Archer Daniels Midland (ADM) is a large multinational trader and processor of agricultural commodities. In 2017, it generated USD 60.8 billion in revenue and USD 1.6 billion in net profit and employed over 31,000 people. ADM owns more than 30 silos in Brazil, as well 13 oilseeds processing plants. It also has operations in eight Brazilian ports. ADM sources a portion of its soybeans in the Cerrado, a vast biodiverse savannah region facing high rates of soy expansion and conversion of native vegetation. This could expose ADM to deforestation risks in its supply chain.

Download the PDF here: ADM — Matopiba Sourcing Could Link Company to Deforestation

- ADM is the fifth largest soy trader in Brazil’s Matopiba region, which is often referred to as the “last soy frontier.” In this region, agricultural expansion increased 253 percent in 2000-2014. Of this expansion, 62 to 68 percent occurred over native vegetation. Within Matopiba, ADM primarily sources from the Brazilian states Bahia and Tocantins, and to a lesser extent from Piauí and Maranhão.

- ADM’s “priority municipalities” in Matopiba saw 13,873 hectares (ha) of deforestation in 2017. The two priority municipalities that experienced the highest levels of deforestation in 2017 were Correntina (Bahia) and Brejinho de Nazaré(Tocantins). In Correntina, nine farms were responsible for 90 to 95 percent of all conversion of native vegetation in 2017. ADM has sourced from one of these farms.

- ADM has committed to a transparent, traceable soy supply chain that does not contribute to deforestation or exploitation. However, its commitment does not include a timeframe. In contrast to its policy for palm oil, ADM does not publish lists of soybean suppliers. ADM’s current efforts focus on traceability and the development of monitoring tools. It does not yet engage with or exclude soy suppliers because of deforestation concerns. As a result, ADM remains exposed to deforestation risks in its supply chain.

- Sourcing of deforestation-linked soybeans from Matopiba could expose ADM to reputational, market access, and financial risks. ADM’s exposure to the high-risk soy production area of Matopiba is limited to 1.5 percent of ADM’s total oilseed-related revenues. However, ADM’s sustainability approach does not mitigate all risks. Such sourcing practices could be contrary to ADM’s own policies, as well as the Cerrado Manifesto. Furthermore, ADM’s recent acquisition of Algar Agro assets, might link ADM to more soy-driven deforestation in Matopiba.

- Cerrado deforestation risks could impact up to 30 percent of ADM’s equity value. The value of assets and sales in ADM’s supply chain in Matopiba is equal to only 0.6 percent of the current market capitalization. More importantly, 18 percent of total net revenues is generated by customers which are signatories of the Cerrado Manifesto. These sales create a value of USD 6 billion for ADM, or 21 percent of its market capitalization. Additionally, continued deforestation might raise financing costs, adding up to a value loss equal to 30 percent of market cap.

ADM: One of Brazil’s Leading Traders

ADM is among the largest multinational traders and processors of agricultural commodities. The company was founded in 1923, when Archer-Daniels Linseed Company acquired Midland Linseed Products Company. It is headquartered in Chicago, Illinois. In 2017, it generated $60.8 billion of revenues and $1.6 billion in net profit, and employed over 31,000 people.

ADM has a vertically integrated business model. The company buys, stores, cleans, transports, crushes, and processes agricultural commodities. ADM operates 270 production facilities and 496 procurement facilities globally, with a total storage capacity of 20.8 million metric tons. ADM is also a large player in transportation. Globally, the company owns 1,800 barges, 12,300 rail cars, 290 trucks, 1,300 trailers, 100 boats, and 10 oceangoing vessels. The company holds a 24.9 percent ownership in Wilmar, Asia’s largest agribusiness group.

Among the Largest Soybean Processors in Brazil

ADM began operations in Brazil in 1997 and is now among the country’s largest processors of soybeans. It is also a top producer of bottled vegetable oils, and one of Brazil’s biggest overall exporters. ADM processes and sells soybeans, corn, and produces animal feeds, biofuels, chemicals and special ingredients for industry use. In Brazil, ADM employs over 3,300 people at processing plants, ports and grain elevators.

ADM owns more than 30 silos in the country as well as port terminals located in Barcarena (Pará), and in Santos (São Paulo). Furthermore, ADM owns 13 oilseeds processing plants. Of these plants, five are for crushing and origination and eight are for refining, packaging, biodiesel, and other purposes. The company is integrating further downstream, adding a portfolio of new products in the food and beverage industries. For instance, ADM markets the branded soybean oils Concórdia and Corcovado to Brazilian end consumers.

ADM purchases soybeans either directly from farmers (60 percent of procurement in Brazil between July 2017 and June 2018) or indirectly from third parties that market crops from many different growers (40 percent). The company sources most of its soy from the state of Mato Grosso, where it operates Brazil’s single largest soy crushing facility. This crusher is located in Rondonópolis and has a capacity of 2,555,000 metric tons per year. Forty-one percent of ADM’s procurement volume comes from indirect suppliers, such as third-party silos and brokers.

ADM reported a 140 percent growth in soy and corn exports from 2016 to 2017, reaching 8 million tons in 2017. The company completed investments in 2017 of 280 million Reais ($86 million) in the port of Santos, expanding its terminal capacity by 33 percent. ADM also quadrupled capacity at its northern Barcarena port, a joint venture with Glencore Plc, cutting the cost of shipping soy and corn.

Figure 1: Leading exporters of Brazilian soy, soymeal and corn

| Company | 2016 | 2017 | Change (%) |

| Bunge | 11.11 | 16.18 | 46 |

| Cargill | 8.76 | 12.16 | 39 |

| Marubeni | 9.38 | 10.01 | 7 |

| COFCO* | 2.17 | 9.30 | 329 |

| Louis Dreyfus | 6.00 | 8.45 | 41 |

| ADM | 3.33 | 8.02 | 141 |

* The increase in COFCO’s exports occurred in part as a result of its acquisition of Noble Agri and Nidera. Volumes in millions of tons. Source: Reuters

Through its SARTCO subsidiary, ADM also offers river transportation services on the Tietê-Paraná and Paraguay-Paraná waterways, and has port operations in Santos (São Paulo), Tubarão (Espírito Santo), Paranaguá (Paraná), São Francisco do Sul (Santa Catarina), Rio Grande (Rio Grande do Sul), Ponta da Madeira (Maranhão) and Aratu (Bahia), and the Barcarena joint venture with Glencore.

Figure 2: ADM’s warehouses and port facilities in Brazil

Source: ADM, Aidenvironment

Fifth Largest Trader in Matopiba

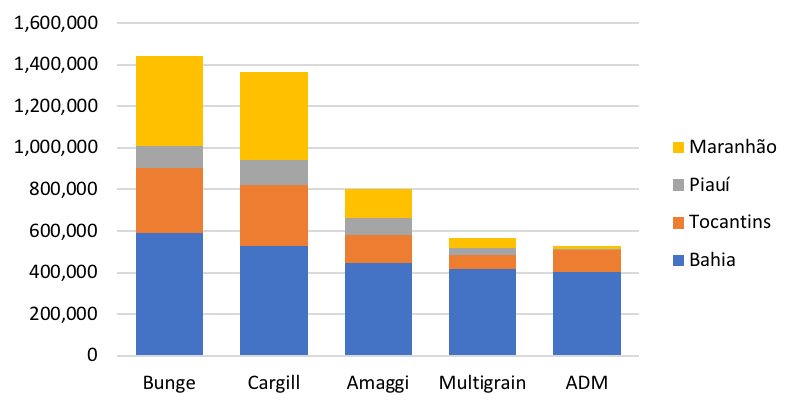

In 2015, ADM was the fifth largest trader in Brazil’s Matopiba region, after Bunge, Cargill, Amaggi, and Multigrain. In that year, ADM mainly sourced from Bahia (404,784 t). In comparison, in the same year, Cargill and Bunge sourced 589,866 t and 529,090 t from Bahian municipalities respectively. ADM sourced relatively low volumes from Piauí and Maranhão. In Piauí, ADM was the 10th largest trader in terms of volume of soy traded. In Maranhão, ADM was the 9th largest trader.

ADM told CRR that in Matopiba it sources 94.3 percent of its soybeans directly from farms.

Figure 3: ADM’s market position in the Matopiba region (Volume of soy traded in tons, 2015)

| Companies | Bahia | Tocantins | Piauí | Maranhão | Total |

| Bunge | 589,866 | 312,054 | 109,106 | 431,090 | 1,442,116 |

| Cargill | 529,090 | 293,326 | 119,162 | 422,479 | 1,364,057 |

| Amaggi | 446,232 | 135,488 | 83,045 | 139,600 | 804,365 |

| Multigrain | 417,848 | 65,535 | 33,358 | 48,557 | 565,298 |

| ADM | 404,784 | 102,011 | 4,697 | 16,803 | 528,295 |

| Agrex | 0 | 262,648 | 27,011 | 222,098 | 511,757 |

| ABC Indústria e Comércio | 0 | 141,362 | 0 | 321,268 | 462,630 |

| Nidera | 225,502 | 78,590 | 7,508 | 0 | 311,600 |

| CHS | 0 | 28,750 | 83,140 | 116,082 | 227,972 |

| Glencore | 0 | 4,130 | 21,590 | 111,896 | 137,616 |

| Fiagril | 0 | 135,943 | 0 | 0 | 135,943 |

| Risa | 0 | 0 | 53,849 | 11,271 | 65,120 |

| Louis Dreyfus | 1,952 | 0 | 0 | 0 | 1,952 |

Source: Trase

Figure 4: ADM’s market position in the Matopiba region (Volume of soy traded in tons, 2015)

Source: Trase

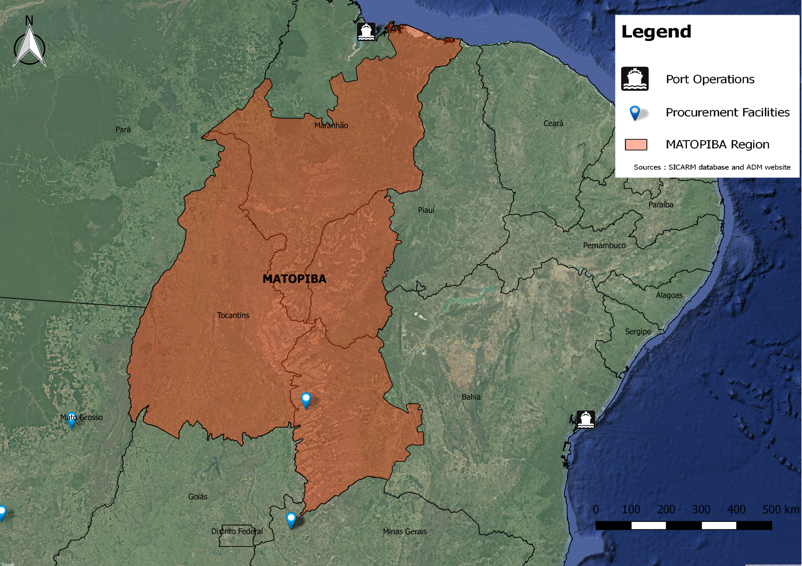

ADM has one warehouse in the Matopiba region, which is located in the municipality of Luís Eduardo Magalhães in Bahia (57,870 tons of capacity). This warehouse is relatively close to Bahia’s border with Tocantins (40 km), Piauí (180 km), and Maranhão (200 km). ADM’s nearest port operations are in Aratu, Bahia (over 800 km from the warehouse) and São Luís, Maranhão (over 1,000 km from the warehouse).

Figure 5: ADM’s warehouse in Bahia and its two port operations in the Northeast

Source: ADM, Aidenvironment

Figure 6 lists the Matopiba municipalities that ADM sourced most soy from in 2016. Of the six largest sourcing municipalities, four are in Bahia, while two are located in Tocantins.

Figure 6: Top 25 municipalities in the Matopiba region that supplied to ADM in 2016

| State | Municipality | Priority municipality for ADM | Estimated volume sold to ADM in 2016 (tons) |

| Bahia | São Desidério | Yes | 105,992 |

| Bahia | Barreiras | Yes | 65,690 |

| Tocantins | Monte do Carmo | Yes | 30,987 |

| Bahia | Luis Eduardo Magalhães | No | 24,255 |

| Bahia | Correntina | Yes | 22,610 |

| Tocantins | Palmas | No | 15,272 |

| Piauí | Corrente | No | 4,602 |

| Bahia | Riachão das Neves | Yes | 3,510 |

| Maranhão | Balsas | Yes | 1,753 |

| Maranhão | Tasso Fragoso | Yes | 1,232 |

| Piauí | Cristalândia do Piauí | No | 836 |

| Maranhão | Loreto | No | 345 |

| Maranhão | São Domingos do Azeitão | No | 300 |

| Maranhão | Sambaíba | No | 291 |

| Maranhão | Riachão | No | 245 |

| Maranhão | Carolina | No | 237 |

| Maranhão | Fortaleza dos Nogueiras | No | 200 |

| Maranhão | São Raimundo das Mangabeiras | No | 170 |

| Maranhão | Pastos Bons | No | 68 |

| Maranhão | Novas Colinas | No | 63 |

| Piauí | Sebastião Barros | No | 55 |

| Maranhão | São Félix de Balsas | No | 48 |

| Maranhão | Colinas | No | 30 |

| Maranhão | Benedito Leite | No | 20 |

| Maranhão | São João dos Patos | No | 15 |

Source: Trase

Deforestation Risks in Bahia and Tocantins

Soy production drives land conversion in the Matopiba region, which is often referred to as the “last soy frontier” in Brazil. From 2000 to 2014, soybean production in the Matopiba region increased from 1 million to 3.4 million ha, which represented a growth of 253 percent. According to a recent study by AgroSatélite, this figure stood at 4.0 million hectares in 2017, representing an average annual increase of 170 thousand hectares between 2014 and 2017 (2007-2014: 250 thousand hectares).

Most of the agricultural expansion in Matopiba occurred on newly deforested land: 68 percent (0.78 million ha) between 2000 and 2007 and 62 percent (1.3 million ha) between 2007 and 2014. Between 2014 and 2016, Matopiba saw a total of 1.7 million hectares of deforestation. To date, only 6.8 percent of that land has been converted to soy. The fact that the conversion process is a multi-year effort partially explains this development. AgroSatélite expects more soy to be grown on this recently deforested land in the coming years.

To improve the traceability of its supplies from the region, ADM has published a list of “Direct Soy Supplier Priority Municipalities.” The Forest Trust (TFT) defined these municipalities based on the following key indicators:

- The rate of conversion of native vegetation;

- The area of native vegetation cover;

- The area of soy cultivation; and

- ADM procurement.

In view of the scale of its soy supply base and the cost to collect farm maps, ADM decided to take a phased, risk-based approach to traceability. This prioritization aimed to focus ADM’s efforts on municipalities in the Matopiba region, where ADM has more leverage, and where a significant area of native vegetation is at risk.

ADM told CRR that the company believes its no-deforestation implementation effort has the most impact in areas where the company engages with a significant number of growers, as well as where significant areas of native vegetation remain and where soy expansion is a major driver of conversion. ADM also clustered priority municipalities to create regional focus areas for implementation and encourage conservation of adjacent areas.

According to ADM, TFT put together a database using ADM sourcing data as well as publicly available sources such as Global Forest Watch, Agroideal, Terraclass, Agrosatelite, and information provided directly by the Brazilian government. After TFT compiled the database, municipalities without soy cultivation or ADM sourcing were excluded. Then ADM conducted a multivariate cluster analysis based on rate of conversion of native vegetation and percentage of municipality covered by native vegetation. Municipalities were grouped into geographic clusters. They were then further refined to focus where ADM had a significant (>5) number of suppliers. ADM aims to focus traceability, mapping, and farmer engagement efforts in 15 initial municipalities.

Figure 7 lists ADM’s priority municipalities and the maximum deforestation calculated for these municipalities in 2017.

Figure 7: Maximum Deforestation in ADM’s Priority Municipalities

| State | Municipality | Maximum deforestation in 2017 (ha) |

| Bahia | Correntina | 4,170.22 |

| Tocantins | Brejinho De Nazaré | 1,150.21 |

| Bahia | São Desidério | 1,077.13 |

| Tocantins | Peixe | 1,034.48 |

| Tocantins | Porto Nacional | 1,011.52 |

| Maranhão | Grajaú | 994.52 |

| Maranhão | Balsas | 930.92 |

| Tocantins | Santa Rosa Do Tocantins | 718.36 |

| Maranhão | Tasso Fragoso | 608.96 |

| Bahia | Formosa Do Rio Preto | 594.6 |

| Tocantins | Monte Do Carmo | 592.78 |

| Bahia | Barreiras | 505.62 |

| Tocantins | Chapada Da Natividade | 215.1 |

| Bahia | Jaborandi | 212.21 |

| Bahia | Riachão Das Neves | 56.69 |

| Total | 13,873 |

Source: ADM, Aidenvironment

Some municipalities that have sold high volumes to ADM, such as Palmas, Corrente and Luis Eduardo Magalhães, were not included in the list of priority municipalities. The reason for this is that ADM believes there are fewer opportunities for conservation of significant areas of native vegetation in these municipalities.

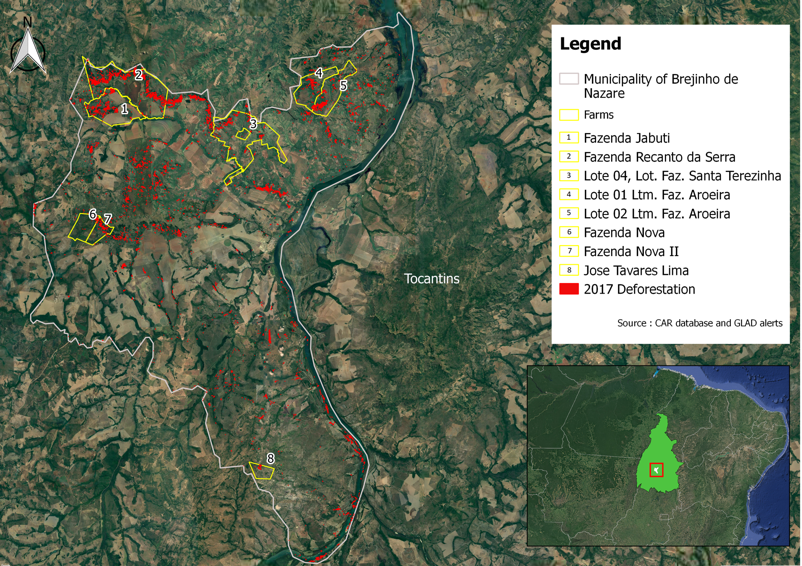

The two municipalities on ADM’s priority list that experienced the highest levels of deforestation in 2017 are Correntina in Bahia and Brejinho de Nazaré in Tocantins (see Figure 7).

Correntina

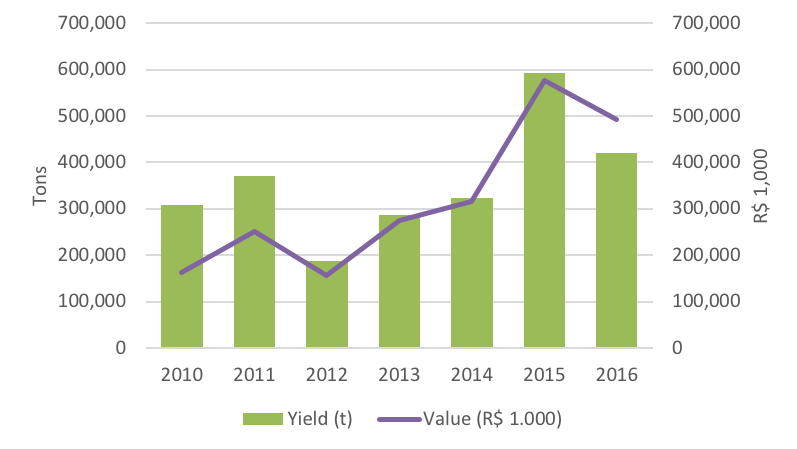

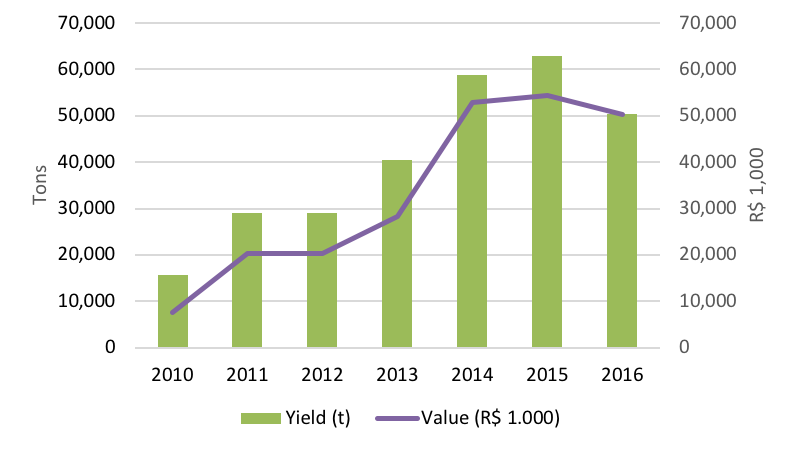

In 2015, Correntina produced 592,800 tons of soy, on a total of 190,000 ha of land. With 0.37 percent of the total production, it ranked 22nd in Brazil in soy production, and third in the state of Bahia. In 2015, the largest exporter of soy from Correntina was Multigrain S.A., which accounted for 42.1 percent of the total exports. The main export destination was China. In 2016, production dropped to 420,000 tons. In that year, the overall yield in Brazil declined due to a persistent drought. From 2010 to 2016, the area planted with soy in Correntina nearly doubled, rising from 101,000 to 200,000 ha.

Figure 9: Soybean Production in Correntina

Sources: Sistema de Informações Municipais, Governo do Estado da Bahia

GIS analysis indicates that the deforested area in Correntina was 4,170 ha in 2017. The Brazilian Ministry of Environment classified 99 percent of the native vegetation of this area as forest types. Ninety-one percent of the clearing took place on nine different farms (see Figure 9). One of these farms, Fazenda Chaparral, is owned by BrasilAgro, who listed ADM as one of its main clients in 2016-2017. ADM stopped sourcing from BrasilAgro after 2016, and is no longer listed as one of BrasilAgro’s main clients in its most recent financial accounts.

ADM states that one of the nine farms where most of the clearing took place in 2017 has a similar name to one of its suppliers. However, contrary to the Ministry of Environment data, ADM suggests that the converted land was not forested. According to the company, it did not source from the deforested areas of that farm. ADM has systems to monitor the polygons where actual deforestation takes place within a farm.

Figure 10: Deforestation on Native Vegetation in Correntina, 2017

Brejinho de Nazaré

In 2015, Brejinho De Nazaré produced 63,000 tons of soy on a total of 21,000 ha of land. With 0.04 percent of the total production, it ranked 348th in Brazil in soy production, and 10th in the state of Tocantins. Granol was the largest exporter of soy in Brejinho de Nazaré that year, accounting for 58.8 percent of the total exports. The main destination was the Netherlands. In 2016, yields fell to 50,296 tons. From 2010 to 2016, the area planted with soy nearly quadrupled from 5,600 ha to 21,500 ha.

Figure 11: Soybean Production in Brejinho de Nazaré

Source: Sistema IBGE de Recuperação Automática – SIDRA

GIS analysis indicates that the deforested area on native vegetation in Brejinho de Nazaré was 1,150 ha in 2017, of which 97 percent was classified as forest by the Brazilian Ministry of Environment. Thirty-nine percent of the clearing in Brejinho de Nazaré took place on eight different farms (see Figure 11). ADM told CRR that the company does not source from any of these farms.

Figure 12: Clearing of Native Vegetation in Brejinho de Nazaré, 2017

ADM Committed to Zero-Deforestation But Without a Timeline

ADM has committed to a transparent, traceable soy supply chain that does not contribute to deforestation or exploitation. Within its global palm oil and soybean supply chains, ADM has committed to the following four goals: (1) no deforestation, (2) no peat, (3) no exploitation, (4) traceability and transparency. ADM does not aim to exclude all forms of conversion.

According to ADM’s “sustainability progress tracker,” the company is doing the following in the soy sector:

- Determining the methodology for identifying regions of high risk to deforestation. The company also identifies areas at the farm level to set aside or conserve in order to comply with ADM’s commitments to no deforestation and no peat;

- Establishing its global footprint and baseline traceability scores for soy;

- Reviewing all direct suppliers based on the volumes they provide to ADM, the risks present in their region(s) of sourcing, and their own policies and action plans for ensuring goals are met within their supply chains;

- Creating an action plan for engagement with suppliers to achieve ADM’s commitment to no deforestation, based on supplier review;

- Monitoring progress on traceability and policy implementation, and producing public progress reports to allow for transparency of progress for concerned stakeholders; and

- Establishing a Grievance and Resolutions procedure for concerned parties to submit questions, complaints or comments about any supplier directly to ADM.

These activities are work in progress. ADM’s progress reports only provide aggregated transparency and traceability data.

Contrary to its policy for palm oil, ADM does not publish a list of soy suppliers. The company gives two reasons for not publishing the list of soy suppliers. Firstly, the company does not want to disclose the names and addresses of farmers, as these details would contain confidential and personal information. Secondly, publishing a list of direct soy suppliers undercuts ADM’s business and the competitive advantage the company might have.

Until the first half of 2018, ADM had a partnership with TFT, an organization that helped ADM identify direct suppliers and build traceable and transparent supply chains. In ADM’s last progress report, published in May 2018, ADM and TFT announced that they achieved 99 percent traceability to a municipality for soybeans procured directly from farmers. ADM and TFT were obtaining farm maps of ADM’s current direct soybean suppliers in the Matopiba region. According to the progress report, ADM and TFT conducted a pilot study addressing land use change in soybean growing areas within the Brazilian Cerrado biome, particularly focusing on Matopiba. Moreover, ADM and TFT wrote that they developed a public-facing “Issues and Resolutions Mechanism,” including a procedure outlining a clear process to resolve any issues that may emerge. The renamed Grievance and Resolutions Mechanism, which includes a log of grievances and resolutions, is available online.

CRR asked ADM how it guarantees that the soy it purchases does not come from recently deforested areas. ADM responded that it has worked toward traceability of its soy supply chain in South America for several years. The company is in the process of obtaining digital property maps to ensure ADM’s supply chain is not connected to deforestation. If ADM discovers that a supplier has deforested after 2015, the year in which ADM published its no-deforestation policy, it will engage with that farm to make sure it takes corrective action.

According to ADM, the next step in its no-deforestation approach is to engage with farmers who are involved in legal deforestation. Currently, ADM focuses on using tools to map suppliers, and its work to counter deforestation is still in its infancy, the company says.

ADM also said it is working with the Cerrado Working Group (CWG) and the Soft Commodities Forum (SCF) of the World Business Council for Sustainable Development for two main reasons. First, the company will determine how no-deforestation commitments should be applied to different geographies and types of vegetation. Second, it will create financial mechanisms that incentivize farmers to leave native vegetation (regardless of forest status) untouched.

Exposure to Deforestation Risks Can Result in Business Risks

CRR has covered ADM’s competitors Bunge and Cargill in separate company reports. In contrast to those companies, ADM’s exposure to the high-risk soy production area of Matopiba is relatively limited. Despite this limited exposure, ADM’s approach to deforestation does not mitigate all risks involved in sourcing soybeans from the Matopiba region. This exposure could result in several business risks.

Reputation Risk

In its no-deforestation policy, ADM states that it commits to building “a transparent, traceable soy supply chain that does not contribute to deforestation or exploitation.” In contrast to some of its competitors, ADM has not set a time commitment for deforestation-free supply chains. Bunge has committed to eliminating deforestation from its supply chain between 2020 and 2025. Cargill aims to halve deforestation across its entire agricultural supply chain by 2020 and end it completely by 2030.

ADM has a Responsible Soybean Standard, a certification program with the main objective of promoting environmentally and socially responsible soy production. The current standard, which is under revision and awaiting approval from the International Trade Center, only tackles illegal deforestation. As a result, ADM may still source from legally deforested areas. The revised standard, expected to be approved in September 2018, would not allow crops from “areas with legal deforestation or legal conversion of HCV native vegetation after March 2015 following the NoDPE Policy of ADM.”

As part of the Cerrado Working Group and the Soft Commodities Forum, ADM aims to identify incentives for farmers not to use permits to deforest legally. Such solutions could include financial incentives.

Although ADM is committed to making its supply chain more traceable and transparent, it does not publish lists of suppliers online. It is likely that ADM sources from farms in Bahia and Tocantins that deforested in 2017, via direct or indirect suppliers. Unless actively mitigated, such ongoing trading relations could be contrary to the spirit of ADM’s no-deforestation commitment, possibly undermining ADM’s reputation.

Market Risk

The Cerrado Manifesto, published by civil society groups and supported by 74 large companies, including likely clients of ADM, urges supply chain actors to strengthen the implementation of their zero-deforestation commitments. ADM’s relationships with these downstream companies may change if it does not adequately address sustainability impacts in its supply chains.

ADM does not support the Cerrado Manifesto. On March 29, 2018, an ADM spokesperson told Mongabay: “In the complex ecosystem and economic environment of the Cerrado, ADM believes that solutions to address deforestation and land use issues must be developed in consultation with, and buy-in from, all relevant stakeholders including local farmers, government, industry and civil society.”

The Cerrado Manifesto calls for immediate action from companies that purchase soy and meat from within the biome, as well as investors active in these sectors, in defense of the Cerrado. This mission includes the adoption of effective policies and commitments to eliminate deforestation and conversion of native vegetation and disassociate supply chains from recently converted areas.

Companies that support the Cerrado Manifesto, which may include some of ADM’s main clients, could call into question the effectiveness of ADM’s policies to halt deforestation and reconsider their trading relations with the company.

Financing Risk

Recently, a number of large institutional investors signed onto the Cerrado Manifesto. Signatories include APG, Robeco, Legal and General Investment Management, and Green Century Capital Management. These investors, with USD 2.8 trillion in assets, are increasingly recognizing soy-driven deforestation as a material financial risk for their investee companies.

In addition, the United Nations-supported Principles for Responsible Investment (PRI) and Ceres have recently expanded their collaborative investor engagement efforts to include dialogue with companies in the soy value chain. This initiative aims to support and coordinate engagements with companies to eliminate deforestation from their soybean supply chains within Latin America. Their working group members hold represent USD 6.3 trillion in assets under management.

While responsible investors are mostly engaging with their investee companies on these issues, they may divest their holdings if such engagement processes conclude unsatisfactorily, or if they see risks as too high. For example, the Norwegian Government Pension Fund divested from one Brazilian soy company in 2017 because of deforestation risks. Such developments could increase ADM’s financing costs.

Financial Risk Analysis

This section analyses the potential financial implications of the sustainability risks that are discussed above. Three important issues in this context are related to reputation risk, market risk and financing risk:

- The financial costs of a zero-deforestation supply chain would mitigate the reputation risk. The calculation of these costs will focus on ADM’s assets in the Matopiba region, which might not be utilized;

- The revenue-at-risk (or market risk) related to customers which have zero-deforestation commitments that cover the Matopiba region;

- The cost of capital risk. Who is financing ADM’s debt and equity? And how will non-compliance related to deforestation in the Matopiba region impact these relations and affect the weighted average cost of capital (WACC)?

Recent results

In the five years from 2013 to 2017, ADM’s net revenue steadily decreased with an average yearly rate of 7.5 percent from USD 89.8 billion (2013) to USD 60.8 billion (2017). This decrease was mainly the result of lower average sales prices. The lower sales prices stemmed mostly from lower underlying agricultural prices for commodities, particularly corn, soybeans and wheat. From 2013 to 2017, ADM’s profitability also decreased, with EBITDA moving down to USD 2.5 billion in 2017 (-4.2 percent CAGR) and net profit staying at USD 1.4 billion (0.0 percent CAGR). Fewer merchandising opportunities in 2015 partially led to the strong decline, while lower margins due to ample global supplies of grain and weaker industry ethanol margins also contributed to the drop.

In 2017, net revenues decreased slightly versus 2016, while EBITDA remained stable and free cash flow generation improved strongly. For 2018, net revenues are expected to rise to USD 64.9 billion and profitability is also expected to increase (Bloomberg consensus). The expected rise in profitability is partially the result of supply disruptions in Argentina and Brazil that led to strong global demand for U.S. commodities. That led to significantly higher volumes and margins for corn, wheat, and soybean exports. Also, high oilseed crush volumes amid continued strong soybean meal demand and robust crush margins are likely to contribute to the expected profitability rise. In South America, high origination volumes and improved margins, largely driven by more aggressive farmer selling and steady demand from China, will also contribute to this expected profitability increase.

Figure 13: Key figures of ADM (Fiscal years end December)

| USD billion | 2013 | 2014 | 2015 | 2016 | 2017 | 2018E | CAGR 2013-17 |

| Net revenues | 89.8 | 81.2 | 67.7 | 62.3 | 60.8 | 64.9 | -7.5% |

| Gross profit | 3.9 | 4.8 | 4.0 | 3.6 | 3.5 | 3.8 | -2.1% |

| EBITDA | 3.1 | 4.0 | 2.4 | 2.5 | 2.5 | 3.4 | -4.2% |

| Operating income | 2.2 | 3.1 | 1.5 | 1.6 | 1.5 | 2.2 | -7.4% |

| Net profit | 1.4 | 2.4 | 1.6 | 1.3 | 1.4 | 1.9 | 0.0% |

| Capital expenditures | -0.9 | -0.9 | -1.1 | -0.9 | -1.0 | -0.8 | 2.1% |

| Free cash flow after capex | 4.3 | 4.0 | 0.6 | 0.7 | 1.2 | 0.1 | -22.5% |

| EPS (USD) | 2.14 | 3.66 | 2.61 | 2.13 | 2.43 | 3.38 | 2.6% |

| EBITDA margin | 3.5% | 4.9% | 3.5% | 4.0% | 4.1% | 5.2% |

Sources: Bloomberg, Chain Reaction Research

Since January 2018, ADM changed its segment reporting to reflect changes in its operating structure:

- Agricultural Services (now Origination);

- Oilseeds Processing (now Oilseeds);

- Corn Processing (now Carbohydrate Solutions);

- Wild Flavors and Specialty Ingredients (now Nutrition).

The European origination business previously reported in Oilseeds has since January 2018 been reported in Origination. Carbohydrate Solutions now includes ADM Milling which was previously reported in Origination. Nutrition now includes Animal Nutrition and certain product lines previously reported in Carbohydrate Solutions, as well as certain product lines previously reported in Oilseeds. The paragraphs below will analyze the importance of each segment for the net revenues and operating income. For this analysis, FY2017 is used. Using half-year figures would likely provide an inaccurate due to seasonal fluctuations.

In the financial year ending December 2017, 43 percent of net revenues came from its agricultural services segment. This segment utilizes ADM’s global grain elevator and transportation networks and port operations to buy, store, clean, and transport agricultural commodities such as oilseeds, corn, wheat, milo, oats, rice, and barley. It resells these commodities primarily as food and feed ingredients and as raw materials for the agricultural processing industry. The other important segment that generated 37 percent of the net revenues was the oilseeds processing segment. Oilseeds encompasses global activities related to the origination, merchandising, crushing, and further processing of oilseeds such as soybeans, cottonseed, sunflower seed, canola, rapeseed, and flaxseed into vegetable oils and protein meals. Finally, 15 percent of Soybeans (17 percent), soybean meal (13 percent) and corn (10 percent) are the specific products that accounted for 10 percent or more of the net revenues. The sustainability risks discussed in the section above mainly exist within the agricultural services and oilseeds processing segments.

The corn processing segment accounted for 36 percent of total operating income. The oilseeds processing segment was the other important profit generator, accounting for 33 percent. Agricultural services made up 23 percent, with wild flavors and specialty ingredients at 11 percent.

Strategy focused on further South American oilseed opportunities

ADM’s strategy consists of three parts:

- Enhancing its core business;

- Improving efficiency and reducing costs;

- Growing its value-added product portfolio.

The company introduced the third part of the strategy a couple of years ago. This part tries to anticipate demographic changes and preferences. It involves growing the nutrition segment, which sells specialty products including natural flavor ingredients, flavor systems, natural colors, animal nutrition products and other specialty food and feed ingredients. As outlined in the report on Cargill, this strategy is in line with other traders making up the ABCD group and tries to anticipate the reduced importance of ADM’s traditional trading activities.

However, ADM’s failed takeover attempt of Bunge could indicate that it seeks other ways to offset years of disappointing trading results. The chance to expand oilseed operations in Brazil, the world’s biggest soy exporter, could be valuable to ADM. More focus by ADM on oilseeds could pay off as that market grows over time — presenting a simpler path to improved returns than a lengthy strategic overhaul. Analysts believe that the most bullish longer-term theme in the agribusiness sector is global vegetable protein demand. ADM’s recent acquisition of certain assets from Brazilian-based Algar Agro, including oilseeds processing facilities in Uberlândia in the state of Minas Gerais, and Porto Franco in Maranhão, shows that ADM is indeed looking to expand its Brazilian oilseed capabilities. The acquisition deal still requires Brazilian regulatory approval but is expected to close by the end of 2018.

Financial risk of potential stranded assets is insignificant

The sustainability analysis presented above shows that ADM currently has 290 oilseed facilities worldwide, with at least 43 facilities located in Brazil. It has one warehouse in the Matopiba region, which is located in the municipality of Luís Eduardo Magalhães in Bahia.

At the end of December 2017, ADM’s total assets related to the oilseed processing segment were valued at USD 11.9 billion, i.e. 30 percent of the total assets. This includes both current and non-current assets. When looking at the book value of property, plant and equipment, some USD 3.4 billion (of the total USD 10.1 billion) is situated outside the United States. A more detailed geographical break down of these assets is not provided by ADM. Based on the overall asset percentage for the oilseed processing segment, estimates suggest that USD 1.0 billion of the property, plant and equipment is used within the oilseed processing segment. Since ADM has only one warehouse in the Matopiba region of in total 290 oilseed facilities, this warehouse represents an estimated value of USD 3.4 million. Therefore, even in case ADM wants to mitigate its deforestation-related risks by writing down this complete facility, the write-downs will have a negligible impact on ADM’s net asset value and share price. Of course, ADM can also mitigate its deforestation-related risks while continuing its operations in the Matopiba region. The complete write-down scenario likely indicates the maximum costs that ADM could face.

ADM traded 528,295 tons of soy in the Matopiba region (2015 figure, see sustainability analysis above). In 2017, it processed 34.7 million of oilseeds in total. Matopiba accounts for roughly 1.5 percent of the total oilseed related revenues. Total net revenues from ADM’s oilseed processing segment were USD 22.5 billion in 2017, with 1.5 percent corresponding to USD 0.3 billion of net revenues from the Matopiba region. This segment makes up 0.6 percent of ADM’s 2017 global net revenues and profits. Assuming the gross margin stays at 5.8 percent, which is the average gross margin over the last four years, the impact on gross profit and EBITDA would be USD 17.4 million. This EBITDA number adds up to USD 174 million in a discounted cash flow model, which equals 0.6 percent of the current market capitalization. Of course, not all of the revenues generated from the Matopiba region will necessarily take a hit if ADM decides to stop sourcing from this region. The gap might be filled by sourcing from another region, but will take some time.

The analysis above indicates that the potential loss of stranded assets and a decrease of net revenues related to the Matopiba region do not pose a significant risk to ADM and its investors. Instead, the situation offers opportunities for ADM to fully adhere to its deforestation commitment without experiencing a substantial impact from noncurrent asset impairments and net revenue declines.

Market-access risk related to sourcing from Matopiba region is severe

As mentioned above in the sustainability risk analysis, ADM’s sustainability approach does not effectively address all risks involved in sourcing soybeans from the Matopiba region. Unless ADM can effectively mitigate these risks, such sourcing practices could be contrary to ADM’s own policies, as well as the Cerrado Manifesto. ADM’s increased interest in the Brazilian soy market, highlighted by its recent acquisition of certain assets from Algar Agro (see above), might cause additional issues. As part of the acquisition deal, ADM will work more closely with Algar Agro and will use Algar’s network of origination and storage silos. Algar Agro’s efforts to tackle deforestation lag behind those of ADM, and the majority of the soy which Algar Agro exported from the Cerrado in 2015 was sourced from the Matopiba region. That suggests that soy traded by Algar Agro is likely linked to areas of soy-driven deforestation.

ADM does not publicly disclose its customer base. Based upon the information presented in its annual and quarterly reports and information on the customers of its competitors Bunge and Cargill presented in earlier CRR reports, the largest animal feed and food manufacturers in the world are the main customers of ADM. As for its reliance on only certain customers, ADM states that “no material part of the company’s business is dependent upon a single customer or very few customers.”

It is likely that several of the Cerrado Manifesto signatories have purchasing relationships with ADM, either directly or indirectly. These signatories might represent 7 to 17.5 percent of ADM’s net revenues. The breakdown translates into:

- USD 4.3 to 10.6 billion revenue-at-risk, taking the FY2017 as the base revenue;

- USD 0.2 to 0.6 billion loss of gross profit and impact on EBITDA, assuming the gross margin stays at 5.8 percent, which is the average gross margin over the last four years;

- USD 2 to 6 billion in a discounted cash flow calculation, which equals 7 to 17.1 percent of Bunge’s current Enterprise Value (Figure 2) and 7.1 to 21.2 percent of its market capitalization (Figure 2).

Compared to the impact of potentially stranded assets, the loss of purchasing relationships poses much more financial risk to ADM. Therefore, it is likely that ADM will mitigate its deforestation related reputation and market risks.

Financiers have engagement opportunities. Cost of capital might increase

Figure 14 shows financial indicators of ADM related to the division of financing. As can be seen, ADM’s net debt amounted to USD 6.7 billion at the end of June 2018 and was on a similar level as end of 2017. Since 2013, net debt has steadily increased, and end of June 2018 reached a value that is 2.4 larger as end of 2013. As a result, the net debt/EBITDA ratio also increased during that period, to reach 2.4X at the end of June 2018, which is quite high for a company like ADM. Figure 14 also shows that the total assets of ADM are for almost 50 percent financed by its equity, while gross debt accounts for almost 20 percent. Issued bonds currently make up total outstanding gross debt. However, at the end of June 2018, ADM held USD 5.0 billion of unused and available borrowing capacity under its committed credit facilities with a number of lending institutions.

Figure 14: Key figures of ADM (Fiscal years end December)

| USD billion | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 Q2 |

| Total assets | 43.8 | 44.0 | 40.2 | 39.8 | 40.0 | 38.8 |

| Total equity | 20.2 | 19.6 | 17.9 | 17.2 | 18.4 | 18.7 |

| Enterprise value | 31.4 | 36.7 | 25.9 | 32.0 | 29.0 | 35.1 |

| Market capitalization | 28.6 | 33.1 | 21.8 | 26.2 | 22.3 | 28.3 |

| Gross debt | 6.9 | 5.7 | 5.9 | 6.9 | 7.5 | 7.6 |

| Cash | 4.1 | 2.1 | 1.8 | 1.1 | 0.9 | 0.9 |

| Net debt | 2.8 | 3.6 | 4.1 | 5.8 | 6.6 | 6.7 |

| Net debt/EBITDA (x) | 0.9 | 0.9 | 1.7 | 2.3 | 2.6 | 2.4 |

Sources: Bloomberg, Chain Reaction Research

ADM is listed on the New York Stock Exchange. Figure 15 shows the top-5 shareholders of ADM as of the most recent filing dates. Most of the top shareholders are from the United States. These shareholders have, on average, weak forest policies, according to Forest 500. Figure 15 also shows the shareholders of ADM that have more robust policies in place: Bank of America (United States) and Goldman Sachs. However, both of them do not specifically discuss soy-related deforestation in their policies. The Government Pension Fund of Norway has a low score, but the company has taken important steps in engaging with Bunge on deforestation related to soy and even divested from one company related to deforestation for soy production (most likely SLC Agricola). Legal & General is a signatory of the Cerrado Manifesto. Because of reputational risk, some of these financial institutions may consider engagement or divestment options.

Figure 15: Top-5 shareholders of ADM as of most recent filing dates

| Financial institution | Country | Forest 500

(1-5 score) |

% outstanding | Value (USD mln) |

| State Farm | United States | 10.06 | 2,441.5 | |

| BlackRock | United States | * | 7.55 | 1,832.9 |

| Vanguard | United States | 7.35 | 1,785.2 | |

| State Street | United States | * | 5.96 | 1,452.4 |

| Macquarie Group | Australia | * | 2.88 | 698.1 |

| — | — | — | — | |

| Bank of America | United States | *** | 0.93 | 226.7 |

| Government Pension Fund of Norway – Global | Norway | ** | 0.92 | 206.1 |

| Goldman Sachs | United States | *** | 0.77 | 187.4 |

| Legal & General | United Kingdom | * | 0.57 | 138.1 |

Source: Thomson Reuters Eikon, Chain Reaction Research

The outstanding gross debt of ADM consists of issued bonds. Figure 15 shows the top-5 bondholders as of the most recent filing dates. Most of these bondholders are US-based investors that score below average on their deforestation policies, according to Forest 500. These bondholders will not likely consider engagement or divestments possibilities. Deutsche Bank is, however, an important bondholder that has above-average deforestation policies in place. It also specifically says that it is is “committed to help achieve zero net deforestation by 2020 in the palm oil, timber, soy and beef sectors.” Aegon and Aviva, meanwhile, are both signatories of the Cerrado Manifesto. Some of these financial institutions may consider engagement or divestment possibilities.

Figure 16: Top-5 bondholders of ADM as of most recent filing dates (N.A. = Not available)

| Financial institution | Country | Forest 500 (1-5 score) | % outstanding | Value (USD mln) |

| Prudential Financial (US) | United States | 4.86 | 314.7 | |

| American International Group (AIG) | United States | 3.47 | 224.9 | |

| Macquarie Group | Australia | * | 3.41 | 220.9 |

| GE Capital Services | United States | N.A. | 2.76 | 178.9 |

| Nationwide Mutual Insurance | United States | N.A. | 2.60 | 168.4 |

| — | — | — | — | |

| Aegon | Netherlands | ** | 1.68 | 109.0 |

| Deutsche Bank | Germany | **** | 1.04 | 67.4 |

| Aviva | United Kingdom | N.A. | 0.63 | 40.8 |

Source: Thomson Reuters Eikon, Chain Reaction Research

At the end of December 2017, ADM had no loans outstanding. However, it does have USD 5 billion in revolving credit facilities that it can draw upon when necessary. These three credit facilities have maturity dates ranging from December 2018 to December 2022 and are renewed on a yearly basis. Figure 17 shows the involved financial institutions and their committed amounts. Most of these financial institutions have above-average deforestation policies in place and could therefore consider engagement or divestment possibilities. JP Morgan Chase (United States) and ING Group (Netherlands) have specific policies in place for soy-related issues. JP Morgan commits to zero-deforestation in 2020, and ING says that clients should not be active in removal of primary forest related to soy production.

Figure 17: Banks providing revolving credit facilities (N.A. = Not available)

| Financial institution | Country | Forest 500 (1-5 score) | Value (USD mln) |

| Bank of America | United States | *** | 750.0 |

| Barclays | United Kingdom | ** | 750.0 |

| Citigroup | United States | **** | 750.0 |

| JPMorgan Chase | United States | **** | 750.0 |

| ABN Amro | Netherlands | N.A. | 333.3 |

| Bank of New York Mellon | United States | * | 333.3 |

| DZ Bank | Germany | N.A. | 333.3 |

| ING Group | Netherlands | **** | 333.3 |

| Regions Financial | United States | N.A. | 333.3 |

| Wells Fargo | United States | * | 333.3 |

Source: Thomson Reuters Eikon, Chain Reaction Research

Above, we calculated that ADM faces a market risk (if it does not appropriately mitigate deforestation related risks) that could result in losing USD 0.2 to 0.6 billion of its EBITDA. The net debt/EBITDA will then potentially move up from 2.4X to 3.0X. This might result into higher interest costs and a higher weighted average cost of capital (WACC). Banks increasingly . An increase in the WACC might further depress the market capitalization of ADM. As a rule-of-thumb, an increase in the WACC by 50 basis-points might reduce ADM’s Enterprise Value based on a Discounted Cash Flow calculation by five to ten percent.

Tax avoidance undermines ADM’s governance reputation

In its 2017 annual report, ADM indicated that 6.9 percent of its total net revenues was attributed to the Cayman Islands. However, according to its 2017 annual report, ADM does not hold any property related to its business in the Cayman Islands. ADM does have seven subsidiaries that are incorporated in the Cayman Islands, which are listed as either holding, investment or management entities. Since the Cayman Islands is a well-known tax haven jurisdiction, the large attribution of net revenues may indicate possible tax avoidance by ADM and could pose a reputation risk. Therefore, in order to counter this risk, ADM can provide more clarity on its reasons for incorporating seven subsidiaries in the Cayman Islands. The current public debate and awareness on tax avoidance issues could otherwise also lead to disrupted customer/financing relationships.

In 2017, the EBIT was 2.6 percent of the total net revenues. If this percentage is applied to the USD 4.2 billion of net revenues that were attributed to the Cayman Islands, USD 110.8 million would be the corresponding EBIT. Assuming this part of the EBIT would otherwise have been taxed at a weighted average corporate tax rate of the other major countries from which ADM derives most of its net revenues (United States, Switzerland, Germany and Brazil), the added tax expense would have totaled USD 33.6 million. That amount would have cut net profit by 2.4 percent. It is of course possible that the EBIT from revenues now attributed to the Cayman Islands is larger. The costs of the operations are not evenly distributed amongst the reported countries. In that case, a larger impact on the net profit will likely occur.