Glencore Agriculture is an agricultural commodity trading company that operates in corn, cotton, soy, and grains markets. Glencore Agriculture has been a stand-alone business since Glencore PLC divested in 2016. Its main shareholders are Glencore PLC (49.99 percent), the Canada Pension Plan Investment Board (CPPIB; 39.99 percent) and the British Columbia Investment Management Corporation (BCI; 9.99 percent). This report assesses Glencore Agriculture’s exposure to deforestation risks in Brazil’s soy supply chain.

Download the PDF: Glencore Agriculture Exposes Canadian Pension Funds to Deforestation Risks

Key Findings:

- Glencore Agriculture is among the largest soybean traders in 15 soy-producing municipalities in Brazil. A total of 41,190 hectares (ha) were deforested in these municipalities between January 1, 2018 and March 31, 2019. CRR concludes that Glencore Agriculture’s deforestation risk is very high in four municipalities in Mato Grosso, Tocantins and Piauí. The company has not adequately excluded sourcing from recently deforested properties.

- Glencore Agriculture has committed to zero-deforestation value chains, but its commitments are not in line with the core principles proposed by the Accountability Framework. Glencore Agriculture, as a member of the Soft Commodities Forum, published its first progress report in June 2019.

- Market position and owner policies make it unlikely that the company’s deforestation risks will translate into material business risks. Glencore Agriculture mainly services the Chinese market, where zero-deforestation market demands are limited. Shareholders CBIPP and BCI have adopted responsible investment policies, but do not identify deforestation as an ESG risk.

- Glencore Agriculture is highly leveraged with a Net Debt/EBITDA multiple of 9.4x, while the company’s EBITDA margins are shrinking. If its top-15 revolving credit facility providers tighten their policies, the company could face higher annual interest charges totaling USD 23 million. For its three shareholders, EBITDA-at-risk, reputation risk, and higher cost of debt could result in a 41 percent reduction in net profits and dividends.

Glencore Agriculture’s role grows in Brazilian soy market

Glencore Agriculture is an agricultural commodity trading company that sources, handles, markets, and processes a variety of commodities, including corn, cotton, soy, and grains. The company holds over 270 storage and handling facilities, 35 processing and refining facilities, and 23 port terminals worldwide. Active in agricultural commodity markets in Australia, Canada, Russia, Argentina and Brazil, Glencore Agriculture markets over 80 million metric tons of commodities per year.

Glencore Agriculture has been a stand-alone business since Glencore PLC divested in 2016. Its three shareholders are Glencore PLC (49.99 percent), the Canada Pension Plan Investment Board (CPPIB; 39.99 percent) and the British Columbia Investment Management Corporation (BCI; 9.99 percent). Its employee trust hold the remaining 0.03 percent of shares. The USD 3.1 billion sale was part of a larger “disposals programme” that Glencore PLC undertook to reduce its net debt position, valuing Glencore Agriculture at USD 6.2 billion at the time.

After the spin-off, Glencore Agriculture sought to expand its business through acquisitions or mergers. In May 2017, Glencore Agriculture confirmed it made an informal approach to take over Bunge Ltd. Whereas Glencore Agriculture and Bunge agreed to refrain from any take-over bids, no deal materialized. Overtures by Louis Dreyfus Commodities for a possible merger likewise did not occur. Financial media now reports that it is unlikely that the company will seek any large mergers or takeovers in the near future, due to the retirement of Glencore Agriculture’s CEO Chris Mahoney and uncertainty over the U.S.-China trade war.

Despite the lack of success in its acquisition strategy, Glencore Agriculture has increased its foothold in Brazil’s soy market through capital investments. For example, Glencore Agriculture is one of four companies that invested in the Tegram terminal in Itaqui in Maranhão. In 2015, it bought a 50 percent stake in the Barcarena grain export terminal in Pará. This terminal quadrupled its capacity in 2018.

Figure 1: Location of Glencore assets and sourcing municipalities

While Glencore Agriculture is not among the seven largest exporters of soybeans from Brazil, it is one of the biggest soybean traders in fifteen different soy-producing municipalities. The company has focused its soy export infrastructure in the northern parts of Brazil. This geographic location provides a competitive advantage for trade to China due to its closer proximity to the Panama Canal. The company’s asset locations also benefit from soy expansion into the northern parts of the Cerrado and Amazon biomes in recent years.

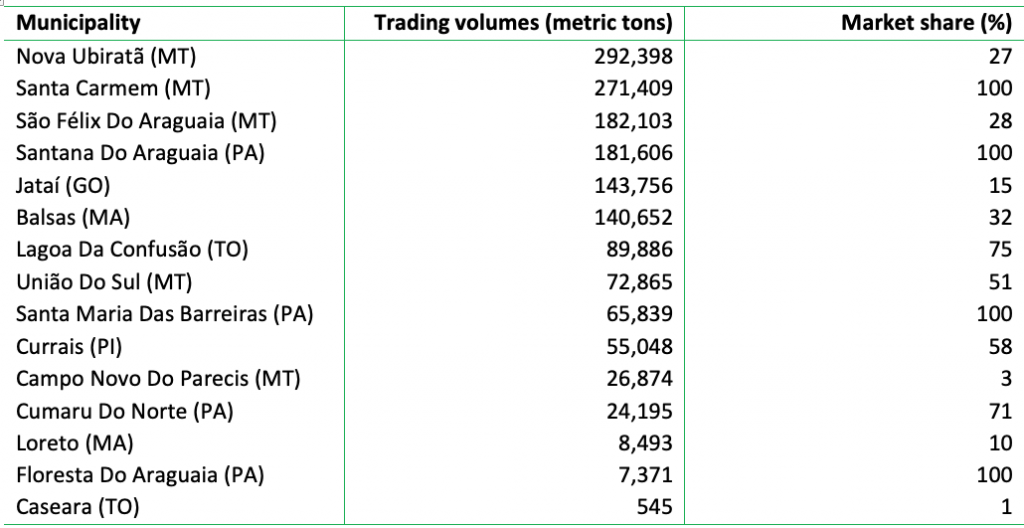

Glencore Agriculture operates four silos in the state of Mato Grosso (MT). It also sources from various municipalities in Para (PA) and Matopiba, Brazil’s newest soy frontier, consisting of the states of Maranhão (MA), Tocantins (TO), Piauí (PI), and Bahia (BA) (Figure 2). Glencore Agriculture does not own any storage assets in these municipalities.

Figure 2: Glencore’s trading volumes and market share in Brazilian municipalities (2017)

Glencore Agriculture’s zero-deforestation approach falls short of Accountability Framework principles

Glencore Agriculture has committed to work toward zero-deforestation value chains. On its website, the company states that it is “working collaboratively with producers and suppliers along our supply chains to eradicate deforestation, increase sustainability and protect high carbon stock forest, valuable conservation areas and peatlands from uncontrolled expansion.’’ The company is a member of the Roundtable for Responsible Soy (RTRS) and a participant in the Amazon Soy Moratorium.

Glencore Agriculture is also a member of the Soft Commodities Forum (SCF), a platform for agricultural companies convened by the World Business Council for Sustainable Development (WBCSD). The SCF identified 25 priority municipalities in the Cerrado for targeted interventions to address native vegetation conversion to soy. Within the context of the SCF, the company published its first progress report in June 2019, which specifies that Glencore Agriculture includes environmental criteria in its soy procurement decisions. The company has integrated a satellite system with data from the Green Grain Protocol in Pará, the Amazon Moratorium, IBAMA embargoed areas, and others into its origination processes. In the case of non-compliance with internal Glencore Agriculture policies, the company will automatically block payments to suppliers.

Glencore Agriculture’s commitment falls short of the core principles proposed by the Accountability Framework. The Accountability Framework is a set of common norms and guidance for establishing, implementing, and monitoring ethical supply chain commitments in agriculture and forestry. Glencore Agriculture’s approach does not:

- Prohibit conversion of non-forested natural ecosystems within its value chain (Core Principle 1.2)

- Specify the scope or describe verifiable actions or time-bound targets (Core Principle 3)

- Establish an effective company grievance mechanism (Core Principle 9.2)

- Report on annual progress, implementation actions and outcomes (Core Principle 12).

Publicly available information is too limited to properly assess whether Glencore adequately manages for supply chain compliance (Core Principle 6) or conducts adequate monitoring and verification (Core Principle 11).

Glencore Agriculture sources soybeans from areas with high deforestation risks

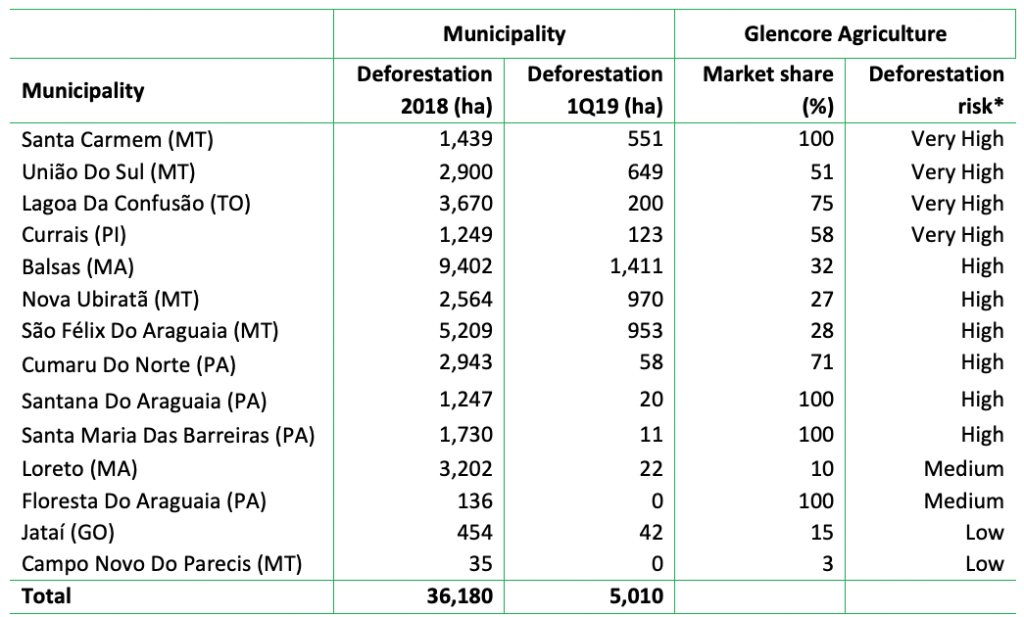

Between January 1, 2018 and March 31, 2019, a total of 41,190 ha were deforested in municipalities from which Glencore Agriculture sources (36,180 ha in FY18 and 5,010 ha in 1Q19). These figures include native vegetation loss in both the Cerrado and Amazon biomes (Figure 3).

Figure 3: Deforestation risk in municipalities from which Glencore Agriculture sources

*Deforestation risk profile determined on the basis of 1) market share >50%, 2) 2018 deforestation rates >1,000ha, 3) 2019 deforestation rates >100ha. Low risk = meeting 0 criteria; medium risk = 1 criterion; high risk = 2 criteria; very high risk = 3 criteria. Sources: Trase, INPE, Mapbiomas Alerta

CRR concludes that Glencore Agriculture’s deforestation risk is very high in the municipalities of Santa Carmem (MT), União do Sul (MT), Lagoa da Confusão (TO), and Currais (PI). In these municipalities, Glencore Agriculture has a market share above 50 percent. More than 1,000 ha of native vegetation were cleared in 2018, and another 100 ha in the first three months of 2019. Whereas other commodities may also drive deforestation in these regions, sourcing soy from these regions may require increased diligence.

It remains unclear whether Glencore Agriculture has engaged with the owners of deforested farms or worked to safeguard against sourcing from these properties. The municipalities of Lagoa da Confusão and Currais, both located in Matopiba, are included in the 25 priority municipalities of the SCF.

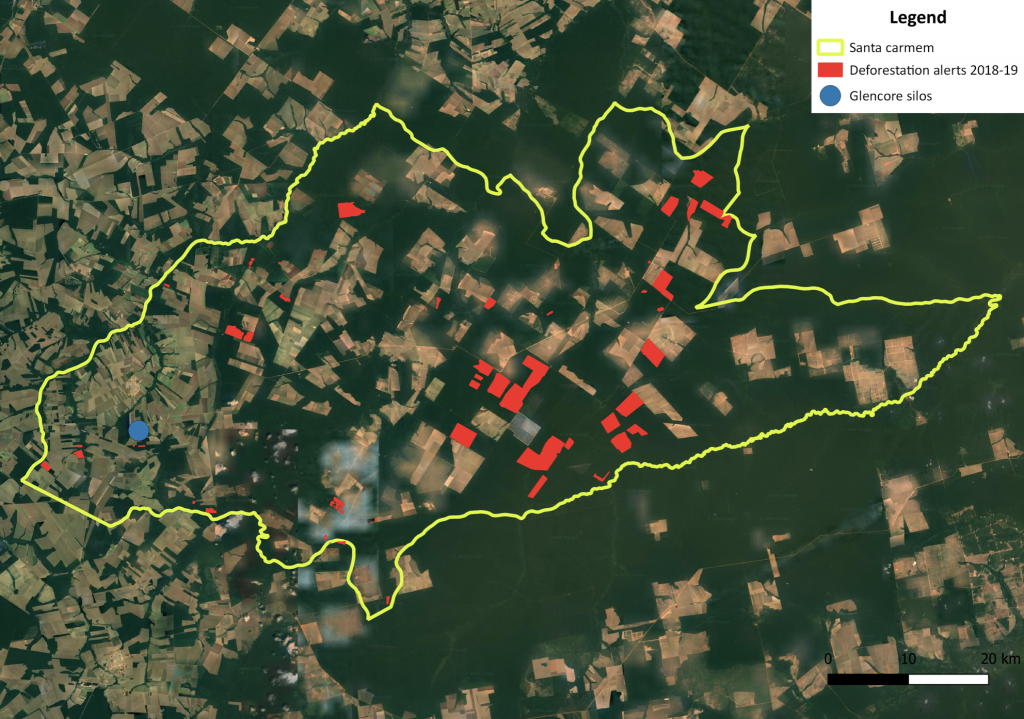

Santa Carmem (MT)

Glencore Agriculture operates a 34,000 metric ton silo in the western part of the municipality of Santa Carmem (MT), where soybeans have been cultivated for over a decade. Santa Carmem is located within the Amazon biome. Trade data suggests that Glencore Agriculture was the sole trader active in this municipality in 2017, with 271,409 metric tons traded. Santa Carmem saw approximately 15,000 ha deforested between 2012 and 2018. The deforestation in 2018 and 1Q19 mostly took place in the central and eastern parts of the municipality (Figure 4).

Figure 4: Deforestation alerts and Glencore assets in Santa Carmem (MT)

Sources: Deter, Conab

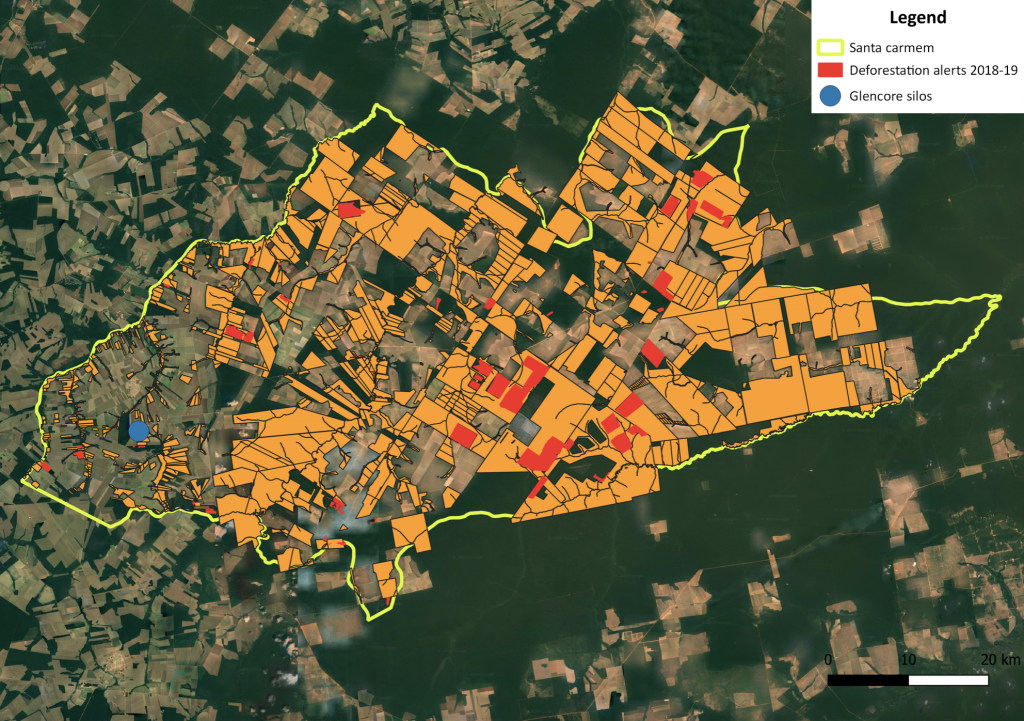

Sixty-four percent of all deforestation alerts from 2018 and 1Q19 overlapped with areas proposed or endorsed as legal reserves. Since Santa Carmem is located within the Amazon biome, Brazil’s Forest Code requires farmers to set aside 80 percent of their land as legal reserves (Figure 5).

Santa Carmem is also among the municipalities with the highest rates of soy production that is non-compliant with the Amazon Moratorium. The latest Amazon Moratorium monitoring report identified 18 polygons where soy was produced in the 2017/18 season and where deforestation occured between 2009-17.

Figure 5: 2018-19 deforestation alerts and legal reserves in Santa Carmem (MT)

Sources: Deter, Conab, CAR

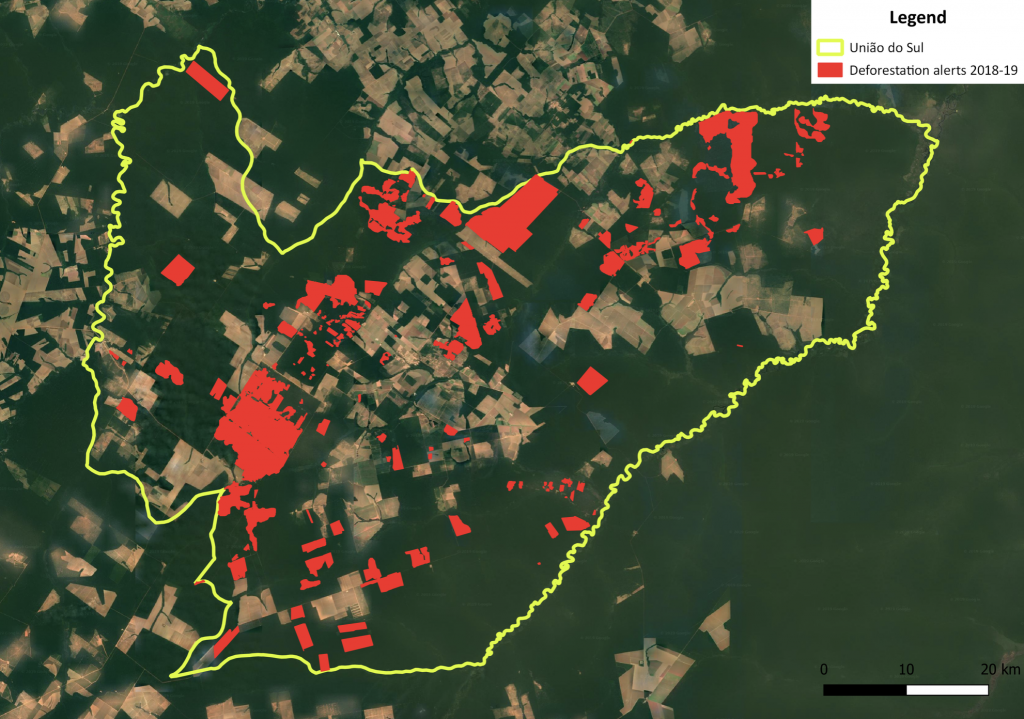

União do Sul

União do Sul, a municipality in Mato Grosso, saw 3,594 ha of deforestation in 2018 and 1Q19, on top of 15,896 ha between 2012 and 2017. Santa Carmem is located within the Amazon biome. Glencore Agriculture sourced 72,865 metric tons of soybeans from the municipality in 2017, and held a 51 percent market share. Glencore Agriculture does not have any assets located within União do Sul, but does have a silo in the adjacent municipality of Santa Carmem. Insurance records show that Glencore Agriculture also trades corn from farms in União do Sul.

Figure 6: Deforestation alerts in União do Sul (MT)

Sources: Deter

The majority of deforestation alerts (62 percent) overlapped with areas proposed or endorsed as Legal Reserves under Brazil’s Forest Code. Since União do Sul is located within the Amazon biome, Brazil’s Forest Code requires farmers to set aside 80 percent of their land as legal reserves.

União do Sul is also among the municipalities with the highest rates of soy production that is non-compliant with the Amazon Moratorium. The latest Amazon Moratorium monitoring report identified 18 polygons where soy was produced in the 2017/18 season and where deforestation occurred between 2009-17.

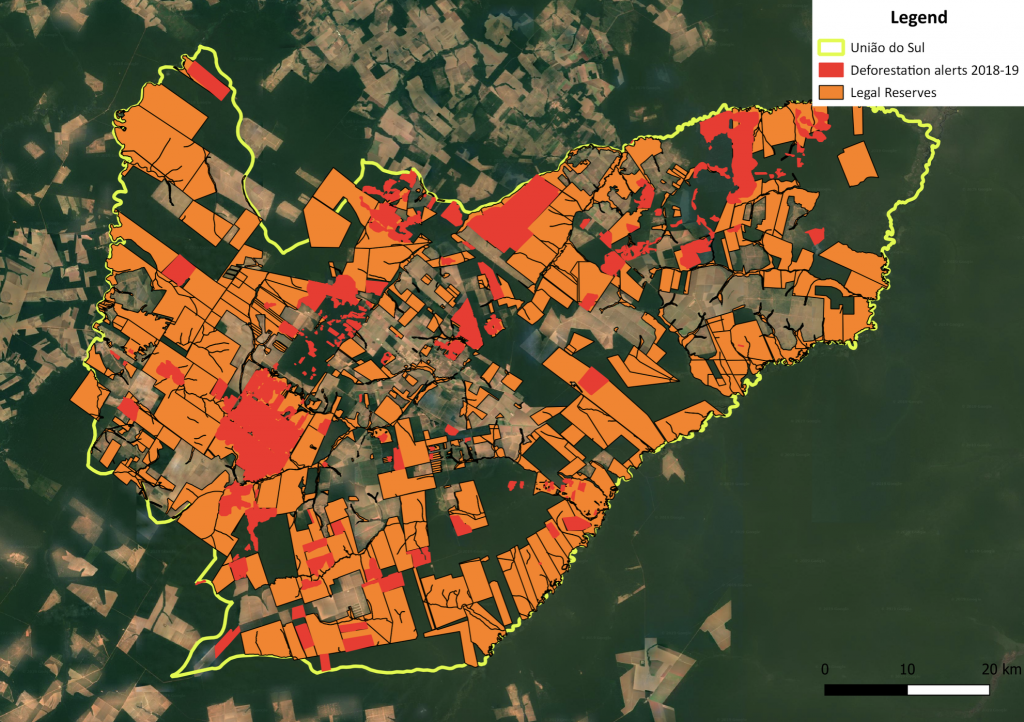

Figure 7: Deforestation alerts and legal reserves in União do Sul (MT)

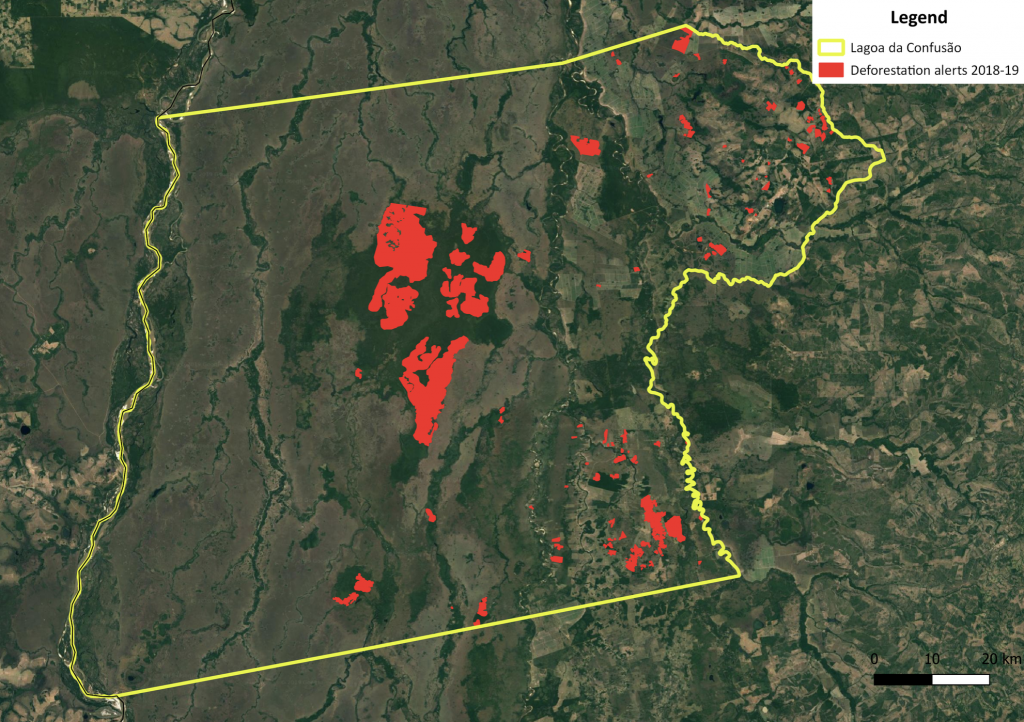

Lagoa da Confusão

Lagoa da Confusão, a main soy-producing municipality in Tocantins, was one of the areas most affected by deforestation in 2018. Lagoa da Confusão, located within the Cerrado biome, produced 121,432 metric tons of soy on 40,130 ha of land in 2017. A total of 3,670 ha were cleared in 2018. Soy and rice are the key agricultural crops grown in a rotational system. Soy producers and warehouses are highly concentrated in the northeast section of the municipality.

Glencore Agriculture is the largest exporter of soy from Lagoa da Confusão. The company accounted for 75 percent of total soy trade in the municipality in 2017.

Illegal and legal deforestation took place in Lagoa da Confusão in 2018. Forty-eight properties in the municipality, totaling 2,583 ha, are embargoed by IBAMA, the administrative arm of Brazil’s Ministry of Environment. Nearly half of these embargoes are linked to illegal deforestation in protected areas or in areas where authorization is pending. In addition, IBAMA fined nine companies and farm owners for deforestation in 2018, totaling nearly BRL 12 million (USD 3.08 million).

Figure 8: Deforestation alerts and Glencore assets in Lagoa da Confusão

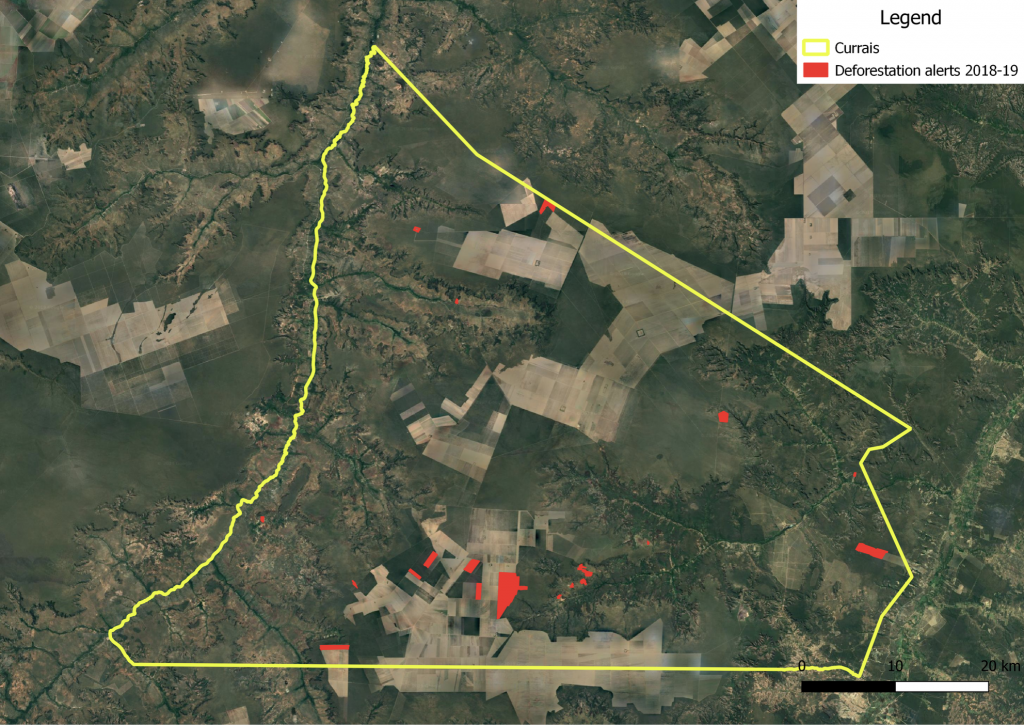

Currais

Currias is a municipality in the south of Piauí, within the area known as Matopiba. It is the sixth largest soy producer in the state of Piauí. Currais saw 1,372ha of deforestation in 2018 and 1Q19, mostly in the south-central part of the municipality where it borders the municipality of Bom Jésus.

Glencore Agriculture sourced 55,048 metric tons of soybeans in Currais in 2017, accounting for 58 percent market share. It does not own any silos or other assets within the municipality. Therefore, the company likely sourced these volumes indirectly through other traders. However, it is possible that Glencore Agriculture also sources soy directly at farm gates or from facilities owned by cooperatives. Nonetheless, Glencore indicated to CRR that it can prove the origin of the volumes it sources.

Figure 9: Deforestation alerts and Glencore assets in Currais (PI)

Sources: Deter

Glencore Agriculture’s deforestation-related business risks may be limited

Glencore Agriculture is exposed to significant risk of deforestation in its Brazilian soy supply chain, particularly in the four municipalities mentioned above. Within the geographies where the company is present, it may present a “leakage” market for deforestation-tainted soy. In several high-risk municipalities, Glencore Agriculture is the only SCF member that purchases soy. These municipalities have a relatively high number of instances of non-compliance with the Amazon Moratorium. Moreover, Cerrado municipalities in which the company operates have high native vegetation conversion rates. In the Cerrado, Glencore Agriculture’s indirect sourcing practices may further elevate its risk as deforestation may be less likely detected and addressed through the company’s zero-deforestation approach.

However, given its market position and owners’ policies, these risks are less likely to translate into material business risks because:

- Market access risks are limited

- Divestment risks are limited

- Legal risks may be adequately mitigated

Market access risks

CRR operationalizes market access risks as ‘‘violations of the responsible sourcing policies of a company’s clients.” However, limited information is available about Glencore Agriculture’s largest clients. Recent trade data suggests that other agricultural commodity traders account for approximately 15 percent of Glencore Agriculture’s client base for Brazilian soy.

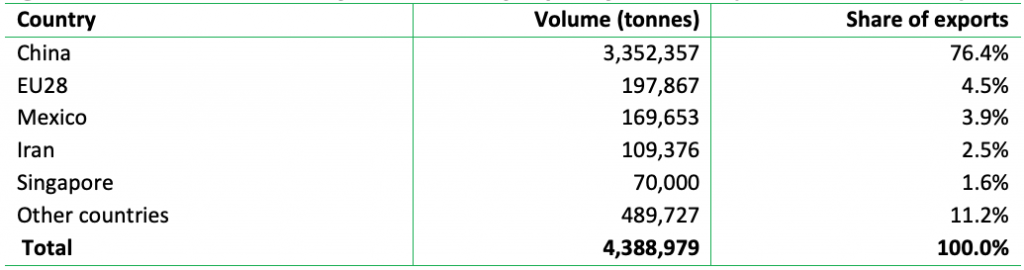

Using trade data as a proxy, Glencore Agriculture’s market access risk appears to be limited. Glencore Agriculture exports approximately 76 percent of its Brazilian soy to China, the largest consumer country of soy globally.

Figure 9: Destination countries for Glencore soy exports from Brazil (Jan 2018 – Mar 2019)*

*Not all Glencore shipments may be captured as for some exports shipper is unknown. Source: Panjiva (2019)

Whereas discussions on China’s role in addressing soy-related deforestation in Latin America are more frequent, there is not yet a clear market demand for zero-deforestation products in the country. The lack of clear standards and limited supply chain transparency may be obstacles to realizing zero-deforestation supply chains to China.

Divestment risks

Given its owners’ policies, divestment risks stemming from deforestation concerns are limited. Two of Glencore Agriculture’s shareholders have adopted responsible investment policies, but do not explicitly identify deforestation as an ESG risk.

CPPIB has identified climate change as one of the focus areas within its approach to sustainable investing. Whereas it does not explicitly mention deforestation in its most recent Sustainable Investment report, it may engage Glencore Agriculture on its deforestation risks in the future. However, financier risks are unlikely to materialize, as CPPIB’s policy states that it does “not screen stocks or eliminate investments based on ESG factors.”

BCI likewise identifies climate change as a priority, but does not make explicit mention of deforestation within that context. BCI has developed its own Climate Action Plan to implement the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD) and it applies a range of ESG indicators to inform its investment decisions and weightings.

The sustainability policies of Glencore Agriculture’s lenders and impacts on its cost of debt is discussed in the next section.

Legal risks

In the scenario that Glencore Agriculture is found to be sourcing soy from illegally deforested areas, it may be susceptible to IBAMA fines. In 2018, IBAMA fined Glencore Agriculture’s peers Cargill and Bunge for a combined USD 6.7 million for sourcing 3,000 metric tons of soy from areas illegally deforested and protected under Brazilian law.

This risk may increase, given that a significant share of deforestation in some of Glencore Agriculture’s sourcing municipalities has taken place on land proposed or endorsed as environmental reserves. However, Glencore Agriculture bases its environmental criteria for soy procurement on IBAMA maps of embargoed areas, among other criteria. It also conducts internal audits of its suppliers for Amazon Moratorium compliance. Glencore indicated to CRR that it has not found any violations in the last 12 years. Glencore may therefore be adequately mitigating this risk.

Financial Risk Analysis

The above-mentioned deforestation risks for Glencore Agriculture could impact the company’s financial performance in the coming years. This section provides an analysis on Glencore Agriculture’s most recent financial performance and estimated financial impact of deforestation risks manifesting at various levels.

Glencore Agriculture’s financial performance show declining margins

Glencore Agriculture’s EBITDA and EBIT margins have seen a decline since 2014 (Figure 10). After Glencore’s sale of its majority stake in Glencore Agriculture, the latter no longer provides details about its financial performance. However, Glencore Agriculture’s adjusted EBITDA shows a CAGR of – 20 percent from 2014 (USD 1.21 million) to 2018 (USD 484 million). The company said smaller crop sizes in Australia, Argentina and Brazil (sugarcane), hot weather in Europe, and the trade war between the US and China impacted volumes and undermined margins. These factors led to the 23 percent EBITDA reduction in 2018 from 2017 levels.

Figure 10: Key financial figures (as of December 31, 2018)

Source: Glencore plc (2015), Annual Report 2015, p. 171; Glencore plc (2017), Annual Report 2017, p. 79; Glencore (2018), Annual Report 2018, p. 54 and 91.

Glencore Agriculture’s Net debt/EBITDA ratio stands at a high 9.3x. At the end of 2018, Glencore Agriculture’s net debt stood at USD 4.48 billion of which USD 180 million cash, USD 2.67 billion long-term debt and USD 1.99 billion short-term debt. Most of the debt comes from revolving credits offered to the company by banks, and through bondholders. The company had almost no bank loans as of December 31, 2018. The net debt/EBITDA ratio stands at 9.3x, which means the company needs to generate 9.3 times EBITDA to pay off all its obligations.

Glencore Agriculture’s assets value in high risk municipalities is low

Glencore Agriculture’s assets in the high-risk municipalities are estimated to be of relatively small size. As a result, stranded asset risk is low. Glencore Agriculture’s soy exports to the EU total 198,000 tons, representing 0.25 percent of grains the company trades (80 million tons). Assuming the same percent for soy-based assets out of total property, plant and equipment value, approximately USD 11 million of assets could be exposed to stranded asset risk.

Glencore Agriculture has a low EBITDA-at-risk arising from deforestation risk

The company’s EBITDA-at-risk is estimated to be low at USD 1.2 million. Glencore Agriculture’s customers include food manufacturers, animal feed manufacturers, consumer product processors, local importers and distributors, and government purchasing entities. Out of its total soy exports, almost 76 percent goes to China. The major revenue risk comes from its customers in the EU which may have commitments to zero-deforestation. Since only 0.25 percent of its total grains business is soy exports to EU28, the estimated EBITDA-at-risk is just USD 1.2 million. In a Discounted Cash Flow (DCF) this is valued at USD 13 million.

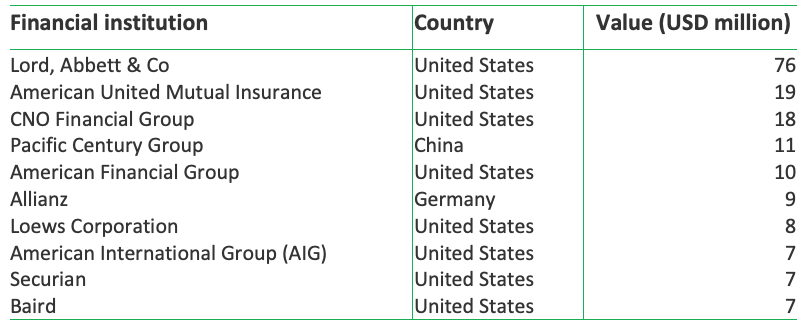

Glencore Agriculture faces high financing risk, as the banks form better deforestation policies

Glencore Agriculture’s bond investors lack deforestation commitments, so the risk of losing bondholders remains low. Glencore Agriculture’s total bonds stood at USD 216 million as of July 2019 (Figure 11). Most of the financial institutions noted in the top 10 bondholders are from the United States and do not have any deforestation-related commitment. Only the German insurer Allianz, which holds four percent of the bonds, has a policy to safeguard the loss of primary forests as a part of its ESG integration approach. Therefore, the company has a small risk of bondholders fleeing.

Figure 11: Glencore Agriculture’s Bondholders

Source: Thomson Reuters Eikon (2019), “Company transactions: Loans,” viewed in July 2019; Thomson Emaxx (2019), “Bondholdings of Viterra Inc, at most recent filing date,” viewed in July 2019; Glencore Agriculture BV, Annual Report 2018, p. 20; Glencore Plc, Annual Report 2018, p. 210-212.

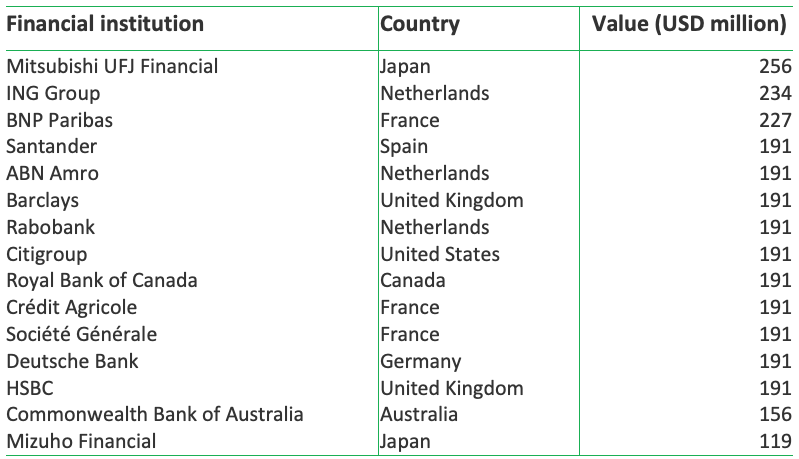

Financial Institutions providing revolving credit facilities to Glencore Agriculture may re-evaluate their relationship with the company, or engage, as they tighten their responsible lending policies. Glencore Agriculture does not have any loans outstanding. However, the company had outstanding revolving credit worth USD 3.97 billion as of July 2019. Figure 12 lists the top 15 financial institutions providing revolving credit facilities to the company. Most of the listed financial institutions have policies related to deforestation/agriculture/forest. As of now, their responsible lending policies may not be in conflict as a result of their financial links to Glencore Agriculture. However, this situation may change in the near future as the institutions further tighten their policies.

Figure 12: Glencore Agriculture’s available revolving credit facilities

Glencore Agriculture holds USD 4.6 billion in debt. Assuming that the cost of debt may rise by 50 basis points with EU banks increasingly linking their customers’ interest rates to sustainability outcomes, the company may face USD 23 million higher annual interest charges. This would result in a reduction in the enterprise value (based on DCF) of USD 257 million.

Reputational risk would further add to value loss

Glencore Agriculture’s reputational loss could mean USD 54 million in DCF for every 1 percent impact on revenues. CRR’s recent report on reputation risks related to deforestation highlighted that a listed company’s value could be materially affected by reputation events. This value risk could be partly related to revenue-at-risk and cost of capital risk (prices of bonds, loans and equity), but could also affect the quality of customer relationship, employee satisfaction, regulatory and legal costs, and consequently, quality of earnings. Every one percent of impact of erosion of reputation due to deforestation would affect the EBITDA by USD 4.8 million (DCF value USD 54 million).

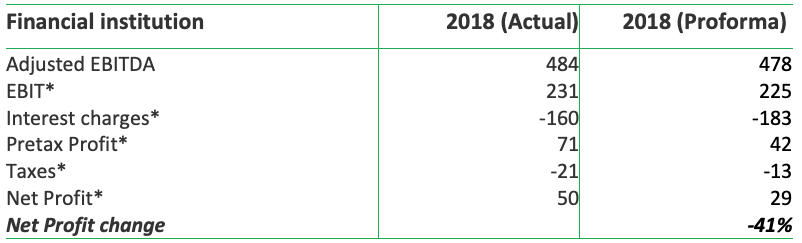

Risk summary: Pro forma net profit 2018 might have taken a 41 percent hit

Glencore Agriculture’s owners may get hit by pro forma net profit impact arising from deforestation- related risks. Taking the value of EBITDA-at-risk from EU soy customers and overall reputational risk impact on Glencore Agriculture’s EBITDA, the company may face material impacts on its net profit, with a decrease of 41 percent. The 41 percent decline is based on CRR assumptions on interest and tax rates. The 41 percent decline would impact dividends received by the three shareholders (see figure 13).

Figure 13: Glencore Agriculture’s deforestation risk proforma 2018 numbers (USD million)

Source: Chain Reaction Research (CRR); *CRR made assumptions on depreciation, amortization, interest rate and tax rate to calculate a net profit number