The palm oil industry has seen considerable transformation in the last few years, as suppliers that are not compliant with NDPE policies have been increasingly excluded from supply chains. However, these gains are undermined when the same suppliers enter supply chains via spot purchases. Yet, little is known about the spot market. This paper seeks to provide information on the market, how it operates, and highlight the risk it presents to NDPE compliance efforts.

Download the PDF here: Spot Market Purchases Allow Deforestation-Linked Palm Oil to Enter NDPE Supply Chains

Report Webinar Recording

Key Findings:

- Long-term contracts in which buyers can set conditions have been the most effective mechanism to transform the palm oil industry. These contracts have allowed buyers to influence suppliers’ behavior and ensure NDPE-compliant supply chains.

- Non-compliant palm oil still enters NDPE supply chains, sometimes via spot purchases. The term “spot market” refers to purchases outside of long-term contracts. Purchases are business-to-business, made at bulking facilities or auctions, or made indirectly via intermediary traders. The spot market differs from the futures market.

- The logistics of the spot market make conducting due diligence difficult. Although buyers often know from whom they are purchasing, the entire supply base of each purchase is often not provided until buyers take hold of the physical product.

- Current market mechanisms stem more from habit than logistical challenges. Spot purchases also tend to be opportunistic. It is therefore likely that some due diligence in the spot market is possible.

- Buyers that have cleaned up their supply chains risk market access if non-compliant growers continue to access NDPE supply chains via spot purchases. At least seven non-compliant companies have entered the supply chain of Sime Darby via spot purchases since 2017. Buyers will be under increasing pressure to apply the same due diligence to spot purchases as they do to long-term contracts.

- Investors could reduce deforestation risk by being alert to red flags. Leakage risk is highest in CIF contracts and in NDPE refineries renting out storage/bulking capacity to non-compliant palm oil suppliers.

78% of Indonesia and Malaysia refining capacity covered by NDPE policies

Wilmar established the first No Deforestation, No Peat, and No Exploitation (NDPE) policy in 2013. In the subsequent seven years, the palm oil industry has transformed to the point where zero-deforestation has become a clear market access criterion. In Malaysia and Indonesia, which together account for 80 percent of the world’s palm oil refining capacity, NDPE policies cover 83 percent of this refining capacity.

Despite this transformation, sections of the palm oil industry remain linked to deforestation. While 83 percent of Malaysia and Indonesia’s refining capacity is covered by NDPE policies, 78 percent is covered by effective implementation. Of the top 10 palm oil deforesters of 2019, six supply to NDPE supply chains. Four of these companies were already among the top deforesters of 2018. Seasonal forest fires, which persist in Indonesia and Malaysia, are linked to the supply chains of major traders with NDPE policies.

CRR has identified several reasons for the leakage of unsustainable palm oil into international supply chains:

- Weak and inconsistent implementation of policies. Several of the large palm oil traders with strict policies have been accused of weak policy implementation or reluctance on suspending companies that violate policies. Lack of industry consensus on suspension and re-entry requirements have also allowed companies suspended by one company with an NDPE policy to remain in the supply chains of other companies with the same policy.

- The leakage refinery segment. Although NDPE policies cover 83 percent of some refining markets, the 17 percent not covered (rising to 22 percent when assessed on implementation) remains a viable business option for some growers, undercutting the economic leverage that has made NDPE policies so effective and hindering behavior change in growers.

- End-user markets that do not set strict sustainability criteria. Consumer and end-user demand for sustainable or NDPE-compliant palm oil is higher in some markets than others. Some companies previously covered by CRR that were actively clearing forests predominantly sold to markets where sustainability demands are typically weak.

- Opaque corporate structures. Obscuring beneficial ownership or using related entities to create distance from problematic subsidiaries, often referred to as “shadow companies,” allows companies to remain in NDPE supply chains while continuing with unsustainable practices out of sight. The lack of clarity among industry stakeholders on what constitutes a corporate group heightens this threat.

- Lack of uptake of Roundtable on Sustainable Palm Oil (RSPO) certified palm oil. Suppliers report difficulties in selling certified palm oil. A segregated (or Identity Preserved in the context of the RSPO) supply chain that can be traced from grower to end-user is the optimal way to ensure palm oil is deforestation-free. However, end-users have typically preferred to purchase certificates rather than physically segregated oil. Moreover, uptake remains inconsistent throughout different geographical markets. Without segregated supply, deforestation-linked palm oil can still enter supply chains.

An additional leakage factor can be identified in the different ways that physical palm oil, either crude palm oil (CPO) or crude palm kernel oil (CPKO), enters supply chains. CRR has identified spot purchases as a leakage risk (See end of report for definitions of spot market terms). Spot purchases are one-off purchases usually made by traders to plug a supply shortfall at their refineries.

Economic leverage applied via long-term contracts

The trade relationship between a CPO/CPKO oil supplier and a buyer is most typically governed by long-term contracts. The length of these contracts differs, but they are typically between three to nine months. Under this type of contract, palm oil is physically delivered from mill directly to the refinery with few other actors involved (i.e brokers or middlemen). Discussions with buyers in the industry indicate most of the trade between suppliers and buyers is covered by long-term contracts. However, given that data on volumes or percentages of the market covered is not publicly available, the capacity to fully analyse the market and assess sustainability risks is limited.

Long-term contracts allow for the most effective implementation of NDPE due to buyers’ ability to set conditions of trade. For example, if a buyer has an NDPE policy, conditions can include the sharing of concession maps, committing to full NDPE compliance, or recovering previously degraded areas. These conditions also allow buyers to add a clause allowing cancellation of the contract for policy infractions.

These long-term contracts are often the preferred type of contract between supplier and buyer because of the stability afforded. This stability and corresponding economic incentive to retain contracts has helped drive transformation of the industry. By using their purchasing power to demand stop work orders, conduct High Carbon Stock (HCS) assessments and implement necessary remedial action, buyers have stopped destructive practices on concessions and ensured company group adherence to NDPE policies. There are several examples in public grievance lists of companies that have adopted stop work orders or conducted HCS assessments after engagement by their buyers (three examples include IOI and NPC Resources, Musim Mas and Anglo Eastern Plantation or Wilmar and Gama).

NGOs will often discuss engagement strategies or specifically pressure a buyer to engage or suspend a supplier. This type of action typically occurs in long-term contract relationships.

Spot purchases allow suppliers to access NDPE markets

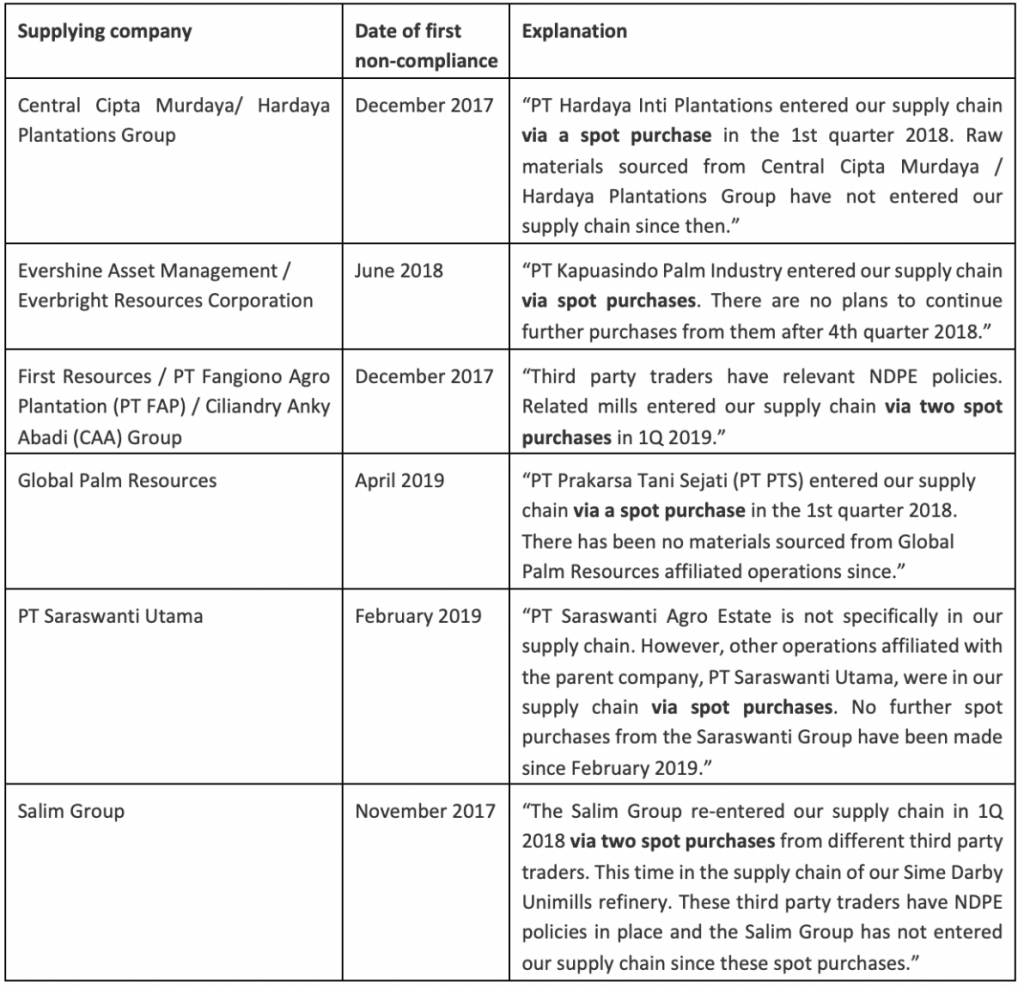

Some non-compliant or suspended companies have appeared in the supply chains of NDPE companies via spot purchases. Spot purchases are made outside of long-term contracts and are often only known if the case is raised publicly and the buyer offers an explanation via a statement or on its grievance list. One example is the Indonesian oil palm developer Saraswanti Group, whose PT Saraswanti Agro Estate in West Kalimantan was clearing habitat of the Bornean orangutan in 2019. The company was connected to the supply chain of Sime Darby, which has a program to remove deforestation-linked palm oil from its supply chain. Sime Darby issued a public statement and reported the case on its grievance list. Sime Darby explained that palm oil from Saraswanti entered its supply chain via spot purchases and that it does “not have a standing purchase contract with the company” and “No further spot purchases from the Saraswanti Group have been made since February 2019.”

Five other suppliers on Sime Darby grievance list also entered its supply chain via spot purchases, the company says (Graphic 1). The implications are that buyers operate differently in the spot market compared to long-term contracts and/or NDPE policies are not being applied to spot purchases.

Graphic 1. The six companies listed on the grievance list of Sime Darby that entered their relationships via spot purchases.

*CRR uses the example of Sime Darby because the company specifically discusses spot market purchases on its grievance list. Other companies may make similar purchases but use different terminology.

Spot purchases make up a small fraction of Sime Darby’s total purchases

Sime Darby confirmed to CRR that volumes contributed by individual mills from spot purchases accounted for a small fraction of the total volumes bought and traded every year. Although the company does not provide volumes, spot purchases from Global Palm Resources and PT Saraswanti in 2019 represented just <0.015 percent of its total supplies for the year.

Between January 2016 and April 2020, the Indonesian palm oil grower Palma Serasih cleared approximately 3,400 hectares (ha) of forest on its PT Nusantara Agro Sentosa estate and approximately 3,000 ha of forest on PT Global Primatama Mandiri, both in East Kalimantan. In response to this ongoing clearance, buyers with NDPE policies suspended Palma Serasih. According to Palma Serasih’s most recent financial statement, for the first three months of 2020, Sime Darby accounted for 31.61 percent of its revenue in this period, second to trader Louis Dreyfus Company (LDC), which accounted for 45.97 percent. According to LDC’s grievance list, it has engaged with Palma Serasih about ongoing deforestation. This level of engagement indicates LDC deals with Palma Serasih via long-term contracts.

In response to questions for this report, Sime Darby confirmed to CRR that it had made two spot purchases at the end of 2019 and beginning of 2020 from Palma Serasih. Sime Darby did not provide volumes for these two purchases.

Buyers and sellers use the spot market but long-term contracts preferred

It is not clear to what extent spot purchases by refiners are opportunistic or part of a specific business strategy. When they are opportunistic, companies use spot purchases as a way of plugging shortfalls in capacity or taking advantage of useful stock that may suddenly be available at an attractive price. Similarly, it is not always clear whether suppliers use the spot market as a stop gap when they have surplus supply that is not covered by long-term contracts or the spot market is preferred because of the freedom it affords.

Whether the spot market is part of a wider business strategy can occasionally be seen in companies’ public documents and submissions. For example:

- Bakrie Sumatra Plantation’s 2018 annual report refers to “fatty acid…targeted for spot market in both local and export markets.”

- The 2015 annual report of Sawit Sumbermas Sarana (SSMS) states: “The Company strategy sells its products directly to customers without the intermediary of a third party. The Company uses a sales system which is based on spot and negotiate the delivery terms on each sale. In accordance with the practice commonly used today for the spot market in Indonesia, the customer pays the Company’s CPO and PK at the maximum of five working days after the sale contract was agreed…”

- A 2014 Credit Suisse paper refers to the Malaysian oil palm developer Genting selling “the bulk of its palm oil on the spot market, and hence should benefit significantly when palm oil prices rally.”

- The Malaysian bank CIMB’s 2009 sector update report identified Indofood Agri and London Sumatra as high earners because “both companies have also timed their fertiliser purchases well and sell almost all their crops on the spot market…”

- Gozco Plantation’s 2009 financial statement says: “PT SA, Subsidiaries sale of crude palm oil to domestic Indonesian customers is priced with reference to the spot market prices for palm oil set at a daily auction sale among Indonesian palm oil produces and their customers, which is conducted in Medan, North Sumatra….”

- In its 2007 annual report, Sinar Mas Agro Resources and Technology (SMART) stated: “When CPO prices are high, our CPO profit margins may be higher than on our value-added refined palm oil products. We may therefore sell a greater proportion of CPO directly to the spot market, at the expense of refining this CPO at our downstream refinery operations….”

- In its 2007 Initial Public Offering, the Indonesian company First Resources stated that they “sell most of our crude palm oil in the domestic spot market. These sales are made in Rupiah, based upon prevailing international U.S. Dollar prices for crude palm oil…”

The reference to the spot market by SSMS in 2015 is noteworthy. In 2Q of that year, refiners GAR, Wilmar and Apical accounted for 58 percent of SSMS’s revenue, before all suspended the company because of policy violations. Purchasing agreements with Unilever and IFFCO ended in 2017 and 2018 respectively. In 2017, SSMS generated 42 percent of its revenue from three companies: the Singaporean traders Just Oil & Grain Pte Ltd and Global Trade Well Pte Ltd, and the Indonesian company PT Panca Nabati Prakarsa. As Palma Serasih shows, percentages of sales as high as 31.61% can be derived from spot purchases, and information about what type of contract SSMS had with these three companies was not available. However, SSMS now sells 86 percent of its produce to PT Citra Borneo Utama, a new refining company to which SSMS is related. This connection implies that SSMS prefers a system with more stability or control.

Whether the Malaysian company Genting predominantly sold CPO on the spot market in 2014 is difficult to determine. Public supplier lists and grievance lists were not the norm at the time, although Genting was already the focus of an RSPO complaint. In 2020, Genting appears as a direct supplier in the supply chains of several trader/refiners, including Fuji Oil, IOI, Itochu Corporation, KLK, Musim Mas, Nisshin OilliO, Sime Darby and Wilmar. Therefore, Genting’s business strategy has likely turned its focus to long-term contracts in the NDPE market.

Similarly, First Resources now sells CPO directly to the following traders: KLK, Musim Mas, Neste Oil and Wilmar. First Resources also has its own refineries, with an annual capacity of 850,000 metric tons (MT). Given this refining capacity and the number of buyers, it is unlikely First Resources is selling significant amounts of palm oil on the spot market.

The Indonesian grower Astra Agro Lestari sells CPO at auction, with spot purchases bought by the Indonesian traders Permata Hijau and Musim Mas. Musim Mas is one of the leading NDPE traders in Indonesia, with a public supplier list and grievance list. Permata Hijau published its list of mill suppliers and a grievance list in April 2020. The supplier list includes standard transparency information such as whether the supply is RSPO certified and location of mills. These details indicate that both refineries have a high degree of knowledge of their supply chains and are using their buying power to work with suppliers to increase transparency. Therefore, spot purchases are likely made in addition to their standard long-term contracts.

Although CRR has heard anecdotally of companies suspended by the NDPE market selling palm oil on the spot market, no publicly available evidence confirms these rumors. Evidence suggests that palm oil suppliers prefer to enter into long-term contracts, while the spot market is used as a stop-gap measure when market opportunities decrease or palm oil prices are not favorable, rather than as a long-term business strategy. Some non-compliant palm oil suppliers choose to enter long-term contracts with buyers that disregard NDPE policies, even though NDPE traders/refiners often offer higher prices and more regular payments. This is the reason why some suppliers make the strategic decision to comply with sustainability requirements.

Mechanisms of the palm oil spot market

Publicly available information about the spot market and how it functions is limited. To understand how the spot market works, CRR conducted interviews with several personnel from large NDPE palm oil traders in Indonesia and Malaysia. They identified the following mechanisms as being key to the spot market trade.

Business-to-business one-time purchases

In some cases, the refinery/area manager will reach out to companies in the same area to purchase needed supplies. The choice of this one-time supplier often depends on the location of the mill and its distance to the refinery. The choice of supplier can also be driven by the reputation of the company and the perceived reliability or quality of its product. Often, the personal relationships of the refinery manager determine the choice.

These purchases can also work both ways. Refiners told CRR that it is not uncommon that they are approached by millers in their area and offered one-off purchases of CPO/CPKO.

Purchases from bulking stations

Bulking stations are usually located at refineries or ports and are used to store CPO/ CPKO. Most refiners own bulking stations. Felda owns one of the largest in the world in terms of capacity in Johor, Peninsular Malaysia. Third-party companies sometimes rent bulking stations from the owners. Millers not operating on long-term contracts can rent these bulking stations, or they can sell their CPO to the station owners to be added to a mix, in the hope that it will be bought at port. Refiners, either directly or via agents working at the ports, can approach bulking stations and make one-off purchases.

In some cases, palm oil companies sell their palm oil housed in bulking stations through tenders. A company may buy a specific amount of palm oil and pay the price upfront. They receive the palm oil after the tender is complete. Buyers do not know who provides this palm oil or its source and usually receive the supplier list at the same time as the palm oil.

Palm oil auctions

Palm oil is also purchased at auctions. Auctions often take place in major urban centres like Jakarta and Medan, and/or near key ports. At these auctions, palm oil producers list their palm oil for sale and buyers place bids. Auctions are for either local or international markets. As mentioned above, coverage of an auction held by Astra Agro Lestari shows that Musim Mas and Permata Hijau bought CPO from Astra in this way. At this auction, Astra managed to sell 7,000 MT out of an offered 16,000 MT.

Auctions typically refer to the trade in futures contract, and the physical product is not provided immediately. However, CRR has been told that auctions also take place while a shipment of palm oil is on its way to a final destination. So, if a shipment of palm oil is arriving at a port, buyers can bid for palm oil on the ship and take ownership of the product when it arrives.

Direct and indirect purchases

Palm oil supply chains are complex, and supply occasionally changes hands many times as it goes from source to end-user (sometimes going through four or five intermediaries). The most straightforward purchase is a direct purchase, which goes from a mill direct to a trader/refiner. In direct trading relationships, when the two parties know each other, a degree of engagement between supplier and buyer usually occurs. In indirect relationships, the last or intermediary buyer usually does not know the supplier. Engagement takes place only between the supplier and the first buyer.

In the NDPE market, buyers usually list their suppliers on their public mill lists. These lists include direct and indirect long-term contract suppliers and spot suppliers. If supply is segregated, the buyer lists only the supplier of that segregated supply. If supply is not segregated, the buyer must list every supplier that has entered the refinery they are buying from, as the supply may have been mixed. Many grievance lists refer to indirect purchases, which shows that NDPE companies are highly exposed in indirect supply chains.

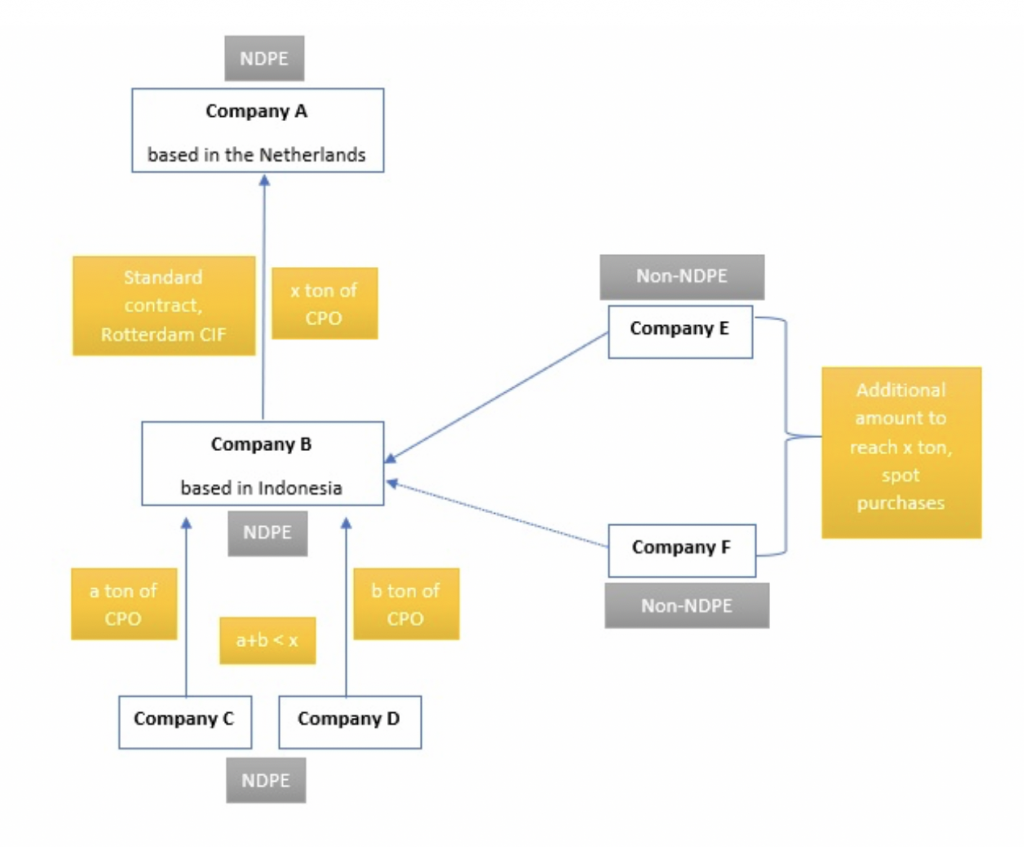

International supply chains are typically facilitated by Cost, Insurance, and Freight (CIF) and Free-On-Board (FOB) contracts. CIF and FOB contracts are between a supplier and buyer and usually the only difference between them is the way freight costs are covered (see definition of market terms at the end of the report). The CIF and FOB markets likely differ via geographical region. The European market has the most information available. For the traders CRR spoke to, a majority of their exposure is in the European market. In Europe, the CIF system is, traders say, the most dominant and is referred to as CIF Rotterdam.

Buyers of CIF products usually have little leverage over the seller in the Rotterdam markets as they only become aware of the product’s origin at the time of delivery. Purchases are often made from bulking facilities or traders. The supply will often already be mixed at the time of sale, often by as many as 10 individual mills. Buyers are given a list of suppliers when they take physical ownership of the oil in Rotterdam. In this scenario, a company that actively decided to not enter a long-term contract with a company may have just bought CPO from the same company in a one-off spot purchase.

The trade is complex and will vary depending on the trader and geographic region, as outlined in Graphic 2:

Graphic 2: Spot purchases entering supply chains via shipments from Indonesia to the Netherlands

Impediments to NDPE compliance

A consistent theme in discourse about the spot market is that current market mechanisms make implementing NDPE policies difficult. Reasons highlighted include the lack of transparency in the market; supply chains are complex and buyers’ exposure is indirect; and the very nature of a one-off transaction removing any incentives for the supplier to commit to NDPE. Underpinning all of these issues is that information about the supply base is not provided until after a purchase is made.

However, it is unclear to what extent these issues are logistical or habits that market players have picked up and could be rectified with rigorous application of NDPE policies. In one-off business-to- business transactions, companies can apply due diligence easily. Due diligence requires a sustainability team with knowledge of industry players or systems in place to verify the sustainability performance of particular companies, communication of sustainability requirements across all business departments, and put procedures in place to stop rogue purchases.

When purchasing from bulking facilities, some companies report that they receive the list of suppliers only when they physically receive the supply of palm oil. However, it is unclear why buyers cannot insist on a list of suppliers before any purchases are made. If the bulking station refuses, the buyer could avoid proceeding with the transaction. Likewise, if NDPE traders buy spot purchase at an auction, they in theory know who the seller is and can decide whether to make a purchase based on the sustainability performance of that supplier.

In the CIF Rotterdam markets, traders also claim the source of the palm oil is only provided when the product is physical delivered. CRR was not able to obtain an example of a typical contract for this type of purchase. However, the Federation of Oils, Seeds and Fats Associations Ltd (FOSFA) claim that 85 percent of the global trade in oils and fats is traded under FOSFA contracts. A contract template for CIF purchases on its website shows that contracts are signed between the seller/s and buyer/s, with brokers also listed. There is no contractual requirement to list all the companies that have contributed to the product being traded, and the “origin” of the contracts refers to the origin country rather than specific companies.

If this contract is the template used for contracts in the CIF Rotterdam market, it indicates that buyers are aware of which company is physically delivering the oil they are purchasing. However, no contractual requirement exists for companies to state which other companies are in that particular supply.

Making spot purchases risks market access

If NDPE policies cannot be applied to spot purchases, companies risk shortfalls in supply and the associated economic losses. However, they enable the leakage market and also risk market access if non-compliant suppliers enter their supply chains. Companies adopting a policy of not making spot purchases is unlikely, as spot purchases are considered a necessary way of plugging shortfalls or responding to unpredictable circumstances.

However, current spot market mechanisms are undermining NDPE supply chains by allowing entry to non-compliant companies. There has been increased focus in 2020 on how to disassociate the palm oil industry from deforestation. Many buyers are still enhancing due diligence in order to ensure deforestation-free supply chains, even in their long-term contracts. The spot market is an additional threat. As transformation of the palm oil industry has been driven by the exclusion of non-compliant suppliers, buyers that continue to make purchases from the spot market without conducting due diligence may face increasing market access risk.

Appendix

Definition of market terms:

The term ‘spot’ is commonly used for any sale or transaction that takes place outside of long-term contracts. It is essentially the practice where the commodity is bought immediately or at short notice. The delivery usually takes place two days after the deal is made. Transactions are settled in cash and at the current market price. The spot market can also take place formally at exchanges or over the counter.

The physical trade in palm oil takes two forms, Cost, Insurance, and Freight (CIF) trading and Free-On-Board (FOB) trading. CIF refers to spot purchases where the cost already includes sea freight charges, insurance, and the product is delivered to the nearest port. FOB is similar except the seller is responsible for delivering the commodity to the nearest port and the costs of the ship’s freight and insurance is borne by the buyer and is additional to the cost of the commodity. CIF trading is how most palm oil enters Europe. In the European context it is referred to as CIF Rotterdam, as Rotterdam is the main entry into Europe. This report is using the CIF Rotterdam market as its example. CIF markets may differ in different geographical regions.

This spot market should not be confused with the futures market or the forward market: The futures market refers to business-to-business contracts between a seller and a buyer, settled directly or through banks or brokers as intermediaries. Terms and conditions such as product needed, price, quantity and delivery dates are agreed in advance, no matter the future price variation. Futures contacts can be exchanged and change hands multiple times, but whoever holds the contract at the delivery date has to take on the physical supply. The futures contract always takes place through an exchange and is highly standardized.

The forward market refers to contracts between a buyer and a seller, off exchange. This type of exchanges are conducted informally (Over-the-Counter marketplace), over the phone or via online communication tools. Final deals are usually made on a bilateral basis or through a counterparty clearing house. Terms and conditions are also agreed in advance, similar to the futures market.