Casino Group is a French multi-banner food retailer, and its subsidiary Grupo Pão de Açúcar (GPA) is Brazil’s second largest retailer. This report analyzes GPA’s deforestation risk exposure based on research carried out by Envol Vert, Réporter Brasil, and Chain Reaction Research (CRR) which shows that GPA purchased beef sourced from farms involved in illegal deforestation.

Download the PDF here: Casino Group’s Legal and Financial Risks Accelerate Due to Deforestation in Brazilian Beef Supply Chain

REPORT WEBINAR RECORDING

Key Findings:

- In 2019, GPA was Brazil’s second largest retailer, with a turnover of BRL 61.5 billion (USD 11.4 billion). It employed 110,834 people, more than any retailer in Brazil and about half of Casino’s global workforce.

- Casino’s subsidiary GPA has not published regular and detailed updates on the implementation of its 2016 beef sourcing policy. Although GPA’s recently updated policy is more comprehensive than previous versions, it still lacks time-bound goals and specific timelines.

- GPA sourced meat from farms involved in deforestation and encroachment on indigenous communities, according to recent research. A portion of meat sold in GPA stores came from four farms that saw approximately 4,500 hectares of forest cleared for cattle ranching.

- Casino and GPA face a significant legal risk due to allegations of non-compliance with French law. In September 2020, a coalition of organizations submitted a preliminary legal filing under the French Law on Duty of Vigilance, asking Casino to respect its legal obligations to take all necessary measures to exclude all beef linked to deforestation from its supply chain. If Casino does not comply within three months, the organizations plan to refer the matter to the competent court.

- Casino and GPA face an increased possibility of escalating financial impacts through financing and reputation risk, valued at USD 2.5 billion. Their shareholders could see respectively 66 percent/83 percent of their value at risk as debt ratios and cash debt costs may deteriorate further.

- Banks could leverage their financing dominance to influence Casino and GPA toward a best-in-class due diligence process. Deutsche Bank, BNP Paribas, HSBC, Société Générale, NatWest, and JPMorgan Chase belong to the top-10 financers of Casino/GPA with a total of USD 7.6 billion. They all have deforestation policies.

Casino is Latin America’s largest food retail company

Casino Guichard-Perrachon S.A. (Casino) is a large French food retailer, generating EUR 34.6 billion (USD 38.8 billion) in net sales and employing 220,000 people worldwide in 2019. The company is listed on the Paris Stock Exchange, with the Rallye Group as a majority shareholder. Casino operates a wide range of hypermarkets, supermarkets, convenience stores, discount stores, and wholesale stores. The company is also active in non-food segments, including renewable energy production, real estate, financial services, data analytics, logistics, and e-commerce. Casino is mainly active in France (7,946 stores) and Latin America (3,225 stores in Brazil, Colombia, Uruguay, and Argentina), with each region accounting for 47 percent of total net sales. Casino is the fifth largest retailer in France, where it has a 10.6 percent market share. In France, some of the company’s banners include Casino Supermarchés, Monoprix, Franprix, Spar, Vival, Le Petit Casino, and Naturalia.

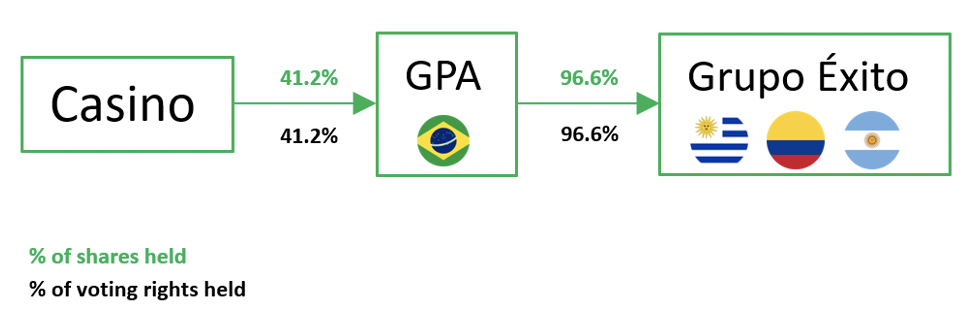

According to its data, Casino was the top retail group in Brazil and Colombia in 2019. In Latin America, all Colombian, Uruguayan, and Argentinian operations report to Casino’s Brazilian subsidiary Grupo Pão de Açúcar (GPA), under the umbrella of Grupo Éxito. In 2019, 50 percent of Casino’s workforce was based in Brazil, compared to 29 percent in France. GPA’s Brazil operations represent 75 percent of Casino’s total sales from its Latin American food segment. In March 2020, GPA migrated its stock to the Novo Mercado segment of the São Paulo Stock Exchange, converting its preferred shares into ordinary shares. GPA is also listed on the NYSE (ticker CBD). Casino holds 41.2 percent of GPA’s shares and voting rights.

Figure 1: Casino in Brazil – Ownership Structure

Source: Casino Full Year Results Presentation, 2019

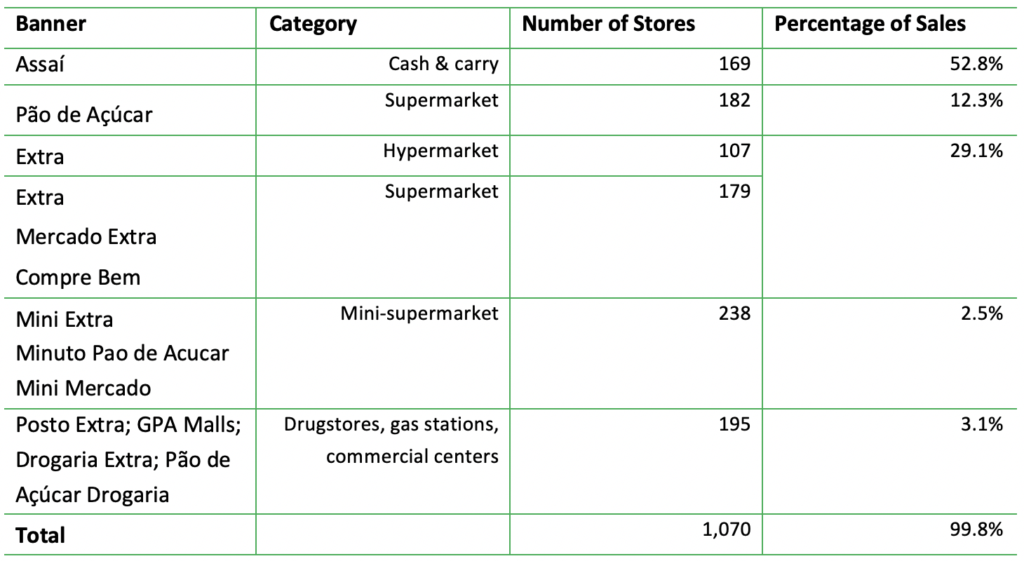

GPA is Brazil’s second largest retailer, with a turnover of BRL 61.5 billion (USD 11.4 billion) in 2019. Last year, the company employed 110,834 people, more than any other retailer in Brazil. GPA is active in 21 out of 26 Brazilian states, and its procurement and distribution are organized through 24 distribution centers and warehouses. In Brazil, GPA operates through two main business units. Multivarejo covers supermarkets, hypermarkets, neighborhood markets, fuel stations, and drugstores, while Assaí operates the cash & carry segment. In June 2019, GPA sold its entire stake in its former subsidiary, Via Varejo S.A. (electronics and appliances retailer).

Figure 2: GPA banners and sales as of Q2 2020

Source: GPA Corporate Presentation, June 2020

GPA aims to open more stores in the Legal Amazon. Specifically, it plans to expand its Assaí footprint to all the states of the Legal Amazon. Assaí represents 52.8 percent of GPA’s sales. Over the past five years, Assaí’s net sales have grown by a factor of 3.4X, making for a market share of 28.5 percent in 2019. With 17 stores currently under construction and 60 new stores planned to open in the coming three years, Assaí is expected to firmly expand its reach in the Legal Amazon.

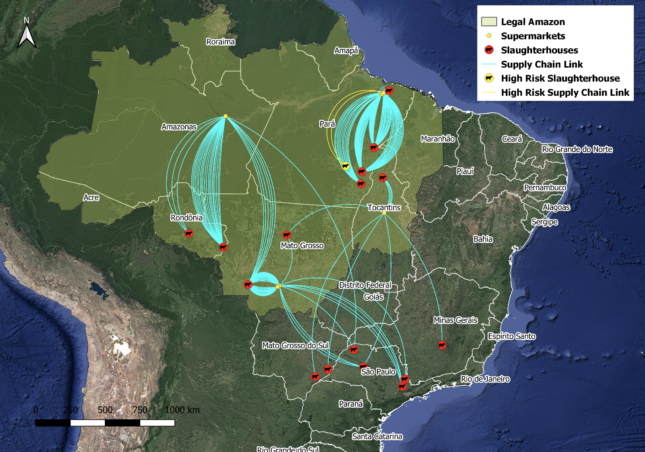

Figure 3: GPA stores in the Legal Amazon

Source: Google Maps, GPA website

GPA relies on direct suppliers to monitor deforestation in its indirect supply chain

Since the publication of its first beef sourcing policy in March 2016, Casino’s subsidiary GPA has not published regular and detailed updates on its implementation. In September 2020, GPA published a new Social and Environmental Beef Purchasing Policy. This revised policy applies to all companies that supply beef products of Brazilian origin, “whether fresh or processed, chilled or frozen, regardless of the biome in which they are located and for all the brands supplied.”

According to the Beef Purchasing Policy, GPA and its suppliers that sell beef of Brazilian origin must ensure that suppliers are:

- Free from deforestation and conversion of native vegetation,

- Free from conditions similar to slave/ child labor,

- Free from environmental embargoes due to deforestation,

- Free from invasions of indigenous lands,

- Free from invasions in environmental conservation areas, and,

- Registered with CAR (Brazil’s Rural Environmental Registry) and in possession of an environmental license, when applicable.

Although GPA’s new beef sourcing policy is more comprehensive than previous versions, it still lacks time-bound goals and specific timelines. In the new policy, GPA commits to publishing progress reports on the policy’s implementation and information related to “quantitative and qualitative Key Performance Indicators (KPIs).” The policy does not mention how, when, and how often this information will be released.

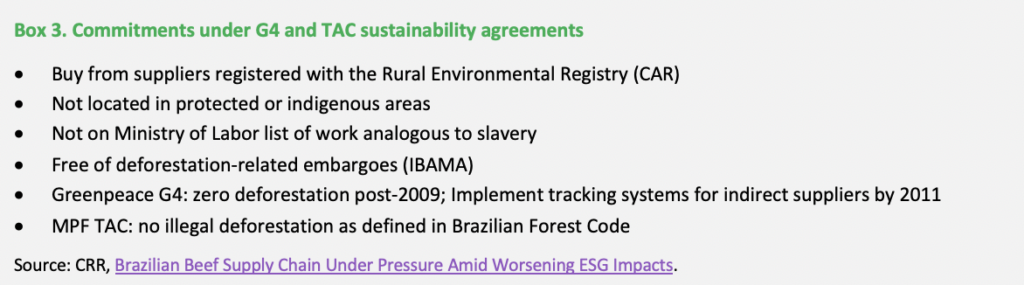

Suppliers to GPA with at least one meatpacking plant located within the Amazon biome or suppliers that purchase livestock in the Amazon biome are required to use the monitoring protocol of the Beef on Track (Boi na Linha) project. Imaflora created this project in 2019, with the support of the Federal Public Prosecution Service. It aims to strengthen the social and environmental commitments of the beef production sector. GPA suppliers are required to “become users of the protocols” of the Beef on Track Project and prove that their farms comply with 12 criteria. Competitors Carrefour, Grupo Big and suppliers JBS, Minerva, and Marfrig are also required to follow this monitoring protocol in order to meet the G4 cattle agreement and the Terms of Adjustment of Conduct (TAC) agreements.

GPA uses a traceability system that contains information on the direct suppliers of livestock to the slaughterhouses GPA sources from. At the end of December 2019, this system included data on 94 percent of GPA’s suppliers. Meat processors are required to implement a geomonitoring system to ensure compliance with GPA’s beef sourcing policy. In its sustainability report for 2019, GPA stated these systems cover 99.6 percent of the meat sold in its stores, meaning that the origins of this meat were monitored and checked. GPA suspended suppliers that did not comply with its sourcing policy or refused to implement a geomonitoring system. Farmers or meat processors could also be blocked for “any type of inconsistency in the process.” From March 2016 to the end of 2019, GPA excluded or rejected 23 suppliers.

GPA only monitors its beef suppliers, but relies on them to monitor the rest of the supply chain. The new beef purchasing policy requires that all beef suppliers provide information on the “direct origin” of the meat sold to GPA. This requirement means that GPA has traceability data on the farms that supply to the slaughterhouses and processors that sell to GPA, but not necessarily on indirect suppliers. The company states that tracing the origin of beef and monitoring indirect farms are “still complex challenges for meatpacking plants, considering that there is a vast number of potential indirect farms in Brazil.” All suppliers that have slaughtering activities are expected to implement a geomonitoring tool, regardless of the geographical location of their plants, and ensure that all cattle batches purchased comply with GPA’s beef purchasing policy. If a direct farm (tier 2 supplier to GPA) does not comply with the Monitoring Protocol for Cattle Suppliers, GPA will suspend that farm from supplying to slaughterhouses. A more direct way of monitoring upstream activities in the supply chain is likely to produce stronger results, because it would allow GPA to discover and address issues at farm level. By relying on direct suppliers to gather data on indirect suppliers, GPA may not have a sufficient level of control over its entire supply chain.

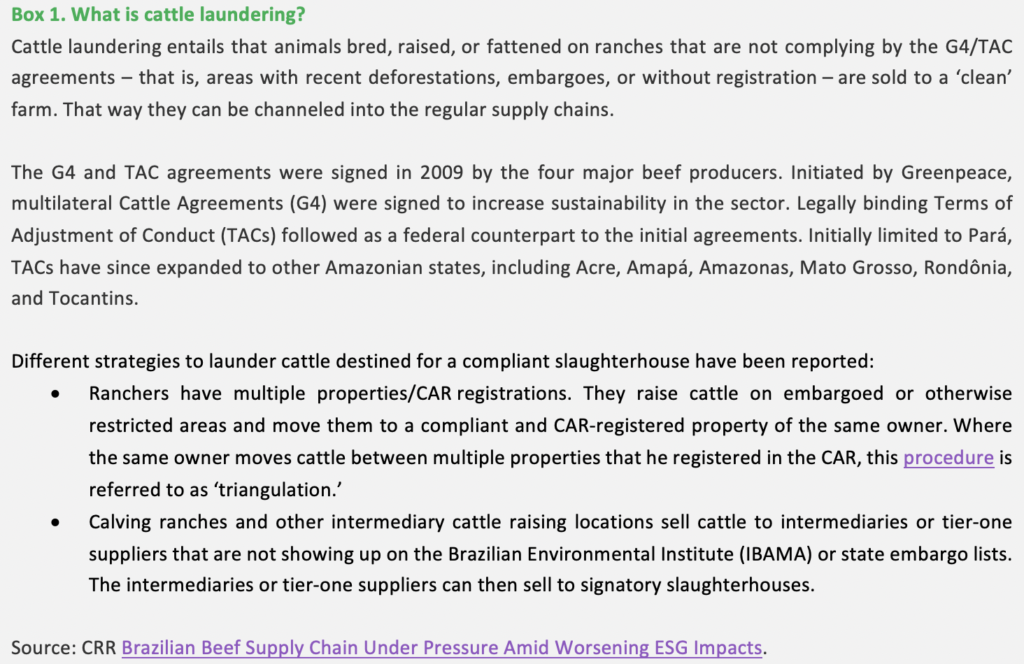

The company recognizes the challenges to track illegal practices such as livestock laundering and leakage. In May 2020, research by Repórter Brasil and Envol Vert showed that moving cattle from one farm to another is common in Brazil. If left unchecked, cattle movement increases deforestation risks as it can enable “cattle laundering” (see Box 1). The researchers found several cases of cattle raised on indigenous lands, in nature reserves, and at farms without a license, even though these practices are forbidden by Brazilian law. By using different strategies to hide the illicit origins of their cattle, farmers can sell livestock to large meatpackers and slaughterhouses, such as JBS, Marfrig, Frigol, and Mercúrio. These companies are direct suppliers to GPA.

Casino and GPA participate in several sectoral and multi-stakeholder initiatives, but impact is unclear

Both companies signed the Statement of Support for the Cerrado Manifesto, but have no specific policies to end deforestation in the Cerrado. Launched in 2017 by civil society organizations, the Cerrado Manifesto called on companies to commit to zero deforestation in the Cerrado biome. Despite being signatories, Casino and GPA have not taken any steps to mitigate their footprint in the Cerrado. GPA’s Beef Sourcing Policy, for instance, does not include specific actions to halt deforestation in the Cerrado biome.

GPA supports the 2006 Soy Moratorium, a voluntary agreement signed by major soy traders that agreed not to buy soy grown on lands deforested after July 2006 in the Brazilian Amazon. Since the signing of the Soy Moratorium, most soy-related deforestation has occurred in the Cerrado, a biome for which GPA does not specify deforestation mitigation measures. GPA has participated in the development of the Proforest Soy Toolkit, but it is unclear to what extent the company uses this toolkit. GPA reports that it cooperates with Aliança da Terra, an NGO that promotes environmental awareness in the agribusiness industry. What this cooperation entails is once again not specified.

GPA reports participating in the Working Group on Indirect Suppliers (GTFI), an initiative led by the National Wildlife Federation and Friends of the Earth, aimed at encouraging cooperation on the subject of indirect suppliers. GTA is also part of the Tropical Forest Alliance (TFA) Working Group, a multistakeholder partnership platform that supports the implementation of private-sector commitments to achieve zero net deforestation. However, GPA’s policies do not specify a time-bound goal for eliminating deforestation from its supply chain. GPA claims to provide a report on forests to CDP, yet CDP scored the company with an “F” for not submitting a response in the forest category for the period from 2017 to 2019. GPA did submit a response in relation to forests to CDP in 2020, but has yet to receive a score. Casino participates in a wider variety of sustainability initiatives in France, but it refers to GPA when reporting on initiatives linked to meat-related deforestation in Brazil.

GPA is exposed to deforestation risk in its beef supply chain

Suppliers to slaughterhouses in Brazil have exposed GPA to deforestation and other sustainability risks. Notwithstanding GPA’s beef purchasing policy, case studies suggest that the company cannot guarantee that its direct suppliers are not exposed to deforestation. In June 2020, French NGO Envol Vert published a report on deforestation in GPA’s supply chain. By tracing the origin of meat sold in GPA stores, Envol Vert found that some of the products came from four farms (all direct suppliers to slaughterhouses that sell to GPA) that have seen around 4,500 hectares (ha) of forest cleared for cattle ranching. Casino responded to these findings by stating that the company fought actively, for many years, against deforestation linked to cattle breeding in Brazil. Casino noted that GPA has been involved with the VISIPEC traceability tool, which is in a trial phase. It is likely that GPA’s new beef sourcing policy was produced partially in response to Envol Vert’s concerns.

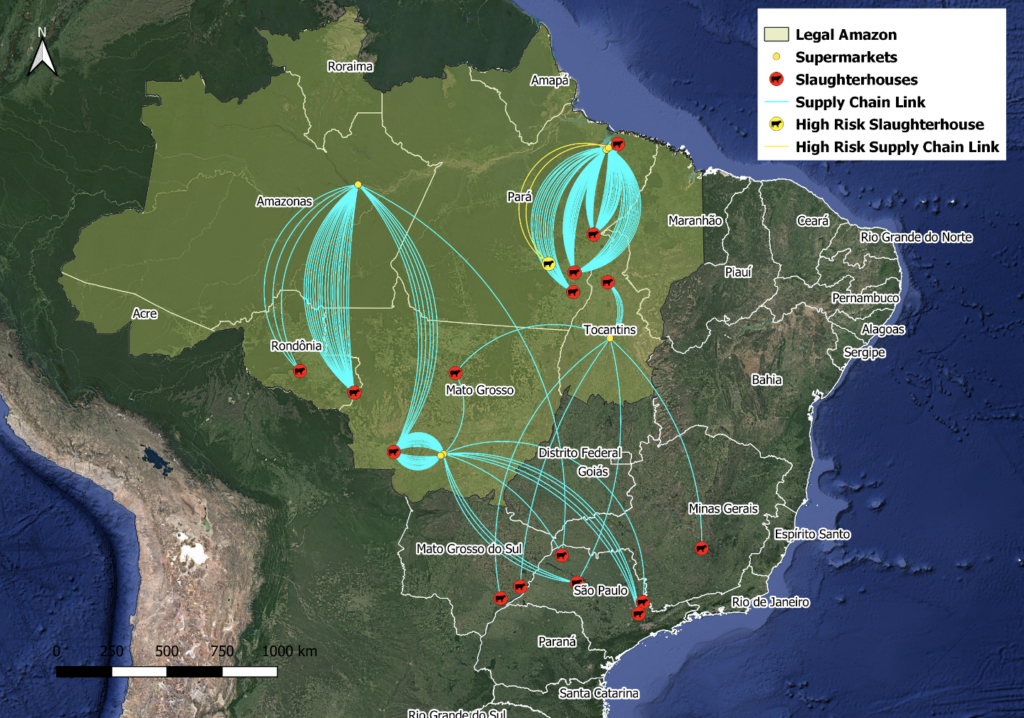

Envol Vert, Réporter Brasil, and CRR carried out a detailed supply chain analysis of meat sold in GPA stores. From October 2019 through June 2020, 131 beef products, both national and private label brands, were sampled from 10 GPA stores (Assaí and Extra banners) located in seven cities in Northern and Northwestern Brazil. The products originated from 21 slaughterhouses across Brazil, 13 of which are located in the Legal Amazon, while one was classified as high risk by Imazon. The research detailed the links between the meat sold in GPA stores, specific slaughterhouses, and direct and indirect farms. A similar investigation carried out in 2019 by CRR and Reporter Brasil found that 30 out of 500 sampled GPA beef products originated from five high-risk slaughterhouses in the Legal Amazon.

Figure 4: Origin and destination of 131 sampled GPA beef products

Source: Réporter Brasil investigation

The research reveals that GPA purchases meat directly sourced from farms involved in deforestation and encroachment of indigenous territories. Considering GPA policy’s focus on not purchasing meat that has been sourced from deforested lands, this research indicates that GPA’s current policies have not been sufficiently effective.

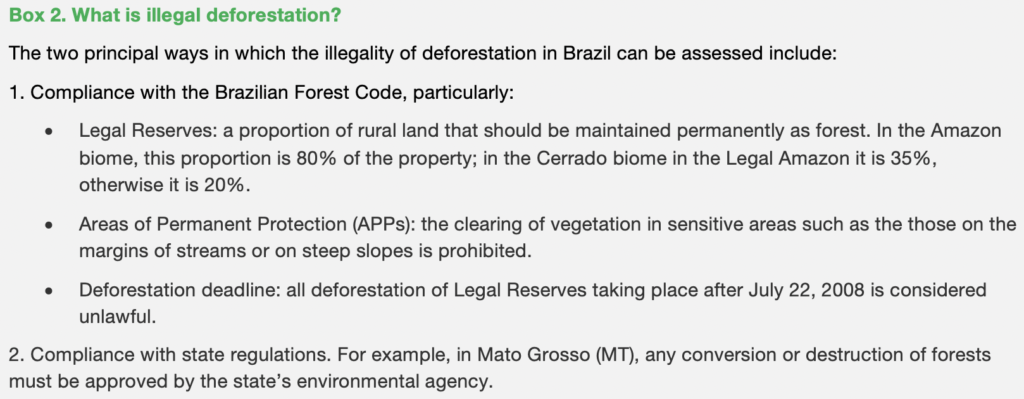

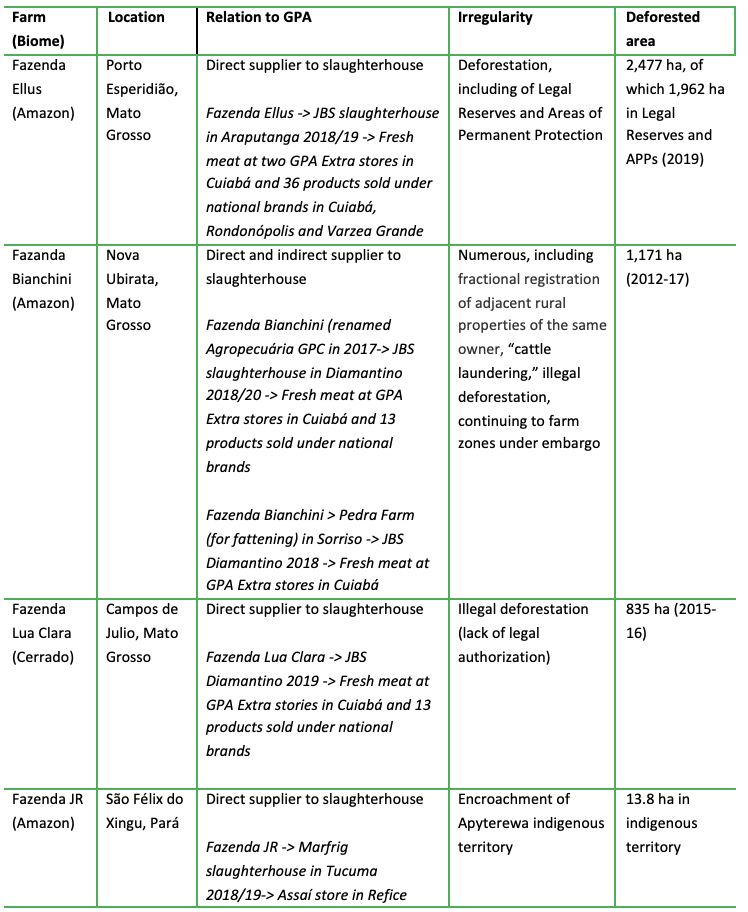

Four case studies of GPA’s sourcing from farms involved in deforestation in the Amazon and the Cerrado are presented briefly below. These examples indicate how GPA sources its meat in practice. They are also selected to illustrate the main ways in which deforestation-linked beef enters retail chains in Brazil. A more extensive overview of the four cases can be found in Annex I.

Figure 5: Deforestation-linked livestock enters GPA’s supply chain via direct suppliers to slaughterhouses

Source: Chain Reaction Research

Irregularities at suppliers in Brazil may indicate breach of French due diligence law

Casino must comply with the French Devoir de Vigilance law (the “Vigilance Law”), which imposes a mandatory due diligence for human rights and environmental impacts. This law requires French companies to establish, publish, and effectively implement measures to identify risks and prevent severe abuses to human rights, fundamental freedoms, the health and safety of individuals, and the environment. In Casino’s vigilance plan for 2020, deforestation is listed as one of 12 main risks related to the company’s activities. Casino mapped deforestation risks of its suppliers in 2017 in partnership with Earthworm Foundation. In 2018, GPA hired another consultancy to conduct a risk assessment that confirmed the first mapping of deforestation risks in Casino’s and GPA’s supply chains.

In its 2020 vigilance plan, Casino said that 100 percent of GPA’s suppliers adhered to its Responsible Beef Sourcing Policy in 2019. The company also stated that the implementation of this policy relied on two principles: (1) transparency and traceability and (2) monitoring of suppliers. In 2019, according to Casino, GPA’s three main suppliers adhered to the beef sourcing policy, while smaller suppliers still worked on an action plan to implement the policy. Since 2016, 23 suppliers have refused to implement GPA’s beef sourcing policy and, as a result, can no longer sell meat to GPA. Nineteen of the meatpackers that supplied GPA had a geomonitoring system in place. In 2019, 99.6 percent of the meat from these suppliers was of controlled origin. The other 0.4 percent was sourced from suppliers that only recently implemented a geomonitoring system or from suppliers that were suspended after refusing to implement an action plan. Moreover, according to Casino’s vigilance plan, GPA identified 22,150 farms that sold cattle to its direct suppliers. The farms were “vetted” by GPA’s suppliers.

Indications suggest that Casino and GPA are not doing enough to comply with the French due diligence law. In July 2020, environmental organization Envol Vert revealed that some meat products sold in GPA supermarkets in Brazil came from farms with irregularities. The organization said that these cases contradicted Casino’s vigilance plan and urged the company to take better measures to stop deforestation in its supply chain.

According to Envol Vert, Casino’s vigilance plan is incomplete because it does not consider indirect suppliers to the company, nor its suppliers in Colombia. Moreover, Casino and GPA delegate the responsibility for monitoring farms to their direct suppliers. For Casino to improve oversight of its supply chain, it would have to monitor risks directly, instead of relying on the efforts of its suppliers. Envol Vert estimates that the farms that supplied to GPA in 2019 were responsible for deforesting 56,000 ha.

Casino and GPA face significant legal and reputational risks amid allegations of incompliance with French law. In September 2020, an international coalition of NGOs and representative indigenous organizations from Colombia and Brazil called on the Casino Group to take all necessary measures to stop sourcing beef from deforested areas and indigenous territories in Brazil, Colombia, and other countries. They submitted a preliminary legal filing under the French law, asking the company to respect its legal obligations by taking necessary measures to exclude all beef linked to deforestation from its supply chain. If Casino does not comply within three months, the organizations plan to refer the matter to the competent court. They also said that they reserve “the right to seek compensation for any resulting damages.”

Business risks associated with deforestation in Group Casino’s supply chains

Potential French due diligence law violations expose Casino and GPA to legal risk

Casino and its GPA subsidiary are exposed to regulatory risk in France. The 2017 French due diligence law imposes unprecedented environmental and human rights duties on all companies operating in France that employ over 5,000 employees in France or 10,000 worldwide, including in the company’s subsidiaries. The law mandates that parent companies identify, prevent, and mitigate environmental and human rights impacts resulting from their activities, the activities of companies they control, and the activities of their subcontractors and suppliers. The law stipulates that companies must publish an annual due diligence plan detailing a risk map, preventive and mitigation measures, an alert mechanism that collects new risks, and a monitoring scheme to assess the implemented measures. Even though Casino has published a due diligence plan, the severity of the violations detailed above exposes the company to litigation risk as parties may judge Casino’s plan inadequate to address environmental risks in its supply chain.

There is a considerable chance that, if taken to court, Casino may lose the legal case over its compliance with the Vigilance Law. While final court rulings on companies’ non-compliance with the Vigilance Law have yet to be announced, the number of parties serving formal notices or bringing companies to court under this law is rapidly increasing. The law has been used in five cases, with two instances so far reaching the courts. All five cases concern companies that, like Casino, already have vigilance plans in place but were deemed unsatisfactory by the requesting parties.

While a legal assessment is required to assess the comprehensiveness and effectiveness of Casino’s vigilance plan, Casino’s exposure to litigation risk is significant when assessed by way of comparison with these five cases:

- The nature of the allegations included the following details:

- They focused on the impacts generated by the activities of the companies and that of their subsidiaries abroad, with emphasis on the fact that “[parent] companies cannot subcontract their responsibilities or outsource their duty of care.” As noted above, Casino largely relies on its subsidiary GPA for deforestation-related duty of care.

- They involved the failure to prevent human rights violations, including indigenous rights, and biodiversity and ecosystem impacts. The four case studies presented in Figure 4 suggest a similar multiplicity of impacts from Casino’s Brazilian operations.

- They noted the insufficiency or absence of stakeholder consultations, as well as the lack of public participation in decision-making processes. Casino’s vigilance plan does not specify which, if any, public stakeholders participated in formulating the plan.

- The companies impact supply chains:

- The companies targeted have influence over supply chains. In the case against XPO Logistics Europe, requesting parties noted that the company “as the economic employer [has] the power and leverage to influence their suppliers and subcontractors and set the standards along their global supply chains.” As the second largest retailer in Brazil, Casino is one of the largest buyers of Brazilian beef products and is exposed to significant deforestation risks in the Amazon and the Cerrado. It therefore exercises widespread influence over its suppliers and the beef supply chain in Brazil.

If Casino loses a legal case, it may be ordered to deploy detailed compliance measures that may force the company to alter its beef supply chain. In the scenario that Casino wins the legal case or delays the judicial process, reputation impacts remain significant. Delaying the process could affect Casino’s demonstrated willingness to comply with the law and undermine its risk perception among investors. If Casino wins the case, it may nonetheless alter its sourcing practices due to pressure from the company’s stakeholders.

Casino and GPA face financing risk

GPA and Casino may be exposed to financing risk as investors call for mitigating illegal deforestation in Brazil. In July 2020, a group of 40 companies and financial sector actors sent a letter to the Brazilian vice president, calling on the government to combat illegal deforestation. Brazilian company CEOs also met with Vice President Hamilton Mourão, asking the government to implement legislation for supply chain tracking. In June 2020, 30 leading financial institutions that collectively hold about USD 3.7 trillion in assets voiced their concerns about the Brazilian beef industry and the possibility of divesting from government bonds and forest-risk sectors if the country does not take action to mitigate the Amazon destruction. As business costs of financing companies linked to the degradation of ecosystems escalate, leading Brazilian retailers – a key outlet for the beef volume sold in the country – may come under increasing scrutiny from investors. A reduced investor risk appetite may lead investors to demand higher returns, increasing the cost of capital.

Concerns about Rallye’s high indebtedness may aggravate financing risks as a result of links to illegal deforestation. In May 2019, Casino parent Rallye entered bankruptcy protection in an attempt to save the group from financial collapse. In November 2019, this observation period was extended by an additional six months. Then, in February 2020, the Paris Commercial Court approved Rallye’s safeguard plans. Rallye pledged Casino shares to creditors as a guarantee for part of its debt. This plan created a vicious cycle, as Casino’s falling share price inhibited Rallye’s refinancing abilities. On April 2, 2019, Moody’s downgraded Casino’s credit rating by two notches to Ba3. Some analysts warn that in its current shape Casino is not investable.

The reputation impacts from perceived legal risk may further exacerbate financing risk for Casino and GPA. Any reputational repercussions from a perceived risk of litigation will likely heighten the companies’ risk perception among investors and further increase cost of capital.

Financial risk assessment: Escalating levels of value risk

The above-mentioned sustainability risks, combined with Casino Group’s financial fundamentals, bring about three levels of risk for investors. These risks include transition risk of its supply chain due diligence process (level 1), financing risk (level 2), and reputation risk (level 3):

- Level 1: Adaptations in supply chain, in line with due diligence law intentions, are needed to be in a best-in-class position.

- Level 2: Apart from the outcome of the legal case, banks and bond investors could demand higher cost of debt if they do not see good execution of due diligence by Casino Group and GPA. The higher cost of capital would affect the profitability and the cash flow of Casino affiliates.

- Level 3: The reputation value of Casino and GPA may be negatively affected. This development could impact the cost of equity and the value of the Casino companies.

Level 1: Legal risk from French Due Diligence Law and cost of adaptation

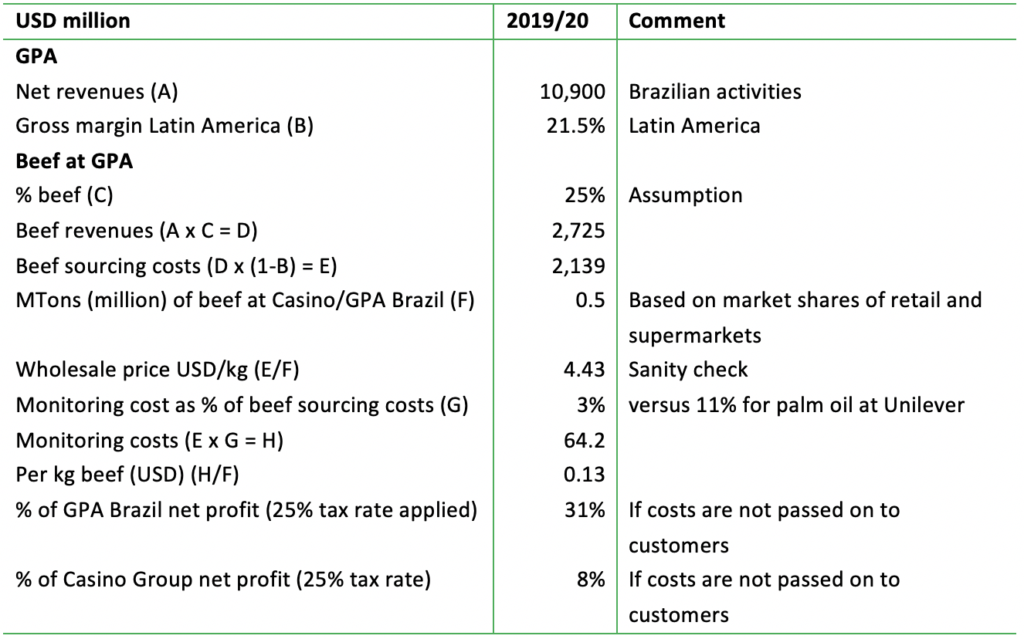

Casino and GPA may face litigation risk due to allegations of incompliance with French law. In the current five cases tied the Vigilance Law, the court may emphasize improvements in policies and their execution instead of giving penalties immediately. Similarly, UK’s Modern Slavery Act has forced companies to improve their procedures and execution of ESG policies. Improved execution of ESG and deforestation policies could lead to extra costs for Casino. In CRR’s report “FMCGs’ Lagging Efforts in NDPE Execution Lead to Deforestation, USD 16-82B Reputation Risk,” the analysis showed that FMCGs had to spend annually tens of millions of U.S. dollars to improve execution and verification in the palm oil supply chain. These costs consist of internal auditing costs, external audits costs, on-site investigation, monitoring by third parties, due diligence, and certified sourcing. The spending per year depends on the volume and value of the sourced material. For Unilever, which currently spends the largest amount in this process in palm oil, expenditures were circa 11 percent of the value of crude palm oil (CPO) sourced.

For Casino/GPA, the total expenditure for better execution of monitoring, verification and sourcing in a sustainable way in the Brazilian beef supply chain will comprise several other cost elements as the beef supply chain differs from that of palm oil. However, various cost elements for auditing, on-site investigations, and due diligence are the same. Moreover, beef sustainably sourced on more expensive, non-deforested land (although certification mechanisms, like RSPO for palm oil, are lacking) would need a premium to incorporate sourcing costs. Assuming that GPA would spend a similar amount annually on improving the beef supply chain that is in line with Unilever’s spending on palm oil monitoring/verification/certification (USD 66 million), GPA would have to spend approximately 3 percent of its beef sourcing costs in order to upgrade in ESG monitoring and verification. Based on 0.5 million MT beef sales, the extra USD 64 million spent would translate to USD 0.13 per kg. The USD total cost is equal to 31 percent of the Brazilian net profit and 8 percent of global Casino Group’s net profit. These percentages are material and could decline if Casino/GPA passes the higher costs onto its customers.

Figure 6: Costs to upgrade GPA’s beef supply chain monitoring/verification to best-in-class

Source: Chain Reaction Research

Level 2: Financing Risk from Bonds and Loans Could Become Material

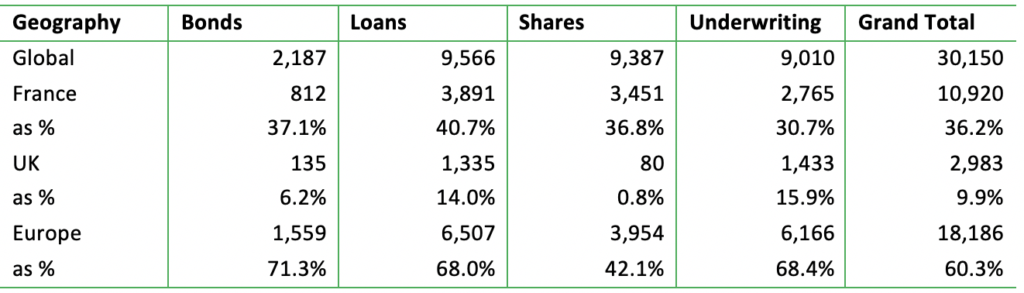

Casino Group and its affiliates could face USD 161 million higher debt financing costs due to two main factors: Conflict with ESG policies of financers and/or ESG regulation by European governments and Casino/GPA’s deteriorating balance sheet and debt ratios. Casino/GPA could face backlash from creditors (bonds and loans) that are affected by national (like the French due diligence law) or upcoming EU regulations. In a broader context, European financers could hesitate financing Casino/GPA because of deforestation links. European financiers, particularly French investors, dominate the financing for Casino and its affiliates. In identified bonds and loans, European investors contribute respectively 71 and 68 percent; in total financing (including shares and underwriting) they contribute 60 percent. The 30 leading financial institutions that collectively control about USD 3.7 trillion in assets and which voiced their concern about the Brazilian beef industry to the Brazilian government control a low percentage of financing, making up only 0.1 percent of the identified total.

Figure 7: Identified financers of Casino Group, GPA and related companies (USD millions)

Source: Chain Reaction Research; Loans: Refinitiv (2020), “Loans, bond and share issuances of selected companies,” viewed in May 2020; Bloomberg (2020), “Loans, bond and share issuances of selected companies,” viewed in May 2020; Investment: Refinitiv (2020), “Shareholdings of selected companies,” viewed in May 2020; Refinitiv (2020), “EMAXX Bondholdings of selected companies,” viewed in May 2020.

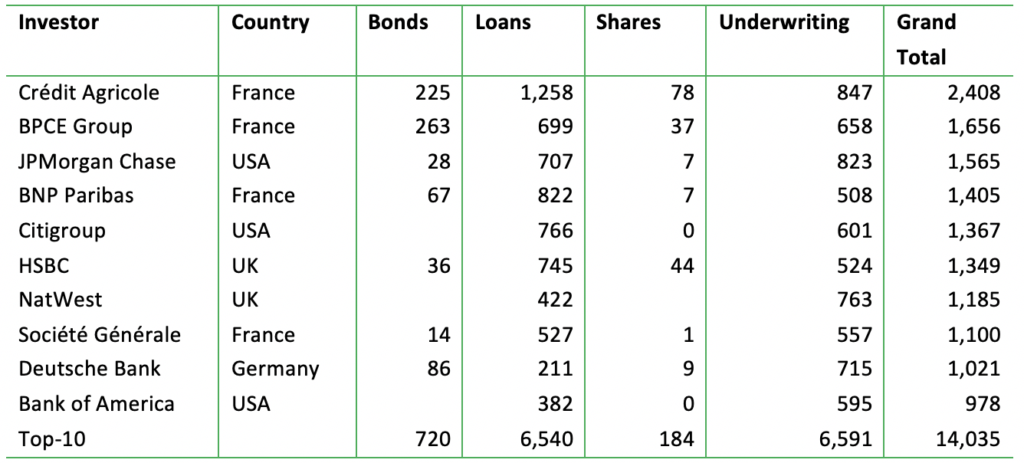

Besides new regulation in Europe, existing financers (shareholders, banks, and bondholders) outside of Europe already face conflict with their forest policies and might demand higher cost of capital or halt refinancing debt. Deutsche Bank (USD 1.0 billion exposure) is a signatory to the New York Declaration on Forests (NYDF). Together with BNP Paribas (USD 1.4 billion exposure), HSBC (USD 1.3 billion), Société Générale (USD 1.1 billion), the NatWest Group, Deutsche Bank is also a member of the Banking Environment Initiative (BEI). It is a signatory to the Soft Commodities Compact and has been committed to No Deforestation, No Peat, No Exploitation (NDPE) starting in 2020. Each of these banks has a variety of policies on deforestation in place, but they also leave significant gaps. In 2019, JPMorgan Chase (exposure USD 1.6 billion), the group company of JPMorgan Asset Management, has released its first climate report based on recommendations by TCFD (Task Force on Climate-related Financial Disclosures). JPMorgan’s policies cover all group activities. The group is also signatory of many other initiatives, including the Consumer Goods Forum, which strives for zero-deforestation.

Citigroup’s forest policies include details on the forestry industry. The bank says that as it seeks “to address the risk of deforestation of high conservation value (HCV) or high carbon stock forests, Citi’s Sustainable Forestry Standard requires robust environmental and social risk assessments for all forestry clients annually.” It also has policies on illegal logging. Through its membership of RSPO, it is committed to NDPE commitments for palm oil. Bank of America’s policies focus on illegal deforestation and on reforestation.

Crédit Agricole, Casino’s largest financier (USD 2.4 billion; Figure 7) implemented a forestry policy for palm oil, although it lacks a holistic policy on deforestation linked to other commodities. BPCE Group is a large financer (USD 1.7 billion) but does not have policies on deforestation.

In the rest of the top 25, several well-known financiers, such as Rabobank, ING, and BlackRock, have become increasingly active in executing deforestation policies and communicating their engagement efforts.

Figure 8: Identified investors’ exposure to Casino and subsidiaries in US Dollars (million)

Source: Chain Reaction Research, Sources: Credit: Refinitiv (2020), “Loans, bond and share issuances of selected companies,” viewed in May 2020; Bloomberg (2020), “Loans, bond and share issuances of selected companies,” viewed in May 2020; Investment: Refinitiv (2020), “Shareholdings of selected companies,” viewed in May 2020; Refinitiv (2020), “EMAXX Bondholdings of selected companies,” viewed in May 2020.

Casino Group’s and GPA’s debt burden is on the rise, exacerbating financing risk

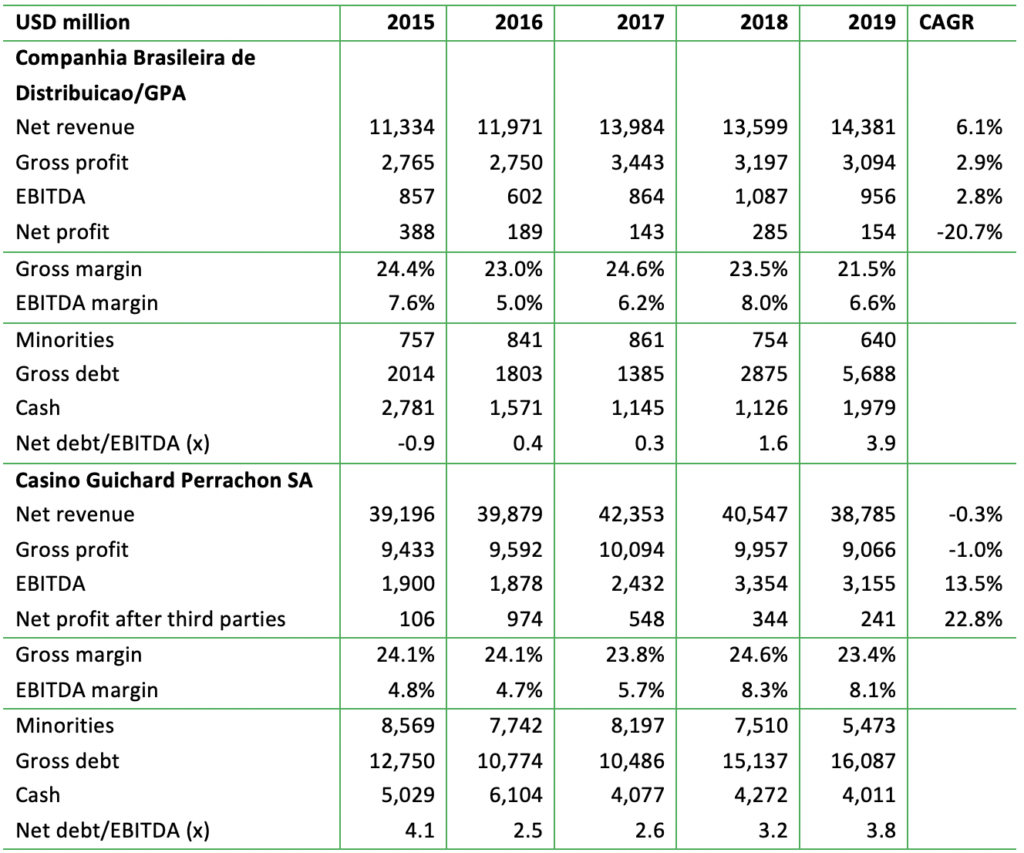

Casino Group’s and GPA’s net debt/EBITDA ratios have deteriorated in recent years. From 2015-19, net revenues and EBITDA saw volatile trends, including scope changes and exchange rate volatility for GPA (Brazilian Real). Both Casino Group and its subsidiary GPA face rising net debt/EBITDA ratios, also due to new accounting principles related to lease commitments. At GPA, the increase is also the result of a new financial structure with the Colombian Almacenes Éxito. Due to consolidation, these changes also affected the Casino Group debt. At the end of 2019, both companies had a net-debt/EBITDA ratio close of 4X, a relatively high level for retailers with exposure in developing markets. Both companies are selling assets to reduce the ratio.

Figure 9: GPA and Casino Group key financials

Source: Chain Reaction Research, Bloomberg

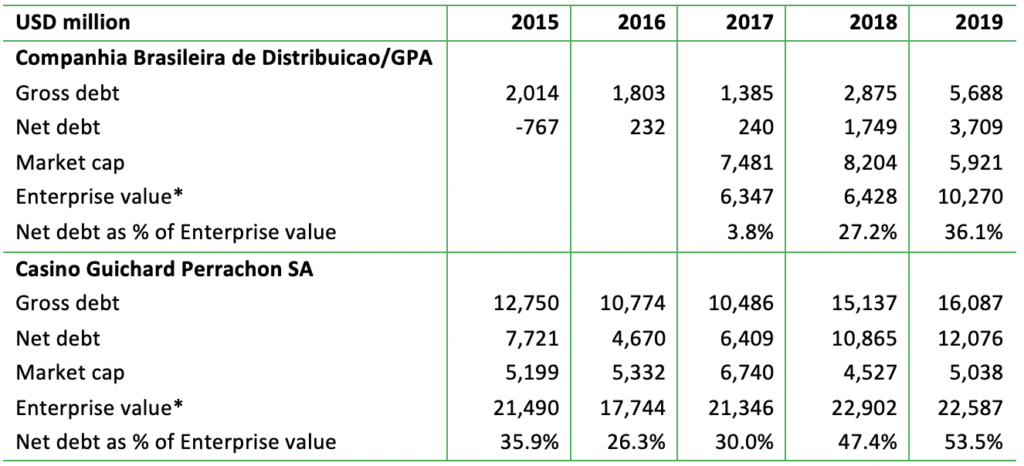

Casino and GPA have become more dependent on debt, which increases engagement opportunities for banks. From 2015 to 2019, GPA and Casino Group gradually became increasingly dependent on debt financing versus equity financing. GPA saw net debt as percentage of its financing value increase from 3.8 percent in 2017 to 36.1 percent in 2019 (Figure 9), before rising further in 2020. Casino Group experienced an increase of 35.9 percent in 2015 to 53.5 percent in 2019. A large part of the identified debt (Figure 7 above) is through loans from financial institutions. Amid the need for periodic renewal of loans, the debt’s relatively large size would enable banks to engage on ESG issues.

Figure 10: GPA’s and Casino Group’s dependence on debt in 2015-2019

Source: Chain Reaction Research, Bloomberg; *Enterprise value consist also of minorities which are not mentioned here.

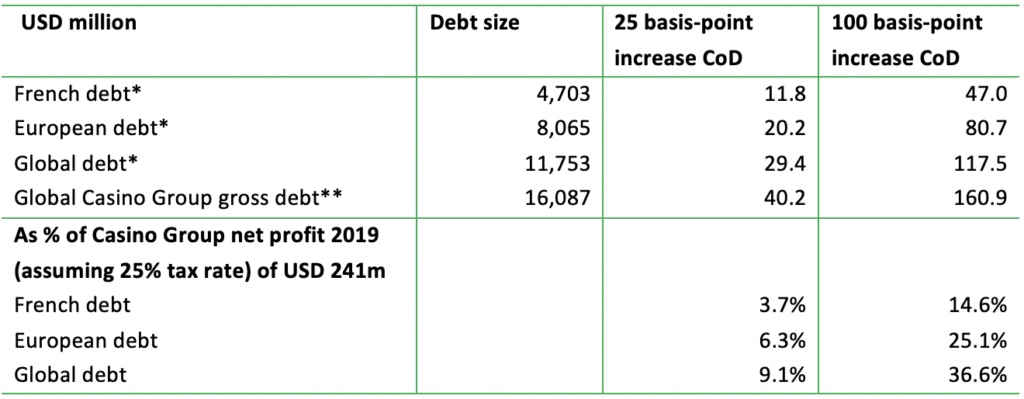

ESG and deforestation policies might raise financing costs by USD 161 million, which is equal to 37 percent of net profit. An increase of 25 basis points of its identified French debt would increase the cost of debt by USD 11.8 million. An increase of 100 basis points in an environment where global debt holders would bring about weak ESG implementation and weak net debt/EBITDA ratios, resulting in a loss of confidence and the cost of debt increasing by USD 160.9 million. Assuming a 25 percent tax rate on interest costs, the financing cost incease could impact net profit by 3.7 percent to 36.6 percent.

Figure 11: Cost of debt (CoD) scenarios (loans, bonds)

Source: Chain Reaction Research, Sources: * Credit: Refinitiv (2020), “Loans, bond and share issuances of selected companies,” viewed in May 2020; Bloomberg (2020), “Loans, bond and share issuances of selected companies,” viewed in May 2020; Investment: Refinitiv (2020), “Shareholdings of selected companies,” viewed in May 2020; Refinitiv (2020), “EMAXX Bondholdings of selected companies,” viewed in May 2020. ** Bloomberg, viewed 14 September 2020.

Level 3: Reputation value could decline further

On top of the higher cash financing costs that could impact net profit, shareholders could lose additional value due to reputation risk. In the report “Deforestation-Driven Reputation Risk Could Become Material for FMCGs,” CRR analyzed that a string of negative reputation news events, along with an inactive social responsibility and non-instant crisis communication, could lead to a 29 percent value decline for shareholders. The outcome could have a limited impact if the activity linked to the reputation event is only a small part of the total business (3 percent, like the famous KitKat case for Nestlé). Figure 11 uses a range of 3 percent to 29 percent. The outcome for the Casino Group seems relatively low compared to GPA amid the current depressed market capitalization of Casino Group. The 29 percent scenario is in line with the outcome of a discounted cash flow (DCF) calculation based on a 100 basis-point increase in the cost of capital. A 100 basis-point increase versus a cost of capital of 7.5 percent would bring about a negative impact of circa 13.3 percent (100/750) on the DCF outcome. If equity is less than 50 percent of enterprise value, equity would be affected by more than 26.6 percent (2 X 13.3) in value, if debt is fully repaid.

Figure 12: Reputation value at risk

Source: Chain Reaction Research; Bloomberg, viewed 14 September 2020.

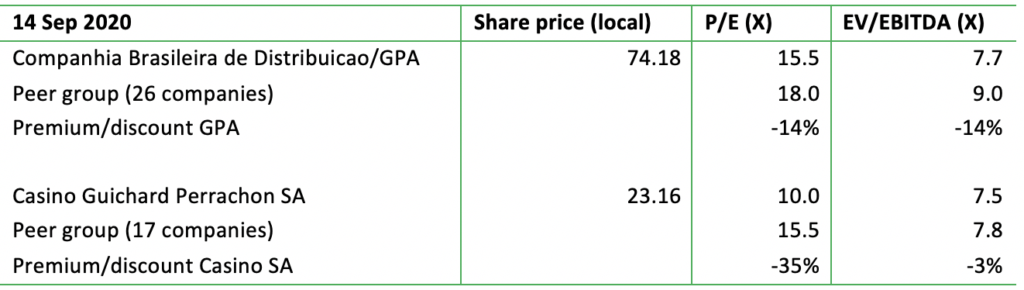

Currently, Casino and GPA’s valuation multiples are already below its relevant peers (Figure 12). These lower multiples for Casino Group and its Brazilian subsidiary GPA have already been affected by continuous disappointing news on various events related to earnings, financial structure, debt levels (including Rallye), and governance. Both companies trade at a substantial discount versus peer groups.

Figure 13: Valuation of GPA and Casino Group versus peers

Source: Chain Reaction Research, Bloomberg; based on Blended forward earnings

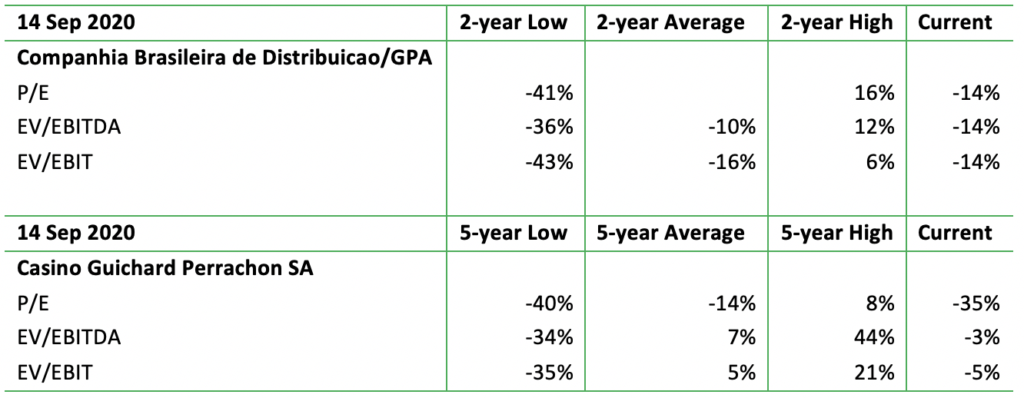

These discounts in valuation multiples could worsen. Compared respectively to two-year and five-year low points of relative valuation, further downside risk could occur for the share price. A reservation is made on the calculation of an exact target share price for the downside potential: in the last two/five year periods the financial structures of both companies have changed due to recent changes in scope and accounting. This makes an analysis based on relative comparisons with historical data less credible. Looking only at the P/E ratio, GPA could face a decline to a relative P/E of -41 percent and Casino Group to -40 percent versus the current positions of respectively -14 and -35 percent. Therefore, the downside potential could be respectively 27 and 5 percent. In EV multiples, the outcomes would be very different, but both would calculate to material downside for share prices.

Figure 14: GPA and Casino Group – Premium/discount of valuation multiples versus peers

Source: Chain Reaction Research, Bloomberg; based on Blended forward earnings

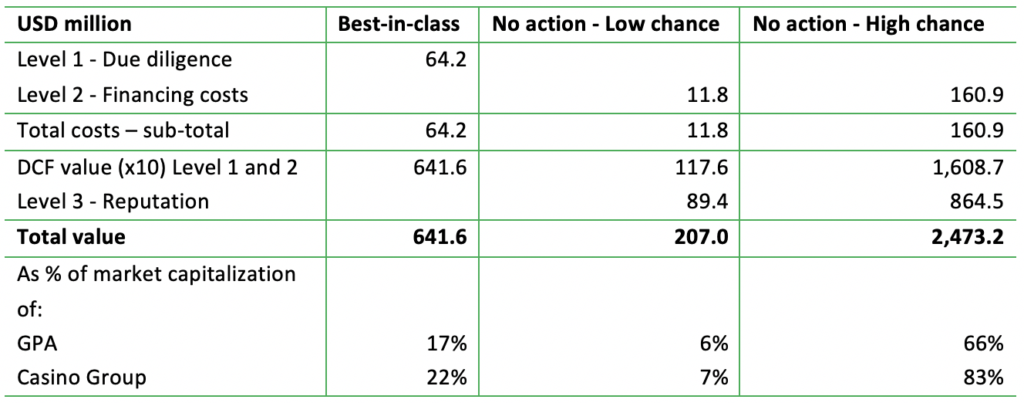

Financial risk summary: A monetary reason for a best-in-class scenario

Casino Group and GPA may face escalating financial impacts through financing and reputation risks. Developing a best-in-class supply chain can lead to costs that are circa 20 percent of GPA’s and Casino’s net profit, if these costs are not passed on to customers. Food retailers usually pass on a large part of cost increases. The financial impact of not taking action on developing a best-in-class supply chain could have a large financial impact, equal to 66 to 83 percent of the current market capitalization. Chances are low that a No-action scenario would not lead to materially higher cash debt costs and limited reputation risk.

Figure 15: Summary of financial impacts in various scenarios

Source: Chain Reaction Research

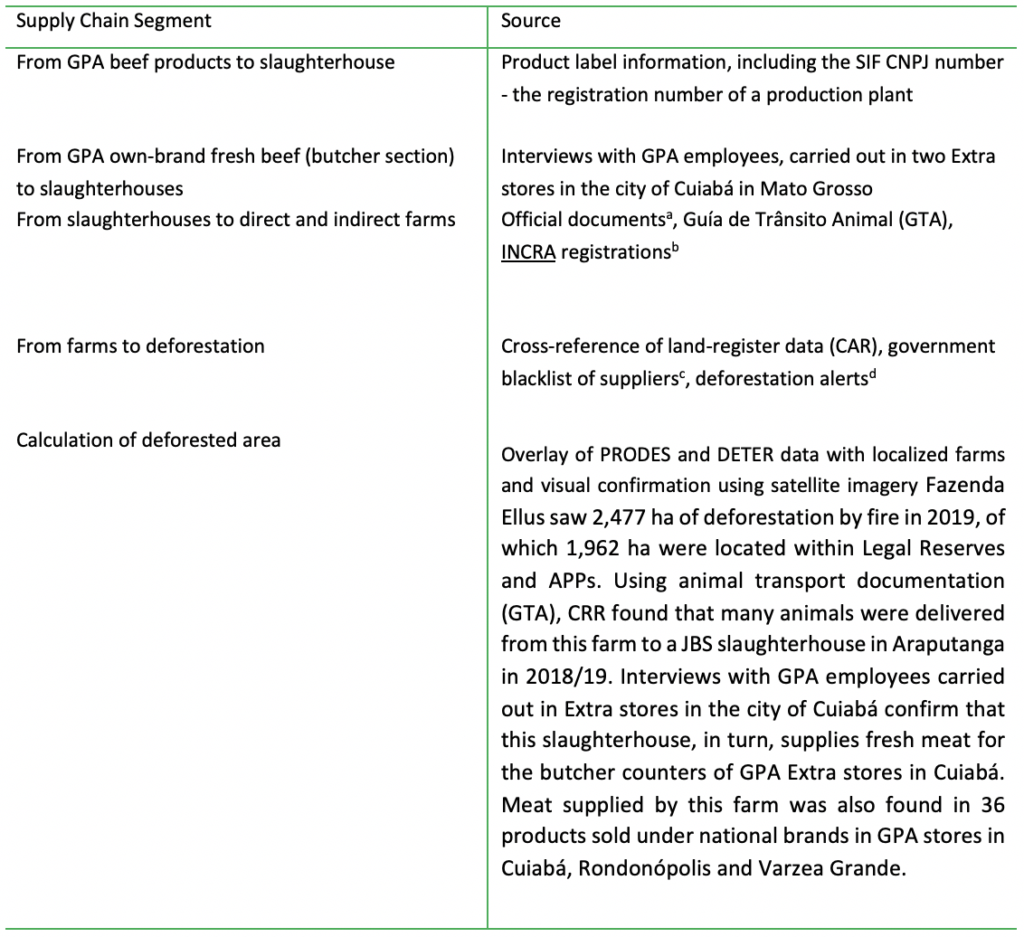

Annex I: GPA’s beef sourcing: Case studies

This annex described the four case studies resulting from the investigations of Envol Vert, Réporter Brasil, and CRR.

The following methodology was used to establish the store-to-farm supply chain links.

Figure 16: Research methodology

Source: Envol Vert report on Casino, 2020. aTo protect sources, Envol Vert did not reveal the exact nature of the documents. bINCRA is the federal government agency responsible for storing various information on all Brazilian rural properties. cBlacklist criteria include slave labor, environmental fines, or areas under embargo. d Including deforestation surveillance systems such as PRODES and Global Forest Watch.

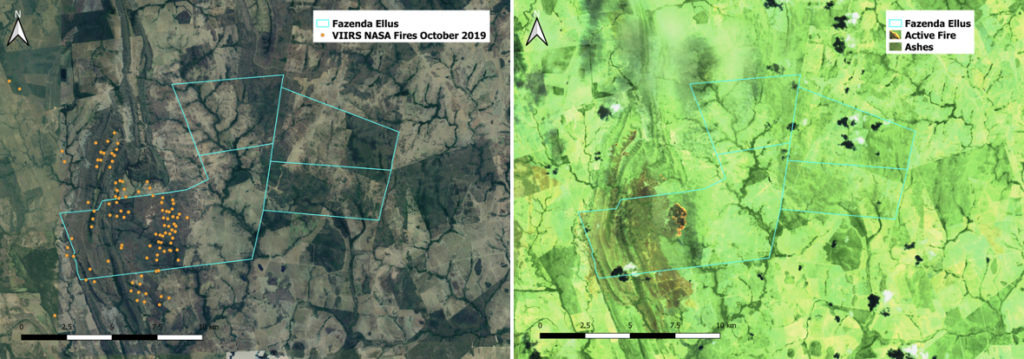

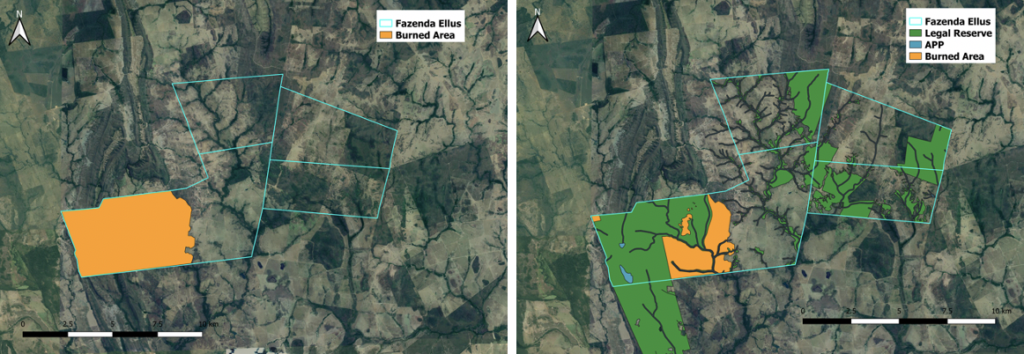

Fazenda Ellus destroys 1,962 ha of Legal Reserves and Areas of Permanent Protection (APPs)

Figure 17: Fires within borders of Fazenda Ellus, October 2019

Source: INCRA, NASA VIIRS Fire alerts (left), INCRA, Sentinel 2 processed imagery (right)

Figure 18: Overlap of area destroyed by fire and protected reserves

Source: INCRA, Sentinel 2 imagery (left), SICAR, INCRA, Sentinel 2 imagery (right) *Reserves include Legal Reserves and Areas of Permanent Protection (APPs).

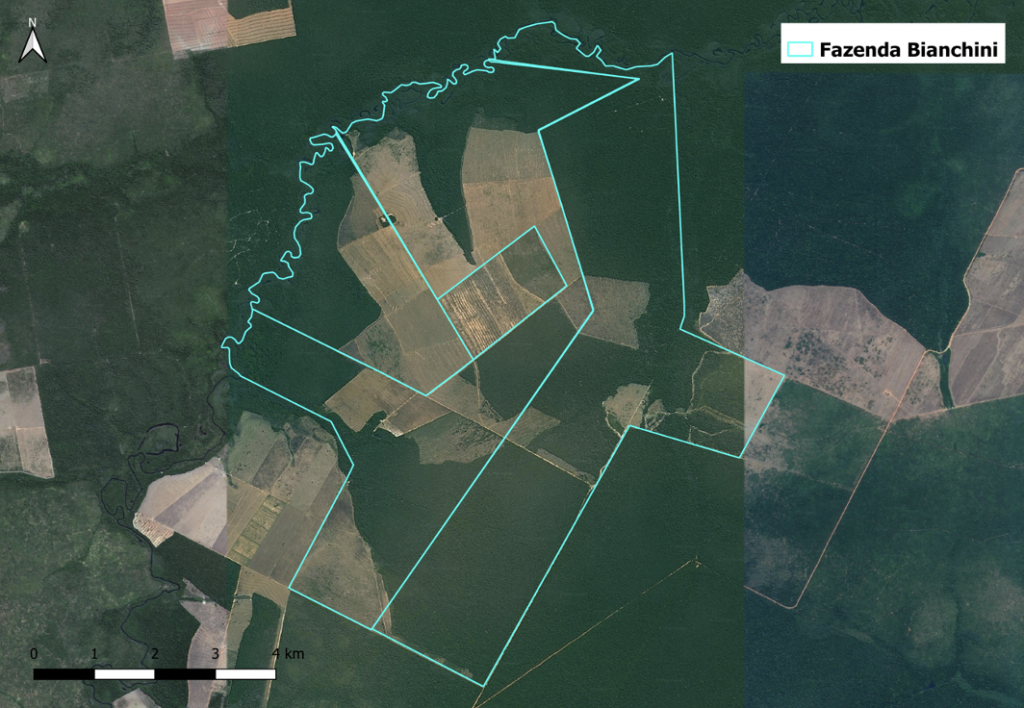

Fazenda Bianchini is involved in “cattle laundering”

Fazenda Bianchini covers an area of 5,562 ha in the heart of the Amazon. It comprises three adjacent areas, each with its separate entry in the rural land registry. Such fractional registration of adjacent rural properties owned by the same landlord is forbidden by Brazilian law. The farm has received a total of USD 5.5 million in fines from IBAMA during the past seven years. Envol Vert reports that environmental violations include illegal deforestation and not respecting IBAMA embargos on the three farms by continuing to graze livestock and prevent the regrowth of vegetation. Envol Vert calculates that a total of 1,171 ha were deforested on the farm during 2012-17.

After the numerous environmental infractions, the property was leased to another farmer to launder cattle. The total area leased was 4,200 ha, including 3,197 ha for pasture. Gustavo Vigano Picoli renamed the farm to Agropecuária GPC. This “new” farm supplied many animals to the JBS slaughterhouse in Diamantino during 2018/2020, which sells fresh meat to GPA’s Extra stores in Cuiabá. Apart from these direct sales, Agropecuária GPC also transferred livestock for fattening to Pedra Farm, a property owned by Mr. Picoli in Sorriso, Mato Grosso. The laundered cattle were then sold to JBS in Diamantino in 2018. These direct and indirect sales from the embargoed farm contravene the obligations of meatpackers under the legally binding Terms of Adjustment of Conduct (TACs) and the G4 cattle agreements. Meat supplied by this farm was also found in 13 products sold under national brands in GPA stores.

Figure 19: Fazenda Bianchini

Source: SIMCAR Mato Grosso

Figure 20: Embargo areas, Fazenda Bianchini

Fazenda Lua Clara in the Cerrado ignores IBAMA embargo

Fazenda Lua Clara sent animals to a JBS slaughterhouse in Diamantino in July 2019 after IBAMA issued an embargo notice for the farm the previous year. As explained above, this slaughterhouse supplies fresh meat to GPA Extra stores in Cuiabá. Meat supplied by this farm was also found in 13 products sold under national brands in GPA stores. An estimated 835 ha were illegally deforested and converted into cattle pasture in this farm during 2015-16. This conversion was conducted without the required legal authorization and is therefore illegal. IBAMA placed the farm under embargo in 2018.

Figure 21: Fazenda Lua Clara

Source: INCRA, Sentinel 2 imagery

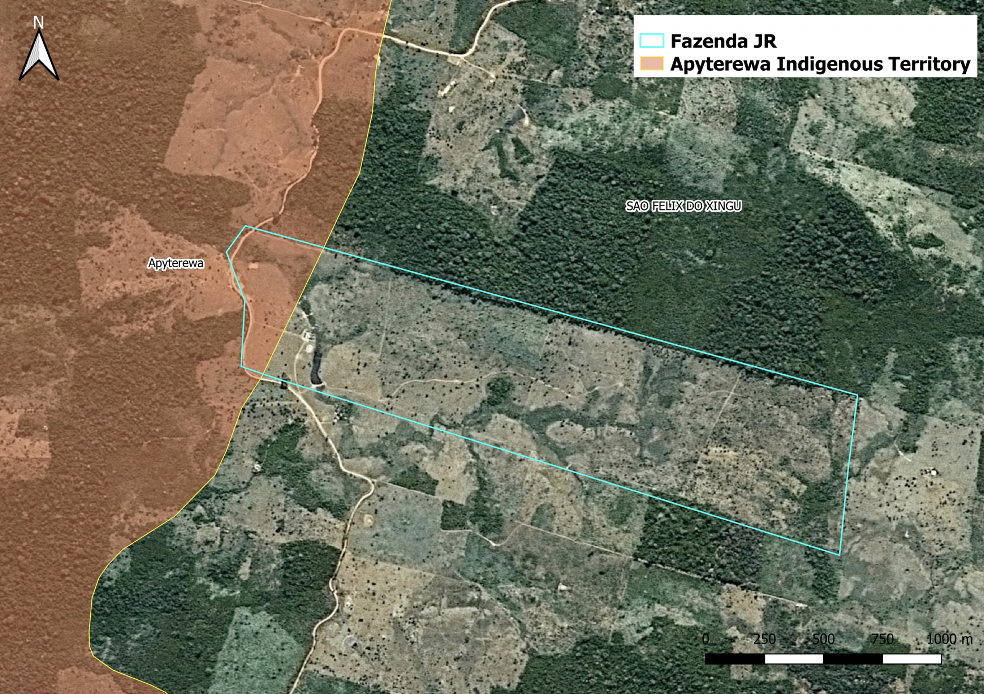

Fazenda JR encroaches the Apyterewa indigenous territory in Pará

Approximately 8.3 percent of Fazenda JR’s farm encroaches the Apyterewa indigenous territory. Between May 2018 and December 2019, this farm supplied livestock to a Marfrig slaughterhouse in Tucuma, which in turn supplied frozen products to a GPA Assaí store in Recife. Commercial cattle ranching is illegal in reserves and indigenous territories, and the TACs commit the meatpackers to not buy cattle from illegally deforested areas, indigenous lands, conservation units, or areas with links to forced labor. Initially limited to Pará, TACs have since expanded to other Amazonian states, including Acre, Amapá, Amazonas, Mato Grosso, Rondônia, and Tocantins. In response to these findings, Marfrig confirmed this transaction as genuine. However, it denied any responsibility and noted the 10 percent margin of error of the mapping tools used to define the coordinates of the farm in question.

Figure 22: Fazenda JR encroaches Apyterewa Indigenous Territory

Source: FUNAI Indigenous lands territories, CAR