In 2017, the Task Force for Climate-Related Financial Disclosure (TCFD) released its recommendations for climate-related disclosures in financial filings. The TCFD has since become the de facto global standard for the financial sector to report on climate change risks. This paper presents a framework for assessing deforestation-related risks in agricultural commodity supply chains that is aligned with the TCFD principles. The framework is based on CRR’s seven years of experience in the palm oil, soy, beef, and farmland sectors.

Download the PDF here: Chain Reaction Research Applies TCFD-aligned Framework to Assess Deforestation Risks

Key Findings:

- Deforestation is the largest climate change risk in agricultural supply chains. The elimination of tropical deforestation would reduce annual global emissions by up to 30 percent. It also constitutes a physical risk to the productivity and yields of agricultural production. However, companies and investors have not yet fully integrated deforestation risks into their risk management systems.

- As the world responds to global climate change and biodiversity loss, companies linked to deforestation may face a range of transition risks. These include legal risks from land, trade, and due diligence requirements. Risks may also come from a shift in market demand as a result of corporate sourcing policies. Civil society campaigns and negative media attention could bring reputational risks.

- Zero-deforestation may create economic opportunities for companies within agricultural commodity supply chains. Those companies that make significant efforts toward meeting their commitments have enjoyed greater market access, improved reputations, and more resilient supply bases. In addition, there may be under-explored opportunities for alternative business models and product offerings.

- CRR’s analytical framework applies equity-level scenario analysis. CRR first assesses a company’s exposure to deforestation and other sustainability issues and identifies related business risks. CRR then develops three scenarios to project how these risks may play out: a low response, a medium response, and a high response

- CRR assesses the materiality of each identified risk based on income statement and balance sheet metrics. Models include revenue-at-risk, cost of capital, and stranded land. The final step in CRR’s model calculates the cumulative impacts and projects a company’s market value and share price under all three scenarios.

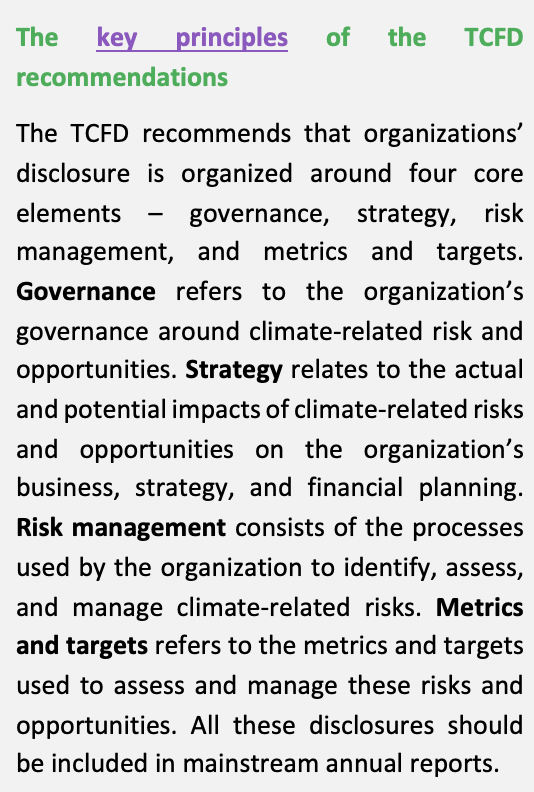

TCFD recommendations and their use by companies and financiers

In 2017, the Financial Stability Board’s Task Force for Climate-Related Financial Disclosure (TCFD) released a set of recommendations for climate-related disclosures in financial filings. Its recommendations represent the most robust framework to disclose the financial materiality of climate risks and opportunities. The TCFD recommendations are designed to capture consistent, useful, and forward-looking information to assist financial markets in their understanding of the financial implications of climate change. Enhanced and coherent disclosure of climate-related risks and opportunities provides investors with the information needed to undertake robust and consistent analyses. Having a common and consistent language to discuss climate-related risks and opportunities helps build a shared awareness. In turn, such awareness allows financiers to engage meaningfully with their investees.

The TCFD has become the de facto global standard for the financial sector to report on climate risks. Since the release of the final TCFD recommendations in June 2017, over 1,500 public- and private-sector organizations have announced their support. Its supporters include financial institutions with over USD 150 trillion in assets. Disclosure of TCFD-aligned information increased by six percentage points between 2017 and 2019. In November 2020, the UK government announced its intention to make TCFD disclosure mandatory by 2025. This move was supported by a group of 250 institutional investors with USD 8.3 trillion under management.

TCFD-aligned disclosures vary greatly across industries. Energy companies and materials and buildings companies are the most aligned in their disclosure. The average level of reporting across the 11 recommended disclosures was 40 percent for energy companies and 30 percent for materials and building companies. For consumer goods companies, this average stood at only 18 percent.

Companies in the agriculture, food and forest products sector disclosed only 25 percent across all categories. Companies in this sector disclosed relatively often on climate-related risks and opportunities (41 percent of all reviewed companies), but relatively low on the resilience of their strategy (1 percent). The TCFD has developed supplementary guidance (see Annex E) to highlight sector-specific metrics for the agriculture, food, and forest products industry. To date, the most common metrics used by the agriculture, food, and forest products sector include scope 1, 2, and 3 emissions, internal carbon prices, water usage, waste management data, and operations energy use disaggregated by source. Underrepresented key metrics for this sector include metrics on land cover, land-use practices, land-use change, water source, water intensity, and location of assets within a coastal or designated flood zone.

Despite growing urgency, deforestation risk disclosure remains poor

Deforestation is the largest climate change risk in agricultural supply chains. The elimination of tropical deforestation today would result in a reduction in annual global emissions of 24 to 30 percent. Furthermore, deforestation is a wide-ranging issue with impacts that reach far beyond climate change. Deforestation has implications for the planetary boundaries of biodiversity, land- system change, freshwater consumption, atmospheric aerosol pollution, as well as for community and land rights and corruption.

Companies and investors have not yet fully integrated deforestation risks into their risk management systems. Company disclosure and transparency on deforestation remains poor. Despite a growing sense of public urgency, many companies failed to report critical forest-related information or include deforestation issues in their risk assessments. While deforestation is often prevalent within the supply chains of companies, transparency on sourcing practices and supply relationships remains sporadic at best.

Investors face various obstacles that complicate the integration of deforestation data into their decision-making processes. Obstacles include insufficient data on upstream actors; the level of data granularity; inability to link data to portfolios; absence or inconsistencies of company identifiers; and the challenge of mapping parent companies to subsidiaries. These obstacles stem from various factors, including supply chain complexity, limited exposure of international investors to upstream companies (where deforestation mainly occurs), and differing information needs across investors.

The TCFD recommendations can be applied to assess material deforestation risks

Chain Reaction Research (CRR) has developed a TCFD-aligned analytical framework to assess the materiality of deforestation exposure. CRR’s framework is designed for independent risk analysis on an equity level. The framework is based on seven years of independent analysis on the business and financial risks of deforestation for companies in the palm oil, soy, beef, and farmland markets. It uses a unique dataset that integrates supply chain and operation data, real-time monitoring of fires and land-use change, cadastral land ownership registrations, company concessions, and company group structures. It applies these datasets to identify company-specific deforestation risks and project their future financial impacts.

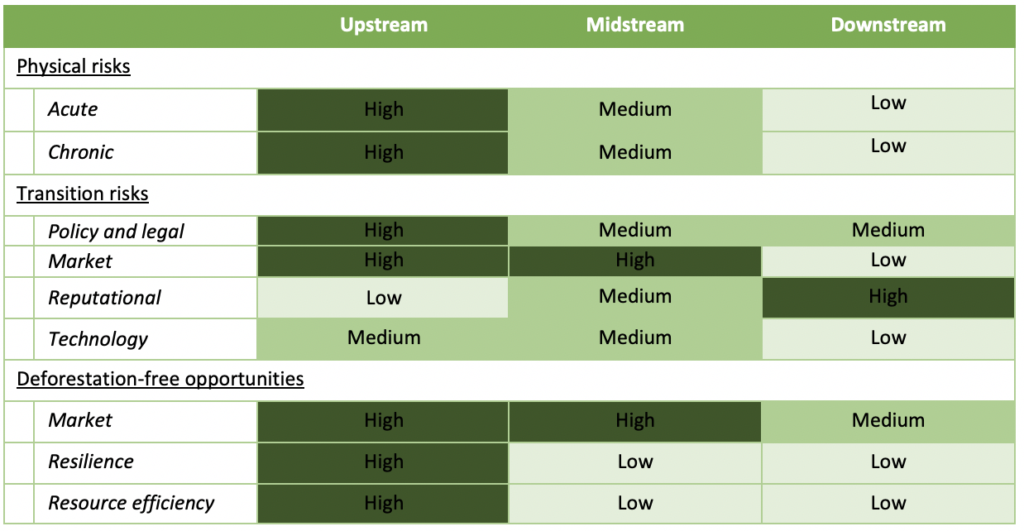

The framework is tailored to capture deforestation risks for companies throughout agricultural commodity supply chains. Companies under assessment include upstream agricultural producers which may be directly contributing to deforestation through expansion of their agricultural land; midstream commodity traders and processors which may purchase commodities from recently deforested farms; and downstream fast-moving consumer goods companies (FMCGs) and retailers that may be exposed to supply chain deforestation further removed from their own operations.

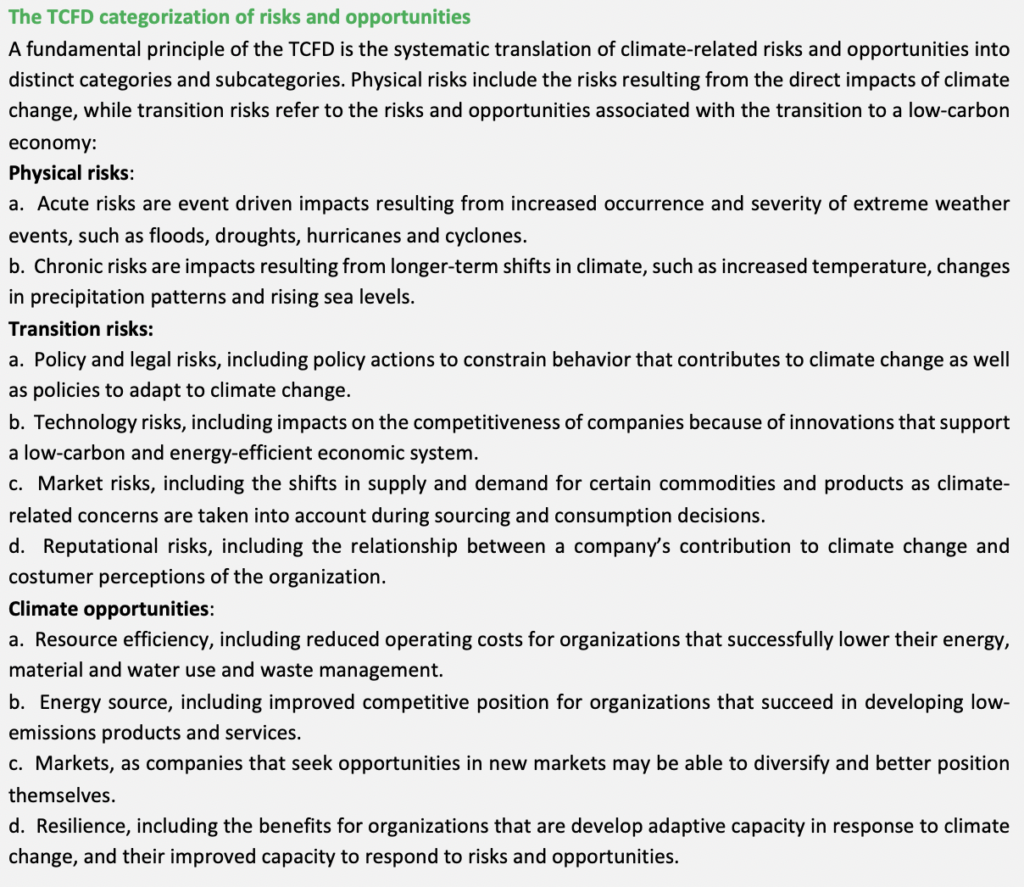

CRR’s framework applies and adapts the TCFD climate-related risk categories to the issue of deforestation. It includes these risk categories in forward-looking scenarios that aim to capture the materiality of each risk. The following sections outline the evidence that underscores CRR’s analytical approach for each of the risk categories.

Figure 1: Deforestation risk levels throughout agricultural commodity supply chains

Source: Chain Reaction Research

Deforestation as a physical risk

“Physical risks resulting from climate change can be event driven (acute) or longer-term shifts (chronic) in climate patterns. Physical risks may have financial implications for organizations, such as direct damage to assets and indirect impacts from supply chain disruption.” – TCFD Final Recommendations

The agricultural productivity of forest-risk commodities is sensitive to temperature and precipitation, and thus affected by climate change. Large-scale conversion of native vegetation into farmland can have significant impacts on local climate, including increased occurrence of droughts, floods, and other erratic weather patterns. Tropical deforestation results in warmer and drier local conditions and may result in more extreme weather events. Such local climate changes can put future agricultural productivity at risk.

Conversion of native vegetation can adversely impact water systems. In Brazil’s Cerrado biome, the conversion of native savannah vegetation has affected the country’s water system. Soy expansion in the Cerrado has contributed to increased droughts and erratic river behavior. Limited rainfall and high evaporation lead to sharp periodic decreases in crop yields and intensify conflicts between agricultural producers and local communities. The region of Matopiba, consisting of the states of Maranhão, Tocantins, Piauí and Bahia, is particularly susceptible to droughts and is expected to develop a drier climate in the next decade. It is also the focal point of Brazil’s expansion of soy cultivation. As most of the soy produced in this region is rainfed, climate change may have significant effects on productivity and yields to the point that certain areas may no longer have sufficient agricultural suitability. Some Matopiba regions have already seen a decline in agricultural suitability.

In the Amazon, deforestation is impacting the evapotranspiration rates that provide rainwater to a large portion of South America. In Brazil, yearly rainfall volumes have decreased by almost 17 percent in the last decade compared to averages from the last 40 years. Regional anomalies in rainfall patterns have been directly attributed to deforestation in the Amazon. The shorter and later rainy seasons in Brazil’s soy, corn, and cotton producing regions have put future production rates at risk.

In Southeast Asia, the deforestation and draining of peatland has caused the subsidence of large tracts of land. The average subsidence rate of 2.2 centimeters per year results in loss of productive land and flooding. This includes both land used for smallholder agriculture as well as large scale oil palm and acacia plantations. The drainage of peatland for acacia tree plantations has been particularly intensive and resulted in average subsidence levels of 4.3 centimeters per year.

Deforestation as a policy and legal risk

“Policy actions around climate change continue to evolve. Their objectives generally fall into two categories—policy actions that attempt to constrain actions that contribute to the adverse effects of climate change or policy actions that seek to promote adaptation to climate change” – TCFD Final Recommendations

Agricultural producers and farmland investors may face increasingly stringent regulations around land tenure and land use change. Measures in tropical forest countries include moratoria and forest regulations. In Indonesia, multiple government-ordered moratoria have impacted growers of oil palm and other commodities, including a moratorium on the issuing of any new concession licenses on primary natural forest and peatland (PIPPIB) and a temporary moratorium on the issuance of new oil palm concession licenses until September 2021. In Brazil, the Forest Code has stipulated biome-specific environmental reserves for landowners. These reserves amount to 80 percent of land located within the Amazon biome, and 35 percent within the Cerrado biome. Farms that have illegally cleared forests and other native vegetation can be fined and placed on public blacklists by Brazil’s environmental agency IBAMA. For upstream producers, these regulations may create risks for the asset value of its landbank, as well as increased costs through fines and restorative measures.

An additional legal risk for upstream producers and farmland investors can come from land conflicts, illegally obtained deeds and titles, and infringement on the rights of local communities. Several areas within tropical forest countries are characterized by insecure land tenure. Examples include the municipality of Formosa do Rio Preto in the Brazilian state of Bahia, which is the third-largest soy-producing municipality in Brazil. Here, two landmark cases have been in court for several years, with multiple land claims annulled and overturned. In the case of JJF Holdings, a 366,000-ha land claim by Jose Valter Dias has been granted and overturned multiple times by state and local courts. The consequent uncertainty of land tenure has been a factor in increasing rates of deforestation in recent years. In Liberia, the recognition of community land rights in the country’s Land Rights Policy contributed to several large oil palm concessions becoming stranded.

Midstream and downstream actors may be exposed to policy and legal risks from emerging due diligence requirements set in import markets. In the European Union, several legislative initiatives aim to minimize the risk that products contributing to deforestation are sold in the European market. The European Commission recently held a public consultation and launched a multi-stakeholder platform to inform a Europe wide legislative proposal. This development followed the introduction of the French “devoir de vigilance” law in 2017, requiring large companies to implement a plan to identify, prevent, and mitigate human rights violations and environmental harm. In the UK, a legislative proposal currently under consideration aims to ensure that commodities used or sold on the UK market are not grown on illegally deforested land. Civil society organizations are actively campaigning to include more stringent requirements to this proposal. In Germany, discussions are ongoing about a similar “Supply Chain Law.” In the longer term, the carbon neutral ambitions of various Asian countries, including China, Japan, and South Korea, may also translate into import restrictions on forest-risk commodities.

Deforestation as a market risk

“While the ways in which markets could be affected by climate change are varied and complex, one of the major ways is through shifts in supply and demand for certain commodities, products, and services as climate-related risks and opportunities are increasingly taken into account.” – TCFD Final Recommendations

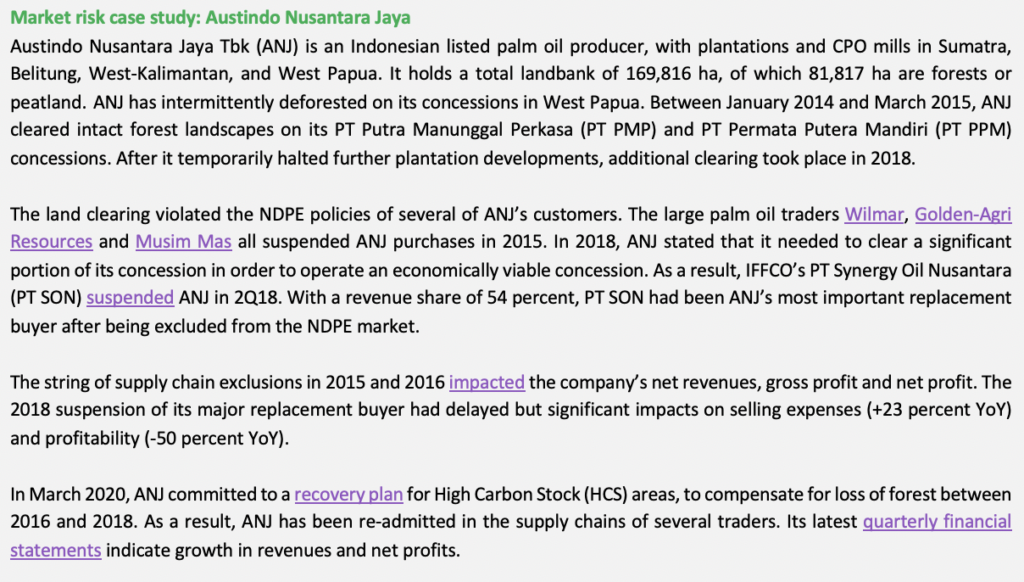

Since 2013, a surge in corporate zero-deforestation commitments has led to market shifts that reflect reduced demand for products that may be linked to deforestation. CRR has collected and analyzed a large number of anecdotal examples of companies facing financial impacts due to supply chain exclusions and suspensions. In the palm oil sector, No Deforestation, No Peat, No Exploitation (NDPE) policies have been implemented on a “company group” basis, whereby a supplier could face suspension regardless of a direct link between the deforestation and the supplied commodity. This has greatly increased the market risk of deforestation, as it reduces the options to service the NDPE market, while simultaneously supplying unsustainable products to the “leakage” market.

Palm oil suppliers found to be non-compliant with NDPE policies have been suspended from corporate supply chains. As a result, non-compliant growers have faced increasingly severe financial impacts. The adoption and implementation of NDPE policies by palm oil traders and refiners has steadily increased over recent years. As of 2020, 83 percent of Indonesia’s and Malaysia’s refining capacity is covered by NDPE policies, with evidence of effective implementation for 78 percent of capacity. Between 2015 and 2019, four publicly traded palm oil growers that faced suspensions lost a combined market value of USD 1.1 billion. Partially as a result of these market risks, deforestation for oil palm in Indonesia has decreased significantly since 2018.

In the soy, leather, and beef supply chains, downstream companies have taken a more geographical approach, resulting in the exclusion of Brazilian commodities from corporate supply chains. Various end-user companies in the soy and beef supply chains have sent clear and public messages to their Brazilian suppliers about the need to address supply chain deforestation. In December 2020, 160 signatories to the Statement of Support for the Cerrado Manifesto demanded soy traders to end trading soy from areas in the Cerrado cleared after 2020, while Bremnes Seafood, a Nordic salmon farming company, stopped using Brazilian soy. In June 2020, a group of 40 European companies issued a public letter in which they warned of an imminent boycott of Brazilian soy, following a similar statement by 14 French consumer goods and retail companies in May 2020. In response to the 2019 Amazon fires, a number of multinational brands, including Nestle, H&M, and VF Corporation, took steps to exclude Brazilian commodities from their supply chains.VF Corporation.

Another market risk comes from downstream companies and retail consumers that ban forest risk commodities altogether. In September 2020, Marks & Spencer committed to excluding embedded soy from its milk products by working with farmers to opt for alternative animal meal options. In 2018, the supermarket chain Iceland cut the use of palm oil from its own branded products. Arguably, these retailers are responding to consumer preference trends toward healthier and more climate friendly diets. Such patterns include growing rates of vegetarianism and consumer boycotts of palm oil and soy.

Deforestation as a reputation risk

“Climate change has been identified as a potential source of reputational risk tied to changing customer or community perceptions of an organization’s contribution to or detraction from the transition to a lower-carbon economy.” – TCFD Final Recommendations

While more difficult to quantify, it is generally accepted that companies that are the target of deforestation allegations face reputational risks. These risks can materialize in lower consumer preference, but also increased difficulties in attracting talented staff, more stringent enforcement of government policies and reduced access to finance. The potential reputational damage of being implicated in deforestation is not only dependent on the nature of the allegations, but also on the corporate response to public criticism.

Consumer brand companies have most often been subject to civil society campaigns and other forms of public criticism. Starting with high-impact campaigns on deforestation in the palm oil supply chains of Nestlé and Unilever at the beginning of this century, a range of different FMCGs have been the target of such campaigns in recent years. These FMCGs include Mondelez, Procter & Gamble, Burger King, PepsiCo, and others.

Midstream traders and processors of forest-risk commodities have also found themselves in the crosshairs of campaigning organizations for their role in driving deforestation in Southeast Asia, Africa, and Latin America. In 2019, Cargill was labelled “the worst company in the world” by a global campaign organization, while large palm oil traders such as Wilmar, Golden Agri-Resources, and Indofood have faced long-standing criticism from international environmental NGOs.

If investors and financiers perceive deforestation risks to be material or that these risks are not adequately mitigated, a company’s reputation within financial markets may be negatively affected. A range of various platforms and initiatives award scores to companies on the quality and implementation of deforestation policies. Rating agencies, engagement service providers, and other ESG data providers are also increasingly integrating deforestation into their evaluation methods. Low ESG benchmark scores can translate into reduced access to sustainable finance through exclusion from sustainable indices and less access to green bonds and other types of green financing.

Zero deforestation as an opportunity

“Efforts to mitigate and adapt to climate change also produce opportunities for organizations, for example, through resource efficiency and cost savings, the adoption of low-emission energy sources, the development of new products and services, access to new markets, and building resilience along the supply chain.” – TCFD Final Recommendations

Zero-deforestation business models may create a range of economic opportunities for companies within agricultural commodity supply chains. The adoption and full implementation of corporate zero-deforestation policies provides one way to mitigate the above-mentioned risks. As of 2020, 498 companies made voluntary commitments within the four key forest-risk sectors. However, most commitments are not fully implemented, as nearly all of the signatories of the 2014 New York Declaration on Forests failed to meet their 2020 deforestation-free deadlines.

Those companies that made serious efforts to meet their commitments have enjoyed greater market access, improved reputations, and more resilient supply bases. The returns of companies that scored higher on sustainability benchmarks have outperformed those of the worst by 20 percent. Companies that are members of the Roundtable for Sustainable Palm Oil (RSPO) have also outperformed their non-member peers in equity returns. A 2019 study by Climate Advisers that compared the returns of listed palm oil companies concluded that “environmental stewardship improves the bottom line.”

In the palm oil sector, a number of upstream growers have adopted zero-deforestation policies, issued stop-work orders, and avoided opportunities to clear additional forests. As a result, these growers have obtained or maintained access to NDPE markets. They have also circumvented potential conflicts and drawn-out negotiations with local communities. Because of market and policy demand for zero-deforestation, several companies were faced with “stranded land.” Stranded land is a type of stranded asset or “assets that have suffered from unanticipated or premature write-downs, devaluations or conversion to liabilities.” Companies that halted deforestation and invested in measures to satisfy the sustainability demands of the NDPE market have benefitted from maintained or renewed access to NDPE clients.

There may be under-explored opportunities that could arise alongside stringent implementation of zero-deforestation policies. While deforestation risks may be mitigated by operating or sourcing procedures, such risks may also be circumvented through adaptations to business models and product offerings. Companies that invest in sustainable alternatives and divest from high-risk operations may have a less urgent need to mitigate deforestation risks with complicated supply chain monitoring systems. For example, plant-based proteins may offer new and more sustainable market opportunities for meat processors. Similarly, companies may also see opportunities in their geographical asset base, prompting them to refrain from conducting business in particularly high-risk regions.

Scenario analysis to assess materiality of risks

A key TCFD recommendation is to conduct scenario analysis in order to better understand how different possible climate futures can affect the resiliency of business strategies. Scenarios to perform climate change risk assessments can be developed at various levels, including at a macro-economic, sectoral, company, and asset level. There are top-down methodologies that conduct macro-economic modelling to assess the impacts of climate change on interest rates, employment rates, and other national-level, macro-economic indicators. Risk assessments can also be conducted on a sectoral, individual company, or asset level. The Network for Greening the Financial System (NGFS), a coalition of central banks and supervisors spanning 42 members and five continents, recommends using both top-down and bottom-up exercises to assess the financial impacts of climate-related risks. While climate-related scenario development and analysis is most developed in the energy sector, a growing awareness about the importance of including deforestation in climate scenario analysis has emerged. In June 2020, Ceres detailed the steps needed to adapt the TCFD framework to a deforestation-focused analysis.

In order to project how deforestation risks may impact individual companies in the future, CRR’s analytical model includes equity-level scenario analysis. CRR’s objective is to identify and quantify the financial risks of deforestation. As CRR’s research is based on primary data collection about sustainability impacts, it can additionally be used for alignment and engagement purposes by responsible investors. Based on the available data and insights of the company under analysis, a number of methodological choices are made in this process:

- Determining risk exposure

The starting point for CRR’s analysis is the assessment of a company’s exposure to deforestation and other sustainability issues. CRR conducts a sustainability risk assessment (SRA) of a company’s agricultural operations and within its supply chain. Through a combination of remote sensing techniques and field investigations, sustainability impacts such as recent deforestation, peatland development, wildfires, or clearing of other native vegetation are identified and measured. The SRA also includes research into impacts on local communities through a combination of desk research and field investigations.

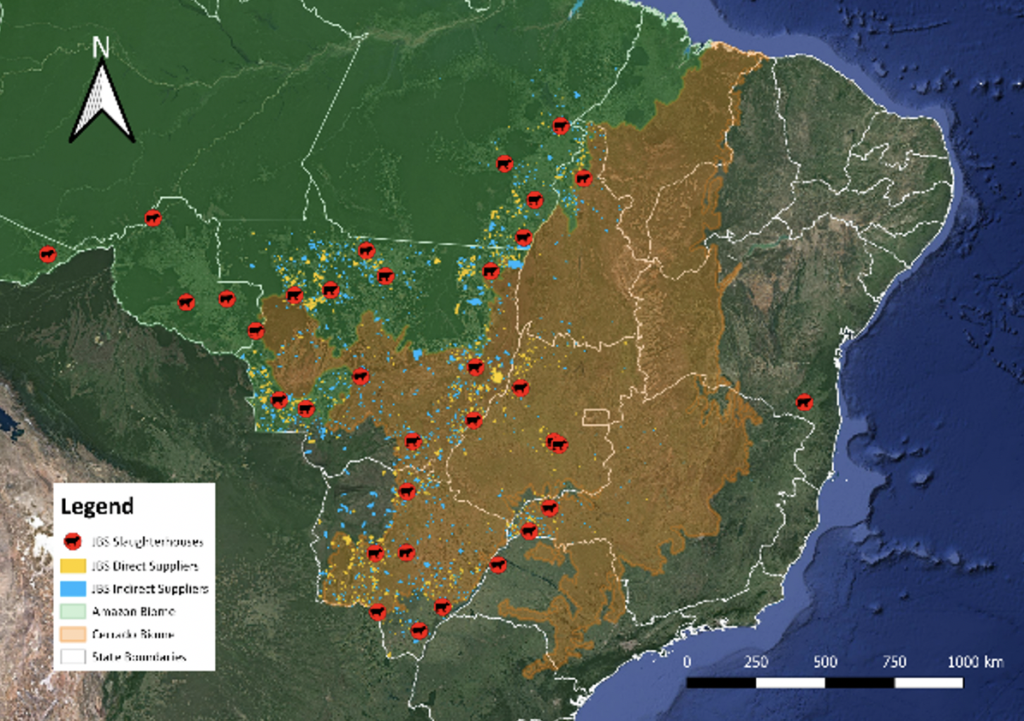

For key companies that CRR has covered in the past, it has developed tailored geospatial datasets that allow for continuous and near real-time monitoring of land-use change. These datasets are based on a composite of sources including satellite monitoring, cadaster and concession ownership data, corporate structures, trade data, and supply chain relationships. In some cases, CRR has collected primary evidence of supply chain linkages, such as through sampling products in supermarkets.

Figure 2: Image produced from in-house geospatial dataset of a meatpacker’s direct and indirect supply chain

After CRR has identified the sustainability impacts, they function as input for the identification of a company’s business risk exposure. The framework includes a systematic assessment of the following:

- The sustainability demands of a company’s clients and markets (market risk)

- The environmental and regulatory context in which a company operates (policy and legal risk)

- Public criticism and advocacy campaigns (reputational risk)

- The company’s reliance on natural capital (physical risk)

Based on this assessment, CRR identifies and discusses the most salient risk categories for each company under analysis. These findings come together in a narrative about the likelihood of each risk occurring, which serves as a justification for the projections made under the various scenarios.

- Defining the scenarios

In order to assess a company’s exposure to transition and physical risks, the TCFD recommends the use of a set of scenarios that cover a reasonable variety of future climatic conditions, both favorable and unfavorable. Generally used scenarios that serve as input for such analysis include those from the IPCC and the IEA.

No such generally accepted scenarios are available that can be applied for equity-level deforestation analysis. Deforestation is not a static issue. Deforestation rates fluctuate over time and differ per region. Whereas deforestation rates in the Brazilian Amazon were particularly high at the beginning of the century, the pace of destruction of the Indonesian rainforest peaked around 2010. Now, rates in Brazil have spiked again, whereas palm oil-driven deforestation in Southeast Asia has come to a near halt. The impacts of deforestation on the bottom line of individual equities also vary. A major challenge of the equity-level scope is that the environmental costs of deforestation may be externalized and physical impacts are not necessarily felt by those that deforest.

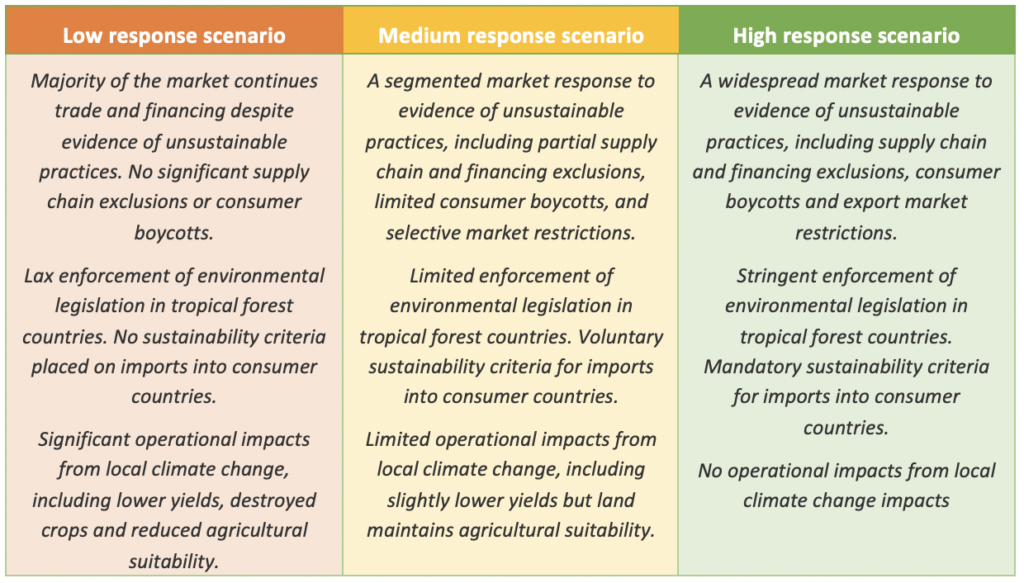

In order to assess future deforestation impacts on companies, CRR assesses three scenarios for each identified risk: a “low response,” a “medium response” and a “high response” scenario. The “low response” scenario assumes a future in which historical deforestation trends continue or increase. In this scenario, evidence of deforestation does not trigger significant stakeholder responses, but may have material physical impacts such as reduced agricultural yields, difficulties sourcing critical raw materials, or damage to properties. This is presented as a “business-as-usual” scenario. The “high response” scenario assumes a global zero-deforestation future. In this scenario, evidence of deforestation triggers widespread market responses and government interventions that directly affect companies. Such responses may include supply chain exclusions, loss of legal licenses and land deeds, restrictions to important export markets, sustained public criticism, and others. Physical impacts of deforestation are largely mitigated. The “medium response” scenario assumes a future in which global deforestation rates are halved. This scenario, which sees more moderate responses, principally functions as an illustration for the scale of potential financial impacts.

Figure 3: Definitional inputs for CRR’s deforestation scenarios

- Setting the metrics

The next step in CRR’s model is to assess the materiality of the identified risks based on a number of financial metrics. By assessing the impacts of the scenarios on a company’s financial statements and its market value, the framework allows to make quantitative projections of the deforestation impacts on a company’s financial performance.

- Income statement

Central to CRR’s model is the projection of a company’s “revenues at risk.” These revenues are defined as sales generated from clients or customers that may change their purchasing practices in response to evidence of deforestation, wildfires, or other sustainability issues. Such clients may include buyers with responsible sourcing policies, consumers, and export markets. When data is available, the exact share of revenues from such clients is used as the basis of the analysis. When such data is not available, the best estimations serve as input. The revenue-at-risk model is applied to the identified market risks and reputational risks.

Secondly, the model captures potential changes in a company’s cost of capital. Such changes may occur if the company faces difficulties obtaining financing from institutions with sustainability policies. Companies can be barred from certain financiers because of their geographical location, sector presence, or being added to exclusion lists. Companies may also face difficulties obtaining green financing at favorable rates. Projections are based on policy assessments of a company’s major shareholders, bondholders and loan issuers. Cost of capital is one relevant metric to calculate reputational risks.

Thirdly, CRR evaluates deforestation impacts on operating costs. Operating costs may increase as a result of fines, damages, legal costs, and stop-work orders issued by regulatory institutions. Companies found to illegally clear land and also those sourcing commodities from such land may face legal action from environmental enforcement agencies. In the palm oil sector, several traders have included demands for restoration and recovery in their responsible sourcing policies. Restoration of high conservation land is also a criterium for RSPO membership. Suppliers that wish to remain or re-enter NDPE supply chains can face recovery liabilities that may result in increased operating costs. To a lesser extent, companies may also incur higher operating costs as a result of more stringent implementation of sustainability policies. Operating costs are a relevant metric for regulatory and market risks.

- Balance sheet

Both the transition and physical risks of deforestation can impact a company’s fixed assets. Stranded assets are an increasingly recognized risk within agricultural commodity supply chains. Stranded land is a salient risk in the palm oil sector, whereby large tracts of forest and peatland remain within oil palm concessions. When the market and regulatory risks of developing such lands outweigh future income, this land should be considered stranded. Farmland assets held by institutional investors may also face significant devaluations when the legality of ownership is challenged or when local climate change impacts negatively affect agronomical suitability. Companies faced with the risk of stranded assets may have to write-off significant asset values.

In the case of livestock sectors, supply chain disruptions and plant closures can result in a devaluation of current assets. For example, pandemic outbreaks and forced temporary plant closures may reduce the value of biological assets as animals have to be preemptively culled.

Intangible assets may be hurt by a company’s reputational damage. Goodwill and trademarks may have to be devalued in case a company does not adequately respond to a public controversy. A company’s future earnings potential may be affected by an inadequate response to controversies.

- Bringing it all together

While CRR projects the impacts on the income statement and balance sheet per identified risk, the final step in CRR’s model is calculating the cumulative impacts. CRR projects a company’s market value and share price under all three scenarios by adding up the adjusted earnings and asset values.

CRR’s model of valuation multiples within peer groups converts the outcomes of the scenario analysis into monetary metrics for equity and debt investors. The scenario outcomes are assessed through benchmarking against industry averages or medians over a five-year period, allowing CRR to estimate share price impacts and contrast them with the current trading price of listed entities. As a result, CRR identifies under- or over-pricing in relative terms and illustrates the downside risk as well as opportunities. The relative valuation approach is particularly suitable to quantify potential reputational impacts.

Additionally, CRR’s model includes a Discounted Cash Flow (DCF) valuation to estimate the impacts of the scenarios on the value of a company. The DCF model first provides and overview of the current state of a company and subsequently integrates the outcomes of the sustainability risk analysis into projected company valuations.