Yum China Holding Inc. (YUMC) is the largest restaurant chain in China. In June 2020, YUMC reportedly filed for a confidential secondary listing in Hong Kong. This report presents the company’s deforestation risk exposure and associated financial risks.

Download the PDF here: Major Deforestation Footprint a Risk for Yum China’s Secondary Listing

Report Webinar Recording:

Key Findings:

- As reported in the media, YUMC’s chicken sourcing is the equivalent of 16 to 24 percent of total chicken consumption in China. As a major fast food restaurant company, YUMC also purchases large quantities of beef, pork, and packaging materials. Its procurement may be linked to forest-risk supply chains, most notably cattle and soy supply chains.

- The company has a sizable deforestation footprint in its supply chains that originate in Brazil. The estimated amount of soy needed to feed YUMC’s chickens equals 0.9 to 1.6 percent of total soybean production in Brazil in 2018/19. This figure excludes soy embedded in YUMC’s pork and beef products.

- YUMC does not recognize the environmental risks in its Brazilian supply chains, so its deforestation exposure remains unmitigated. YUMC has no sustainability or responsible sourcing policies for soy and cattle, and only limited policies for palm oil and paper.

- Its equity value may be impacted by USD 3.0 billion market access risk. Changes in consumer behavior due to COVID-19, U.S.-China tensions, and a growing awareness of meat’s impact on health and deforestation might affect YUMC’s revenue growth model and its profits.

- A USD 2 billion secondary listing in Hong Kong could elevate investors’ concerns. Total risks could be USD 5.7 billion, 31 percent of equity value. YUMC has weak ESG credentials. Its material link to deforestation and forest fires, U.S.-China tensions, and health concerns from meat consumption add to revenue risk, financing risk, and reputation risk.

- Investors with USD 1 billion in YUMC could be in conflict with their own policies. More than 80 investors representing USD 6.5 trillion of assets under management have questioned leading fast food chains on GHG emissions in their supply chains. YUMC shareholders such as BNP Paribas, Norges Bank, Legal & General, and JPMorgan might reconsider their positions or engage the company to support their investment value.

Yum China is the largest restaurant company in China

Yum China (YUMC) is the largest restaurant company in China, generating USD 8.8 billion in revenues and employing over 450,000 people in 2019. YUMC, a publicly traded, U.S. incorporated fast-food restaurant company headquartered in Shanghai, China, operates 9,295 stores across more than 1,400 cities as of Q1 2020, serving over 2 billion costumers each year. Following its separation from Yum! Brands Inc. in 2016, YUMC acquired the exclusive right to operate and sub-license the KFC, Pizza Hut, and Taco Bell brands in mainland China. Its brand portfolio consists of three main segments:

- Western dining: KFC (the largest quick-service restaurant by system sales, spanning 6,500 stores as of the end of 2019), Pizza Hut (the largest casual dining restaurant by system sales, spanning 2,200 stores) and Taco Bell (seven units, with vast room to expand).

- Chinese dining: Little Sheep (310 units in both China and international markets), East Dawning (15 units), and Huang Ji Huang (acquired in April 2020, Huang Ji Huang has over 640 restaurants in China and internationally).

- Coffee: COFFii & JOY (53 units) and Lavazza Asia.

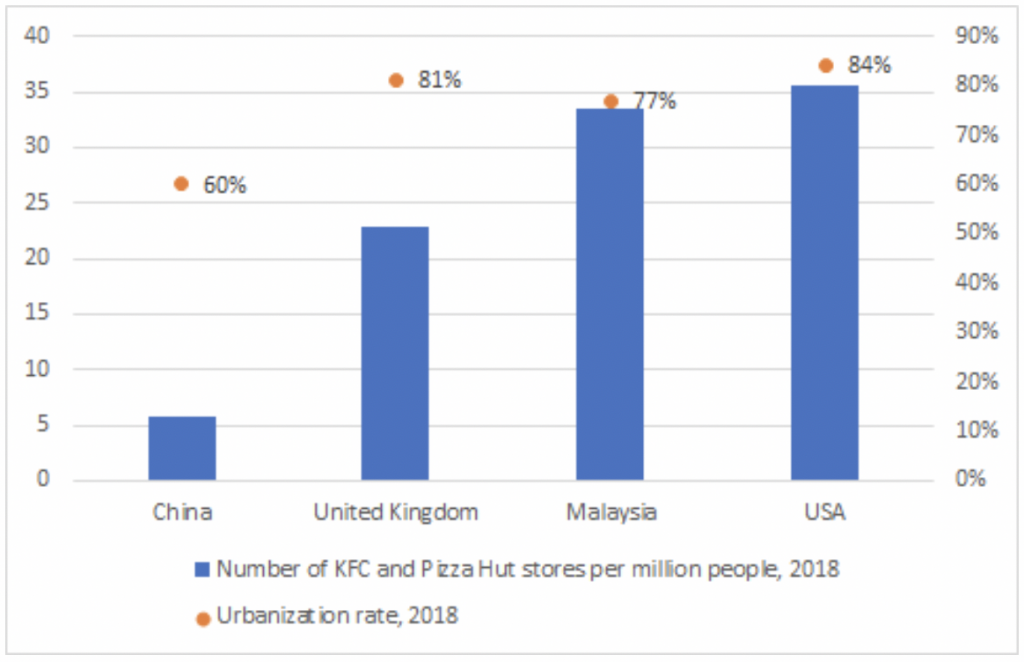

YUMC’s strategy centers on rapidly expanding its number of stores in both existing and new cities. From 2014 to 2019, YUMC’s compounded annual growth in new restaurant openings averaged 6 percent. From 2016 to 2018, it opened an average of two new stores per day. In 1Q 2020 alone, the company opened 179 new stores despite the temporary closure of 30 percent of its stores due to COVID-19. Comparing different markets (see Figure 1), YUMC sees vast room to increase its market reach, stating that it has the long-term potential to grow to at least 20,000 restaurants and penetrate around 1,000 new cities. The company is accelerating the expansion of its logistics layout. It will soon operate 32 logistics centers, a 33 percent increase compared to its capacity at of the end of 2019. In 2020, YUMC aims to open between 800 and 850 new stores, especially in smaller cities, where fewer competitors and Western dining options exist.

Figure 1: Growth potential of KFC and Pizza Hut in China, as of the end of 2018

Source: 2019 Investor Day – YUMC Overview – Innovation Powering Growth.

YUMC is rapidly expanding its presence in the Chinese cuisine and coffee markets. Despite the growing popularity of Western fast food, Chinese food represents the bulk of the catering industry in China. In April 2020, YUMC paid USD 185 million for a controlling stake in Huang Ji Huang, a leading Chinese-style casual dining franchise business. In May 2020, YUMC formed a joint venture with Italian coffee maker Lavazza Group to open Lavazza-branded shops in China. The company is also expanding its KFC K-coffee offerings.

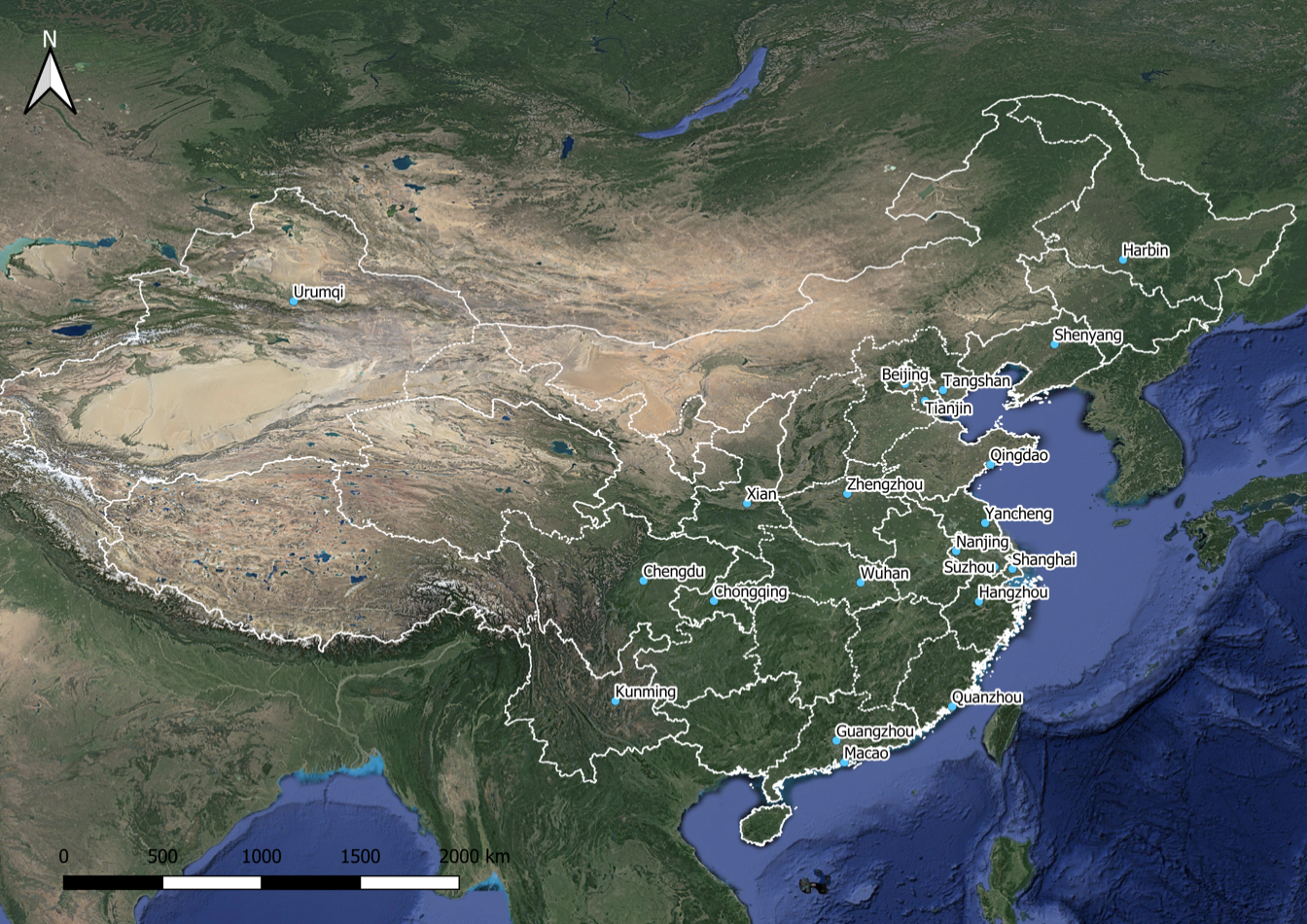

YUMC uses an integrated supply chain management system to procure inputs and supplies. The company centrally purchases the vast majority of food and paper products and then sells and distributes them to its restaurants. YUMC’s supply chain management system employs 1,600 staff and sources from over 800 independent suppliers, mostly within China. The company owns and operates a logistics system spanning a network of 24 logistics centers and five consolidation centers as of the end of 2019. YUMC claims that its logistics distribution system daily covers a distance that is the equivalent of circling the Earth five times.

YUMC is rapidly expanding its presence in the Chinese cuisine and coffee markets. Despite the growing popularity of Western fast food, Chinese food represents the bulk of the catering industry in China. In April 2020, YUMC paid USD 185 million for a controlling stake in Huang Ji Huang, a leading Chinese-style casual dining franchise business. In May 2020, YUMC formed a joint venture with Italian coffee maker Lavazza Group to open Lavazza-branded shops in China. The company is also expanding its KFC K-coffee offerings.

YUMC uses an integrated supply chain management system to procure inputs and supplies. The company centrally purchases the vast majority of food and paper products and then sells and distributes them to its restaurants. YUMC’s supply chain management system employs 1,600 staff and sources from over 800 independent suppliers, mostly within China. The company owns and operates a logistics system spanning a network of 24 logistics centers and five consolidation centers as of the end of 2019. YUMC claims that its logistics distribution system daily covers a distance that is the equivalent of circling the Earth five times.

Figure 2: Yum China logistics centers, as of July 2019

Source: 2019 Investor Day – YUMC Overview – Innovation Powering Growth. Note: While the picture here dates from July 2019 and depicts 21 logistics centers, as of the end of 2019 Yum China utilized 24 logistics centers and five consolidation centers.

Yum China has a sizable deforestation footprint

Yum China purchases large volumes of forest-risk commodities

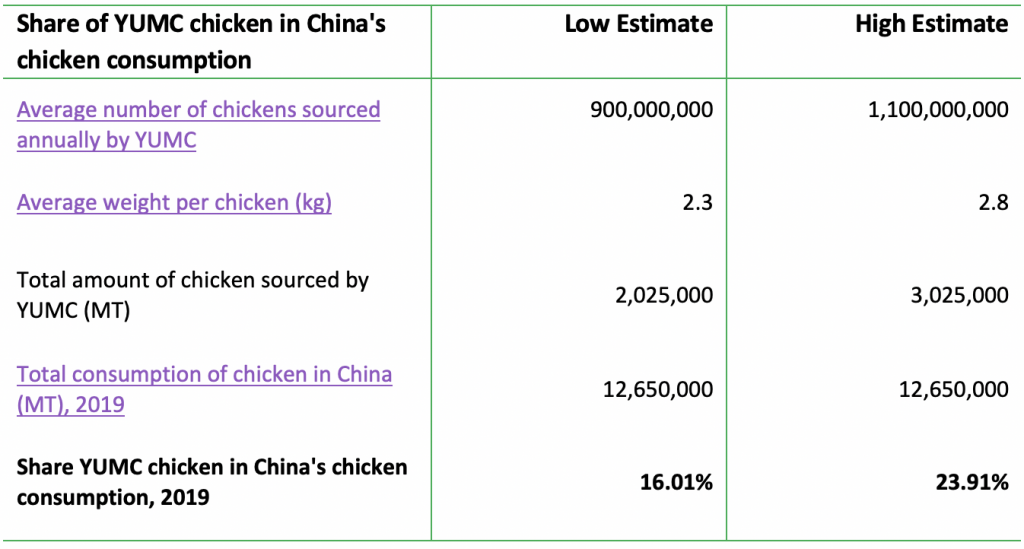

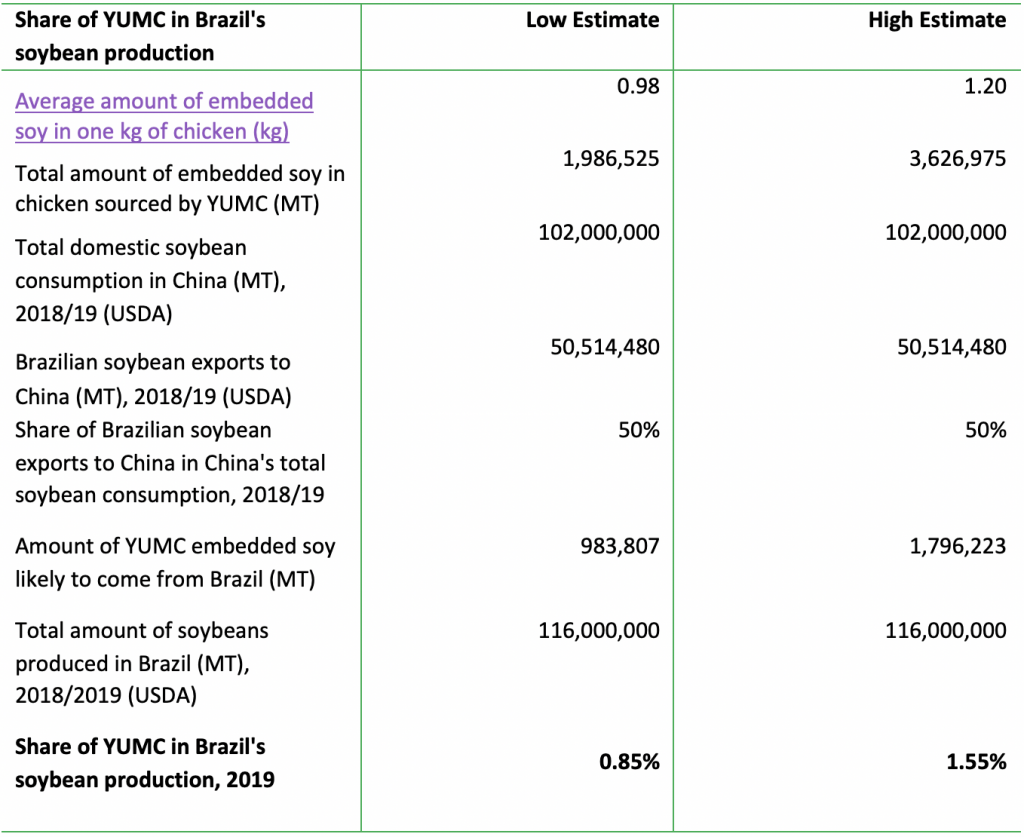

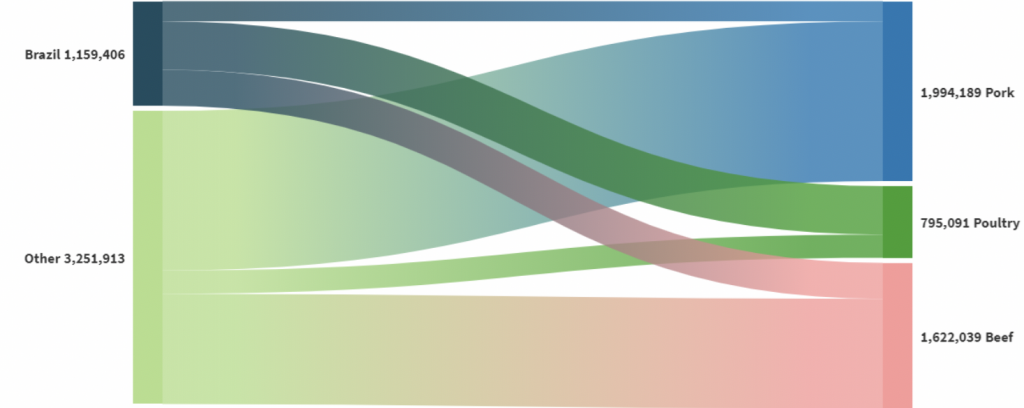

As a major fast food restaurant company, YUMC purchases large amounts of commodities that contribute to deforestation, such as meat and pulp/paper. Its main purchases include beef, chicken, and pork products. Its costs for food and paper purchases were approximately USD 2.5 billion in 2019. While the company does not publish specific figures, media reports suggest that YUMC buys around 1 billion chickens per year. Based on this number of purchased chickens, CRR estimates that about 16 to 24 percent of overall Chinese chicken consumption is channeled through YUMC’s restaurants (see Figure 3 below). Based on this calculation, CRR estimates that YUMC may be the indirect recipient of 0.9 to 1.6 percent of total soybean production in Brazil during crop year 2018-19 (see Figure 4 below). The figure is likely higher, as lack of available information did not allow for CRR to consider YUMC’s purchases of pork and beef. In addition, the company also sources paper and packaging as well as palm oil-based cooking oil. YUMC uses large volumes of paper and packaging. In 2019, annual shipment volumes totaled 100 million boxes.

CRR reached out to YUMC for comment on this report but the company did not provide details in its response.

Figure 3: Estimates of Yum China’s share of total chicken consumption in China, 2019

Figure 4: Estimates of Yum China’s share of total soybean production in Brazil, 2019

Note: The low and high estimates are calculated using a 10 percent range for the relevant figures reported in the listed sources.

Chinese demand for chicken, pork, and beef drives deforestation in South America. Brazilian soy is an essential ingredient of feed for chicken, pork, and beef in China, the world’s largest animal feed producer and the largest importer of Brazilian soybeans. China’s meat production is therefore linked to high levels of deforestation through embedded Brazilian soy. Imported Brazilian beef also carries an elevated risk of being linked to deforestation, as cattle ranching is a primary driver of deforestation in the Amazon, the biome where roughly 40 percent of the country’s herd is located. Similarly, China is the largest importer of chicken and pork from Brazil, which in turn have been reared on soy.

As YUMC pursues rapid expansion, its animal protein demand is expected to surge. Based on its reported system sales, CRR estimates that YUMC has the largest market share – around 5 percent – in China’s fast-food restaurants industry. With rapid growth of its restaurant market, China is on track to become the world’s largest by 2023. China’s restaurant market is projected to grow by a CAGR of 8 percent during 2018-23, compared to a CAGR of 3 percent and 2 percent for the U.S. and EU restaurant markets, respectively. YUMC’s expected growth in China’s market would sharply increase the company’s demand for meat. COVID-induced declines in spending on restaurant dining already suggest a likely increase in YUMC’s beef demand, with the company trying out new product lines such as delivering raw steaks for home-cooking. China’s increased reliance on Brazilian soybeans and meat products will heighten YUMC’s deforestation and carbon emissions footprint.

China is Brazil’s largest trading partner for soy and beef

Brazil is the world’s largest soy producer, accounting for 37 percent of the global total, or 123 million metric tons (MT), in 2019/2020. As the world’s largest animal feed producer, China uses large volumes of Brazilian soy as a source of high-quality protein in animal feed. China is currently the world’s largest meat producer and consumer. Between 2010 and 2017, China’s soy imports from Brazil increased 170 percent. In 2019, China was the biggest importer of Brazilian soybeans, accounting for 65 percent of Brazil’s soybean exports (including soybean meal). Deficient domestic protein crop production and ongoing U.S.-China trade uncertainty continue to drive China’s imports of Brazilian soybeans. During January-May 2020, Brazil’s soybean exports to China increased by around 36.8 percent year-on-year. As a result, deforestation-risk soy is embedded in beef, poultry, and pork produced in China.

China is a leading importer of soy produced in the Matopiba region of the Cerrado, a hotspot for soy-driven deforestation. Between 2005 and 2016, 76 percent of the total area of native Cerrado vegetation cleared for soy cultivation occurred in Matopiba (at the intersection of Maranhão, Tocantins, Piauí, and Bahía). This rapid expansion of soybean production has been linked to widespread deforestation, biodiversity loss, fires, emission of greenhouse gases, and disruption of water systems. In total, China was exposed to a total deforestation risk of 460 square kilometers in 2017, or 5.6Mt CO2e, in relation to its soy imports from the Cerrado biome.

China is also a major importer of Brazilian meat. China is the leading destination of Brazilian poultry and pork, accounting for circa 18 percent of total exports in 2019. African Swine Flu (ASF)-induced decline in domestic pork production and ongoing U.S.-China retaliatory tariffs contribute to high demand for Brazilian meat. China’s imports of Brazilian chicken rose by 94 percent month-on-month in December 2019, and during the first two months of 2020, Brazilian chicken exports to China grew by 59 percent. Brazil’s pork exports are also expected to increase by 33 percent year-on-year in 2020, with China as a leading market. Data confirms that China is a recipient of high volumes of embedded soy. Crucially, Brazilian exports of frozen beef to China during January–May 2020 grew by 128 percent over the levels in the same period in 2019. Cattle ranching is the top driver of deforestation in the Amazon region, accounting for 80% of deforestation.

Figure 5: China’s pork, poultry, and beef imports from Brazil, 2019

Source: Trademap

COVID 19-induced food shortages and fears over a second coronavirus wave later in the year may further increase China’s reliance on Brazilian meat and soy. The “depopulation” of millions of farm animals in the U.S. and China, as well China’s shortages of fertilizers and seeds due to COVID-related supply chain disruptions, has increased China’s imports of Brazilian soy and meat. While millions of animals were culled in the U.S. and China due to COVID-related plant closures, Brazilian plants have stepped in to fill the gap. China’s demand for soy is also expected to surge as the country prepares for a restocking boom in swine and poultry.

As concerns over a possible second wave of COVID-19 cases looms, China has asked trading firms and food processors to stockpile beans. In early April 2020, Wei Baigang of the Chinese Ministry of Agriculture stated that the government is focusing on soy, an essential foodstuff that China imports in massive quantities. April saw an all-time high in Brazilian agribusiness exports, fueled by sales of soy to China. Total soy exports from Brazil increased by 73.4 percent year-on-year, propelled by a year-on-year increase of over 70 percent in China’s soy imports.

Yum China fails to recognize beef and soy deforestation risks

YUMC recognizes deforestation as an issue only in its palm oil and paper use. In its most recent sustainability report, YUMC reported meeting its targets of sourcing 100 percent RSPO-certified palm oil and refusing to purchase paper products from suppliers that knowingly cause deforestation. In its 2018 communication of progress to the RSPO, YUMC indicated that it used 93,607 MT of palm oil as cooking oil for its fried foods. All volumes were RSPO certified through “book and claim,” considered one of the weakest methods to gain RSPO certification.

Despite accounting for 16 to 24 percent of China’s chicken consumption, YUMC does not have sustainability commitments for meat. The company has not put forth any communication regarding measures to address deforestation or other sustainability issues in these supply chains. YUMC’s environmental priorities, goals, and commitments largely remained the same in 2018 and 2019. They are detailed in a half page (see page 2). YUMC’s environmental priorities include “sustainable restaurants” and a “sustainable supply chain.” The former focuses on reducing water and energy consumption in restaurants, ensuring that consumer facing packaging material is recyclable, etc. The latter mentions only its palm oil and paper commitments and a CSR supplier audit that does not consider deforestation risks.

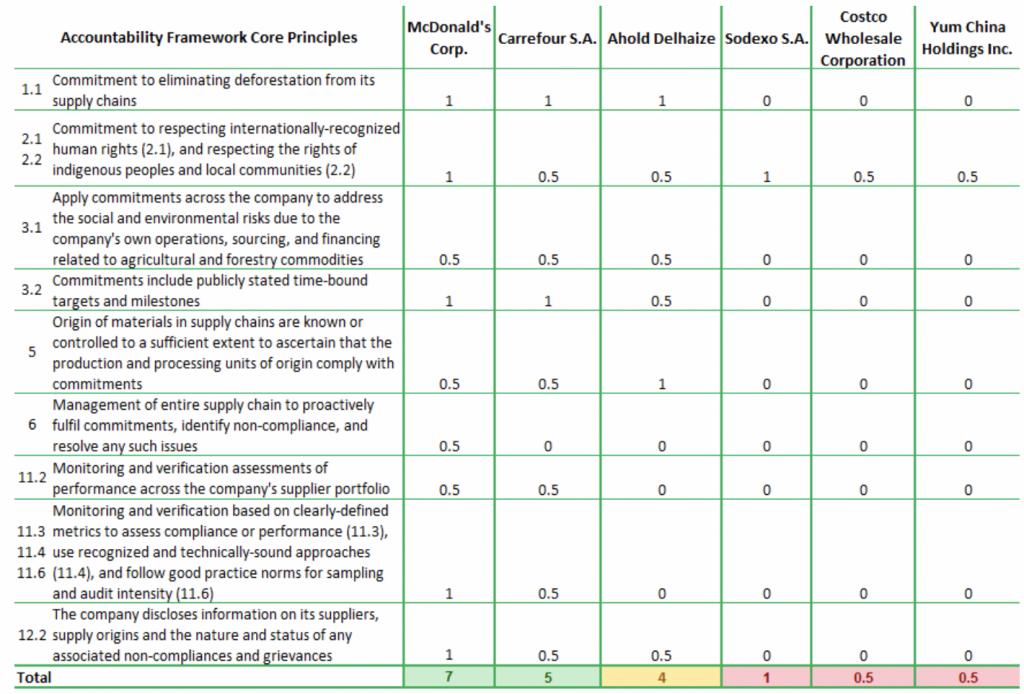

YUMC vastly underperforms its peers in sustainability commitments for soy and cattle sourcing. When assessed against the Core Principles of the Accountability Framework, YUMC lags nearly all its peers. YUMC does not use its centralized procurement model and in-house, integrated supply chain management system to implement deforestation-free sourcing. Instead, YUMC “guides suppliers to gradually manage their own upstream suppliers.” YUMC’s score stands in contrast to other retail and food service companies, including McDonald’s, Carrefour S.A., and Ahold Delhaize. McDonald’s and Carrefour S.A. have committed to a deforestation-free supply chain, largely meeting basic expectations concerning strategy, implementation, disclosure, and performance. McDonald’s has a deforestation policy that includes risk assessments, traceability, and sourcing of sustainably certified products. Carrefour, meanwhile, actively engages its direct suppliers on deforestation risks in both its soy and beef supply chains in Brazil.

Figure 6: Accountability Framework Scoring for Soy and Beef Commitments, 2019 – Retail/Food Service

Source: Accountability Framework Core Principles, company websites and sustainability reports.

A notable omission is YUMC’s lack of transparency regarding suppliers and terms of its CSR supplier audit. YUMC’s CSR supplier audit does not consider deforestation or climate emissions risk. Out of YUMC’s more than 800 suppliers, YUMC’s CSR audit covers only critical suppliers, which total around 400. Crucially, YUMC says that its CSR audits do not apply to overseas suppliers. “Environmental management and security” is mentioned as part of the audit but no further description is provided. Similar to the CSR audit, YUMC’s Supplier Code of Conduct (CoC) – signed by all suppliers – does not address deforestation or climate emissions risks, cautioning instead against “major violation of environmental laws and regulations.”

Sunner Group, one of the largest poultry producers in China and YUMC’s most important poultry supplier, imports beef from Brazil through Minerva and Marfrig, two of the companies most exposed to the 2019 Brazil fires in their supply chains. In 2014, then parent company Yum! Brands published its list of suppliers in China following an incident with expired meat. The list included subsidiaries of Wilmar, COFCO, and WH Group. In April 2020, YUMC’s KFC announced that Cargill would supply its plant-based fried chicken. Both WH Group and Cargill are exposed to deforestation risks in Brazil. WH Group is facing increasing pressure following its poor track record with pandemics.

Yum China is exposed to material business risks

YUMC’s links to deforestation in its supply chain may expose the company to material business and financial risks. Its lagging deforestation policies suggest that the company may not be able to adequately mitigate these business risks. The company’s intention for a new stock listing in Hong Kong may lead to increased investor scrutiny. As a consumer-facing company, YUMC is also exposed to consumer reputational risks. Deforestation may exacerbate additional risks related to COVID-19 and volatile U.S.-China relations.

Yum China may face increasing ESG scrutiny

Investor ESG scrutiny may increase ahead of YUMC’s intended Hong Kong listing. Investors increasingly recognize the fast food industry as a climate-risk sector. Already, more than 80 investors representing USD 6.5 trillion have urged McDonald’s, KFC, and Burger King to reduce greenhouse gas emissions in their supply chains, with the animal agriculture industry highlighted as a major source of emissions. YUMC’s high exposure and inadequate management of deforestation and climate risks may raise red flags for investors. As investors increasingly move to align their portfolios with global climate goals, its rating as a laggard among its peers in soy and cattle in sustainability commitments will likely render the company ineligible for climate-friendly portfolios.

Deforestation risk exposure could exacerbate already existing investor concerns:

- COVID-19 may sink overall investor risk appetite. CDP reports that, in 2019, companies headquartered in China were behind the average response rate in terms of identifying climate-related opportunities. The proportion of companies which identified opportunities but were unable to realize them was also higher in China than in other countries. As the link between the COVID-19 pandemic and commodity-driven deforestation becomes clearer, YUMC’s investors may demand higher returns on their investment, leading to a higher cost of capital.

- Uncertainty over U.S.-China relations may continue. Despite some easing of U.S.-China trade tensions, COVID-19 may prevent Beijing from fulfilling the terms of the phase one trade deal. Further developments between the two countries remain uncertain. As a result, YUMC may see uncertainty as it operates in China but is listed in the U.S. YUMC’s high exposure to “country risk” may heighten the risk perception among investors and further increase cost of capital.

- YUMC is exposed to legal and regulatory risks in China. Since 2016, the company has been under a national audit on transfer pricing by the STA (Chinese State Taxation Administration) regarding its related party transactions during 2006-15. The audit’s focus appears to centre on YUMC’s franchise arrangement with Yum! Brands. YUMC assesses that “it is reasonably possible that there could be significant developments within the next 12 months.” YUMC also reports that the lessors of most of the company’s 7,300 leased properties had not registered the lease agreements with government authorities in China.

- YUMC faces the risk of a possible delisting from the New York Stock Exchange. U.S.’s Public Company Accounting Oversight Board (PCAOB) is unable to inspect YUMC’s auditor. In June 2019, lawmakers introduced bills in the two houses of U.S. Congress that would oblige the SEC to develop a list of foreign issuers for which the PCAOB is unable to inspect or investigate auditor reports issued by foreign public accounting companies. The Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges (EQUITABLE) Act stipulates increased disclosure requirements for such issuers and, starting in 2025, delisting issuers included on the SEC’s list for three successive years from U.S. stock exchanges. YUMC reports that proceedings instituted by the SEC against its public accounting firm may result in regulators determining that YUMC’s financial statements are not in compliance with requirements of the Exchange Act.

Yum China may be exposed to consumer reputational risks

YUMC may be exposed to reputational fallout as the fast-food industry faces increased scrutiny over its role in driving deforestation. Since 2019, SumofUs has been pressuring KFC and Pizza Hut to “take deforestation off the menu!” and amend their opaque and vague reporting. Greenpeace urged McDonald’s, Burger King, and KFC to speak up about the Amazon fires in 2019. As Amazon fires are expected to increase this year, YUMC may become a key target of civil society campaigns. As the link between COVID-19, deforestation, and agricultural production becomes clearer, this pressure will only increase. Reputational events related to deforestation may impact not only YUMC through less customers and lower employee satisfaction, but also Yum! Brands as the brand owner of KFC, Pizza Hut, and Taco Bell.

The impact of COVID-19 on health awareness may increase consumer scrutiny. The pandemic is reportedly making the case for consumers to change their diet. Fast-food predisposes consumers to the underlying conditions that worsen the effects of the virus – obesity and chronic diseases such as hypertension and type-2 diabetes. These conditions are among the strongest predictors that an individual infected with COVID-19 will be hospitalized with a severe case of the disease. A recent uptick in studies on fast food and obesity in China, combined with increasing concerns over links between meat and viral diseases in China, may raise standards for responsible behavior on the part of YUMC.

Volatile U.S.-China relations may also impact consumer sentiment toward YUMC, further lowering tolerance of any future negative publicity. YUMC reports that “changes in trade relations between the United States and China may trigger negative customer sentiment towards Western brands in China, potentially resulting in a negative impact on our results of operations and financial condition.” Tensions between Beijing and Washington may rise again as China is not close to fulfilling the terms of the phase one trade deal. U.S. President Trump has recently threatened more tariffs on China, or even tearing up the phase one trade deal itself should China fall short of its purchase commitments. The November presidential elections in the U.S. represent an additional factor of uncertainty for U.S.-China relations. Meanwhile, COVID-19 has triggered an “unprecedented xenophobic rise in China.” YUMC has been previously affected by hostile U.S.-China relations. In 2016, following the International Court of Arbitration’s ruling against China’s territorial claims in the South China Sea, groups of patriotic Chinese unfurled banners outside a dozen KFC outlets, urging a boycott. As COVID-19 sparks a new trend in consumption behavior — with people increasingly wanting an “emotional connection or affinity with brands” — the blowback from any negative reputation events could be material.

Financial Risk Analysis: Poor ESG Performance Threatens USD 2 billion Hong Kong listing

YUMC’s equity value might be impacted by USD 3.0 billion market access risk and USD 2.5 billion financing risk. The overarching reputation risk for investors could be valued at USD 3.7 billion to USD 5.7 billion. This value impact ranges from 8 percent to 31 percent of equity value. Shareholders are the main group affected by ESG factors as YUMC has a relatively low level of gross debt.

Strong growth through 2019, debt level is low

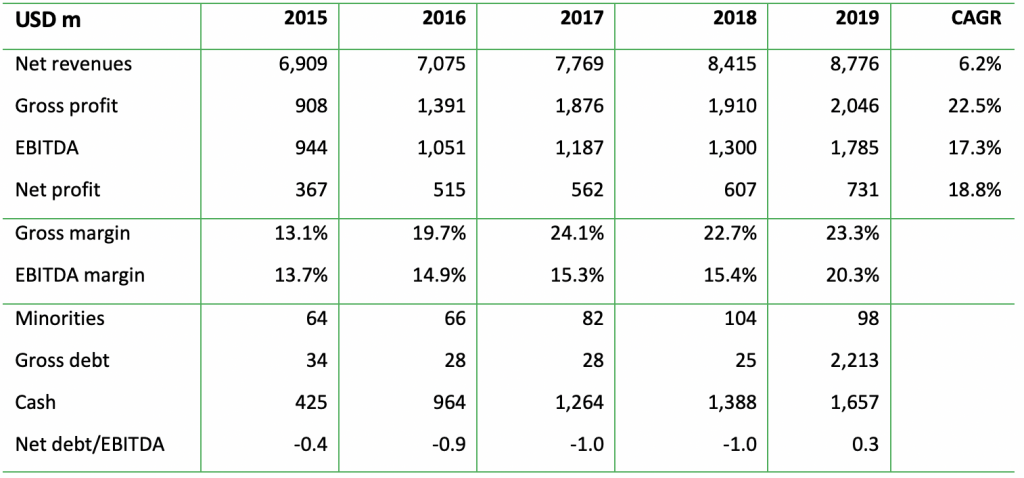

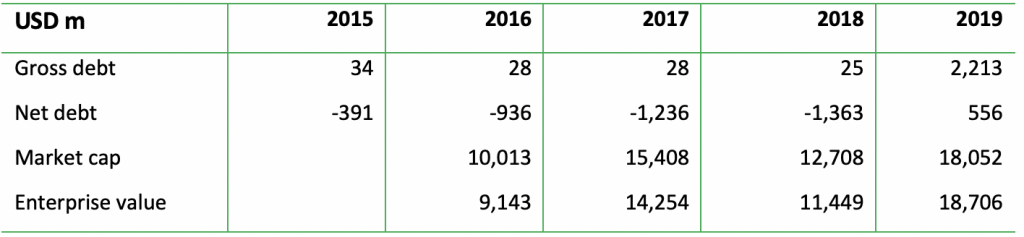

YUMC realized growth in 2015-19 but has been heavily affected by COVID-19. In the period 2015-19, YUMC realized a 6.2 percent average annual growth in net revenues, while its profitability grew even stronger: The compounded (annual) average growth rate (CAGR) in gross profit was 22.5 percent, in EBITDA 17.3 percent, and in net profit 18.8 percent. Consequently, both the gross margin and EBITDA margin showed increases. During this growth period, the key numbers in the balance sheet remained at a low level, with net-debt/EBITDA initially negative and only rising in 2019 to a 0.3X. This rise was the result of an accounting change as lease liabilities of USD 1.8 billion were added to the balance sheet. The 0.3X net-debt/EBITDA ratio is a low outcome in the Fast-Moving Consumer Good (FMCG) industry where higher debt levels could lead to a ratio of 1.5-3.0X.

COVID-19 led to a 24 percent net revenue decline in 1Q20. The operating profit fell 68 percent to USD 97 million. By mid-February, 35 percent of the stores were closed. Net profit declined by 72 percent to USD 62 million. In April 2020, the company finalized its acquisition of Huang Ji Huang for approximately USD 185 million. Also, it acquired a 25 percent equity interest in an unconsolidated affiliate that operates KFC stores in and around Suzhou, China for USD 149 million. The two acquisitions will have increased bank lending. The company indicates that COVID-19 may continue to have a material impact on results.

Figure 7: Yum China Holdings key financials

Source: Chain Reaction Research, Bloomberg

Four factors affect Yum China’s revenue growth model: USD 3.0 billion value impact

Market access might be affected by changing consumer habits based on four crucial trends. Chinese consumers may give more weight to the following: 1) Health concerns related to meat consumption; consumers might reduce meat consumption and switch increasingly to meat alternatives. Through COVID-19, the awareness of zoonotic diseases has increased substantially while the perception of contaminated imported meat can affect imports; 2) Consumers becoming more concerned about the effects of deforestation; 3) The impact from U.S.-China trade war bringing about an extra potential risk for consumer loyalty to fast food consumption with an American appearance; and 4) Restaurant sales structurally affected by social distancing.

The total impact of the four factors could disturb the growth model of YUMC. Its growth model is based on opening a high number of new outlets every year. Instead of opening new stores, existing stores might face negative like-for-like sales, which would affect gross profit and EBITDA. The size of the combined impact of the four factors can be evaluated in a scenario analysis based on recent market research. An important input is that Chinese Millennials (born between 1981 and 1996) are more concerned about sustainability issues than their parents. With 70 percent of Chinese consumers aware of the benefits of sustainable consumption, a shift in consumption could emerge.

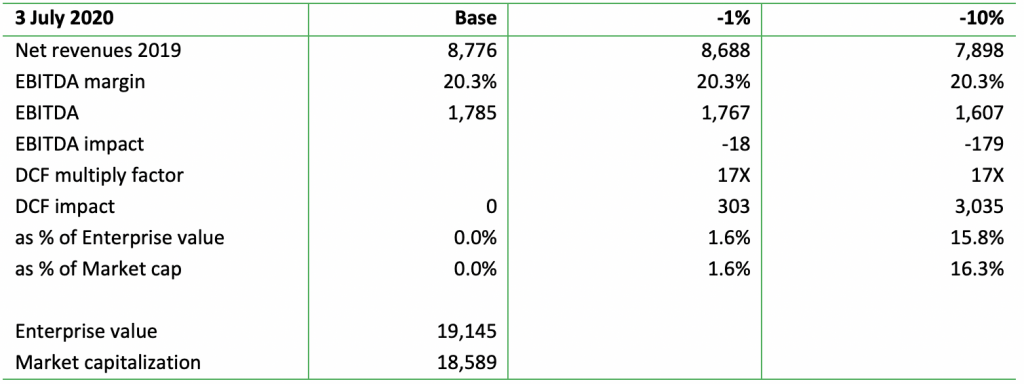

Every 1 percent reduction in demand may impact net revenues by USD 88 million and EBITDA by USD 18 million. In a DCF context, this impact could add up to a value of USD 303 million. If demand would develop structurally on a 10 percent lower level than the market anticipates (see last column in Figure 8) for the next 10 years, the value impact could be USD 3.0 billion, which is 16 percent of current market capitalization.

Figure 8: Revenue-at-risk scenarios, pro forma (USD million)

Source: Chain Reaction Research, Bloomberg

YUMC could dampen these impacts by addressing all four consumer trends. For instance, by becoming a leader in a group of global fast food chain and vegan meat producers which are quickly scaling up alternatives.

Yum China financing mainly based on shareholders with limited deforestation policies, but investors with USD 1 billion face conflict

YUMC’s financing is nearly completely based on equity. JPMorgan’s USD 637 million exposure and its deforestation policies could bring about engagement on the subject of YUMC’s material links to Brazilian soy. BNP Paribas, Norges Bank, and Legal & General, meanwhile, all have smaller positions but more stringent policies.

YUMC is mainly financed by equity, while debt is a relatively minor financing instrument. Net-debt/EBITDA is a relatively low 0.3X in 2019 (Figure 9) and of the total enterprise value of USD 18.7 billion (end of 2019), USD 2.2 billion consists of gross debt, of which more than 80 percent in lease commitments. Net debt is USD 556 million as the company is holding USD 1.7 billion cash (Figure 9). This financial strength offers resilience in the face of the uncertain COVID-19 environment. The company will not have immediate debt service problems, although it may have less cash to expand its business.

Figure 9: Yum China Holdings debt and market capitalization

Source: Chain Reaction Research, Bloomberg; data 3 June 2020

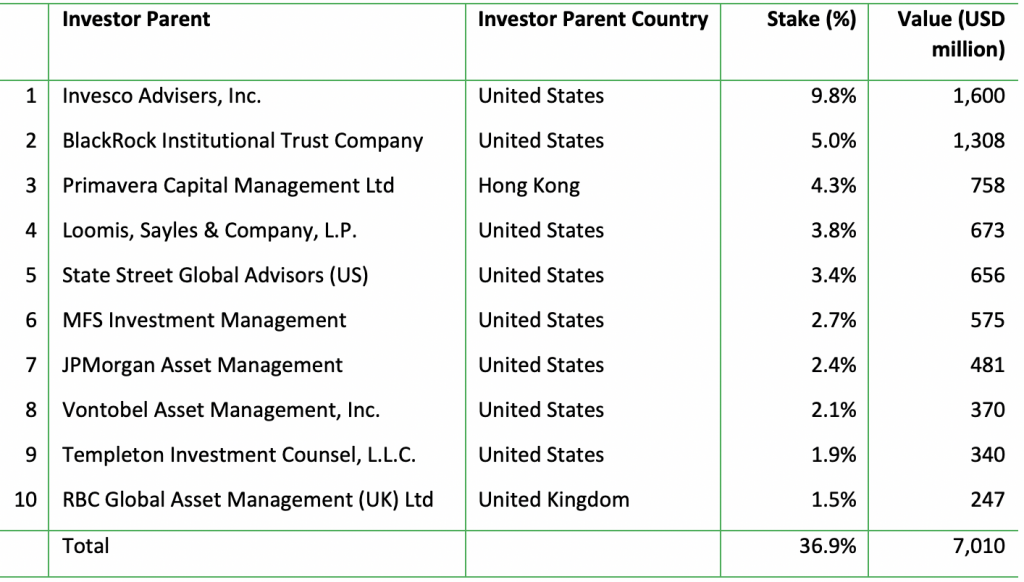

The top-10 shareholders of YUMC control in total 37 percent of the shares (Figure 10). Invesco, Primavera and Loomis, Sayles & Company have no policies on deforestation. BlackRock has been very vocal on climate change recently, but it lacks a policy on deforestation. Nevertheless, it says it is engaging with palm oil companies. State Street has no policy on deforestation. It says to target a reduction in GHG emissions by 30 percent by 2025, but scope, base and details are lacking. MFS is a signatory of the Principles for Responsible Investment (PRI) and of Carbon Disclosure Project (CDP), but the initiatives do not entail policies on deforestation. Vontobel has disclosed to CDP and is signatory of PRI, but details on deforestation are lacking. Templeton is member of PRI and CDP but has no deforestation policies. RBC is in the same position.

In 2019, JPMorgan Chase, which is the group company of JPMorgan Asset Management, released its first climate report based on recommendations by TCFD (Task Force on Climate-related Financial Disclosures). JPMorgan Chase policies cover all group activities. The group is also signatory of many other initiatives, including the Consumer Goods Forum, which strives for zero-deforestation. JPMorgan Asset Management USA has USD 481 million invested in YUMC, but JPMorgan subsidiaries from other regions also own shares, bringing the total number to USD 637 million, which would catapult it to the number four shareholder. This position creates an opportunity to engage.

The group of top-20 shareholders contains investors with large stakes in USD, such as Norges Bank (1.0 percent; USD 181 million), Nuveen (0.9 percent; USD 135 million), Legal & General (0.8 percent; USD 124 million) and BNP Paribas (0.2 percent; USD 29 million). These investors have clear intentions or policies on deforestation, or have other links to deforestation on which engagement is taking place (such as Nuveen’s position in Radar).

Figure 10: Yum China Holdings’ shareholders

Source: Chain Reaction Research, Bloomberg; data 3 June 2020

As of December 31, 2019, YUMC had credit facilities valued at USD 415 million, with onshore at USD 215 million and offshore at USD 200 million. The remaining terms ranged from less than one year to three years. The company and other data searches provide no names for YUMC’s debt relations.

A USD 2 billion Hong Kong listing could elevate financing and investors’ reputation risk

Financing risk could increase if YUMC launches as secondary offering in Hong Kong. YUMC’s cost of capital could be affected by 1) ESG factors, including awareness about health impact of meat consumption, and deforestation; 2) The impact of the uncertainty about the U.S.-China relations considering YUMC’s high exposure to China. A potential de-listing of YUMC on the New York stock exchange would also affect cost of capital.

Recent studies from Erasmus University and others show the connection between ESG outcomes and cost of capital. Higher cost of capital might impact equity value by USD 2.5 billion. The findings in the current report on YUMC’s material link to deforestation might impact the cost of debt and the cost of capital. A 10 basis-point increase in the costs of capital, because of financing risk, could have a USD 250 million negative impact on the value of YUMC, based on DCF calculations and assuming a cost of capital of 7 percent. A 1 percent increase leads to a tenfold impact, or USD 2.5 billion.

The publicity of the secondary listing and the need to search for a new investor base could further elevate the value risk for shareholders. YUMC’s link to deforestation, which is larger than previously believed, could see more attention if the company decides for a secondary offering in Hong Kong. The Financial Times reported that YUMC is contacting banks to pitch for an advisory role in a listing that could be worth up to USD 2 billion. The company has a strong balance sheet, but the offering could give access to new funds as the current low profitability due to COVID-19 generates no cash for planned growth of further roll-out of its formulas.

Technically, a secondary listing is aimed at creating a broader investor base. YUMC’s investor base in New York (and funds that invest in New York-listed stocks) can be expanded by investors which technically have to invest in Asian and Chinese stocks. An expanded investor base could increase the demand for shares and raise the value per share. However, the timing of a secondary listing, which would occur at a moment that deforestation and fires in Brazil are rising, could bring about a financial risk for existing and new shareholders. The publicity of strong links between YUMC, deforestation in Brazil and climate change as well as its low ESG ranking (see Figure 6 above) could temper interest for the share offering. For instance, Chinese Millennials are more interested in ESG issues than their parents, and research shows that this might impact their investments. Also, existing YUMC investors could reconsider their positions in New York, possibly bringing about higher cost of capital. A 1 percent increase leads to a USD 2.5 billion impact and is part of the broader investor reputation value reduction (see below: between USD 3.7 – 5.7 billion).

A complete de-listing from the New York Stock Exchange (and a 100 percent move to Hong Kong) could bring about similar impacts on valuation of the shares for a secondary listing. An additional impact could be investors who are required to have U.S.-listed stocks in their portfolio willing to divest.

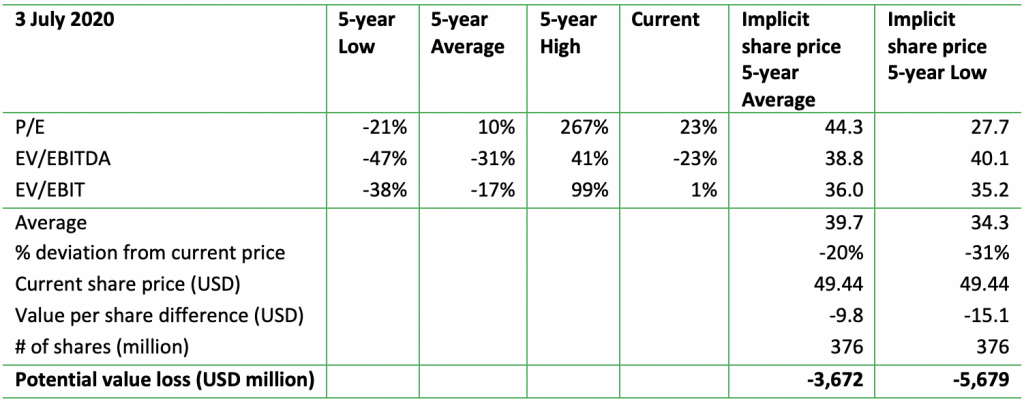

The overarching reputation value risk could affect YUMC shareholders by USD 3.7–5.7 billion. The reputation value impact for investors could be larger amid a broader range of impacts, including (perceptions of) the weakening of a brand, a decline in consumer loyalty, and reluctance to work for a low-ESG rated company. Based on the methodology used in CRR reports on reputation risk, a nearly 30 percent impact on the share price could bring about a reduction of USD 5.2 billion in market capitalization. Investors could realize that YUMC’s net sales are materially exposed to meat ingredients (with their impact on health and deforestation/climate). Combined with the other risk factor (U.S.-China relations), there could be a perfect storm.

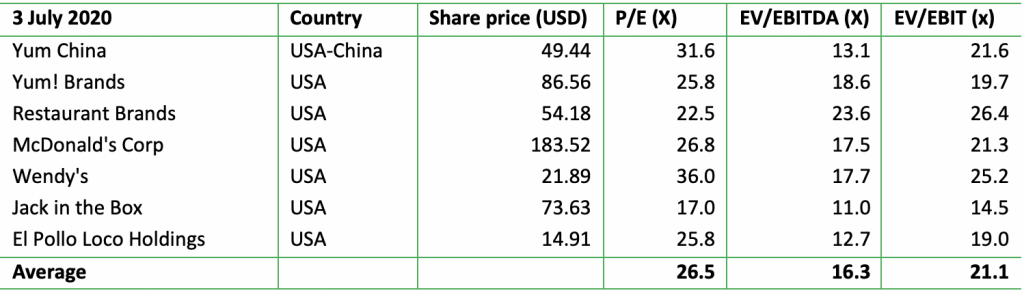

Another approach in the calculation of the potential impact of reputation events can be based on the current relative valuation (in a peer group: see Figure 12 below) of YUMC versus its own history. If YUMC relative valuation would decline to its five-year average, the potential value loss would be 20 percent or USD 3.7 billion. A decline to the five-year low in relative valuation equates to a loss of 31 percent or USD 5.7 billion.

Figure 11: Yum China Holdings – Potential downside from reputation events

Source: Chain Reaction Research, Bloomberg; data 3 July 2020

Figure 12: Yum China Holdings – Peer group

Source: Chain Reaction Research, Bloomberg; data 3 July 2020