Approximately 18 percent of global greenhouse gas emissions comes from deforestation. Palm oil and soybeans are two of the four main crops driving deforestation, next to other environmental and social problems. Investor awareness regarding the material risks emerging in the palm oil sector has grown, but soy-related risks are not yet widely recognised. This paper aims to compare the two supply chains and draw lessons for investors in dealing with companies in the soy supply chain.

Download the PDF here: ESG Lessons from Palm Oil for Soy Supply Chain Investors

Key Findings

- Sustainability risks are significant and persistent: Palm oil and soy significantly contribute to deforestation, climate change and biodiversity loss, as well as land rights conflicts, corruption and labour rights violations. With external pressure, the sector will have more incentives to solve these sustainability risks.

- Certification schemes do not deliver on their promise: Neither the RSPO (palm oil) nor the RTRS and ProTerra (soy) have yet brought about a sustainable transformation of the entire sector.

- There are a lot of uncertainties around public policy measures: Policy initiatives in producer countries can make a huge impact, as demonstrated by the strong reduction of deforestation rates in Brazil since 2004. The Jokowi government in Indonesia is also taking substantive initiatives now, but in Brazil the Temer government is undermining progress. Presidential elections in Brazil (October 2018) and Indonesia (April 2019) may bring major shifts again.

- International political and procurement power is driving change: International awareness on the negative sustainability impacts of oil palm cultivation has brought about foreign governments and buyers to act, spurring movement towards sector transformation. Foreign governments, buyers and investors will likely exert more pressure on the soy sector in the coming years as well.

- Sourcing transparency is the key to sector transformation: Insights into the origin of the palm oil or soy that a company uses enables the proper implementation of sustainability commitments. The soy supply chain is still lagging behind the palm oil supply chain in this respect.

- Business-as-usual may become a high-risk strategy: Oil palm plantation companies hanging on to business-as-usual practices have lost important customers, accrued fines and seen their capital costs increase. While the transformation of the soy sector is still less advanced, business-as-usual may eventually become high-risk in this sector as well.

- Investors are exposed across their portfolios: Investments in the palm oil sector have exposed investors to the risk of lower returns as well as to reputational risks. Investors may expect similar financial and reputational risks across their portfolios, through investments in soy growers, traders, animal feed producers, slaughterhouses, dairy companies, retailers and banks.

- Investors can take action: Investors can collect information, analyse their portfolios, engage with companies in the soy supply chain and shift investments to companies that offer upside potential as they address sustainability risks in a comprehensive way.

Sustainability Risks Are Persistent in Palm Oil and Soy

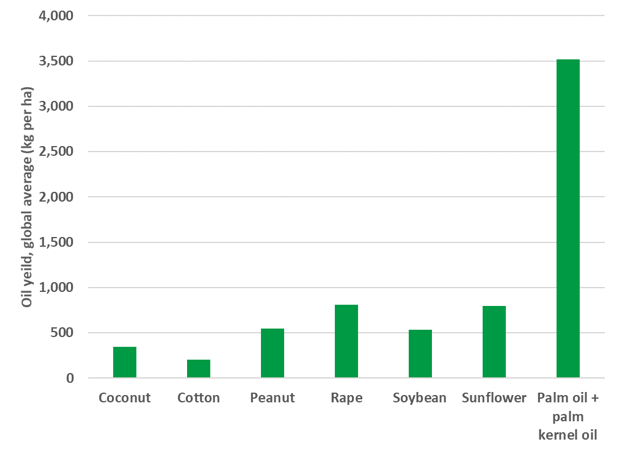

The oil palm tree has by far the highest yield per hectare compared to other edible oil crops such as soybeans, sunflower and rapeseed. This has contributed to the rapidly increasing use of palm oil as cooking oil and as an ingredient in food products such as margarine, confectionery, chocolate, ice cream and bakery products. It is also widely used in non-food products, such as soap, candles, cosmetics and biofuels.

Figure 1 Average yields of edible oils per hectare, 2018/2019

Source: USDA

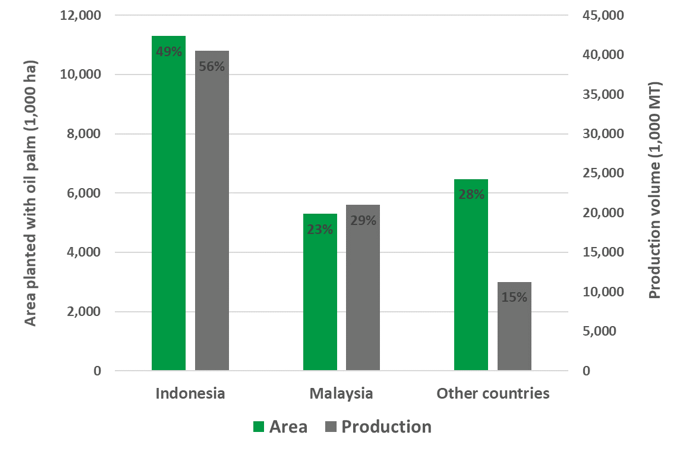

Malaysia and Indonesia together account for 85 percent of global palm oil production, with Indonesia showing the fastest growth: the harvested area has increased tenfold in 25 years to 11.3 million ha in 2018 – three times the size of the Netherlands. This swift growth has brought significant economic benefits to Indonesia, but has come at a high social and environmental price. The palm oil sector has caused deforestation and biodiversity loss, contributed to climate change, violated the land rights of local communities and the labour rights of its workers, and is prone to corruption and tax avoidance.

Figure 2 Palm oil acreage and harvested volume, 2018/2019

Source: USDA

The sustainability risks of the palm oil sector are well documented, thanks to satellite monitoring, scientific research, companies in the supply chain making their supply chains transparent, and on-the-ground activities of NGOs and media. The Indonesian forest fires of 2015, which lay a blanket of smog over the Southeast Asian region, showed the externalities caused by the sector. The Paris Climate Change Agreement signed in December 2015 also played a crucial role, as it acknowledged the strong contribution of deforestation and peat development to climate change.

As long as these issues are not addressed in a profound way, NGOs and consumers increasingly put pressure on foreign governments, buyers, financiers and other actors to take initiatives. These actions may range from denying investments to unsustainable palm oil producers and excluding them from supply chains, to an outright ban of all palm oil – irrespective of the conditions under which it is produced. With these forces gaining more impetus globally, the development perspectives of the entire sector are at stake.

The Soy Sector Is Facing Similar Sustainability Issues

While not yet as present in the international spotlight as the palm oil sector, the soy sector is creating similar sustainability problems and may thus expect increasing international scrutiny. Soybeans are mainly cultivated and crushed for the soy meal, which is the most important protein source in animal feed for poultry, pork and dairy. The soy oil is a valuable by-product, used in many food and personal care products.

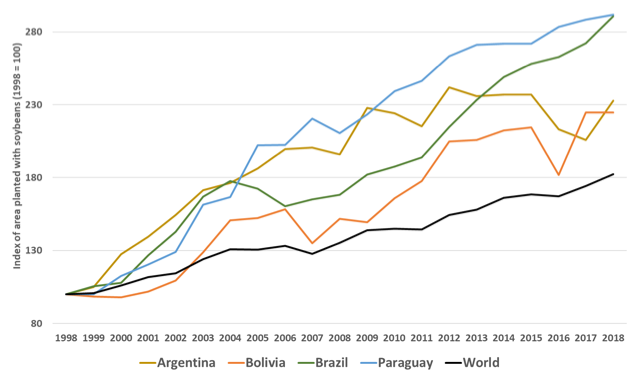

Figure 3 Growth of areas planted with soybeans (1998 =100)

Source: USDA

Over the last 20 years, the global soybean cultivation area has almost doubled to 130 million ha. As the Brazilian soy acreage almost tripled in the same period to 37.5 million ha, Brazil is now the leading global soy producer – accounting for 33% of global production. Soy cultivation in other Latin American countries is also rapidly expanding. The impacts of this expansion on deforestation and biodiversity loss are increasingly documented. International attention for the sector’s role in creating land right conflicts, corruption and labour rights’ violations is still limited, but can be expected to increase further.

Until 2017, international attention for the negative impacts of soy cultivation had a strong geographical focus. The vast tropical rainforests of the Amazon region of Brazil with their unique biodiversity, for example, have captured the public imagination, which Greenpeace used to exert the pressure needed to halt most soy expansion in this region. In 2006, the voluntary Amazon Soy Moratorium was announced for soy production in the Amazon, which was extended indefinitely in 2016. While the moratorium did not completely block soy expansion, it slowed down deforestation in this region. “Before the moratorium, 30 percent of soy expansion occurred through deforestation, and after the moratorium only about 1 percent of the new soy expansion came at the expense of forests,” concluded a Science article in 2015.

Yet since 2006, soy expansion shifted to areas such as the Cerrado in Brazil and forest regions in Colombia, Paraguay, Argentina and Bolivia, contributing to deforestation, biodiversity loss and land rights conflicts in those regions as well. Like the palm oil sector, the soy sector has not yet been able to address the sector’s negative sustainability impacts in a profound way. The Cerrado region, Brazil’s vast wooded savanna covering around 20 percent of the country, is highly biodiverse and important for carbon capture. It has now lost 46 percent of its native vegetation cover. Effective steps are needed to address soy-related sustainability risks, as the world will be watching more closely. Being even more export-oriented than the palm oil sector, the soy sector could eventually risk its license to operate.

Certification Schemes Do Not Fully Deliver on Their Promise

About fifteen years ago, sustainability certification of commodity producers emerged as the answer to various sustainability risks. Together with key traders and processing companies, nature conservancy organisation WWF initiated multi-stakeholder forums such as the Roundtable on Sustainable Palm Oil (RSPO) and the Roundtable on Responsible Soy (RTRS). Of the two, the RSPO managed to attract a much broader and more diverse membership, including plantation companies, refiners, traders, banks, governments, environmental NGOs and community organisations.

Roundtable on Sustainable Palm Oil Delivers Mixed Results

Hopes were high when the RSPO launched its certification scheme for Certified Sustainable Palm Oil (CSPO) in 2007. The certification process aims to give traders, consumer goods companies and end-consumers independent third-party assurance that their palm oil is produced in a sustainable way, without creating deforestation nor land rights conflicts. Over the years, CSPO has reached a 19 percent share of the global palm oil market. Many palm oil buyers in established markets in Europe and North America are now sourcing exclusively RSPO-certified palm oil.

Many food, chemical and biofuel companies have tried to mitigate growing consumer concerns by promising to switch sourcing to 100 percent CSPO. To meet their promises, these companies have put pressure on their suppliers to move towards certification. For many plantation companies and traders, conforming to the demands of their buyers is the only way to ensure continued access to attractive export markets. Against this backdrop, the RSPO has created awareness regarding sustainability issues among palm oil growers and traders. It has also stimulated the adoption of improved production practices, helping avoid biodiversity loss and reducing deforestation.

Overall, however, the RSPO has not yet brought about transformation of all segments of the supply chain: the upstream plantation level, the midstream level of traders and refiners, and the downstream consumer market level. The RSPO principles and criteria are to avoid deforestation. Yet, the RSPO has not been able to motivate all its members to “walk the talk.” Too many of them do not apply the RSPO principles and criteria to all their business activities. They are not strict enough to avoid deforestation.

The ambivalent approach of many RSPO-members to CSPO certification is not addressed effectively by the RSPO. Transparency on supply chain relationships has never been a pre-condition for CSPO certification. This makes it difficult to assess if traders and refiners are demanding CSPO certification from all their suppliers. They are looking to see if consumer goods companies are living up to their promises to consumers. They are also assessing whether plantation companies are achieving certification for more than a few of their plantations — enough to serve the more demanding export markets.

A second issue is the dominance of the growers, supported by their governments, in RSPO and RTRS standard settings and dealing with complaints on non-adherence. This situation results in weak standards and poor enforcement among non-compliant members.

A third issue is how the implementation and monitoring of certification schemes is contracted out to private auditors. Auditors are typically reluctant to be too critical of their clients. Together, these problems lead to the conclusion that thus far, the RSPO has failed to transform commercial practices across the board and to address the sector’s sustainability risks in a structural way.

The suspension by the RSPO of the Swiss food giant Nestlé in June 2018 indicates that the big downstream and consumer goods companies might be losing faith in commodity certification schemes as well. The RSPO suspended Nestlé because the company did not submit a progress report on how the company is working towards 100 percent CSPO in its supply chains. However, the company points to “fundamental differences in the theory of change” with the RSPO: “We believe in achieving traceability to plantations and transforming supply chain practices through interventionist activities instead of solely relying on audits or certificates.”

Although Nestlé was reinstated three weeks later and the company expressed its support for “RSPO’s role in driving industry wide change,” the quarrel indicates that industry players committed to more sustainable supply chains are shifting to other intervention strategies. Now the RSPO Principles and Criteria are being reviewed again after five years, and NGOs are pushing for significant change. If the RSPO does not adopt such changes by November 2018, some NGOs and downstream companies may walk away.

Roundtable on Responsible Soy Even Weaker Than RSPO

By contrast to the RSPO, the membership of the Roundtable on Responsible Soy (RTRS) has always been less diverse, with limited involvement of environmental NGOs, labour unions and community organizations. This has resulted in weaker certification standards and compliance mechanisms. The pressure by downstream companies on the soy growers to achieve certification has been lighter.

As of 2015, only 2 percent of global soy production is certified. Two-thirds of RTRS certified soy is consumed by only one country, the Netherlands. After assessing the use of certified soy by 133 meat, dairy and retail companies in 9 European countries, WWF concluded: “While some front-running companies are leading the way on responsible soy, far too many are lagging behind – or hiding from responsibility completely.”

There are a lot of uncertainties around public policy measures

Public policies of production countries, or the lack of policies, strongly influence the development of the palm oil and soy sectors. However, it is difficult to assess their impact on the longer term, as government policies probably will change – and change again.

Indonesia Strives to Transform the Palm Oil Sector

Under President Suharto, who ruled Indonesia authoritatively for more than thirty years beginning in 1965, Indonesia stimulated the palm oil sector in a controlled manner — mostly benefiting a small group of his business friends. Since his fall in 1998, the country has seen a movement of political decentralisation, giving more power and autonomy to the province and district levels. Different from neighbouring Malaysia, where the government’s pledge in the late 1990s to maintain at least 50 percent of its forest cover curtailed expansion, Indonesia executed expansionist policies focused on market creation and production goals with limited incentives for technology driven intensification. This resulted in an unrestrained expansion of the palm oil acreage, not in the least to fill the pockets of the local leaders. National legislation and regulations dealing with the side effects, if introduced at all, were hampered by the weak implementation powers of national bodies and corruption in the juridical system.

However, changes are now occurring in government circles. The devastating forest fires and haze of 2015 have played a large part in this change, as has Indonesia’s global commitment to reduce its GHG emissions under the Paris Climate Change Agreement. Just as important, since President Jokowi assumed office in 2014, there has been more attention on increasing state income by combatting corruption and tax avoidance. International financial support for sustainable forest management, among other countries such as Norway, also contributed to the government’s change in attitude.

For these diverse reasons, the Indonesian government is now introducing more stringent regulations affecting the palm oil sector, including:

- The first moratorium on new licences in primary forest and peatland concessions was announced in 2011, and the present moratorium is running until 2019. Additionally, in 2016, a five-year moratorium on all new palm oil licences was announced;

- In its Nationally Determined Contribution (NDC) to the Paris Climate Change Agreement, Indonesia set an unconditional emissions reduction target of 29 percent compared to the business-as-usual scenario by 2030. Stricter land use governance is expected, since 63 percent of Indonesia’s GHG emissions are the result of land use change and peat and forest fires;

- In December 2016, a moratorium on peat development came into force and the government established the Peat Restoration Agency that same year;

- To tackle tax avoidance, in July 2017 a new controlled foreign company (CFC) regulation came into force;

- And also in July 2017, Indonesia’s Financial Services Authority (OJK) issued its Regulation on Sustainable Finance, which demands banks to ensure that the companies they finance meet all (environmental) regulations.

- Since March 2018, a presidential regulation requires legal entities to declare the identity of beneficial owners. This aims to reduce opportunities for illicit activities such as tax evasion and corruption.

Collectively, these policy initiatives show that Indonesia aims for a fundamental transformation of the sector. Implementation and enforcement of these new policy initiatives remain a large bottleneck, but there has been progress. For example, the anti-corruption agency KPK is chasing corruption and tax avoidance schemes, some plantation companies have been fined because of causing forest fires, and some concessions have been revoked. The Ministry of Environment won a court case against the powerful pulp and paper company APRIL over the development of peatland. This development sends a signal to all pulp and oil palm plantation companies: Ignoring government regulations is no longer risk-free.

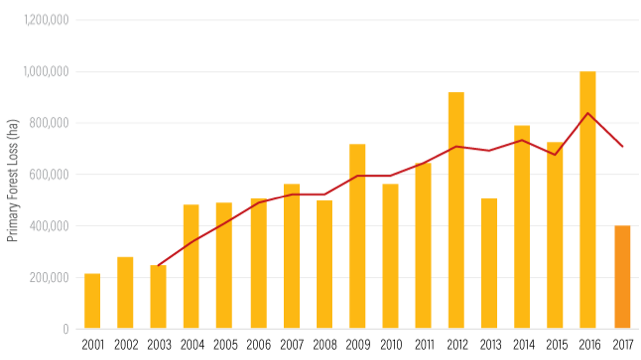

As a result of these policy initiatives, the annual deforestation rate in Indonesia in 2017 dropped to the lowest level since 2004. This decrease is likely due in part to the national peat drainage moratorium, in effect since 2016. Primary forest loss in protected peat areas fell by 88 percent between 2016 and 2017, reaching the lowest level ever recorded.

Figure 4 Primary forest loss in Indonesia

Source: WRI

Yet, government policies can change once again. Whether the government’s actions to transform the palm oil sector will persist in the coming years will depend largely on the outcome of the presidential elections in April 2019.

Brazil Gives the Soy Sector More Room for Expansion

The political climate in Brazil has also been oscillating. Like in Indonesia, local landlords (the “ruralistas”) control the governments at the state and district levels. These rural leaders have always pushed strongly for the expansion of soy cultivation. But under the more progressive national leadership of presidents Lula and Dilma (2003-2016), their power declined.

Since 2004, the Brazilian government took various steps to stop deforestation in the Amazon region and other high biodiversity regions. These steps include:

- The Action Plan for the Prevention and Control of Deforestation in the Legal Amazon (PPCDAm), launched in 2004, introduced better cooperation between different government levels on the issue of deforestation, satellite monitoring by the National Institute of Spatial Research (INPE) and stronger enforcement of environmental regulations by the Institute for the Environment and Renewable Natural Resources (IBAMA);

- Extensive expansion of conservation units (protected land) and recognition of indigenous lands;

- In 2007, a Presidential Decree made it possible to single out municipalities with very high deforestation rates for more rigorous monitoring of irregular activity and harsher registration and licensing requirements;

- Credits from the National Rural Credit System (SNCR) for agricultural activities in the Amazon biome in 2008 became conditional upon presentation of proof of the borrower’s compliance with environmental legislation and legitimacy of land claims;

- In 2010 the ABC Program was created, a multi-billion-dollar credit line specifically dedicated to finance agricultural practices with high productivity and low greenhouse gas emissions.

- In the following years, the Banco Central do Brasil (BCB) introduced more sustainability-related regulations. For instance, it prohibited lending to entities or individuals associated with the employment of slave labour. Also, the BCB issued guidelines on how to implement sustainability criteria into the day-to-day practices of commercial banks.

Taken together with the voluntary Amazon Moratorium, these policy measures largely explain why the annual Brazilian deforestation rates fell from 2.7 million ha in 2004 to an average of 0.7 million ha per year in the period 2011-2017.

Figure 5 Deforestation in the Brazilian Amazon

Source: INPE

In August 2016, however, the Senate impeached President Dilma based on questionable corruption charges against her and former president Lula. She was replaced by the evidently corrupt vice president, Temer, who represents the interests of the ruling elite. To please the powerful ruralista lobby, the Temer administration is quickly reversing earlier regulations aiming to deal with the sustainability risks created by the forestry and agriculture sectors.

In March 2018, Brazil’s Supreme Court (STF) approved several controversial revisions to the Forest Code adopted by the Temer administration, including granting amnesty to those who illegally cleared land in nature reserves before July 2008. Cattle ranching and crop cultivation can continue there, without the need for reforestation or payment of fines previously levied by IBAMA. According to advocacy group De Olho nos Ruralistas, this amnesty pardons R$ 8.4 billion (USD 2.6 billion) in fines for the illegal deforestation of over 330,000 ha, mostly carried out between 2006 and 2008. Reporter Brasil, meanwhile, exposed that 249 members of Congress and ministers had received close to R$ 59 million (USD 18 million) in donations from individuals and businesses that IBAMA fined for illegal deforestation.

The STF also maintained the constitutionality of other Forest Code provisions deemed to weaken environmental protection in the country. This includes a new provision to allow people who previously carried out illegal deforestation to obtain new licenses. Positively, however, the STF reiterated essential elements of environmental legislation, including the need to protect forests for future generations and consider the consequences of deforestation to the country’s biodiversity and prosperity.

The present political climate in Brazil is not forcing the soy sector to address its detrimental impacts on the climate, biodiversity and local communities. On the contrary, soy expansion is increasing. But the lesson learned from Indonesia is that government policies can easily change again, caused by pressure from international stakeholders and a shift in the domestic political climate.

After a long period of uncertainty, the Superior Electoral Court at the end of August finally decided that progressive ex-president Lula cannot participate in the presidential elections of October 2018, now he is being imprisoned on corruption charges. If Lula would have participated, he would almost certainly have won. But now he is not, far-right candidate Jair Bolsonaro is the top candidate.

International Political and Procurement Power Is Driving Change

Pressure by foreign governments and international palm oil buyers played an important role in starting the comprehensive transformation of the palm oil sector taking place in the past few years.

Foreign Government Policies Set Limits

One example is the Amsterdam Declaration of December 2015, in which six countries — Denmark, France, Germany, Norway, The Netherlands and the United Kingdom — committed to pushing all EU countries and private sector stakeholders towards complete palm oil sustainability and traceability.

The Paris Climate Change Agreement, which came into force in November 2016, highlights the critical role of the land use sector, including palm oil and other plantations, in relation to climate change. The agreement requires all signatory countries to put maximum effort into reducing their impact on climate change.

Another example is the ongoing revision of the European Union’s biofuel policy, which aims for 10 percent of transport fuel consumed in each EU country to come from biofuels by 2020. In April 2017, however, the European Parliament voted in favour of a motion to ban biofuels made from edible oils, including palm oil and soy oil, to avoid contributing to deforestation, peat development, labour rights violations and community conflicts. In June, the EU reached a compromise to phase out the use of edible oils as biofuels by 2030, which is perceived as a “war on palm oil” by Indonesian growers.

Palm Oil Buyers Push for No Deforestation

Even more remarkable is how international palm oil buyers have used their market power in recent years. With certification schemes and public policies in production countries not providing sufficient answers to the sustainability risks created by the palm oil sector, NGOs continued to expose how well-known food and personal care brands still contained unsustainable palm oil. Approximately five years ago, the large palm oil traders and refiners as well as their main customers (the consumer goods companies) realized that more ambitious steps were needed to maintain the credibility of their sustainable sourcing promises.

Responding to this pressure, Wilmar International – by far the largest palm oil trader and refiner in the world – became the first to announce a “No Deforestation, No Peat and No Exploitation” (NDPE) policy in 2013. The market leader promised to start banning plantation companies involved in deforestation, development of peat lands, or conflicts with local communities from its supply chains. The company has kept its promise – sometimes after some pressure – by excluding various plantation companies from supplying to its refineries.

Many other palm oil refiners, traders and consumer goods companies, such as Unilever and PepsiCo, have also embraced NDPE policies. When a supplier is in violation of a refiner or trader’s policy, the trader or refiner can cease purchasing. This action has already happened multiple times over the past few years, with many oil palm plantation companies losing substantial revenues as a result.

As many refineries make NDPE commitments, plantation companies will have to follow within a few years to retain access to the market. Twenty-nine company groups controlling 74 percent of the palm oil refining market in Indonesia and Malaysia have adopted NDPE policies which require them to source only from compliant suppliers by various target dates.

Foreign Government and Buyer Pressure Growing in the Soy Sector

Even though the trend is not yet as pronounced as in the palm oil sector, the soy industry has clearly started to feel the pressure of foreign governments and buyers. Here as well, the clear link between deforestation and climate change acknowledged in the Paris Climate Agreement garnered a lot of attention. Therefore, the EU is also phasing out soy oil as a biofuel by 2030.

A few years later than the main downstream companies in the palm oil supply chain, the international dairy, meat and retail companies, which are ultimately buying most of the global soy harvest, are now turning their eye on the soy sector as well. Since the launch of the Cerrado Manifesto in September 2017, 61 large downstream consumer goods and retail companies such as Nestlé, Unilever, Carrefour, Tesco, Walmart, and McDonald’s, endorsed it. In this manifesto, civil society groups urged immediate action by companies that purchase soy and beef to eliminate deforestation and conversion of native vegetation in the Cerrado.

In November 2017, the China Meat Association (CMA) and 64 Chinese company members together with WWF announced the Chinese Sustainable Meat Declaration. Since China is the recipient of two-thirds of Brazilian soy exports, an implementation of this commitment to avoid land degradation, deforestation and conversion of natural vegetation in livestock production and feed value chains could put significant pressure on soy producers and traders to improve their sustainability performance.

Responding to such pressure from their buyers, the big soy traders – ADM, Amaggi, Bunge, Cargill, Coamo, Cofco, Louis Dreyfus, Marubeni and Mitsui – have begun to adopt and implement zero-deforestation policies in the soy sector as well. At least 49 percent of Brazil’s soy trade is now covered by some type of zero-deforestation commitment. Most of these pledges are not yet adequate to prevent the conversion of natural habitats. The focus lies mostly on eliminating illegal deforestation from supply chains.

Recently, new soy supply policies of two main international commodity traders raised the bar for the industry. Bunge strengthened its no-deforestation policy, after pressure from shareholders such as the New York State Common Retirement Fund, to include legal deforestation and a public non-compliance mechanism. Louis Dreyfus now requires suppliers to protect native vegetation, such as found in the Cerrado, and the rights of indigenous and local communities on their soy supply chains. Their announcements put further pressure on competitors such as Cargill, which was recently fined for millions of dollars by the Brazilian environmental enforcement agency IBAMA because of driving destruction of protected areas.

Sourcing Transparency Is the Key to Sector Transformation

Despite the success of the NDPE policies, a segment of the market continues to produce or purchase palm oil from recently deforested plantations and cleared peatlands. Such “leakage” of unsustainable palm oil continues because some palm oil refineries source Crude Palm Oil (CPO) without placing meaningful sustainability criteria on their suppliers. These refineries still have export markets they can sell to. Recent data released by the Indonesian Palm Oil Association (GAPKI) show a significant increase in exports of Indonesian palm oil to India, China, Bangladesh and African countries. Buyers in these regions typically do not have well developed sustainability criteria. At the same time, consumer sustainability demands are also weak.

Unsustainable palm oil also continues to be used for biofuel. Sustainability standards for biofuels are not stringent, and even these low standards are not always enforced. The Indonesian government, for instance, has a biofuel target of 30 percent blending in transport fuel supply by 2025. Producers subsidies support the biofuel market. The subsidies aim to reduce the dependence of Indonesia on oil imports and to support the domestic agricultural economy, as well as being presented as a means for climate change mitigation.

Another source of leakage occurs when refiners which do have NDPE policies in place do not always implement their policies very strictly. Some plantation groups take advantage of this limited due diligence by keeping controversial practices at some of their plantations out of sight through the use of opaque ownership structures.

The most effective way to address this leakage problem is increasing transparency on supply relationships. Various palm oil traders and downstream buyers have started publishing detailed data on the suppliers from which they source their palm oil. Now that more players are following this example, the market becomes more transparent. It also becomes easier to identify which plantation companies, traders, refiners and downstream companies profit from the leakage of unsustainable palm oil. Actions by governments, buyers and NGOs in turn focuses on these players.

As of now, such supply chain transparency is not yet a normal practice in the soy sector. Growers, traders and buyers therefore can get away more easily with poor sustainability practices. However, under NGO pressure, this situation may change rapidly in the coming years. When some companies in the soy supply chain follow the example of the palm oil sector, the pressure on other players to commit to no-deforestation policies will likely increase.

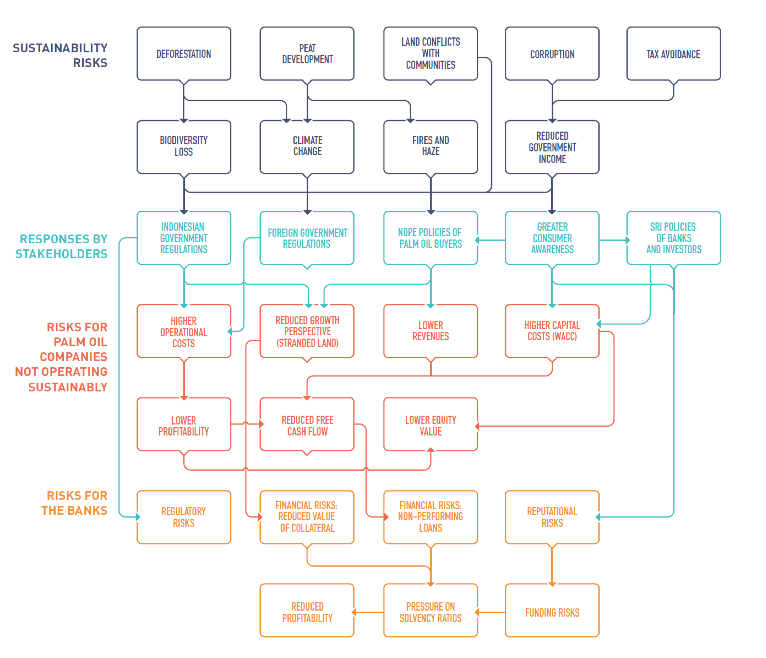

Business-as-usual May Become a High-Risk Strategy

Because of the responses of various stakeholders to the sustainability risks in the palm oil sector, business-as-usual is turning into a high-risk strategy. Plantation, refining, and trading companies operating in the palm oil sector must deal with a rapidly changing environment. Some examples of these emerging risks are:

Higher operational costs: Plantation company FGV Holdings, for instance, had to pay damages of almost USD 3 million in a case brought by a smallholder over fraud surrounding the oil extraction rate in 2010. In 2016, the company still faced similar legal cases pending for a total value of USD 600 million. Fines for using fire to clear land, such as happened to Sampoerna Agro, are also more likely.

Reduced growth perspectives: Of the 20 million hectares of Indonesian palm oil concessions in the hands of plantation companies, 12 million hectares have already been developed and eight million hectares are still awaiting development. A CRR study found in April 2017 that six million hectares of these undeveloped oil palm concessions (around 75 percent) can never be developed. They are located in forest areas or on peatland. Government regulations and policies of major palm oil buyers and financiers make it impossible to develop these concessions – which therefore become stranded land.

Figure 6 Sustainability risks turning into financial risks

Source: Profundo

Lower revenues: Failure to comply with sustainable sourcing policies can result in losing customers and — therefore — lower revenues. In March 2016, the RSPO suspended IOI due to the clearing of forests in violation of RSPO’s policy. As a result, at least 26 customers suspended contracts. The company’s share price dropped significantly, and its debt was downgraded.

When CRR exposed in April 2016 that Felda Global Ventures was also violating RSPO standards by developing peatland, the company decided to withdraw its CSPO certificates for many plantations. This immediately reduced the CPO sold to foreign customers.

In another example, Unilever suspended purchasing CPO from plantation company SSMS in June 2017 because the supplier did not comply with Unilever’s supply chain commitments. With the suspension of this contract, the oil palm plantation company lost a buyer that was equivalent to 8.4 percent of its 2016 revenue. The suspension therefore created a strong and immediate financial risk for this plantation company. When companies are pressured to negotiate new delivery contracts on short notice, they do not typically achieve the same terms and conditions enjoyed with prior trading relations.

Higher capital costs: As shown on the Forests & Finance website, many international banks have adopted ESG policies on the palm oil sector setting criteria regarding deforestation, peat and social conflicts. These banks will no longer be willing to lend money to companies violating their policies. In Indonesia, financial regulator OJK has put pressure on the country’s banks with regulation on sustainable finance. This action is to ensure the banks’ corporate customers meet all government regulations aimed at protecting the environment. Domestic or foreign banks still prepared to invest in non-sustainable plantation companies will demand a higher interest rate to compensate for the additional risks to which they are exposed.

Similarly, more and more institutional investors are paying attention to sustainability issues in the palm oil sector. Under the umbrella of the Principles for Responsible Investment (PRI), around 25 large, international investors have collaborated since 2011 in the Sustainable Palm Oil Investor Working Group to raise awareness of sustainability issues in the palm oil sector among investors and engage with companies in support of more sustainable practices.

To be able to lure investors to buying their shares and bonds, non-sustainable palm oil companies will have to offer a higher return on investment. This situation could lead to higher costs of both debt and equity, increasing the weighted average cost of capital (WACC).

Reputational risks: Sustainability risks could have material impacts for downstream companies in the palm oil supply chain as well. For companies selling food products, detergents and personal care products to consumers, their reputation and brand names are very important assets. If this reputation takes a hit because the company is exposed as buying palm oil linked to biodiversity loss and human rights abuses, this will likely have a significant material impact.

Material Risks Also Emerging in the Soy Sector

Comparable sustainability-related risks are emerging for companies in the soy sector as well: farmers, traders, animal feed producers, slaughterhouses and food companies. These risks are less pronounced than in the palm oil sector, but several trends and uncertainties may bring them to the fore:

- The uncertain impact of the presidential elections of October 2018 in Brazil on public policies regarding the soy sector as well as on public prosecution of offenders;

- The growing pressure on the other big soy traders to follow the example of Louis Dreyfus in adopting a zero-deforestation policy for the soy sector;

- The increasing awareness among international food and retail companies of the sustainability impacts of the soy sector, also outside the Amazon, as shown by the Cerrado Manifesto;

- The emergence of ESG policies on soy in the financial sector, as well as increased investor attention to the sector. In September 2017, the PRI and the American organization Ceres launched the Investor Initiative for Sustainable Forests, which supports investors on their engagement with companies to eliminate deforestation. In July 2018, they announced an expansion to include engagement with companies exposed to deforestation risks linked to soy production in South America.

Taken together, these trends may initiate a similar sector transformation as is happening in the palm oil sector. For soy growers, but also for the traders and the consumer goods’ companies down the supply chain, business-as-usual could then turn into a high-risk strategy involving higher operational costs, reduced growth perspectives, lower revenues, higher capital costs and more reputational risks.

Investors Are Exposed Across Their Portfolios

Many domestic and international investors are exposed to the sustainability risks created by the palm oil sector. This exposure occurs not only from investing in the shares and bonds issued by listed plantation companies, but also by investments in traders and refiners, consumer goods companies and banks linked to the palm oil sector. These sustainability risks can result in material risks for these investors through two pathways:

- Reduced investment returns: Higher operational costs, lower revenues, higher capital costs and reputational risks can all contribute to a lower equity value of the stocks of companies in the palm oil supply. Reduced growth perspectives for plantation companies also may reduce returns on equity for investors. A CRR study showed that equity markets react positively to the acquisition of new concessions by palm oil plantation companies. If, under current market conditions, a significant part of these concessions can no longer be developed because they contain forests and peat land, the equity markets would adjust share prices downwards. For any 10 percent of a company’s total concessions which cannot be developed, it risks losing 3.5 percent of its market capitalisation. If 30 percent cannot be developed — the average across Indonesian oil palm plantation companies — a loss greater than 10 percent may result.

- Reputational risks: Affected by their investments in the palm oil and soy sectors, investors themselves may become exposed to reputational risks as well. The website Deforestation Free Funds clearly highlights the exposure of asset managers such as Dimensional, TIAA and Vanguard to the palm oil sector. Dutch pension fund ABP, one of the largest in the world, recently divested from a South Korean firm operating a controversial palm oil plantation in the Indonesian province Papua. Moreover, the large Californian pension fund CalPERS recently responded to this pressure by changing its Governance & Sustainability Principles. It is the first large asset manager in the U.S. to formally recognize that deforestation and ecosystem degradation pose material investment risks and the first to acknowledge “land rights” as an issue requiring disclosure by companies.

For investors, it is not always clear how they are exposed to these material risks. Their exposure is not limited to companies classified as belonging to the palm oil or soy sectors, according to industry classifications such as NACE, NAICS and ICB.

Investors Exposed Across Their Portfolio to Palm Oil Risks

Investors may be exposed to sustainability risks created by palm oil production, when investing in:

- Listed plantation companies, such as Tunas Baru Lampung, Indofood Agri Resources, IOI and FGV Holdings;

- Palm oil trading and refining companies, such as Wilmar International and KLK;

- Consumer goods companies producing various food products, detergents and personal care products, such as Unilever and Kraft Heinz;

- Listed biofuel producers, such as Neste;

- Banks playing a significant role in financing the palm oil sector. An example is the Malaysian listed financial group Maybank, singled out as the most important financier of the Southeast Asian palm oil sector. As one of its main shareholders, the Norwegian Pension Fund Global in 2017 engaged with Maybank and two other Malaysian banks over their financing of the palm oil sector.

Investor Awareness in the Soy Sector Lagging Behind

While investors have been learning how sustainability risks created by the palm oil sector can become material for them and how they can be directly and indirectly exposed, investor awareness regarding the soy sector is still lagging. Similar to the palm oil sector, investors may face reputational risks as well as a reduced return on equity for stocks linked to the sustainability issues caused by soy cultivation.

In contrast to the palm oil sector, these investor risks are hardly linked to investments in the companies which are growing soy — as only a few growers are listed on a stock exchange. But the growers that are listed, such as SLC Agrícola and BrasilAgro, show that risks for those investing in their stocks can become very material. And additionally, investors will also face risks when they invest in:

- Listed soy traders such as ADM and Bunge. Their competitor Cargill is not listed, but has issued many bonds to institutional investors worldwide;

- Animal feed producers;

- Slaughterhouses and meat processors such as JBS, and dairy companies such as Danone and Nestlé ;

- Retailers such as Tesco;

- Banks financing the soy sector, such as Banco do Brasil, Banco Santander and Sumitomo Mitsui Banking.

Similar to their exposure to the palm oil supply chain, investors are exposed in multiple ways across their portfolios to the financial and reputational risks created by unsustainable soy production.

How Investors Can Address Soy Supply Chain Risks

The lessons learned from the palm oil sector could provide guidance to investors on the steps to take to address the reduced investment returns and reputational risks linked to the soy supply chain, which are emerging across their portfolios. The following steps are suggested:

- Collect information on which companies are involved in the soy supply chain, via the CRR website, the Chain and other sources;

- Analyse their portfolios to find growers, traders, animal feed producers, slaughterhouses, dairy companies, retailers and banks exposed to soy-risks;

- Engage with these companies to understand and — where necessary — improve their policies in addressing soy-related sustainability risks; and

- Shift investments to companies in the soy supply chain who offer upside potential as they address sustainability risks in the soy-supply chain in a comprehensive way.