Key Findings

- RSPO Complaint Panel ruling on non-compliance expected soon

- RSPO’s formal rules require that IOI be suspended from selling CSPO if grievance is upheld in the Panel’s final ruling

- Several other buyers may suspend IOI independent from RSPO ruling

- Any form of suspension would trigger further CSPO contract revaluation

Overview

The RSPO Complaints Panel’s pending decision on IOI Corporation’s (IOI:MK) operations in Sarawak and West Kalimantan concerns illegal land grabbing, peatland clearing and drainage, loss of High Conservation Value (HCV) forests, and planting palm oil trees illegally inside a forest reserve. RSPO’s certification procedures stipulate that such infractions may result in suspension of group membership. Should the Panel follow formal rules, IOI might experience a decrease in revenue from sales of its Certified Sustainable Palm Oil (CSPO) contracts, resulting in free cash flow contractions in a tight margin market.

Over the past five years, IOI has struggled to convert consistent increases in CPO production into greater revenue and follow-on share price increases. With the 63 companies with significant agricultural exposure that trade on the Bursa Malaysia, Indonesia Stock Exchange, and Singapore Exchange underperforming regional indices in 2015, IOI is facing both sectoral downdrafts and a possible unfavourable RSPO suspension, potentially putting further downward pressure on their share price. While IOI’s 5-year CPO production compound annual growth rate (CAGR) is up 2.6%, over the same 5-year period, IOI’s 5-year revenue CAGR is -6.35%.

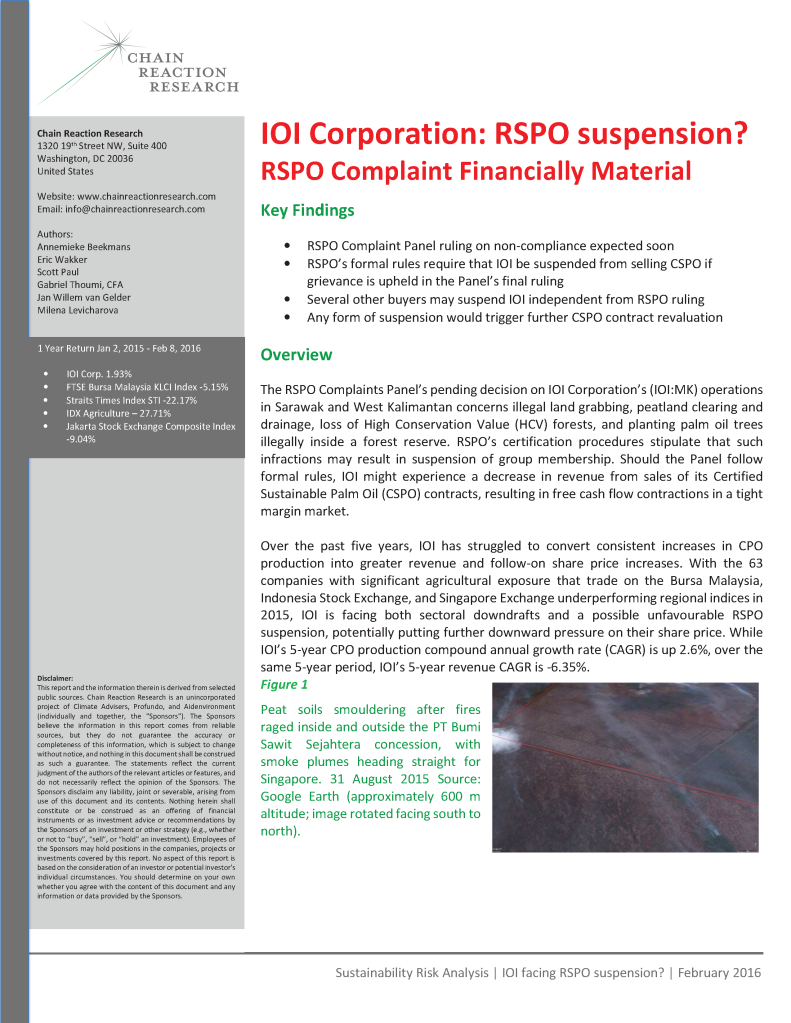

Figure 1: Peat soils smouldering after fires raged inside and outside the PT Bumi Sawit Sejahtera concession, with smoke plumes heading straight for Singapore. 31 August 2015. Source: Google Earth (approximately 600 m altitude; image rotated facing south to north).

IOI Status

IOI is a Malaysian palm oil producer, refiner and trader, whose business segments include palm oil plantations, refineries, related manufacturing activities, and real estate. IOI’s main businesses are undertaken by IOI Corporation (IOI:MK) in the upstream and downstream palm oil business and IOI Properties Group Bhd in the real estate business. Both segments are publicly listed as separate entities on Bursa Malaysia. IOI’s current market cap is $7.2 billion1, positioning the company among the largest in the sector.

IOI contributes approximately 67%2 to the Group’s earnings. Its plantations are concentrated 64% in East Malaysia, 25% in Peninsular Malaysia, and 11% in Indonesia. In addition, IOI is a prominent member of the Roundtable on Sustainable Palm Oil (RSPO). Two-thirds of its planted land bank and 12 of 14 mills are RSPO-certified. It is also one of the largest global suppliers of CSPO. IOI reported in 2015 that 38% of its palm oil sold was CSPO and 94% of its production traceable to the mill.3

IOI has four palm oil refineries. Three are in Malaysia. One is in Rotterdam. The four refineries are RSPO certified for the production of segregated RSPO palm oil. The Rotterdam facility also permits the company to have direct exposure via pipelines to the Finnish biofuel producer Neste Oil. Neste Oil has already on different occasions suspended purchases from IOI Corporation because of RSPO non-compliance.4

RSPO Complaints

IOI is currently subject to formal RPSO complaints on its operations in Sarawak, Malaysia, and West Kalimantan, Indonesia. Filed by various NGOs in November 2010 and March 2015, the complaints concern illegal land grabbing, peatland clearing and drainage, loss of HCV area, and planting inside a forest reserve. In September 2015 Chain Reaction Research reported about IOI’s possible suspension from the RSPO and – consequently – from the CSPO market.5

RSPO Complaint #1: Sarawak, Malaysia: In 1997, IOI acquired a 70%-stake in IOI Pelita, a Sarawak plantation company, in spite of a lawsuit filed by Kayan and Kenyah villagers over the estate’s occupation of Native Customary Land without Free Prior and Informed Consent. On behalf of community members, NGOs filed a formal complaint against IOI in November 2010. IOI Pelita and the Long Teran Kanan community engaged repeatedly in unsuccessful mediation efforts. In December 2015, the latest attempt was led by IOI’s JV partner and also failed. Following earlier proceedings, in May 2012 RSPO ruled that IOI Pelita would remain prohibited from obtaining RSPO certification until the conflict was resolved along RSPO’s P&C. This ruling may have had a perverse impact because it has allowed IOI to benefit from RSPO certification across the board whilst leaving the conflict unresolved. To correct the situation, we expect that the Complaints Panel will weigh this in its final ruling in regard to the current complaint.

RSPO Complaint #2: West Kalimantan, Indonesia: In March 2015, Aidenvironment revived and expanded an earlier complaint filed four years earlier. The grievance alleges that IOI’s majority owned subsidiaries in West Kalimantan seriously flouted RSPO’s standards and procedures. It is alleged that IOI’s subsidiaries PT BNS and PT SKS illegally deforested 11,750 hectares, 1,300 ha inside the Manismata protected forest reserve, without having secured legally required plantation business permits. Despite earlier commitments made by IOI to follow due legal procedure, it was found that PT BNS still occupied some land within the reserve in 2015.

Figure 2: Land development (dark green) between January and December 2009, inside and outside forestland release boundaries of IOI subsidiaries PT SKS and PT BNS (red lines) overlaid with the West Kalimantan forestland designation map of 2004.

Furthermore, the new complaint also highlights non-compliance with a host of other RSPO standards in the adjacent concession held under subsidiary PT BSS, including deep peat clearance and drainage of conservation areas. In 2015, IOI commissioned verification studies which found “no sighting of the fire prevention and control measures as per [Environmental Impact Assessment] such as fire towers.” Additionally, IOI’s verifier Intertek found that PT BSS’ land was being drained without floodgates that are essential to control groundwater levels. IOI’s other assessor, Aksenta, reported that a large portion of the concession area was burnt for clearing in 2014. Additional research by CRR partners found that some 66% of PT BSS’ land bank burnt at least once in 2014 and 2015, while fires affected 5,500 ha in PT SKS and PT BNS in 2015 alone. By October 2015, a vast area of at least 60,000 ha inside and in the vicinity of IOI’s concessions had burnt. This is shown visibly as brown areas in the Landsat image of mid-October 2015 below.

Figure 3: Brown areas are 60,000 ha inside and in the vicinity of IOI’s concessions that had burnt.

Complaints Panel ruling remains pending

NGOs first documented concerns about IOI’s compliance with RSPO standards six years ago. At present, RSPO’s Complaints Panel has yet to reach a final decision after reviewing the new complaint. In August 2015, the Panel threatened IOI with suspension6 if it failed to adequately address the complaint, specifying cause a month later. The complainant has since dismissed IOI’s responses as inadequate and insists that RSPO enforce its own partial certification rules which state that members will be suspended if their non-certified subsidiaries operate in violation of law, are involved in significant land conflicts and/or replacement of High Conservation Value areas.

RSPO’s Complaints Panel ruling will be subject to intense scrutiny. The IOI complaint case is sensitive within RSPO circles as the Executive Board’s handling of initial complaints in 2010-11 has been severely criticized. As a result, NGOs have submitted a resolution on “Guaranteeing Fairness, Transparency and Impartiality in RSPO’s Complaint System.” In November 2013, RSPO’s General Assembly adopted the Resolution by a large majority.

Though RSPO recently has tightened its standards and procedures, its partial certification requirements remain in place, and were last revised in 2011. If suspension is enforced according to these requirements, the whole IOI Group (Loders Croklaan included) would be suspended from trading CSPO until the complaint is resolved. In a best case scenario, RSPO would convene conflicting parties to work towards joint resolution. For the Ketapang case, this would require a 3-6 month period but the Sarawak complaint may require a longer period of time to come to resolution.

IOI’s overall exposure to sustainability risks

25% of IOI’s land bank contested. IOI’s total contested land is 25% of the corporation’s total land bank (206,918 ha7). This figure takes into account the above mentioned land conflicts, peat land drainage and HCV clearing on PT BSS, as well as forest clearing outside concession boundaries, the absence of legal permits and absence NPP submission to RSPO for PT BNS and PT SKS. These four concessions are not RSPO certified and contested.

In addition, new information has come to light that IOI’s estates in West Kalimantan suffered from significant fire outbreak in 2014 and 20158. Given findings of its own certification bodies that inadequate fire prevention and mitigation measures were in place, IOI can therefore be considered as contributor to the extreme regional haze August to October, 2015. The fourth Corporation’s concession PT KPAM has yet to be developed and is deemed contested because its Location Permit has expired.

Figure 4: Overview of RSPO certified and non-certified IOI concessions

Strong policy commitments, weak enforcement. IOI has been a core member of the RSPO since 2004, with representation of the Board of Governors for many years. In 2009, IOI published its first sustainability policy, including commitments to not open up peatland and forestland. In 2010, a detailed study9 highlighted IOI’s failures to comply with its own policy. In early 2014, IOI’s CEO committed to even more ambitious sustainability targets, which were followed up by subsidiary Loders Croklaan’s “Taking Responsibility”10 policy that was embraced by the whole Corporation in January 2015. These complains demonstrate that IOI struggles to implement its policies in greenfield projects and brownfield acquisitions.

IOI Corporation’s possible suspension: potential revenue impacts

RSPO’s suspension is expected to be short-term, possibly lasting up to one year. This may result in lost revenue, reputational damage, and potential downdraft in equity valuation. IOI’s established buyers, who purchase its CSPO in accordance with their sustainability policies, may retract, and IOI’s sales may be impacted.

Figure 5: Which customers could retract? Tons of palm oil sold by IOI’s Malaysian refineries for July – November 2015

Figure 5 gives an idea which companies buy from the Malaysian refineries of IOI Corp.

In the short-term, it is unlikely that IOI’s rebranded CPO (formerly CSPO) may find substitute buyers, resulting in increasing financial costs from longer-term physical storage. Without substitute buyers, a RSPO suspension will be an earnings drag for IOI in the short-term. On previous controversial occasions, some IOI clients did not hesitate to stop purchases. Neste Oil ceased buying from IOI after they had not adhered to agreed-upon ESG standards. On other occasions, buyers have also retracted from their suppliers over environmental and sustainable reasons11.

Figure 6: Share of RSPO certified palm oil in IOI Corp’s total sales. Source: RSPO IOI ACOP progress report 2014, p.6 and RSPO IOI ACOP progress report 2013, p.5

Apart from being RSPO members, several of IOI’s buyers have adopted No Deforestation, No Peat, No Exploitation Policy (NDPE) policies. These buyers have acted more rigorously on suppliers’ non-compliance than has RSPO. For example, GAR, Apical and Wilmar have suspended several suppliers over the past two years. In order to calculate how much revenue IOI could lose in case of RSPO suspension, its RSPO Annual Communications of Progress (ACOP) progress reports were used as reference

Figure 6 shows that IOI sold an estimated 418,000 tons CSPO during 2016, compared to an estimated 1,096,000 total CPO sales – or 38%. If sales volumes are similar in 2016, with average annual selling price of $522 per ton, up to $223 million of potential CSPO revenue may delayed or diminished. Table 1 demonstrates revenue loss scenarios, depending on whether IOI sell its CSPO at premium or discount to CPO depending on its ability to sell CPO without provenance.

Table 1 – CSPO revenue losses: Sensitivity to CSPO sales lost and CSPO price premium, millions

| CSPO Premium to average

price/tonne |

% CSPO sales lost | |||||

| 0% | 20% | 40% | 60% | 80% | 100% | |

| -10% | -$11 | -$32 | -$51 | -$71 | -$92 | -$111 |

| -5% | -$6 | -$27 | -$48 | -$69 | -$90 | -$111 |

| -2% | -$2 | -$24 | -$46 | -$68 | -$89 | -$111 |

| 0% | 0 | -$22 | -$45 | -$67 | -$89 | -$111 |

| 2% | $2 | -$20 | -$43 | -$66 | -$89 | -$111 |

| 5% | $6 | -$18 | -$41 | -$65 | -$88 | -$111 |

| 10% | $11 | -$13 | -$38 | -$62 | -$87 | -$111 |

Scenario analysis generally shows that IOI may lose revenue from its possible RSPO suspension. In a worst case scenario IOI could lose 50% of its CSPO sales in 2016 – if the suspension is for six months – taking a revenue hit of $111 million. On the other hand, if IOI retains its CSPO sales, it could potentially realize a premium to last year’s sales with a $11 million revenue increase. Many of IOI’s clients, including Neste, Wilmar, Golden Agri Resources, and Apical, have sustainability policies at place. These clients are also RSPO members. Therefore, they are likely to refrain from buying CPO. Although the company could potentially sell this CPO to others, it might be difficult – and it is uncertain – to find substitute buyers in the short run, considering complicated local logistics and a saturated marketplace.

Table 2 – Comparison of 2016 scenarios, millions

|

Indicator |

Baseline scenario 2016 | Worst case scenario 2016 |

| Sales | $2,716 | $2,591 |

| Net Income | $306 | $200 |

| Net Income Margin | 11.3% | 7.7% |

| Return on Assets | 9.1% | 6.0% |

| Return on Equity | 24.3% | 15.9% |

Table 3 – Sensitivity of 2016 revenue to loss of customers and CPO price

|

% CSPO not sold |

Price of CPO (USD/ton) | ||||||

| $ 480 | $ 504 | $ 528 | $ 552 | $ 576 | $ 600 | $ 624 | |

| 5% | $ 2,693 | $ 2,692 | $ 2,692 | $ 2,691 | $ 2,690 | $ 2,690 | $ 2,689 |

| 10% | $ 2,682 | $ 2,682 | $ 2,681 | $ 2,679 | $ 2,678 | $ 2,677 | $ 2,676 |

| 20% | $ 2,662 | $ 2,660 | $ 2,658 | $ 2,656 | $ 2,654 | $ 2,652 | $ 2,650 |

| 30% | $ 2,642 | $ 2,639 | $ 2,636 | $ 2,633 | $ 2,630 | $ 2,627 | $ 2,624 |

| 40% | $ 2,622 | $ 2,618 | $ 2,614 | $ 2,610 | $ 2,606 | $ 2,602 | $ 2,598 |

| 50% | $ 2,602 | $ 2,597 | $ 2,592 | $ 2,587 | $ 2,582 | $ 2,577 | $ 2,572 |

In addition, Table 4 presents the sensitivity of the Return on Equity to the % CSPO not sold and sales growth. On the left, the column indicates the percentage of annual CSPO sales not realized as juxtaposed to the potential sales growth, horizontally. Considering that the suspension scenario discussed above can vary depending on these inputs, the table gives a fair opportunity to observe the response of ROE. Currently, the suspension scenario assumes that 50% of the annual CSPO is not sold and that sales continue to exhibit negative growth of -2% per annum, the cross-check is showed in bold.

Table 4: ROE 2016 Sensitivity to % CSPO not sold & % Sales Growth

|

% CSPO not sold |

Sales Growth | ||||||

| -0.06 | -0.04 | -0.02 | 0 | 0.02 | 0.04 | 0.06 | |

| 5% | 15.9% | 16.2% | 16.5% | 16.8% | 17.1% | 17.4% | 17.7% |

| 10% | 15.8% | 16.1% | 16.4% | 16.7% | 17.1% | 17.4% | 17.7% |

| 20% | 15.7% | 16.0% | 16.3% | 16.6% | 16.9% | 17.2% | 17.5% |

| 30% | 15.6% | 15.9% | 16.2% | 16.5% | 16.8% | 17.1% | 17.4% |

| 40% | 15.5% | 15.8% | 16.1% | 16.4% | 16.7% | 17.0% | 17.3% |

| 50% | 15.3% | 15.6% | 15.9% | 16.3% | 16.6% | 16.9% | 17.2% |

RSPO Complaint Risk to Institutional Investors and Banks

Tan Sri Dato’ Lee Shin Cheng owns 47.9% of the company. Lee has a direct interest in the company of only 1.06%, the rest 46.8%12 being held by corporations owned by his family. This concentrated ownership structure reduces the ability for other shareholders to exert influence on the company.

Figure 7: Ownership structure of IOI Corporation. Source: IOI Corporation (August, 2015), “Annual Report 2015”; Bumitama Agri (December 2014), “Annual Report 2014.” IOI Corporation, “Organisation Chart”, website IOI Corporation. Viewed in December 2015; Website: Bursa Malaysia viewed in December 2015.

83% of IOI’s shares are held by Malaysian entities or individuals. The Malaysian governed owns a 1% stake. The main institutional investors are listed in Table 5. None are RSPO members.

Table 5 – Top institutional shareholders of IOI Corporation

| Investor parent | Investor | Country | Shares Millions | Value Millions | Ownership |

|

Yayasan Pelaburan Bumiputra |

Permodalan Nasional Berhad | Malaysia | 580 | $557 | 9.0% |

| Employees Provident Fund | Employees Provident Fund | Malaysia | 539 | $617 | 8.3% |

| Safra Group | Bank J. Safra Sarasin | Switzerland | 279 | $268 | 4.3% |

| KWAP Retirement Fund | Kumpulan Wang Persaraan | Malaysia | 175 | $168 | 2.7% |

| Annhow Holdings | Annhow Holdings | Malaysia | 123 | $118 | 1.9% |

| Vanguard | The Vanguard Group | United States | 67 | $64 | 1.0% |

| GIC | GIC Private | Singapore | 45 | $43 | 0.7% |

| Prudential (UK) | Eastspring Investments | Malaysia | 40 | $39 | 0.6% |

| Oversea-Chinese Banking Corporation | Great Eastern Life Assurance (Malaysia) | Malaysia | 38 | $36 | 0.6% |

| BlackRock | BlackRock Institutional Trust Company | United States | 38 | $44 | 0.6% |

| Public Mutual | Public Mutual | Malaysia | 34 | $33 | 0.5% |

| Rickoh Holdings | Rickoh Holdings | Malaysia | 33 | $31 | 0.5% |

| Dimensional Fund Advisors | Dimensional Fund Advisors | United States | 18 | $18 | 0.3% |

| CIMB Group | CIMB-Principal Asset Management | Malaysia | 15 | $14 | 0.2% |

| JPMorgan Chase | J.P. Morgan Asset Management | Singapore | 14 | $14 | 0.2% |

| Pensioenfonds Zorg & Welzijn | PGGM Vermogensbeheer | Netherlands | 11 | $12 | 0.2% |

Source: ThomsonEikon, “Shareholdings – IOI Corp”, viewed in February 2016

Table 6 provides an overview of the banks which have provided loans to IOI or underwritten stock or debt over the past five years. Three of IOI’s banks are RSPO members. These banks may reconsider their relationship with IOI if IOI is suspended from the RSPO. Furthermore, RSPO members HSBC, Citigroup, and Standard Chartered’s own environmental and social policies specific to palm oil risks may also impact their banking relationship with IOI valued at $595 million, depending on how loan and underwriting covenants are written and enacted upon.

Table 6 – Banks financing IOI Corporation (2010-2015)

|

Investor Parent |

Investor Parent Country | RSPO

Member |

Loans (million) | Underwritings (million) |

| AmBank Group | Malaysia | No | $95 | |

| Bank of China | China | No | $50 | |

| Citigroup | United States | Yes | $150 | |

| DBS | Singapore | No | $80 | |

| HSBC | United Kingdom | Yes | $100 | $150 |

| Malayan Banking | Malaysia | No | $173 | |

| Mitsubishi UFJ Financial | Japan | No | $607 | $150 |

| Mizuho Financial | Japan | No | $35 | |

| Morgan Stanley | United States | No | $150 | |

| Oversea-Chinese Banking Corporation | Singapore | No | $343 | |

| RHB Banking | Malaysia | No | $95 | |

| Standard Chartered | United Kingdom | Yes | $80 | $95 |

| Sumitomo Mitsui Financial | Japan | No | $355 | |

| United Overseas Bank | Singapore | No | $80 | |

| Total | $1,730 | $1,058 |

Source: ThomsonONE, “IOI Corp: Loans and issuances”, viewed in February 2016.

References

- MYR translated at 0.24 USD / MYR per Feb 10, 2016

- Bloomberg. IOI Corp. Bhd. Segment results. Viewed in December 2015

- IOI Corporation (2015, August). Annual report 2015. IOI

- Neste Oil (2015 April). Releases and News, online: https://neste.com/fi/en/neste-suspends-crude-palm-oil-purchases-ioi-and- demands-completion-action-program, viewed on 10 December, 2015.

- https://chainreactionresearch.com/2015/09/30/ioi-risks-rspo-market-suspension/

- http://www.rspo.org/members/complaints/status-of-complaints/view/80

- IOI Corporation (n.d.), “Estates and Mills”, online: http://www.ioigroup.com/Content/BUSINESS/B_Estates, viewed on 08 December, 2015

- https://chainreactionresearch.files.wordpress.com/2015/12/crr-fire-study- 120115-v-3.pdf

- http://www.foeeurope.org/sites/default/files/publications/FoEE_Too_ pdf

- http://europe.ioiloders.com/taking-responsibility

- Koswanage, N. (2011, April 7). Green palm oil body censures Malaysia’s IOI, Uniliver. Online: http://www.reuters.com/article/us-malaysia-palm-ioi- idUSTRE73620520110407, viewed in February, 2016.

- IOI Corporation (2015, August). Annual report 2015. IOI