Despite the increase in palm oil refining capacity covered by No Deforestation, No Peat, No Exploitation (NDPE) policies, eight of 25 largest refiners are still operating in the leakage market. This report analyzes the financiers and investors in these companies, updating a study published by Chain Reaction Research (CRR) in 2018. The financial institutions are also assessed by their palm oil policies, with the focus on their zero-deforestation pledges and policies that require clients to have supply chain transparency and traceability.

Download the PDF here: Asian Banks Continue to Finance the Palm Oil Refining Sector as Leakage Declines

Watch the recording of our webinar with Forests&Finance:

Key Findings:

- CRR identified USD 9.6 billion in loans and underwriting services toward leakage refiners in 2015-2021. The financing is higher compared to CRR’s 2018 leakage refiners study. However, this increase does not necessarily indicate a rising trend, but a continuation as the study analyzes a different set of companies. Asian banks have increased their exposure, while Western institutional investors have retreated.

- Salim Group has received the largest amount of financing at USD 5.7 billion, followed by Perkebunan Nusantara with USD 2.1 billion and Tunas Baru Lampung with USD 1.6 billion. For Gokul Agro and Kwantas, CRR identified relatively smaller amounts in terms of financing, USD 97 million and USD 73 million, respectively. The remaining six companies, BEST Group, Darmex Agro, Wings Group, Incasi Raya, Emami Agrotech, and Patanjali Ayurved, either do not disclose financial information or their disclosures do not include the names of their financiers.

- Indonesian banks are by far the largest financiers of non-NDPE refiners with USD 5.1 billion loans and underwriting services. 54 percent of the total financing came from Indonesian banks, followed by Japanese banks with USD 2.1 billion (23 percent). In shares and bonds, U.S. investors top the list with USD 140 million worth of shares and bonds in leakage refiners.

- The bank DBS contradicts its palm oil supply chain transparency policy by providing loans to Salim Group, whereas other financiers do not require their clients to have supply chain transparency. Among investors, BNP Paribas is the only one which requires palm oil supply chain transparency by their clients, yet the bank’s asset management arm holds shares in Salim Group. Although more than half of the banks and investors have zero-deforestation policies, there is a lack of policies requiring clients to have supply chain transparency.

The number of NDPE refiners increases, but leakage refining continues

In order to cut the direct link between deforestation and palm oil, the largest palm oil refiners have adopted No Deforestation, No Peat, No Exploitation (NDPE) policies since 2013. Refiners have committed to NDPE policies that cover their own plantations and the plantations of their third-party suppliers. This market mechanism functions best when the entire industry follows its commitments. However, non-cooperating refiners continue to leak unsustainable palm oil into the market.

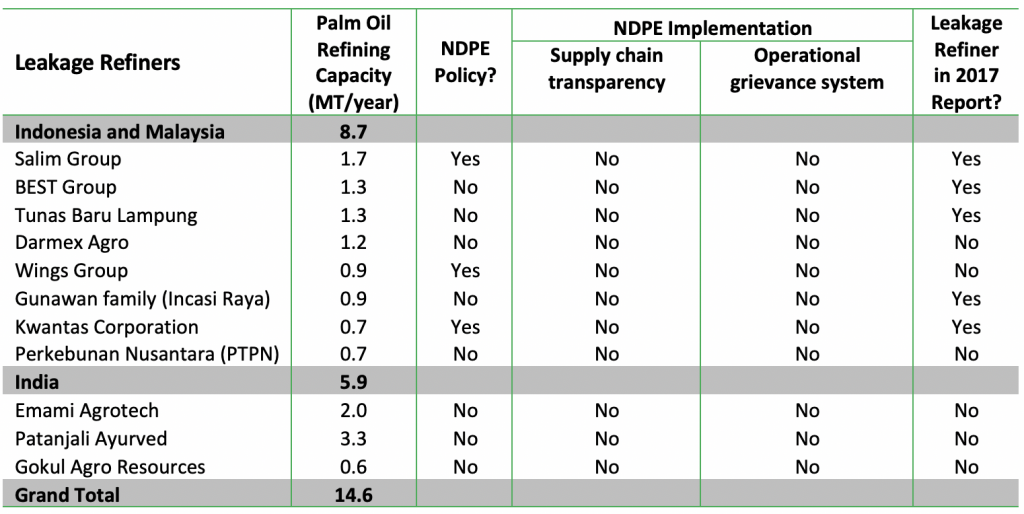

Palm oil refining capacity in Indonesia and Malaysia that is covered by NDPE policies increased from 74 percent in 2017 to 83 percent as of April 2020, as reported by CRR. CRR assessed refiners with NDPE policies based on implementation of the two main KPIs: 1) Supply chain transparency and 2) Operational grievance systems. The eleven largest refiners in Indonesia and Malaysia had NDPE policies in 2020, with Salim Group the only one of the 11 to fall short on its NDPE implementation. Seventy-eight percent of palm oil production was covered by refiners that are transparent about their supply chains and have an operational grievance system. Eight of the 25 largest refiners in Indonesia and Malaysia remain part of the leakage market, as they have no NDPE policy and/or fall short in NDPE implementation.

All eleven major refiners named in the April 2020 CRR report are still part of the leakage market at this moment in 2021. As of June 2021, no changes in policy or implementation compared to April 2020 were found for the refiners listed in Figure 1. Five of the 11 companies with palm oil refining operations were also listed as leakage refiners back in 2017. The 2020 CRR report revealed more leakage refineries as the selection was not only on the presence of an NDPE policy but also on its execution/implementation.

Figure 1: Leakage palm oil refiners

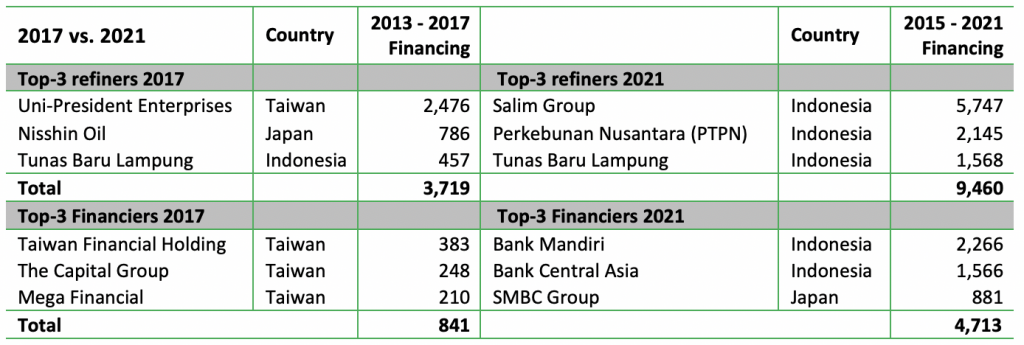

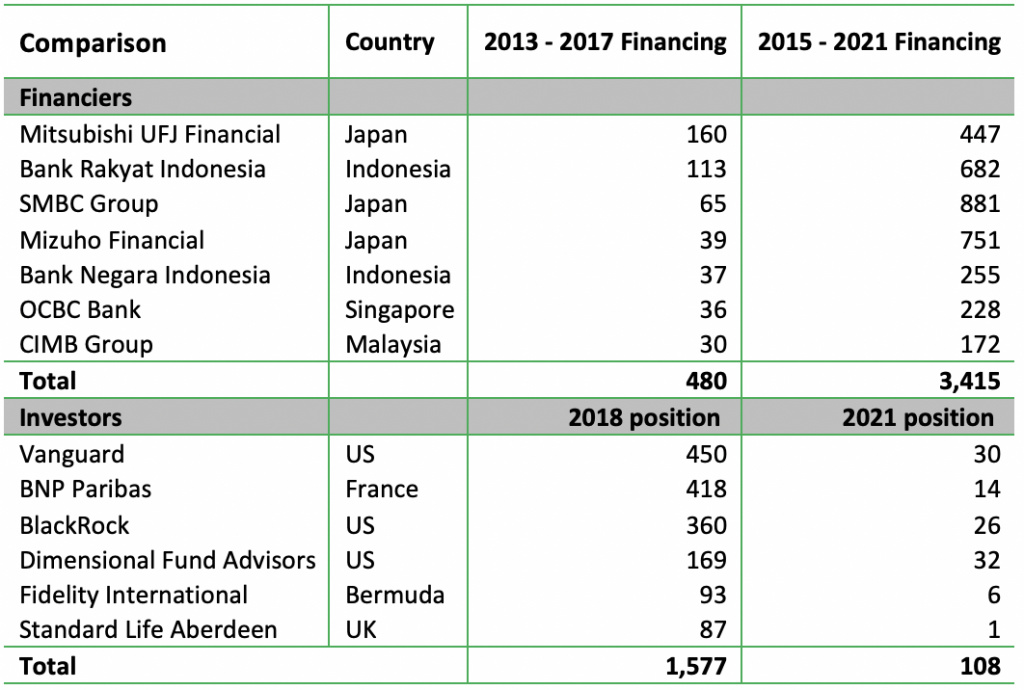

Regarding the financing received by leakage refiners, the 2018 CRR report served as a reference to track changes in the top financiers and their clients. Figure 2 compares the USD amount of financing (loans and underwriting) identified for 2013 – 2017 period with the current study findings for 2015 – 2021. The majority of the variation stems from Uni-President Enterprises becoming NDPE compliant since the original study, as well as Salim Group having more identified financing amounts. The comparison confirms that this flow of financing continues toward leakage refiners. However, since the analyzed companies are different (barring Tunas Baru Lampung), the increase in identified financing amount does not necessarily indicate a rising trend. Figure 3 presents the comparison of financiers and investors that are identified in both the 2018 report and in this current study. The latest findings for 2015 -2021 period are discussed in detail in the coming sections of the report.

Figure 2: Comparison of leakage refinery financing 2017 vs. 2021 (USD million)

Source: CRR 2018, Forests & Finance, Refinitiv Eikon viewed in May 2021, Company reports

Figure 3 shows increased financing flows (loans and underwriting) from Asian banks, while Western investors seem to have reduced their investments. Especially on the investments side, Uni-President Enterprises becoming NDPE compliant after 2017 meant that a large portion of leakage refiner shareholdings by Western investors are no longer in the leakage market.

Figure 3: Comparison of financiers and investors 2017 vs. 2021 (USD million)

Source: CRR 2018, Forests & Finance, Refinitiv Eikon viewed in May 2021, Company reports

Leakage refiners received USD 9.6 billion in financing, majority provided by Indonesian and Japanese banks

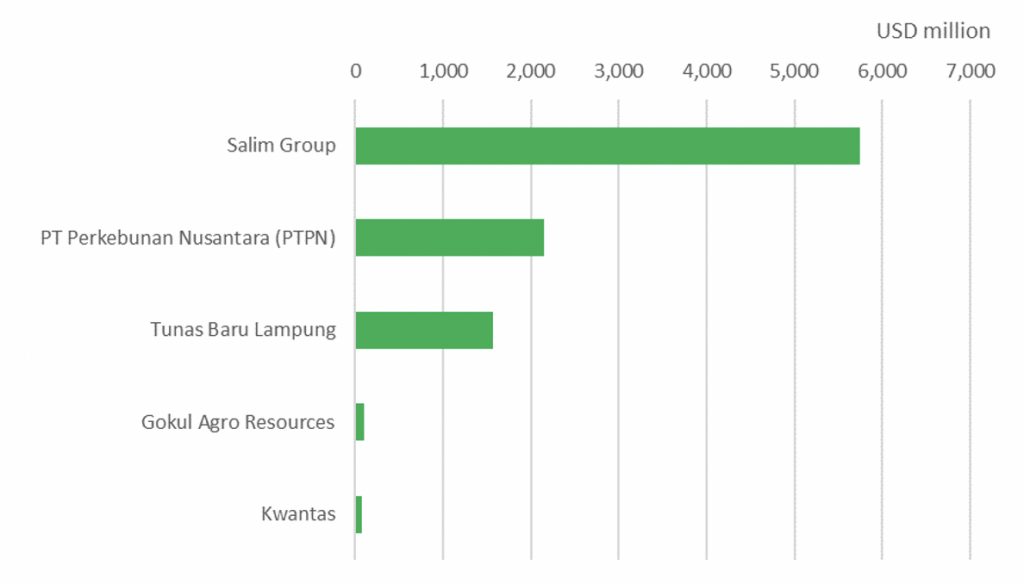

Between 2015 and 2021, a total of USD 9.6 billion worth of loans and underwriting services were identified for five out of the 11 leakage refiners on our list. Salim Group received the largest amount of financing at USD 5.7 billion, followed by PTPN with USD 2.1 billion and Tunas Baru Lampung with USD 1.6 billion. For Gokul Agro Resources and Kwantas Corporation, CRR identified relatively smaller amounts in terms of financing, USD 97 million and USD 73 million, respectively (see Figure 4). The remaining six companies, BEST Group, Darmex Agro, Wings Group, Incasi Raya (Gunawan family), Emami Agrotech, and Patanjali Ayurved, either do not disclose financial information or their disclosures do not include the names of their financiers.

Figure 4: Total loans and underwriting by company (2015-2021)

Source: Forests & Finance, Refinitiv Eikon viewed in May 2021, Company reports

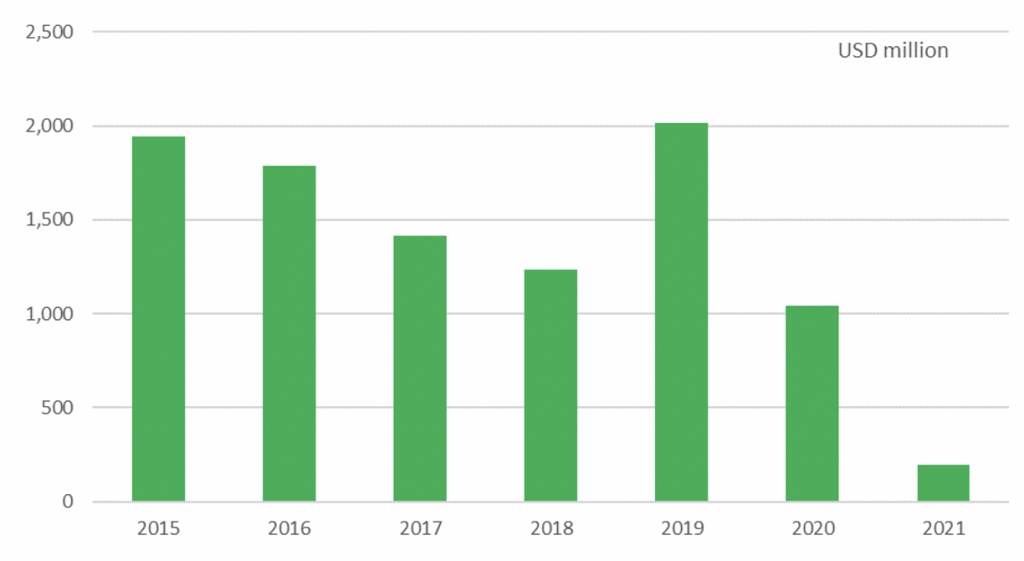

An annual average of USD 1.5 billion financing was identified as financing for leakage refiners. Figure 5 shows the yearly progress of identified loans and underwritings where the increase in 2019 could be explained by the renewal (and increase) of Salim Group’s corporate loan from Bank Central Asia. The main reason behind the still small amount of new identified financing in 2021, apart from being only five months in, is that the major source of financial information for these companies is their annual reports, which will not be available until 2022.

Figure 5: Total loans and underwriting by year (2015-2021)

Source: Forests & Finance, Refinitiv Eikon viewed in May 2021, Company reports

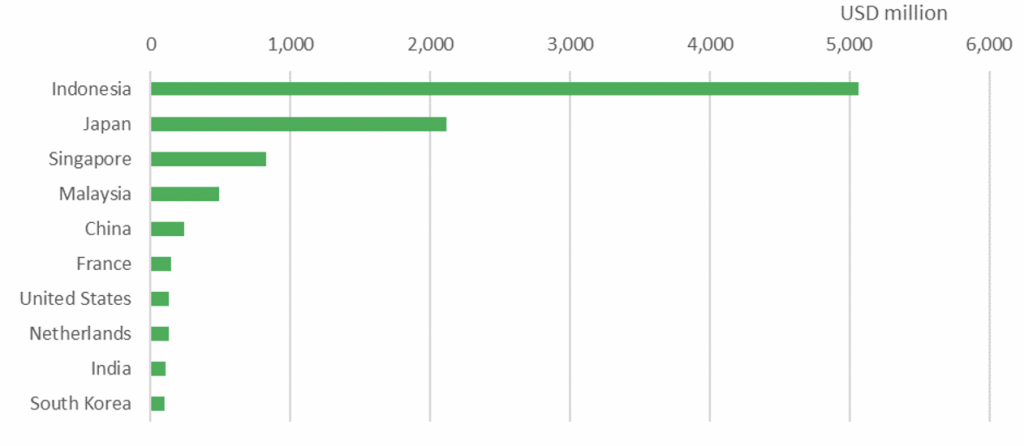

Indonesian banks are by far the largest financiers with USD 5.1 billion of identified financing. Fifty-four percent of the total financing came from Indonesian banks, followed by Japanese financial institutions with USD 2.1 billion (23 percent) and Singapore with USD 0.8 billion (nine percent) as the top three. Only five percent of the total identified financing came from countries outside of the East Asia region.

Figure 6: Total loans and underwriting by country (2015-2021)

Source: Forests & Finance, Refinitiv Eikon viewed in May 2021, Company reports

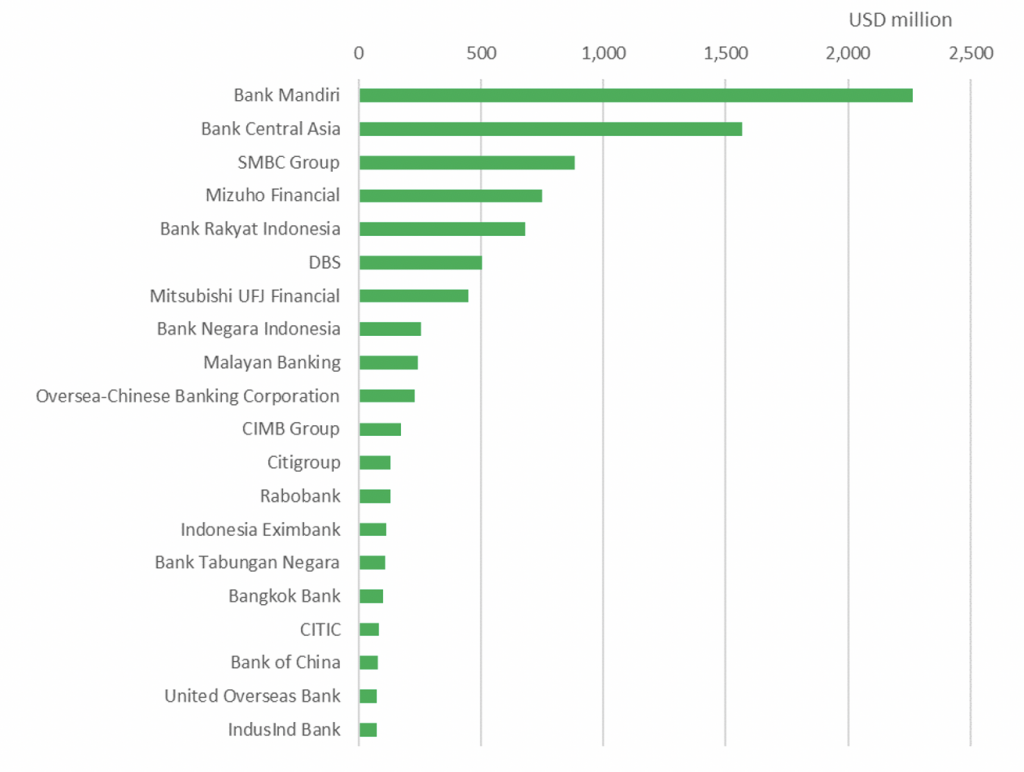

Indonesian government-owned Bank Mandiri tops the list of financiers with USD 2.3 billion. Bank Central Asia, another Indonesian bank in which the owner of Salim Group, Anthoni Salim, also has a 1.8 percent stake, provided the second-largest financing with USD 1.6 billion. Japanese banks SMBC, Mizuho, and MUFG are also active in financing leakage refiners in Indonesia and Malaysia. Outside of the East Asia region, Citi (United States) and Rabobank (Netherlands) provided USD 130 million each, whereas French banks BPCE Group and BNP Paribas both provided USD 66 million.

Figure 7: Total loans and underwriting by financier (2015-2021)

Source: Forests & Finance, Refinitiv Eikon viewed in May 2021, Company reports

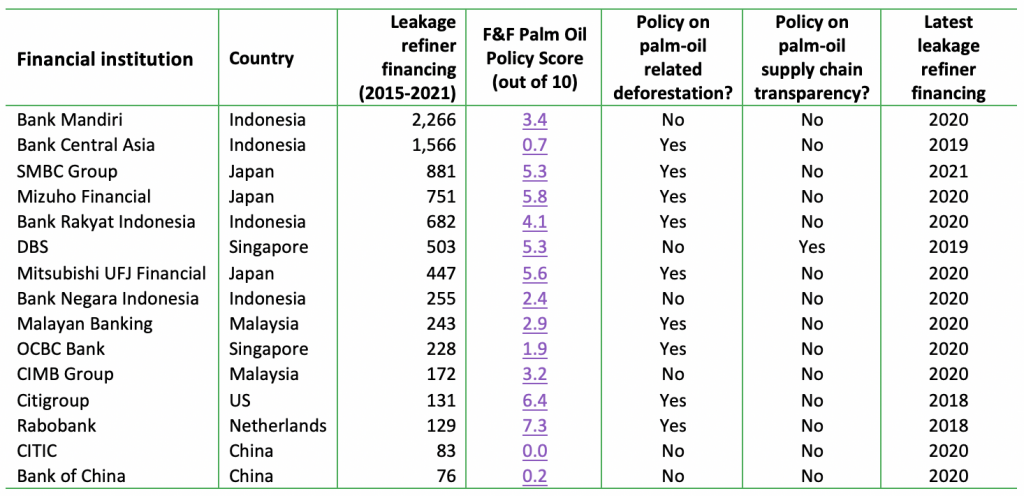

DBS bank contradicts its palm-oil supply chain transparency policy with loans provided to Salim Group, whereas other financial institutions assessed by Forests & Finance (F&F) lacks the policy all together. According to the 2021 update of F&F financing data and bank assessments, including 15 of the top-20 leakage refiner financiers, 9 of them have a zero-deforestation (F&F criteria #1) policy on palm-oil related activities (see Figure 8). Only DBS bank has also a palm-oil supply chain transparency and traceability policy (F&F criteria #30), which is crucial in countering the leakage palm-oil market (see Appendix).

Figure 8: Forests & Finance bank policy assessments (June 2021)

Source: Forests & Finance, Refinitiv Eikon viewed in May 2021, Company reports

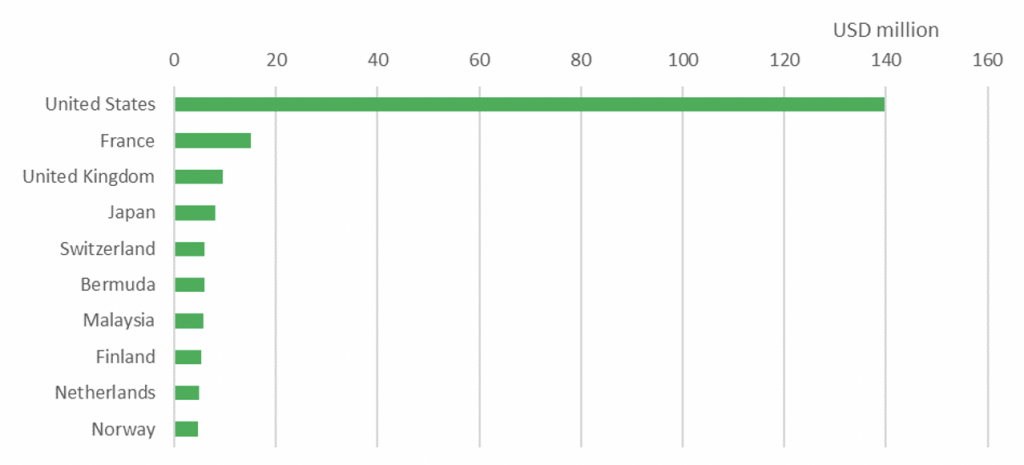

U.S. investors are by far the largest

While the financing side (loans and underwriting services) was dominated by banks from East Asia, 93 percent of institutional investments came from outside the region. Investors from United States hold USD 140 million worth shares and bonds of Salim Group, Kwantas and Tunas Baru Lampung as per latest filings. The most likely reasons why there are minimal identified institutional investments from East Asia are that majority of the big investors in the target companies are individuals and that the filings from institutional investors in the region are less common.

Figure 9: Total shareholding and bondholding by country (latest filings)

Source: Forests & Finance

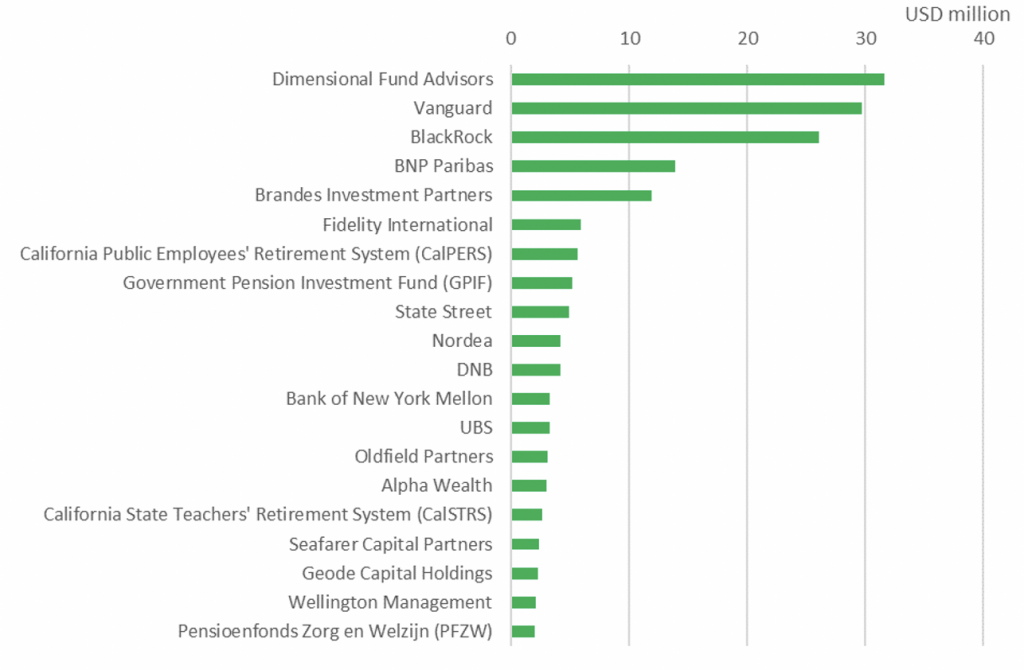

Figure 10 shows the top 20 investors in leakage refiners with U.S. investors Dimensional Fund Advisors, Vanguard, and BlackRock topping the list with USD 31.6 million, USD 29.7 million, and USD 26.0 million investments, respectively. As presented in Figure 3, these amounts are much lower than 3-4 years ago, mainly due to Uni-President Enterprises becoming NDPE compliant.

Figure 10: Total shareholding and bondholding by investor (latest filings)

Source: Forests & Finance

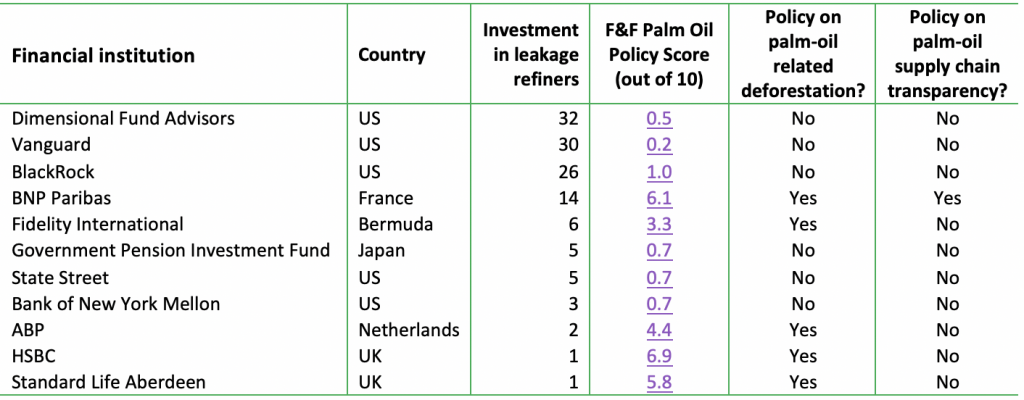

BNP Paribas is the only current investor in leakage refiners with a policy on palm oil supply chain transparency. Figure 11 shows that only five of 11 leakage refiner investors have zero-deforestation policies on palm oil-related activities.

Figure 11: Forests & Finance bank policy assessments (June 2021)

Source: Forests & Finance

Financing for leakage refiners continues while banks lack transparency policies

In light of the findings in this report, CRR concludes that, although the leakage market has shrunk compared to 2017, financing flows and investments toward leakage refiners continue. Although refiners on the leakage list have significantly changed, altering the scope of the analysis, seven financier institutions and six investors identified back in 2018 are still actively financing and investing in leakage refiners (Figure 3). Asian banks have increased their exposure, while shareholding/bondholdings by Western investors have declined. The recently updated policy assessments by Forests & Finance show that only two out of 26 financiers and investors have policies that require palm oil-related clients (or invested companies) and their suppliers to ensure supply chain transparency and traceability. The lack of supply chain policies creates room for financing and investments to continue flowing to leakage refiners.

Appendix: Criteria #30 in Forests & Finance methodology

Criteria 30: Companies and their suppliers must ensure supply chain transparency and traceability

“The financial institution should require that the companies it finances or invests in are transparent on their supply chains and have a time-bound plan to ensure that all the forest-risk commodities they buy, process and/or sell can be traced back to a specific farm, plantation or land-based operation of one of their suppliers. This requirement should also apply to the company’s subsidiaries and direct and indirect suppliers. For companies operating in, or sourcing from, the cattle sector in Brazil, this means that they can provide full traceability through GTAs of all intermediates in the supply chain. Many companies which have adopted No Deforestation, No Peat, No Exploitation (NDPE) policies have increased their supply chain transparency by publishing detailed lists of their suppliers, including direct suppliers, indirect suppliers with processing facilities, and raw material producers.”