Many fast-moving consumer goods (FMCG) companies have publicly committed to a 2020 deadline to end deforestation in their supply chains. However, it is becoming increasingly clear that most FMCGs will not meet this deadline. NGO campaigns against individual FMCGs and benchmark studies that show the differences in implementation of zero-deforestation commitments indicate increasing reputation risks for the sector. For an FMCG company, business risks related to tropical deforestation, such as market access risk, stranded asset risk, and the risk of higher costs of capital, contribute to only a small deviation in the total share value. However, reputation risk may become a much stronger value driver for them. This study explores the scientific knowledge on valuing this reputation risk.

Download the PDF here: Deforestation-Driven Reputation Risk Could Become Material for FMCGs

Please see here for the recording of our webinar on this report.

Key Findings:

- Not meeting the 2020 deadline of zero-deforestation commitments could lead to financial risks for investors in FMCGs. This development is likely already happening, and it might accelerate after the 2020 deadline. FMCGs meeting their zero-deforestation targets could outperform in share price versus peers that lag behind.

- Reputation events can impact a company’s value by 30 percent. This value impact has increased in the last 20 years through the effect of social media. Scientific studies show that events harming a company’s reputation have a material negative impact on the value of a company. However, acknowledgment of the situation and taking measures in proper supply chain management can reverse the negative reputation impact.

- CRR case studies confirm the scientific research on the value impact of reputation risk. Nestlé (deforestation, 2010), BP (environmental disaster, 2010), RSPO (breach of certification, 2015), JBS (deforestation/corruption, 2016/17), and Facebook (privacy breaches, 2018) all dealt with reputation events which showed negative impacts on the companies’ market value, some of which reached 30 percent.

- In the long term, a positive reputation improves earnings. This positive impact can stem from better client and supply chain relationships, quality personnel, and ultimately enhanced earnings capacity. Companies with stronger reputations tend to see lower costs of capital.

- With societal awareness of deforestation’s climate impact rising quickly, value gaps of up to 70 percent might develop between FMCGs based on their reputations. Companies are increasingly adopting commitments related to the key deforestation drivers: palm, soy, and cattle. With improving transparency, differences in climate and deforestation policies and governance among FMCGs are more visible. The leaders could outperform laggards substantially – highlighting the investment hazard related to reputation risk from links to deforestation.

FMCGs may face reputation risk as 2020 deadline approaches

This report explores the value impact of reputation risks that FMCGs may experience if they are not able to meet to 2020 zero-deforestation deadlines. Various statements, including the zero-net deforestation resolution by the Consumer Good Forum, and the New York Declaration on Forests (NYDF) support 2020 targets. The NYDF is a partnership of governments, multinational companies, investors, civil society, and indigenous people which seek to halve deforestation by 2020 and eliminate it by 2030.

With the 2020 deadline approaching, NGOs have campaigned against various FMCGs, such as Nestlé, Mondelez, Restaurant Brands International (Burger King) and PepsiCo. Moreover, many benchmark studies have been conducted about the different approaches FMCG companies are taking to execute their zero-deforestation commitments. The 2020 deadline may lead to a growing awareness among stakeholders. As a result, more NGO campaigns, action by ESG investors, and regulation could take place. These developments could affect the reputation of an FMCG company. Reputation risk for corporations is gaining attention as a consequence of market globalization, increasing transparency of supply chains, and tighter regulation.

The valuation of the financial impact of deforestation risks is relatively straightforward for upstream companies (growers/plantations) and midstream actors (traders and refineries). Due to high visibility of supply chains and financing, the following concepts determine financial impacts of deforestation risks:

- Revenue loss and market access (revenue-at-risk);

- Loss of asset value (stranded asset risk);

- Impact on cost of capital due to non-ESG behavior (cost-of-capital risk).

Although downstream/FMCG companies face similar risks when their suppliers deforest land or contend with other sustainability problems, the financial impacts of stranded asset risk, market access risk, and cost-of-capital risk tend to be relatively small for this sector:

- Market access: FMCGs often have various product groups with different ingredients. If consumers stop purchasing products containing non-NDPE (No Deforestation, No Peat, No Exploitation) palm oil, this development would affect only a small part of a FMCG’s portfolio. Moreover, FMCGs can change vendors if a certain supplier is exposed as “unsustainable.” In current market conditions, ample palm oil suppliers meeting NDPE-criteria are available. By improving due diligence when choosing suppliers, an FMCG can ensure continued market access.

- Stranded assets: FMCGs do not have stranded assets like upstream and midstream companies. In the upstream segment, plantations/farms might have assets located on peat land or in forested areas, whose value might be material as percentage of equity. For midstream companies like Bunge, Cargill and ADM, CRR concluded that the value impact of stranded assets in the deforestation-relevant states of the Cerrado amounted to less than 1 percent of the companies’ market cap. Downstream companies’ assets will face a lower impact as they will not become stranded through stricter NDPE policies. Their investments in infrastructure are even less dependent on deforestation-linked supply.

- Cost-of-capital risk: FMCGs are often not as highly leveraged as upstream companies, which are more capital intensive and have relatively high net debt/EBITDA ratios. Consequently, the loss of essential debt financers is less felt in the FMCG industry.

Reputation risk is a broader risk concept. FMCGs may face relatively large reputation risks if their sourcing of raw materials from suppliers causing deforestation and other sustainability problems are exposed. These revelations could immediately affect the buying decisions of large numbers of consumers who purchase the FMCG’s products in supermarket stores, in (fast-food) restaurants, and on-line. They could also affect employees’ desire to work in such a company, financing by banks, bondholders and shareholders, regulations, and ultimately brand value. Negative trends in these areas could all result in lower profits and lower valuation multiples for FMCGs which are publicly listed.

Reputation risk: Challenges in definition, methodologies and overlap with other risks

Luca Professione (2014, Politecnico Milano) states that a detailed widely-accepted definition of reputation is still absent. This gap hinders the development of methodologies to measure the magnitude of a company’s reputation. Qualitative methodologies, however, are available, assigning a numeric score to the reputation of an organization based on stakeholder surveys.

Quantitative methodologies have a straightforward methodology, mostly focusing on the differences between a company’s market value (market capitalization) and its book value. As a further refinement, the brand value (the earnings capacity of a brand) could be added to the book value, as is done in the research of Pentland/AON. The common weakness of these approaches is that brand values are published only once per year. Concerning the reported intangible assets, these include the goodwill (brand value + value of client lists) that is paid for acquired brands/companies. Because of the limited data availability on book values and brand values, focusing on changes in market value is the best starting point.

When considering various definitions of reputation risk, they can overlap with other risks. Reputation risk can be defined as a risk to a company resulting from changes in perceptions by key stakeholders, including customers, investors, and regulators. Shifting stakeholder perceptions are typically triggered by “reputation events” related to ethics, safety, security, sustainability, contamination, quality, governance, and innovation.

Reputation risk can lead to a loss in revenue, increased operating, capital or regulatory costs, and reduced shareholder value. The loss of brand value and the reduction in loyalty by personnel are also possible additional impacts. This study focuses on these intangible elements that could affect shareholders’ value, next to the more tangible effects from revenue-at-risk and stranded asset risk. The study recognizes the problem of overlap.

Scientific studies: Value impact of a reputation event can be material

In 2005, Jonathan M. Karpoff et al. examined data collected between 1980 and 2000 that involved 478 cases which included publicly traded companies linked to environmental violations. The study concluded that news of an environmental violation corresponds to a loss in market capitalization. More specifically, in the case of an alleged environmental violation, the average stock return was -1.69 percent. When charges were filed against the firm, this percentage was -1.58. This finding means that an FMCG with a USD 100 billion market cap might lose USD 1.69 billion of its market cap, as its reputation is negatively impacted. If the company is involved in more violations, the impact would multiply.

Researchers have also studied reputation loss due to unexpected restatements of a company’s profits or annual accounts. In a 2004 event study, Palmrose et al. analyzed the determinants of the stock market reaction to restatement announcements. A negative stock price reaction of circa 9 percent occurred over a two-day window. The Palmrose research focuses on only the two-day window and does not elaborate on longer-term effects of these restatements.

A study by Pentland Analytics and AON, published in 2018, focused on reputation risk in the “Cyber Age.” The research looked at the development of the reputation premium, which is defined as the difference between the market capitalization and the net asset value (including intangibles like goodwill).

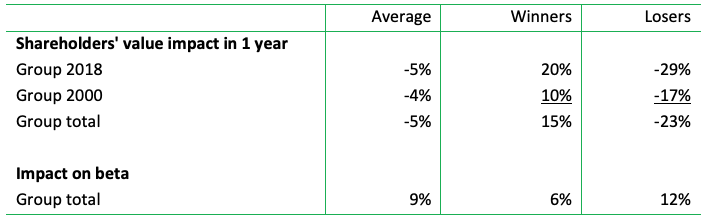

The study includes 125 events that occurred in the last decade (2008-2018) and the impact on the share price during one entire year. These events include, for example, mass fatality events, poor governance and business practices, product and service failures, cyberattacks, accounting irregularities, and marketing and communication blunders. On average, 5 percent of shareholder value is lost over the post-event year, with a major portion already lost in the first five trading days after the event. A company’s equity beta (measure of volatility) is 9 percent higher than in its previous year, directly impacting the company’s cost of capital. A DCF model shows that a 9 percent increase in the beta will impact the cost of capital by three percentage points. This may impact the enterprise value by a negative 3 percent.

This five percent loss on shareholders’ value, however, masks the large difference between “winners” and “losers.” Approximately half of the companies dealing with a reputation event initially face a value dip, but afterwards their value growth continues. The other half of the group sees an acceleration of the decline in value. The study states that the main difference between “winners” and “losers” should be found in the following elements:

- Crisis communications must be instant and global to spur a recovery in value;

- Active social responsibility is a critical element of a value-creating response;

- Neither firm size nor reputation premium offers any protection against value loss.

The gap between winners and losers is large and increases further over time within one year. After one year, winners have gained 20 percent in value, while the losers have lost nearly 30 percent in value.

Researchers compare the data from the 2018 study with data from a previous study they did in 2000. The shareholders’ value impact of 2018 is much stronger, for the winners as well as for the losers (see figure 1). The larger gap in 2018 could stem from today’s larger connectivity due to social media.

Figure 1: Reputation Risk Value Impact 2000 versus 2018

Source: AON, 2018

Another finding is that the beta increased in the period 2000 – 2018 for both the winners (+6 percent) as well as for the losers (+12 percent). The increase for the losers is much stronger. Over the longer term, this leads to a much stronger value impact on the market cap. Chain Reaction Research (CRR) calculated that a 12 percent impact on the beta has a -4 percent impact on the Enterprise Value calculation. The winners, which were also hurt by a reputation event, face an increase of 6 percent on the beta and therefore a -2 percent impact on their enterprise value.

There is no definitive explanation given why the winners are able to gain from reputation events more in the 2018 group than in the 2000 group. One possible factor could be that the winners have improved marketing strategies in place to deal with events, possibly even using social media to their advantage to show how they have positively reacted to damaging events.

An in-depth study by Professione (2015) analyzed the reputation status of the supply chain of food and beverage companies. The study includes a quantitative model which relies on stakeholder analysis and their reactions to a potential reputation-related event. In that model, a company faces the probability of several risks that can result in reputation damage. Professione derived these risks from a historical pool of data on 62 events in the last 15 years. Risks set off a chain reaction: a certain risk leads to an event that subsequently leads to a stakeholder reaction. Surveys, interviews, and historical analysis of similar past events help identify these reactions.

Professione applies the model to a hypothetical dairy company that faces a bacterial contamination risk. The reactions of customers and investors, the stakeholder group, were based on generated surveys. Eight events, with the “forced product recall” the most probable, were the inputs for the simulation. The study estimated that there was a value-at-risk of 28 percent of the enterprise value.

Good reputation management leads to improved financial results

Good reputation leads to better profits and financial strength. In 2005, Carmeli and Tishler looked at the perceived organizational reputations of 86 Israeli industrial companies and their relationships with the companies’ financial performance. The proxy for reputation was customer satisfaction. The methodology used path analysis to show that a positive relationship occurred between the reputation of a company and its financial strength. More specifically, researchers found a positive effect of organizational reputation to a firm’s growth (beta=0.405) and to the accumulation of customers’ orders (beta=0.278). Subsequently, the researchers found that a firm’s growth has a positive effect on market share (beta=0.353) and profitability (beta=0.318), while accumulation of customers’ orders has a positive effect on market share (beta=0.334). Finally, a larger market share has a positive effect on profitability (beta=0.278) and profitability has a positive effect on financial strength (beta=0.278).

Firms with a better reputation demonstrate greater profit persistence, according to Roberts and Dowling. Companies possessing relatively better reputations have a higher probability of sustaining superior financial performance.

Presence in the media, as a marketing tool, helps reputation, as shown in 2000 by Deephouse. A study of 121 US commercial banks showed a correlation between a positive effect of “media favorableness” and the banks’ return on assets (ROA). The authors created the variable of media favorableness by taking into account all articles relevant to the bank in question, both positive and negative, as well as the total number of articles. Subsequently, a regression estimates the effect of media favorableness to ROA. The coefficient was positive (beta= 0.22; 22 percent better than average) and significant (p-value< 0.05).

Companies in all markets around the world are aware of reputation risk. A 2014 survey by Deloitte in more than 300 companies from the Americas (34 percent), Europe/Middle-East/Africa (EMEA) (33 percent), and Asia-Pacific (33 percent) showed that reputation risk is very high on their agendas and that reputation damage would mostly affect revenues and brand value. With more than 25 percent of the market value of a company attributable to reputation, acknowledging importance of reputation is a logical outcome.

Finally, evidence shows that companies with good reputations can improve their borrowing opportunities. De Wilde (2012) concludes that “leveraged buyouts by reputable private equity groups are more leveraged, rely less on traditional bank debt and don’t get more favorable lending terms just because they acquire better companies.”

CRR case studies indicate that reputation events can have material value impact

In order to add to the literature study above, this section adds five case studies on reputation events that have had various value impacts on the companies involved. The first study, on Nestlé, provides an example on how the market value of FMCGs, up to now, has hardly been hurt by deforestation events.

The lack of impact from deforestation, however, may change, based on conclusions from case studies from other sectors. These show how, through a combination of increasing awareness by media, NGOs and customers’ policies, the impact on the share price could be significant. In fact, some negative effects on share prices might have already occurred ahead of key deadlines, such as the 2020 zero-deforestation commitments. They are also likely to continue for many years after the deadline. The combination of these case studies, along with the increasing availability of benchmarking reports from SPOTT, Forest500, CDP and WWF, reflects the financials risks from FMCGs not meeting their 2020 deforestation commitments.

More information on the statistical methodology applied can be found in the Appendix of this study.

Nestlé – 2010 KitKat campaign by Greenpeace – reputation event turned positive

On March 17, 2010, Greenpeace (GP) launched a campaign against Nestlé’s KitKat brand by showing a video in which an orangutan’s finger was inside a KitKat package. The NGO aimed to raise awareness about Nestlé’s sourcing of palm oil from deforested Indonesian rainforests.

Looking at the days immediately following the launching of the campaign, there was no impact. However, on April 15, 2010, GP disrupted Nestlé’s annual general meeting in Lausanne with protests. For April 15-16, Cumulative Abnormal Returns (CAR) was -0.04, meaning that the event negatively influenced Nestlé’s stock by 4 percent. A few days later, on Monday April 19, Nestlé announced the NGO Forest Trust would audit its supply chain and committed to 50 percent sustainable palm oil by the end of 2011. For the following three days, Nestlé experienced abnormal positive returns. CAR was calculated at 0.03, meaning that Nestlé benefitted from that announcement with a 3 percent positive impact. CRR drew the following conclusions from the Nestlé – GP case study:

- The initial reputation damaging event had a follow-up by GP resulting in greater impact. This development could be due to the fact that social media reach was low in early 2010 compared to today.

- Nestlé’s acknowledgment of the situation and taking measurements to clean its supply chain likely brought about a positive reputation event with a significant impact.

This case study from Nestlé are complemented by others on Mondelēz, PepsiCo and Restaurant Brands International. These companies have also dealt with deforestation issues in their supply chains. Most likely, a combination of the size of their overall operations globally, the relatively small share of the problematic agricultural commodity in the company’s total sourcing, and the still relatively low level of awareness by crucial stakeholders (investors, banks, customers) has resulted in only limited impacts on the companies’ values.

BP – 2010 Deepwater Horizon explosion: A large impact, but only after one year

On April 20, 2010, an explosion on the BP operated Deepwater Horizon oil drilling platform in the Gulf of Mexico took place. The explosion killed 11 workers and injured 17 others. It is considered to be one of the most damaging environmental marine events in history.

Following this event there, the CAR was -0.01, meaning that the event negatively affected BP’s stock by 1 percent three trading days after April 20. Chain Reaction Research (CRR) used Europe’s 600 Oil & Gas Index and 2,525 data points to estimate the alpha and the beta coefficients of equation (see 3 in the appendix for more details).

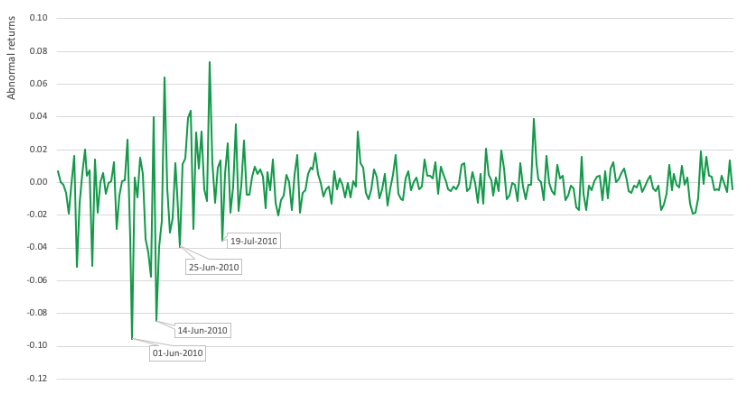

The CAR model limits the scope of impact to a few days after the initial announcement of the reputation damaging event (April 20, 2010). However, the magnitude of the event and its consequences grew over time. In terms of reputation loss, BP experienced abnormal returns for many months after the event. Figure 2 below shows the progression of abnormal returns for a year after explosion took place. Until mid-June, the impact was significant. On June 1, 2010 and June 14, 2010 abnormal returns were -0.10 and -0.08 units, respectively, meaning BP’s stock was negatively affected by 10 and 8 percent respectively during those time periods. On June 1, oil began washing up on beaches, making the damage even more visible to the public. The negative effect continued after that, but less dominant the following months. For the entire year (April 20, 2010 – April 20, 2011), the average abnormal return was -0.29 (= minus 29 percent relative stock price), including expectations of high fines and payments, which came on top of reputation loss.

Figure 2: Abnormal returns of BP, April 20, 2010 – April 20, 2011

Source: Chain Reaction Research

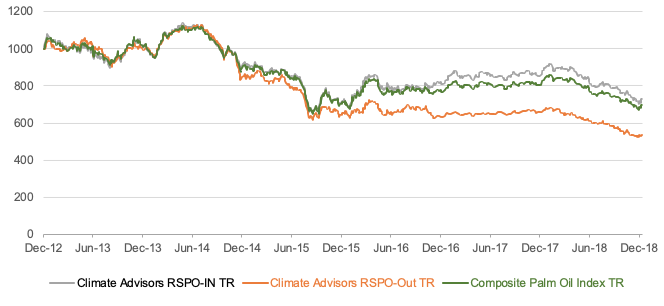

RSPO – 2015: A string of countries moved to adopting RSPO for imported palm oil – a material impact

The Roundtable on Sustainable Palm Oil (RSPO) saw an eventful year in 2015, as Europe reached major milestones. In 2015, the RSPO help facilitate industry commitments toward 100 percent RSPO-certified palm oil uptake in countries such as Belgium, France, Germany, the Netherlands, Norway, Sweden, Denmark, the UK, and Italy.

The green line (see Figure 3 below) constitutes the share price development of companies in the palm oil industry. The companies that are included derive more than 20 percent of their revenues from palm oil, and the index is rebalanced quarterly. The gap after 2015 has been material: The companies complying with RSPO guidelines have performed circa 40 percent better than the companies that did not join the RSPO.

The weaker outcomes for the RSPO-Out group may be a result from market access risk, stranded assets, and higher cost of capital. In an upcoming study from CRR, these factors will receive more attention. However, the share price differences could partly stem from reputation loss for the companies that did not join the RSPO (or the NDPE market) and/or reputation gain for those that did. Finally, the better performance for RSPO members has gradually increased, showing that reputation effects factor over the long run.

These trends indicate that 2015 was only the start of deviating share price performances and that the total impact of risks related to market access, stranded assets, cost of capital, and reputation take years to materialize. In line with this, the reputation impact of not meeting the 2020 zero-deforestation commitments might have already had an impact on companies’ values and could increase beyond 2020.

Figure 3: Climate Advisers Palm Oil Index Performance

Source: Climate Advisers

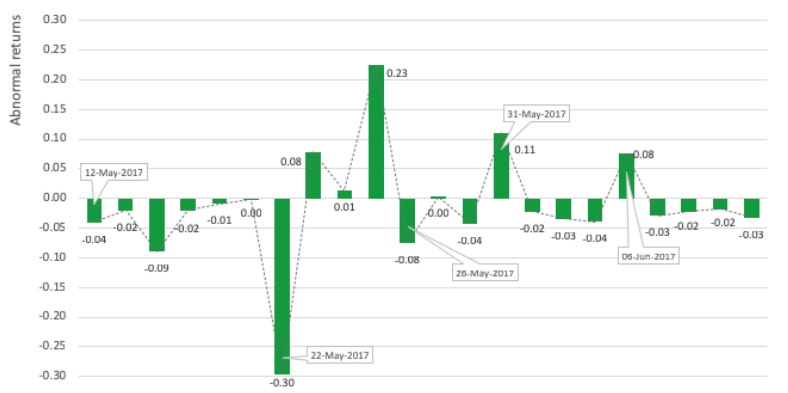

JBS – A material reputation impact from a series of events in 2016-2017

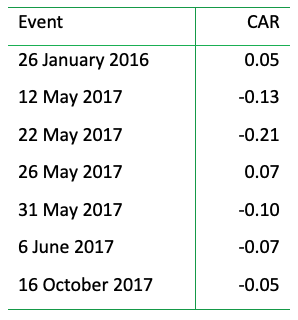

A report published by CRR in 2017 looked at JBS, the world’s largest meat company and the biggest beef exporter from Brazil, and the following events that took place between 2016 and 2017. The incidents had their own financial impact, and in total they negatively affected the company’s reputation:

- January 16, 2016: JBS shares fell after executives were charged with financial crimes involving a series of loans made to related companies.

- May 12, 2017: The Brazilian Federal Audit Court (TCU) accused the company for fraud over loans by the Brazilian Development Bank (BNDES).

- May 22, 2017: Moody’s downgraded JBS.

- May 26, 2017: JBS chairman of the board resigned.

- May 31, 2017: JBS agreed to leniency settlement.

- June 6, 2017: Divestment by JBS of beef operations in Argentina, Paraguay, Uruguay to Minerva.

- October 16, 2017: JBS files for withdrawal of IPO of its subsidiary JBS Foods International.

See Figure 4 below for the CAR for above-mentioned events. CRR chose the São Paulo SE Bovespa Index market proxy and used 2,457 data points of historical price data to estimate the alpha and the beta coefficients of equation (3). More details can be found in the appendix.

Figure 4: Cumulative Abnormal Returns per event studied

Source: Chain Reaction Research

CRR found impact for five out of seven of the events. The two most negative impacts occurred on May 12 and May 22, 2017. When the TCU accused JBS of fraud for the loans it obtained by BNDES, CAR was -0.13, meaning that JBS’ stock was negatively affected by 13 percent. Moody’s downgraded JBS on May 22 due to seven of its executives entering plea bargain agreements for corruption. For this event, CAR was -0.21, which translated into JBS’ stock falling by 21 percent.

While the CAR after each event is a method to measure the impact of each event separately, the case of JBS consisted of a sequence of events that significantly affected the company’s reputation in the long run. Figure 5 below shows the abnormal returns JBS experienced for two months after May 12, 2017.

Figure 5: Abnormal returns of JBS, May 12, 2017 – June 12, 2017

Source: Chain Reaction Research

For those two months, the average abnormal returns for JBS was -0.01. The company even continued to experience abnormal returns for a year after May 12, 2017. The average abnormal return between May 12, 2017 and May 12, 2018 was -0.002. These negative returns show that an unfolding reputation damaging event can have an impact on a company’s performance in the long run.

Facebook – 2018 Cambridge Analytica scandal: A material impact

On March 17, 2018, research conducted by The New York Times and The Observer revealed that Cambridge Analytica, a voter-profiling company, mined the personal data of millions of Facebook users without their consent.

The CAR for the next three trading days after the event was -0.08 units, meaning that Facebook’s stock fell by 8 percent. The FANG (Facebook, Amazon, Netflix, Google) index and 732 data points of historical price data were used to estimate the alpha and the beta coefficients of equation (see appendix).

Figure 6 below shows the abnormal returns Facebook experienced two months after the event. The company saw continuous negative abnormal returns until March 26, 2018. Overall, for the two months after the event, Facebook saw on average -0.002 abnormal returns.

Figure 6: Abnormal returns of Facebook, March 17, 2018 – May 17, 2018

Source: Chain Reaction Research

Based on the scientific literature and five case studies, here are the sub-conclusions:

- Reputation events have an impact on shareholders’ value in a one-year time frame.

- This impact has become more material from 2000 to 2018, with the rise of social media as a possible factor.

- For reputation events in the food and beverage industry, sourcing and the supply chain are both identified in various categories of reputation risk. With more transparency and control of the supply chain, an FMCG company could reduce its reputation risk substantially.

- A positive reputation does not only have an impact on shareholders’ value, but also on structural profitability.

- CRR’s case studies also appear to show that through time, the impact increases. This trend was reflected in BP’s 2010 reputation event and Facebook’s 2018 reputation issue, and both appear comparable when looking to the relevance for both companies’ core businesses.

- In the RSPO case study, which is linked to the issue of deforestation, the share prices of companies that joined the RSPO show a material outperformance.

Reputation events can materially affect FMCGs sourcing beef, soy, and palm oil from deforested areas

FMCG companies are confronted with increasing reputation risk because public attention for their social and environmental performance is growing. In response, FMCGs are making more commitments to zero-deforestation by 2020, but the implementation is still weak. With the increased focus on Environmental, Social and Governance (ESG) criteria by investors, the distinction between FMCGs on zero-deforestation policies and implementation might lead to major variations in share price performances.

Up to now, the debate on climate change has mostly centered around the impact of the fossil fuel industry. Now, however, the focus on deforestation as a source of climate change is gradually growing on the agendas of investors, bankers, the FMCG industry, and other stakeholders.

With zero-deforestation statements increasingly signed by companies and financers and pressure to meet Paris Agreement commitment, stakeholders are facing increasing pressure to act. In CDP’s Global Supply Chain Report 2019, it concluded that major purchasers are now deselecting suppliers based on environmental performance. The CDP report states: “For decades major corporations have outsourced their environmental impact to other companies — and often countries — in their value chain. But with supply chain emissions 5.5 times more than a company’s direct operations, these large corporations are a powerful lever in the transition to a sustainable economy.”

A strong increase in public attention for climate change

The increase in social media use, coupled with more campaigning by NGOs, may make it more difficult for companies to ignore issues such as climate change and deforestation. The 2017 Eco Pulse study — an annual survey which takes the “temperature” of consumer spending and behavior — showed that the percentage of consumers who said they stopped buying a product based on the environmental reputation of a company increased sharply in the 12-month survey period – from 11 percent to 33 percent.

On deforestation and its impact on climate change specifically, limited research has been executed on increasing awareness by consumers. The fact that companies become increasingly active in reporting on policies related to climate change and deforestation, could be taken as a proxy (see next section).

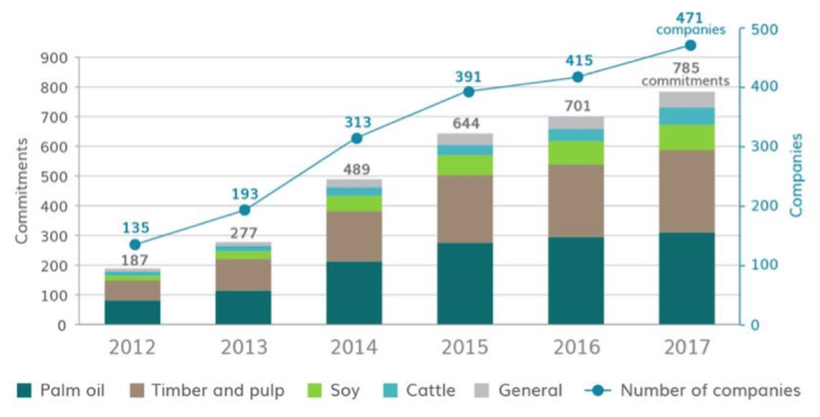

Zero-deforestation commitments have increased, but implementation is weak

When looking to the number and the category of signatories of statements that advocate zero-deforestation, it is evident that pressure is increasing. Climate Focus shows that the number of corporate commitments reached 785 in 2017. In the 2012-2017 period, the commitments that companies made on zero-deforestation had increased substantially (Figure 7). Most commitments are on palm and timber. The data confirms that companies hardly made any new commitments in the soy and cattle sectors in 2017, and only a small number of new commitments in the palm sector. The lack of commitments is happening while cattle is by far the largest source of deforestation in the agricultural commodity chains. This trend of shrinking growth in commitments may be the result of the fact that most companies which actively focus on sustainability have already announced targets.

Figure 7: Commitments on zero-deforestation, 2012-2017

Source: Compiled by Climate Focus based on 2017 data presented on Supply-Change.org

CDP’s Global Supply Chain Report 2019 shows that only 57 percent of suppliers are reporting emission reduction activities. Moreover, only 35 percent have structured carbon reduction targets, and just three percent have targets in line with what scientist say is necessary. The number of companies disclosing forest-risk commodity information to their customers more than tripled in 2018, but overall only 47 percent of suppliers reported producing a forests-related risk assessment and only 17 percent have set deforestation-related targets. This 17 percent contrasts with the 35 percent of companies that have structured carbon reduction targets which are linked to fossil fuel companies.

Forest 500’s recently published report, The Countdown to 2020, shows that with the 2020 deadline approaching, none of the Forest 500 companies and financial institutions assessed in 2018 are on track to eliminate commodity-driven deforestation from their supply chains and portfolios by 2020. Only half have made commitments to do so by 2020 or earlier. Despite the commitments, deforestation is increasing. A gap has formed between commitments and implementation. Financial institutions are lagging FMCGs in deforestation commitments.

Regarding FMCGs, the following conclusions from the Forest 500 report are relevant:

- Of the companies listed in Forest 500 report, 149, or 43 percent, of the most influential companies in forest-risk supply chains are still not publicly reporting on action to address the risk of deforestation in their supply chains.

- These companies have not set commitments, shown an understanding of their activities’ impacts, or the understood the risks they face.

Reputation value-at-risk for FMCGs: Substantial and moving to higher levels

Increasingly, various stakeholders such as consumers, investors, and bankers will differentiate between FMCGs on the basis of their sustainability performance, leading to potential material investment risks (for the losers) as well as investment opportunities (for the winners).

Two studies, mentioned above, provided guidance to the reputation value-at-risk effects of these developments: Professione showed that an ESG event in the supply chain of FMCGs could result in a value-at-risk of 28 percent, and Pentland Analytics and AON showed that the “losers” in reputation events may face a negative value impact of 29 percent.

An additional element in the latter study is the difference in value performance between winners and losers. Based on an index of 100 in a 2018 event, the losers would have declined to 71 in index value, while the winners would have increased the index value to 120. Thus, winners ended with a value that was 69 percent above the losers. In contrast, in the year 2000, these index numbers would have been respectively 110 versus 83, implying that winners outperformed losers by 33 percent. The difference between winners and losers is underscored by Climate Advisers’ share price index of RSPO-In and RSPO-Out.

Recently, CDP’s Fast Moving Consumers study showed a peer comparison of nine food companies and seven Household & Personal care companies, representing 38 percent of the global market capitalization in this sector. The study focused on “which FMCG companies are ready for the low-carbon economy transition, related to their supply chain, water stress, changing consumer preferences and their climate governance and strategy.” The CDP study not only focused on deforestation; it gives high importance to climate impact of activity throughout the supply chain (affecting Scope 3 emissions). The companies were ranked on four elements:

- Transition risk – raw material risk and Scope 3 emission exposure. The research considers palm oil, meat, dairy, and soy emission impact.

- Physical risk – focus on water stress exposure.

- Transition opportunity risk – impact of consumer changes and investments in renewable energy. Will more environmentally friendly consumption affect the revenues of the company?

- Climate governance & strategy — companies’ governance frameworks including mission reduction targets and the alignment of remuneration with low-carbon objectives.

This CDP analysis provides an input for investors to make a distinction between companies that may become leaders and those that may become laggards in implementing zero-deforestation and other climate commitments. In the Food & Beverage category, Danone and Nestlé are considered leaders, while Mondelez and Kraft Heinz are the laggards. In the Household and Personal Care category, Unilever and L’Oréal are listed as the leaders while the laggards are P&G and Estée Lauder.

Finally, reputation risk impacts on the value of FMCG companies could occur alongside a rise in the cost of capital. An increasing number of banks are already issuing loans that are connected to sustainability targets. ING is already active in this field through loans to Wilmar and DSM. The companies can reduce the interest rates by ca 50 basis-points by meeting sustainability commitments. This number may look low. However, the impact of 50 bps lower borrowing costs on the cost of capital (including cost of equity) can improve the enterprise value of a company (market value of equity and net debt) by 5-10 percent. With financial institutions increasingly focusing on sustainability loans and a strong growth in green bonds and climate bonds, a positive reputation with regards deforestation policies along with execution can substantially support a company’s value.

Taking the above-mentioned trends together, it is likely that the reputation impact on the share price of FMCGs for not meeting 2020 zero-deforestation commitments could be significant. However, this reputation impact is not likely to materialize overnight starting in 2020. Due to their gradually increasing awareness on the involvement of FMCGs in deforestation trends, some consumers, investors, bankers, regulators, and other stakeholders are already changing their buying behavior, capital allocation, etc., implying that an impact on share prices has already begun. But as reputation impact occurs gradually, it is at times difficult to measure. The reputation impact cannot always be separated from other factors simultaneously affecting companies’ share prices. But in the years after 2020, it is likely that the reputation impact of how FMCGs are implementing their zero-deforestation commitments will lead to different share price developments for companies throughout the sector.

Appendix – Methodology

In order to measure a company’s financial performance, its cumulative abnormal returns (CAR) in a time window of three days post the reputational damaging event needs to be calculated. CAR is defined as the sum of abnormal returns from day one to three post the event. Abnormal returns are defined as the difference between the actual returns of a company and the expected returns under normal circumstances (if the event never happened). The expected returns of a company can be estimated with an OLS regression by looking at the relationship of the company’s returns and the market returns. As a proxy for the market returns, the return of an index should be chosen. In the case of a lack of a relevant index, a peer group of the studied company should be chosen, and the average return of the group should replace the index. After that, with the usage of historical price data, the alpha constant and the beta coefficient can be estimated. If the estimation for the beta is significant, then the correct market index was used.

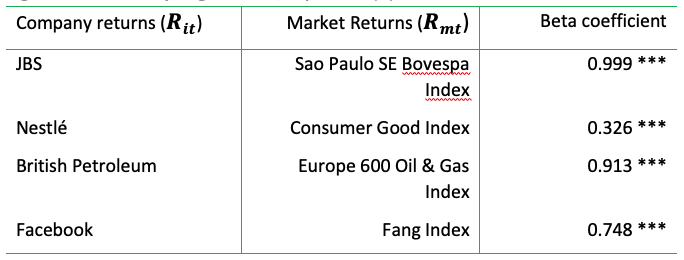

Model

Figure 8 below shows the beta coefficients estimated for the OLS regression corresponding to equation (3). All coefficients are significant at 1 percent level. This shows that the index selected per company studied was appropriate.

Figure 8 Case study regressions, equation (3)

***, **, * indicate significance levels of 1 percent, 5 percent, 10 percent, respectively.

Limitations of statistical methodology

Finally, in quantifying reputation risk, the limitations of the methodology used for the case studies should be taken into account:

- Complications of event may unfold over a longer time (for instance with tobacco).

- The lack of a good peer group/index may hinder the comparison of performance.

- For unlisted companies, the calculation is not possible.

- The isolation of a risk event.