Cargill is the largest privately-held company in the United States and the second largest soy exporter in Brazil. In April 2018, Chain Reaction Research (CRR) concluded that Cargill’s 2030 zero-deforestation deadline allowed its Brazilian suppliers to continue deforesting in the Cerrado. This report assesses Cargill’s current deforestation risks in Brazil’s soy supply chain, given recent changes in corporate policies, market conditions and deforestation trends.

Download PDF here: Cargill’s New Policies Insufficient to Fully Mitigate Deforestation Risks in Brazil

Key Findings:

- Cargill has faced lower revenues and profitability over the past five years. Cargill recognizes that its traditional business model of large sourcing networks and arbitrage trading “is over.” Cargill has strengthened its supplier relationships and diversified into animal nutrition and meat production.

- In February 2019, Cargill published a new soy policy and an updated forest policy. Cargill will provide financial incentives to help curb deforestation and apply non-compliance mechanisms. As a member of the Soft Commodities Forum (SCF), Cargill is prioritizing 25 Cerrado municipalities with targeted interventions.

- Cargill’s new policies may not mitigate all deforestation risks in its Brazilian supply chain. Cargill may be exposed to Cerrado deforestation risks beyond the 25 SCF priority municipalities. Financial incentives may not discourage legal deforestation. Non-compliance with the Soy Moratorium remains a risk in the Amazon biome.

- Value of deforestation risks could be material. Cargill’s assets in high-risk areas are estimated at USD 0.3 billion, one percent of total fixed assets. Its deforestation risk exposure could lead to revenue-at-risk, financing and reputation risk, with a combined value of USD 19 billion.

- Cargill may face higher cost of capital as its lenders may tighten their deforestation policies. Cargill lenders with policies include BNP Paribas, Barclays, Deutsche Bank, RBS, Santander, Standard Chartered, JP Morgan, Rabobank, Société Générale, Citigroup, ING Group, Mitsubishi UFJ Financial, and HSBC.

Cargill remains Brazil’s second largest exporter

Cargill is one of the world’s biggest agricultural commodities suppliers. The company operates four business segments: Animal nutrition and protein, food ingredients and applications, originating and processing, and industrial and financial services. It is the largest privately held corporation in the United States, with FY2019 revenue of USD 113.5 billion. Adjusted operating earnings in FY2019 were USD 2.8 billion, down by 12 percent from FY 2018.

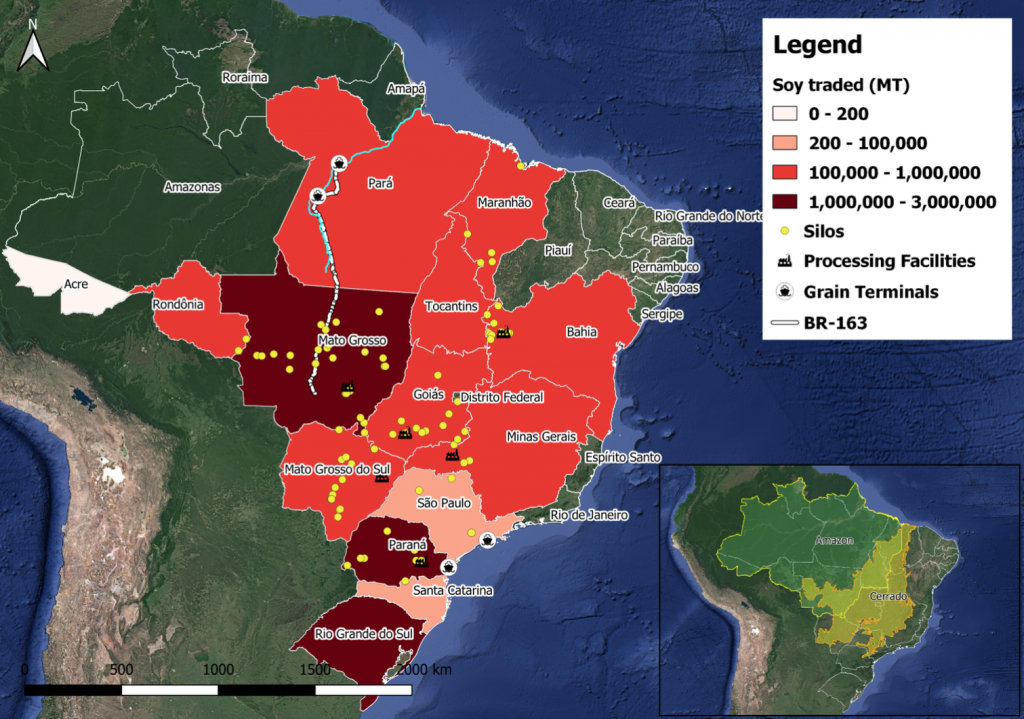

Cargill is the second largest soy exporter in Brazil, handling 12.2 million metric tons of soybeans in 2018. The company’s subsidiary Cargill Agrícola S.A., headquartered in São Paulo (Brazil), has a presence in 17 Brazilian states, operates industrial units and offices in 160 municipalities, and has over 10,000 employees. The company operates six soy-processing facilities (Figure 1), five port terminals (one through a joint venture with Louis Dreyfus Commodities), 152 warehouses, and one innovation center. Since April 2018, Cargill has invested in expanding and modernizing several oilseed-processing plants in Brazil.

Cargill is the largest soy exporter in 236 municipalities in Brazil. It sources soybeans from all the major production areas throughout Brazil (Figure 1), with a dominant presence in Mato Grosso (2.9 million metric tons in 2017), Paraná (2.4 million), Rio Grande do Sul (1.2 million), Mato Grosso do Sul (1 million) and Goiás (0.7 million).

Figure 1: Cargill’s soy facilities and sourcing areas in Brazil

Sources: Trase 2017, SICARM 2019, Cargill website 2019

Cargill adapts business strategy to more supplier engagement and product diversification

Cargill recognizes that its traditional business model in the agricultural supply chain “is over.” While Cargill traditionally relied on a large sourcing network and arbitrage trading, its business model is changing. More players have entered the commodity trading market, while producers have grown larger and invested in their own storage assets. These trends have prompted Cargill’s suppliers to time their sales when prices are higher. In addition, information on commodity prices, trade flows, and crop yields are becoming widely available and affordable to Cargill’s suppliers and clients. The competitive advantage of grain traders’ inside knowledge is therefore diminishing.

In addition, China-U.S. trade tensions and supply chain disruptions particularly affect Cargill’s origination and processing business. Profits in Cargill’s main grain trading and processing segment declined in March 2019 as a result of lower U.S. sales of soy to the Chinese market and a deadly swine virus in China. Due to the China-U.S. trade dispute, the United States is expected to export 13.5 million metric tons less soybeans in 2019 compared to the previous year, as China reduced imports of U.S.-grown products. In addition, the swine fever in China translated into less demand for animal feed, affecting global demand for soy. China’s soybean imports may fall by 5-8 million metric tons due to the outbreak. Forecasts point to a 14-18 percent decline in Brazilian soybean exports in 2019 as a result of less Chinese buying, a lower harvest projection, and rising domestic demand for biodiesel use.

To balance market volatility and smaller margins, Cargill has strengthened its supplier relationships and diversified into other segments. Moreover, Cargill’s geographic spread buffers vulnerability to shifting soy markets and supply chain disruptions. To guarantee supply of raw materials, the company has offered more services to farmers, such as digital tools to guide cultivation. The tools provide grain marketing decision support, e-commerce, and account management software. Moreover, the company trained over 475,000 farmers worldwide in sustainable agricultural practices in 2018.

Cargill has moved into animal nutrition and meat production. The animal nutrition and protein segment was the largest contributor to its earnings in FY2018, accounting for almost half of Cargill’s adjusted operating earnings. While grains trading is crucial to Cargill’s operations worldwide, the company has expanded its business of producing animal feed, rearing livestock, and selling meat. Unlike its competitors Bunge, ADM, and Louis Dreyfus, the company has increasingly invested in beef processing in North America, as well as poultry and fish. In Brazil, Cargill’s subsidiary Nutron Alimentos Ltda produces animal nutrition for various species, including cattle, poultry, swine, and supplements for the cattle breeding business.

Cargill adopts new soy and forest policies with wider scope and priorities, but caveats remain

In February 2019, Cargill published its Policy on South American Soy. The commitment includes:

- A transformation to deforestation-free supply chains, while protecting native vegetation beyond forests;

- The promotion of responsible production, which benefits farmers and surrounding communities;

- Respecting and upholding the rights of workers, indigenous peoples and communities; and

- Upholding high standards of transparency through reporting of key metrics, progress and grievances.

Cargill’s June 2019 Action Plan specifies incentives it offers to suppliers for alternatives to native vegetation conversion, as well as its mechanisms to address non-compliant suppliers. The action plan consists of six elements and is based on the Soy Toolkit (produced by Proforest on behalf of the Good Growth Partnership) and the Accountability Framework. Cargill commits to “providing US$30 million in funds to accelerate economically viable options for farmers as alternatives to converting native vegetation.”

Cargill’s non-compliance protocol does not specify corrective actions required from suppliers that deforest legally. The protocol includes the suspension of suppliers that violate pre-existing embargoed or protected areas, appear on forced labor lists, and engage in illegal operations. Other plans involve categorizing and prioritizing suppliers by risk level.

The company also updated its Forest Policy in February 2019. The new policy, which applies to all agricultural supply chains, is an update of the company’s 2015 Forest Protection Action Plans. The 2015 action plan for sustainable soy, which focused on compliance with the Soy Moratorium and the Brazilian Forest Code, prioritized tackling illegal deforestation, i.e. deforestation inside legal reserves, in embargoed areas, natural conservation areas, or in properties without a Rural Environmental Registry (CAR).

The new soy policy and the updated forest policy are wider in scope and priorities (Figure 2). Specific to Brazil, the latest soy policy (Figure 2) now includes the Cerrado, a large tropical savanna biome that covers more than 20 percent of Brazil and has seen high rates of deforestation since 2000. Moreover, the policy includes protecting native vegetation beyond forests, with “the aim to end native vegetation conversion in the shortest time possible reconciling the production of soy with environmental, economic and social interests.”

Cargill’s 2019 policies do not specify a time-bound zero-deforestation commitment. Cargill has communicated to CRR that it remains committed to making all its agricultural supply chains deforestation-free by 2030. The company has publicly stated that it does not expect to meet the 2020 midpoint deadline stipulated in the 2014 New York Declaration on Forests (NYDF). Cargill states that “its revised policies, operational guidelines and supply chain specific time-bound action plans reflect the guidance received, through consultation, from civil society for greater implementation transparency.”

Figure 2: Comparison of Cargill’s 2015 and 2019 policies and plans in Brazil

Sources: Cargill Policy on Forests (2015), Forest Protection Action Plans (2015), Cargill Soy Policy (2019), Cargill updated Forest Policy (2019), Cargill Soy Action Plan (2019)

Cargill commits to transparent and traceable soy supply chains in 25 high-risk Cerrado municipalities

In February 2019, Cargill also committed to a common framework supporting transparent and traceable soy supply chains in Brazil’s Cerrado region. Six members of the World Business Council for Sustainable Development’s (WBCSD) Soft Commodities Forum (SCF) committed to disclose supply chain data by monitoring and publishing municipality-level trade data. The first report was published June 6, 2019. In addition to Cargill, the members include Bunge, Louis Dreyfus Company, Archer Daniels Midland, Glencore Agriculture, and COFCO International.

The SCF identified 25 priority municipalities in the Cerrado for targeted interventions to address native vegetation conversion to soy. These municipalities (Figure 3) were selected on the basis of 1) location within the Cerrado biome; 2) relevance of soy planting; 3) where soy is driving native vegetation conversion; and 4) where multiple SCF members are present. Each of the SCF members report individually on the percentages of soy sourced directly and indirectly from farmers in these municipalities.

Figure 3: Soft Commodity Forum prioritization of 25 high-risk municipalities

Source: SCF Progress Report (June 2019)

According to its June 2019 Progress Report, Cargill sourced 37.4 percent of its Brazilian soybeans from the Cerrado. A total of 23.1 percent of its Cerrado supplies originate from the SCF priority municipalities, mainly from direct suppliers (96.6 percent).

Cargill’s soy and deforestation policies may not mitigate all risks

With the broader scope and additional measures, Cargill has taken a next step toward a zero-deforestation supply chain. However, with rapid action needed to limit climate change, its actions may not fully address its exposure to deforestation risks. The Amazon is close to reaching a tipping point after which it may undergo irreversible changes, the Cerrado conversion is affecting Brazil’s water systems, and recent deforestation rates are increasing in both the Amazon and Cerrado biomes. CRR recognizes three main risks that Cargill’s approach may not fully mitigate:

- Cargill may be exposed to Cerrado deforestation risks beyond the 25 SCF priority municipalities;

- Financial incentives may not be enough to discourage producers from deforesting legally within the 25 SCF priority municipalities; and

- Non-compliance with the Amazon Moratorium is a significant risk in municipalities where Cargill is present.

Cargill may be exposed to Cerrado deforestation risks beyond the 25 SCF priority municipalities

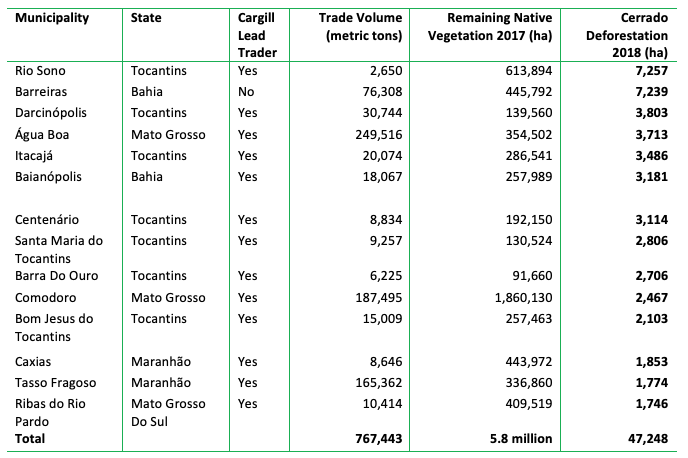

Cargill is exposed to deforestation risks in at least 14 municipalities in the Cerrado that the SCF did not prioritize.A total of 47,248 ha of Cerrado vegetation was lost in 2018 in these 14 municipalities (Figure 4).

Seven of these municipalities are located in the state of Tocantins. Soy sourced from Tocantins carries a high risk of being connected with legal and illegal land clearing, and multiple socio-political controversies. In addition, four municipalities (Darcinópolis, Água Boa, Bom Jesus do Tocantins, and Comodoro) fall within both the Amazon and Cerrado biomes. The SCF has not prioritized these municipalities, but they have seen significant rates of Cerrado deforestation and are at the frontier of agricultural expansion. The situation is similar in the municipality of Comodoro (MT), where Cargill is the largest soy trader (sourcing 187,495 MT in 2017) and large strands of native vegetation remain.

Figure 4: High-risk municipalities for Cargill not prioritized in the Soft Commodities Forum

*High-risk municipalities are defined as: 1) High deforestation rates in 2018; 2) Cargill is a major buyer of soy; and 3) significant strands of native vegetation remain. Sources: Trase 2017, Mapbiomas 2017, Prodes 2018

Financial incentives may not discourage producers from deforesting within SCF priority municipalities

Cargill’s Soy Action Plan and the SCF Progress Report provide limited details on how the company will monitor high-risk municipalities and suppliers. Cargill’s Soy Action Plan suggests categorizing suppliers by risk level but remains unclear on the company’s related actions. By June 2020, the company will develop a list of priority farmers and producers for “deeper dialogue and action.” Moreover, as stated in the SCF commitment, “subsequent reporting will provide information on specific actions being taken to improve direct engagement with farmers to address risks in the municipalities.” A more detailed description of how Cargill will address deforestation risks within the 25 SCF priority municipalities is expected in its next progress update.

Cargill may offer financial incentives to suppliers in exchange for refraining from legal deforestation. This intervention would align with the position of the Cerrado Working Group (GTC). Cargill will exclude farms from its supply chain in the case of illegal deforestation or other non-compliance of its Soy Action Plan. Legal deforestation is not considered non-compliance.

It remains uncertain whether incentive schemes will dissuade producers from further conversion of native vegetation. In direct response to Cargill’s policy update, the producer association Aprosoja issued a press release voicing its opposition to the compensation plans. The association is poised to expand grain production in the Cerrado. If a producer refuses to participate in the incentive scheme and deforests further, Cargill’s current approach provides no guarantee that such deforestation is excluded from its supply chain.

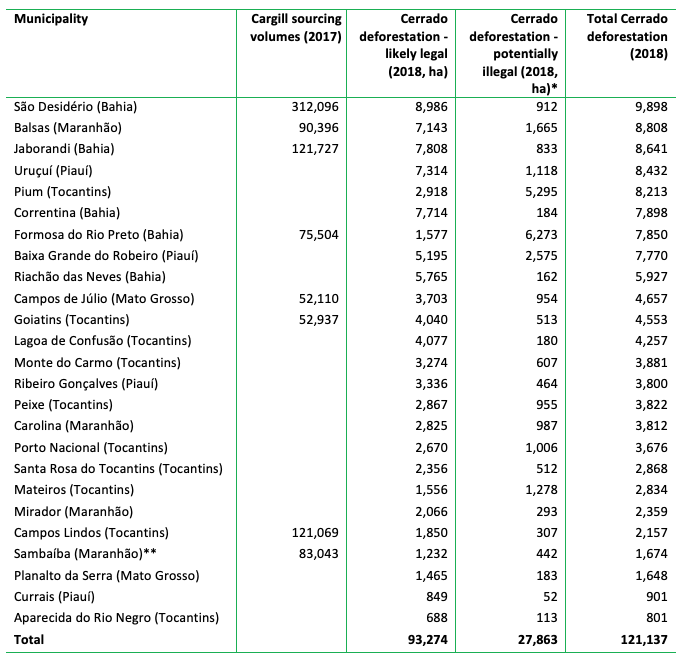

In 2018, the SCF priority municipalities saw a total of 121,137 ha of Cerrado deforestation, of which 77 percent (93,274 ha) was likely legal (Figure 5). In Goiatins, Jaborandi, Campos Lindos, and Sao Desidério, Cargill was the largest purchaser of soy in 2017. Therefore, Cargill will likely allocate a significant portion of the funds used as an alternative for native vegetation conversion to farmers in those municipalities. Cargill was also the largest buyer in Sambaíba in 2017, but closed its warehouse in 2018.

Figure 5: Cargill presence and deforestation rates in 25 SCF priority municipalities

*Potentially illegal is defined as deforestation taking place on land designated as indigenous territories, natural reserves, legal reserves under Brazil’s Forest Code, and areas of permanent protection under Brazil’s Forest Code; ** Cargill closed its warehouse in Sambaíba in 2018. Sources: Trase 2017, CAR 2019, Prodes 2018

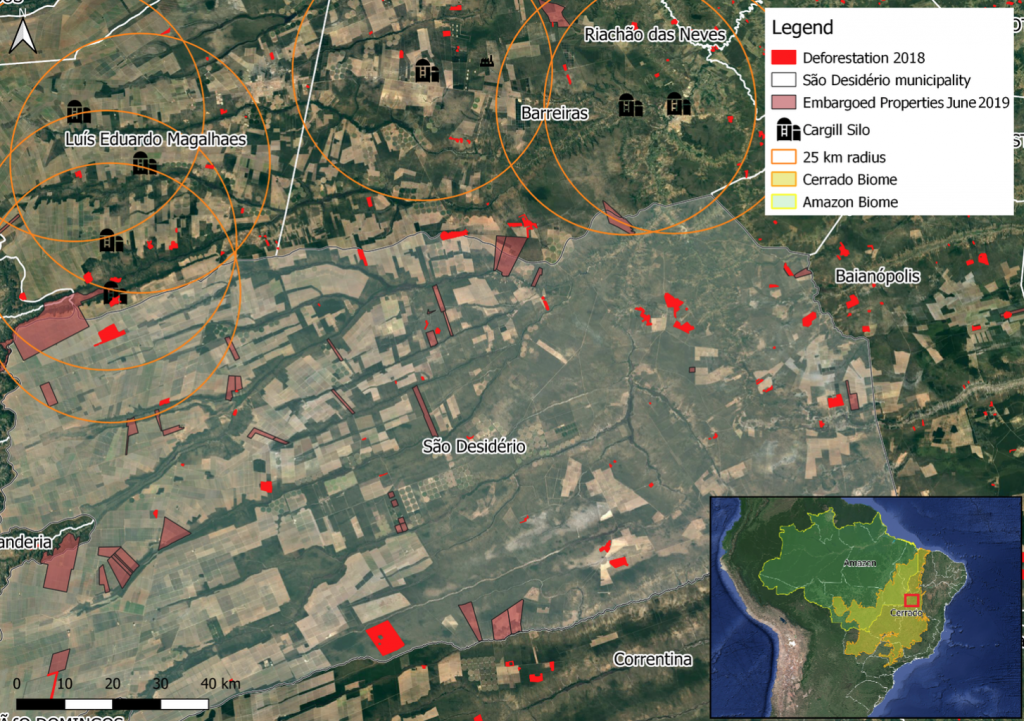

São Desidério (Bahia) has lost the highest amount of native Cerrado vegetation since the beginning of 2018. A total of 9,898 ha was cleared in 2018. Between January and May 2019, nearly 3,000 ha was lost. Cargill buys 24 percent of the traded soy in the municipality (1.3 million MT). The company sourced 312,096 MT of soy from São Desidério, and another 171,809 MT from nearby soy municipalities Formosa do Rio Preto, Barreiras, Cotegipe, Tabocas do Brejo Velho, and Baianópolis. One of the of largest deforested areas in São Desidério falls within a 25-kilometer radius around Cargill’s storage facilities (Figure 6).

Thirty-nine farms in São Desidério are embargoed by IBAMA, Brazil’s Environmental Protection Agency. IBAMA embargoed them for illegal deforestation in protected areas or in areas where authorization is pending. In addition, Comissão Pastoral Da Terra (CPT), a Brazilian organization tracking land, water, and labor conflicts and casualties in Brazil, reported eight agrarian conflicts in 2018 in the municipality and the five bordering municipalities from where Cargill sources. The conflicts involved 257 families and an area of 80,000 ha. In 2017, CPT reported three conflicts, involving 635 families.

Figure 6: Deforestation, embargoed areas, and Cargill facilities in São Desidério

Sources: Trase 2017, CAR 2019, IBAMA 2019, SICARM 2019, Prodes 2018

Non-compliance with the Amazon Moratorium remains a significant risk

In addition to deforestation risks in the Cerrado, Cargill may face a decrease in sourcing areas because of the Amazon Moratorium. In 2018, 370,808 ha of Amazon vegetation was deforested in the municipalities where Cargill sources soybeans. The 2017/18 Soy Moratorium monitoring report lists 60 municipalities with soy production that is non-compliant with the Soy Moratorium. In these municipalities, soy was grown during the 2017/18 season, deforestation took place between 2009-2017, and some of the soy production takes place on deforested land.

Cargill is the dominant soy trader in the municipalities of Cláudia and Tabaporã in Mato Grosso (MT), Pimenteiras do Oeste in Rondônia (RO), and Dom Eliseu in Pará (PA) (Figure 7). In these municipalities, Cargill holds a market share larger than 50 percent. They all have more than 1,000 ha of polygons blocked through the Soy Moratorium. Several have seen an uptake in deforestation in 2018 and 2019. The higher deforestation rates may result in more areas blocked through the Soy Moratorium in coming years.

Figure 7: Cargill’s presence and recent deforestation in selected Amazon municipalities

Source: ABIOVE, Trase 2017, Prodes 2018

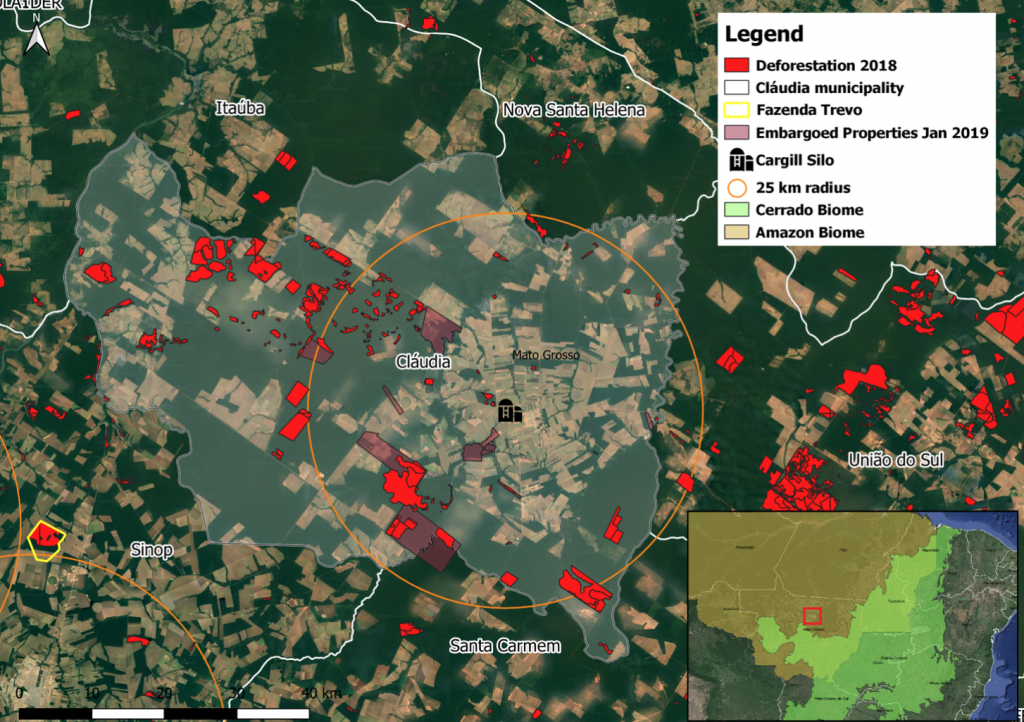

In the municipality of Cláudia (MT), deforestation rates have nearly quadrupled since 2016. The municipality is among the top five municipalities with the highest deforestation rates in 2018. A total of 18,292 ha of native Amazon vegetation were lost. The soy-producing area is situated in both the Amazon and the Cerrado, potentially causing loss of native vegetation in both biomes. A total of 354,375 metric tons of soy were produced in 2017, occupying a total of 105,000 ha of land.

Cargill is the main trader in Cláudia, with a reported market share of 69.8 percent. Cargill owns a warehouse in Cláudia with storage capacity of 720,000 metric tons and mainly exports to China. While Cofco Brasil, Cláudia Armazéns Gerais, and Sipal Indústria e Comércio operate neighboring warehouses, none of them exceeds a capacity of 100,000 metric tons. In a 25-kilometer radius around Cargill’s warehouse, 8,390 ha of native vegetation were cleared in 2018 (Figure 8).

At least one farm with supply chain links to Cargill (Fazenda Trevo) appears to have logged, potentially illegally, 955 ha of Amazon vegetation in 2017. Logging patterns as identified on this farm regularly precede full conversion of forest to farmland. In 2017, the owner of this farm supplied corn to Cargill Agrícola (Figure 8). This farm may be blocked under the Soy Moratorium next year.

Figure 8: Deforestation, embargoed areas, and Cargill facilities in Cláudia

Sources: Trase 2017, CAR 2019, IBAMA 2019, SICARM 2019, Prodes 2018

Business risks may mount due to failure to meet zero-deforestation commitments

Cargill has admitted that it will not meet the 2020 NYDF midpoint deadline for zero-deforestation supply chains. Most other NYDF signatories will also fail to meet this deadline. Meanwhile, deforestation rates in both the Cerrado and the Amazon biomes are rapidly increasing. As a result, the company may become more exposed to reputation and market access risks. These risks may become material to Cargill’s business model.

Cargill finds itself in the crosshairs of civil society

Cargill’s updated soy policy and action plan triggered an instant backlash from Mighty Earth, a U.S.-based campaign organisation. Mighty criticized the perceived lack of ambition of Cargill’s update and pointed specifically at the absence of a non-compliance mechanism that goes beyond minimum legal requirements. Mighty also flagged the low amount of funds dedicated to zero-deforestation compared to Cargill’s overall annual revenues. In July 2019, Mighty named Cargill “the worst company in the world.”

Mighty’s press release is just one example of the increasing pressure by civil society on deforestation-linked supply chain actors. This pressure is occurring globally and specifically in the Cerrado. As 2020, the year generally set as the deadline for deforestation-free supply chains, is approaching, more frequent and intensive public campaigns are likely. As Cargill remains active in deforestation hotspots in the Cerrado and its policies fall short of civil society expectations, such campaigns will likely continue.

A demonstratable decrease in deforestation in the SCF priority municipalities would mitigate this risk. However, anything short of that development may lead to public calls for more rigorous measures, including suspensions of supplier groups that deforest legally or even a complete withdrawal from controversial hotspots.

Cargill may fail to meet expectations of clients

Signatories of the Statement of Support (SoS) for the Cerrado Manifesto are calling for greater action to address legal deforestation. Signatories include a number of likely Cargill clients. Cargill’s updated soy policy does not ban legal deforestation. It is unclear how Cargill will deal with soy suppliers that are clearing native vegetation but comply with Brazilian law. Cargill uses ambiguous language with regard to the distinction between legal and illegal deforestation. The company states that it will “use our influence and activities to create incentives to conserve native vegetation and provide environmental services above those required by the law.” The language suggests that Cargill continues to allow legal deforestation in its supply chain. This action may contradict the policies and ambitions of Cargill’s clients, many of whom have made their own 2020 commitments. In response, Cargill states that it “will promote customer uptake of certification and proprietary Deforestation and Conversion Free programs that drive farm-level progress such as Triple S, Smart Soy, RTRS, Proterra, 2BS and ISSC.”

Cargill may not adequately assure its clients that high-risk suppliers are excluded from their indirect supply chains, since the company does not disclose its list of soy suppliers. While the SCF contributes to traceability in Cargill’s soy supply chain in the Cerrado, information on specific supply chain links is not publicly available. This situation makes it difficult to determine the presence of deforestation-linked soy in supply chains. Within the municipalities of São Desidério and Cláudia, soy suppliers in the vicinity of Cargill facilities are connected to legal and illegal deforestation of Cerrado and Amazon vegetation, environmental fines, embargoed areas, and land and water disputes.

Hidden suppliers represent a risk in an area that is seeing negative environmental and social impacts from soy agribusiness. Cargill states it will have “internal controls to prevent purchases of products that are from non-compliant areas as identified by the Brazilian Ministry of the Environment (IBAMA).” It is unclear to what extent the monitoring mechanisms of Cargill cover farms that have recently illegally deforested. The case of Cláudia shows that past suppliers to Cargill may be blocked in the future.

Financial Risk Analysis

The elaborated deforestation-related risks could impact Cargill’s financial performance at various levels. This section explains:

- The financial costs of a zero-deforestation supply chain. This calculation focuses on Cargill’s assets in Brazil which might become stranded, the establishment of a monitoring system and the incentives to farmers. These initiatives are mentioned in the June 2019 Action Plan by Cargill.

- The revenue-at-risk related to customers that have zero-deforestation commitments.

- The cost of capital risk, detailing the financiers of Cargill’s loans and bondholders and how noncompliance related to deforestation in Brazil may impact these relations.

- Reputation risk and its impact on Cargill given it is a non-listed company.

Recent results and financials: Pressure on profits

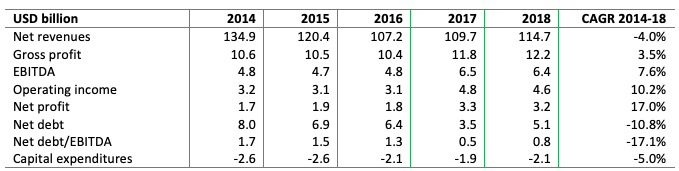

Cargill has been under pressure from decreasing revenues and profits during the past five years (Figure 9). From 2014-2018, Cargill’s net revenue CAGR was -4 percent. The revenues declined from USD 134.9 billion (2014) to USD 114.7 billion (2018). This decrease is partially the result of falling prices in the grain and oilseeds market. From 2014-2018, Cargill’s profitability has improved with EBITDA rising to USD 6.4 billion in 2018 (7.6 percent CAGR) and net profit reaching USD 3.2 billion (17.0 percent CAGR). In 2018, net revenues and EBITDA increased slightly by five percent and three percent respectively versus 2017. However, EBIT and net profit decreased by four percent and three percent respectively.

All of Cargill’s business segments in 2018 saw results fall below year-ago levels except for industrial and financial services. In its fiscal 2019 full year earnings release, Cargill reported a 12 percent decrease in adjusted operating earnings to USD 2.8 billion. Net profit decreased by 17 percent to USD 2.6 billion compared to the previous year. Net revenues declined by one percent to USD 113.5 billion. Lower earnings were the result of flooding, declining export sales due to Chinese swine fever, and trade flow disruptions amid the U.S.-Chinese trade war.

Figure 9: Key financial figures (as of 31st May)

Note: 2019 figures are not included as the Annual Report 2019 is not published as of publication of this report. Source: Bloomberg

During 2014-2018, net debt decreased by 36 percent from USD 8 billion to USD 5.1 billion. Compared to 2017, net debt increased by 46 percent in 2018. This increase is likely from the consolidation of various acquisitions that the company completed. During 2018, Cargill invested 71 percent of it USD 5.2 billion cash flow from operations in acquisitions, joint ventures, and new facilities. Still, net debt/EBITDA ratio remains low at 0.8x.

The animal nutrition and protein segment was the “largest contributor” to the company’s adjusted operating earnings in 2018 at almost 50 percent. In 2018, Latin America made up 11 percent of total sales and 22 percent of total personnel.

Stranded asset risk: Cargill has fixed assets in high-risk municipalities, but value is relatively small

With substantial assets in Brazil, including silos, processing facilities and grain terminals Cargill could face risks of stranded assets. Cargill’s Brazilian operations accounted for approximately 12 percent of its net revenues in 2017. Based on Cargill’s total property and other assets of USD 26.3 billion, approximately USD 3.2 billion could be linked to Brazil. Assuming 50 percent of this value is connected to soy, the value of Cargill’s soy-related assets is estimated to be USD 1.6 billion.

A total of 16 percent of Cargill’s silo capacity is located in high-risk municipalities including those prioritized by SCF. As a result, USD 253 million, or one percent, of the company’s net assets may be at risk. Cargill’s silos in Brazil have a total capacity of 9,176 million tons.

Cargill’s monitoring costs are estimated to be USD 25 million. Cargill does not provide specific details about the costs of monitoring its supply chains and the farmer incentive program. In an earlier report on AAK from CRR, the annual supply chain monitoring costs were estimated at USD 5-10 million. As Cargill’s footprint is much larger than that of AAK’s, USD 25 million could be a fair estimate. This amount would represent only 0.4 percent of Cargill’s EBITDA.

Cargill’s farmer incentive program is USD 30 million, or 0.5 percent of its 2018 EBITDA. That, however, is a one-time cost. These costs are relatively small given Cargill’s size.

Revenue at Risk: Revised zero-deforestation targets may affect EBITDA by USD 1.6 billion

Leading food processors, food retailers, and restaurants linked to Cargill are increasingly adopting zero-deforestation policies. Cargill does not provide a list of its material/biggest clients. Its customer base consists of farmers and meat processors in its animal nutrition and protein unit, food processors in its food ingredients and applications unit, and animal feed companies and food processors in its origination and processing unit. Food processors are thus an important client segment. Food retailers and food services companies are linked to Cargill through the animal feed used in their supply chains for livestock products such as meat and dairy. With leading food processors, retailers, and food services companies increasingly adopting zero-deforestation policies, Cargill may lose clients to its competitors that are aligned with these targets.

Europe contributed 25 percent of Cargill’s 2018 net revenues, which puts approximately USD 29 billion at risk. A previous CRR report concluded that Europe-based FMCGs in particular may face reputation risks when sourcing from deforested land. This risk is related to EU regulations and their relatively advanced policies. According to Forest Trends, about 32 percent of the total researched companies with zero deforestation commitments are based in Europe. As the Cargill’s EBITDA margin is 5.6 percent, the EBITDA-at-risk would total USD 1.6 billion. There are two effects from this:

- The pro forma EBITDA of USD 4.8 billion would lead to a Net debt/EBITDA ratio of 1.1X, which is still a healthy level.

- In value terms, based on a DCF calculation with a seven percent costs of capital, a decline of USD 1.6 billion EBITDA would result in a value loss of USD 17.9 billion. In terms of a private company like Cargill, this loss would translate into USD 17.9 billion present value of lower future dividends and investment opportunities.

Financing risk is limited due to debt reduction, loan providers might develop leverage

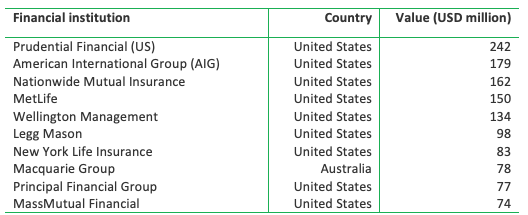

Cargill’s financing risk is limited due to debt reduction. The company increased its debt slightly in 2018. However, the net debt/EBITDA ratio is still at a safe level below 1X. At the end of FY2018, the company’s total gross debt stood at USD 9.2 billion (Bloomberg). The majority of this debt (USD 7.1 billion) is in bonds.

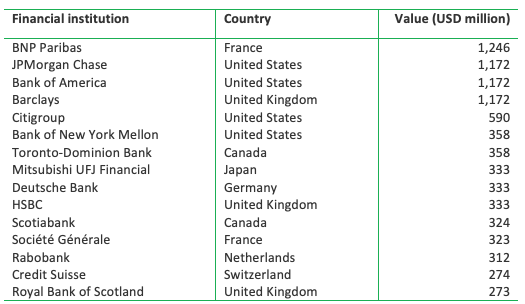

The company’s bond owners have weak or no zero-deforestation policies. Figure 10 below shows the top 10 financial institutions holding Cargill bonds. Most of the bondholders are based in the United States. None of the financial institutions have a deforestation policy or are signatories to the Statement of Support (SoS) for the Cerrado Manifesto, implying that a willingness to engage or divest is likely absent.

Figure 10: Cargill’s Bondholders

Source: Thomson Reuter Eikon (2019),”Bondholdings, at most recent filing date,” viewed in July 2019.

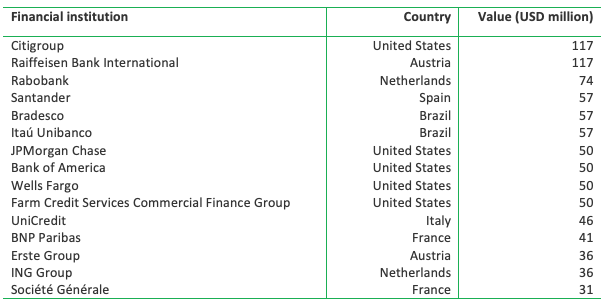

Cargill’s loan providers may develop leverage. It has outstanding loans that total USD 995 million. Figure 11 lists the top 15 banks providing loans to Cargill entities.

Figure 11: Cargills’s outstanding loans

Source: Thomson Reuters Eikon (2019), “Loans, Jan 2013 – July 2019,” viewed in July 2019; Bloomberg (2019), “Loans, Jan 2013 – July 2019,” viewed in July 2019.

Cargill also has revolving credit facilities totaling nearly USD 13.1 billion. The company will likely use only a small part. Figure 12 shows the top 15 contributors to the Cargill’s outstanding revolving facility.

Figure 12: Cargills’s available revolving credit facilities

Source: Thomson Reuters Eikon (2019), “Loans, Jan 2013 – July 2019,” viewed in July 2019; Bloomberg (2019), “Loans, Jan 2013 – July 2019,” viewed in July 2019.

Cargill may face higher cost of capital as its lenders may tighten their deforestation policies and move towards stricter compliance. The following banks provide loans or credit to Cargill but have adopted the Soft Commodities Compact: BNP Paribas, Barclays, Deutsche Bank, RBS, Santander, Standard Chartered, JP Morgan, Rabobank, and Société Générale. Furthermore, Barclays and Deutsche Bank have also endorsed the NYDF. Other financial institutions such as Citigroup, ING Group, Standard Chartered, RBS, Mitsubishi UFJ Financial, and HSBC have developed their own agriculture/forestry/palm oil sector policies.

CRR has indicated that a 0.5 percent increase in the cost of capital may lead to a negative 5-10 percent impact on the enterprise value. In case of a seven percent cost of capital, the impact is circa -10 percent. Cargill’s USD 9.2 billion gross debt may face USD 46 million of higher annual interest charges, which would result in a value (based on DCF) of USD 530 million.

Reputation risk might negatively impact Cargill’s EBITDA

Reputation risk as a result of failing to comply with deforestation targets could impact Cargill’s financials both directly and indirectly. CRR’s recent report on reputation risks related to deforestation highlighted that a listed company’s value could be materially affected by reputation events. This value risk could be partly related to revenue-at-risk and cost of capital risk (prices of bonds, loans and equity), but could also affect the quality of customer relationship, employee satisfaction, regulatory and legal costs, and consequently, quality of earnings. Cargill’s non-listed shares cannot be impacted by reputation risk. Reputation can make bondholders decide to engage or divest. This impact is already covered in the section on financing risks. The direct risk is covered in the section on revenue-at-risk.

FMCG, restaurant and food retail companies may fear reputation risks from their upstream supply chain related to sourcing from Cargill. This indirect effect might be material. Cargill might lose its status as a preferred supplier and a good employer. This effect would not only occur in its soy-related activities but also affect all other and global businesses of Cargill such as its food/protein business. Consumer boycotts of meat and dairy products may accelerate if these supply chains are not deforestation-free. In such a scenario, every one percent loss in its revenues or every one percent extra operational cost would lead to USD 64 million less EBITDA. The value of the lower EBITDA in a DCF calculation with a cost of capital of seven percent would lead to a value loss of USD 731 million for every one percent of opportunity loss in revenues or costs.

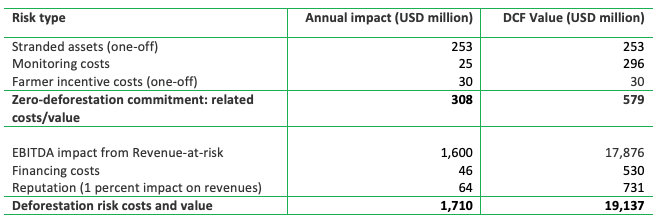

Risk summary: Value of deforestation risks outweighs adjustment measures’ value

The annual costs and the DCF value of costs related to zero-deforestation commitments are outweighed by the annual costs and the DCF value of continuing weak commitments to zero-deforestation. Figure 13 summarizes the various risks for Cargill.

Figure 13: Cargill: Summary of estimated financial impacts

Source: CRR