Fast Moving Consumer Good (FMCG) companies have increasingly developed zero-deforestation or NDPE policies. Still, deforestation continues to show up in the supply chain of various FMCGs for which palm oil and its derivatives are a material input. Weak monitoring and verification mechanisms at times allow leakage of deforestation-linked palm oil into supply chains and consequently impact the reputation of individual companies. This report analyses the key performance indicators needed to reduce risks and positively impact the reputational value for FMCGs sourcing palm oil and its derivatives. The report estimates the potential costs and, mainly reputational, benefits of a best-in-class approach.

Download the PDF here: FMCGs’ Lagging Efforts in NDPE Execution Lead to Deforestation, USD 16-82B Reputation Risk

REPORT WEBINAR RECORDING

Key Findings:

- Four Key Performance Indicators (KPIs) can help measure leakage risk. The FMCG industry is lagging in deforestation policies and even more in execution. Key KPIs to help reduce leakage are: 1) Presence of an NDPE policy; 2) Up-to-date list of palm oil mills and grievance list; 3) External auditing; and 4) TCFD process and/or CDP Forest disclosure.

- 88 percent of the top-25 FMCGs are lagging in NDPE execution. Eight percent of companies are lagging in all KPIs, while 80 percent have an NDPE policy but are lagging in a semi-annual update of the mill list and/or lack of a grievance list. These include publicly listed companies such as Henkel, Procter & Gamble, Reckitt Benckiser, Kellogg’s, Mondelez International, General Mills, PZ Cussons and BASF.

- There is a large variation in spending on NDPE execution between various FMCGs. Best-in-class execution is a low-cost burden. The cost would be 0.3-0.9 percent of EBITDA and 0.1 percent of palm oil-related product revenues. Moreover, higher costs can be passed on to consumers.

- FMCGs’ misperception of deforestation’s financial impact might be a factor behind low execution spending. The leading eight FMCGs anticipate a value loss based on a discounted cash flow of USD 1.8 billion, but the reputation value-at-risk is 9X to 45X higher at USD 16 billion-82 billion, or 3-15 percent of equity values.

- Investors appear to have ample financial reason to engage with FMCGs to help halt deforestation. FMCGs’ high U.S. dollar exposure to reputation risk combined with their profitable palm oil-related businesses could initiate more collaboration in smallholders’ tree renewal programs.

A recurring problem: The gap between policies and results

FMCGs continue to see a gap between their intentions to halt deforestation and their impact on the ground in Indonesia as well as in Brazil. This gap negatively affects FMCGs’ reputations. In various reports, Chain Reaction Research (CRR) highlights the need for better implementation and execution of NDPE or zero-deforestation policies. A 2019 report on Procter & Gamble, for example, concluded that an improvement in the implementation and monitoring phase, or “the execution,” could lead to extra costs equal to 0.1 percent of its gross profit.

There are ample examples that FMCGs with deforestation commitments are linked to palm oil-driven deforestation in Indonesia and in Brazil. CRR’s semi-annual publication on the top-10 deforesters in Indonesia reveals that large FMCGs with zero-deforestation policies are material customers of implicated plantations. For instance, analysis from February 2020 links Kellogg’s, Nestlé, PepsiCo, Danone, Unilever, and Mondelez International to four or more of these top-10 deforesters. Rainforest Action Network (RAN) found in January 2020 that eight global FMCGs – Kellogg’s, General Mills, Mondelez, Hershey’s, Mars, PepsiCo, Nestlé and Unilever – are involved in a key area of Southeast Asia, known as the Leuser ecosystem, a highly biodiverse rainforest and peatland area on Sumatra. None of the companies were reportedly avoiding deforestation-linked palm oil.

Different FMCGs implement their zero-deforestation policies via different methods. These steps include publishing a policy, signing intention letters (such as the Cerrado Manifesto), joining global platforms like the Consumer Good Forum (CGF), the Roundtable on Sustainable Palm Oil (RSPO) or the Roundtable on Responsible Soy (RTRS), installing internal audit and governance systems, checking through external audits, sourcing certificated palm or soy, contracting third-party monitoring, and planning site visits.

When sourcing of palm oil, many FMCGs rely on information from palm oil traders or refineries that supply them. Food retailers in turn rely on commitments and work of FMCGs supplying branded products. For their private label brands, retailers set up a separate governance channel. In total, retailers’ supply chain is even more complex than the manufacturers’ supply chain because of the high number of direct and indirect suppliers. In case of continuing links to deforestation violations, in particular FMCGs may have to worry about reputation risk, which could impact their market capitalization and their enterprise value. Reputation risk is a financial risk for investors. This report elaborates on the key performance indicators (KPIs) which are essential for companies in narrowing the gap between policy and impact. The report also provides an assessment of costs and benefits of integrating these KPIs.

Recent studies emphasize leakage risk in FMCGs’ supply chain

Various high-level benchmark reports show the shortcomings of FMCGs in establishing forest policies as well as the gap between establishing zero-deforestation policies and proactive execution and verification by FMCGs. Analysis of ESG processes by leading FMCGs confirms leakage of deforestation-linked palm oil, leaving room for increasing transparency on investments in this execution process.

Global Canopy, in its Forest500 Annual Report 2019, says that 140, or 40 percent, of the 350 most influential companies (including retailers) in six forest-risk supply chains do not have any deforestation commitment. Seventy-five (or 21 percent) of the companies have policies on only one of the commodities they source, but not for the others. Moreover, of the 210 companies with commitments, 100 (or 48 percent) “do not report on progress for all implementation, including Unilever, McDonald’s, Nike and Vans owner, VF Corp.”

The Carbon Disclosure Project’s (CDP) 2019 report The Money Trees, the role of corporate action in the fight against deforestation concludes that companies have both an awareness gap and an execution gap. The report included 306 “high impact forests risk” companies that reported in 2018 to CDP’s disclosure platform in 2018. Still, 70 percent of companies asked to disclose on forest risks failed to do so and did not report. CDP offers a list of 30 large companies that, in the period 2016-2018, consistently did not report forest-related information. In the FMCG group, the list includes British American Tobacco, Mondelez, Hormel Foods, PT Indofood Sukses Makmur and Ferrero. Among the companies that reported, 29 percent does not include forest-related issues in their risk assessments. However, nearly all that include forest-related assessments (92 percent) identify substantial risks. CDP identifies an execution gap as follows:

- 24 percent of reporting companies show no or limited action on deforestation, such as not acting on all identified deforestation-risk commodities in their supply chains.

- 75 percent of reporting companies did not report on the potential financial losses from deforestation.

- While 90 percent of retailers and manufacturers have begun implementation, 28 percent of suppliers have yet to do so. This gap could be preventing companies from meeting public commitments.

To improve execution, CDP proposes setting targets (for example, to increase traceability), using certification, engaging with supply chain actors, or taking part in external initiatives to achieve zero- deforestation production.

WWF Palm Oil Buyers Scorecard for 2019 analyzed 173 companies in total in the categories of FMCG, retailers and foodservice. These companies purchased 8.95 million metric tons (MT) of palm oil (>10 percent of global palm oil production), of which 5.21 million MT is RSPO certified palm oil (CSPO). This 5.21 million MT equal around one-third of total CSPO production. At this moment, 19 percent of global palm oil production is RSPO certified, and RSPO has 4,780 members. In WWF’s methodology for scoring companies, they can earn a total of 22 points, of which 16 is related to the own supply chain of companies. Segregated and identity-preserved CSPO scores better than Book & Claim (10 points), and commitments to buy CSPO can earn three points. Companies can earn one point for traceability to mills or plantations, while scope and policies of suppliers account for two points. In line with CDP recommendations for companies looking beyond their own supply chains, WWF adds points for memberships in the RSPO and the Palm Oil Innovation Group (POIG) (2 points) and on-the-ground investments in sustainable palm oil producing areas. The WWF outcomes for the top-24 (Upfield is missing) FMCGs is on average 14.1 (of the 22 points) and range from 5.0 for Lam Soon Cannery to 19.3 for L’Oréal and Ferrero. Most companies still have gaps in their deforestation-free supply chain policies and execution.

Finally, the OECD Pilot Project on Responsible Agricultural Supply Chains in Southeast Asia: Baseline report (2020) found that only few companies have developed comprehensive written policies across “all relevant areas of responsible business.” The research looked into 23 companies active in Southeast Asia, including global FMCGs. Only 29 percent had mapped their supply chains, while the other 71 percent said that high complexity, high costs or lack of internal support were reasons for not acting. Of those that mapped their supply chains, 54 percent said that it was a “significant spend or cost.” Moreover, 35 percent of the companies stated they “always” carry out enhanced due diligence in high-risk contexts.

The OECD concluded that 21 percent of the companies have no verification (or that it was not applicable) on environmental standards, the most relevant factor related to NDPE. For these environmental standards, 21 percent of all companies have written policies on biodiversity and 21 percent on their greenhouse gas footprint. Approximately 50 percent have written policies on waste management, water management, and chemical substances.

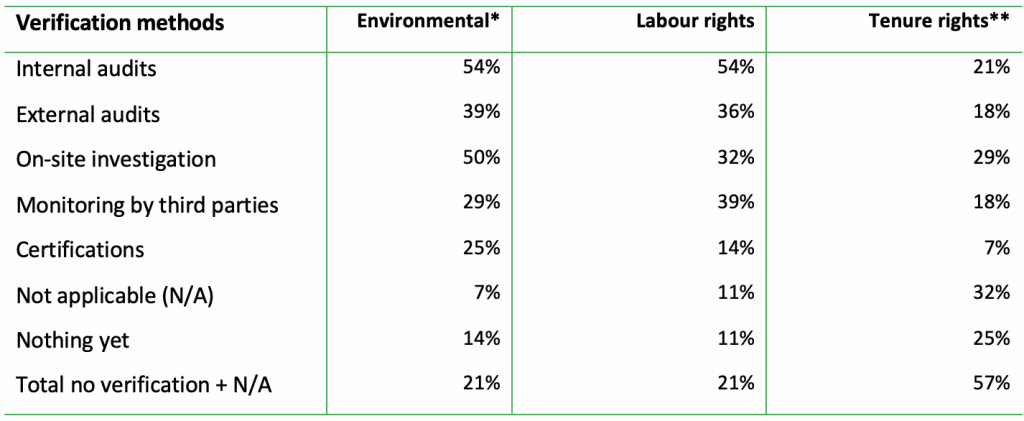

In the verification process, audits are common as 54 percent of the companies have internal audits and 39 percent have external audits. On-site investigations are organized by 39 percent of the companies (see Figure 1 below). The OECD adds that “the key factor for presence of verification appears to be the presence of existing policy i.e. something to verify.” Challenges of verification processes include “the practicalities of verifying actions across large and complex supply chains, made up of sometimes thousands of suppliers operating over multiple locations and countries where national laws and practices can differ markedly.” Moreover, companies do mention the difficulty in finding and using verifiers and lack of trained personnel. Another key finding by the OECD was that a number of companies stressed that the acceptance of the plan by stakeholders outside the direct control of the company, for instance Tier 1, Beyond-Tier 1 business partners and other external stakeholders, made up the major challenge in the adoption of risk management plans. This challenge was critical to the implementation of actions under the plan.

Figure 1: OECD – Use of verification processes across issue-specific standards

Source: OECD Pilot Project on Responsible Agricultural Supply Chains in Southeast Asia *Environmental protection and sustainable use of natural resources; ** Tenure rights over and access to natural resources

Large FMCGs have the potential to lead the transformation to a zero-deforestation outcome. Reports from the CDP, WWF and OECD form the basis for further research on how these leaders have structured their processes to reduce leakage and how the trade-off between cost and benefits is handled. For instance, the OECD does not indicate costs for the various steps and its query did not include the frequency of, for instance, on-site investigations. For its part, the WWF ranking methodology weighs heavily on the process of CSPO certification. A fully segregated supply chain is desirable, especially for FMCGs which source palm oil indirectly. However, a fully segregated supply chain does not necessarily exclude leakage of deforestation-linked palm oil. Using opaque and complex corporate structures, even among palm oil producers with NDPE policies, has hidden links with controversial assets and deforestation.

The Key Performance Indicators (KPIs) for NDPE Execution

As companies and investors look to prevent financial losses, four key performance indicators could be crucial to reduce risk, increase return on their investments, and protect their reputation value.

Based on CRR interviews with investors and experts in NDPE execution in the palm oil chain, FMCGs and their investors could apply the following four KPIs to reduce leakage risk in their sourcing and investments respectively:

- NDPE policy in place: Yes or No.

- Transparency of an up-to-date supplier/palm oil mill list: Yes or No for a semiannually updated mill list would show positive behavior by FMCGs as traders update every quarter. In the case of materiality for FMCGs, due diligence of the suppliers is necessary – a grievance list is a proxy for this.

- External auditing: Yes or No. In the future, investors and FMCG customers could increasingly value the presence of an independent check or a “second opinion.” A third-party auditor would use instruments like regular site visits and landscape verification.

- An additional tool for investors is the presence of non-financial reporting according to the TCFD (Task Force on Climate-related Financial Disclosures) process and/or up-to-date disclosure in an established format such as “CDP Forest.” If this occurs, including an in-depth analysis of “Cost of Response” and “Quantitative Risks,” FMCG’s work processes and employees would be adopting a sustainable route for palm oil. For instance, Unilever puts the total cost of response at EUR 60 million, which is substantially higher than costs estimated by other FMCGs.

These four KPIs distinguish the quality of the implementation process internally through indicators 1 and 2, and the additional external control through indicators 3 and 4.

KPIs: NDPE policy, up-to-date mill list and grievance list

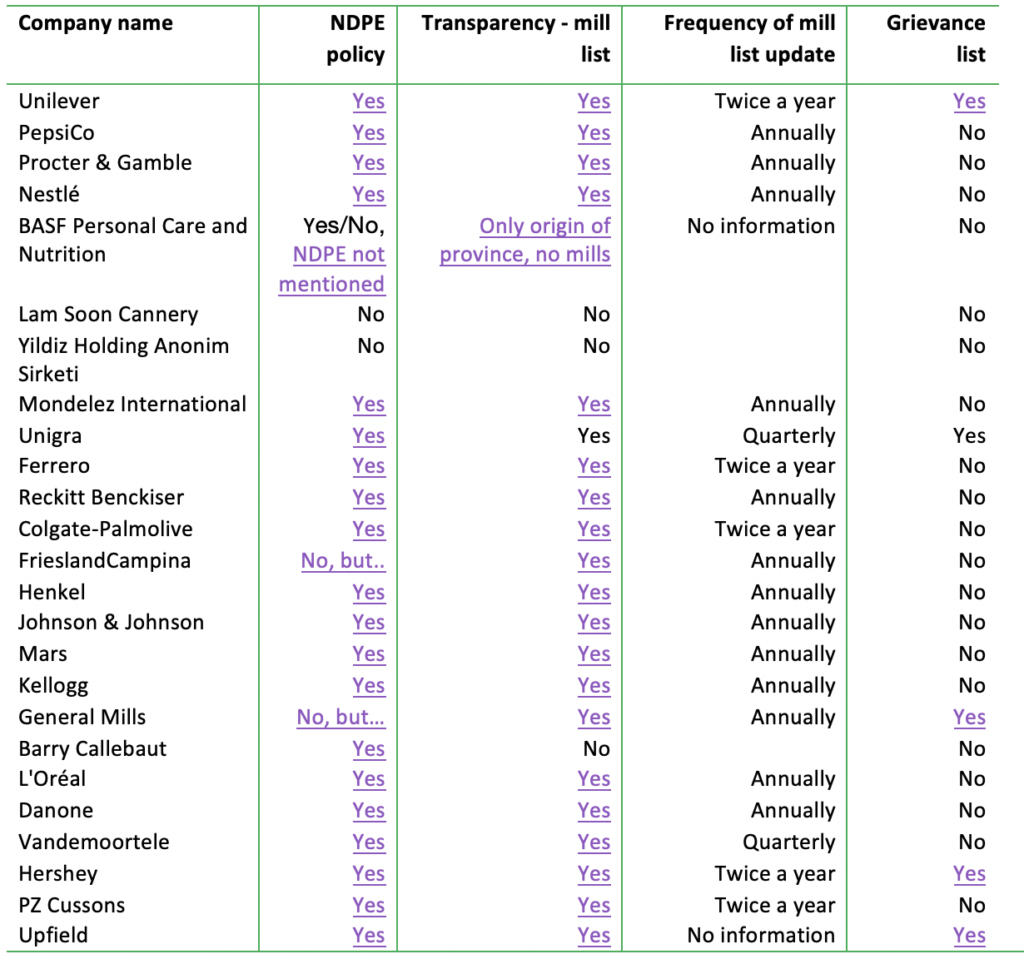

The top-25 palm oil sourcing FMCGs listed below are buying 9 percent of the global palm oil production (the order in Figure 2 is based on sourced volumes: see appendix). Most companies are publicly listed, but a small group is privately owned (Ferrero, Yildiz, Unigra, Mars, Upfield) or is a cooperative (FrieslandCampina).

Figure 2: KPIs on NDPE Policy, mill list, frequency of update, and grievance list

Source: Chain Reaction Research, Aidenvironment, based on public information including websites; the order is based on sourced volumes

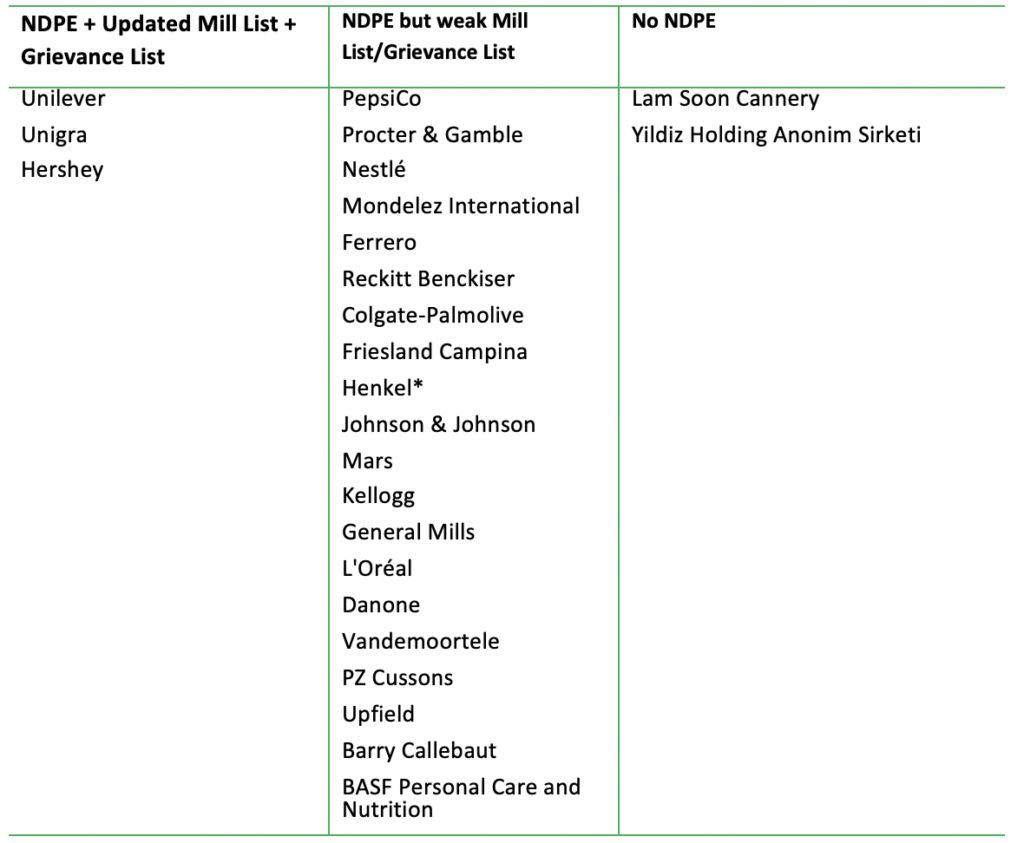

Figure 3 shows that a small leading group has NDPE policies, mill lists updated every half year, and grievance lists. A second group has NDPE policies, but they lack regular updated mill lists or grievance lists. This group is large and contains major FMCGs which face reputation risk or financing risk if their processes do not improve. Finally, another group includes companies with no NDPE policies and/or no mill lists and no grievance lists, signaling that they will likely have to conduct major overhauls in order to reduce risk.

Figure 3: Summary of KPIs in NDPE, Mill list and Grievance List*

Source: Chain Reaction Research, company websites. *Henkel commented that the palm kernel supply chain creates more complexity than the palm oil supply chain and that this impacts its KPI outcomes.

KPIs: External Auditing and Published Risk Analysis

While no standard yet exists for external auditing process in NDPE for financial information, publicly available information can be used to evaluate the integrity of the execution. Independent landscape research, TCFD, or CDP Forest disclosure provide insight into the quality of processes.

An external audit is an examination that is conducted by an independent accountant. This type of audit is mostly intended to certify financial and non-financial statements of an entity. This certification is required by external stakeholders that have invested money in a company. Unilever provides an example on how extensive this certification can be executed.

In financial reporting and auditing, certain processes (including governance), along with financial data and ratios, are crucial and can be checked in a standardized way. In non-financial reporting, the Sustainability Accounting Standard Board (SASB) gives definitions specifically for agricultural commodities and palm oil. It also provides guidelines on how to discuss deforestation risks. These provide infrastructure for reporting on TCFD and the EU’s NFRD (Non-Financial Reporting Directive) for specific climate-related disclosure processes, which may give details on impact of deforestation. The initiatives are still voluntary. The outcomes (or absence of them) offer opportunity to compare FMCGs and provide investors a guide for engagement when considering questions to discuss with companies regarding financially material issues. For instance, Unilever has an extensive description of its TCFD process.

An additional tool for an independent judgment of FMCG exposure to forest-risk commodities is the CDP Forest disclosure. It provides details of risks identified with the potential to have a substantive financial or strategic impact on businesses, and companies’ response to those risks. Also, for the selected forest risk commodities, CDP provides details of the identified opportunities with the potential to have a substantive financial or strategic impact on a business. CDP rates the specific commodity policies from A (good) to F (absent).

A large group has not replied to specific requests by the CDP. However, several companies provide insight into the costs of responses to specific risks. Of the companies in the left column (the “good” executors in KPI 1 and 2) of Figure 3, Unilever has independent auditing and up-to-date TCFD and CDP reporting. Meanwhile, Unigra is not in the CDP list and, since it is a private company, also feels less pressure for a TCFD approach. External auditing cannot be found. Hershey does not show an external auditing process and reached only a B- rating in the CDP Forest disclosure.

On the other side of the industry, Lam Soon and Yildiz, which are the companies with no NDPE policies and no palm oil mill and grievance lists, the question on external auditing is not relevant.

The large group of companies in the middle column of Figure 3 still has room to upgrade NDPE implementation processes. Of this list of 20 companies (80 percent) that need to improve on the first two KPIs, 12 (or 48 percent of the top-25) did not receive an A rating by CDP or did not submit information. They are also lagging in the external/independent rating process:

- B, or lower rating: Reckitt Benckiser (B), Henkel (B-), Kellogg’s (B), General Mills (C)

- No rating, not in CDP Forest, or did not fill in (F): Procter & Gamble, Mondelez International, Ferrero, Vandemoortele, PZ Cussons, Upfield, FrieslandCampina, BASF Personal Care and Nutrition.

Of these 12 companies, four are privately owned (Ferrero, Vandemoortele), cooperative (Friesland) or owned by private equity (Upfield). The other eight companies are publicly listed, and their shareholders in particular could be negatively affected by material reputation risk.

For these companies, the TCFD implementation and/or the external/independent auditing initiatives are as follows:

- Reckitt Benckiser’s TCFD does not include a specific mention of palm oil and deforestation risk. Its ISAE 3000 external check mainly covers the process of working out the policy on paper, but is not specific like the ISO 26000 (sustainable business), and does not check deforestation on the ground. Reckitt Benckiser is active in a palm oil monitoring project in Brazil with PZ Cussons, Earthworm Foundation and Airbus, monitoring the palm oil supply chain through real-time satellite technology.

- Henkel has no TCFD approach, but it does have undergo external auditing of its sustainability processes through KPMG. This includes a risk analysis consisting of a media search on performance. However, no specifics on palm oil or deforestation auditing are mentioned in this process.

- Mondelez International has introduced a TCFD Alignment Index, first published in 2020 for the financial year 2019. The company has made disclosures in the context of the CDP Climate Report. The company says that it uses external auditors to monitor its compliance, but provides only the detail that “external experts include World Wildlife Fund, Quantis and various investment groups.”

- Kellogg’s does not appear active in a detailed TCFD process, and no information can be found on external auditing on specifically palm oil or deforestation.

- General Mills is starting to implement TCFD disclosures. It has external auditing for its factories, but not of its supply chains. General Mills has reached an A- rating in its CDP Climate application, but there are no details on palm oil, even upon request from CRR.

- Procter & Gamble has no TCFD or independent auditing process of its palm oil deforestation risk. In 2019, a Chain Reaction Research report concluded that the company has a weak NDPE implementation.

- PZ Cussons relies for external control on Earthworm Foundation, and the company’s TCFD could not be found. The company is using satellite technology to monitor and independently verify its suppliers’ commitment to protecting forested areas. This activity is through the program mentioned in the bullet on Reckitt Benckiser (see above).

- BASF achieved an A- score in the CDP reporting on climate protection (not on forests). No other initiatives on independent verification can be found.

Barry Callebaut has a special position but is lagging in NDPE execution. It has no mill list and no grievance list. It has filled in the CDP Forest disclosure and has received a high A- rating for its palm oil implementation. The company invests USD 2.1 million in the GPS mapping of its farmers (for all forest-related commodities, not only for palm). It sees USD 72.6 million as reputational and market risk, which is calculated under the assumption that 1 percent of its revenues could be lost.

Financial costs for FMCGs of a strong NDPE policy execution

The assessment of the costs of a best-in-class execution method provides an important input to evaluate the “trade-off” between execution costs and reputation value of FMCGs. The costs represent 0.3-0.9 percent of FMCGs relevant EBITDA and in the palm oil value chain these costs are only 0.1 percent of the relevant revenue of FMCGs.

The bullets below provide a summary of a cost analysis based on annual reports, information from internet, and interviews with businesses active in verification. The classification of the OECD from Figure 1 is used. These six OECD activities seem more extensive than the four KPIs, but the KPIs are in turn all included in the OECD process.

- Internal auditing costs: ten to several hundred thousand of US Dollars.

- External audits costs: ten to several hundred thousand of US Dollars, at most.

- On-site investigation: tens of millions of US Dollars, in case of materiality (at most tens of thousands per site).

- Monitoring by third parties/due diligence/collective: tens of thousands to one million US Dollar.

- Blockchain and other technologies: These solutions can reduce existing administration costs.

- RSPO-certified palm oil: Buying certified palm oil might cost USD 30 per metric tonne (MT), or a premium of more than 5 percent. This cost is related to the costs for palm oil producers which pay at least USD 8-12 per MT to gain certification, excluding additional expenses from audit fees, logistics, and environmental assessments.

The total costs of a total monitoring and verification process per company would exist of a fixed cost for certain elements, and variable costs. The costs will partly vary depending on the total tons of CPO, PKO and derivatives it is sourcing and on the number of plantations from which it is sourcing.

The current expenditures by FMCGs shows wide differences per company

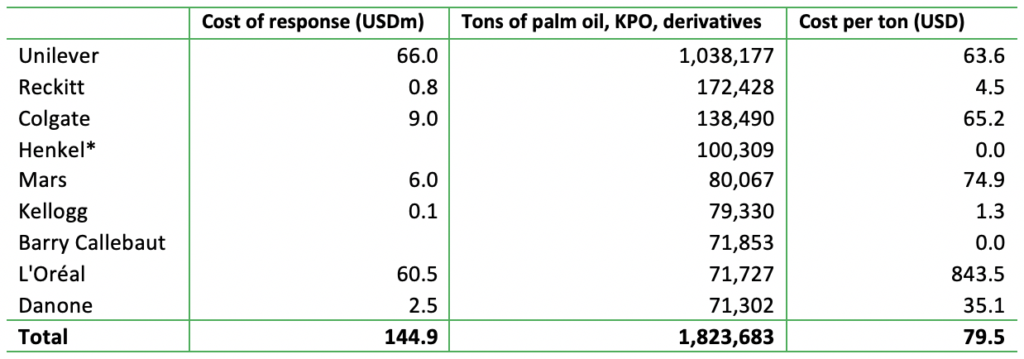

The CDP Forest disclosure provides insight into expenditures by FMCGs. Unilever’s cost of response is by far the highest, but per ton (including palm oil, KPO and derivatives) Mars and L’Oréal spend more. Unilever spends USD 70 million when other forest-risk commodities are included. Unilever’s annual cost of USD 66 million in palm oil represents both the purchase of certified materials and its investments in programs throughout its supply chain.

L’Oréal’s cost of response is USD 60.5 million. It includes USD 6 million one-off capital costs from environmental impact reduction efforts; costs of implementation of the group’s zero-deforestation policy, such as the annual cost of RSPO certification, the annual cost of projects management, a one-off cost for suppliers’ support, mainly on traceability and consulting costs; and one-off experimentation and sponsoring costs. Additionally, it includes the cost of sustainable sourcing, but this could be double counting by the company. Excluding average CPO costs of USD 600 per MT, USD 243.5 per MT would still be high.

On the other hand, Kellogg’s seems to spend only USD 1.30 per ton. The company says that it engages with its suppliers in its supply chain on traceability to promote best management practices and encourage certified production. Through its partnership with the NGO Proforest, Kellogg’s says it works with each palm oil supplier to report on their global traceability to mill and plantation and publicly share their action plan to achieve these goals bi-annually. For Danone, the USD 2.5 million represents five percent premium prices for certified palm oil (products), but the company does not specify other costs. Reckitt Benckiser’s cost of response is USD 0.8 million funding for its participation in a program with Earthworm, which is focused on preventing deforestation in the upstream part of the supply chain. The costs also include Reckitt Benckiser’s internal resources and programs used to support its participation and associated internal management and reporting processes. This cost is annual and ongoing.

Overall, the CDP disclosure on cost differ substantially between companies. Some include the premium paid for certified commodities, while others do not. As a result, numbers are not comparable and also lack transparency.

Figure 4: Cost of response in forest risks related to palm oil; selection of FMCGs*

Source: Chain Reaction Research, CDP Forest disclosures. *Henkel commented that the palm kernel supply chain creates more complexity than the palm oil supply chain and that this impacts the outcomes.

Expenditures by FMCGs might need to increase to USD 65 per ton, at least

Expenditures by Unilever, Colgate, and Mars (Figure 4) all vary in the range of USD 63-75 per MT, which is more than 10 percent of the CPO price per ton. These costs cover probably largely the indicative cost lines for all auditing, certification, and part of the on-site investigation given in the bullets above. Of these companies, Unilever appears to have its verification in order, while Mars is lagging in actualizing its mill list more often and establishing a grievance list. Meanwhile, Colgate has yet to establish a grievance list. The expenditure of Henkel, Kellogg’s, Barry Callebaut, Reckitt Benckiser, and Danone are lagging. That is also likely the case for companies that do not report on financial risks and cost of response, which makes up the majority of the group.

How do these costs compare to verification in other industries? Currently, banks are active in creating more robust monitoring and verification in an ESG-sensitive supply chain as a core activity of bank services. For instance, Dutch banks are investing heavily in the expansion of anti-money laundering departments. The largest Dutch bank, ING, faces regulatory costs higher than USD 1.1 billion in 2019 (USD 1.04 billion in 2018). In anti-money laundering only, the company employed 4,000 people globally. Other banks also hired thousands of anti-money laundering FTEs. However, money laundering is a criminal activity that potentially affects the core business of a bank, while “legal” deforestation by palm plantations impacts only part of an FMCG’s business.

New initiatives could impact the future expenditures by FMCGs in monitoring supply chains. For instance, the Sustainable Trade Initiative IDH is developing the Verified Sourcing Area (VSA) approach. The model looks beyond individual supply chains to address systemic sustainability issues across sourcing areas. The initiative would also be cost-efficient. Pilots are ongoing in Indonesia, Brazil, and Vietnam. This initiative follows an earlier report with proposals to team-up and scale-up existing landscape verification systems. These systems would replace internal standards and/or certification. Examples of existing tools include Trase, Mato Grosso’s state monitoring via the PCI Monitor, and solutions provided by private-sector actors like ChainPoint. ChainPoint is active in supply chain mapping, traceability, audit management, supplier assessment, and blockchain.

Regarding high costs of palm oil verification, some recent developments may in fact reduce costs for FMCGs and improve their reputation at the same time. An interesting example is blockchain. An increasing number of FMCGs is trialing blockchain to provide consumers insight on the origin of a product. For instance, Danone is using blockchain in its Track & Connect service for some of its infant nutrition brands. The combination of blockchain, serialization and aggregation technology, together with QR codes, is supporting traceability “from farm to fork.” This technology may sound revolutionary, but it is mainly a technological solution to make the well-known tracking & tracing more cost-efficient. Although the tool itself does not solve the problem of deforestation, it can improve the reputation value of an FMCG.

The execution costs of USD 65 per MT – a relatively low burden for FMCGs – leave profits intact

The execution costs of an NDPE policy by FMCGs are less than 1 percent of FMCGs profits on palm oil- related products. This (extra) costs can be easily passed on via higher sale prices.

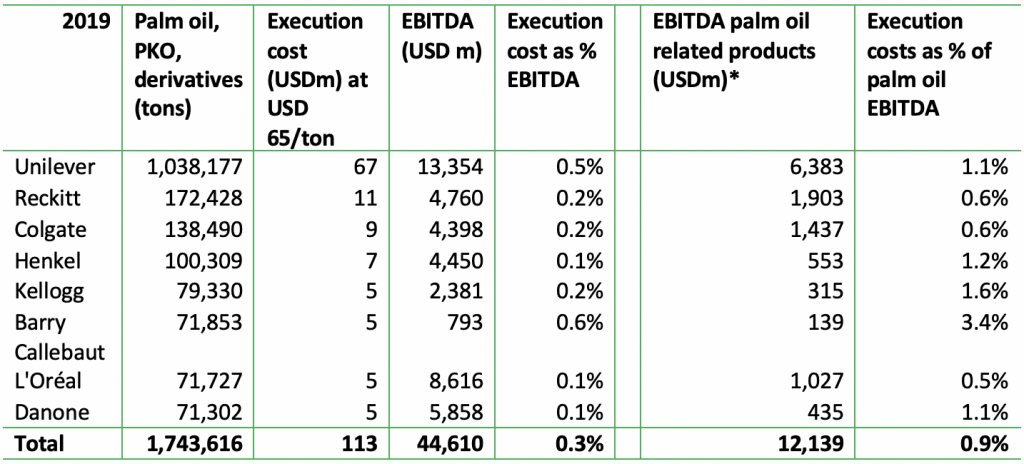

The USD 65 per MT implementation and execution cost is more than 10 percent of the COP price per ton. This level would result in a total of USD 113 million for a selection of eight FMCGs, or 0.3 percent of their total EBITDA (earnings before interest, tax, depreciation, and amortization). The costs of USD 113 million represent 0.9 percent of the USD 12.1 billion EBITDA of palm oil-related products.

Figure 5: FMCGs – Palm oil NDPE execution costs versus the relevant earnings number

Source: Chain Reaction Research; * based on calculation of palm oil cost X 25 = costs of palm oil related product (CoPOrP). This CoPOrP as % of total cost of sales X global EBITDA = EBITDA palm oil related products. The Procter & Gamble case study is a basis for this. See Figure 6

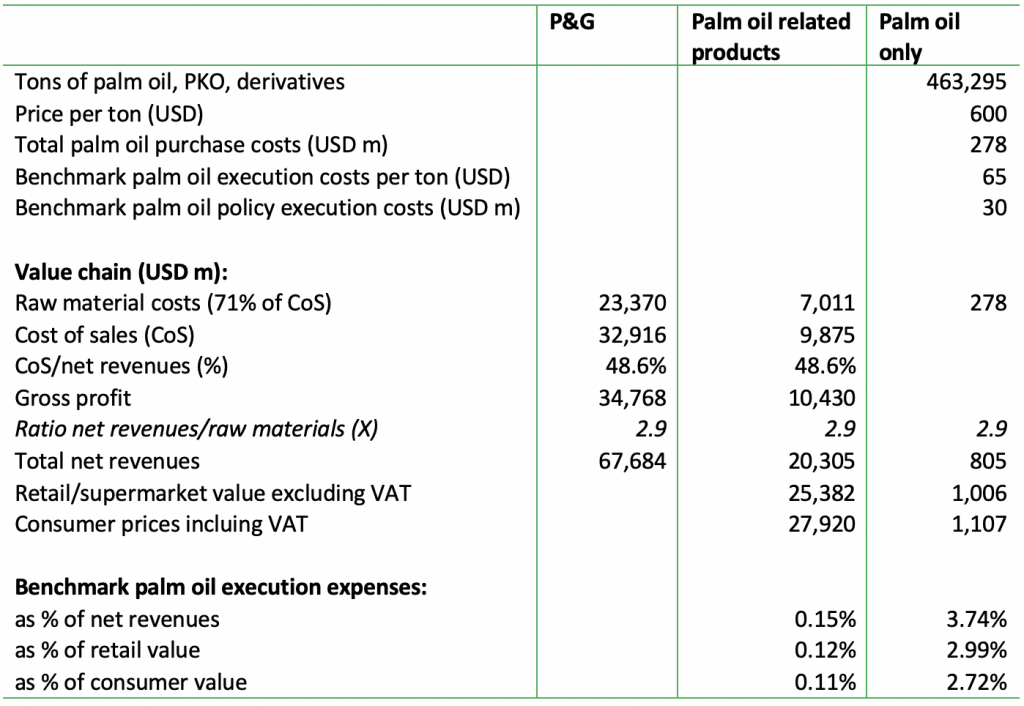

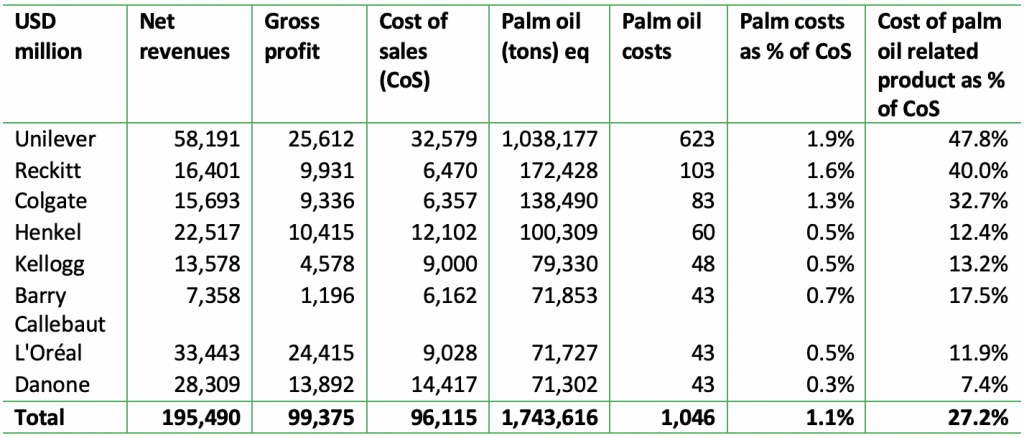

Procter & Gamble (P&G) – not in the list above as it gave no specific costs data – indicates that 20-40 percent of its revenues are dependent on palm oil. Cost of sales (including cost of factories and distribution) accounts for 49 percent of revenues. Unilever provides further details, noting that raw material costs are 71 percent of its total cost of sales. P&G’s total palm oil purchasing volume multiplied by price per metric ton adds up to USD 278 million. Thus, palm oil costs account for only 4.0 percent of raw material costs of palm oil-related products (USD 7,011 million; see Figure 6).

Looking to the entire value chain, the multiple of input cost to output price is 2.9X for P&G (italic in Figure 6). In retail, the mark-up is another 25 percent. The same is assumed for palm oil-related products. Applying the 2.9X for palm oil costs to output costs and the mark-up to retail price, the value chain value for palm oil would be USD 805 million excluding retail, and USD 1 billion including retail. The USD 30 million benchmark execution costs for P&G (see Figure 6, fifth row) would be 3.0 percent of the palm oil value chain and only 0.12 percent of the value chain of the products which include palm oil (see last two rows in Figure 6).

Figure 6: Procter & Gamble – Palm oil NDPE execution costs and a value chain analysis

Source: Chain Reaction Research, P&G Annual Report FY2019, Unilever Annual report FY2019

Barry Callebaut indicated that profit margins might not be affected by higher sustainability execution costs. In the context of its activities to make its cocoa supply chain more sustainable, the company said it would be able to pass on the higher costs to customers. There would only be an impact on the balance sheet. This impact is related to higher inventory costs (certified products at stock are more expensive than not-certified material) and negligible on debt and on net profits.

Value-at-Risk due to Weak NDPE Policy Execution – Misperception by FMCGs

FMCGs underestimate the potential negative value impact of a weak NDPE policy execution. The necessary additional expenditures for a stronger NDPE policy execution are relatively small versus the potential loss of reputation value.

FMCGs own assessments of financial impacts from palm oil risk valued at a couple of billion US Dollars

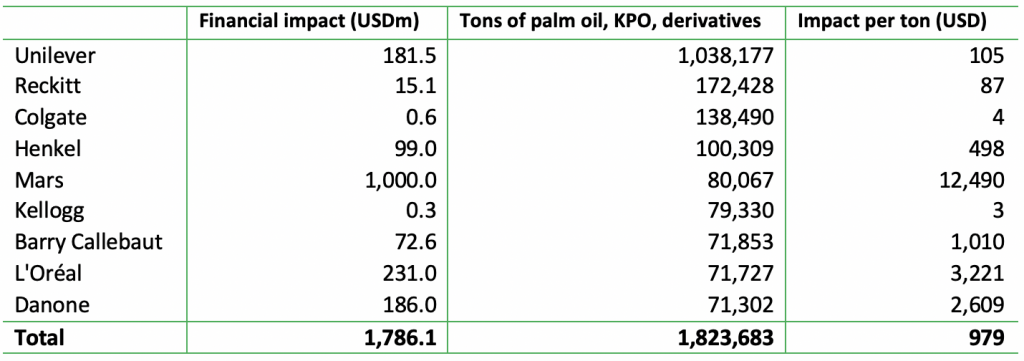

The outcomes in Figure 7 vary widely as they are based on different methodologies and different risk assessments by various companies:

- Mars expects the largest financial impact from forest risks related to palm oil. The USD 1 billion estimate includes only the European business risk, as consumers in this market are the most sensitive to sustainability concerns.

- Unilever calculates palm oil’s financial impact in the range of USD 109-182 million. This number assumes losing some clients and product sales if non-compliant palm oil is used, impacting sales by 3-5 percent. Implicitly, Unilever sees only USD 3.6 billion product value related to palm oil, versus USD 20 billion for P&G, while Unilever generates USD 32.7 billion net turnover in personal care, home care, and food products that contain palm oil.

- For its part, L’Oréal uses another risk calculation. The company distinguishes sourcing risk and market access and reputation risk. Sourcing risk refers to the impact of more expensive palm oil, so it does not result in a decline in net revenues. For the reputation/market access, the financial risk could be USD 231 million.

- Reckitt Benckiser’s largest part, USD 10 million, is based on its experience in one case that showed how regulatory costs related to land tenure rights can lead to higher raw material costs.

- Danone bases its indications, like several other FMCGs, on the 2017 Cone Communication CSR Study. This study says that “46 percent of global clients declared that they have stopped purchasing a product the year before because a company supported an issue contrary to their beliefs.”

The financial impact of this sample of nine companies totals USD 1,786 million.

Figure 7: Financial impact of forest-risks related to palm oil; selection of FMCGs

Source: Chain Reaction Research, CDP Forest applications

Excluding the non-listed Mars from the USD 1,786 million financial impact, the remaining USD 786 million would total 0.4 percent of the net turnover of the group of USD 195 billion (see Figure 10 Appendix). The USD 1,786 million value number mainly consists of market access risk, which would be an annual number, and does not reflect reputation value loss calculations.

The market access risk could lead to lower net turnover, estimated by the companies to be circa USD 1,786 million (USD 786 million excluding Mars) for the group of eight in Figure 7. This group has a 23 percent EBITDA margin (USD 44.6 billion EBITDA from Figure 5 as percentage of net revenues of USD 195.5 billion in Figure 10, Appendix). The loss of EBITDA would be USD 410 million (USD 180 million excluding Mars).

The above means that, according to the selected FMCGs, the value loss would total USD 4.1 billion (USD 1.8 billion excluding Mars) in a Discounted (Future) Cash Flow (DCF) valuation methodology (it requires a multiple of 10X of the lost EBITDA to calculate the reduction in DCF).

Reputation risk of palm oil-related deforestation might be 9-45X fold

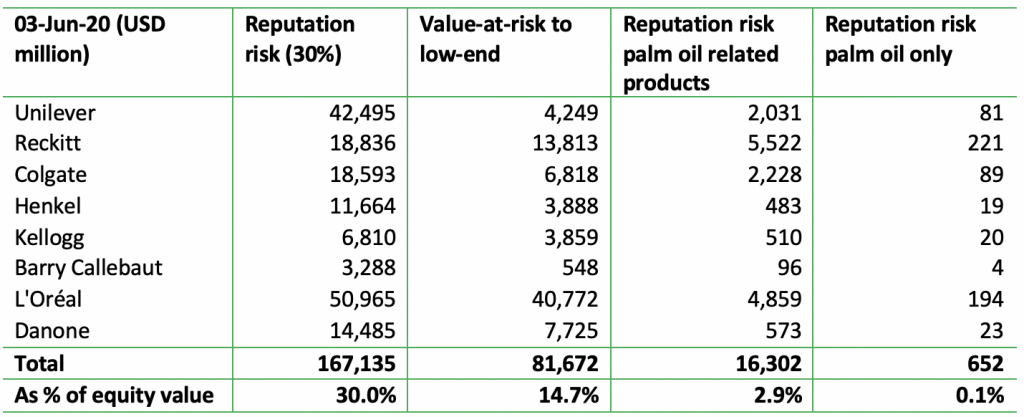

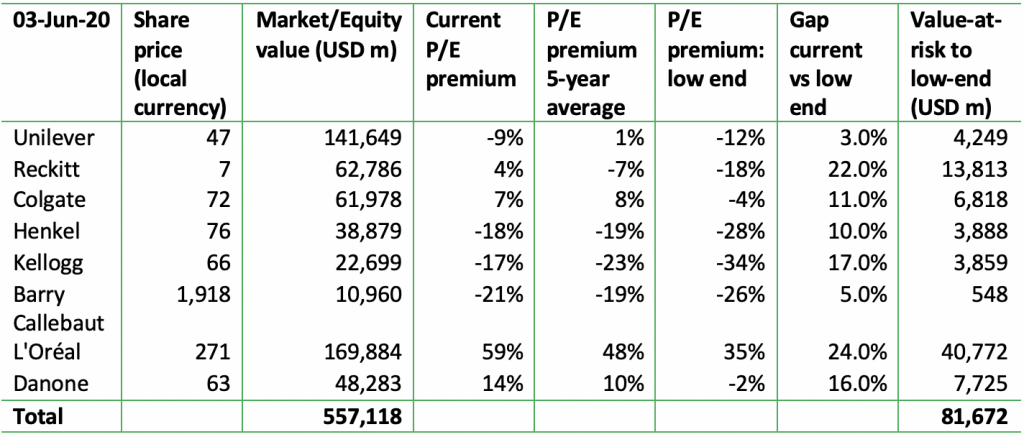

The outcome noted above contrasts with CRR’s report on valuing reputation risk. This report concluded that the reputation value-at-risk is complementary while also overlapping with the outcomes of market access risk, financing risk, and regulatory risk. In total, the number for reputation risk could be larger than the sum of these parts as companies are also confronted with long-term effects such as unfavorable contracts, adverse positioning in supermarket shelves, and a weaker position to attract high-qualified personnel. These factors would negatively impact the share price in due time. CRR developed two methodologies to value reputation risk. The first methodology is based on outcomes of third-part studies about the relation between ESG events and value, further supported by own case studies. In the second methodology, the current relative price/earnings ratio (versus the market multiple) is compared to the five-year average of this premium or discount in order to develop conclusions on the sensitivity for a string of reputation events.

In Figure 8, the first column (with numbers) represents the outcome aligned with the first methodology in the report “Deforestation-Driven Reputation Risk Could Become Material for FMCGs.” Research showed that underperformance in ESG management might undermine value by 30 percent. The second column represents the “Relative P/E” methodology explained in the paragraph following Figure 8. Column 3 and 4 are refinements in this methodology. Based on Procter & Gamble’s guidance, the revenues of palm oil-related products are calculated, while the reputation risk value is calculated for these products only (see Column 3). Column 4 is calculated for palm oil only. Reputation value-at-risk ranges from 0.1 percent to 30 percent of equity value. The reputation methodologies and refinements have their own merits. The first methodology (column 1) is best suited for a one-product company (like oil & gas majors), while the second methodology (column 2) and the refinement for palm oil related products (column 3) appear to provide the most relevant range of USD 16.3 billion to USD 81.7 billion (2.9 to 14.7 percent of market cap). Column 4 is likely less relevant as FMCGs re-package palm oil and its derivatives in value-added products.

Note that the range of most relevant reputation risk outcomes is 9-45X larger than the DCF value at risk implicitly calculated by the FMCGs themselves, which was USD 1.8 billion excluding Mars. This misperception among FMCGs could lead to a misallocation of investments related to sustainability efforts and a misallocation in NDPE execution costs.

Figure 8: Valuation of reputation risk: Two methodologies and refinements

Source: Chain Reaction Research, Bloomberg

In order to explain the second methodology based on relative price-earning (P/E) ratios, CRR reports on Procter & Gamble and the Walmart formed a crucial step. These reports explained that in case the current P/E relative (P/E divided by the P/E of the market) had a premium versus a 5-year average relative P/E or the low-end of the range in the last 5-year period, the share price could become sensitive to a series of negative reputation events. As a result, a total of USD 81.7 billion value could be at risk. This amount is 14.7 percent of the total equity value of the eight stocks.

Figure 9: Reputation value risk based on relative P/E methodology

Source: Chain Reaction Research, Bloomberg

FMCGs’ financial risk of deforestation and a solution for misallocation

Investors’ potential financial risk related to deforestation and their subsequent engagement with FMCGs could initiate efforts to halt palm oil-related deforestation. FMCGs’ dominance in the palm oil value chain and their large earnings based on palm oil-related products provide financial opportunities that could stop deforestation.

Two crucial conclusions from the sections above include:

- The value chain example of Procter & Gamble in Figure 6 highlighted the relatively moderate size of the NDPE execution costs versus the size of the value chain at the FMCG level. For Procter & Gamble, the costs total 0.15 percent of its net turnover on palm oil related products. The total annual costs for the selection of eight companies would amount to USD 113 million (Figure 5), or 0.9 percent of the USD 12.1 billion EBITDA generated on palm oil related products. The DCF value of these execution costs would be USD 1.1 billion.

- The calculations on reputation risk inform investors about the financial risks they are facing through financing FMCGs that are seeing their reputations undermined due to links to deforestation. The value-at-risk range would vary between USD 16.3 billion to USD 81.7 billion (Figure 8), 9-45X larger than the USD 1.8 billion perceived by the eight FMCGs.

These outcomes can be applied to the group of 25 FMCGs mentioned at the start of this report. The group of eight FMCGs source 1.8 million MT (palm oil + derivatives), while the group of 25 sources 5.4 million MT or 8 percent of the global palm oil production. Thus, for the 25 leading FMCGs, the numbers could be multiplied by 3x, meaning that NDPE execution spending could amount to USD 339 million per year, with a DCF value of USD 3.4 billion. The reputation risk related to products containing palm oil could be estimated (using 3X) at USD 49 billion to USD 245 billion. The palm oil-related EBITDA could be valued at USD 36 billion, although this estimate might be too high as smaller companies often have lower margins than the large ones. However, an outcome between USD 20-30 billion seems realistic.

The size of financial risks could enable new initiatives to end deforestation and strengthen the brand

With increasing pressure from consumers and food retailers for deforestation-free supply chains and 80 percent of the palm oil market still not certified, FMCGs can anticipate pressure from their stakeholders to improve and extend their processes. This pressure could go hand-in-hand with FMCGs’ desire to strengthen their brands and distinguish them more from FMCGs with less stringent policies on ending deforestation. An increase in execution costs might improve the brands’ status, followed by increased marketing and communication costs on this subject.

One example of possible increased spending by FMCGs related to the deforestation risk is through smallholders. In the CRR report “Future Smallholder Deforestation: Possible Palm Oil Risk,” CRR calculated the palm tree renewal cost for the coming 25 years at USD 1.1 billion per year and USD 28 billion for the period of 25 years. This burden weighs heavily on smallholders, which lack financial buffers. Therefore, deforestation risk and fire risk may increase in the coming years.

Currently, costs for a solution of this dilemma are born by smallholders, the governments, large plantation companies, while FMCGs occasionally participate in a project. The current report analyzed that the leading 25 FMCGs face a financial risk of USD 49 billion-245 billion, which could be largely solved by a value (DCF based) of USD 3.4 billion in upgraded execution. At the same time, the top-25 realize an EBITDA of USD 20 billion-30 billion on palm oil-related products. The annual USD 1.1 billion replanting costs would amount to 3.7-5.5 percent of this EBITDA.

Conclusion: As the shares of most of this top-25 FMCGs form a crucial part of investment portfolios, investors could see ample financial reason to engage with FMCGs on initiatives like smallholders’ tree renewal programs.

Appendix

Figure 10: Key data of eight selected Fast-Moving Consumer Good companies (FMCGs)

Source: Chain Reaction Research, Bloomberg, WWF