JBS, Marfrig, and Minerva are the largest meat processors in Brazil, dominating beef processing and exports. The cattle industry is the main driver of deforestation in Brazil. This report, which builds on CRR’s earlier JBS analysis, assesses the companies’ exposure to deforestation and analyses their market, reputation, and technology risks. CRR has located and monitored 1,545 direct suppliers and 3,164 indirect suppliers that are connected to the top three meatpackers in seven states in the Cerrado and Amazon biomes.

Download the PDF here: JBS, Marfrig, and Minerva: Material Financial Risk from Deforestation in Beef Supply Chains

REPORT WEBINAR RECORDING

Key Findings:

- The Brazilian cattle industry is dominated by JBS, Marfrig, and Minerva. JBS is the largest animal protein company and the second-largest food company in the world; Marfrig is the world’s second-largest beef company by production capacity; and Minerva is an export-oriented beef company.

- Marfrig, Minerva, and JBS have focused on compliance in direct supply chains, but show little progress on monitoring indirect supply chains. The implementation of the G4 and TAC agreements by the companies still has significant gaps and delays.

- The top three’s exposure to deforestation is higher in their indirect supply chains than in their direct supply chains, according to CRR’s sample. For instance, 1,874 indirect suppliers to JBS cleared 50,852 ha from 2008 to 2019, and 983 direct JBS suppliers deforested 20,296 ha. JBS has a total of 50,000 direct suppliers, with an unknown number of indirect suppliers.

- The big three’s 40-58 percent exposure to debt financing and their 24-32 percent exposure to European financing may lead to (re)financing risks. JBS and Marfrig rely on European financial institutions for 30 percent of their financing. Santander, Rabobank, HSBC, BNP Paribas, and Barclays have leverage to engage.

- The meatpackers’ 11-33 percent exposure of total turnover to China and Europe poses market risks. A decline in demand related to deforestation regulation in Europe and COVID-19, along with technology changes in China, could have a material negative impact on earnings capacity.

JBS, Marfrig, and Minerva: Three meatpackers dominate beef production and exports

Since 2017, Brazil has been the largest exporter of beef in the world, accounting for 21.2 percent of total global beef exports in 2019. Brazilian beef production has grown steadily in the past two decades, and in 2019, the livestock sector represented 8.5 percent of Brazil’s GDP. The beef industry’s expansion is the result of stable feed prices, increasing domestic demand, and strong Chinese imports. Since the outbreak of the African swine fever in August 2018, pork production across Asia was decimated, spurring an increase in beef imports. While most Brazilian beef is consumed domestically, the proportion of beef destined for export markets has increased from 18 percent in 2015 to 23 percent in 2019. Key importing markets include China, Hong Kong, Egypt, Chile, the United States, and the European Union. During the first half year of 2020, the volume of Brazilian bovine meat to China increased by 148 percent compared to the previous year. During this period, China received 52 percent of all Brazilian beef exports.

The Brazilian cattle industry is dominated by a handful of meat processing companies. JBS, Marfrig, and Minerva have the highest slaughtering capacity among a large number of meatpackers. The industry is characterized by heightened and continued pressure from investors, policymakers, and civil society over its role in driving deforestation, forest fires, and human rights abuses in the Brazilian Amazon. To give but one example, the EU-Mercosur agreement, which totals about EUR 36 billion (USD 43.8 billion) of EU imports per year, is under threat due to concerns of deforestation and forest fires in the Amazon, not least driven by the expansion of cattle ranching.

JBS: The largest animal protein company and the second-largest food company in the world

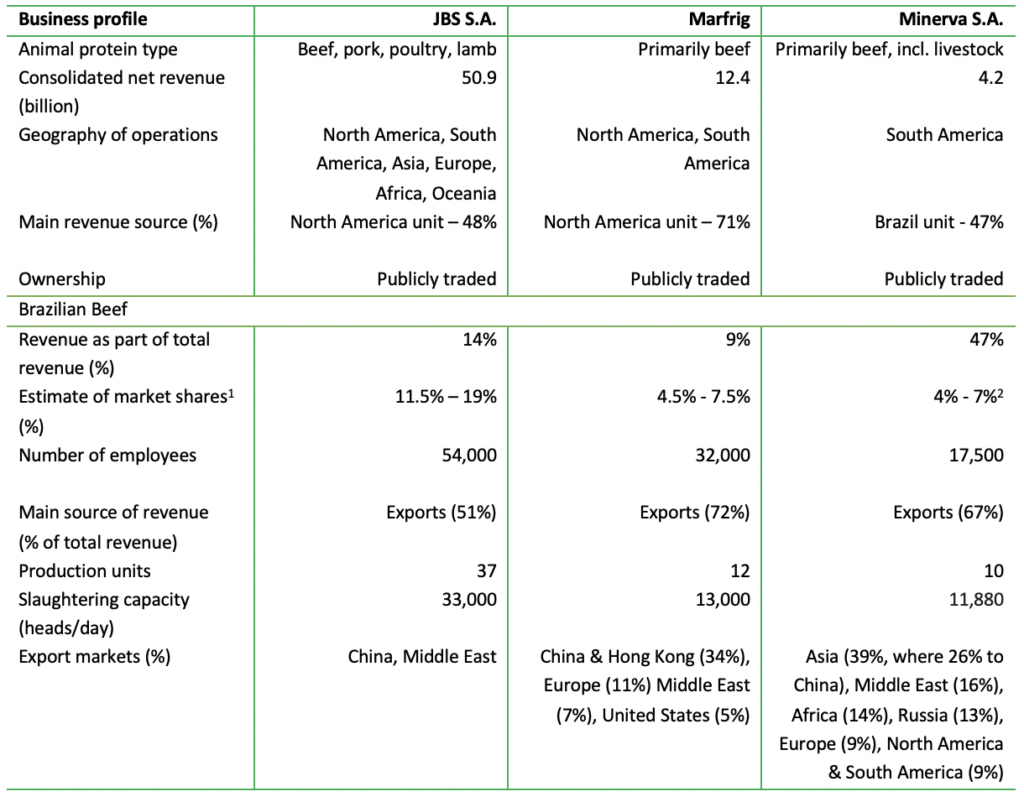

JBS is the largest animal protein company and the second-largest food company in the world, generating revenues of USD 50.9 billion in 2019. JBS produces and processes beef, as well as pork, poultry, and lamb. Its operations span five continents. The company is publicly listed on the Novo Mercado segment of São Paulo Stock Exchange. Members of the Batista family are controlling shareholders through J&F Investments. Apart from Brazil, JBS’s South America presence is mainly in Uruguay, Argentina, and Mexico, where the company’s operations mainly involve leather and poultry production.

In the Brazilian beef sector, JBS has a market share of 11.5 to 19 percent (see Figure 1). JBS Brazil, the Brazilian beef business unit, made up 14 percent of JBS’ global revenues in 2019. In Brazil, JBS operated 37 production units with a daily slaughtering capacity of 33,000 heads per day in 2019. Export markets represented 51 percent of JBS Brazil’s sales. The company has a growing presence in the Chinese market, which accounted for 26.1 percent of JBS’ global exports in 1Q20 and 33.4 percent in 2Q20. In January 2020, JBS signed a Memorandum of Understanding with WH Group, a large Hong Kong-based meatpacker, to supply up to USD 717 million of beef, poultry, and pork products to the Chinese market annually. This partnership followed a November 2018 deal with Alibaba worth USD 1.5 billion.

JBS distributes a range of beef, pork, and poultry products under various brand names, including Friboi, Swift, Bertin, Pilgrim’s, and others. The company also operates related businesses, such as leather, biodiesel, personal care and cleaning, solid waste management, and metal packaging.

Marfrig: The world’s second-largest beef company by production capacity

Marfrig is the world’s second-largest beef company by production capacity, posting USD 12.4 billion in 2019. Marfrig is reducing its poultry, pork, and fish activities, as it seeks to focus on and expand its beef operations. The company operates in North and South America. Its North American unit generated 71 percent of total revenues in 2019. In South America (28 percent of revenues in June 2020), Marfrig is present in Brazil, Uruguay, Argentina, and Chile. Marfrig is listed on the Novo Mercado segment of São Paulo Stock Exchange. Marfrig’s Chairman Marcos Antonio Molina dos Santo is a controlling shareholder of Marfrig through his own portfolio (6 percent) and his financial investment service MMS Participações SA (38 percent).

Marfrig’s market share in the Brazilian beef industry is between 4.5-7.5 percent (see Figure 1). In 2019, Marfrig’s operations in Brazil generated 9 percent of the company’s total revenues. Marfrig operated 12 production units in Brazil and had a daily slaughtering capacity of 13,000 heads per day in 2019. Marfrig in Brazil was heavily reliant on exports, which made up 72 percent of the business unit’s revenues in 2019. Key export markets included mainland China and Hong Kong (33.9 percent of revenues) and the European Union (10.8 percent). Of the three big meatpackers, Marfrig is the company with the highest number of beef processing units authorized to export to China. Throughout South America, Marfrig operates 13 plants that were authorized to export to China (seven of which are in Brazil), accounting for 70 percent of the entire region’s installed capacity.

Marfrig’s core business is protein. Since 2019, the company has shifted its focus to beef, higher value-added and plant-based products, and improving the performance of its North American business unit. By doing so, Marfrig aims to become a “simple, focused company” and is “confident that [it] is focused on the right protein.” Marfrig has also made a clear choice that China is its primary export destination of its South American beef.

Minerva: An export-oriented beef company

Minerva is an export-oriented beef company that accounts for 17 percent of all beef exports from Brazil. It holds between 4 and 7 percent of Brazil’s beef production capacity (see Figure 1). In 2019, the company accounted for 84 percent of beef exports from Colombia, 45 percent from Paraguay, 20 percent from Uruguay, and 14 percent from Argentina. Minerva, a South American leader in beef exports, generated USD 4.2 billion in 2019. The company’s activities are divided into two main business segments: meat and livestock. The meat segment (98 percent of net revenues) is involved in the production and sale of beef, while the livestock unit (2 percent) focuses on live cattle export mainly to Halal meat markets. Minerva is publicly listed on the listed on the Novo Mercado segment of São Paulo Stock Exchange, where its main shareholders include SALIC (UK) Limited (33.83 percent) and VDQ Holding S.A. (17.59 percent), as of November 2020.

Minerva’s Brazilian industry division accounted for 46.7 percent of the company’s total revenues in 2019. It comprises 10 production units with a slaughtering capacity of 10,980 heads per day, while the Athena Division has 13 units with a total capacity of 14,500. The Athena Foods Division — Minerva’s operations outside Brazil — reached 40.1 percent of total revenues in 2019. Exports accounted for 66.8 percent of Minerva’s total revenues in 2019. Key export destinations included Asia (39 percent of revenues, with China alone receiving 26 percent), the Middle East (16 percent), Africa (14 percent), and Russia (13 percent). Indonesia, the largest Halal meat consuming market in the world, is likely to play an increasingly important role in Minerva’s exports as 10 meat processing plants in Brazil were recently approved to export to Indonesia. Minerva operates five of these 10.

Minerva is exposed to deforestation-related financial risks as well as foreign exchange fluctuation risks. Unlike Marfrig, which has 86 percent of net revenues denominated in USD, only 66 percent of Minerva’s revenues are denominated in strong currencies, mainly USD (data provided by the company). CRR estimates that 79 percent of debt was exposed to exchange rate variation as of 4Q19. While Minerva’s customer portfolio is diversified as no single foreign customer accounts for 10 percent or more of the company’s total revenues, the relative importance of Minerva’s Brazilian operations may expose the company to deforestation-linked financial pressure.

Figure 1 – Business Profiles of JBS, Marfrig, and Minerva – FY 2019 (in USD)

Source: Company annual reports, reference documents, sustainability reports, and investor presentations. 1 Market shares are calculated based on production capacity, with the lower value assuming 150 working days per year, and the upper value using 250 days.2 While Minerva’s share based on production capacity is somewhere between 4 and 7 percent, the company reports enjoying a 17 percent market share in exported Brazilian beef.

Sample of suppliers shows deforestation in supply chains of the top three meatpackers, JBS with highest exposure

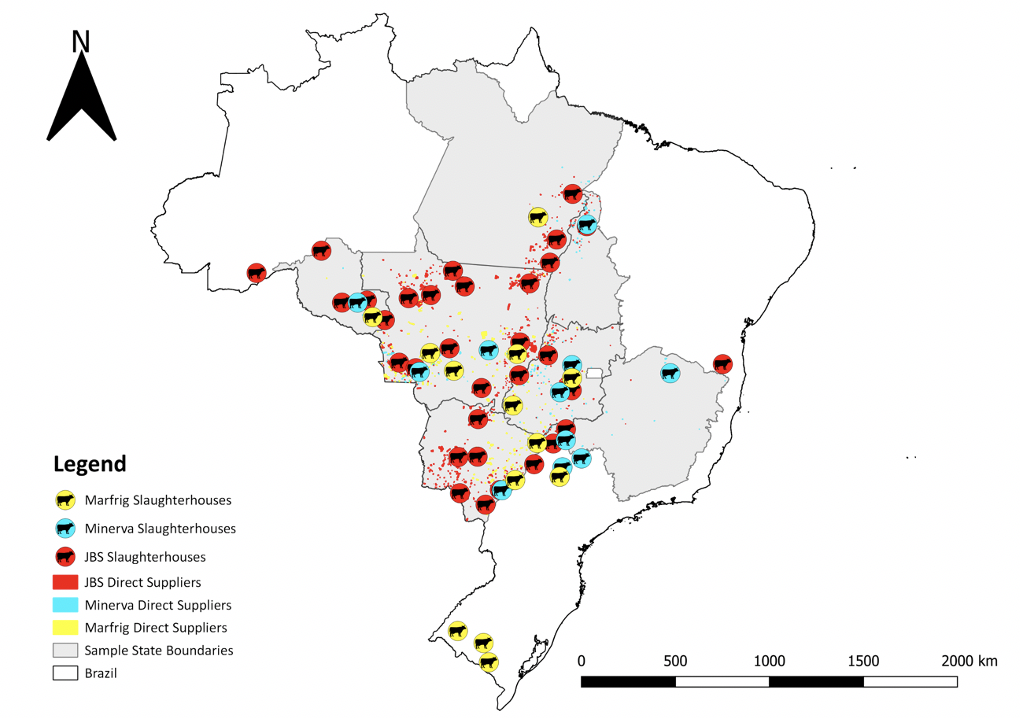

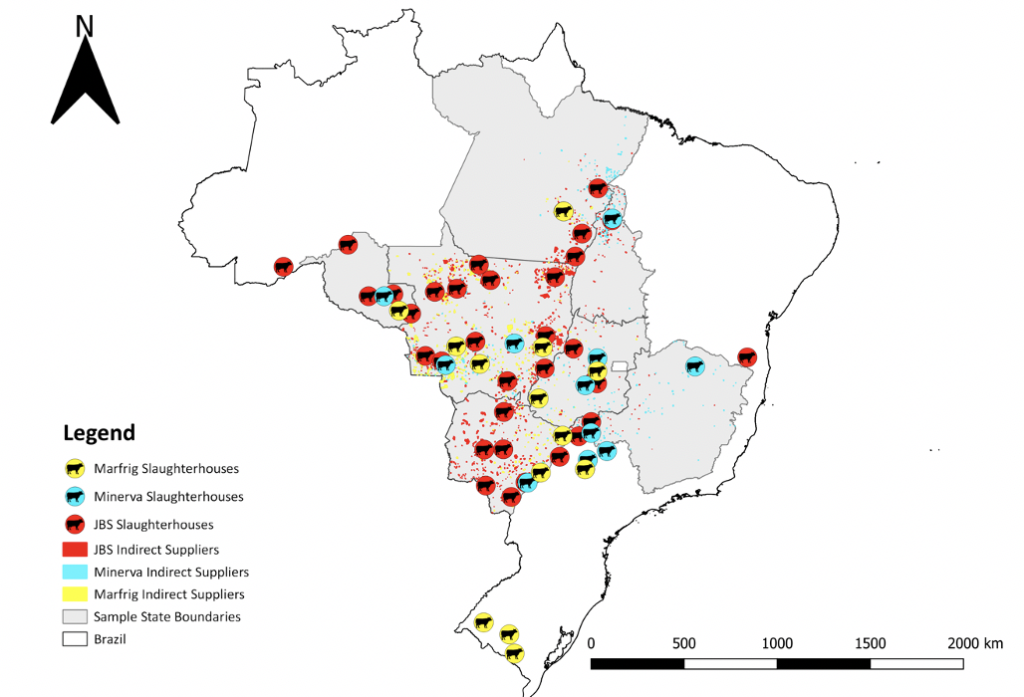

Based on animal transportation and rural cadaster data, CRR has located 1,545 direct suppliers and 3,164 indirect suppliers in the Cerrado and Amazon biomes. This data represents only a small sample of the total of suppliers to JBS, Marfrig and Minerva. For instance, JBS states that it has 50,000 direct suppliers. The suppliers located by CRR operate in the states of Goiás, Minas Gerais, Mato Grosso do Sul, Mato Grosso, Pará, and Tocantins (see Annex for CRR’s methodology). Direct suppliers send one or more batches of cattle directly to a top-three slaughterhouse. From indirect suppliers, cattle batches move through one or more farms before being sold to one of the top-three slaughterhouses.

Figure 2 – Location of 1,545 direct suppliers to the top-three meatpackers

Source: Chain Reaction Research, based on Ministry of Agriculture and animal transportation permits (GTA).

Figure 3 – Location of 3,164 indirect suppliers to the top three meatpackers

Source: Chain Reaction Research, based on Ministry of Agriculture and animal transportation permits (GTA).

Most direct suppliers in the sample trade with only one of the top three meatpackers. Of the 1,545 direct suppliers to Marfrig, Minerva, and JBS in CRR’s sample, 81.1 percent sold to only one of the three meatpackers, while 10.9 percent of the farms supplied two meatpackers (Marfrig and Minerva, Marfrig and JBS, or Minerva and JBS). Only 5.1 percent of the direct suppliers sold livestock to all three meatpackers. The most common overlap is the combination of Minerva and JBS: 5 percent of the farms that traded with two meatpackers sold cattle to both Minerva and JBS.

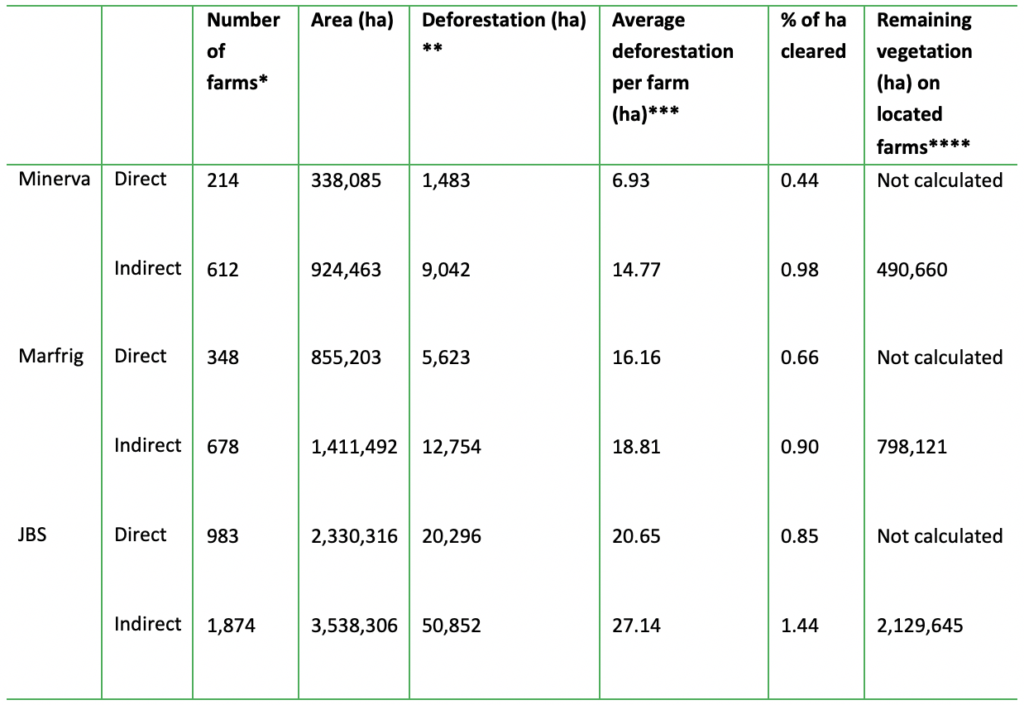

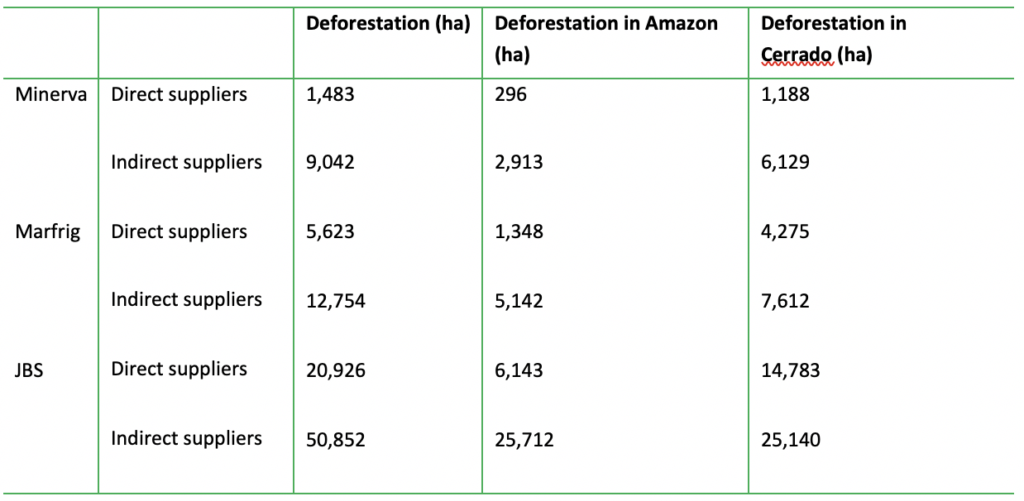

Absolute and relative deforestation figures reveal that the top three’s exposure to deforestation is higher in their indirect supply chains than in their direct supply chains. At the 983 identified properties that are linked directly to JBS, 20,296 hectares (ha) were deforested between 2008 and 2019. For Marfrig and Minerva, the amount of area deforested is much lower (see Figure 4). Notwithstanding the lower number of direct suppliers to Marfrig and Minerva in the sample, there was less deforestation at direct suppliers to these two companies than at JBS suppliers. Land-use change represented 0.85 percent of the cumulative land area of the farms that supplied directly to JBS. For Marfrig, this share was 0.66 percent and for Minerva 0.44 percent. Land clearing in JBS’ indirect supply chain is also more common than in the indirect supply chains of Marfrig and Minerva. At JBS’ indirect suppliers, 1.44 percent of land was cleared between 2008 and 2019, compared to 0.98 percent at Minerva’s indirect suppliers and 0.90 percent at Marfrig’s indirect suppliers.

Figure 4 – Deforestation at suppliers to Minerva, Marfrig and JBS slaughterhouses, 2008-2019

*Properties were identified in 2019 GTA records. Properties were located through matching with rural cadaster data (SIGEF and SNCI) **Deforestation calculated on the basis of annual confirmed PRODES data since 2008 ***Remaining vegetation calculated on the basis of data from INPE and FREL. Source: Chain Reaction Research.

In the CRR sample, suppliers in the Cerrado biome are responsible for more land clearing than Amazon-based suppliers. Approximately 71 percent (14,783 ha) of the detected land clearing in JBS’ direct supply chain occurred in the Cerrado biome, in some cases without the required environmental licenses. The numbers for Minerva and Marfrig are in the same range: 80 percent of the detected land clearing in Minerva’s direct supply chain took place in the Cerrado biome. In Marfrig’s direct supply chain, 76 percent of the total amount of deforestation occurred in the Cerrado (Figure 5).

Figure 5 – Deforestation at suppliers to Minerva, Marfrig and JBS slaughterhouses, 2008-2019, per biome

Source: Chain Reaction Research

Weak commitments, slow implementation undermine efforts to halt deforestation

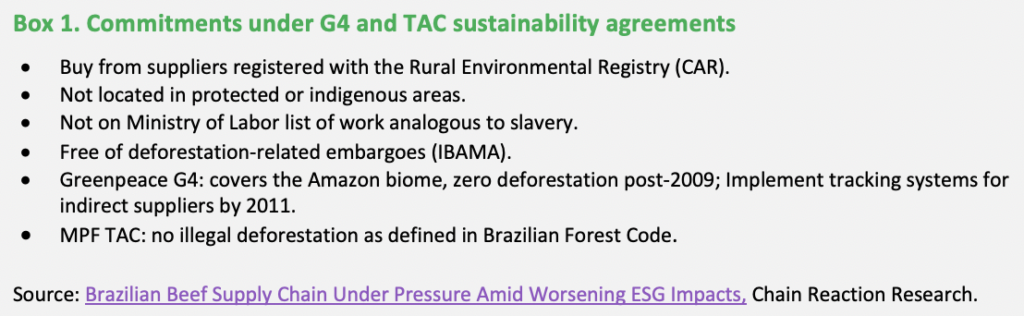

Prompted by NGO reports and campaigns that exposed the cattle industry’s practices in relation to illegal deforestation and forced labor, the top meatpackers signed two agreements in 2009. The four major beef producers (JBS, Marfrig, Minerva, Bertin – acquired by JBS later the same year) signed multilateral Cattle Agreements (G4) initiated by environmental NGO Greenpeace to increase sustainability in the sector. Legally binding Terms of Adjustment of Conduct (TACs) with the Federal Prosecutor’s Office of Pará as a federal counterpart to the G4 (Box 2) followed the initial agreements. The TACs commit the meatpackers to not buy cattle from illegally deforested areas, indigenous lands, conservation units, or areas with links to forced labor. Initially limited to Pará, TACs have since expanded to other Amazonian states, including Acre, Amapá, Amazonas, Mato Grosso, Rondônia, and Tocantins.

JBS and Marfrig announced new commitments to monitor indirect suppliers by 2025 in September and July 2020, respectively. JBS announced that its Green Platform will use blockchain technology and GTAs (cattle movement documents) for monitoring, and the company will block suppliers that do not cooperate and comply. JBS will roll out its platform first in Mato Grosso, the state holding Brazil’s biggest cattle herd. Critics have observed that such a commitment simply gives JBS an additional five years to continue to purchase cattle linked to deforestation and human rights abuses while allowing the company to placate its investors at a time when JBS risks becoming a major global divestment target. Minerva stated: “Differently from its peers, [the company] is not postponing actions to tackle deforestation from its supply chain from direct and indirect suppliers. Minerva Foods is acting now with the best available tool [the VISPEC monitoring tool] to check indirect suppliers.”

Apart from committing to monitoring 100 percent of direct and indirect suppliers in the Amazon by 2025, Marfrig’s new target (Verde+ Plan) extends the zero-deforestation commitment to the Cerrado biome by 2030. The plan, designed in partnership with IDH, envisions the launch of a Risk Mitigation Map for Indirect Suppliers by 2022, as well as the adaptation of Marfrig’s satellite geo-monitoring system to monitor the Cerrado by the end of 2020. The monitoring of indirect suppliers in the Amazon will be implemented through partnering with Amigos da Terra – Amazônia Brasileira for developing a program using VISIPEC’s traceability tool under Marfrig’s operations. Unlike JBS, Marfrig’s plan will focus on reintegrating suppliers (during 2022-25) through the promotion of best practices rather than excluding suppliers with irregularities.

The top three meatpackers have focused on compliance in direct supply chains, but show little progress on indirect supply chain monitoring

TAC audits commissioned by the large meatpackers report high levels of compliance for direct suppliers, but their connections to indirect suppliers remain largely out of sight. TAC signatories have used a combination of tools, including geospatial and socio-environmental monitoring, to verify compliance against registers of ranches embargoed due to illegal deforestation, forced labor, or other problematic conduct. However, these tools are still limited to direct supply chains, leaving out the large group of indirect suppliers.

JBS, Marfrig, and Minerva are not yet monitoring their indirect supply chains. Despite sustainability targets made since 2008 and the recent commitments of JBS and Marfrig, investigations still connect these meatpackers to purchases of “laundered” cattle originating from areas linked to deforestation, breaches of indigenous rights, or forced labor. The G4 meatpackers say that they are confident that their cattle purchases do not come from areas that violate their sustainability agreements. However, they also admit that they cannot determine the origin of many of these cattle.

JBS refuses to answer direct questions about its share of beef sourced from indirect suppliers. The 2019 audit of commitments under the G4 states that “[i]n the case of indirect suppliers, JBS has not yet been successful in implementing traceability processes.” The company highlights the need to access GTAs to be able to identify indirect suppliers. In 2020, JBS has been discussing options for introducing a green GTA (“GTA Verde”) with the Ministry of Agriculture, Livestock and Supply (MAPA). MAPA’s GTA issuing system would automatically cross-check information from the requesting farms with information on areas embargoed by the environmental authority IBAMA for illegal deforestation. JBS would then request that its direct suppliers purchase only from properties that sell animals with “GTA-Verde.”

Meanwhile, the company further reduced its already limited supply chain transparency. In 2019, JBS took down a website that let customers search product codes for the name and coordinates of the last farm to rear the animal before slaughter. Customers are now redirected to another site, which provides only the name and municipality of the ranches but no precise location. The company cited legal concerns based on the Brazilian General Data Protection Regulation. CRR’s recent report on JBS showed that deforestation exposure is significantly higher in its indirect supply chain than in its direct supply chain and large strands of native vegetation are at risk.

Marfrig has used a voluntary self-declaratory mechanism for its suppliers called a Request Form of Information (RFI) since 2013. The company asks the farm delivering the cattle to provide the name of its supplier, including tax number and the name of the farm. In 2019, 30 percent of Marfrig’s cattle supply from the Amazon were covered by the RFI. The company states that it aims for 100 percent of its indirect suppliers to be covered by an RFI by 2025. Like JBS, Marfrig says that it has no systematic verification of indirect suppliers amid “the lack of a nationally implemented public traceability policy [which] makes it difficult to implement such a verification.”

In July 2020, Marfrig announced that it will implement a five-year project to track cattle from critical areas in the Amazon. The company made this statement in parallel with its signing on to a business letter from 38 Brazilian and international companies that offered support to the federal government to find solutions to sustainability issues, including combating illegal deforestation in the Amazon and other biomes. Traceability information published on Marfrig’s website allows customers to identify the name of the last farm and the municipality, but it provides no precise locations.

Like its main competitors, Minerva reports high compliance for its direct supply chain, but does not have a control system capable of monitoring its indirect suppliers. In its latest audit report published in 2020, the auditor concluded that the company has not met standards on indirect suppliers, “given that the monitoring of these indirect suppliers depends on support and investments from the government in technologies that promote the traceability of cattle from birth to slaughter.” Minerva has not made any statements on its share of indirect suppliers in its cattle purchases.

Regarding transparency, Minerva offers an origination calendar for Pará on its website. However, Minerva only offers the name of the municipality and property, and does not provide information on sourcing in other states. According to the company, over 9,000 suppliers in the Amazon region are monitored using geographic information systems, comprising a total area of over 9 million ha. Minerva also states that more than 2,400 producers have been blacklisted for deforesting in the Amazon, encroachment on indigenous lands and environmental protection areas, farming in embargoed areas, and/or using forced/child labor.

In July 2020, new supplier monitoring and protocols for TAC slaughterhouses were implemented. The new protocols, developed by NGO Imaflora and approved by Brazil’s Public Prosecutor’s Office, meatpackers, and retailers, aim to standardize monitoring approaches across the industry. In addition to geospatial analysis to identify illegal deforestation or activities on indigenous lands and the checking against embargoed areas, these protocols added a new standard. It is a “theoretical index” of livestock productivity per hectare per year. Slaughterhouses will apply this index to identify suspected cases of laundering cattle. The property will be classified as suspected and delisted as a supplier if a livestock supplying property has productivity above the maximum quantity established and cannot justify it with the use of more productive production systems such as confinement. However, this protocol only defines rules for direct suppliers. Rules for indirect suppliers will not be defined until the next phase of the project.

Cases of laundering cattle in supply chains uncovered

Investigations by journalists, researchers, and NGOs have regularly uncovered cases of non-compliance in cattle supply chains linked to leading meatpackers. The following examples from 2020 illustrate the scale of the problem:

- In March 2020, Gibbs Land Use and Environment Lab (GLUE) published research on EU exports of beef linked to Amazon deforestation. The research is based on the SISBOV identification systems for bovines, which is obligatory for beef to be eligible for export to Europe after slaughtering in SIF slaughterhouses under regulations to prevent foot-and-mouth disease. The system covers around 1 percent of Brazil’s cattle ranches. The research found that 138 farms that sold cattle to EU-export approved SIFs in 2019 purchased cattle from around 300 indirect suppliers with almost 13,000 ha of deforestation between 2010 and 2017. According to the report, JBS, Marfrig, and Minerva were the only EU-exporting meatpackers that bought from the properties with Amazon deforestation in 2019.

- In June 2020, Greenpeace published a report with evidence that cattle grazing on deforested land within the Ricardo Franco national park in Mato Grosso was sold to JBS, Minerva, and Marfrig. According to the environmental organization, the cattle were laundered through a nearby farm called Barra Mansa, which sold cattle to slaughterhouses in Mato Grosso owned by JBS, Minerva, and Marfrig between 2018-19.

- In June and December 2020, investigations by Repórter Brasil linked JBS and Marfrig to unauthorized deforestation in the Cerrado biome. Both meatpackers received cattle from farms that cleared Cerrado vegetation between 2011 and 2016 without the required environmental licenses. JBS signed a comprehensive agreement in 2011 that covers the so-called Legal Amazon and part of the Cerrado.

- While commercial cattle ranching is illegal in reserves and indigenous territories, encroachment and murder have repeatedly been linked to cattle ranching in the Amazon. In July 2020, Amnesty International documented several instances of cattle from illegal ranching in reserves in the Amazon state of Rondônia that entered JBS’ supply chain. In an investigation of cattle laundering published in June 2020, Repórter Brasil found that cattle being raised on various farms in the indigenous territory of Apyterewa in Pará were sold to various nearby farms outside the territory borders. These farms then sold cattle to slaughterhouses owned by meatpackers Marfrig, Frigol, and Mercúrio. In March 2020, Repórter Brasil alleged that JBS and Marfrig sourced cattle indirectly from land owned by a fugitive named de Souza. He was charged in 2017 with the murders of nine men who were squatting on remote forest land known as the Colniza slaughter.

JBS, Marfrig, and Minerva are exposed to material business risks

Both the growing concern over Amazon deforestation and the global responses to COVID-19 may have long-term impacts on the meatpackers’ business, posing a range of different business risks. These risks may adversely impact the companies’ business models. This section discusses reputation, financing risks, market access, and technology risks facing the three large meatpackers.

Reputation and financing risks: increased investor concerns and shareholder action

International financial institutions are increasingly wary of Brazilian investments, particularly the meatpacking sector. In June 2020, a group of 30 institutional investors from Europe and Asia called on the Brazilian government to curb environmental destruction. In a public letter, these investors signaled their intent to divest from Brazilian assets – corporate as well as sovereign – and highlighted their concern for Brazil’s meatpacking industry and its role in driving deforestation. Investor signatories represented USD 3.7 trillion assets under management.

JBS faces the highest financing risk among the meatpackers. At least one investor, Nordea Asset Management, has announced that it has excluded JBS from all assets it sells. In August 2020, reports said that HSBC “sounded alarms” over its JBS investment due to deforestation inaction. These actions followed a string of shareholder action and engagement toward JBS in recent years:

- In March 2020, 95 current and past shareholders initiated legal arbitration, seeking BRL 1.4 billion (USD 280 million) in compensation for damages caused by JBS illegal practices. The shareholders’ claims are based on false and misleading statements made by JBS and its executive officers since its IPO in 2007.

- The Council of Ethics of the Swedish National Government Pension Funds reported on its engagement with JBS in its 2019 annual report: “The Amazon is once again in focus with an increase in illegal wildfires during the autumn of 2019. The Council on Ethics has strengthened its focus on soy production and cattle farming with the aim to ensure that companies like JBS, Bunge and Archer Daniel Midlands are sourcing their products from legally deforested parts of the Amazon.”

- In July 2018, Norges Bank officially placed JBS on its exclusion list following a recommendation from its Council of Ethics. Norges owned USD 143 million in JBS shares at the time and cited “gross corruption” as the exclusion criterion. JBS remains on this list as of March 2020.

- In April 2018, Dutch asset manager APG voted against the re-election of three of JBS’ directors. APG ranks among the ten largest JBS shareholders.

As financers grow wary of Brazil’s political and economic climate and concerns about deforestation increase, JBS as well as Marfrig and Minerva may see an outflow from current investors and significantly reduced interest from potential investors. Reduced investor appetite could also complicate the sale process of BNDES’ JBS shares. Similarly, Marfrig recently saw major changes to its shareholder base. Before divesting from Marfrig during 1Q2020 as part of a restructuring initiative, BNDES owned 30 percent of the company’s shares. Minerva has also faced considerable investor pressure. In December 2019, two UN-appointed experts told the World Bank to reconsider its investment in Minerva because of the company’s links to deforestation. The Bank admitted that Minerva’s inability to monitor its indirect supply chain prevents the Bank from knowing how many cattle raised on illegally deforested land are present in the company’s supply chain.

Divestments, exclusions, refusals to extend loans, and other actions from financial institutions would affect the meatpackers’ cost structure, and thus their net profits. In particular, the cost of debt may rise if banks refuse to extend loans and the companies are forced to seek new financiers during difficult circumstances. Also, due to low valuation of the shares, the issuance of new shares to fund acquisitions becomes increasingly dilutive.

Market Risk: Restrictions to export markets and supply chain exclusions

COVID-19 has resulted in restrictions in export markets for meatpackers’ products produced in plants with virus outbreaks. In June 2020, China announced that it increased its inspections of imported meat products after a second wave of COVID-19 infections began due to an outbreak at a wholesale market in Beijing. Chinese customs no longer accept import licenses from 15 meat plants. The four suspended plants in Brazil include one JBS poultry plant and one Marfrig beef plant. This move followed an earlier suspension of beef imports from Australia, possibly in retaliation for Australia’s criticism over China’s handling of the COVID-19 outbreak. Of the four Australian meat plants subject to this suspension, two were JBS-owned plants. The more restrictive Chinese approach to imported meat products may affect all three companies’ Brazilian exports to China, which has been a notable growth market for the companies in recent years, constituting 33.9 percent of Marfrig’s Brazilian beef exports and 26 percent of Minerva’s.

Concerns over wildfires and deforestation may also result in further exclusions from corporate supply chains for non-compliance of responsible sourcing policies. In the aftermath of the 2019 fires in the Amazon, global fashion brands H&M and VF Corporation suspended all use of leather originating from Brazil because of the cattle industry’s role in the fires. In May 2020, a group of more than 40 British supermarkets warned the Brazilian government that it may boycott Brazilian products if legislation that allows for increased Amazon deforestation passes. In August 2020, a Greenpeace UK campaign called on retailer Tesco to cut all ties with JBS. With Brazil undergoing another intense fire season, more boycotts, exclusions, and suspensions may occur.

Reputation and Technology Risk: Growing Chinese consumer wariness for imported meat products and substitution threats by plant-based proteins

In addition to restrictions by Chinese customs, trends in Chinese consumer preferences may also negatively impact the meatpackers’ export potential. Both the outbreak of the African swine fever and the outbreak of COVID-19 have raised questions among Chinese consumers about the safety and sustainability of animal proteins. Market research firms project that interest in plant-based protein and lab-grown meat will grow among consumers in China during the next 10 years. As plant-based proteins are not new to Chinese consumers, market acceptance of alternative meat products is likely to grow as consumers become more educated about the nutritional, health, and safety benefits.

The World Economic Forum also notes that demand for plant-based protein is surging in Asia as a result of consumer suspicions over possible links between animal meat and COVID-19. This shift in demand is most notable in Hong Kong and mainland China. The virus outbreak has accelerated an ongoing trend that already caught the attention of the beef industry’s plant-based rivals Beyond Meat and Impossible Foods. Both international and local companies are producing alternative meats used in dumplings, noodles, rice, and fast-food products.

Plant-based proteins are rapidly becoming a viable and economic substitute product for animal proteins amid a rapid decline in production costs. In May 2020, Beyond Meat’s CEO indicated that the company is ready to compete directly with real beef on price terms in supermarkets. The surge in beef prices caused by the COVID-19 triggered supply chain disruptions has narrowed the gap in relative prices. Beyond Burger’s gross margins provide room for the company to lower retail prices in order to capture market share from real meat products. In March 2020, Impossible Foods made a similar move when it cut its vegan product prices by 15 percent. Both Beyond Meat and Impossible Foods have entered the Chinese market. Plant-based meat alternatives may therefore cut into the meatpackers’ Chinese meat market share and its revenues.

Financial Risk Analysis: Leading Meatpackers Do Face Material Impact

For evaluating investment risk, the financial analysis emphasizes the following: 1) the exposure to European financiers as these are adapting to zero-deforestation policies, and 2) the exposure to export markets in China and Europe. The value of investments in JBS, Marfrig, and Minerva can be affected by financing and reputation risk, as well as by market access and technology risk mainly in European and Chinese markets. Meanwhile, financiers with zero-deforestation policies may engage the companies on ending deforestation to reduce investment risk.

A further increase in financing risk dominates an already discounted reputation risk

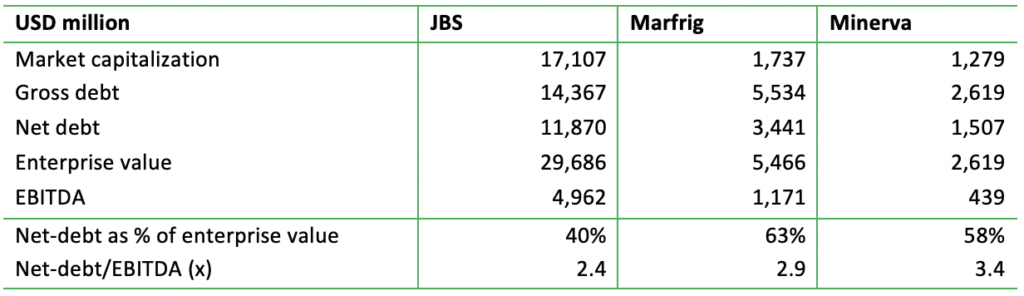

In market value, Marfrig and Minerva are much smaller than JBS (Figure 6), but they are all highly dependent on debt financing. The smaller companies Marfrig and Minerva are relatively dependent on financing by debt as their net-debt/EBITDA is respectively 2.9x and 3.4X and their net-debt as percentage of enterprise value is more than 50 percent.

Figure 6: Key numbers in financing of JBS, Marfrig, and Minerva (2019)

Source: Bloomberg, viewed October 21, 2020

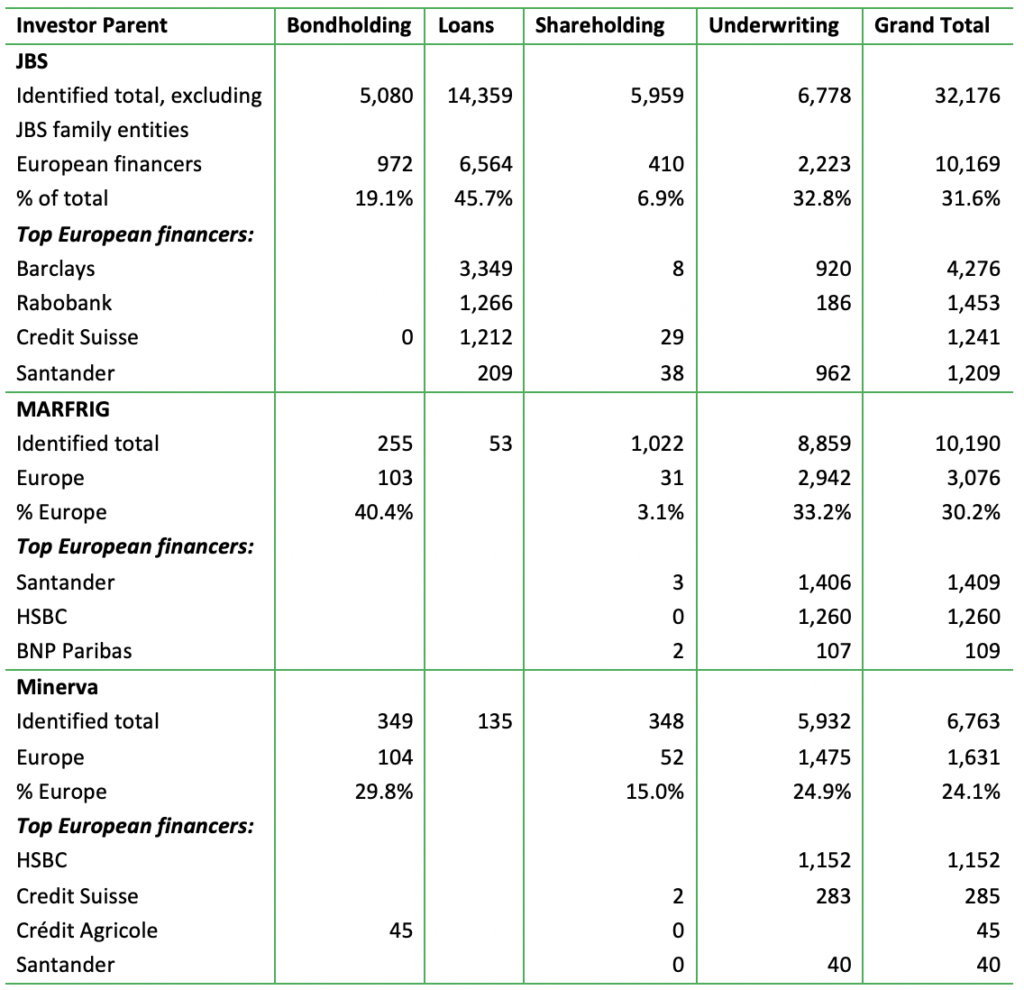

With a high reliance on refinancing debt and underwriting services from European financiers, financing costs for Brazilian meatpackers could increase. The dependence on European financers is 31.6 percent and 30.2 percent (Figure 7, last column) for respectively JBS and Marfrig. This financing consists of identified loans and underwriting (in the last five years) and current shareholding and bond holdings. For Minerva, dependence is 24.1 percent. With respect to Marfrig and Minerva, European financers are active in the underwriting of bonds and share issuances, while they offer JBS a more balanced spread of financing instruments. Most of the top European financiers (Barclays, Rabobank, Santander, and BNP Paribas) have zero-deforestation policies on beef or are very vocal (HSBC) on the issue. However, some (Credit Agricole, Credit Suisse) have policies that still focus on palm oil only. Because of proposed European legislation to reduce deforestation in supply chains, financing costs for the three companies might increase as re-financing of loans and bonds and underwriting services could be affected.

Figure 7: Identified Financing to JBS, Minerva and JBS and exposure to European financiers (USD millions)

Source: Chain Reaction Research, Thomson-Eikon, Bloomberg; data June 3, 2020

Reputation risk for Brazilian meatpackers is smaller than for large fast-moving consumer good companies (FMCGs). Moreover, reputation risk appears to be already discounted in the low valuation for the meatpackers. In relation to deforestation, slaughterhouses and meatpackers are most exposed to market access risk, while stranded asset risk and reputation risk are relatively small. Reputation risk is concentrated in FMCGs. When focusing on the less volatile EV/EBITDA, the valuation of the three Brazilian meatpackers is lower than that of counterparts in South America and North America. This reflects international investors’ reluctance to invest in JBS, Marfrig and Minerva. This reluctance is mainly the consequence of a weak reputation, which has led to a high cost of equity. With share price values close to book value per share, the possibility of further reputation risk for these companies is limited.

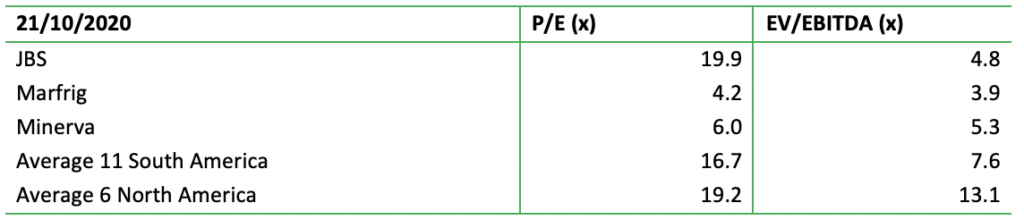

Figure 8: Valuation JBS, Minerva, and Marfrig 2020 (FY1)

Source: Chain Reaction Research, Bloomberg; data October 21, 2020

Dependence on exports to China and Europe emphasizes market access and technology risk

A decline in exports to China and Europe could significantly hurt earnings capacity and put further pressure on debt re-financing. Market access risk (due to COVID-19 and sustainable sourcing policies) and technology risk are mainly related to exports to Europe and China. The 2Q20 results show that Minerva has the highest exposure to exports (76 percent) and an elevated exposure to China (28 percent). For JBS and Marfrig, these numbers are lower. For all three meatpackers, European exports contribute a single-digit percentage to net turnover. A negative impact on Chinese and European exports will likely hurt EBITDA, leading to an increase in the net-debt/EBITDA ratio. An analysis for JBS showed a pro-forma increase from 2.4X to 3.2X, which would be a material event for lenders. This dynamic would worsen the (re)financing risk, and a hit to EBITDA would negatively impact the value of investments.

Figure 9: Net turnover exposure to total exports, to exports to Europe and to China (2Q20)

Source: Chain Reaction Research based on 2Q20 company financial results and/or presentations

The sum of the various risks can be material for meatpackers

Similar to JBS, Marfrig and Minerva may be confronted with negative EBITDA impacts. Physical risk, market access risk, financial risk and technology and innovation risk, as discussed in the report “JBS: Outsized Deforestation in Supply Chain, COVID-19 Pose Fundamental Business Risks” made up 5 to 26 percent of JBS’ EBITDA in various scenarios. The impact of plant closures related to COVID-19 had a material impact in some scenarios. Amid exposure to financing risk and the relative size of the exports to Europe and China, Marfrig and Minerva may also be confronted with material impacts.

Annex: Methodological notes for deforestation analysis

This annex describes the methodology used by CRR to map indirect and direct suppliers to JBS, Marfrig, and Minerva. It describes the following:

- The main sources of data used

- A description of data processing and database development

- A description of data analysis and quality checks

- The limitations to the methodology

1. Data sources

The main sources of data used for this report include:

- Animal transportation permits (GTAs).These permits are mandatory sanitary documents required when transporting cattle between two properties. CRR used 2019 GTA records from the states of Minas Gerais, Goías, Mato Grosso, Mato Grosso do Sul, Pará, Rondônia, and Tocantins to identify the names of the farms that directly and indirectly supply Marfrig and Minerva.

- Rural cadasters and property registries.CRR used the SIGEF (Sistema de Gestão Fundiária) and SNCI cadasters and property registries obtained from Brazil’s National Institute for Colonization and Agricultural Reform (INCRA).

- Annual confirmed deforestation data. CRR used the official annual data from the Brazilian government’s Program to Calculate Deforestation in the Amazon (PRODES) as the basis for the deforestation calculations in both the Amazon and the Cerrado.

- Previous CRR research on JBS. The results of this data analysis were first published in August 2020.

2. Data processing and database construction

The following three steps were taken to construct the database for this report:

- Clean and prepare GTA information. Using R studio, a script was written to clean text within both our GTA dataset and the SIGEF and SNCI land registries to ensure the highest possible success of string matching. Examples of this cleaning include the conversion of Portuguese characters to English (ã to a), standardizing the spacing between words, and standardizing the name of companies (i.e. Marfrig Global Foods, Marfrig, Marfrig S/A).

- Identify direct and indirect suppliers of Marfrig and Minerva. A script was written to search through the GTA dataset and extract all entries that had a Marfrig or Minerva slaughterhouse as the final destination. Filtering was applied for “abate” (slaughter) and “bovinos” (cattle) to limit data to the beef supply chains of Marfrig and Minerva and ensure a slaughterhouse was the end destination. To identify indirect suppliers, CRR repeated this process with Marfrig and Minerva’s direct suppliers as the registered destination of the cattle transport. In order to avoid false positives, CRR only included records whereby the owner name, farm name, and municipality matched. CRR applied the filters of engorda (fattening) or reprodução (reproduction) as the purpose for transportation. Through this method, a total of 10,281 direct supply farms and 38,485 indirect supply farms to Marfrig, and 6,758 direct supply farms and 30,374 indirect supply farms to Minerva were identified. These farms each supplied one or more batches of cattle. An excel sheet with the details of these suppliers was created (“Marfrig and Minerva identified suppliers”).

- Geographically locate suppliers. Using R studio, CRR performed string matching to match the “Marfrig and Minerva identified supplier” dataset to the SIGEF and SNCI cadaster and property registries for the six states within the scope of this analysis. In order to avoid false positives, records were only included if a match was found between datasets on a) the name of the landowner; b) the name of the farm; and c) the municipality of the farm. If two or less of these metric matches, suppliers were excluded from further analysis. Through this method, a total of 348 and 214 direct supply farms and 678 and 612 indirect supply farms were located for Marfrig and Minerva respectively. Four shapefiles with georeferenced data were created in QGIS (“Marfrig located direct supplying farms” and “Marfrig located indirect supplying farms” and “Minerva located direct supplying farms” and “Minerva located indirect supplying farms”).

3. Data analysis and quality checks

The “Marfrig/Minerva located direct supplying farms” and “Marfrig/Minerva located indirect supplying farms” shapefiles were subsequently used as the base map for analysis of deforestation through the following steps:

Overlaying PRODES deforestation data. CRR used confirmed PRODES deforestation alerts from Instituto Nacional de Pesquisas Espaciais (INPE) for the years 2008-2019. CRR chose 2008 as the cut-off year as it is in line with Brazil’s Forest Code. Deforestation data was intersected with the four shapefiles to calculate deforestation at each located property, resulting in a total of 5,623 ha for the 348 Marfrig direct supply farms and 12,754 ha for the 678 Marfrig indirect supply farms. This also resulted in 1,483 ha for the 214 Minerva direct supply farms and 9,042 ha for the 612 Minerva indirect supply farms.

Projections of deforestation footprint in direct and indirect supply chain. To be able to extrapolate the findings in our sample, CRR calculated averages for deforestation per property. For the located direct supply farms, CRR calculated an average of 16.16 ha per property for Marfrig (5,623 ha of deforestation divided by 348 located properties) and 6.93 ha per property for Minerva (1,483 ha of deforestation divided by 214 located properties).

Quality checks. CRR conducted several quality checks during various phases of the data analysis. These include:

- Confirming that the slaughterhouses listed as the destination in the GTA records are still owned by Marfrig and Minerva by matching record with the list of assets included in their corporate reference documents.

- Removing the duplicate records of located properties that have both SIGEF and SNCI registrations in order to avoid double-counting.

- Intersecting deforestation alerts with property boundaries to exclude deforested areas that spill over farm boundaries.

- Conducting, at each stage of the analysis, sample quality checks to ensure proper functioning of the applied scripts.

- Calculating the average deforestation per farm for both properties with and without deforestation in order to balance projected estimates for Marfrig and Minerva’s full deforestation risk exposure and account for the reality that not all supplying farms have deforestation.

4. Methodological limitations

CRR’s data and analytical methods pose a number of limitations that merit caution in interpretation of the presented findings. They include:

Conservative estimates and projections. CRR made several choices that resulted in more cautious estimates and potential underreporting of totals. These include:

- Not attributing deforestation outside farm boundaries. In several cases, deforestation alerts transgress farm boundaries. CRR excluded all deforestation that took place outside of farm boundaries from our calculations, despite the likelihood that they are part of a single deforestation event.

- Making projections based on 2019 GTA records. CRR projects the total deforestation footprint on the number of properties included in our 2019 GTA records. As a result, the projections exclude Marfrig and Minerva suppliers that did not supply the company in 2019, but did so in other years. Projections also exclude any suppliers with faulty, fraudulent, or absent GTA records.

- Excluding poor data on Rondônia. The GTA dataset does not include adequate data for this state. In Rondônia, there has been significant deforestation in recent years, and \Marfrig and Minerva have a presence there.

- Not covering third-tier supply chains and beyond. The analysis is based on identified suppliers in the first and second tiers of Marfrig and Minerva’s supply chains. It excludes any farms that may be further removed from the slaughterhouse. Cattle typically move from property to property multiple times during their lifetime and any deforestation risks in these tiers are also fully unmitigated.

No distinction between legal and illegal deforestation. This analysis does not make a distinction between legal and illegal deforestation and does not make any claims of illegal practices by Marfrig, Minerva, or any of their suppliers, other than referring to third-party reports. In particular, in the Cerrado biome, the majority of deforestation falls within the scope of Brazil’s Forest Code.