In 2017, Chain Reaction Research (CRR) reported 6.1 million hectares (ha) of forest and peatland remained on oil palm concessions, land that can be considered “stranded assets.” This update discusses figures and trends in the palm oil industry since 2017 and argues that oil palm development on forest and peatland will remain economically unviable for the foreseeable future.

Download the PDF here: 28% of Indonesia’s Landbank Is Stranded

Download the translated version here: Stranded land report_Bahasa

Key Findings:

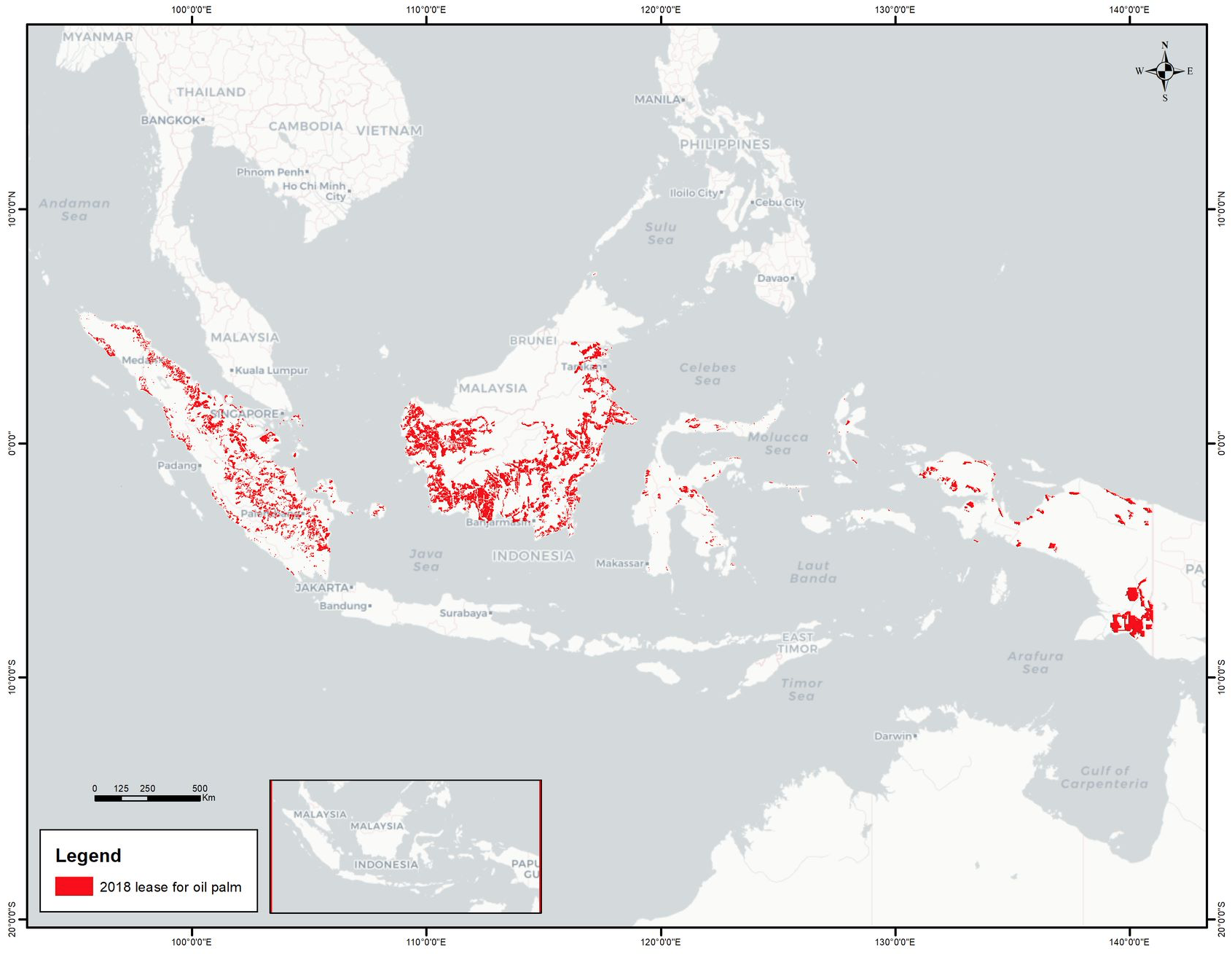

- Since 2017, issuances of new concessions for oil palm plantations in Indonesia have come to a near halt while deforestation rates have dropped. As of May 2019, 22.3 million ha have been issued as oil palm concessions in Indonesia, equal to 12 percent of the country’s land cover, and 6.4 million ha of forest and peatland remain within concessions. This area represents 28.4 percent of the total area under oil palm concessions.

- Undeveloped forest and peatland remain stranded assets in the palm oil sector. The economic viability of oil palm development on forest has come under increasing pressure. Such development is non-compliant with responsible sourcing policies, while non-compliance sanctions have become more severe and detection more likely. The company groups that hold the largest tracts include Indogunta, Hayel Saeed Anaam Group, and Korindo.

- Demand for recovery and restoration to compensate for past deforestation is an emerging trend. Some companies require suppliers on their grievance lists to recover and restore deforested land in order to maintain or regain supply contracts. Oil palm growers may be forced to recognize and settle liabilities for past deforestation.

- Companies with stranded land in 2017 have used a range of strategies to handle these assets. Gama stopped all deforestation to regain entry to NDPE markets. HSA Group used an opaque ownership structure to deny involvement in a controversial project. Austindo Nusantara Jaya opted to service the leakage market. Korindo explored the biofuels market after NDPE suspension.

- A possible solution to the stranded land conundrum is to allocate social forestry programs on stranded land. At least one oil palm grower has dedicated CSR budget to support communities to apply for social forestry allocations with the Indonesian government.

Expansion of oil palm concessions in Indonesia has come to a near halt

In the last two years, the expansion of Indonesia’s palm oil sector has slowed, in line with Indonesian government policies. The issuances of new concessions for oil palm plantations have come to a near halt. At the end of 2018, the area given out as oil palm concessions in Indonesia stands at 22.3 million ha. While this figure is slightly higher than the 21 million ha reported in 2017, the difference may be explained by increased availability of data for older concessions. During the same time span, the Indonesian government first announced and then adopted a presidential instruction that includes a stop on the issuing of new oil palm licenses, in addition to a moratorium on any land use licenses on forest and peatland.

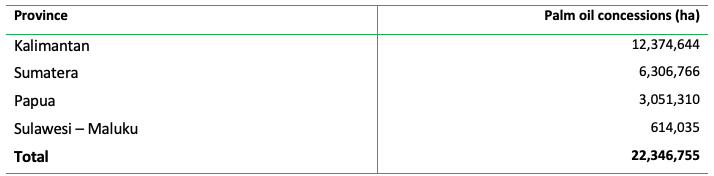

Notwithstanding the deceleration of concession expansion, palm oil remains the commodity with the largest geographical footprint in the country. Oil palm concessions cover more than 12 percent of Indonesia’s total land cover. With 12.4 million ha, the island of Kalimantan is home to most palm oil concessions, followed by Sumatera (6.3 million ha), Papua (3.1 million ha), and Sulawesi/Maluku (614,000 ha).

Figure 1: Land given out as oil palm concessions in Indonesia (2018)

Figure 2: Land given out as oil palm concessions per island (2018)

Sources: BPN, RSPO, District/Province Government, KLHK

Production of palm oil has gone up in recent years. Production on already planted land grew, as the planted area with mature oil palms increased. According to the U.S. Department of Agriculture (USDA), production reached 41.5 million tonnes in 2018/19 and is expected to grow to 43 million tonnes in 2019/20. The USDA projects that the planted area will remain the same in the coming years.

6.4 million hectares of forest and peat on oil palm concessions remain

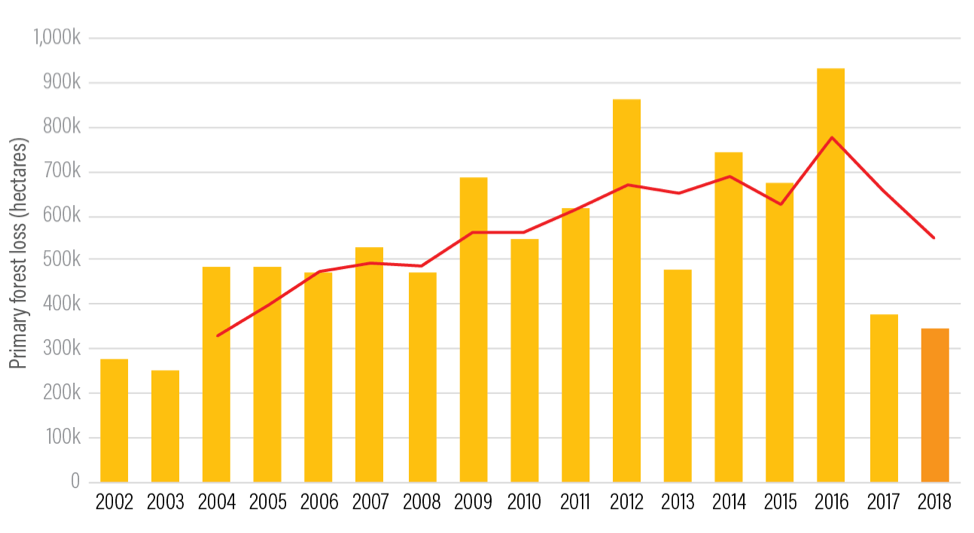

Parallel to the halt in concession expansion, deforestation rates within concessions have also seen a significant drop. In 2017, deforestation on oil palm concessions in Indonesia totaled 95,000 ha. In 2018, this figure stood at 74,000 ha for Indonesia, Malaysia, and Papua New Guinea combined. The decline in palm oil deforestation is also illustrated by overall figures on primary forest loss in Indonesia from Global Forest Watch (GFW), which show a decrease of nearly two-thirds in deforestation rates from 2016 to 2018 (Figure 3). In addition to large-scale oil palm plantations, other drivers of deforestation in Indonesia include timber plantations and smallholder farms.

Figure 3: Primary forest loss in Indonesia 2002-2018

Source: Global Forest Watch

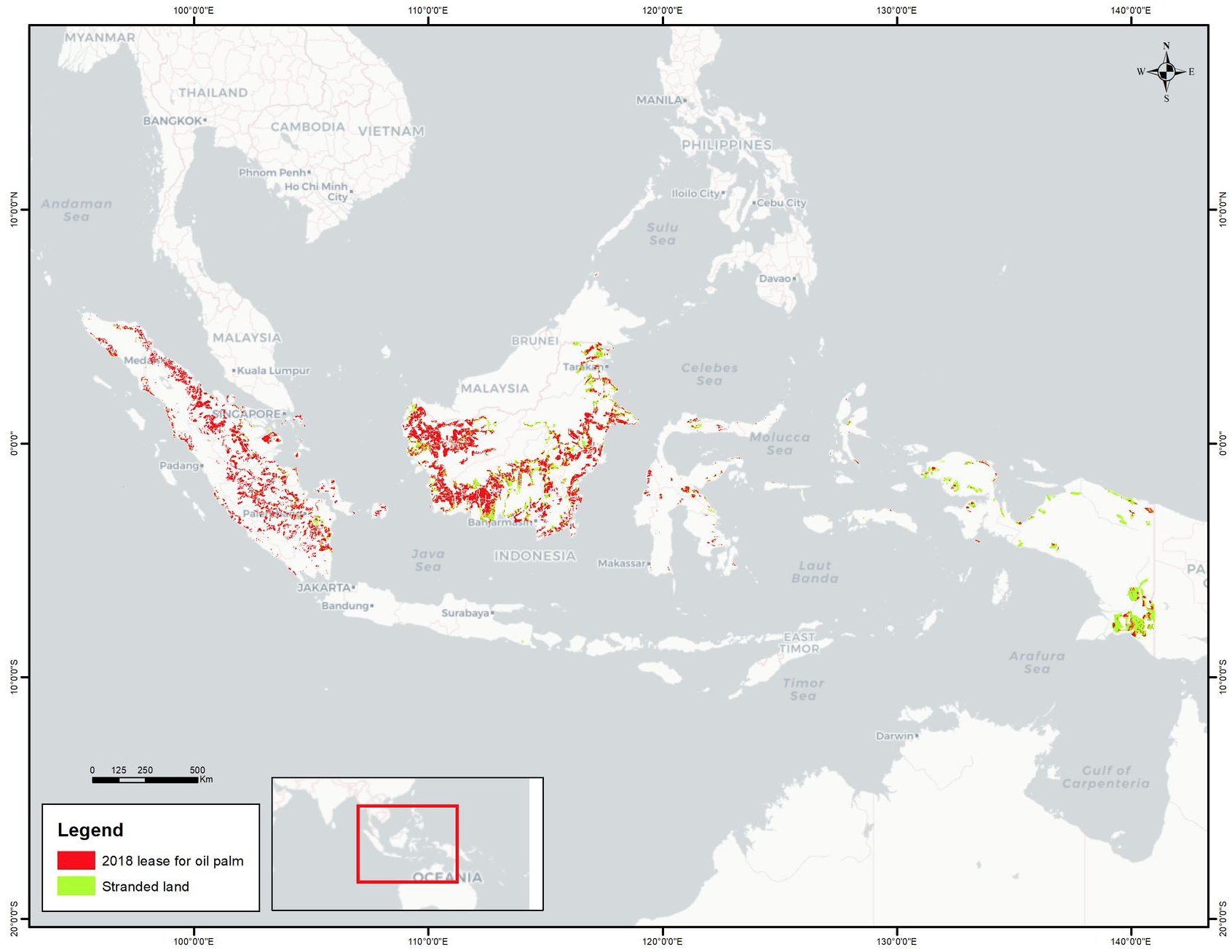

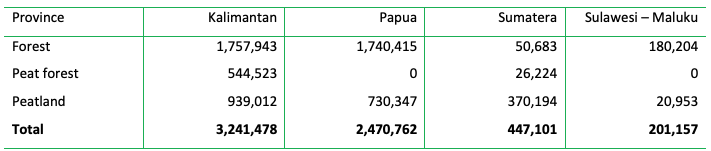

The amount of remaining forest and peatland within concessions stands at 6.4 million ha. This area represents 28.4 percent of the total concession areas. The figure is higher than the 6.1 million ha reported in 2017. The increase is attributed to improved concession data availability and land cover reclassification. Most forest and peatland remain on concessions in Kalimantan (3.2 million ha; 26 percent of concession area) and Papua (2.5 million ha; 81 percent).

Figure 4: Forest and peatland remaining on oil palm concessions in Indonesia (2018)

Figure 5: Forest and peatland remaining in oil palm concessions per island (2018)

Sources: Wetlands International, Kementerian Pertanian, RePProt, FEG KLHK, Aidenvironment, KLHK

As reported in CRR’s 2017 report, remaining forest and peatland can be considered “stranded land” for the purpose of palm oil expansion. Stranded land is a type of stranded assets, or “assets that have suffered from unanticipated or premature write-downs, devaluations or conversion to liabilities.” Conversion of remaining forest and peatland into oil palm concessions is no longer economically viable, as it carries the risk of exclusion from markets that adhere to No Deforestation, No Peat, No Exploitation (NDPE) policies, as well as possible legal liabilities. Due to stranded assets, the Indonesian palm oil industry may be facing a trend of lower growth and equity revaluations.

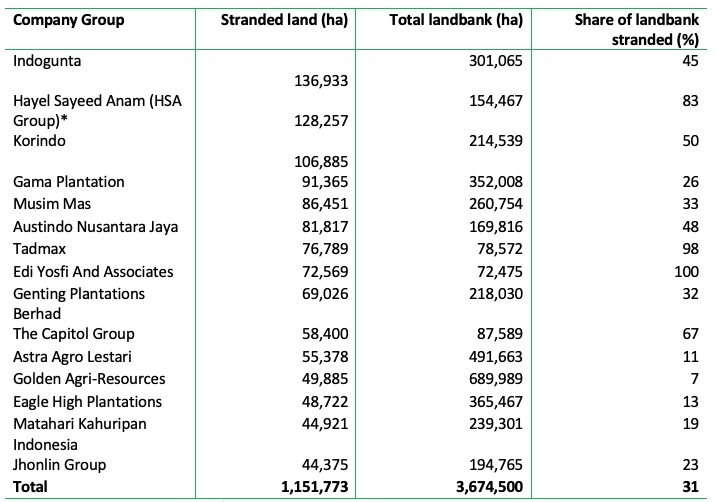

The company groups that hold the largest tracts of stranded land include Indogunta (136,933 ha), Hayel Saeed Anam Group (HSA Group, 128,257 ha), and Korindo (106,885 ha). All three company groups hold large concessions in Papua, either directly or through related entities. The 15 companies with the most stranded land hold a combined 1.15 million ha of undevelopable assets. In the case of Tadmax and the entities controlled by Edi Yosfi and associates, almost their entire landbank consists of forest or peatland. These 15 company groups hold no more than 18 percent of all stranded land. This low concentration illustrates that stranded land is an industry-wide issue.

Figure 6: Top 15 Company Groups with the most stranded land (2018)

*Related entities with joint control and/or ownership, confirmed until June 2018. Source: Aidenvironment

Market and policy demand for zero-deforestation unlikely to change – stranded land to remain an issue for foreseeable future

The economic viability of developing new palm oil concessions on forested or peatland has come under increasing pressure in recent years. Through actions by palm oil stakeholders, including traders/refiners, FMCG companies, civil society and governments, deforestation has become a tangible business risk for oil palm growers. Developing forested concessions may now result in immediate suspensions from NDPE supply chains. These trends are unlikely to change in the near future, and CRR projects that NDPE will remain a condition for access to the majority of palm oil markets. Leakage markets in India, Indonesia and for biofuels and marine fuels may continue to exist, but they are likely to offer less attractive prices and payment conditions.

Deforestation is now more likely to be non-compliant with buyer policies, and sanctions are becoming more severe. The NDPE market segment has grown in the last two years, as a number of “leakage” refiners, including Intercontinental Specialty Fats (ISF), IFFCO, Pacific Inter-Link (a subsidiary of the HSA Group) and Fuji Oil, have adopted responsible sourcing policies or zero-deforestation commitments. Each of these four actors also publish grievance lists, and ISF, IFFCO and Fuji Oil all report supply chain suspensions as the outcome of one or more grievances. Simultaneously, pre-existing policies are implemented with increasing rigor, as Wilmar and others have moved to a “suspend then engage” approach to non-compliance.

Detection of NDPE non-compliance has also become more common. Not only has near real-time satellite information become publicly available, but transparency around supply chain relations, corporate ownership, and concession data has also increased. These changes have facilitated supply chain monitoring and accelerated identification of deforestation within specific supply chains.

Suppressed crude palm oil (CPO) prices have affected the viability of oil palm expansion into forested areas. CIFOR identified that plantation expansion peaked in correlation with CPO price peaks. However, since January 2017, CPO futures prices have dropped some 31 percent.

Sector now demands restoration and recovery plans for past deforestation

An emerging trend in the NDPE market is the demand for recovery and restoration plans to compensate for past deforestation, in addition to requiring stop-work orders and moratoria on future land clearing. The Accountability Framework, a joint set of standards for supply chain commitments launched in June 2019, identifies the company responsibility to remedy past deforestation or conversion and details a set of parameters for effective restoration approaches. The new Principles and Criteria of the RSPO, adopted in November 2018, likewise apply its Remediation and Compensation Procedure for any land clearing without a prior assessment of High Conservation Value or High Carbon Stock (HCV-HSCA). This procedure stipulates the development and implementation of a Remediation and Compensation Plan, with an indicative liability figure of USD 2,500-3,000 per hectare.

Some NDPE companies have publicly communicated that third-party suppliers featuring on their grievance lists will have to develop Recovery Plans in order to maintain or regain supply contracts. Such plans need to include commitments to protect and restore forests and peatland, as well as assist local communities to secure social forestry rights. Oil palm growers Gama and Felda Global Ventures have set a precedent in accepting their responsibility for recovery of forest and peatland. Gama has committed to implement its own Recovery Plans to indemnify some of the past harms. These plans include assistance to local communities to secure land rights and develop alternative economic activities.

Because of these changes, maintaining or regaining access to the NDPE market may not only require an oil palm grower to forego economic opportunities by implementing stop-work orders and moratoria. It may also require the grower to recognize and settle liabilities for past deforestation. Future deforestation is more likely to trigger restoration demands from traders and refiners, adding significant restoration costs to the equation.

Deforestation may be sanctioned under government’s concession review process

In addition to market responses to NDPE non-compliance, the Indonesian government may take legal action against deforestation under its palm oil moratorium. A moratorium on the issuance of new palm oil licenses for concessions in land designated as primary forest and peatland was first issued in 2011, extended in 2013, and extended again in 2015, for two years. In September 2018, President Jokowi officially signed a new three-year palm oil moratorium, via Presidential Instruction No. 8/ 2018 on Suspension and Evaluation of Palm Oil Plantation Licenses and Improvement of Palm Oil Plantation Productivity. In April 2019, Jokowi was re-elected as president of Indonesia for a second five-year term.

As part of the moratorium, the government will conduct a review of existing concessions and forest release permits. The review will specifically look at forests inside concessions that have not yet been converted. The Ministry of Environment & Forestry has identified one million ha of palm oil plantations operating illegally in forest areas. Based on the outcomes of the evaluations, the ministry may reclassify such areas to forest categories. Although a Presidential Instruction has no basis in Indonesian law, the moratorium adds further bureaucratic obstacles to land clearing in forested areas. In some cases, the government may force the return of forested land to the state. Such a scenario would force an oil palm grower to take write-downs on its assets, as well as on development expenses.

Company responses to stranded land: Halting forest clearing, obscuring corporate ownership or servicing the leakage market

Companies with significant stranded land in their portfolio face a clear dilemma: either write down the value of their assets and investments or develop the land at the risk of losing NDPE market access. As CRR described in 2017, the operational status of the concession determines how this dilemma plays out. Companies may forfeit fully undeveloped concessions with limited direct costs incurred, whereas development that is suspended prior to achieving financial hurdle rates can include significant cost write-offs. Cost write-offs could occur when less land is developed than needed to feed a CPO mill (approximately 6,000-8,000 ha).

In 2017, the ten companies with the largest amounts of stranded land within their concessions were Austindo Nusantara Jaya, PTT Green, Eagle High Plantations, Genting, Salim Group, Hardaya, Gama, Astra Agro Lestari, HSA Group, and Korindo. These companies have used a range of strategies to handle these assets. Below are three demonstrable approaches:

- Cease deforestation, implement a stop work order, adopt an NDPE policy, and invest in the measures necessary to satisfy the sustainability demands of the NDPE market. This process allows access to the NDPE markets.

- Disassociate or obscure ownership of the concession with significant stranded land. The approach of using “shadow companies” is intended to continue clearing while simultaneously servicing the NDPE market, but it may not be successful.

- Continue deforestation and service palm oil leakage buyers or seek business opportunities in biofuel and other non-traditional end use markets.

Gama Plantation: Forest clearing stopped after NDPE suspension

Gama Plantation aggressively developed its landbank until it faced NDPE suspensions in 2018. It has since adopted an NDPE policy, consolidated its holdings under one entity, and halted all forest clearings.

Gama Plantation (previously referred to as Gandasawit Utama) had approximately 100,000 ha of stranded land in 2016. In 2018, reports by Greenpeace and Chain Reaction Research highlighted the ownership links between Gama and Wilmar. Greenpeace identified 21,500 ha of forest clearance by Gama since December 2013, predominantly on its plantations in West Kalimantan and West Papua, Indonesia.

In June 2018, Wilmar announced it would stop sourcing from ten Gama companies. Faced with the loss of their biggest buyer, Gama agreed to take measures necessary to remain in the NDPE market. The agreement committed Gama to consolidate their business under one corporate entity, implement an immediate stop work order on all concessions, adopt an NDPE policy, conduct HCS assessments, and develop a compensation and remediation plan for previous forest clearance. Gama’s first progress report, published in February 2019, details significant strides toward meeting these commitments. CRR analysis confirms that since the implementation of the stop work order in August 2018, forest clearance on Gama concessions has ceased. In March 2019, Wilmar’s Suspension Committee lifted Gama’s suspension.

HSA Group: Ownership on personal title used to deny involvement in controversial project

HSA Group responded to NDPE buyer engagement and NGO pressure by denying ownership of the large Papua concession, but was excluded from the NDPE market.

In 2017, HSA Group, together with Tadmax and the Menara Group, held the most stranded land in Indonesia (246,531 ha). This land was part of a 273,394-ha project in West Papua, known as the Tanah Merah project. The Tanah Merah project and its ownership have long been shrouded in secrecy. Four concessions on the project were linked to HSA Group: PT Megakarya Jaya Raya (PT MJR), PT Kartika Cipta Pratama (PT KCP), PT Graha Kencana Mulia (PT GKM), and PT Energi Samudera Kencana (PT ESK).

Notary acts listed Fouad Hayel Saeed Anam, the managing director of the Malaysia and Indonesia arms of HSA Group, as the president commissioner of all four entities. Notary acts also listed Salah Ahmed Hayel Saeed, a Director/ Manager of Pacific Inter-Link’s refining division PT Pacific Palmindo Industri, as Commissioner of PT ESK and PT MJR and President Director of PT GKM and PT KCP, and Nakul Rastogi, a Trading Director of Pacific Inter-Link, as Director of PT GKM and PT KCP.

NDPE traders engaged HSA Group and its subsidiary Pacific Inter-Link concerning the Tanah Merah project. HSA Group reportedly denied involvement in the Tanah Merah project during these engagements. Similarly, the company denied involvement in an official statement to NGOs that had investigated the company in 2018. The company stated that family members joined the board of the four companies “in their personal capacities.”

In June 2018, all individuals affiliated with HSA Group disappeared from notary acts and were replaced as commissioners or directors of these companies. It is unclear if HSA Group has fully divested or the case involves “shadow companies,” where related corporate entities are used to disassociate company groups from controversial assets.

Ongoing discussions are taking place within NDPE traders and civil society concerning definitions of company groups and the precise scope of NDPE sourcing policies. CRR projects that frontrunners will implement NDPE policies on a broad scope that includes company holdings, subsidiaries, joint ventures, associates, and related entities. Such related entities would constitute of companies controlled, jointly controlled, or significantly influenced by the same individuals or their close family members.

Austindo Nusantara Jaya: Deforestation and servicing leakage market

Austindo Nusantara Jaya (ANJ) continued to clear its landbank despite repeated supply chain exclusions. NGOs and international media have extensively covered Austindo Nusantara Jaya’s forest clearance in West Papua. The clearance led to ANJ’s suspension from main NDPE supply chains in 2015, including the supply chains of Wilmar, Musim Mas, Bunge Loders Croklaan and GAR. Additional traders and consumer goods companies also began removing ANJ from their supply chains due to the company’s unwillingness to comply with NDPE commitments.

ANJ’s response to the continued controversy over its development of HCS areas was inconsistent. Already an RSPO member with a commitment to 100 percent certification by 2022, in November 2016 it adopted an NDPE policy with commitments to conserving primary forest, HCS and HCV areas and banning peat development. In 2016, the company temporarily halted land clearing in West Papua while conducting a review of its HCV areas. ANJ also showed a commitment to protecting HCV areas on PT Kayung Agro Lestari in West Kalimantan, collaborating with a local NGO to release rescued orangutans in to the plantations HCV area and instigate a conservation plan to monitor the animals.

Despite these actions, the company continued to clear forest in West Papua. In 2018, ANJ cleared over 2,000 ha, making it the 10th biggest deforester in the region that year. With the clearance on PT Putra Manunggal Perkasa, ANJ became the first company to violate the RSPO’s new Principles & Criteria on HCS conservation in November 2018. The RSPO’s Investigation & Monitoring Unit is currently investigating ANJ and has asked for clarification on inconsistencies in land use planning on its concessions. No new clearing has been identified since December 2018.

ANJ’s ability to find replacement buyers in the palm oil leakage market likely influenced the company’s decision to continue deforesting after being excluded from NDPE supply chains. After the NDPE suspensions, ANJ’s largest suppliers were PT Synergy Oil Nusantara (owned by IFFCO) and Gokul Agro Resources, a player in the Indian leakage market. These two clients accounted for 60-70 percent of quarterly sales between 2Q 2017 and 2Q 2018. However, ANJ’s 2018 annual report no longer lists PT SON or Gokul Agro Resources as significant buyers. PT SON’s 2018 supplier list specifies that ANJ has been suspended as of June 2018 because of clearance of potential High Carbon Stock forest.

Korindo: Exploring maritime biofuel market after NDPE suspension

Korindo moved into the marine fuel market in 2019, after it had been excluded from the NDPE market in 2016. In 2013, the Korean-Indonesian timber and palm oil company restarted clearing tropical forest for oil palm in West Papua and North Maluku. As a result, by 2016, Korindo had cleared 30,000 ha of forest on seven concessions, 12,000 ha of it primary forest. Korindo’s deforestation and lack of commitment to NDPE resulted in suspension from the NDPE market. Nestlé, Bunge Loders Croklaan, Musim Mas, Wilmar and Cargill, among others, committed to not sourcing from Korindo. Korindo was also subject to prolonged advocacy campaigns from civil society organizations. In 2018, a consortium of NGOs documented that construction of the Ariake Arena in Tokyo, a planned venue for the 2020 summer Olympics, included plywood from Korindo’s Indonesian concessions. Japanese timber and building materials trading company Sumitomo Forestry supplied the wood to the venue.

In 2019, Korindo began seeking business opportunities in the regional biofuel market, through a joint venture with the South Korean companies GF Oil and Sejong Technology. They are currently establishing a biofuel plant on the Indonesian island of Bintan and will use CPO from Korindo’s mills to produce biofuel. GF Oil was established in 2012 to market biofuel to industries as a way of reducing greenhouse gas emissions. This venture is understood to be linked to GF Oil’s promotion of biofuel as a way for companies to be compliant with the International Maritime Organization’s global sulphur cap, which takes effect in 2020.

With both Indonesia and Malaysia promoting the domestic production and consumption of biofuels, this growing market may provide new business opportunities for companies excluded from international NDPE markets.

Social forestry may provide solution to stranded land conundrum

With the greater recognition of forested and peatland as stranded assets, questions arise about the most sustainable alternative use of this land. While development for palm oil may not be economically viable or environmentally sustainable, abandoning the area may also pose problems. The government of Indonesia could reclaim the land and reassign it for other purposes such as mining or the cultivation of other crops, thereby posing new threats to the forest. Abandoning a project may also create or exacerbate conflicts with local communities. Their expectations to see economic benefits from palm oil may foster resentment against companies.

One possible solution gaining traction is allocating stranded land for social forestry under government programs that aim to alleviate poverty, halt deforestation, end forestland conflicts, and mitigate climate change. This program, launched in 2016, aims for community management of 12.7 million ha of forest until 2021. However, the Ministry of Environment and Forestry has so far allocated only some 15 percent of this land.

Bumitama is an example of an oil palm grower that has dedicated CSR budgets to develop landscape projects that include support to communities to apply for social forestry allocations. These programs focus on both stranded land and land outside of concession boundaries. While challenges inevitably remain, corporate support for community management of land may become the most viable option to mitigate the various risks associated with stranded land.

One potential challenge is that the Ministry of Environment and Forestry has included only permanent forestland in its indicative map of potential sites for social forestry projects. Most, if not all, of the remaining forest on oil palm concessions are classified as areas for other purposes. Thus, overlap between stranded land and social forestry allocations is limited. However, reassignments of social forestry allocations in the future may follow the government review of oil palm concessions under the palm oil moratorium.