China is a key market for palm oil (PO), palm kernel oil (PKO) and derivatives from Indonesia and Malaysia. This paper maps the role of the Chinese market and Chinese actors along the palm oil supply chain, from upstream production to midstream trading to downstream consumption, as well as the position of Chinese financial institutions in these different segments.

Download the PDF here: China, the Second-Largest Palm Oil Importer, Lags in NDPE Commitments and Transparency

Key Findings:

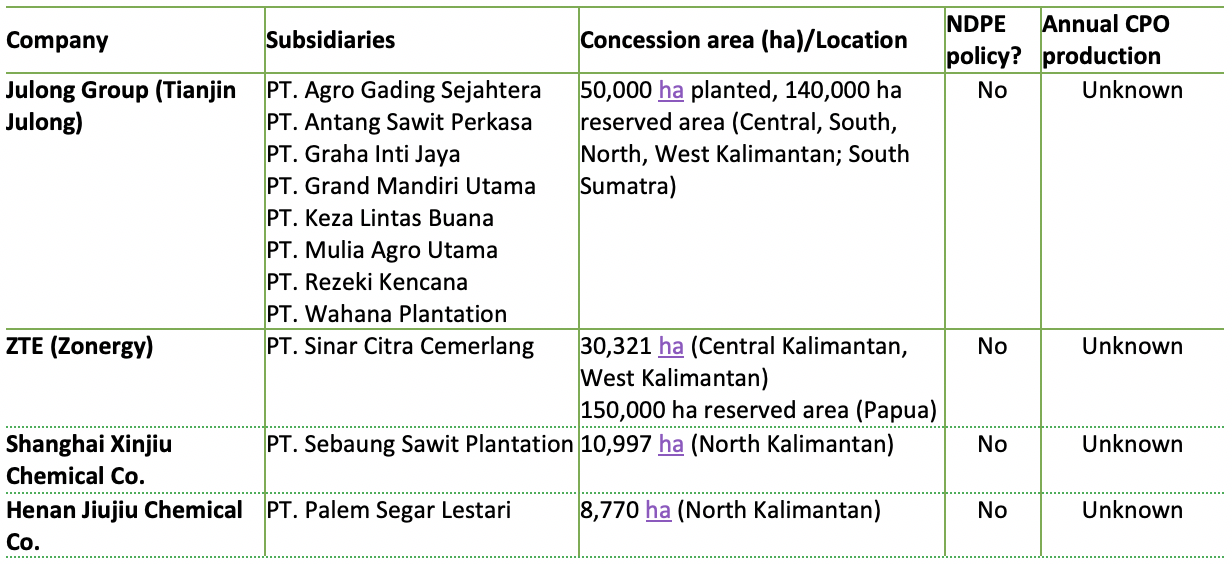

- Four Chinese companies operate palm oil plantations in Indonesia on 100,000 ha, with a much larger landbank. Julong Group (Tianjin Julong), ZTE (Zonergy), Henan Jiujiu Chemical Co. and Shanghai Xinjiu Chemical Co. lack No Deforestation, No Peat, No Exploitation (NDPE) policies and three of the companies have seen documented sustainability issues.

- In 2019, China was the second-largest importer of palm oil with a share of 13 percent and the third-largest consumer globally. Moreover, the country imports large volumes of palm kernel oil and palm oil derivatives, including palm fatty acid distillates (PFAD) for the chemical industry, palm kernel expeller for use as a high-protein animal feed, and biodiesel.

- Seven of the top-10 suppliers of Indonesian palm oil to China have NDPE policies. Leakage refiners without an NDPE policy or those lagging in their implementation accounted for at least 12 percent of Indonesian palm oil supplies to China.

- Eighty percent of palm oil is consumed as edible oil in China while 20 percent is used in industrial processes. Palm oil competes with soybean oil as a key edible oil, accounting for around one-fifth of edible oil consumption. It is used predominantly for instant noodles, processed foods, frying, and industrial baking. Palm-related policies and transparent reporting are exceptions.

- The launch of the China Sustainable Palm Oil Alliance in 2018 led to a rapid growth in the number of Chinese RSPO members. However, with a share of around 2 percent certified palm oil use by mid-2020, it is unlikely that they achieved the 10 percent goal in 2020.

Chinese banks provided USD 3.9 billion in credit to upstream palm oil companies. In comparison with financial institutions from other Asian countries, China plays a less important role, accounting for 7 percent of upstream palm oil financing between 2013-2019. Chinese banks have so far not published ESG risk mitigation policies and standards for clients in deforestation-risk sectors.

China is a key actor in the global palm oil supply chain

China is now the second-largest importer and third-largest consumer of palm oil in the world. Chinese companies are present in all segments of the international palm oil supply chain, from upstream production to midstream refining and trading to downstream processing. This role includes investments in palm oil plantations in Indonesia as well as large imports and consumption of palm oil, especially as an edible oil, driven by a large and growing population. Palm oil demand in China depends primarily on uses in food and oleochemicals.

Chinese plantation companies active in Indonesia

Palm oil production in Kalimantan and Sumatra

Subsidiaries of four Chinese companies operate palm oil plantations in Indonesia. Data availability in relation to subsidiaries, concession sizes, planted area, and production of crude palm oil (CPO) is limited. The companies’ plantations and reserve areas are located in Kalimantan, Papua and Sumatra (Figure 1). None of the four companies has a No Deforestation, No Peat, No Exploitation (NDPE) policy in place.

Figure 1: Chinese companies operating oil palm plantations in Indonesia

Sources: Company websites; Notary Acts Indonesia.

Links to deforestation, fires, and community rights breaches

Julong Group’s plantations have been linked to widespread fire alerts in recent years. Julong Group is involved in the entire palm oil value chain, including cultivation, oils and fats processing, port logistics, trade and merchandising, R&D, branded edible oil, and financial service. The group’s palm oil plantations are organized under Julong Indonesia. According to the company, plantations in Kalimantan and Sumatra cover 50,000 hectares (ha) with an additional 140,000 ha reserved area. Greenpeace documented fires on 6,800 ha of Julong Group’s plantations between 2015-2018 and an additional 263 ha in the first nine months of 2019. Its subsidiaries PT Palmina Utama (PT PU) and PT Kalimantan Lestari Mandiri have been subject to court actions over fires. PT PU has reportedly been charged with an IDR 22.3 billion (USD 1.6 million) fire-related fine.

Julong Group’s subsidiary PT. Rezeki Kencana (PT. RK) is one of the plantation companies that received a permit inside a protected area in Indonesia. The plantation in Kubu Raya district (West Kalimantan), where it has been operating since 2010, overlaps with the protected Sungai Arus Deras forest. Forest and peat in the plantation have been cleared for palm oil and local communities have been deprived of their rights. Around 2,600 ha of land belonging to the people of Kampung Baru Village and Jangkang II Village overlap with PT. RK’s plantation. PT. RK cleared 2,600 ha of land for palm trees previously used by local farmers without their free, prior, and informed consent (FPIC). In early 2020, the Indonesian Supreme Court declared that plantation companies’ operations inside protected forests are illegal. Civil society organizations called on the Indonesian government to review plantation permits in protected areas accordingly.

Tianjin Julong’s membership in the Roundtable on Sustainable Palm Oil (RSPO) was suspended in 2017. In the SPOTT ESG Policy Transparency Assessment, Tianjin Julong Group has one of the lowest scores at less than 1 percent. Julong palm oil subsidiaries are included in the supply chains of many international downstream companies, such as Avon, Johnson & Johnson, Kellog’s, L’Oréal, Nestlé, Pepsico, and Unilever.

The Indonesian plantations of Shanghai Xinjiu Chemical Co. and Henan Jiujiu Chemical Co. saw widespread deforestation and peat conversion in 2019 and the first half of 2020. CRR research documented 2,077 ha of peat and peat forest being cleared on the PT. Sebaung Sawit concession in North Kalimantan during those 18 months. On the Palem Segar Lestari plantation, 821 ha of peat and peat forest were cleared. The plantations do not operate their own mills and therefore are not included in supplier lists. It remains unclear where the fresh fruit bunches (FFB) are processed.

ZTE, Henan Jiujiu Chemical Co. and Shanghai Xinjiu Chemical Co. are not members of the RSPO and have not been evaluated by SPOTT on their ESG policy transparency.

China is a key market for palm oil and derivatives

Palm oil imports and consumption are growing, influenced by market and policy developments

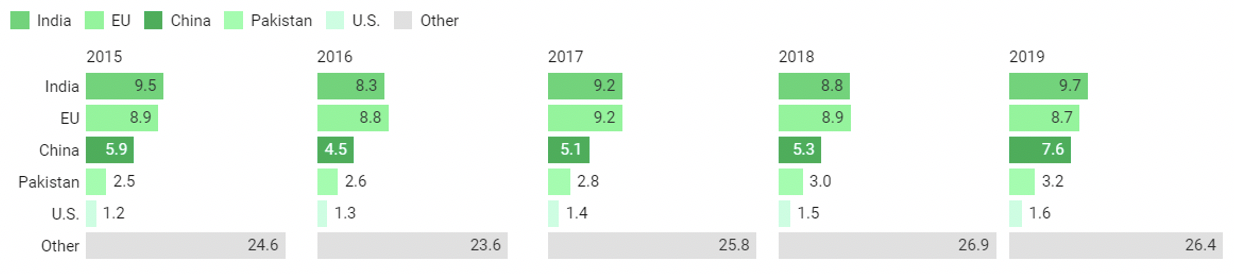

China has become one of the top importers and consumers of palm oil and derivatives worldwide. In 2019, China was the second-largest importing country of palm oil with a share of 13 percent (7.6 million tons), and the largest importer of palm kernel oil with a share of 29 percent in global imports (930,000 tons).

Figure 2: Top-5 palm oil importers globally 2015 to 2019 (million tons)

Note: Imports of individual EU member states have been summed up, making the region the 2nd largest importer. Source: ITC TradeMap (2020).

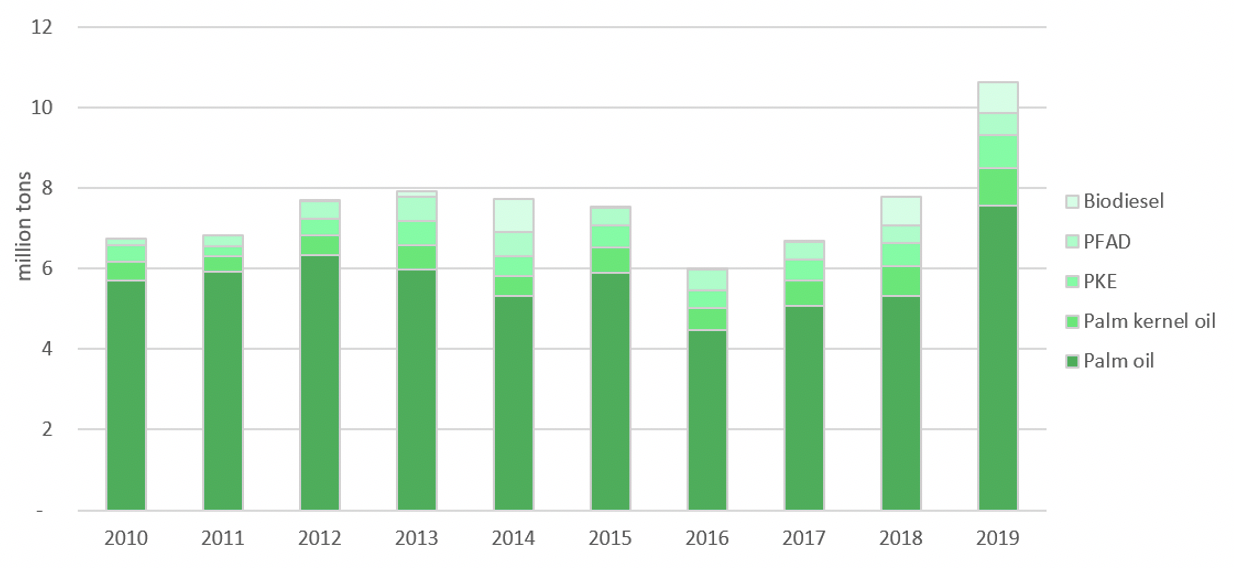

Moreover, the country’s imports of palm fatty acid distillates (PFAD) — a by-product of the oil refining process which is used as a raw material for the oleochemicals industry including biodiesel, in animal feed, and the laundry soap industry — were the third-largest globally with a share of 9 percent (543,000 tons). Imports of palm kernel expeller (PKE) for use as a high-protein animal feed totaled 833,000 tons in 2019, making China the fifth-largest global importer in 2019 (Figure 3).

In all four segments, the leading palm oil producers Indonesia and Malaysia account for more than 95 percent of Chinese supplies. Looking at consumption, China is now the third-largest consumer of palm oil behind Indonesia and India, as well as the third-largest consumer of palm kernel oil behind Indonesia and Malaysia.

Trade in palm oil, palm kernel oil, and derivatives is influenced by various market- and policy-driven factors (Figure 3). The dip in Chinese imports after 2015 was likely linked to the introduction of a limitation of trade financing for Chinese commodity imports, driving the withdrawal of importers from the market. Meanwhile, the increase in imports since 2018 has been likely driven by the decrease in soy imports because of the U.S.-China trade war. At the same time, demand for ready-made products like instant noodles and fast food is increasing in China. The COVID-19 pandemic led to a drop in imports at the beginning of 2020. However, they recovered during the course of the year, driven also by increased home cooking.

Figure 3: Chinese imports of palm oil, palm kernel oil, palm oil-based products, 2010 to 2019

Source: ITC TradeMap (2020).

Palm oil imports to China are expected to further increase in the coming years. With the U.S.-China trade war remaining unpredictable and the EU Commission planning to phase out palm oil-based biofuels by 2030, China is an attractive growth market for Indonesia. A growing economy will likely increase demand for ready-made and fast foods for which palm oil is a widely used ingredient. At the same time, China removed import quotas for palm oil in 2019. Moreover, the impact of the African Swine Flu outbreak in China favored imports of palm oil in recent years. The significant loss in the country’s pig herd meant that demand for soybean meal also plunged, causing soybean oil to lose its price advantage over palm oil. However, this dynamic may reverse course as pig herds are recovering.

Additionally, the Chinese government reportedly plans to move away from genetically modified (GM) soybean oil, with consumer caution towards GM products as a likely driver. Such a move would likely result in a further shift to palm oil for food products.

Majority of Indonesian palm oil exports to China covered by NDPE policy commitments, but leakage persists

As China sources the vast majority of palm oil and derived products from Indonesia and Malaysia, most imports are covered by NDPE policies of supplying traders and refiners. With palm oil as the key product, Indonesia accounted for 71.2 percent of palm oil supplies in 2019 while Malaysia was responsible for 27.4 percent.

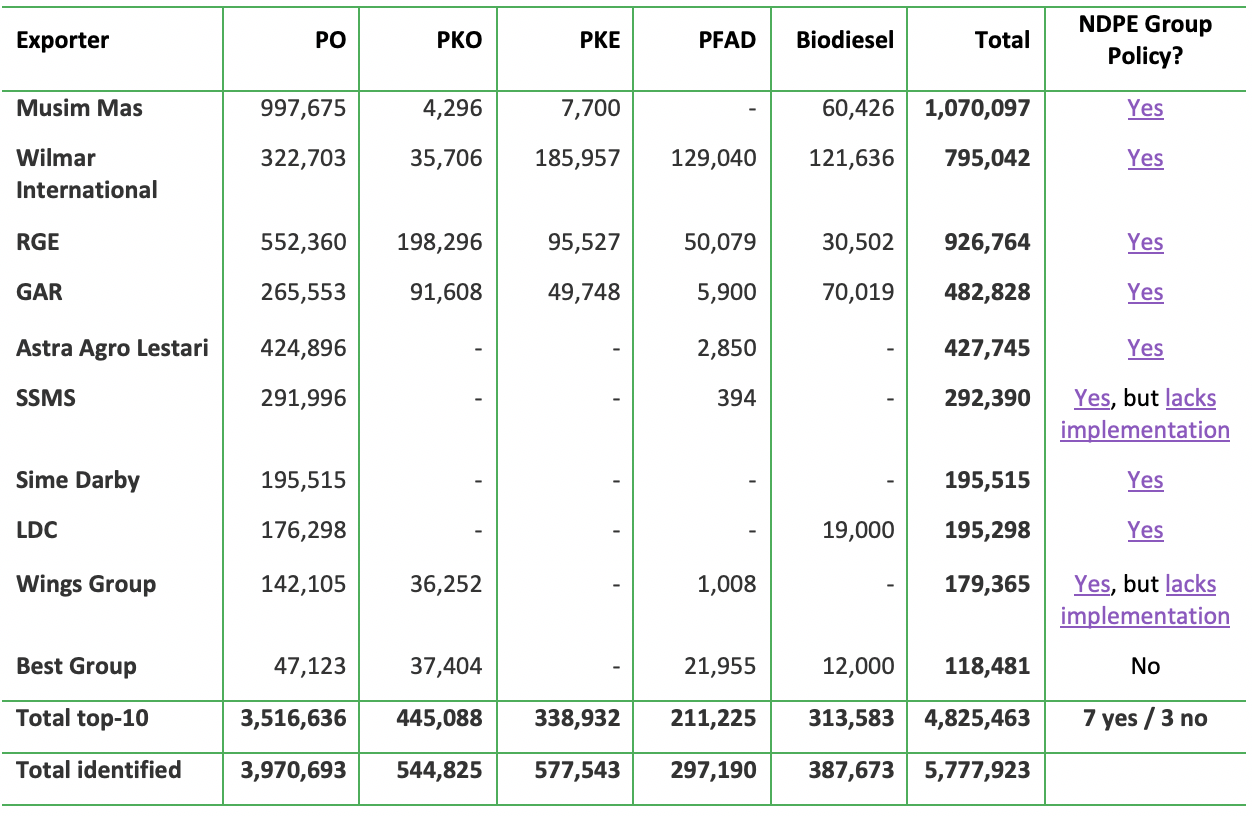

Of the top-10 Indonesian suppliers during the 12 months from July 2019 to June 2020, seven have NDPE policies (Figure 8). The top-5 exporting groups to China were Musim Mas (1.1 million tons), Wilmar International (795,000 tons), Royal Golden Eagle Group (RGE, including Asian Agri and Apical) (927,000 tons), Golden Agri Resources (GAR) (483,000 tons), and Astra Agro Lestari (428,000 tons). These companies, which account for around two-thirds of Indonesian exports to China, all have NDPE policies (Figure 4).

Figure 4: Top-10 Indonesian palm oil exporting groups to China, July 2019-June 2020 (tons)

Note: trade data for individual companies may not be complete. Sources: Indonesian trade data, corporate websites, CRR paper on leakage refiners (2020).

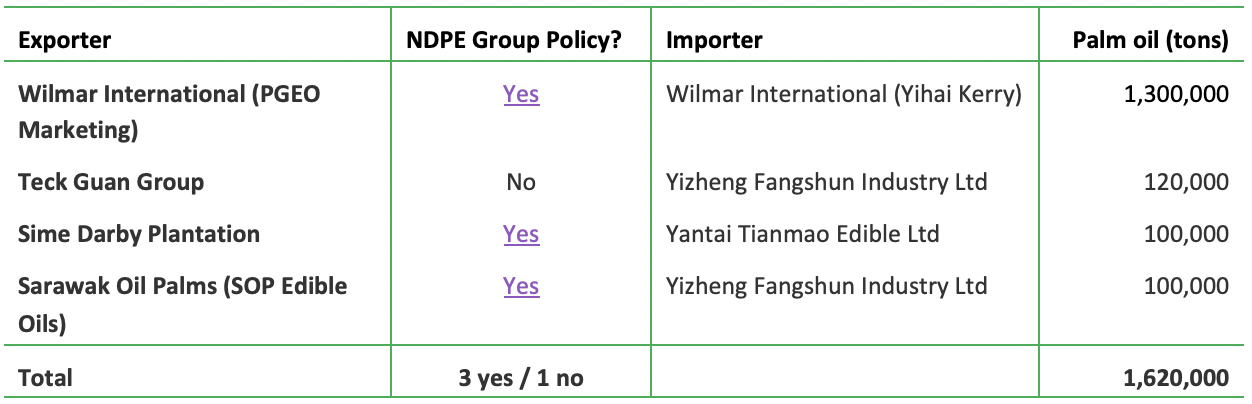

Information on Malaysian suppliers, which accounted for more than a quarter of Chinese imports in 2019, is more difficult to access. In March 2019, three Chinese importers signed forward-looking purchase agreements for a total of 1.62 million tons of palm oil from four Malaysian suppliers (Figure 5).

Figure 5: Malaysian suppliers in purchase agreements with Chinese buyers, March 2019 (tons)

Source: The Edge Markets (March 2019), CRR paper on leakage refiners (2020).

While an NDPE policy demonstrates awareness of the serious sustainability issues linked to palm oil production, relying on only the policy is not a guarantee for compliance. Large NDPE suppliers, including Wilmar, GAR and Sime Darby, have also been repeatedly linked to environmental and human rights issues in the recent past.

Four of the top exporters of palm oil and derivatives from Indonesia and Malaysia to China fall into the category of leakage refiners. Best Group and Teck Guan Group have no NDPE policy, while Wings Group and SSMS have policies but lack in implementation as transparency on supply chains and grievances is missing. These groups accounted for 10.2 percent of the identified Indonesian exports to China in 2019. This share increases to at least 12.4 percent when looking at a longer list of Indonesian palm oil suppliers to China, as additional large leakage suppliers in the top-25 include Darmex Agro, Incasi Raya, PT Perkebunan Nusantara (PTPN), Salim Group, and Tunas Baru Lampung. These actors are among the five largest leakage refiners of Indonesia and Malaysia.

Large players dominate Chinese palm oil import and processing, but overall domestic trading and processing is fragmented among a large number of actors

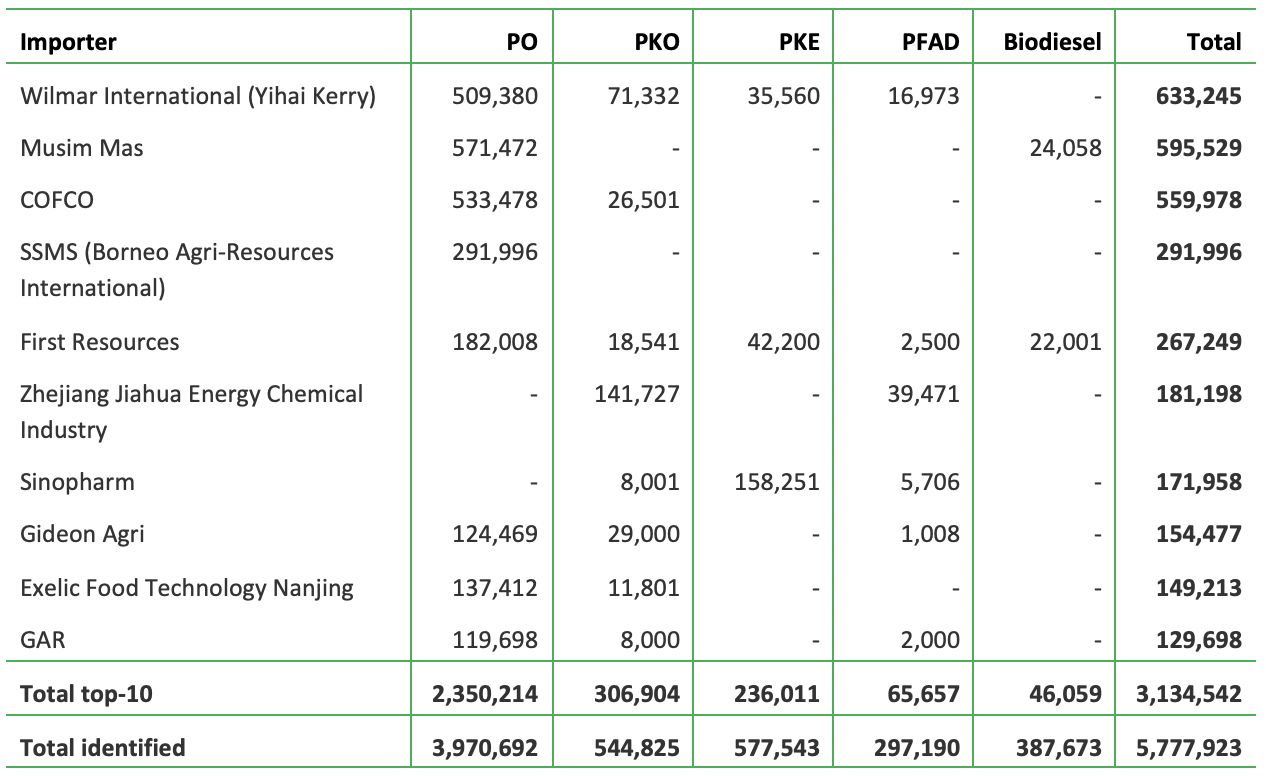

Wilmar, Musim Mas, and COFCO are by far the largest importers of palm oil to China. There are an estimated 10,000 palm oil trading companies in China, but the midstream market is dominated by a handful of large actors. The three leading importers companies accounted for approximately one-third of the imports of palm oil and derivatives from Indonesia, and at least Wilmar also plays an important role in importing from Malaysia.

After its listing in October 2020, Yihai Kerry is operating as an 89.99 percent subsidiary of Wilmar International (Singapore) in China. Yihai Kerry is involved in oilseed crushing, refining, specialty fats, and oleochemicals, among others. It is marketing edible oils under its own brands as well as in the B2B segment. Musim Mas (Singapore) is engaged in the merchandising and distribution of palm oil in China through its subsidiaries Intercontinental Oils & Fats and Shanghai Continental. COFCO is a Chinese state-owned, globally operating agri-business company which is involved in the palm oil supply chain as a trader and refiner. The company supplies palm oil to markets in China and India and operates a refinery in India.

Figure 6: Top-10 Chinese groups importing palm oil and derivatives from Indonesia, July 2019-June 2020 (tons)

Note: trade data for individual companies may not be complete. Source: Indonesian trade data, corporate websites, CRR paper on leakage refiners (2020).

Borneo Agri-Resources International (BARI) and Gideon Agri are responsible for most imports from Indonesian leakage refiners or producers which lag in NDPE implementation. The two companies received at least 62 percent of potentially non-compliant palm oil products exported by Indonesian refiners. Both BARI and Gideon Agri are Singapore-based companies engaged in trading of crude and refined palm oil products. BARI is related to SSMS, and Gideon Agri is a subsidiary of Universal Wellbeing (BVI), which markets consumer goods in several Asian countries.

The large importers (Figure 5 and Figure 6) are also important actors in the oil processing industry. According to the China Grain Industry Association, the following companies were the top palm oil processors in 2018:

- Yihai Kerry Golden Dragon Fish Grain, Oil and Food Co. (Yihai Kerry / Wilmar)

- COFCO Donghai Grain and Oil Industry (Zhangjiagang) Co. (COFCO)

- Yizheng Fangshun Grains & Oils Industry Co., Ltd.

- China Grain Reserve Zhenjiang Grain and Oil Co., Ltd. (China Grain Reserves Corp. (Sinograin))

- Guangzhou Zhizhiyuan Oils Industry Co., Ltd. (Dongling Group)

- Guangdong Eagle Mark Food Co., Ltd. (Yingma Food Co., Ltd.)

- Henan Qihua Edible Oil Co., Ltd. (Qihua Edible Oil Co., Ltd.)

Musim Mas operates three oil refineries in China and markets palm oil via its Chinese subsidiary Shanghai Continental Co.

Among the Chinese companies with their own investments in palm oil production, Julong Group owns an oils and fats processing facility in Tianjin Port Free Trade Zone, which reportedly has the largest capacity in China with 1.35 million tons of palm oil fractionation annually and 700,000 tons of oil refining. In Jiangsu (East China), Julong Group operates palm oil processing of 1 million tons of fractionation annually and 600,000 tons of oils refining. Another facility is under construction in Dongguan in South China. Shanghai Xinjiu Chemical Co. and Henan Jiujiu Chemical Co. are both chemical companies specialized in the production of fatty acids.

Palm oil is the second most important edible oil consumed in China

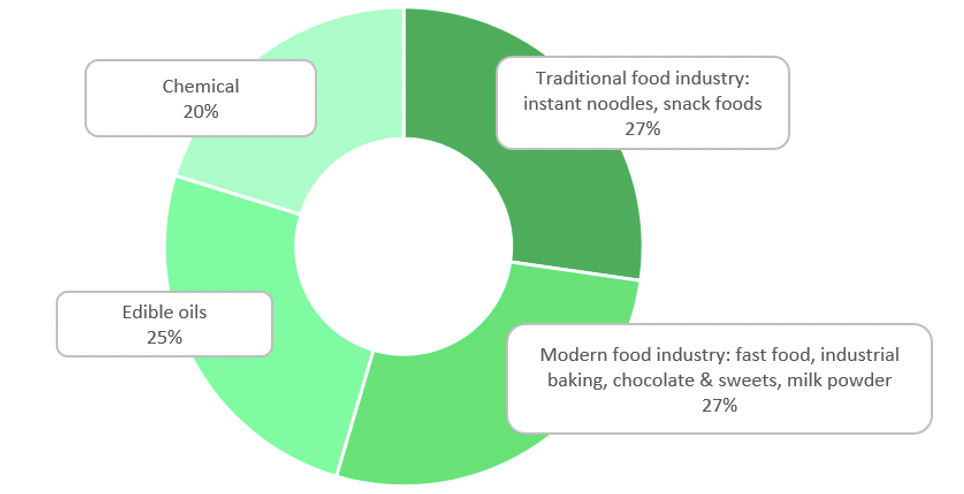

While soybean oil remains the most consumed edible oil in China with a share of around 45 percent, palm oil consumption is second with shares of 17-21 percent of edible oil consumption. The distribution between the important edible oils, namely soybean, palm, and rapeseed oil, is closely linked to price as well as global political developments. Overall, edible oil consumption in China has seen a CAGR of 4.54 percent between 2012/13 and 2017/18, which has also increased palm oil imports. More than half of the palm oil imported to China is used in the food industry, while another quarter is used as edible oil (Figure 6).

A key driver of palm oil use in the Chinese food sector is the growth of the processed food and catering industry. Important food industry segments include fast food with sales reaching CNY 908 billion (USD 132 billion) in 2018 and the industrial baking industry with sales of CNY 102 billion (USD 15 billion). Both segments experienced y-o-y growth rates between 4.0-6.6 percent in recent years. With an estimated annual consumption of 40 billion packs, the consumption of instant noodles accounts for approximately one-quarter of total edible palm oil consumption in China.

Figure 7: Distribution of palm oil consumption across sectors in China, 2018

Source: Oilcn (2019).

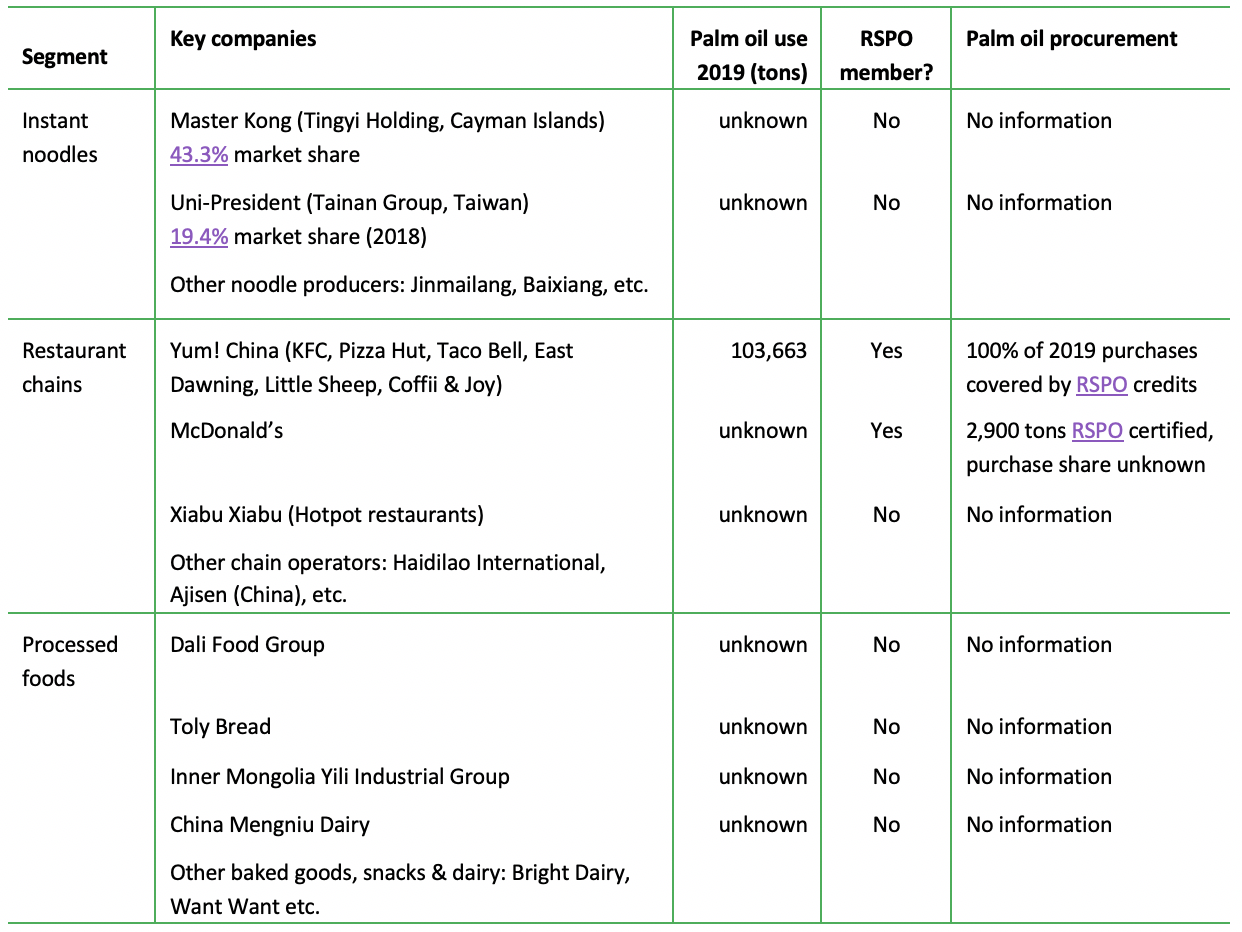

Many of the Chinese food-producing and retailing companies with exposure to palm oil-related sustainability risks publish no information on their palm oil use and procurement (Figure 8).

Figure 8: Important Chinese FMCGs and restaurant chains processing palm oil (examples)

Sources: Qianzhan (2020); Rabobank (2020); DBS Group Research (2020); Guotai Junan Securities (2020); RSPO; Company websites.

Chinese market for palm oil-based biodiesel so far limited but set to grow

While Chinese biodiesel production predominantly relies on used cooking oil (UCO) as feedstock, biodiesel imports are predominantly palm oil-based. The Chinese government had set an ambitious target of increasing annual biodiesel production to 2.0 million metric tons of biodiesel by 2020. However, in the absence of a blending mandate and dominated by small-scale private businesses, domestic production reached only 1.0 million tons in 2019, down from 1.2 million tons in 2018. Driven by the COVID-19 pandemic and low crude oil prices, a further drop is expected in 2020.

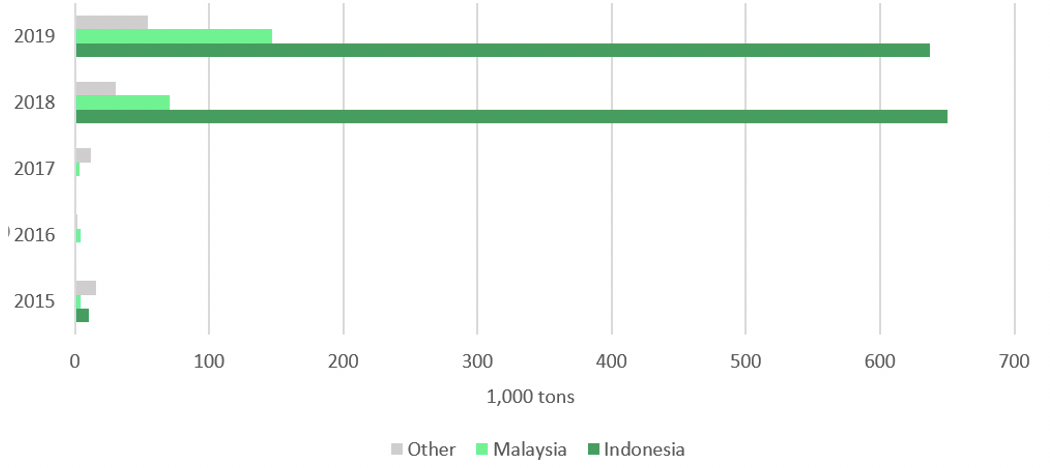

Demand for biodiesel based on palm oil as the cheapest feedstock expands when fossil fuel prices increase, but production, imports, and consumption collapse when fossil fuel prices drop. When the price for biodiesel weakens, it is unable to compete with typically lower priced fossil fuel-based diesel. These fluctuations are visible in the development of biodiesel imports to China (Figure 9). As the price for Brent crude jumped in early 2019, biodiesel imports to China sharply increased.

Biodiesel imports are predominantly sourced from Indonesia, pointing to palm oil or palm oil fatty acid (PFAD) as feedstock. In 2019, Indonesia accounted for 637,000 metric tons or around 75 percent of total Chinese biodiesel imports, followed by Malaysia with 147,000 tons (17 percent). In addition, China imports PFAD from Indonesia and Malaysia, and a portion is likely processed into biodiesel. Increasingly stringent environmental measures in relation to CO2 emissions may increase prospects for biodiesel use in China in the coming years, notably also in the aviation and shipping sectors.

Figure 9: Chinese biodiesel imports, 2015-2019 (1,000 tons)

Source: ITC TradeMap (2020).

Among the Chinese imports of biodiesel from Indonesia, leakage refiners accounted for an estimated 14 percent of supply in the twelve months to June 2020. These include Tunas Baru Lampung, Darmex Agro, and Best Group. The majority of imports were sourced from refiners with NDPE commitments. This division reflects the share of NDPE commitments among Indonesian palm oil refiners.

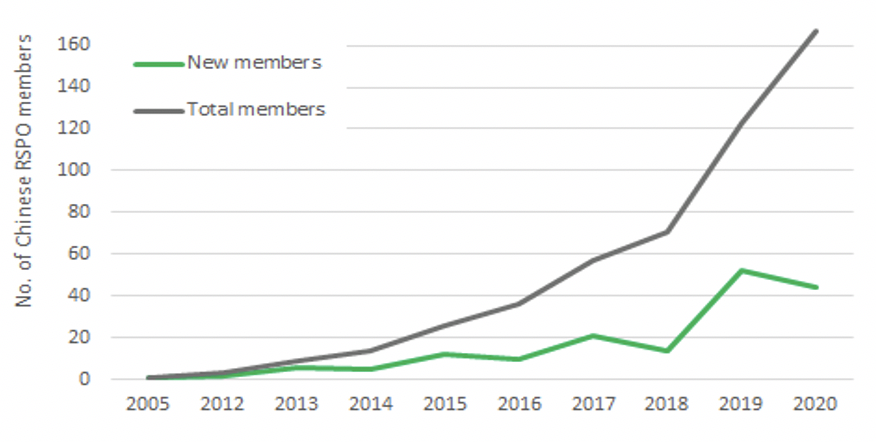

Rapid growth of Chinese RSPO membership

There are currently 167 members of the RSPO registered in China. A quarter (39) are ordinary members, and the remainder are associates. Of the ordinary members, ten are consumer goods manufacturers, 27 are palm oil processors and/or traders, and two are retailers. The associate members are all (128) supply chain associates. Associate members are active in the supply chain of RSPO-certified palm oil (CPO) and purchase less than 500 metric tons of palm oil products per year.

China’s main agro-commodity trading company – COFCO – has been a member of the RSPO since 2005. Its oilseed and grain trading peer – Sinograin – has been a member since 2016. Restaurant operator Yum! China, which was spun off from its Yum! Brands in 2016, became a member in 2018, two months after Yum! Brands. Notably, the four Chinese upstream palm oil companies (ZTE/Zonergy, Tianjin Julong, Henan Jiujiu Chemical Co. and Shanghai Xinjiu Chemical Co.) are not members of the RSPO.

The rapid growth in new members since 2018 is attributable to the launch of the China Sustainable Palm Oil Alliance (Figure 10). This initiative has been launched by the RSPO together with the Chinese Chamber of Commerce of Foodstuffs and Native Produce (CFNA) and the World Wildlife Fund (WWF). Key supply chain stakeholders, including Mars Wrigley Confectionery, L’Oréal China, AAK, Cargill China, COFCO, Sinograin, HSBC, and Yihai Kerry made a joint commitment to promote the uptake of certified palm oil in China.

Figure 10: Number of Chinese members of the RSPO

Source: RSPO (2020).

While the RSPO in 2018 formulated a target of 10 percent CPO in China in 2020, only around 2 percent of Chinese palm oil imports are currently certified. Although the Chinese membership of RSPO has increased rapidly, the uptake of CPO is still comparatively low. The annual RSPO reports of four important companies show varying degrees of RSPO adoption in 2019. COFCO registered 5.87 percent, and Sinograin’s and Dow Chemical’s purchases both stood at 0.0 percent. Meanwhile, Yum China reports 100 percent uptake of CPO in 2019. For important international actors such as Wilmar and Musim Mas, no information on the share of CPO in country-level volumes is available.

Chinese financial institutions accounted for 7 percent of upstream palm oil financing 2013-2019

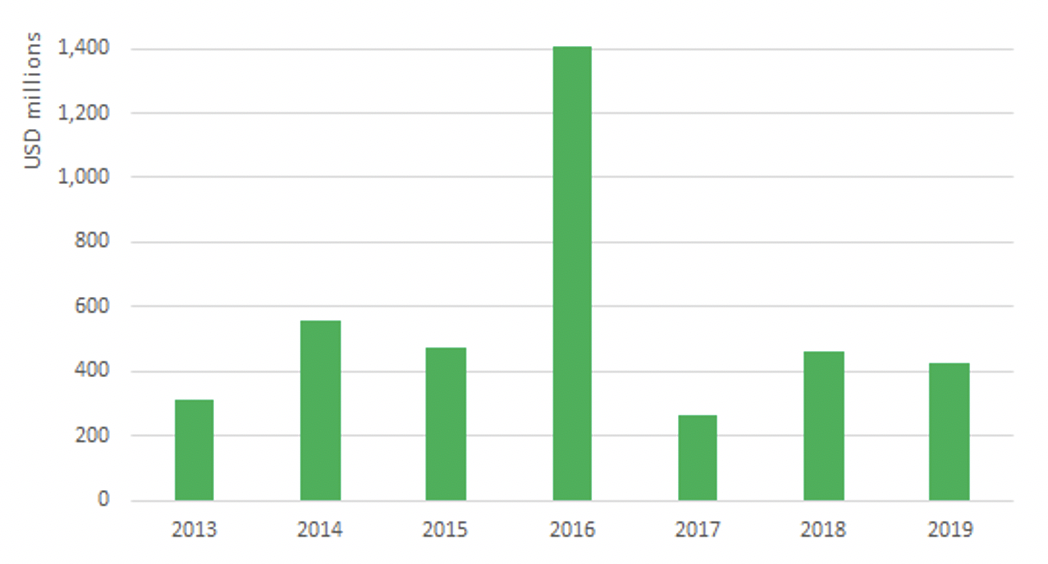

Annual credit values through loans and underwriting services provided by Chinese financial institutions to companies engaged in palm oil activities in Southeast Asia fluctuated between USD 200 million and USD 600 million from 2013-2019 (Figure 11). Key companies involved in the palm oil market are part of larger conglomerates. Therefore, adjusters are used in the following figures to account for this part of their business activities. The spike in 2016 stemmed from the underwriting services provided to COFCO in preparation for its full acquisition of Nidera.

In terms of total financing, Chinese financial institutions play a less important role in upstream palm oil financing than their peers in Malaysia, Indonesia, and Singapore. This role is partly due to the limited number of Chinese companies operating in the upstream palm oil segment. This segment is dominated by companies headquartered in Malaysia, Indonesia, and Singapore. Approximately 60 percent of all palm oil financing in the period 2013-2019 was provided by financial institutions from these three countries, accounting for respectively 24 percent, 22 percent, and 11 percent. Japanese financial institutions were the fourth largest palm oil financiers (11 percent) followed by Chinese financial institutions (7 percent of total palm oil financing).

Figure 11: Chinese loans and underwriting to up- and midstream palm oil (2013-2019, USD millions)

Note: All figures are adjusted for palm oil attributable value. Source: Forests & Finance (2020).

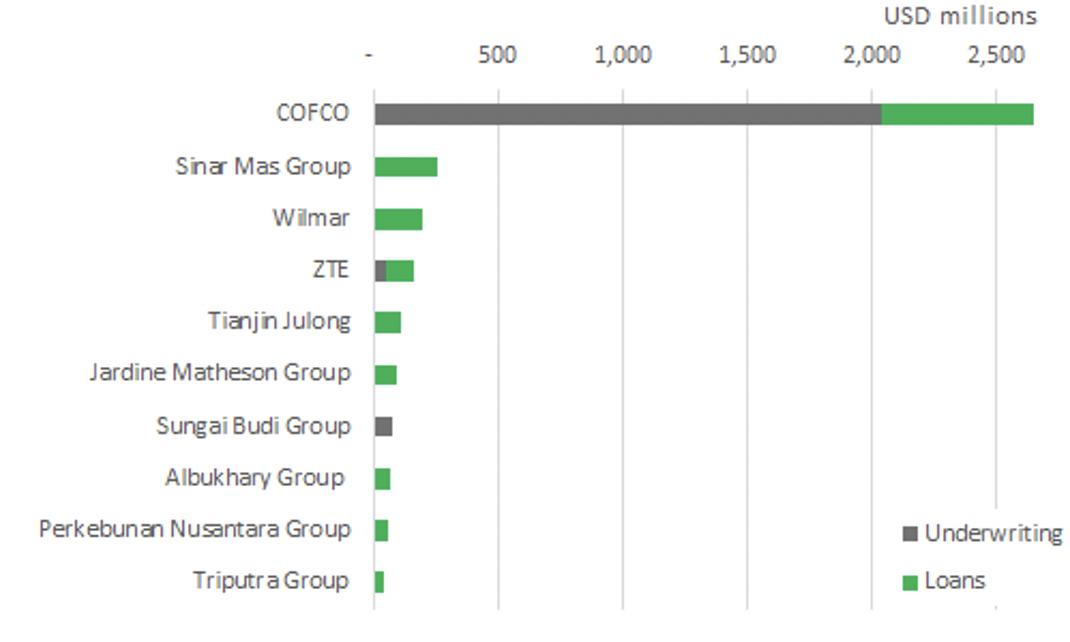

COFCO was by far the most important palm oil client of Chinese financial institutions during the analyzed period from 2013-2019, with a total credit value of USD 2.65 billion (Figure 12). The value of financing provided to other companies engaged in the palm oil sector in Southeast Asia is considerably smaller.

Figure 12: Top 10 palm oil clients of Chinese financial institutions (2013-2019, USD millions)

Note: All figures are adjusted for palm oil attributable value. Source: Forests & Finance (2020).

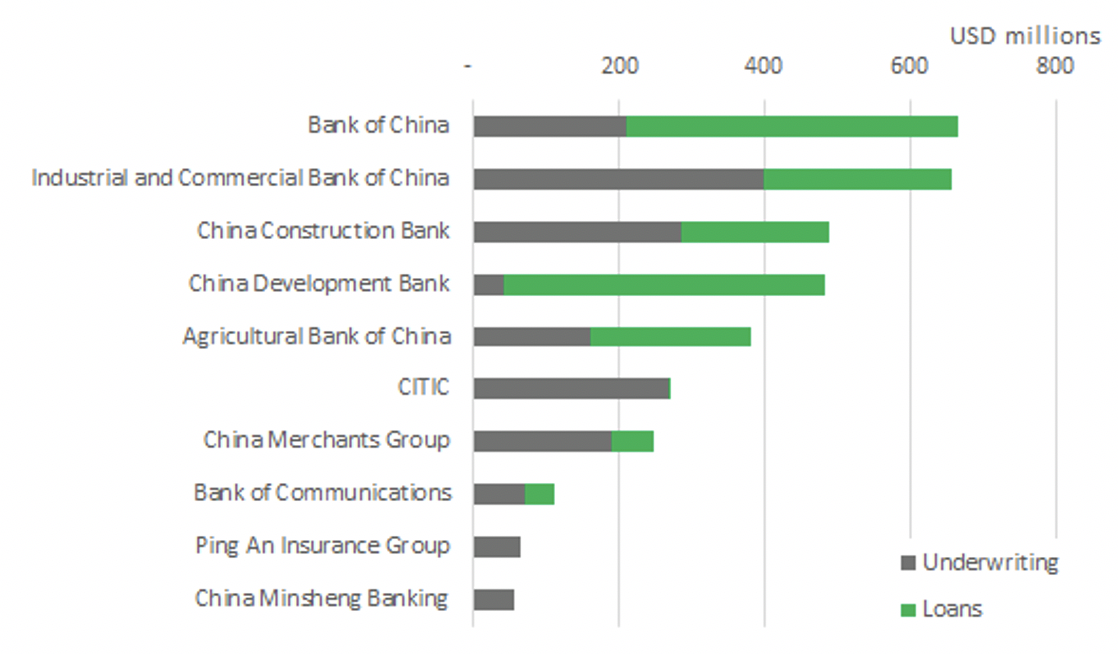

All large Chinese banks provided credit to companies engaged in the palm oil sector. Bank of China and Industrial and Commercial Bank of China are the Chinese financial institutions with the highest levels of financing (Figure 13). In total, the Chinese banks provided USD 3.9 billion in credit to palm oil companies.

Figure 13: Top-10 Chinese creditors of palm oil (2013-2019, USD millions)

Note: All figures are adjusted for palm oil attributable value. Source: Forests & Finance (2020).

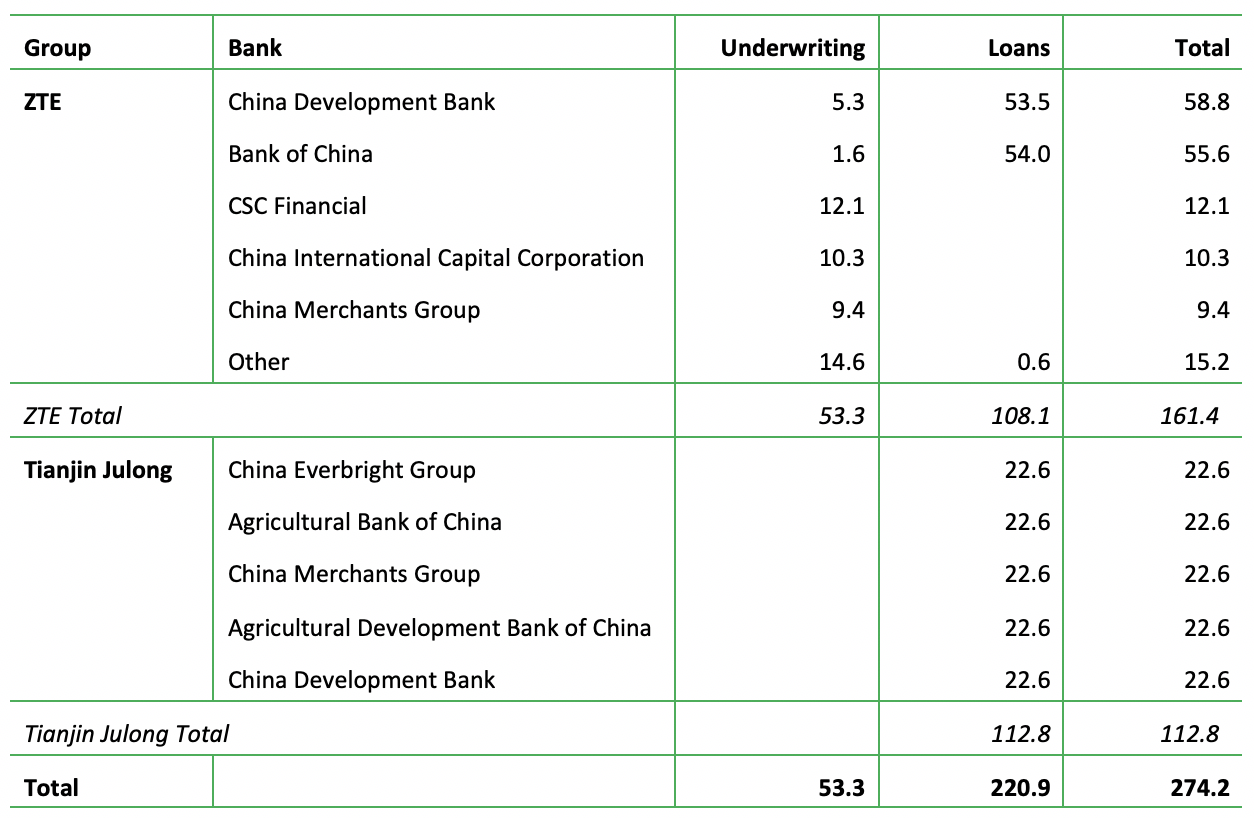

The Chinese-owned plantation companies ZTE and Tianjin Julong received loans and underwriting services from several leading Chinese financial institutions (Figure 14). For the other Chinese actors engaged in upstream palm oil operations, no financial links could be identified.

Figure 14: Top 5 Chinese creditors of Chinese palm oil companies in Indonesia (2013-2019, USD millions)

Note: All figures are adjusted for palm oil attributable value. Source: Forests & Finance (2020).

Chinese companies engaged in upstream and midstream palm oil activities are generally private companies that are not listed on the stock exchange or state-owned companies. Only ZTE is listed on the stock exchange.

Chinese financial institutions do not publish ESG risk mitigation policies and standards; nor do they publish the minimum standards they expect their clients in deforestation-risk sectors – such as palm oil – to meet. Domestic banks have so far not incorporated guidelines for business decisions in relation to the environmental and social risks connected to palm oil. Nevertheless, since 2007, the China Banking Insurance Regulatory Commission (CBIRC) has been encouraging Chinese financial institutions to integrate ESG considerations into their due diligence, client onboarding, and monitoring practices. These recommendations were formalized in the Green Credit Guidelines in 2012. In 2017, the CBIRC issued the Guidelines on Regulating the Banking Industry in Serving Enterprises’ Overseas Development and Strengthening Risk Control. These guidelines were developed to mitigate the increasing ESG risks that Chinese financial institutions and their clients were exposed to outside of China.

The combination of these two guidelines covers the risks that Chinese financial institutions are exposed to when financing companies in the palm oil value chain. However, the extent to which these guidelines have driven structural changes in the ESG risk mitigation strategies of Chinese financial institutions is unclear. They remain linked to companies exposed to ESG risks and implicated environmental and social rights violations.