The beef and soy sectors have been two of the major drivers of deforestation in the Brazilian Amazon and Cerrado biomes in recent years. Financial institutions with exposure to these sectors may be inadvertently contributing to climate change and biodiversity loss. As global stakeholders react to these threats, financial institutions may become increasingly more exposed to financial risks. This report, using Forests & Finance data, shows who is financing these two sectors.

Download the PDF here: Domestic Banks Finance 74% of Brazilian Beef & Soy

Key Findings:

- Financing provided to the beef and soy sectors in Brazil totaled USD 100 billion from 2013 to April 2020. According to the Forests & Finance database, USD 82 billion of loans and USD 13 billion of underwritings, as well as USD 5 billion in shares and USD 1 billion in bonds, were provided to these sectors.

- 74 percent of the total identified financing originated from Brazilian financial institutions. They provided USD 66.2 billion in loans and USD 5.4 billion in underwriting. They also hold USD 3.0 billion in shares and USD 3.0 million in bonds. Banco do Brasil provided by far the highest amount of financing (USD 42.4 billion).

- Foreign financial institutions provided USD 14.5 billion to the beef sector and USD 11.2 billion to the soy industry. Santander, Rabobank, HSBC, and JPMorgan Chase are among the top-25 financiers.

- These four banks have deforestation policies while financing soy and beef companies that have been repeatedly linked to deforestation in their supply chains. Their main exposure is to Brazil’s three big meatpackers, JBS, Marfrig, and Minerva, along with the soy trader Cargill.

- The key element in the financing chain is Brazil’s National Rural Credit System. Managed by the Central Bank of Brazil, the system has channeled loans to agriculture sectors, mainly beef and soy, constituting 91 percent of all identified loans in this research. Because of legal requirements, around two-thirds of the funding comes from deposits at Brazilian banks, while the interest rates on approximately 75 percent of the credit is subsidized.

- European investors have leverage to engage on deforestation. Since the Rural Credit System does not offer an effective mechanism to promote sustainable agriculture, increased attention from the EU and the ECB on deforestation risk may lead to European financiers becoming more alert about reputation and investment risk.

Beef and soy sectors are the two major drivers of deforestation in Brazil

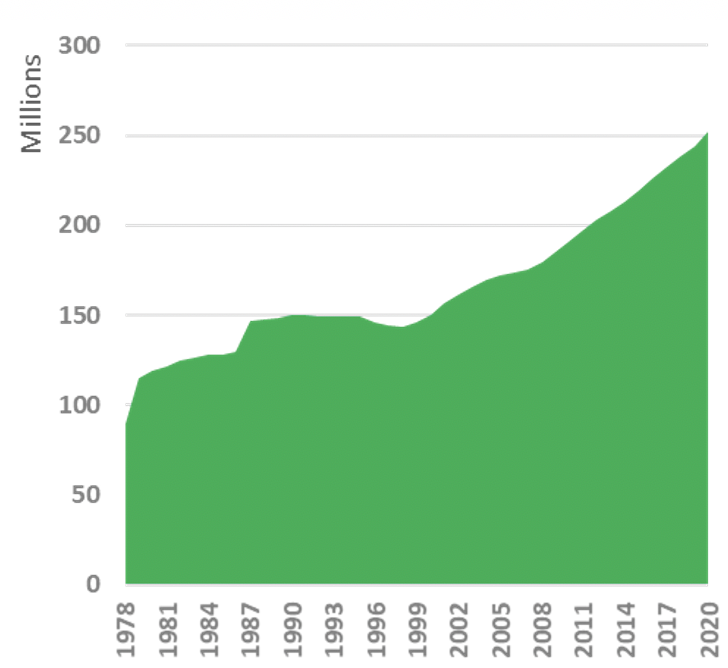

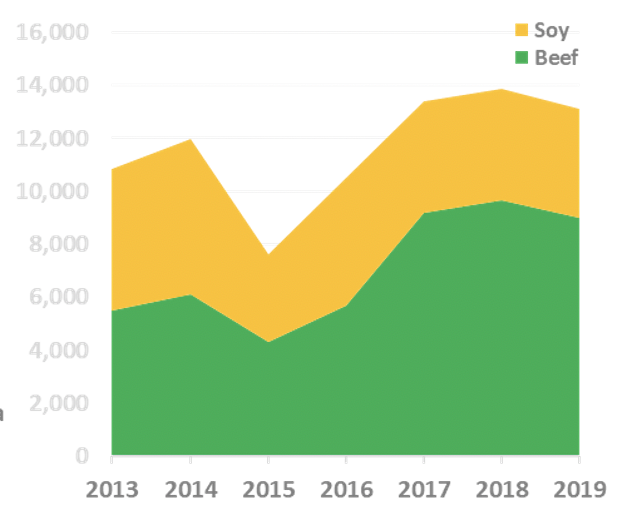

In recent years, cattle ranching in the Amazon biome and soy cultivation shifting to the Cerrado have been the most important drivers of deforestation in Brazil. As Chain Reaction Research’s August 2020 report on the Brazilian beef supply chain showed, the sector’s expansion (Figure 1) is driven by increasing demand in export markets amid favorable political, legislative, and enforcement changes. Cattle ranching is responsible for large-scale deforestation, estimated to account for 80 percent of land clearing in every country with Amazon forest cover. Another motivation for cattle rearing is conversion of the underlying land, which can be used for different commodities. Cattle rearing is a low-cost operation that prevents forests from growing back.

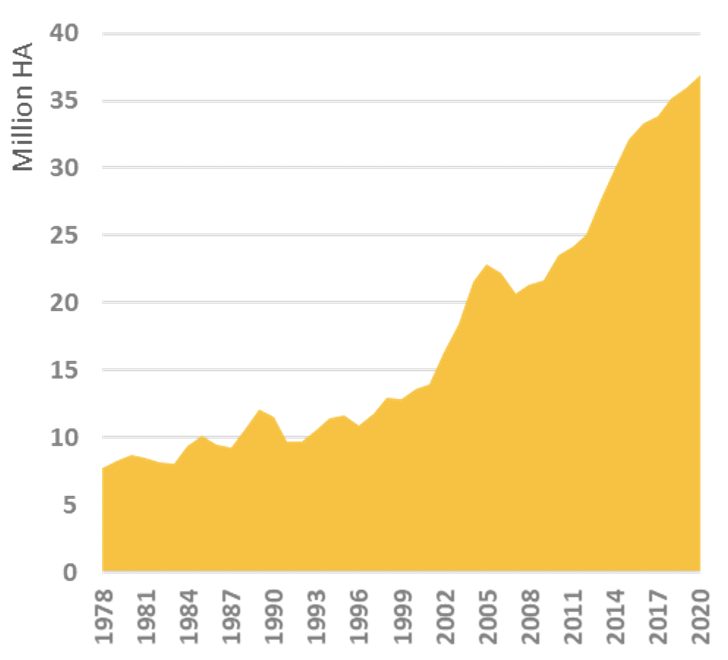

The sharp rise in soy cultivation area (Figure 2) is driven by its role as an important source of easily digestible, high-quality protein for livestock farming as well as a source of vegetable oil. Soybean meal accounted for around 70 percent of the world’s production of oilseed meal for the livestock industry in 2019/20.

Annual data from INPE shows that after eight years of decline, the deforestation rate in Brazilian Amazon increased again in 2013, and reached 11.1 thousand km2 per annum in 2020, the highest annual rate since 2008. In Cerrado Biome, the deforestation estimate for 2019 was 6.5 thousand km2.

Figure 1: Cattle Herd Size Brazil

Source: USDA

Figure 2: Soy Cultivation Area Brazil

Source: USDA

Brazil’s beef and soy sectors have received USD 100 billion of financing

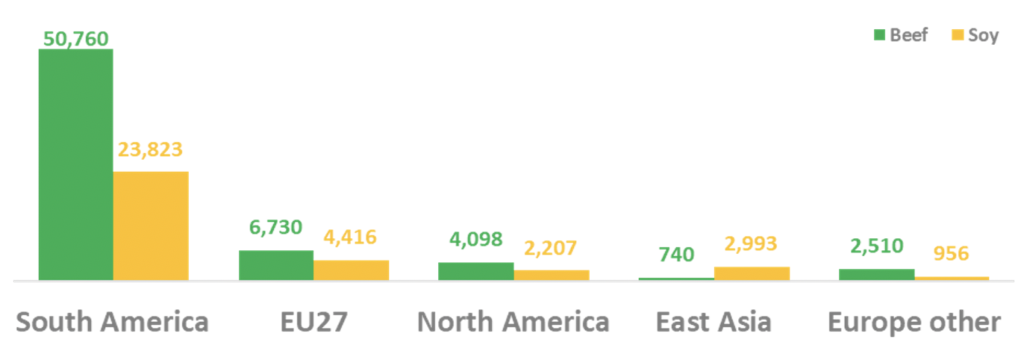

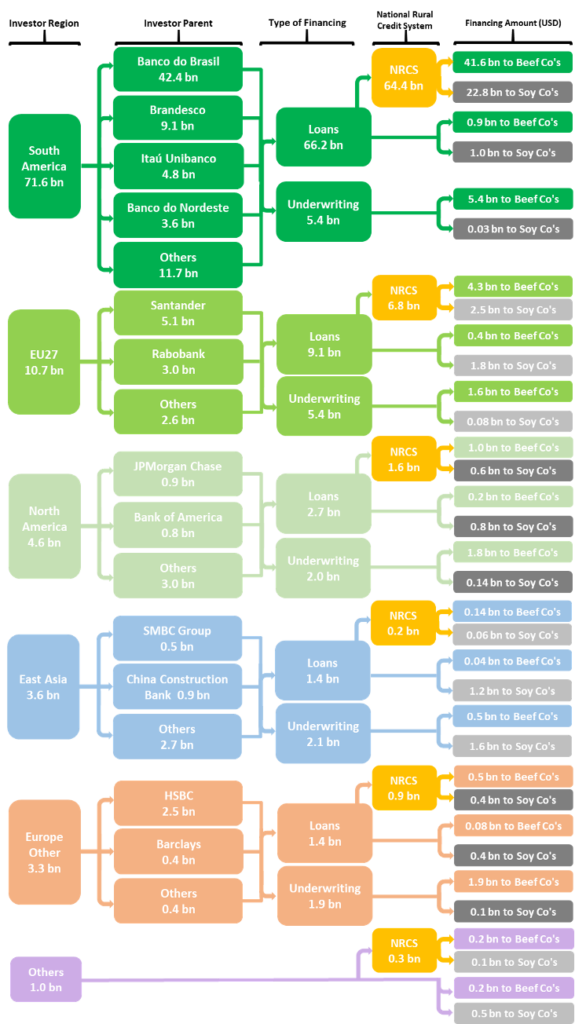

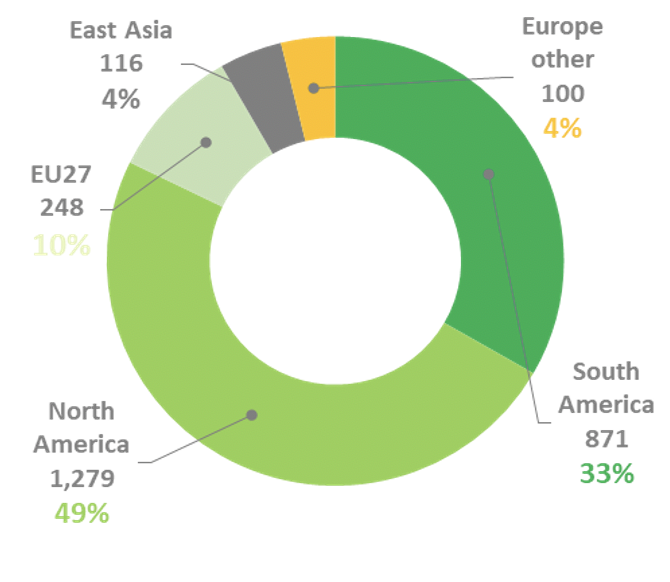

On a regional basis, South American financial institutions provide 74 percent of the total financing since 2013 that was identified by Forests & Finance. EU27 and North America follow with 11 percent and 6 percent, respectively. While the type of financing from EU27 is concentrated on loans (81 percent), North American banks and investors are evenly active in every form categorized in this report. Financiers from East Asia and other European countries provided relatively small but still sizable funds, while East Asia was more focused on the soy sector and Europe (ex-EU27) more focused on beef.

Figure 3: Total identified financing by source region (in USD millions)

Source: forestsandfinance.org, the region “Europe Other” mainly consists of UK, Norway and Switzerland

Loans as the dominant type of financing

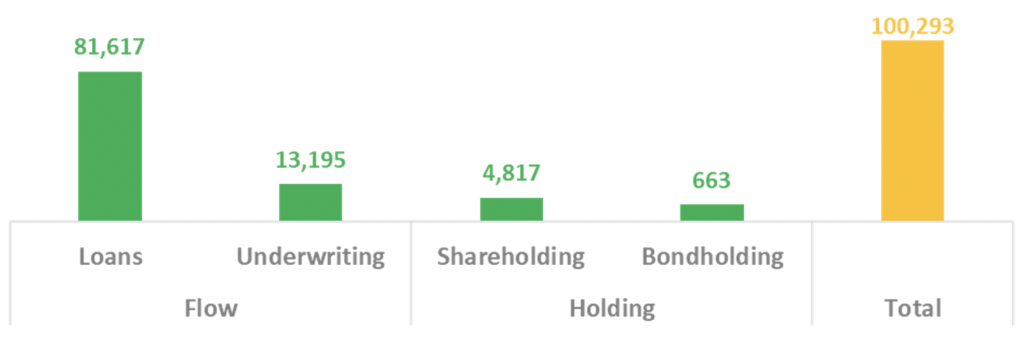

Loans accounted for 81 percent of total financing identified by Forests & Finance. Forests & Finance identified USD 81.6 billion worth of loans, which stood out as the most important source of financing for the two sectors. Underwritings of USD 13.2 billion were the second largest source of financing. However, they involved more foreign investments due to the more international nature of share and bond issuances. Share and bond holdings were both relatively small.

Figure 4: Total identified financing by type (in USD millions)

Source: forestsandfinance.org, Loans and underwriting constitute the flow type of financing whereas share and bond holdings are categorized as holdings. 95% of financing is in the form of flows, which represents all identified loans and underwriting between 2013 and April 2020 on a cumulative basis. The holding type of financing reflects the most recently available filings in April 2020.

Figure 5: Map of loan and underwriting provided to Brazilian beef and soy sectors by banks

Source: forestsandfinance.org, NRCS: National Rural Credit System, in USD

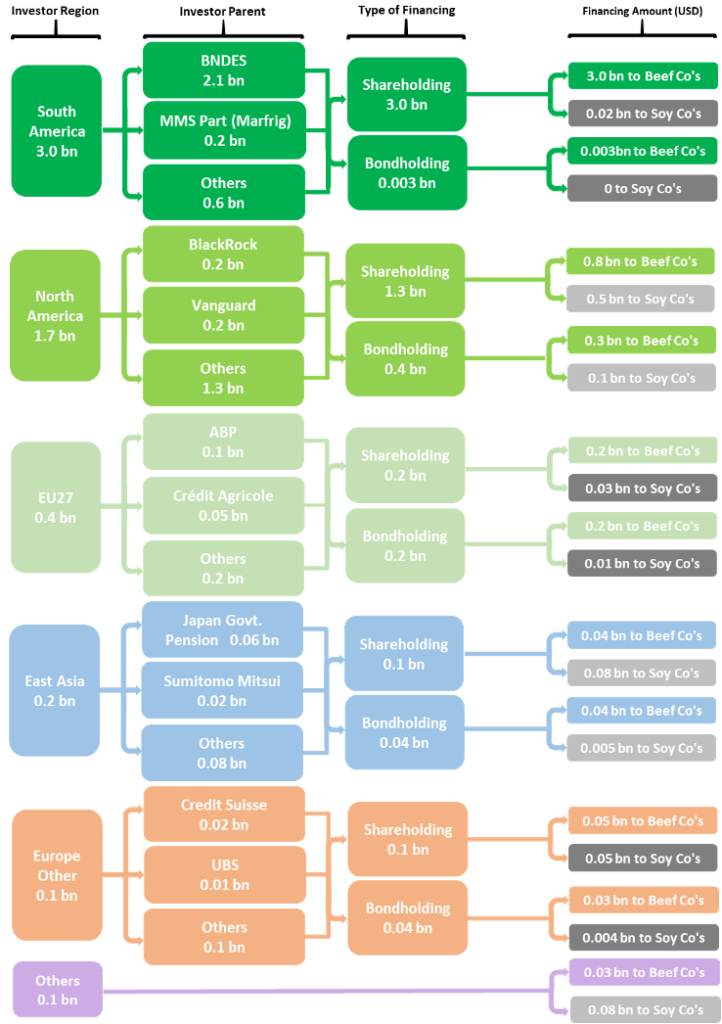

Figure 6: Map of share and bond holdings in Brazilian beef and soy sectors by investors

Source: forestsandfinance.org, in USD

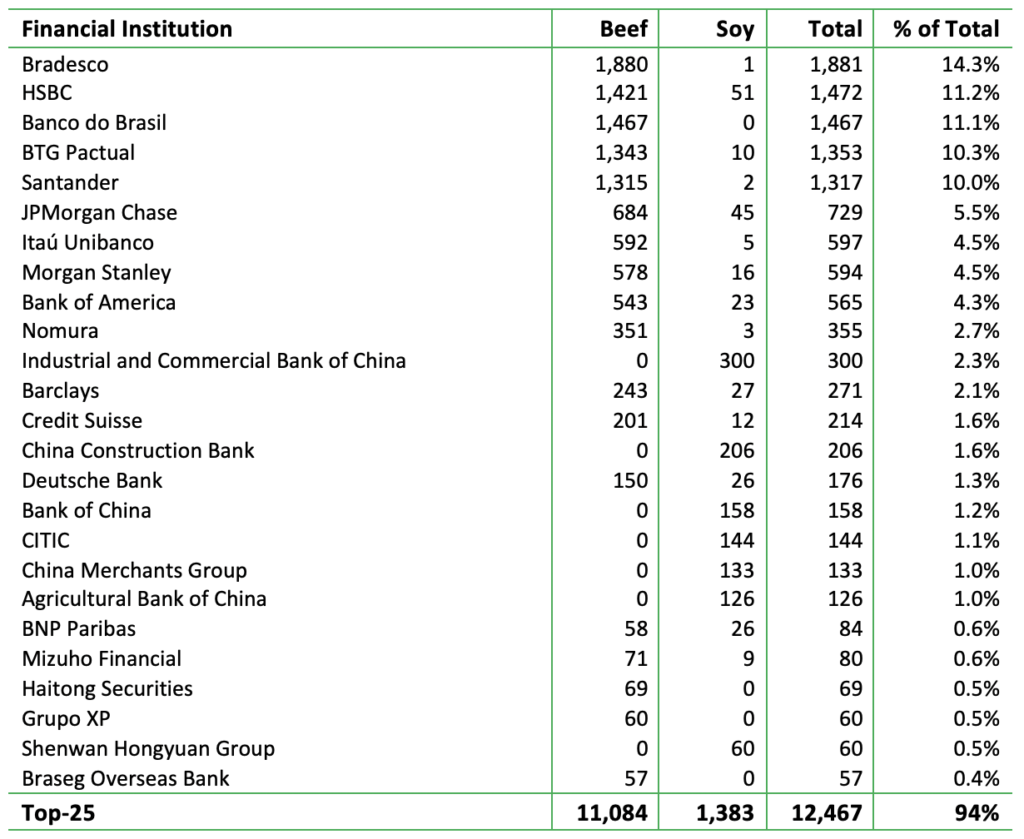

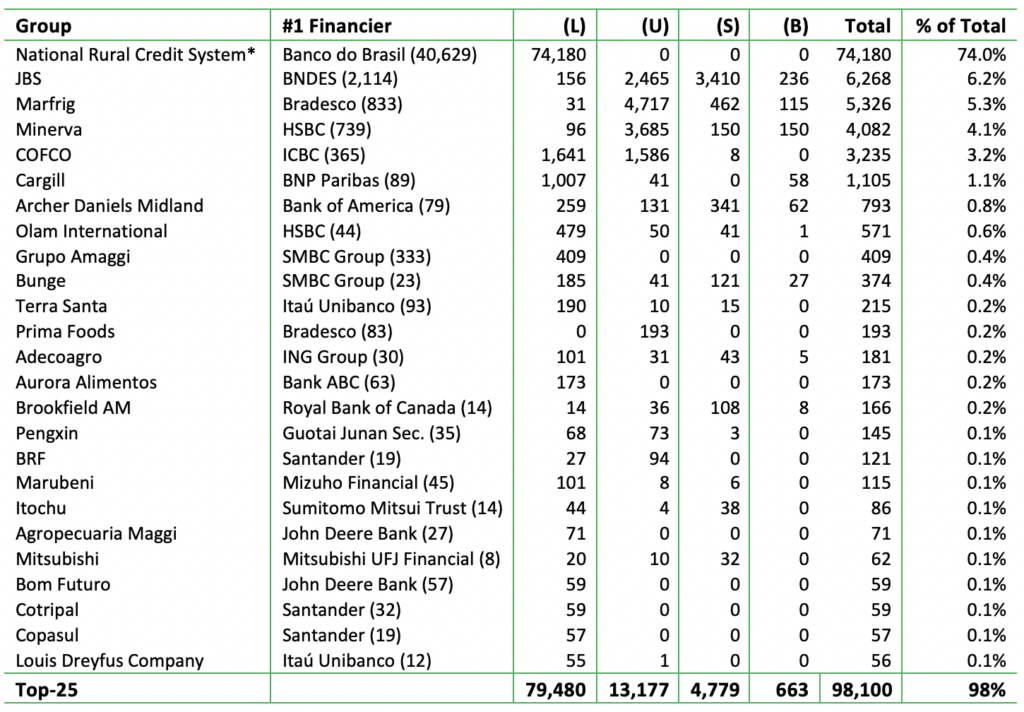

Banco do Brasil is the largest financier of Brazilian beef and soy

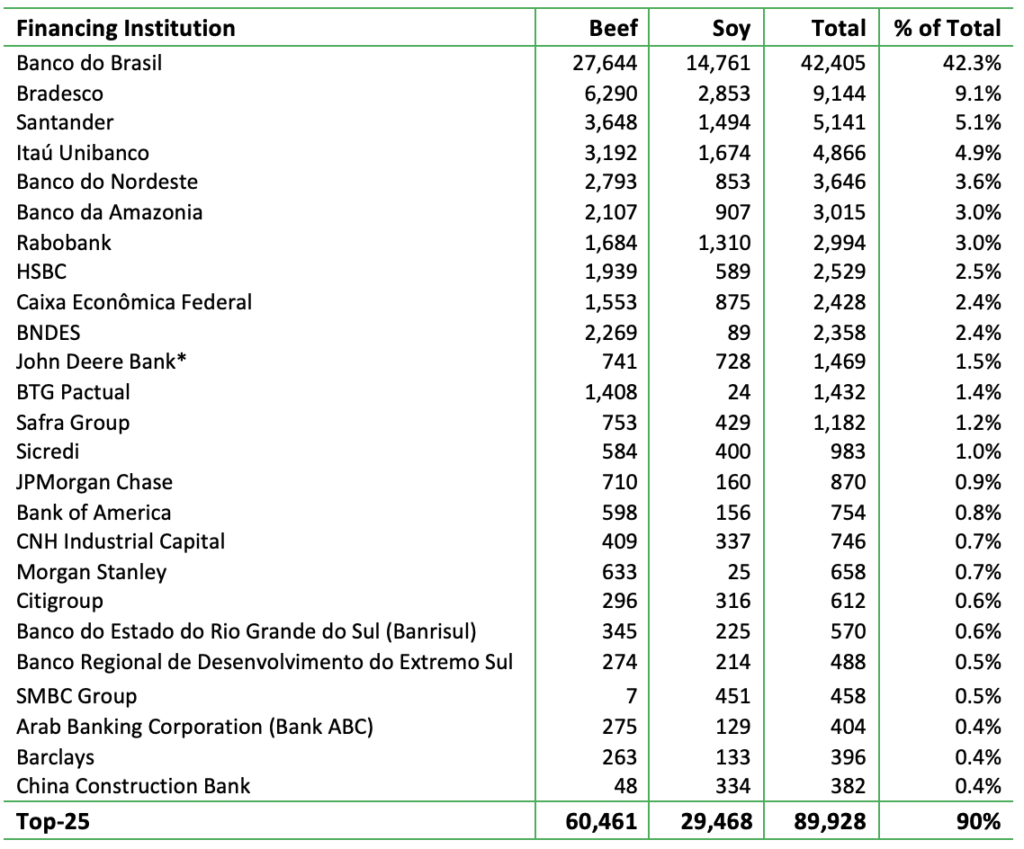

Brazilian banks provided the majority of the total financing to beef and soy sectors, accounting for 81 percent of the total. Twelve of the top-25 financiers listed in Figure 7 are Brazilian banks. Government-controlled Banco do Brasil (59 percent owned by federal bodies of Brazil) tops the list by a very wide margin. Banco do Brasil provided USD 42.4 billion to the beef and soy sectors between 2013 and April 2020 (42.3 percent of total), mostly in the form of loans, but also through underwriting, bonds and shareholdings.

In total, the top 25 financiers accounted for 90 percent of identified financing provided to the two sectors, with USD 60.5 billion to beef and USD 29.5 billion to soy. Financial institutions from outside of Brazil with sizeable exposure are Santander from Spain with USD 5.1 billion, Rabobank from Netherlands with USD 3.0 billion, HSBC from United Kingdom with USD 2.5 billion, and JPMorgan Chase from the United States with USD 0.9 billion.

Figure 7: Top-25 financiers (in USD millions)

Source: forestsandfinance.org, viewed in October 2020,*John Deere Bank is the lease financing arm of the agriculture equipment company

Foreign institutions with environmental commitments

All foreign financial institutions identified with meaningful exposure have financing relationships with at least one of the companies in Figure 8, which is a selection of companies with links to deforestation previously mentioned by Chain Reaction Research (JBS, Marfrig, Minerva, Cargill, Bunge). Even so, the financial institutions have remained active in their relationships with these companies, based on the most recent financing data.

Figure 8: Selected foreign institutions’ exposure to forest-risk companies (in USD millions)

Source: forestsandfinance.org, (L): Loans, (U): Underwriting, (S): Shareholding, * National Rural Credit System, the USD value of exposures shown on the table were adjusted to present the proportions related to beef and soy activities. The original amounts are higher on a whole company basis.

The following list shows the environmental policies of the financial institutions listed in Figure 8 and The Forests & Finance Bank Policy Assessments (see Appendix 1):

- Santander: “Zero net deforestation by 2020” – Soft Commodities Compact

- Rabobank: “Zero net deforestation by 2020” (see source) – Soft Commodities Compact

- The bank’s policy was assessed as “Strong forest-risk sector policy” and scored 39 out of 50 on Forests & Finance Bank Policy Assessment.

- HSBC: According to the bank’s Agricultural Commodities Policy document under Soy, Cattle Ranching and Rubberwood sectors, “HSBC will not knowingly provide financial services to high-risk customers involved directly in or sourcing from suppliers involved in Deforestation, that is: the conversion of areas (often forests) necessary to protect HCVs; the conversion of primary tropical forests; or clearance by burning.”

- The bank’s policy was assessed as “Good forest-risk sector policy with some gaps” and scored 30 out of 50 on Forests & Finance Bank Policy Assessment.

- JP Morgan Chase: “Zero net deforestation by 2020” (see source) – Soft Commodities Compact

- The bank’s policy was assessed as “Fair forest-risk sector policy with gaps” and scored 28 out of 50 on Forests & Finance Bank Policy Assessment.

- Bank of America: According to the bank’s Environmental and Social Risk Policy Framework document under prohibited list, “Bank of America will not knowingly engage in illegal activities including, Illegal logging or uncontrolled fire – including transactions in which a client engages in illegal logging or uncontrolled use of fire for clearing forest lands.”

This group of financiers, dominated by European FIs, provide 14 percent of the total financing to Brazilian soy and beef companies. They may face reputation risk in view of their deforestation policies and changing (European) regulation on deforestation and due diligence of supply chains.

Providing financing to forest-risk sectors, in this case beef and soy, especially to JBS, Marfrig, Minerva and Cargill and Bunge, (a selection of companies with links to deforestation mentioned by CRR) may expose the banks to financial and reputation risks through deforestation. In particular, financiers from Europe could face reputation risk due to increasing focus on deforestation-free supply chains by European regulations.

Loans are the largest source of financing with the rural credit system as the main channel

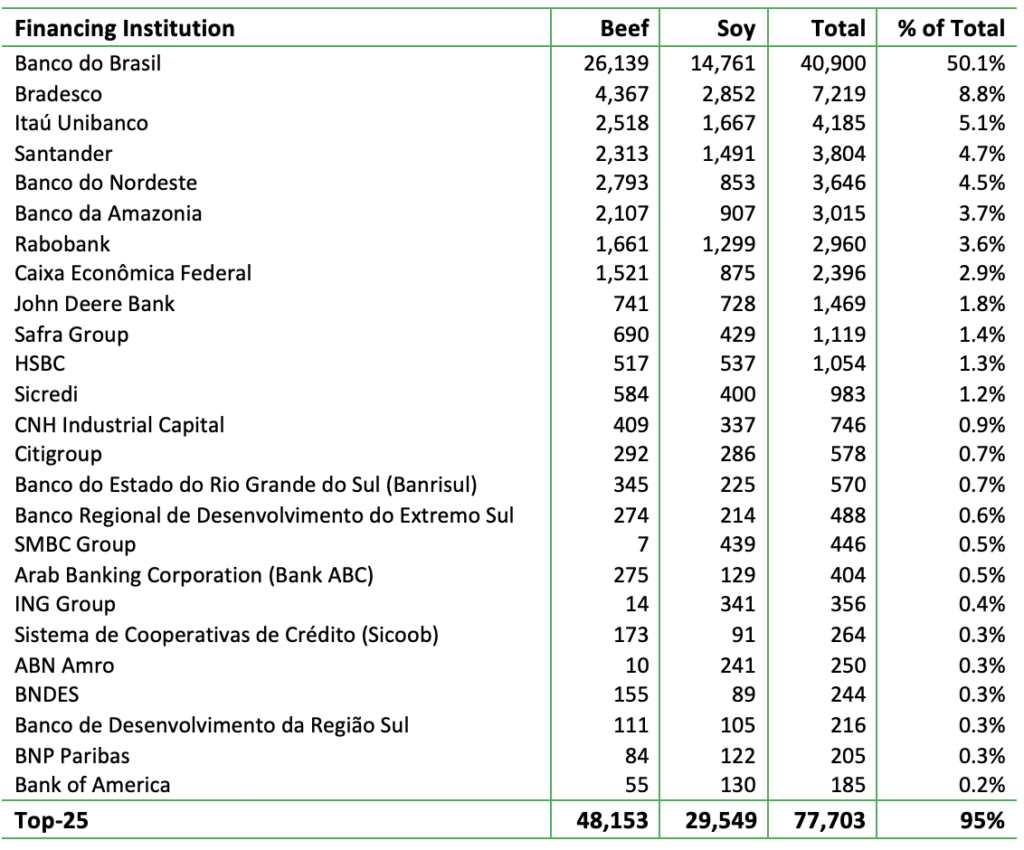

Ninety-one percent of loans were extended via the National Rural Credit System, where the ultimate receiver and the maturity of the funds are not disclosed. The Top-25 list of loan providers (see Figure 9) covers 95 percent of all loans that originated between 2013 and April 2020. While Brazilian banks populate most of the list with Banco do Brasil in the lead, a majority of these local loans are facilitated through a financing system called Sistema Nacional de Crédito Rural (National Rural Credit System). The information provided by the Central Bank of Brazil, which also manages the credit system, suggests that the funding for the program is mainly rule-based. For example, it includes legal reserve requirements for demand and rural savings deposits at Brazilian banks. Additionally, interest rates for the majority of the credit that the system provides are subsidized. More detailed information on how the data is incorporated into the Forests & Finance database is included in Box 1 below.

Figure 9: Top-25 Loan Providers (in USD millions)

Source: forestsandfinance.org

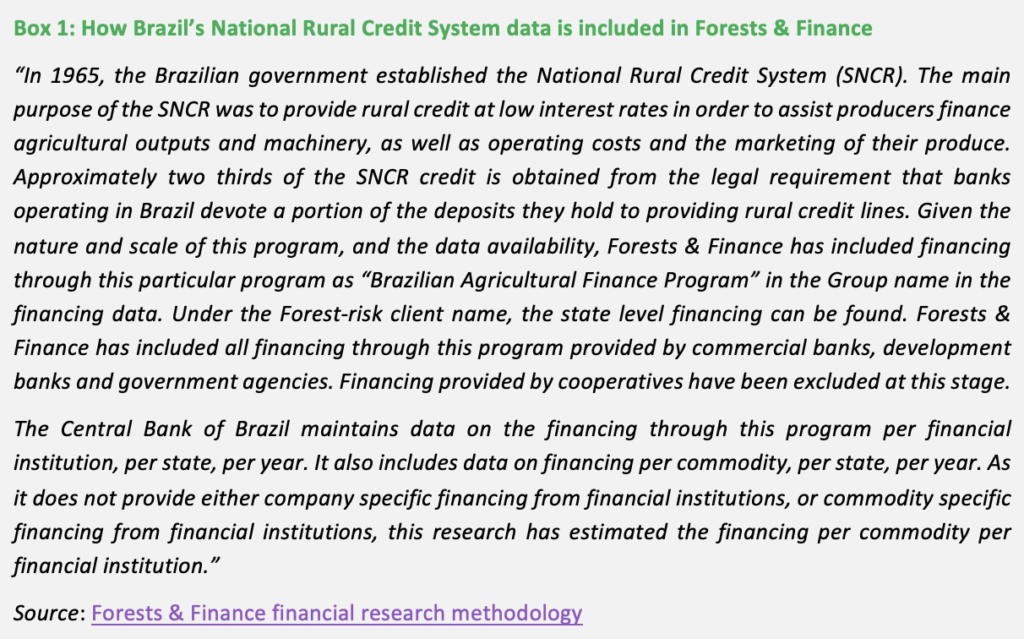

Brazil’s National Rural Credit System

Analysis of the National Rural Credit System based on the data from the Central Bank of Brazil reveals that the majority of the provided rural credit has flowed to the beef and soy sectors. Although the total outstanding loans extended via the program grew from BRL 272 billion (USD 82 billion) in May 2017 to BRL 320 billion (USD 59 billion) in May 2020, the amount in USD declined due to a sharp devaluation of the local currency. The total outstanding loan amount in the program corresponded to, on average, 9.5 percent of the loans in the whole Brazilian banking system for the last four years. The level of annual origination of loans implies around 20 months of average maturity for the loans in the system.

Figure 10: The National Rural Credit System in Brazil (in USD billions)

Source: Central Bank of Brazil

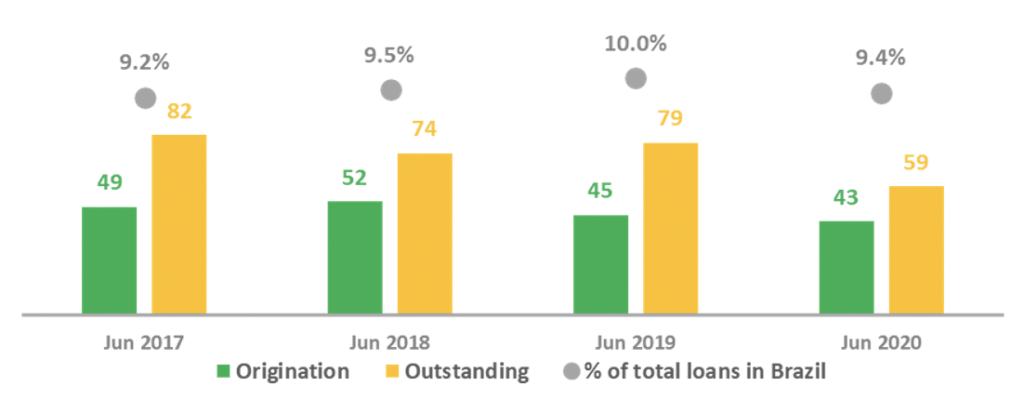

Figure 11: National Rural Credit System by type of recipient and subsidy

Source: Central Bank of Brazil

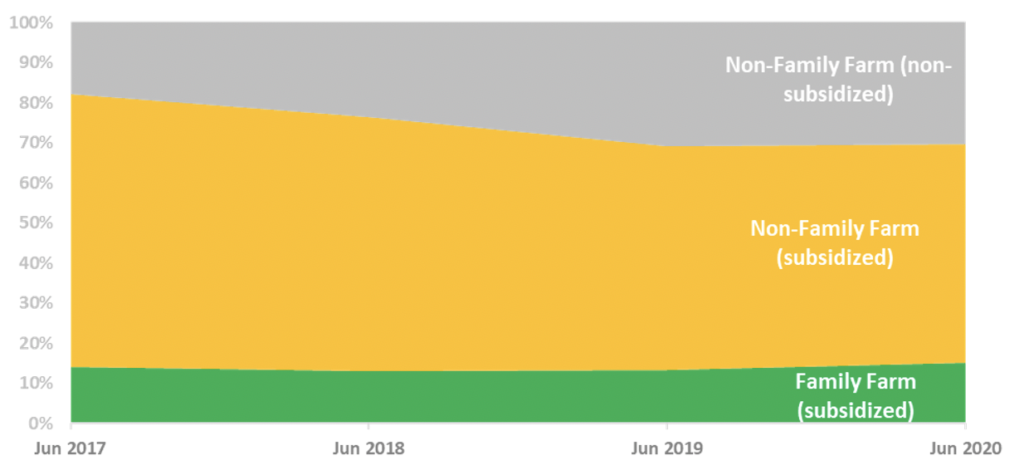

On average, 75 percent of the loans the National Rural Credit System provided between June 2017 and June 2020 was subsidized with lower-than-market interest rates. Although small family farms received lower interest rates with more subsidies (see Figure 11), they received only about 13 percent of total loans. Subsidized annual interest rates were 30 percent lower compared to freely set (non-subsidized) rates for non-family farms and 55 percent lower for family farms.

Figure 12: Average annual interest rates on National Rural Credit System in Brazil

Source: Central Bank of Brazil

The effect of the National Rural Credit System on deforestation

Research on the impact of the National Rural Credit System points to a change in the system’s lending policy in 2008. Approval of subsidized rural credit in the Amazon is conditioned upon proof of compliance with environmental regulations. Mostly through a reduction in credit volumes (mainly in municipalities where cattle ranching is the main economic activity), deforestation in the Amazon biome between 2009 and 2011 was 60 percent lower than it would have been without credit restrictions.

In its 2020 policy note, the World Bank stated that a small number of large farms receive the majority of the rural financing, while 85 percent of all farmers in Brazil do not have access to credit. Additionally, most of the rural credit is for short-term working capital type financing, with limited longer-term investment financing. Thus, the probability of rural credit positively affecting sustainable agriculture investments is deemed to be low.

Figure 13: Loans by Region (in USD millions)

Figure 14: Loans* (USD millions)

Source: forestsandfinance.org. *The difference in loan flows between different figures in the report stems from the sector adjustments in Forests & Finance data (see appendix 1) as well as exclusion of some of the funders in National Rural Credit System (see box 1)

Underwriting

The cumulative underwriting of share and bond issuances between 2013 and April 2020 amounts to USD 13.2 billion. Seventy-seven percent of this total is provided for the bond issues of the three big meat packers — JBS, Marfrig and Minerva. Since almost all these bond issuances were USD denominated, international financial institutions had elevated participation, underwriting 60 percent of the total deal sizes, significantly higher compared to their contribution in loans.

Figure 15: Top-25 Underwriters (in USD millions)

Source: forestsandfinance.org

Historical development

Total identified underwriting fell as low as USD 334 million in 2015 mainly because of drought. That was followed by a boom year with deals reaching USD 3.2 billion.

Figure 16: Regional Underwriting (in USD millions)

Source: forestsandfinance.org

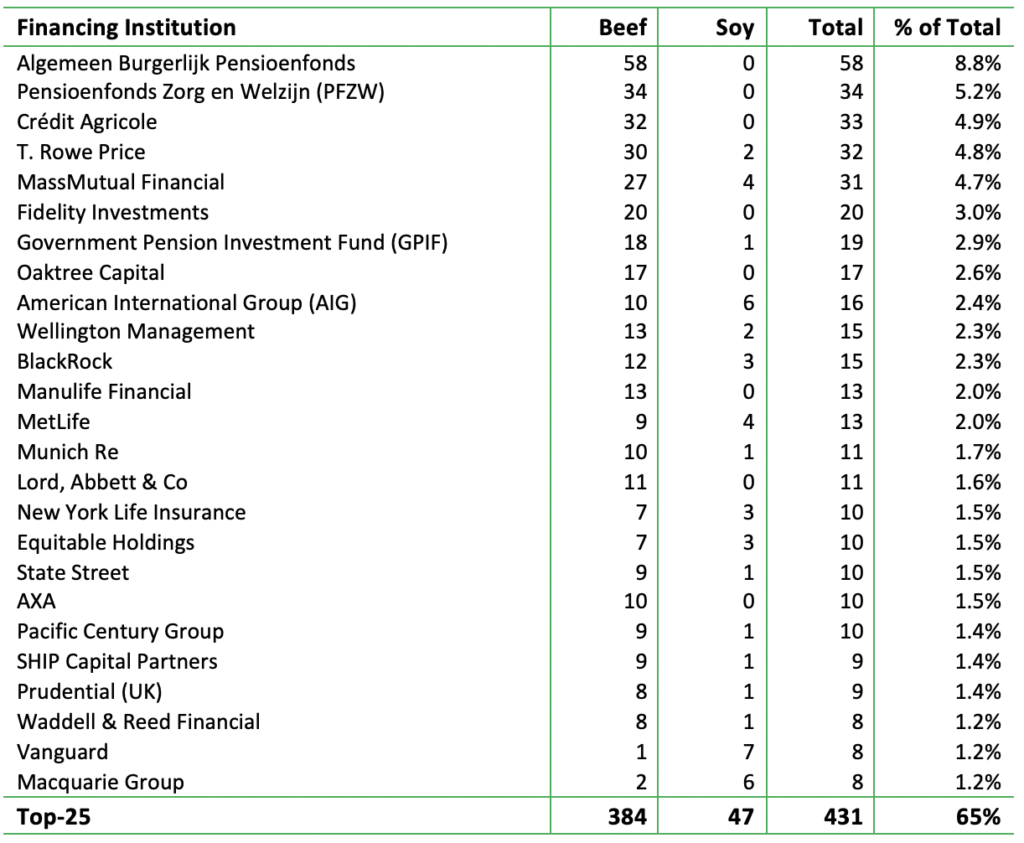

Shareholding

Shareholding data is more diversified due to the involvement of global equity funds, specifically in the form of ETFs. When BNDES’ (Brazilian Development Bank) 21.3 percent stake (worth USD 2.1 billion, adjusted for the share of JBS’ beef operations) in JBS is excluded as an outlier, North American investors have the highest percentage at 49 percent vs. 33 percent for South America. BNDES divested from Marfrig at the end of 1Q2020, selling its 30 percent share in the company (worth around USD 500 million). BNDES has stated its aim to divest from JBS as well, but the sale has not materialized yet.

Figure 17: Regional Shareholding (in USD million)

Source: forestsandfinance.org, adjusted for BNDES stake in JBS

Figure 18: Top-25 Shareholders (in USD millions)

Source: forestsandfinance.org

Bondholding

Bondholding is the smallest area of identified financing received by beef and soy sectors in Brazil with only USD 663 million, amounting to just 0.7 percent of the total identified financing. Local investors from the South American region have virtually no holdings in the bonds, while North America (58 percent) and EU27 (29 percent) have the highest exposure.

Figure 19: Regional Bondholding (in USD millions)

Source: forestsandfinance.org

Figure 20: Top-25 Bondholders (in USD millions)

Source: forestsandfinance.org

European financiers in a position to engage on sustainable soy and beef

By financing 12 percent of the total Brazilian beef and soy financing, European investors and banks have the potential to contribute to reducing deforestation in the beef and soy supply chains. When JPMorgan Chase and Bank of America are included, 14 percent of financing is through FIs with policies on deforestation.

A large part of the financing of the Brazilian soy and beef sectors flows through rural credit from Brazilian banks, which currently have minimal impact on sustainable agriculture. However, European financers face reputation risk due to the development of EU regulations on deforestation in supply chains. Moreover, the European Central bank (ECB) gives an increasing weight to climate change, deforestation, and biodiversity risks. All financiers face investment risks since the companies they finance may be confronted by an accumulation of market access risk, regulation risk, and financing risk. Equity holdings could also lose value due to reputation risk.

As European banks and investors are also financed by their own investors, these financial institutions are also in position to prevent a repetition of losses made through financing the fossil fuel industry, which is also linked climate change.

Appendix 1: Forests & Finance

The aim, scope, methodology, and partners of Forests & Finance, as summarized on the website:

Forestsandfinance.org aims to highlight the role that finance plays in enabling tropical deforestation. It is the result of extensive research and investigations by a coalition of campaign and research organizations including Rainforest Action Network, TuK INDONESIA, Profundo, Amazon Watch, Repórter Brasil and BankTrack. The Forests & Finance database assesses the financial services received by over 300 companies & over 16,000 small-scale forest-risk companies that received finance who are directly involved in the beef, palm oil, pulp & paper, rubber, soy and tropical timber (“forest-risk sector”) supply chains and whose operations impact natural tropical forests in Southeast Asia, Brazil as well as Central and West Africa. Not all of the companies selected for the database are engaged in harmful operations. However, all are engaged in large scale operations in tropical forest regions that have a high risk of causing deforestation and associated social impacts. Financial institutions that do business with these companies are therefore highly exposed to deforestation risks.

Financial databases Refinitiv (formerly known as Thomson EIKON), Bloomberg IJGlobal, TradeFinanceAnalytics, company register filings, as well as publicly available company reports, were used to identify corporate loans, credit and underwriting facilities provided to the selected companies in the period 2013-2020 (April). Investments in bonds and shares of the selected companies were identified through Refinitiv and Bloomberg at the most recently available filing date in April 2020. These financial databases provide access to real time market data, news, fundamental data, analytics, trading and messaging tools. The BNDES Transparency portal and Brazil’s Central Bank portal were used to identify additional financial flows to forest-risk companies in Brazil. This research provides a deal-level dataset of specific relationships between selected companies and any linked financial institution. Of the more than 300 companies researched, only 230 companies had identifiable financing where the financier, financing amount, and start date were known within the period of study.

Companies with business activities outside of the forest-risk sector recorded amounts reduced to more accurately present the proportion of financing that can be reasonably attributed to the forest-risk sector operations of the selected company. Where available financial information did not specify the purpose of investment or receiving division within the parent company group, reduction factors were individually calculated by comparing a company’s forest-risk sector activities relative to its parent group total activities. Further adjusters were calculated for companies operating in multiple geographies within the scope of this research.

The commercial banks identified in this study were evaluated to determine the strength of any publicly available policies relevant to tropical forest-risk sector investment decision-making, and subsequently scored against a range of criteria incorporating environmental, social and governance standards. Each of the major banks was allocated a score on the scope of its policies and its environmental and social standards. The Forests & Finance Bank Policy Assessment Methodology is based on the Fair Finance Guide (FFG) with a focus on the forest-risk sector.

The data and assessments presented in this website have not been provided by or authorized by any of the financial institutions or clients concerned. While every attempt has been made to research and present data and assessments accurately and objectively, it is difficult to guarantee complete accuracy. This is not least because of the lack of consistency and transparency in how financial institutions and forest-risk sector clients record key financial and company information. Where there has been ambiguity in source information of financial services, the authors of this website have acted cautiously, resulting in a likely underestimation of the true amounts of finance involved. The authors are committed to correcting any identified errors at the earliest opportunity.

Visit the website for more information and to use the database.

Appendix 2: Top Recipients of Financing on identified by Forests & Finance

Figure 21: Top-25 Recipients of Financing (in USD millions)

Source: forestsandfinance.org