Initial Risk Analysis: Sawit Sumbermas Sarana Tbk.

December 9, 2013

Chain Reaction Research conducted this Initial Risk Analysis identifying serious undisclosed risks associated with the scheduled December 12 Initial Public Offering of the palm oil company Sawit Subermas Sarana Tbk. on the Jakarta Stock Exchange.

Download as PDF

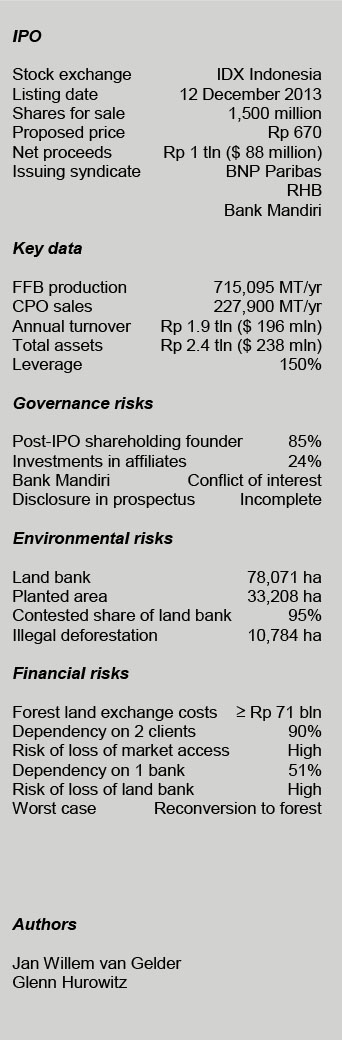

Indonesian oil palm company PT Sawit Sumbermas Sarana Tbk. (SSMS), which is managing plantations and palm oil mills in Central Kalimantan, is making an Initial Public Offering (IPO) on the Jakarta stock exchange on 12 December 2013. BNP Paribas, RHB and Bank Mandiri are managing and underwriting the issuance.1

Serious Governance and Sustainability Risks

Investors buying the shares of SSMS are exposed to serious governance and sustainability risks which are likely to affect the performance of SSMS’s shares and the position of the public shareholders of SSMS:

- Post-IPO ownership of the company continues to be dominated by Abdul Rasyid and his family, who have invested a significant part of SSMS’s assets in associated companies outside the control of the shareholders of SSMS;

- Bank Mandiri is very strongly exposed as a lender to SSMS and at the same time is involved in underwriting the share issuance. As part of the IPO’s proceeds will be used to repay Bank Mandiri’s debt, this constitutes a clear conflict of interest;

- SSMS is not disclosing all relevant facts (on land permits, related party transactions, etc.) in its English-language prospectus. While more relevant facts are included in the Indonesian-language prospectus, some critical information on applications with the Ministry of Forestry is missing there as well;

- While SSMS and its subsidiaries hold a total land bank of 78,071 ha, of which 33,208 ha are already planted, an analysis based on spatial data and permits applied for by the company suggests that no less than 95% of the company’s total land bank is contested: full authorization to use such lands for oil palm plantations has not been granted by central government agencies. It is doubtful that the company will be able to get this authorization, based on existing regulations, and doing so will be very expensive. In the worst case scenario, the company will have to convert some of its plantations back to forests;

- Based on satellite images we conclude that SSMS has deforested approximately 10,784 ha in the period 2003-2012. As most of this area lacked central government authorization for conversion to oil palm plantations, this deforestation was clearly illegal;

- A significant part of the company’s land bank overlaps with potential orangutan habitat and is located on peatland;

- The company is dependent on only two palm oil traders for almost 90% of its sales. Both have adopted commitments to clean up their supply chains and exclude suppliers involved in environmental and social abuses. SSMS therefore runs a serious risk in losing its access to the market, with disastrous financial consequences for the company.

More details on these risks are provided in this report.

Key facts on the IPO of SSMS

The Indonesian oil palm plantation company PT Sawit Sumbermas Sarana Tbk. (SSMS) is making an Initial Public Offering (IPO) on the Jakarta stock exchange on 12 December 2013 by offering up to 1,500,000,000 ordinary shares of par value Rp. 100 each to the public. BNP Paribas (Singapore Branch) is the Sole Global Coordinator of the issuance and, together with RHB OSK Investment Bank Berhad, it is one of the two International Selling Agents. PT BNP Paribas Securities Indonesia is one of the three Domestic Underwriters of the issuance, together with PT Mandiri Sekuritas and PT RHB OSK Securities Indonesia.2

SSMS has four plantation subsidiaries, whose plantations are located in Central Kalimantan:3

- PT Kalimantan Sawit Abadi (KSA);

- PT Mitra Mendawai Sejati (MMS);

- PT Ahmad Saleh Perkasa (ASP), and

- PT Sawit Mandiri Lestari (SML).

The company expects to raise Rp 1,000 billion (US$ 87.8 million) with the IPO.4 SSMS aims to utilize the net proceeds as follows:5

- 60.5% will be used for the development and planting of the existing landbank, acquisition of new land and the construction of new mills and supporting facilities of PT Sawit Mandiri Lestari and PT Ahmad Saleh Perkasa;

- 25.0% will be used for partial or full payment of PT Mitra Mendawai Sejati’s debt; and

- 14.5% will be used as working capital, in this case to purchase FFBs and fertilizer, and to finance general operation expenses.

The IPO of SSMS raises a number of governance and sustainability concerns which are discussed in the sections below.

Control of public shareholders over the company’s assets

The shareholder rights of public shareholders investing in SSMS are not adequately strong:

- Mr. Abdul Rasyid is the founder of SSMS. Through shareholdings of his family members, as well as four investment companies owned by his family members (PT Citra Borneo Indah, PT Prima Sawit Borneo, PT Putra Borneo Agro Lestari and PT Mandiri Indah Lestari), he at present controls 100% of the shares of the company. Following the IPO, 84.7% of the company’s equity will be retained under control of Abdul Rasyid through his family members. Prospective minority shareholders will thus have very limited opportunity to ensure that the company is being managed in their interest after the IPO.

6 - While SSMS is a plantation holding company and not a bank, SSMS provides significant loans to two external, related companies: PT Surya Borneo Industri and PT Citra Borneo Utama. The first company (which also is called PT Sawit Borneo Industri elsewhere in the Prospectus) is developing a bulking terminal and jetty facilities, and the second company is developing a palm oil refinery.

7The total value of the loans granted by SSMS to these two companies amounts to Rp 457.2 billion in total,8whereas the 18.4% shareholdings of SSMS and its subsidiaries in both companies have a value of Rp 95 billion.9Therefore, total investments in the two companies equal no less than 23.5% of the company’s total assets, making SSMS heavily reliant on the performance of these two unlisted external companies.10In addition, the loans are unsecured. For the public shareholders of SSMS this creates the risk that significant parts of the assets they invest in are fully outside their control.

Conflict of interest – Bank Mandiri

The dominant role of Bank Mandiri as lender to the company and its role as underwriter create a conflict of interest:

- Bank Mandiri accounts for 84.4% of the total liabilities of SSMS and for 50.7% of total equity and liabilities.

11SSMS is therefore heavily reliant on financing from the Indonesian state-owned Bank Mandiri.12SSMS’s reliance on a single creditor represents a serious governance risk because Bank Mandiri is firmly positioned to insist that SSMS’s management prioritizes repayment of its loans over the broader interests of the company, such as those of minority shareholders as well as sustainability interests. - Meanwhile, PT Mandiri Sekuritas, a subsidiary of Bank Mandiri, is also one of the three underwriters of the IPO. Of the proceeds of the IPO, 25% is scheduled to be used to repay debts of PT Mitra Mendawai Sejati, a subsidiary of SSMS.

13This debt is payable to Bank Mandiri.14PT Mandiri Sekuritas’ role in the IPO therefore represents a clear conflict of interest: as an underwriter, PT Mandiri Sekuritas has a duty to make an independent assessment of the value of the company’s shares in order to recommend to investors whether or not to buy the shares of SSMS. But at the same time, Bank Mandiri has a clear interest in maximizing the proceeds of the IPO, so that SSMS can repay its outstanding bank loans to Bank Mandiri.

Inadequate disclosure to investors

SSMS issued two different versions of its prospectus – one was released in English, and a Bahasa Indonesia version was published two days later.15 Remarkably, the Indonesian version is different from the English version. The Indonesian version presents a more complete list of permits, a more detailed description of related party transactions and includes a legal opinion from a SSMS lawyer.16 However, relevant information on applications with the Ministry of Forestry is missing from the Indonesian prospectus as well (see below).

No government authorization to develop most of its land bank

According to the prospectus, SSMS holds a total land bank of 78,071 ha in Kotawaringin Barat, Lamandau and Seruyan districts in Central Kalimantan.17 Additionally, SSMS has a management contract to manage all plantations of two external oil palm plantation companies: PT Tanjung Sawit Abadi and PT Sawit Multi Utama. The two companies have a combined land bank of 30,818 hectares in Central Kalimantan.18

The prospectus acknowledges that the company may not be able to secure legal access to its full land bank, because locally issued permits over certain portions of land have not been cleared by national level government agencies.19 Although SSMS has already planted 33,208 hectares, or 42.5% of its land bank,20 the company has yet to secure full authorization on the national level to use these lands for oil palm plantations.

Especially for forest areas, authorization is not granted automatically after local permits are obtained. Such lands are considered contested because the authorization may not be granted if certain portions of land are not legally eligible for authorization or if the application is inappropriate.

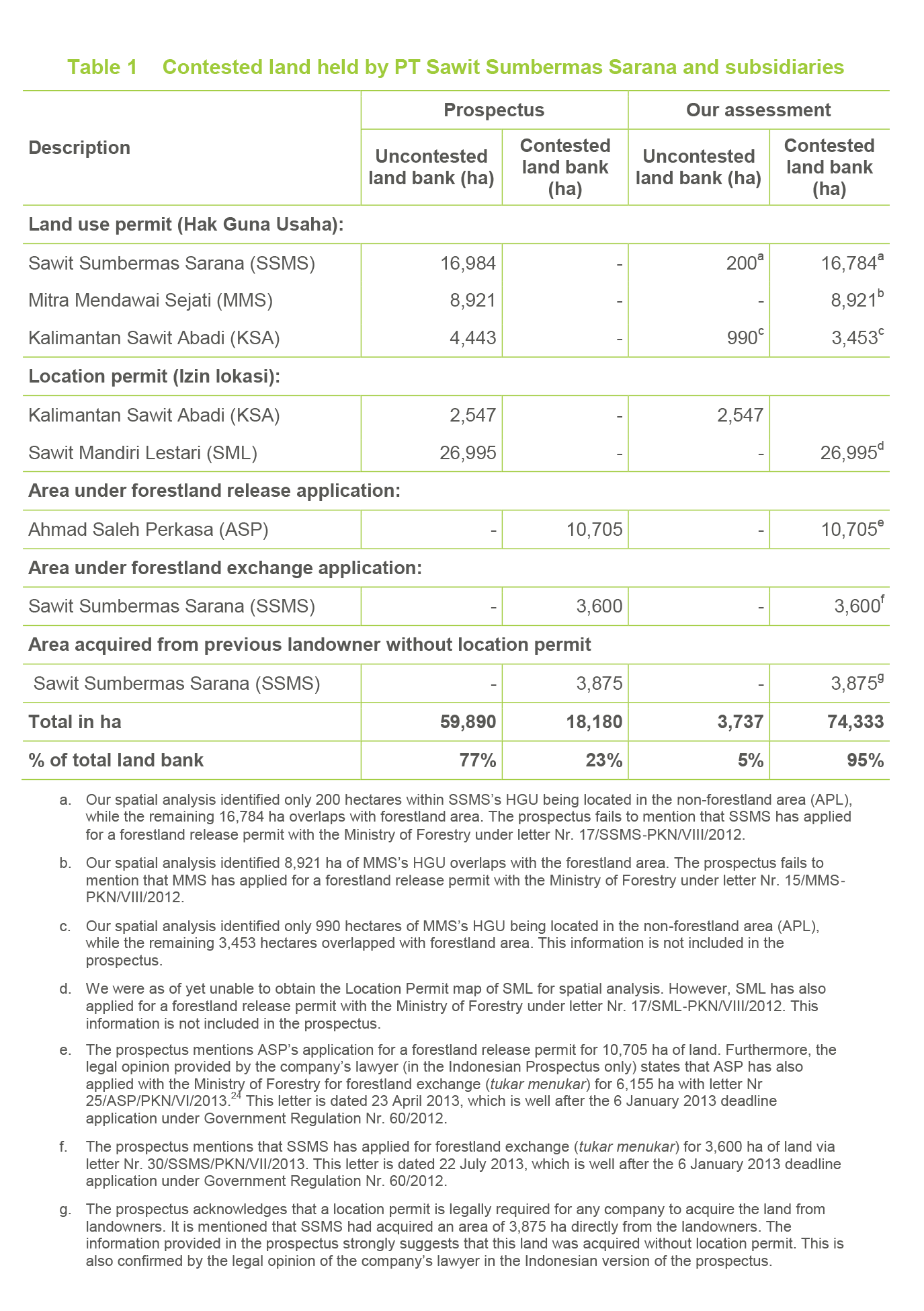

In the prospectus, SSMS reports it holds 18,180 ha of contested land, just under a quarter (23%) of its reported total land bank (78,071 ha). This involves three tracts of land, two of which (10,705 ha and 3,600 ha) reportedly overlap with forestland (kawasan hutan) under the jurisdiction of the Ministry of Forestry. The Ministry of Forestry can release such land for oil palm development, but only under certain terms and conditions. The third reported tract of contested land (3,875 ha) appears to have been acquired by the Group in non-compliance with laws pertaining to Location Permits.21

However, upon close scrutiny of the SSMS prospectus and data from the Indonesian Ministry of Forestry, we observed that the prospectus seriously underreports the percentage of the company’s landbank which is contested. The prospectus fails to mention that all of SSMS’s subsidiaries have applied for forestland release permits (Izin Pelepasan Kawasan Hutan or IPKH) or forest area exchange.22

Based on these applications and our spatial analysis,23 we assess that no less than 95% of SSMS’s total land bank is contested, which is dramatically larger than the share reported in the prospectus (23%). Our findings are presented in Table 1.

We conclude that for 74,333 ha, or 95% of the company’s total land bank, full authorization to use such lands for oil palm plantations has not been granted by central government agencies and – according to normal regulations – will not easily be granted either.

To get official approval to develop its land bank into oil palm plantations, SSMS is highly dependent on Government Regulation Nr. 60/2012, issued in July 2012. This regulation offered plantation companies a six-month window of opportunity (until January 2013) to apply for post hoc settlement with the Ministry of Forestry over forestland that had been occupied (cleared and planted) without prior Ministerial approval. If the application is eligible, and such land is mapped as Convertible Production Forest (HPK), the Ministry will issue a forestland release permit. For a significant part of its land bank, SSMS has applied for forestland release permits with the Ministry of Forestry. These applications are only partly mentioned in the prospectus:

- PT Sawit Sumbermas Sarana (SSMS) has applied for a forestland release permit with the Ministry of Forestry under letter Nr. 17/SSMS‐PKN/VIII/2012.

25This is not mentioned in the prospectus. - PT Mitra Mendawai Sejati (MMS) has applied for a forestland release permit with the Ministry of Forestry under letter Nr. 15/MMS‐PKN/VIII/2012.

26This is not mentioned in the prospectus. - PT Sawit Mandiri Lestari (SML) has also applied for a forestland release permit with the Ministry of Forestry under letter Nr. 17/SML‐PKN/VIII/2012.27 This is not mentioned in the prospectus.

- PT Ahmad Saleh Perkasa (ASP) has applied with the Ministry of Forestry for a forestland release permit for 10,705 ha of land under letter Nr. 02/ASP‐PKN/VIII/12.

28This is mentioned in the prospectus.29

Forestland release permits cannot be issued if the eligible land is mapped by the Ministry of Forestry as Production Forest (HP) or Limited Production Forest (HPT). In that case, the applicant is required to apply for a forestland area exchange arrangement (“tukar menukar”). Applicants must then propose appropriate sites to exchange their land with, within two years. Said land must cover 100% of the Production Forest (HP) or Limited Production Forest (HPT) area previously occupied without authorization. Exchange land must be located in a non-forestry development zone, which means that it is mapped as either Convertible Production Forest (HPK) or Other Land Use (APL).

According to the Indonesian version of the prospectus, SSMS has applied for an exchange arrangement (“tukar menukar”) for two tracts of land totalling 9,755 ha:

- PT Sawit Sumbermas Sarana (SSMS) has applied for forestland exchange for 3,600 ha of land via letter Nr. 30/SSMS/PKN/VII/2013. This letter is dated 22 July 2013.

30 - PT Ahmad Saleh Perkasa (ASP) has applied with the Ministry of Forestry for forestland exchange for 6,155 ha with letter Nr 25/ASP/PKN/VI/2013. This letter is dated 23 April 2013.

31

There are two problems with these applications: firstly, the applications were made in April and July 2013, well after the six months period stipulated in Government Regulation Nr. 60/2012, which ended on 6 January 2013. Secondly, to fulfill the conditions of the exchange arrangement, the company must acquire at least 9,755 ha of land eligible for exchange in Central Kalimantan. This poses a major challenge to the company because most areas mapped as APL and HPK in Central Kalimantan are already occupied by communities, settlements and other oil palm plantation companies, whilst the proposed exchange land must be demonstrably unencumbered with rights and claims. SSMS will thus have to purchase the proposed exchange land from the current landowners and occupants.

The prospectus does not present information on the funds that will be required to acquire land for the forestland exchange process. Based on the land procurement price paid by PT ASP in 2011, Rp 7.3 million per ha,32 the budget required by SSMS to acquire 9,755 ha is estimated at Rp 71.1 billion.

This budget equals 7% of the planned proceeds of the IPO. However, of the 74,333 ha of the company’s land bank which is contested (see Table 1), we think that significantly more than 9,755 ha could be located in areas mapped as Production Forest (HP) or Limited Production Forest (HPT). To get authorization to use this area for oil palm development, SSMS would then need to acquire considerably more land for the forestland exchange process. Investors therefore run the risk that a significant part of the IPO proceeds must be used solely to gain authorization by the central government for SSMS’s existing oil palm plantations – and not for expansion.

And investors run an even larger risk: given the fact that SSMS has applied for the forestland exchange process well after the six month period stipulated in Government Regulation Nr. 60/2012, investors run a serious risk that this authorization will not be granted at all for a significant part of the land bank of SSMS, including the parts already planted. This would mean, as described in the prospectus, that “the land must be returned to its original usage”.33 Oil palm would need to be replaced by forest again.

Illegal deforestation

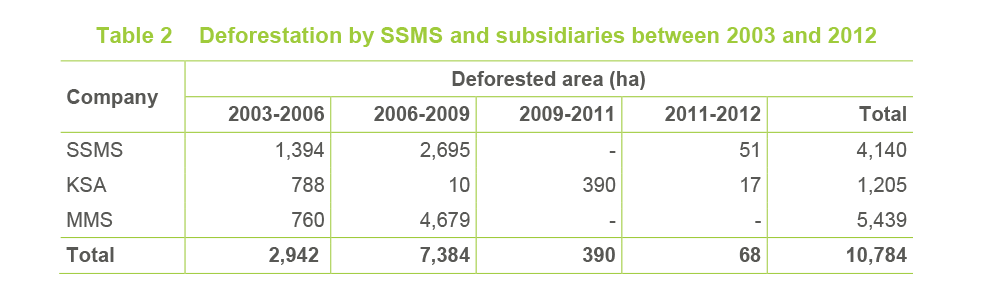

We overlaid the company’s land bank for which Hak Guna Usaha (HGU) are obtained (a total of 30,348 ha) with Landsat 5 and 7 satellite imagery (30m) from the Ministry of Forestry for 4 different time periods: 2003-2006, 2006-2009, 2009-2011 and 2011-2012. Based on these overlays, we estimate that SSMS and two of its subsidiaries, PT Kalimantan Sawit Abadi (KSA) and PT Mitra Mendawai Sejati (MMS) have jointly deforested approximately 10,784 ha in the period 2003-2012 (see Table 2).

The figures in Table 2 imply that over a third (35.4%) of SSMS’s HGU areas were deforested during this nine-year period. Because most of this HGU area was contested, without central government authorization for conversion to oil palm plantations (see Table 1), this deforestation was clearly illegal.

Limited commitment to HCVF conservation

The prospectus acknowledges that compliance with the principles of the Indonesian Sustainable Palm Oil Foundation (ISPO), which is legally required, may prevent the company from developing High Conservation Value Forest (HCVF).34 Voluntary commitment to the Roundtable on Sustainable Palm Oil (RSPO) implies similar impact and, contrary to ISPO, RSPO membership obliges the company to publicly consult stakeholders about upcoming new plantings. At present two subsidiaries (PT MMS and PT KSA) are ISPO certified. PT SSMS is RSPO certified, but not ISPO certified. The company mentions the intention to get all four plantation subsidiaries RSPO certified.35

RSPO is currently developing a standard procedure for companies to compensate potential HCV loss. Companies are required to report to RSPO how much land they have developed since 2010 without HCVF assessments. The prospectus states that the company is performing HCVF studies in all of its plantations and that the Group currently has 1,526 ha of land set aside for conservation.36 This translates into just 2% of the company’s claimed land bank.

Conversion of orangutan habitat in plantations

SSMS’s identifiable land bank was overlaid with the best available map of actual and potential orangutan habitat for Borneo island. This map was prepared some ten years ago, i.e. before the company commenced large-scale land clearing.37 We found that approximately 21,000 ha (or 44%) of SSMS’s identifiable land bank overlaps with actual and potential orangutan habitat. We estimate that two-thirds of this habitat had been converted into oil palm plantations by 2012.

A significant acreage of undeveloped orangutan habitat (approximately 7,000 ha) remains in PT ASP and in an undeveloped unit of PT KSA. The prospectus states that SSMS intends to use the net proceeds of the IPO, among others, for the development and planting of existing land bank, such as in PT ASP.38

The Indonesian version of the prospectus notes that the company may incur additional costs to comply with the requirements and implementation of a Memorandum of Understanding signed on June 11, 2011 between Wilmar International (the main customer of the company), the Central Kalimantan government and the Borneo Orangutan Survival Foundation on a program for long-term protection and conservation of orangutans. Through this MoU, parties aim to develop a pilot project for best practices in orangutan conservation in oil palm plantations in Central Kalimantan.39

Development of plantations on peatland

The prospectus reports that just 4% (1,328 ha) of the Group’s planted land bank is located on peat.40 We overlaid the identifiable land bank with the Wetlands International peatland map.41 Our analysis shows that while only 1% (209 ha) of SSMS’s planted land bank is located on peat, 14% of SSMS’s identifiable land bank (approx. 6,600 ha) contains undeveloped peatland.

Dependency on only two buyers

For its sales of crude palm oil, SSMS currently largely depends on two buyers: Wilmar (60.7% of total sales) and SMART (28.6%).42 Both companies are large, well-known palm oil traders with a broad customer base among the world’s largest consumer goods companies, such as Nestlé, Ferrero Rocher, Unilever, Mondelez and others. Increasingly, these companies are adopting sourcing policies or commitments that require the ability to trace palm oil to known suppliers in order to limit purchases of palm oil from companies connected to potential controversy (illegality, deforestation, peatland development and land conflicts).

These commitments have a strong impact on big traders such as Wilmar and SMART, which are forced to make similar commitments. Just last week, Wilmar International launched a new “No Deforestation, No Peat, No Exploitation” policy that aims to advance an environmentally and socially responsible palm oil industry.43

Given the serious governance and sustainability issues linked to SSMS and its subsidiaries, we consider it a serious risk for SSMS that its main buyers may feel obliged to end the commercial relationships with the company. In that case, the cash flow of SSMS would halt immediately as few other buyers are available on short notice.

All efforts are made to use reliable data sources and check findings. The authors of this report cannot guarantee that no errors were made in the analysis. In particular, no warranty regarding the accuracy or fitness for a purpose is given in connection with such information and materials. This document does not have any regard to the specific investment objectives, financial situation and particular needs of any specific recipient. It is for informational purposes only and is not intended to nor will it create or induce the creation of any binding legal relations. It does not constitute or form part of any offer or solicitation of any offer to buy or sell any securities.

References

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. iv.

- Lubis, A., “Sawit Sumbermas expects to raise Rp 1 trillion in IPO”, The Jakarta Post, 8 November 2013.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 39.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 142.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 107.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 143-144, F-176.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 107, F-105 – F-106.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. F-16 – F-17.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. F-16 – F-17.

- The company has secured short-term loans from Bank Mandiri with a total value of Rp 66 billion and long- term loans with a total value of Rp 1,125.6 billion. Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. F-129 – F-133.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 7.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. F-134 – F-136.

- The English version of the prospectus – the “Preliminary Offering Memorandum” – was made available on the SSMS website on 5 November 2013. The Bahasa version – the , “Prospektus Awal” – was issued on 7 November 2013.

- Sawit Sumbermas Sarana, “Prospektus Awal”, PT Sawit Sumbermas Sarana, 7 November 2013, p. 235- 265.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 4.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 144.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 18-20.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 5.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 3, 79.

- Data obtained from the Indonesian Ministry of Forestry, December 2013.

- Our spatial analysis is based on the following sources: PT Sumbermas Sarana Prospectus, land use permit and cadastral maps derived from the ArcGIS server of the National Land Agency (BPN) and the Forestland area map and deforestation time series maps derived from the ArcGIS server of Ministry of Forestry.

- Sawit Sumbermas Sarana, “Prospektus Awal”, PT Sawit Sumbermas Sarana, 7 November 2013, p. 256.

- Ministry of Forestry, “Matrik Permohonan Pelepasan Kawasan Hutan Keterlanjuran Sesuai Pp.60 Tahun 2012”, Kementerian Kehutanan Republik Indonesia, October 2013.

- Ministry of Forestry, “Matrik Permohonan Pelepasan Kawasan Hutan Keterlanjuran Sesuai Pp.60 Tahun 2012”, Kementerian Kehutanan Republik Indonesia, October 2013.

- Ministry of Forestry, “Matrik Permohonan Pelepasan Kawasan Hutan Keterlanjuran Sesuai Pp.60 Tahun 2012”, Kementerian Kehutanan Republik Indonesia, October 2013.

- Ministry of Forestry, “Matrik Permohonan Pelepasan Kawasan Hutan Keterlanjuran Sesuai Pp.60 Tahun 2012”, Kementerian Kehutanan Republik Indonesia, October 2013.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 3.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 3.

- Sawit Sumbermas Sarana, “Prospektus Awal”, PT Sawit Sumbermas Sarana, 7 November 2013, p. 256.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 4.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 19.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 111.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 112.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 18.

- Meijaard, E., Dennis, R. and Singleton, I. (2004) Borneo Orangutan PHVA Habitats Units: Composite dataset developed by Meijaard & Dennis [2003] and amended by delegates of the Orangutan PHVA Workshop, Jakarta, January 15-18, 2004 [Subsequently further updated by E. Meijaard).

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 39.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum – Indonesian version”, PT Sawit Sumbermas Sarana, 7 November 2013, p. 71.

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 101.

- Wahyunto, S. Ritung and H. Subagjo (2004). Peta Sebaran Lahan Gambut, Luas dan Kandungan Karbon di Kalimantan / Map of Peat land Distribution Area and Carbon Content in Kalimantan, 2000 – 2002. Wetlands International – Indonesia Programme & Wildlife Habitat Canada (WHC).

- Sawit Sumbermas Sarana, “Preliminary Offering Memorandum”, PT Sawit Sumbermas Sarana, 5 November 2013, p. 5.

- Wilmar International, “News Release: Wilmar International Announces Policy to Protect Forests and Communities”, Wilmar International, 5 December 2013.