Comprehensive Risk Analysis: Triputra Agro Persada

May 21, 2015

Triputra Agro Persada (Triputra/TAP) is a privately owned Indonesian palm oil and rubber plantation company. This Comprehensive Risk Analysis gives an overview of the company, delves into the environmental and social issues it faces, and presents a financial analysis of how sustainability risks may impact the bottom line.

Triputra Agro Persada (Triputra/TAP) is a privately owned Indonesian palm oil and rubber plantation company. The company has a land bank of approximately 300,000 hectares, of which around 164,000 ha is currently planted with palm oil. The company is one of the fastest growing palm oil companies in Indonesia, planting an estimated 100,000 ha from 2010 to 2014, and is aiming to expand its operations even further in the coming years. With 25 palm oil plantation subsidiaries, the company produced an estimated 323,000 tonnes of crude palm oil (CPO) in 2014. However, it is not active further downstream in the supply chain, selling all of its CPO to processors and traders.

As the palm oil sector undergoes radical transformation, Chain Reaction Research (CRR) assessed the sustainability and financial risks of Triputra’s policies and practices, based on compliance with national laws and regulations, customer sustainability policies, and certification standards. This report gives an overview of the company, delves into the environmental and social issues it faces, and presents a financial analysis of how sustainability risks may impact the bottom line.

A draft version of the sustainability risks identified in this report was sent to Triputra for review on April 10, 2015. Triputra representatives did not provide any specific information to CRR in response to the report’s findings before the time of publication.

Sustainability and Financial Risks

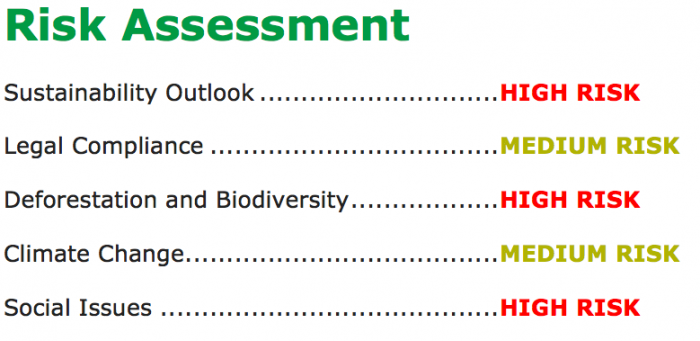

After extensive research, it is clear that Triputra has very little transparency about its sustainability policies, having not published an Annual Report since 2012. This lack of transparency alone poses a serious risk for the company with customers that require greater levels of openness. Nevertheless, the available information on Triputra’s record shows that the company faces serious issues in its operations, including deforestation, peatland development, and conflicts with local communities:

- From 2006 – 2014, Triputra’s plantation companies were responsible for 37,300 ha of documented deforestation in Indonesia. That is an area about twice the size of the island of Manhattan.

- Triputra’s current land bank covers 28,100 ha of potential and actual orangutan habitat, much of which has been converted to palm oil plantations.

- The company has also developed 16,300 ha of carbon-rich peatlands, which is the climate equivalent of the annual carbon pollution from 415,000 cars.

- Triputra and its subsidiaries have faced a number of conflicts with local communities and smallholders, several of which are still unresolved and on-going.

Assessing Triputra’s sustainability risk exposure has proved relatively challenging, as the group remains unlisted on any stock exchange, and therefore relatively opaque. Triputra’s latest publicly available Annual Report is from 2012. The group’s membership in the Roundtable on Sustainable Palm Oil (RSPO) since 2007 offered limited further insight into Triputra’s sustainability policies and practices. There is very little information available on assessments and/or conservation by the company of High Conservation Value (HCV) or High Carbon Stock (HCS) areas.

Triputra has been a member of the RSPO since June 2007. CRR’s findings indicate that Triputra has been substandard in delivering on the requirements of its membership, making the company vulnerable to being challenged through formal complaints, and to being suspended or expelled from the Roundtable’s membership.

These issues put the company at serious risk of losing market access to both traders and end users that have adopted No Deforestation, No Peat, No Exploitation policies and require transparency. In addition, Triputra faces some risk of losing access to global capital markets as investors tighten sustainability requirements going forward.

For example, Wilmar International, the world’s largest palm oil trader, is likely to be Triputra’s largest customer. At the end of 2012, Wilmar accounted for 44% of Triputra’s trade receivables. In December 2013, Wilmar committed to a No Deforestation, No Peat, No Exploitation policy for its supply chain. In January 2015, Wilmar disclosed most of its suppliers, on a palm oil mill level, that deliver to its refineries and oleochemical factories. This disclosure showed that eight of Triputra’s CPO mills sold to Wilmar facilities in the first nine months of 2014. Without reforming its sustainability practices and providing greater transparency, Triputra faces serious risk of losing its ability to sell to Wilmar.

To evaluate the potential financial impacts of these sustainability risks, CRR employed a model based on Triputra’s most recent financial statements from 2012, and estimated future earnings. CRR developed a baseline scenario in which sustainability issues have no impact on Triputra’s business, as well as three alternative scenarios that account for varying impacts. For each scenario, CRR identified the impact on key financial indicators such as Return on Equity, Return on Assets, leverage and profit margins. The analysis showed:

- Triputra could potentially lose global customers if its practices are not compliant with companies, such as Wilmar, that have adopted No Deforestation policies. This could result in a 10.4% loss in net income margin, a 2.3% drop in RoA, and 22.9% drop in RoE.

- Triputra could be required to acquire and reforest compensation land to be handed over to the government for its illegal occupation of forestland. This could result in an 8.4% loss in net income margin, a 2.6% drop in RoA, and 27.2% drop in RoE.

- Triputra could have to pay compensation costs to the RSPO for its deforestation since 2006, estimated to be approximately USD 30 million in fees. This would create a temporary drop in the net income margin, RoE, and RoA.

Conclusion

In all three of the alternative scenarios analysed by CRR, Triputra’s key financial indicators are depressed in comparison to the baseline scenario, while the debt-equity ratio increases to dangerously high levels. There is also a possibility that these different scenarios could occur simultaneously, creating cumulative and more serious impacts on financial indicators. Additionally, a significant risk embedded in all scenarios is that they could result in further damage to the reputation of Triputra Agro Persada among customers, investors, and the public. This could trigger additional scenarios with negative consequences on the financial indicators of the company, such as major customers cancelling purchasing contracts and banks and investors denying financing and investments.

Since Triputra is an upstream palm oil company that is dependent on processors and traders to buy its products, poor management of sustainability and governance issues on its plantations could have potentially significant negative financial impacts. This underscores the fact that addressing current and past sustainability issues – such as deforestation, peatland development, and social conflicts – will be critical to Triputra’s financial stability. The extent to which the company is able to successfully resolve these issues could significantly affect its financial performance in the coming years.

Disclaimer

This report and the information therein is derived from selected public sources. Chain Reaction Research is an unincorporated project of Climate Advisers, Profundo and Aidenvironment (individually and together, the “Sponsors”). The Sponsors believe the information in this report comes from reliable sources, but they do not guarantee the accuracy or completeness of this information, which is subject to change without notice, and nothing in this document shall be construed as such a guarantee. The statements reflect the current judgment of the authors of the relevant articles or features, and do not necessarily reflect the opinion of the Sponsors. The Sponsors disclaim any liability, joint or severable, arising from use of this document and its contents. Nothing herein shall constitute or be construed as an offering of financial instruments or as investment advice or recommendations by the Sponsors of an investment or other strategy (e.g., whether or not to “buy”, “sell”, or “hold” an investment). Employees of the Sponsors may hold positions in the companies, projects or investments covered by this report. No aspect of this report is based on the consideration of an investor or potential investor’s individual circumstances. You should determine on your own whether you agree with the content of this document and any information or data provided by the Sponsors.