LPD), which KLK now controls with a majority interest of 81.5 percent.

2008: 50-year concessions for two estates signed with the government of Liberia. The estates include 21,757 ha, with expansion areas totaling 66,773 ha; of this 25,797 ha are set aside for outgrower programs. 2015: 7,474 ha planted with oil palm. |

| (SIME:MK) | Largest oil palm plantation company in the world with 1 million ha of plantation land bank in 2015. In SE Asia, oil palm was planted on:

308,307 ha in Malaysia 204,412 ha in Indonesia 82,068 ha in PNG & Solomon Islands. Small area of rubber, sugar cane, and pasture. |

2009: Sime Darby Plantations signed a 63-year concession agreement for 220,000 ha with the government of Liberia.

2015: Planted area of 10,518 ha: 10,411 ha palm oil 107 ha rubber. 2016: self-imposed moratorium creates delays for previously announced plans for extra 6,000 ha of oil palm, 4,000 ha of rubber. |

| Wilmar International | WIL is one of the largest agri-commodity producers, processors and traders globally. Total land bank of 331,000 ha, with oil palm in SE Asia in 2015 planted on

166,000 ha in Indonesia 57,800 ha in Malaysia. It also directly manages smallholder schemes in Indonesia. |

WIL has 16,900 ha planted in Africa. Through joint ventures and associates, WIL owns 46,000 ha of plantations in West Africa and Uganda. It also directly manages 31,428 ha under smallholder schemes in Indonesia and Africa, and 148,000 ha under the smallholder and outgrower schemes through joint ventures and associates in Africa, including minority interests in Uganda, Côte d’Ivoire and Liberia.

Ghana: WIL holds a 77 percent-stake in Benso Oil Palm Plantation (BOPP) in Ghana. Land bank of 6,799 ha through a 50-year leasehold valid until 2026. In 2015, WIL had 4,666 ha under production. Nigeria: PZ Wilmar is a joint venture between PZ Cussons (UK) and WIL. Plans call for 50,000 ha of oil palm plantation in Cross River State. 2015: around 30,000 ha planted. Reportedly over $500 million to be injected into the venture in Cross River State. |

| Olam International (OLAM:SG) | Leading agricultural commodity originator and trader. No own oil palm or rubber plantations in SE Asia. | OLAM entered 60/40-joint ventures for palm oil and rubber plantations with the Gabon government in 2010. Planned development of 100,000 ha of palm plantations over 2 phases out of a total leasehold land bank of 300,000 ha.

2015: 31,500 ha of palm oil and 7,500 ha of rubber planted. By 2017: 50,000 ha of palm and 28,000 ha of rubber planned. Capital expenditure for oil palm plantation until 2017 is given as$500 million. Smallholder program covering 30,000 ha planned in the second phase. |

Figure 3: Expansion projects of SE Asian plantation companies in frontier areas

Latin America: Palm oil expansion in Latin America is still dominated by local players. SE Asian producers, processors or traders currently seem to limit their activities to Africa. Negotiations for realizing palm oil plantations in Latin America have been documented but development has not materialized yet. The Malaysian Federal Land Authority (FELDA), which later founded Felda Global Ventures, reportedly made an attempt to set up a subsidiary in Brazil in 2008 for the development of palm oil plantations in the Amazon, but the company has denied the existence of these plans. Sime Darby, the largest plantation company in the world, was reportedly offered 70,000 ha of land for investment for up to US$ 300 million by the Peruvian government in 2012. The company has never confirmed the existence of such a deal.

SE Asian Corporations Investing in New Frontiers: Six large SE Asian corporations with existing or anticipated involvement in agriculture frontier expansion are shown above in Figure 3. Key risks associated with this expansion are highlighted below, with a focus on challenges and lessons learned based on the example of developments in Liberia. Liberia is interesting to investors, as the government has given concessions to 5 percent of the country to a small number of mostly SE Asian palm oil corporations.

Legal and Regulatory Uncertainty: Risk of Stranded Assets

Weak Law Enforcement and Changing Policies: West and Central African countries have recently been developing strategies to increase rural development via agricultural investment. Large-scale palm oil plantations are seen as a means to provide employment, finance and infrastructure and to obtain foreign exchange. However, to achieve this while mitigating environmental and social risks is a challenging endeavor, especially in post-conflict environments. Operational risks in changing policy and governance landscapes are unpredictable and are significantly elevated in these countries.

“Of course we are worried about the ecological consequences, but we have to grow the economy. We have to create jobs for our own people. How we do it sustainably is where we are struggling.”

Amara Konneh, finance minister of Liberia

Weak law enforcement, an overall lack of policies promoting agricultural development risk mitigation and concerns about the long-term security of investments are seen as key financial risks to investment in Africa. Notably, African countries with a suitable climate for palm oil production are among the least stable in the region and are ranked among the lowest in the world for political stability. At the same time, countries with weak land governance, or implementation thereof, often show a disproportionate share of investor interest in the recent surge for land.

Weak Land Tenure Regimes Create Conflicts with Customary Rights-Holders: One of the most significant risks to investment in plantations in Africa is the uncertainty of land titles and a lack of clarity around customary and legal ownership. In many West and Central African countries, the protection of private property is still limited to lands with registered titles. Up to 90 percent of sub-Saharan Africa’s land area is untitled and thus without legal owners, consequently falling to the state. However, the absence of formal land ownership documentation does not necessarily mean that the land is unoccupied, unused or unclaimed by forest-dependent communities. The vast majority of forested land is claimed under customary rights by at least one ethnic group or community. Customary rights refer to very long occupation, custom and practice. These rights have often not been formally recorded or recognized but are passed on verbally and through agreements between communities. If such land is allocated to logging or plantation companies aiming to exploit forest resources, this can lead to conflicts with customary forest rights-holders.

Some legislative frameworks, such as in the Democratic Republic of Congo, in principle recognize customary land rights and oblige investors to undertake prior consultation with Indigenous Peoples and other local communities, and to compensate for any loss of customary usage rights. However, uncertainties about the implementation process can aggravate land tenure insecurity and property conflicts.

Stranded land assets: Uncertain land-tenure can lead to stranded assets, resulting in putting potential future revenue at risk. For the firm’s operations, capped land bank implies fewer hectares to harvest and hence less production volume. This implies lower revenue and write-offs.

Lessons Learned: Land Rights Conflicts in Liberia

Despite laws governing concessions in Liberia at the time that several large palm oil concessions were awarded (2008 to 2010), breaches of national laws and policies have been documented. The Liberian government assumed that it was entitled to grant concession over undeeded lands at will, often neglecting the rights of customary communities.

Non-Compliance in Concession Awards: The UN Security Council’s Panel of Experts to Liberia highlighted a lack of compliance with public procurement regulations in the award of GVL’s concession. In a post-award process audit commissioned under the Liberia Extractive Industries Transparency Initiative (LEITI) for extractive industry contracts granted in Liberia, the three major contracts for industrial palm oil plantations granted between 2009-11 were all found to be only partially compliant (Maryland Palm Oil – part of SIFCA – and Sime Darby Plantation) or non-compliant (GVL) with national laws and procedures. Breaches identified include concession terms exceeding the maximum of fifty years as laid down in the Public Lands Law; stability clauses exceeding the maximum of 15 years as laid down in the Revenue Code of 2000; concessions being awarded without competitive bidding; and a lack of stakeholder forums during the award process. So far these findings have had no direct consequences.

The concession of Equatorial Palm Oil (PAL), now majority-owned by KLK, was not part of the review as it was signed before the review period.

Strengthening of Community Rights: While Liberia still does not have a central land registry, the requirement for free, prior and informed consent (FPIC) has become a key principle in the country’s 2009 Community Rights Law with Respect to Forest Lands. In 2013, a new land policy came into force, resulting from the realization that large amounts of forestry management concessions and timber sales contracts were located on lands subject to community claims based on customary ownership. A draft Land Rights Act is currently under discussion. Although the law does not directly alter the leasehold rights for the private sector concessions granted in the past, the recognition of customary rights to land and resources in Liberian legislation is undergoing significant improvements and communities are increasingly aware of their rights. While applicable Liberian law is generally recognized as being strong, its enforcement is not. As concluded in a recent report, “The state has failed to set appropriate standards or progressive precedence for the private sector to follow.”

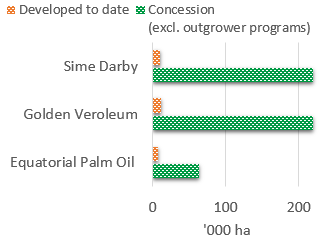

Figure 4: Liberian concession areas vs. area developed to date

Expansion Plans Delayed: As shown in Figure 4, Equatorial Palm Oil (KLK), Sime Darby, and Golden Veroleum’s expansion plans are delayed because of regulatory, operational, and financial risks. The Ebola epidemic was one contributing factor, but more notable were the objections of local communities to the expansion on their customary land.

- Equatorial Palm Oilexpected in 2010 that from 50,000 to 100,000 ha would be productive in the near-term. By 2015, it had planted only 7,474 ha.

- Golden Veroleumaims to develop more than 200,000 ha in Liberia. By 2012, the company had frozen expansion plans at the request of the RSPOafter community complaints. Expansion started again in 2013, but by the end of 2015, only around 12,000 ha had been planted, of which 4,684 ha was new in 2015.

- Sime Darby’splans to develop 120,000 ha by 2020 no longer seem realistic today. Land rights issues and a self-imposed moratorium on new deforestation contributed to the delay, resulting in only 10,518 ha planted to date.

Free, Prior, and Informed Consent: Risk of Contested Land Rights

Recognition of Rights to Land and Resources: FPIC and fair, equitable, and legally enforceable agreements are of critical importance to forest-dependent communities, and also provide dependability for companies. The recognition and respect of rights to lands, territories and natural resources, in combination with increased transparency by investors over contracts and deals, is a critical precondition for avoiding or solving conflicts around land.

Due to the insecure land tenure, it is difficult to ensure uncontested land rights. This carries risks for companies because relying on government assurances may not be sufficient to avoid community grievances against state-granted concessions.

Lessons Learned: FPIC and No Deforestation in Liberia

Neglecting local rights to such fundamental resources as land and water leads to conflict and social tension. This reduces economic viability and puts the potential contribution of an investment to a sustained improvement of livelihoods at risk.

The requirements for FPIC have not only been strengthened under Liberian law but also apply under the RSPO, where securing FPIC from communities prior to establishing oil palm plantations on customary land is a mandatory requirement. Companies in breach of these obligations risk losing their RSPO certification. The companies profiled in the report are all members of the RSPO.

Golden Veroleum’s (GVL) activities in Liberia have repeatedly been criticized by civil society organizations. Investigations in 2015 by the Forest Peoples Programme identified fundamental flaws in the company’s approach to FPIC.

Since 2012, local communities from three districts have filed complaints with the RSPO against GVL for disrespecting communities’ right to FPIC and lacking a comprehensive and participatory independent social and environmental impact assessment including proper identification of primary forest, High Conservation Value (HCV) areas, and local peoples’ land.

GVL and its lead investor Golden Agri-Resources (GGR) refuted these assertions by referring to their policies and initiatives, including community engagement and a pledge to support the Government of Liberia’s initiative to stop deforestation by 2020. GGR announced an ambitious Forest Conservation Policy (FCP) early in 2011, stating its aim to move towards sustainable production practices and a no-deforestation footprint. A particular focus lies on identifying HCS forests.

Greenpeace noted progress in ending deforestation within GGR’s supply chain in 2014 and 2015, but found shortcomings in implementing FPIC and conflict resolution, the quality of its HCV assessment, and its supply chain transparency. There have been outbreaks of violence at the GVL concession spurred by land and employment issues. The NGO Global Witness published a report in October 2016 documenting breaches of community rights on the GVL concession.

The RSPO Complaints Panel published its final decision in September 2015, outlining a list of action points for the company and requiring the publication of quarterly progress reports for a period of 12 months, after which progress will be reviewed. GVL replied to this decision with a detailed response, outlining the steps it intends to take.

Equatorial Palm Oil , majority-owned by Kuala Lumpur Kepong Palm Oil , has been the subject of complaints from local communities and civil society organizations regarding breaches of FPIC obligations and disregard of community rights.

A complaint to the RSPO on grounds of violation of the RSPO’s principles and criteria in regards to land use and local community rights was filed in 2013. The RSPO responded that, “[t]here are reasonable grounds to believe that the RSPO Principles and Criteria has been breached.” The complaints panel demanded that PAL not carry out planting in disputed areas, and that it submit an action plan addressing outstanding issues.

The company and the complainants engaged in a participatory mapping process, and in May 2016 a Memorandum of Understanding to resolve the complaint was signed between the stakeholders. It includes a final map of lands where the communities have not consented to oil palm development and the agreement that EPO/KLK would not develop these areas.

Sime Darby’s activities in Liberia have also initially been accompanied by conflicts and controversies. In 2011, the company received a$50,000 fine by the Liberian Environmental Protection Agency due to non-compliance with the terms and conditions of the permit. In 2011, local communities affected by Sime Darby’s operations filed an RSPO complaint, stating that the company allegedly operated in violation of the RSPO Principles and Criteria and in violation of the RSPO’s New Plantings Procedure, by “acquiring lands without respecting customary rights and without the free, prior and informed consent of the customary land owners […], peoples’ land were taken […] clearing lands prior to the completion of new plantings procedure (NPP).”

Sime Darby and community groups entered a process of resolving these issues following RSPO requirements. The company acknowledged shortcomings in its procedures and announced steps to address the complaints. The RSPO complaint was withdrawn in January 2012. The company agreed to halt expansion under a self-imposed moratorium in 2014. It further agreed to fulfill several social commitments for the affected communities and has implemented several sustainability policies and processes including FPIC and the identification of HCS forests. The company states that it “[…] will not proceed with development in an area where the leaders and the community have not given their express approval“.

Evidence is emerging that Sime Darby is upholding its improved FPIC procedures in its current community negotiations. It has also imposed a moratorium on new clearings, awaiting the results of a trial of High Carbon Stock (HCS) methodologies. While this reduces risks associated with unsustainable business operations, it does delay the company’s original aggressive expansion plans.

No Deforestation Policies: Risk of Stranded Land Assets

Market pressures can contribute to the development of stranded land assets. Government and court rulings, and investors’ and buyers’ NDPE policies, could force companies to cease further development of their land bank if it overlaps with forests, peatland, protected species habitats or land rights claimed by local communities. Hundreds of corporations worldwide have made commitments to eliminate tropical deforestation from their commodity supply chains. The Paris Agreements, and the Norway partnerships with several African and Latin American countries, might drive financial resources to address the role of deforestation in climate change more than ever before. Institutional investors, such as the Government Pension Fund of Norway are increasingly divesting from corporations driving deforestation.

Financial Performance at Risk Over Poor CSR Operational Management

If disregarding environmental and social issues in industrial palm oil production when entering frontier markets, corporations and their financiers face considerable risks.

- Stranded land assets: Access to land involves many stakeholders: government, local communities, and businesses. Palm oil businesses usually obtain land concessions from the state. If the legal and land tenure situation changes, a concession may effectively be revoked. This may be provoked by the legal recognition of communal land rights, HCS/HCV provisions and measures to conserve biodiversity. This may lead to delayed revenues and asset write-offs on-balance sheet, reduced growth prospects and decreased market valuation

- Reputational damage leads to loss of customers: Customers may not want to be connected to a company linked to social and environmental risk, or that does not comply with a buyer’s zero-deforestation procurement policy. By not meeting policies implemented by a large share of buyers, palm oil growers put potential future revenue at risk, as shown by revenue-at-risk leading to decreased earningsfor Sawit Sumbermas Sarana, Provident Agro, and Austindo Nusantara Jaya.

- Sawit Sumbermas Sarana: 2016 42 percent quarterly revenue at risk based on Q4 2015 actual revenue losses of 0 percent to 5 percent when SSMS did not meet buyers’ NDPE policy expectations.

- Provident Agro: 2016 37 percent quarterly revenue at risk based on Q4 2015 actual revenue losses of 15 percent when PALM did not meet buyers’ NDPE policy expectation

- Austindo Nusantara Jaya: 2016 35 percent quarterly revenue at risk based on Q4 2015 actual revenue losses of 10 percent when ANJT did not meet buyers’ NDPE policy expectations.

- Loss of financiers and higher costs of debt and equity: Reputation risk can lead to increased financial costs. As more and more banks and institutional investors have adopted responsible financing and investing policies, violation of standards could lead to disinvestment, banks charging higher costs or refusing to lend money.

- Increasing costs for higher sustainability performance:Unclear land title, the increasing seriousness with which FPIC processes are being conducted, and recognition of the need to conserve HCV forests and HCS areas may slow the speed of plantation development and result in higher costs. Land disputes can delay or even derail existing plans and future expansion prospects.

- Lower returns on investment from policy risk: If deforestation and community rights are tackled more seriously on international and national levels, the conventional approach of companies active in large-scale plantation development – or their buyers – may no longer be compliant. Their financial stakeholders could then experience lower returns on investments and higher risk profiles.

Risk Mitigation Can Enhance Returns

Palm oil development in Africa does not have to be damaging. Palm oil has many favorable attributes over its full life cycle. It has a positive carbon balance and when grown in a landscape mosaic it can play a role in biodiversity conservation. However, the available evidence raises many questions about the long-term viability and the social and environmental footprint of expansion of the palm oil industry in these countries, and these investments’ financial returns.

Models where palm oil companies provide technical and financial support to smallholders may be beneficial in economic, social, and environmental terms. This requires a move away from the large-scale concession model. Industrial plantations, following certain criteria, can generate sustained benefits for local communities. Such an approach would reduce production areas from existing concession agreements through conservation of HCV and HCS areas, consideration of community sites and buffer zones for food production. The development of plantations on land that has already been cleared and is not required for the production of food crops avoids the further conversion of primary forest, thus also helping to achieve countries’ commitments for emission cuts under REDD+. A sustainable intensification of existing plantations without putting additional pressure on natural forests could also contribute to meeting the growing demand for palm oil.

Companies could help to ease impasses that currently block more efficient palm oil production. Companies have the means to obtain quality-planting material, to supply agricultural inputs at competitive prices to smallholders and to obtain bank loans for the development and maintenance of plantations according to commercial standards. While it shifts the burden of development onto the smallholders and exposes them to higher risks, it also is an opportunity for them to enter the sector. Customary land rights and pro-poor development models are prerequisites to any new model, and would be in the mutual benefit of communities and investors.

From an investor’s perspective, respecting local communities as mature negotiation partners and entering into a balanced cooperation with them could reduce the level of social conflict, project delays and long-term operational risk. This may offer efficient pathways to enable profitable investments in African countries while at the same time providing long-term sustainable development opportunities for rural people and avoiding lengthy processes to solve land rights disputes.