Download report here: Shadow Companies Present Palm Oil Investor Risks and Undermine NDPE Efforts

Since 2013, companies, governments, investors and civil society have taken steps to stop deforestation, fires, peatland development, and mitigate labor and human rights risks in the palm oil sector. These transformative actions include the adoption of No Deforestation, No Peat, No Exploitation (NDPE) sourcing policies, sustainable management policies, government moratoria, stop work orders, and supply chain transparency. Chain Reaction Research reports that 74 percent of SE Asia’s palm oil refining capacity is now covered by such NDPE policies. However, deforestation persists and unsustainable palm oil continues to be produced, traded and consumed. Ten companies out of a sample of 100 seem to be responsible for 75 percent of all palm-oil deforestation in Indonesia, Malaysia, and PNG in 2017, totaling 40,000 hectares. This paper explores how using related corporate entities and opaque ownership structures contribute to the ‘leakage’ of unsustainable palm oil to world markets.

Key Findings

- Deforestation often occurs at related-parties that belong to the same ultimate owners as NDPE committed entities. While not technically part of the same company, their mutual beneficial owners and directors link controversial assets to listed entities. Beneficial owners aim to keep deforestation out of sight instead of complying with NDPE policies across all their business activities. Widely used strategies include:

- Establish side businesses owned by majority owners and their families

- Sell assets to related-parties after grievances have been filed

- The beneficial ownership of controversial assets is often hidden as a strategy to address buyer NDPE policies without relinquishing control of a valuable asset. Companies and their majority owners:

- Own controversial assets through opaque and complex corporate structures

- Repeatedly transfer administrative ownership of controversial assets

- Actors that apply such strategies include Sawit Sumbermas Sarana, GAMA, Bintang Harapan Desa, and the Fangiono, Tee, and Salim family holdings. These actors have all deforested as recent as 2017, and all operate mills that feature on the list of suppliers of NDPE traders/refiners and consumer goods companies.

- If successful, these strategies could delegitimize the NDPE efforts of the palm oil traders/refiners that control 74 percent of the refining market and large consumer good companies. Continued sourcing relations expose NDPE traders/refiners and consumer goods companies to significant reputation damage as they will continue to be publicly associated with cases of deforestation.

- Listed plantation companies’ minority investors and financiers face reputation and market risks from related-parties’ controversies. When the beneficial ownership of a controversial asset becomes public, civil society and media exposure on deforestation can reflect on investors and financiers. When NDPE trader/refiners act on controversies at related-parties, investors and financiers are exposed to market risks.

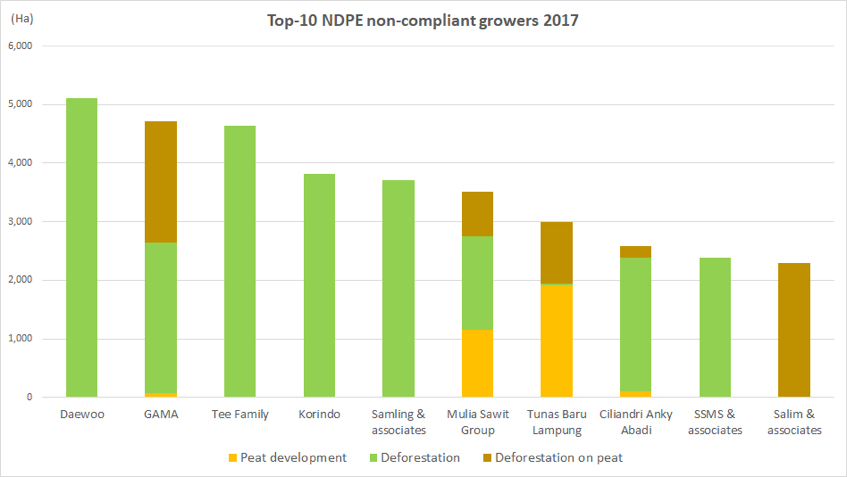

Ten Companies Caused 40 Thousand Hectares of Palm Oil-Related Deforestation in Indonesia, Malaysia and PNG in 2017

Despite ongoing efforts to achieve a deforestation free palm oil sector, forest and peatland clearing continues in SE Asia. Unsustainable palm oil continues to enter domestic and international supply chains. As shown in Figure 1 (below), Chain Reaction Research-partner Aidenvironment identified 10 company groups that are responsible for 40,000 ha of palm oil-related deforestation in Indonesia, Malaysia and PNG in 2017. This represents 75 percent of all identified deforestation of a sample of 100 companies.

| Figure 1: Top 10 NDPE non-compliant growers, 2017

Source: Aidenvironment, forthcoming |

This top 10 list includes several groups with complex and opaque ownership structures, where some but not all entities are incorporated in stock listed entities.

Deforestation Takes Place at Related-Parties to NDPE Committed Company Groups

Deforestation often occurs at concessions that belong to the same ultimate owners as NDPE committed company groups. While not legally part of the same company group, their mutual beneficial owners and officers link them to each other. These ultimate beneficial owners attempt to keep ongoing deforestation and the associated market access risks out of sight of buyers, investors and civil society rather than to comply with NDPE policies across all related business activities.

These controversial plantations belong to ‘related parties’ to the NDPE committed company groups. The International Accounting Standards define related parties as follows:

“A related party is a person or an entity that is related to the reporting entity: A person or a close member of that person’s family is related to a reporting entity if that person has control, joint control, or significant influence over the entity or is a member of its key management personnel.” In each of the cases presented in this report, deforestation has been identified at plantations that are under the control, significant influence or management of the same individuals or their direct families.

Ultimate Beneficial Ownership of Controversial Plantations Remains Hidden

Transparency on the ultimate beneficial ownership of companies – both publicly listed and privately-held – has long been a topic of interest for regulators, academics and civil society. The OECD concluded that ownership and control structures are often not adequately revealed in an accessible way, and that the definition of beneficial ownership is often too limited. Civil society organizations point to the risk that anonymous companies are used for crime, corruption, tax evasion and financing of terrorism.

On March 5, 2018, the Indonesian government enacted the Presidential Regulation No 13. This regulation aims to create transparency in the ownership of corporate entities, to monitor corporate control and to reduce opportunities to misuse such legal entities for illicit purposes, particularly money laundering and terrorism. It requires all legal entities in Indonesia to disclose information on their beneficial ownership to an ‘authorized agency’. Presidential regulation No 13 defines beneficial owners as “an individual who enjoys the power to appoint and remove the directors, commissioners, managers, trustees, or supervisors of a corporation, who has control over the corporation, who is entitled to receive, and /or actually receives, direct or indirect benefit from the corporation, who is the true owner of the assets or share capital of the corporation, and / or who satisfies the other criteria set out in this Presidential Regulation.”

This paper shows that anonymous companies are used to hide palm-oil-related deforestation and other unsustainable practices. Palm oil company groups hide beneficial ownership in controversial assets to comply with buyer NDPE policies without losing control of these controversial assets. These controversial assets are hidden through opaque ownership structures, public registration in the name of family members, or through the sale to related-parties. While the Presidential regulation only recognizes persons as beneficial owners, not companies, the regulation should, if applied correctly, increase transparency throughout the Indonesian palm oil sector.

GAMA, Sawit Sumbermas Sarana, the Salim Group, Bintang Harapan Desa, and the Tee family and the Fangiono family holdings are among the entities that apply a variety of different corporate structure strategies to disassociate controversial investments from listed company groups.

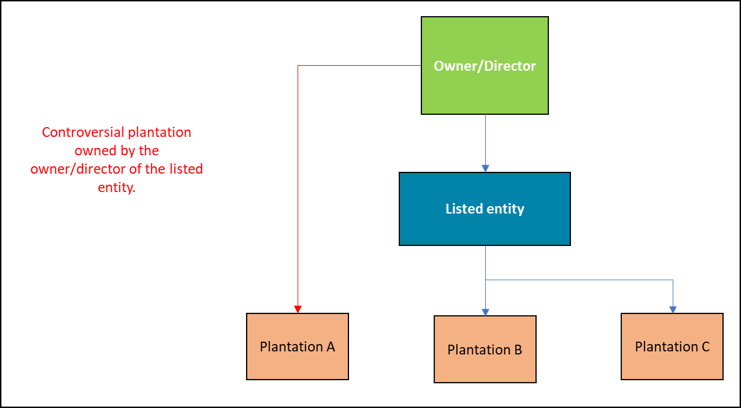

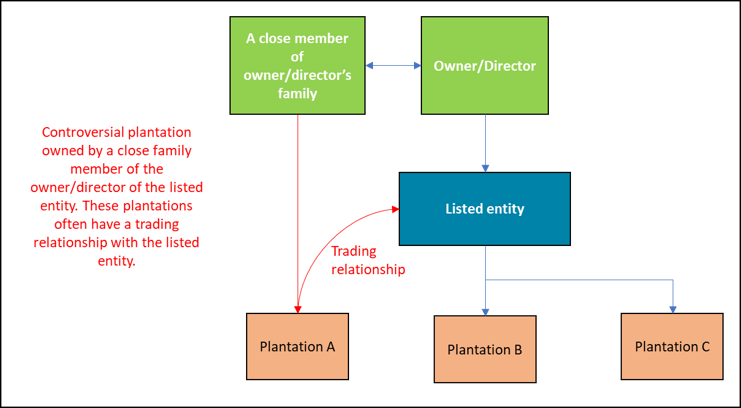

Strategy One: Side Businesses Owned by Investors and Their Families

As shown in Figures 2 and 3 (below), many tycoons with majority interests in Indonesian publicly-traded palm oil companies control a vast network of companies across many sectors. These individuals and their family members often control assets that are not incorporated in the listed entity. By structuring the controversial assets outside of the listed entity, scrutiny by NDPE buyers might be avoided.

| Figure 2: Controversial Assets Owned by the Owner/ Director of the Listed Entity

Source: Aidenvironment |

| Figure 3: Controversial Assets Owned by Family Members of Owner / Director of the Listed Entity

Source: Aidenvironment |

Case Study: Tee Family

For example, the Tee family have majority and minority ownership of groups of companies known as the Prosper Group. This includes the Bursa Malaysia-listed Far East Holdings Bhd. As shown in Figure 5 (below), the Tee family are the majority owners of four palm oil mills and the minority owners of another four mills. As shown in Figure 4 (below), these eight mills supply most large NDPE traders/refiners. These mills typically appear in supply lists as the ‘Prosper Group’, or a variation of ‘Prosper’.

Figure 4: Prosper Group — Commercial Relationships

| Prosper Group: Traders and consumer goods companies with Prosper Group mills in their direct or indirect supply chains | ||

| Wilmar | IOI | Musim Mas |

| Mewah | Bunge | Sime Darby |

| ADM | AAK | Cargill |

| Colgate Palmolive | PepsiCo | Reckitt Benckiser |

| General Mills | Mondelez | P&G |

| Nestle | Olam | Mars |

| Unilever | ||

Source: Aidenvironment

The Tee family also own and are directors of Bewani Oil Palm Plantation in Papua New Guinea. The Bewani project covers a Special Agricultural Business License, 139,909 ha in Vanimo, West Sepik province, near the border with West Papua. The diagram below illustrates the ownership structure of this entity.

| Figure 5: Tee family holdings corporate structure

Source: Aidenvironment |

The project has been accused of irregularities in the permit process, and of taking land without local people’s consent. In June 2013, the PNG Commission on Inquiry on SABLs recommended that the Bewani SABL should be revoked. In March 2017, Papua New Guinea’s Prime Minister repeated an earlier statement that all SABL’s previously issued have been declared illegal and operations should be stopped. In February 2018, Loop PNG and other local media stated that the Bewani Oil Palm Plantation license had been canceled, although this was contested in a recent article in The National newspaper. Since January 2014, 12,461 ha of forest has been cleared on the plantation, and the remaining 93,167 of forest ha is at risk of being deforested.

Deforestation at the Bewani Oil Palm Plantation, Papua New Guinea between August 2016 and May 2018

Case Study: Fangiono Family

Similarly, through various family trusts, the Fangiono family owns 70 percent of Singapore listed First Resources Ltd, and also controls PT Ciliandry Anky Abadi. First Resources holds 210,000 ha of palm oil plantations across Riau, East Kalimantan and West Kalimantan. As shown in Figure 6 (below), the company is committed to zero-deforestation at all its operations, and is a supplier to at least 20 traders/refiners and consumer goods companies with NDPE policies.

| Figure 6: First Resources / PT Ciliandry Anky Abadi — Commercial Relationships |

| First Resources / PT Ciliandry Anky Abadi: Traders and consumer goods companies they sell to | ||

| Wilmar | IOI | Musim Mas |

| Mars | Bunge | Sime Darby |

| ADM | AAK | Asian Agri |

| Golden Agri-Resources | Cargill | Reckitt Benckiser |

| General Mills | PepsiCo | P&G |

| Nestle | Olam | Colgate Palmolive |

| Unilever | ||

Source: Aidenvironment

PT Ciliandry Anky Abadi is a privately-held plantation company with a 120,000 ha landbank in Central Kalimantan. It is controlled by a British Virgin Island-registered entity that has ownership links to Martias Fangiono, the founder of First Resources. From August 2016 to January 2018, PT Ciliandry Anky Abadi deforested 4,005 ha of forest and peat.

Deforestation at PT Ciliandry Anky Abadi, Central Kalimantan between between February 2017 and May 2018

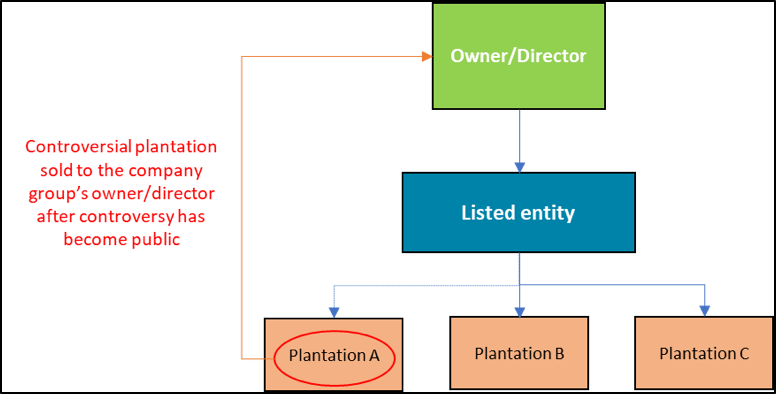

Strategy Two: Selling Controversial Assets to Related-Parties

Another method of hiding controversial assets is by selling them to related parties after grievances have been filed. In such cases, plantation companies aim to mitigate the risk of client suspension by separating themselves from the controversy after it has become public. The controversial assets are sold by the more publicly known and typically publicly traded company groups, but remain under direct control of these same publicly-traded entities’ directors or shareholders.

Figure 7 (below) illustrates this scenario, where the listed entity sells controversial Plantation A to its owner or director. This way, the listed entity is distanced of any controversial activities, yet the mutual owner of the listed entity and Plantation A maintains control or influence.

| Figure 7: Controversial Assets Sold After Public Controversy

|

Source: Aidenvironment

Case Study: Bintang Harapan Desa

For example, after Genting sold its 70 percent stake in the PT Permata Sawit Mandiri to its joint venture partner Bintang Harapan Desa, PT Permata Sawit Mandiri was subsequently sold to a Bintang Harapan Desa’ director. PT Permata Sawit Mandiri controls a 17,022 ha concession in West Kalimantan. 10,000 ha of this concession is High Carbon Stock forest and orangutan habitat. Genting, the previous owner of the concession, had concluded that it could not be fully developed and that is was therefore not economically viable. Bintang Harapan Desa purchased PT Permata Sawit Mandiri in January 2017. As shown in Figure 8 (below), it started deforestation of the High Carbon Stock forest in June 2017. From June to December 2017, 210 ha of High Carbon Stock forest was cleared on the concession.

| Figure 8: Drone footage of PT Permata Sawit Mandiri, West Kalimantan in November 2017

Source: Aidenvironment |

Several NDPE traders/refiners engaged the company during this time. In September 2017, Bintang Harapan Desa sold its shares in PT Permata Sawit Mandiri to PT Mulia Agro Investama and indicated to NDPE buyers that it was no longer associated with the concession. However, PT Mulia Agro Investama’s beneficial owner is Kurni Samsudin, a former director and current employee of Bintang Harapan Desa. Figures 9 and 10 below illustrate how the controversial asset remained a related party. Figure 11 (below) shows potential commercial relationships between Bintang Harapan Desa and NDPE buyers.

| Figure 9: PT Permata Sawit Mandiri Ownership Structure Prior to September 2017

Source: Aidenvironment |

| Figure 10: PT Permata Sawit Mandiri Ownership Structure After September 2017

Source: Aidenvironment |

Figure 11: Bintang Harapan Desa — Commercial Relationships

| Bintang Harapan Desa: Traders and consumer goods companies it sells to directly and indirectly | ||

| Wilmar | IOI Corporation | Colgate Palmolive |

| Nestlé | Olam | Mars |

| AAK | ADM | Asian Agri |

| Bunge | Cargill | PepsiCo |

| Reckitt Benckiser | Sime Darby | |

Source: Aidenvironment

Case Study: Sawit Sumbermas Sarana

Similarly, Sawit Sumbermas Sarana sold its subsidiary PT Sawit Mandiri Lestari in December 2015, after being subject to a RSPO complaint. The RSPO complaint, focused on allegations of a flawed High Conservation Value assessment and Free, Prior and Informed Consent process, was subsequently closed. The RSPO’s May 2016 closure letter stated:

“PT Sawit Mandiri Lestari is no longer owned or controlled by PT SSMS. Under such conditions, the RSPO Complaints System is not applicable to PT SML as a non-RSPO member.”

Deforestation at PT Sawit Mandiri Lestari, Central Kalimantan between January 2017 and April 2018

Notary acts from February 2016 showed that PT Sawit Mandiri Lestari remained registered at the address of Sawit Sumbermas Sarana’s headquarters and that its Commercial Director still remained at the helm of PT Sawit Mandiri Lestari after the sale. In September 2017, Haeruddin Tahir became the main director of PT Sawit Mandiri Lestari. This is likely the same Haeruddin Taher (surname spelt differently) who appears as Director of Plantation Development in Sawit Sumbermas Sarana’s 2015 annual report, indicating management links remain between the two companies.

In 2014 and 2015, Wilmar, Golden Agri-Resources, and Apical all suspended purchases of palm oil from Sawit Sumbermas Sarana because of violations of their NDPE purchasing policies. This represented a loss of 81 percent of the company’s client base. Despite the divestment of PT Sawit Mandiri Lestari, none of these buyers have re-established sourcing relationships. In June 2017, Unilever also suspended sourcing from Sawit Sumbermas Sarana. Figure 12 (below) shows potential commercial relationships between Sawit Sumbermas Sarana and NDPE buyers.

| Figure 12: Sawit Sumbermas Sarana — Commercial Relationships |

| Sawit Sumbermas Sarana: Traders and consumer goods companies its sells to directly and indirectly | ||

| ADM | Reckitt Benckiser | Cargill |

| Nestlé | Olam | Colgate Palmolive |

| Mars | PepsiCo | Bunge |

| IOI Corporation | ||

Source: Aidenvironment

Strategy Three: Opaque and Complex Corporate Structures

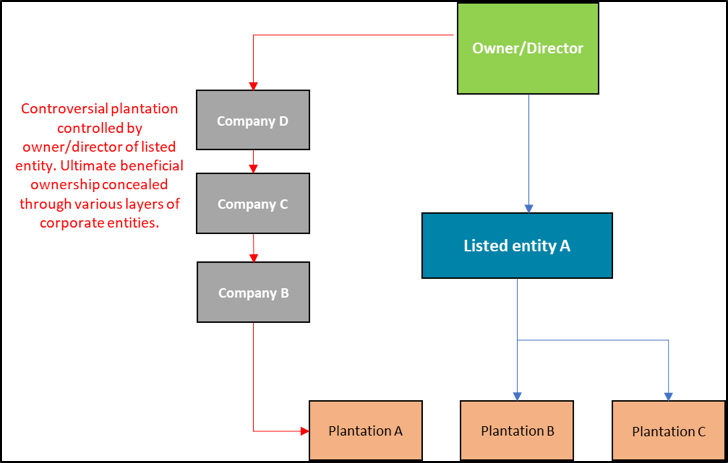

As shown in Figure 13 (below), a third and often complimentary strategy is to hide the beneficial ownership of controversial assets behind various layers of corporate entities and opaque ownership structures. This separates controversial assets from non-controversial business activities. It also complicates efforts to hold the beneficial owners accountable for violations of legal regulations or responsible sourcing policies.

| Figure 13: Controversial Asset Controlled by Owner / Director of Listed Entity

|

Source: Aidenvironment

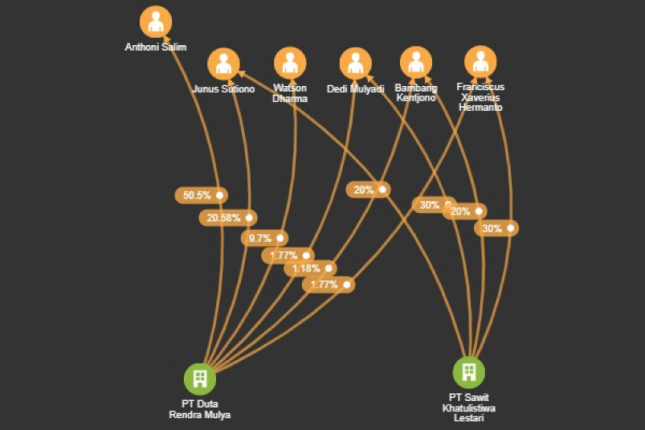

Case Study: Salim Group

According to Forbes, Anthoni Salim and his family are the fourth wealthiest in Indonesia. The Salim Group owns 45.0 percent of Hong Kong-listed First Pacific Company Ltd. First Pacific owns 50.1 percent in the IDX-listed Indofood Sukses Makmur. In turn, Indofood Sukses Makmur owns 74.3 percent in Indofood Agri, which is a vertically integrated palm oil producer with more than 300,000 ha of planted area, 26 CPO mills and 1.4 million MT refining capacity. Indofood Sukses Makmur has joint ventures with Nestlé and PepsiCo. First Pacific has a joint venture with Wilmar. All three JV partners have NDPE policies.

Anthoni Salim’s investments also include the oil palm companies PT Duta Rendra Mulya and PT Sawit Khatulistiwa Lestari. These two companies hold adjacent concessions totaling 19,595 ha in Ketungau, West Kalimantan. They are mostly located on forested peatland. From 2013 to 2017, 9,534 ha of peat forest was deforested at these concessions, which may be in violation of Indonesia’s peat regulation and the NDPE policies of palm oil trader/refiners. PT Sawit Khatulistiwa Lestari’s November 2017 deforestation is show in Figure 14 (below).

| Figure 14: Drone footage of PT Sawit Khatulistiwa Lestari, West Kalimantan in November 2017

Source: Aidenvironment |

Anthoni Salim’s control of these companies is opaque. Originally a forestry company, PT Duta Rendra Mulya changed its line of business to palm oil in 2013. Salim’s controlling ownership over PT Duta Rendra Mulya is concealed under several layers of corporate ownership. PT Sawit Khatulistiwa Lestari is related to Anthoni Salim through business associates. As illustrated in Figure 15 (below), four co-owners of PT Duta Rendra Mulya jointly own PT Sawit Khatulistiwa Lestari.

| Figure 15: PT Duta Rendra Mulya and PT Sawit Khatulistiwa Lestari Ownership Structure

Source: Aidenvironment, Government of Indonesia notary |

Strategy Four: Repeated Transfer of Administrative Ownership

Companies often add a layer of complexity by regularly changing the administrative control and ownership of corporate entities.

Case Study: GAMA Group

The GAMA Group – which stands for GAnda and MArtua – is a conglomerate of companies owned by members of the Sitorus family. The GAMA Group is also referred to as Ganda Sawit Utama, Ganda Group, or Agro Mandiri Semesta.

GAMA Group has an opaque structure of ownership, with shares in plantation companies held through multiple layers. Entities are owned by family members and are sometimes registered offshore. Changes in ownership and directorship appear to occur with some frequency.

The GAMA Group does not publicly reveal its landbank. It owns at least 25 plantation companies with a total landbank of over 400,000 ha. GAMA is one of the largest oil palm companies in Indonesia. While Andy Indigo (son of Ganda Sitorus), Clement Zichri and Felix Vincent Ang (nephews of Ganda Sitorus), and Jacqueline Sitorus (daughter of Martua Sitorus) are listed as shareholders in most of the GAMA Group’s oil palm companies, Ganda Sitorus and his brother Martua Sitorus are believed to be the ultimate beneficial owners.

This opaque ownership structure hides GAMA’s links to deforestation.

GAMA is linked to PT Agrinusa Persada Mulia and PT Agriprima Cipta Persada through PT Perkebunan Prima Manunggal, where Andy Indigo is a commissioner, and Papua-based PT Karya Agung Megah Utama (KAMU), which is controlled by Ganda (68 percent of shares) and Jacqueline Sitorus (32 percent of shares). PT Perkebunan Prima Manunggal owns 95 percent of PT Agrinusa Persada Mulia and PT Agriprima Cipta Persada, while PT Karya Agung Megah Utama has a minority stake. The Ministry of Forestry’s 2011 land cover maps show that 79 percent, or 36,000 ha, of the concession comprised primary and secondary forests. From February 2014 to April 2018, PT Agrinusa Persada Mulia and PT Agriprima Cipta Persada cleared 5,245 and 6,520 hectares of forest, respectively.

Similarly, Ganda Sawit Utama owned 95 percent of PT Graha Agro Nusantara until early 2017. After reports of clearing of a peat swamp forest and orangutan habitat in West Kalimantan, PT Graha Agro Nusantara’s ownership structure changed. Capital Ocean Ventures Ltd, a British Virgin Island-registered entity, now is the beneficial owner of PT Graha Agro Nusantara while Sitorus’ family members Clement Zichri Ang and Felix Vincent Ang own 5 percent of PT Graha Agro Nusantara.

Figure 16 (below) illustrates the complexity of GAMA Group’s corporate structure. Figure 17 (below) lists GAMA Group’s commercial relationships.

| Figure 16: GAMA Group’s corporate structure

Source: Aidenvironment |

Figure 17: GAMA Group — Commercial Relationships

| GAMA Group: Traders and consumer goods companies with GAMA mills in their supply chains | ||

| Wilmar | IOI Corporation | Sime Darby |

| ADM | Cargill | Nestlé |

| General Mills | PepsiCo | Unilever |

| Mars | AAK | Colgate Palmolive |

| Musim Mas | Olam | P&G |

| Reckitt Benckiser | ||

Source: Aidenvironment

Traders and Investors Face Reputation and Market Risks

Hiding or disassociating the beneficial ownership of controversial assets enables ongoing deforestation and the ‘leakage’ of unsustainable palm oil into consumer markets. This poses a risk to the effectiveness of NDPE policies and presents financial risks for minority investors.

Shadow Companies Delegitimize Trader’s NDPE Efforts

There can be legitimate reasons for beneficial owners to keep assets temporarily separate from listed entities with NDPE policies. For example, a newly acquired plantation that was poorly managed by the previous owners could negatively impact a listed entities’ sustainability certifications. The new owner may not want to sacrifice its sustainability certificates during the time required to resolve the plantation’s management issues.

However, prolonged separation and hidden ownership of controversial plantations poses the risk that growers continue to enjoy access to the NDPE market while actively deforesting at the same time. This may delegitimize the NDPE efforts of the palm oil traders/refiners that control 74 percent of the refining market, as well as of the large consumer goods companies.

The examples discussed in this paper signify the mixed success that growers have had in applying this strategy. Sawit Sumbermas Sarana and the Salim Group’s listed entities have experienced negative business impacts because of controversies in the privately-held related entities. Despite divesting PT SML to a related-party in 2016, Sawit Sumbermas Sarana has not regained access to the NDPE buyers that suspended it in 2015, and lost Unilever in 2017. In the case of the Salim Group, the deforestation at PT DRM and PT SKL were not the only issues that the group has been confronted with. Concerns over labor issues and deforestation has led PepsiCo to cut ties with Indofood Agri Resources, Citigroup to cancel all its loans to Indofood Agri Resources and its subsidiaries, and Nestle to take over the sourcing of palm oil for products manufactured under its joint venture with Indofood.

In other examples, company groups are successful in retaining access to the NDPE market, despite related-parties’ deforestation. The Tee family’s investment in the Bewani project in Papua New Guinea has not affected Prosper Group’s access to the 17 NDPE buyers it sells palm oil to. GAMA’s clearing of over 10,000 ha has also not impacted its access to the largest palm oil traders and consumer goods companies.

Should NDPE traders/refiners and consumer goods companies be unable to close this loophole in their responsible sourcing approaches, it could expose them to significant reputation damage as they continue to be publicly associated with cases of deforestation.

Investors and Financiers Face Reputation Risks

Hiding controversial assets poses financial risks for the minority shareholders and financiers of the listed entities. Exposure of beneficial ownership can result in reputational risks from negative media coverage and market risk due to NDPE non-compliance. These risks can reflect on all parties associated with the listed entity. Civil society and media exposure to deforestation and peat clearing can reflect on the financiers and minority shareholders of the listed entities.

In April 2018, Rabobank, Citibank, BNP Paribas and other banks faced public scrutiny over their ties with the Salim Group. Their loans were issued to Indofood and First Pacific, the listed entities affiliated with the Salim Group. Deforestation at the related-parties PT DRM and PT SKL have reflected back to them publicly. Many of the banks have made public zero-deforestation commitments, further increasing the potential reputational damage of this case. Some of the banks, including Citigroup, Standard Chartered and HSBC, recognized their responsibility to address matters at group level, even in cases where they lack a direct relationship to the problematic company. Meanwhile, BNP Paribas and Sumitomo Mitsui Financial Group, refused to acknowledge responsibility on the grounds that the controversial entities were not their direct clients.

Listed Plantation Companies Face Market Risks

When NDPE buyers act on controversies at related parties, listed plantation companies can face market risks. Suspension of trading relations can result in revenue impacts, declining share price, and increasing cost of capital.

Best practice NDPE policies define their scope to include ‘all third-party suppliers from whom we purchase or with whom we have a trading relationship.’ Whereas the wording of such policies leaves some room for interpretation, it can be read as applying to the ultimate beneficial owners of the companies from whom they source. This could result in situations where listed companies are suspended from supplying NDPE buyers because of NDPE non-compliance at related parties.

As mentioned above, there are a number of examples where controversies at related parties has triggered actions by companies with NDPE policies, or where the divestment to a related party has not resulted in regaining access to the NDPE market. This illustrates that due diligence processes should include both deforestation risks as well as assessments of related parties.

Disclaimer: This report reflects findings from an investigation led by AidEnvironment. While we believe the findings are accurate, including those about beneficial ownership and control, Chain Reaction Research and its member organizations are not at this time alleging any fraud, illegality or criminal activity by any company or party.