Procter & Gamble (P&G) is a NYSE-listed multinational consumer goods company headquartered in Cincinnati, Ohio. P&G provides branded products and services in the home and personal care sectors in more than 180 countries. The company has a No Deforestation, No Peat, No Exploitation (NDPE) policy that covers all third-party suppliers, and it has committed to developing a traceable supply chain. P&G applies its responsible sourcing policy at the supplier group level, but relies on intermediary traders to engage with non-compliant growers and ensure a clean supply chain. In July 2019, P&G changed its organization design to six Sector Business Units (SBUs). It has decentralized responsibility for supply chains across its new business units.

Download the PDF here: Procter & Gamble’s Deforestation Exposure May Affect Reputation

Key Findings:

- The bulk of P&G’s procurement of palm oil products comes from non-certified sources. P&G uses substantially more palm kernel oil than crude palm oil, at 296,610 metric tons per annum compared to 33,557 tons per annum. While 100 percent of its palm oil is RSPO certified, only 10.1 percent of its palm kernel is. Limited volumes of available physically certified palm kernel have constrained P&G.

- P&G has not updated its supplier list of palm oil mills since 2017. The list features 15 companies that had active forest or peatland clearance in their owned or affiliated landbanks in 2016-2019. These include Tabung Haji, Fangiono Agro Plantations, Ta Ann, and Kalimantan Sawit Kusumas.

- P&G’s reliance on actions taken by its direct suppliers in cases of non-compliance may not fully mitigate its reputational risks. P&G confirmed to CRR that non-compliant suppliers enter its supply chain via Wilmar and Musim Mas. P&G relies on actions taken by these traders. CRR findings confirm that non-compliant suppliers remain in P&G’s supply chain.

- P&G’s USD 41 billion reputation risk, equal to 14 percent of its equity value, dwarfs the cost of solutions. Besides reputation risk, market access risk, particularly related to zero-deforestation commitments of European customers, could be valued at USD 24 billion, and financing risk at USD 1.5 billion. Meanwhile, the DCF value of annual monitoring, implementation costs and RSPO certified palm oil would amount to USD 175 million.

Procter & Gamble owns multiple globally recognized brand products

Procter & Gamble (P&G) is a NYSE-listed multinational consumer goods company headquartered in Cincinnati, Ohio. P&G provides branded products and services in the home and personal care sectors. P&G’s brands include Pampers, Tide, Ariel, Always, Pantene, Old Spice, Bounty, Dawn, Febreeze, Gain, Charmin, Downy, Ace, Crest, Oral-B, Olay, Tampax, Head & Shoulders, Gillette, Braun, Fusion & Vicks. P&G employs circa 97,000 employees globally and has operations in approximately 70 countries. Its products are sold in more than 180 countries.

Walmart and its affiliates are P&G’s biggest customers, representing approximately 15 percent of P&G’s total sales in 2018-19. No other customer represents more than 10 percent of total sales. P&G’s products are mainly sold through retail channels, wholesalers, and online.

In July 2019, P&G changed its organization design to six Sector Business Units (SBUs). These six SBUs (Fabric and Home Care, Baby and Feminine Care, Family Care and P&G Ventures, Beauty, Grooming, and Health Care) manage P&G’s ten product categories (hair care, skin and personal care, grooming, oral care, personal health care, fabric care, home care, baby care, feminine care and family care).

Procter & Gamble has decentralized responsibility for supply chains across its new business units. In its 2019 annual report, P&G states that the SBUs “will be responsible for global brand strategy, innovation and supply chain.” P&G also aims to cut costs in its supply chain through investments in “multi-category manufacturing sites” in geographically strategic locations. In markets that are particularly important to P&G, such as the United States and China, the new business units have more freedom and responsibility for their supply chains.

P&G uses relatively little palm oil, but it does use substantive amounts of palm kernel oil. In 2018, Procter & Gamble used 33,557 tons of crude and refined palm oil and 296,610 tons of palm kernel oil.

Procter & Gamble has publicly committed to zero-deforestation, but implementation is lacking

P&G has a No Deforestation, No Peat, No Exploitation (NDPE) policy and has committed to developing a traceable supply chain to ensure its suppliers commit to the following:

- No development of High Conservation Value (HCV) areas and High Carbon Stock (HCS) forests

- No new development of peat lands regardless of depth

- No burning to clear land for new development or replanting

- Respect for human and labor rights

- Respect land tenure rights, including rights of indigenous and local communities to give or withhold their free, prior and informed consent for development of land they own legally, communally or by custom

P&G also commits to “work with suppliers, industry peers, NGOs, academic experts and other stakeholders to promote consistent industry standards and practices in palm oil sourcing with the aim of achieving full traceability and eliminating deforestation.” P&G has been a member of the RSPO since September 2010 and signed the New York Declaration on Forests in September 2014. Through its membership of the Consumer Goods Forum, the company has committed to zero net deforestation in its supply chain by 2020.

The scope of P&G’s policies applies to its suppliers on a company group level. P&G indicated to CRR that it expects compliance across a supplier’s enterprise-wide operations. The company also said that it has been acting accordingly in cases of non-compliance. In 2017 and 2018, P&G conducted a risk assessment of palm oil mills in their supply base in order to map high-risk mills based on presence of deforestation risk factors in the area surrounding the mill. The company assessed 1,269 mills and identified ~90 (~7 percent) as high risk. The majority of these (>85 percent) were third-party mills used by direct suppliers. P&G has committed to future verification efforts on sourcing areas characterized as high risk according to their risk assessment.

The bulk of P&G’s annual procurement of palm oil products comes from non-certified sources. In P&G’s latest available RSPO Annual Communication of Progress (ACoP) report, submitted for 2018, the company said it used 33,557 tons of crude and refined palm oil and 296,610 tons of crude and refined palm kernel oil annually. P&G said that 100 percent of its palm oil was certified under the RSPO’s mass balance and segregated schemes in 2018. Of the 296,610 tons of palm kernel oil used, just 30,030 tons (10.1 percent) were certified. According to its 2018 citizenship report, the company’s certified palm kernel figure was even lower, at just five percent. P&G indicated to CRR that it is constrained by limited volumes of physically certified palm kernel oil supply in the market.

P&G most recent list of palm oil mills covers the year 2017. It was released in February 2018, after Greenpeace called on the company to disclose the names of its supply mills and the company groups that control these mills. P&G also does not publicly disclose which palm oil traders and refiners and specific mills it is exposed to. However, the company indicated to CRR that Wilmar and Musim Mas are its direct suppliers. In a written submission to CRR, P&G clarified that it will update its public supplier list annually. The next mill list, for July 1, 2018 to June 30, 2019, will appear in its next Citizens Report, due out in December 2019.

Industry best practice requires the publication of mill list updates on a quarterly or biannual basis. Resolution GA15-6B, passed by the RSPO at its annual RT conference in November 2018, commits companies engaged in primary procurement of palm oil products to update their public supplier lists every quarter. Through the resolution, RSPO will extend this commitment to secondary procurers by the end of 2019.

P&G appears to rely on actions by its direct suppliers in the case of non-compliance. In response to the list of non-compliant suppliers in P&G’s mill list (see below), P&G referred to actions taken by Wilmar and Musim Mas. It remains unclear to what extent P&G undertakes its own monitoring, due diligence or supplier engagement.

Multiple suppliers are non-compliant with P&G’s NDPE policy

P&G’s 2017 supplier mills list contains several companies that actively cleared in their own or affiliated landbanks. Several have seen deforestation activities continue in 2018 and 2019. It is, however, unclear if any of these suppliers were identified as being high risk in P&G’s mill assessment.

P&G confirmed to CRR that these suppliers appear in its supply chain via Wilmar and Musim Mas. Of these 15 companies, P&G states that six (IndoAgri, Tunas Baru Lamung, Prosper, Tabung Haji, Austindo Nusantara Jaya and DD Plantations) are no longer in its supply chain. Eight of the remaining nine suppliers (bar Sarawak Oil Palm/ Shin Yang) have been engaged by either Wilmar or Musim Mas. It is unknown whether P&G also engages directly with growers that are non-compliant, or if it relies solely on the intermediary trader.

Figure 1: Deforestation by suppliers (from 2016 to 2019) on P&G’s list

*As indicated by P&G to CRR

Source: Aidenvironment

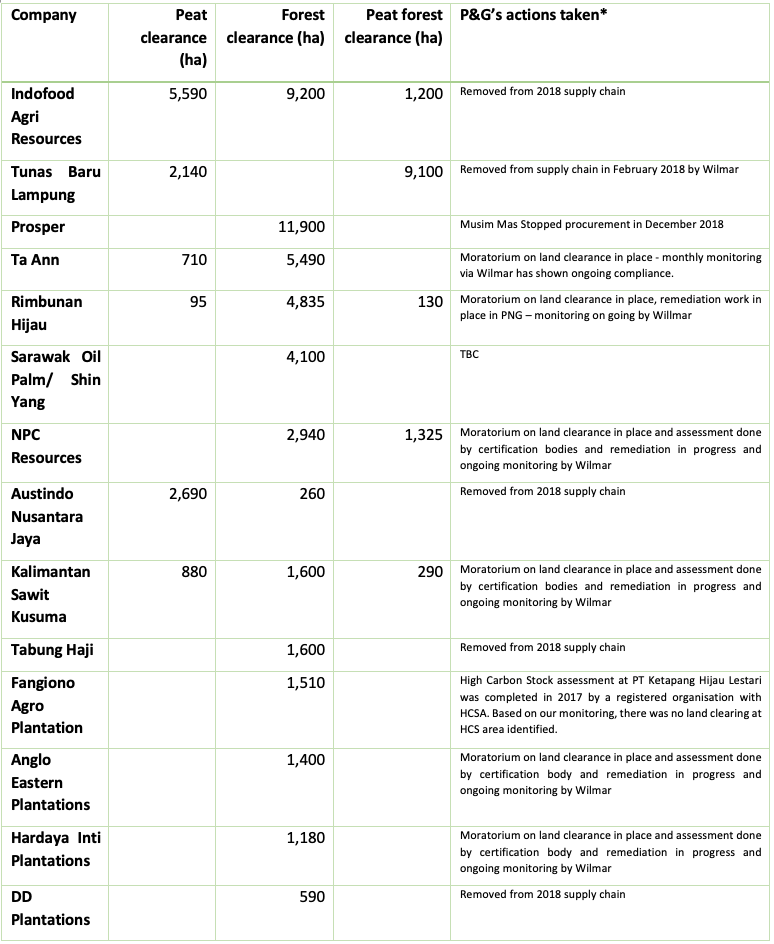

Case study 1: Ta Ann and related companies cleared 6,505 ha of forest and peat

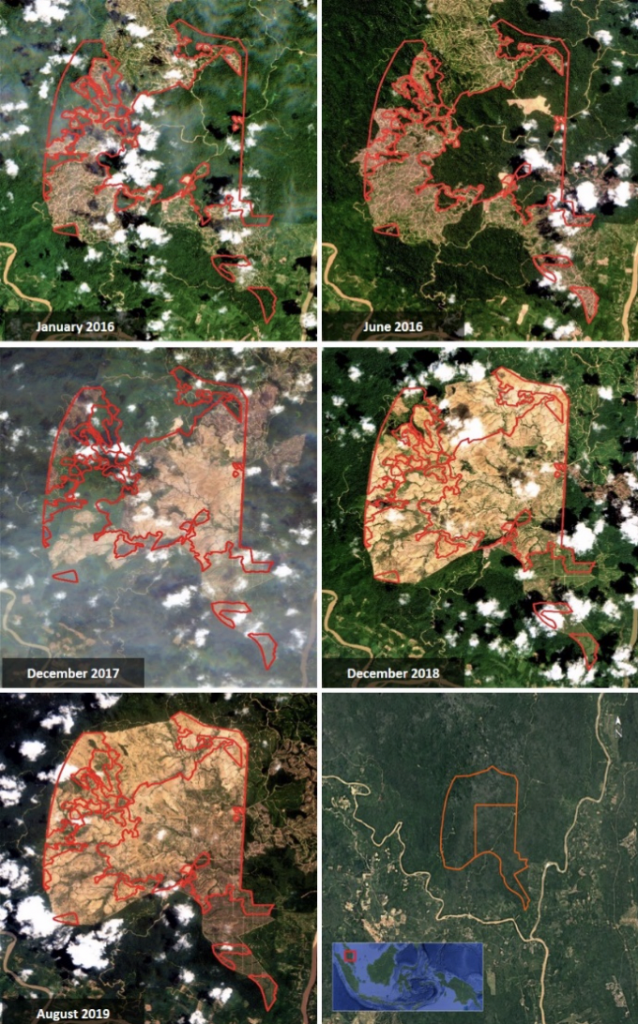

Ta Ann Holdings Berhad, a listed Malaysian company operating in Sarawak, features in P&G’s supply chain through its Manis Oil Sdn Bhd mill. Ta Ann, a privately-owned company, is linked, through its shareholders, to several other companies active in land development. Tan Ann Holdings Berhad is the largest shareholder in the Bursa Malaysia-listed Sarawak Plantation Berhad (Figure 2).

Five oil palm plantation companies owned by Ta Ann and Sarawak Plantation Berhad cleared an estimated 6,505 hectares of forest and peat in Sarawak between January 2016 and August 2019.

- Sarawak Plantation’s company Tellania Oil Palm Sdn Bhd developed 710 ha of peat between August 2016 and August 2019.

- Ta Ann Pelita Ngemah cleared 2,460 ha of forest between January 2016 and August 2019.

- Ta Ann Holdings’ company Ta Ann Pelita Baleh Sdn Bhd cleared 3,030 ha of forest between January 2016 and August 2019.

P&G indicated that Ta Ann has issued a moratorium on land clearing and that Wilmar’s monthly monitoring shows the company is in compliance. However, Wilmar’s grievance list has not been updated since July 2019, while deforestation has been detected as recently as August 2019.

Figure 2: Deforestation on Ta Ann Pelita Ngemah in Sarawak between December 2016 and August 2019

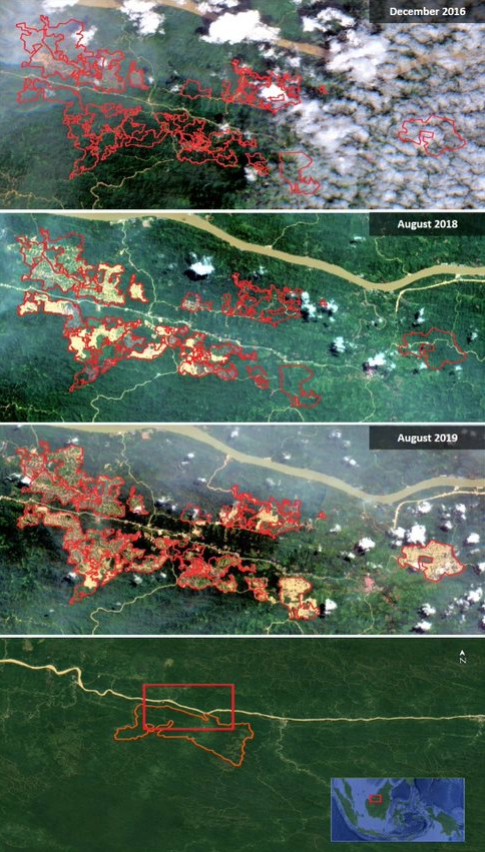

Case study 2: Kalimantan Sawit Kusuma deforested 2,775 ha

PT Kalimantan Sawit Kusuma (KSK) is a company group that operates plantations in the districts of Sambas, Kubu Raya, and Ketapang in West Kalimantan, and in the Sukamara district in Central Kalimantan. KSK owns over 50 percent shares of three oil palm plantation companies: PT Kalimantan Sawit Kusuma, PT Fajar Saudara Lestari, and PT Mitra Saudara Lestari. Both PT Kalimantan Sawit Kusuma and PT Fajar Saudara Lestari on P&G’s 2017 palm oil mills list.

KSK has actively cleared forest and peat on several concessions;

- PT Fajar Saudara Lestari cleared 845 ha of forest and 340 ha of peat between May 2017 and October 2018.

- PT Mitra Saudara Lestari cleared 665 ha of forest from November 2016 to October 2018.

- PT Kalimantan Sawit Kusuma cleared 65 ha of forest, 490 ha of peat, and 230 ha of peat forest between April 2017 and November 2018. The clearing happened in areas considered habitat of the Bornean orangutan (Pongo pygmaeus).

Although deforestation has slowed in 2019, 30 ha of forest, 60 ha of peat forest, and 50 ha of peat have been cleared on the PT Kalimantan Sawit Kusuma concession this year.

P&G indicated that a moratorium on land clearance is in effect. It added that certification bodies are carrying out assessments and a remediation process and that Wilmar is conducting ongoing monitoring. However, this case does not feature on Wilmar’s grievance list, and no further information is available about the issue date of the moratorium.

Figure 3: Deforestation and peat clearance on PT Kalimantan Sawit Kusuma between March 2016 and November 2018

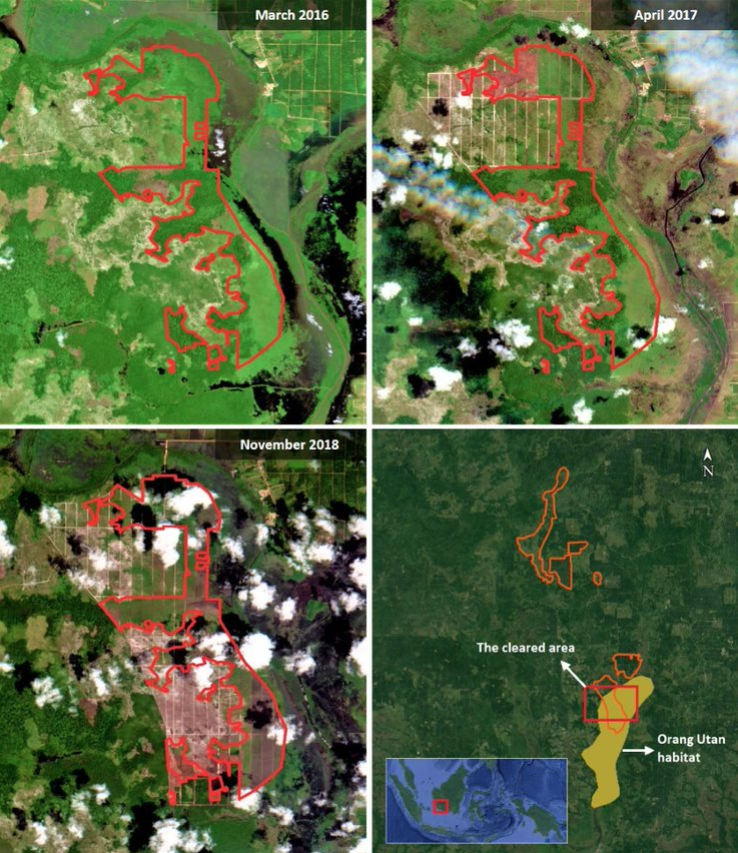

Case study 3: 1,515 ha deforestation at Fangiono Agro Plantations concessions

PT Fangiono Agro Plantation (PT FAP) is an Indonesian palm oil plantation company with a landbank of 136,496 hectares in Kalimantan and Sumatra and five CPO mills in Kalimantan. PT FAP features twice on P&G’s palm oil mill list, through its Bhumi Simanggaris Indah and Karangjuang Hijau Lestari mills.

PT Fangiono Agro Plantation is 95 percent owned by Prinsep Management Ltd, a trust based in the British Virgin Islands. PT Perkasa Fangiono True, which is managed by the Fangiono family, owns the remaining 5 percent. The family is also the owner and controller of the Singapore-listed First Resources Ltd and the Indonesian company PT Ciliandry Angky Abadi.

Between June 2016 and August 2019, PT Fangiono Plantation’s PT Ketapang Hijau Lestari cleared 1,360 ha of forest on its concession. The company also cleared 155 ha of forest between February 2017 and May 2019 on its PT Tirta Madu Sawit Jaya concession.

P&G, however, indicated that Wilmar’s monitoring showed no clearing on land identified as High Carbon Stock during a 2017 assessment by a registered HCSA organization. While the HCS assessment for this concession is registered on the HCSA website, it is not publicly available. Wilmar is also awaiting a full copy of this assessment.

Figure 4: Deforestation on PT Ketapang Hijau Lestari between June 2016 and August 2019

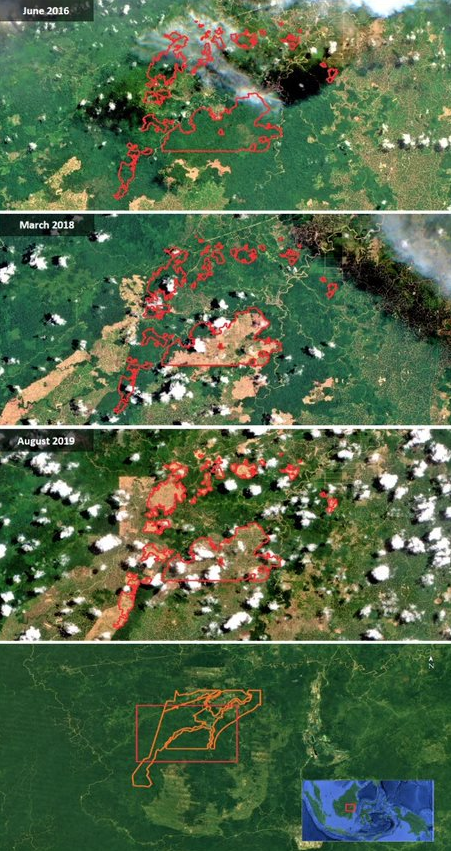

Case study 4: 1,600 ha of forest cleared by Tabung Haji

TH Plantations, a subsidiary of Malaysian government-linked company Tabung Haji, features eight times on P&G’s 2017 palm oil mill list. CRR reported on peat and forest clearance on TH Plantations’ subsidiaries PT Persada Kencana Prima concession in North Kalimantan and Hydroflow in Sarawak.

In 2017, TH Plantations’ subsidiary THP Agro Management Sdn Bhd submitted an Environmental Impact Assessment (EIA) for a 1,619 ha concession in Pahang, Peninsular Malaysia. In 2018, another EIA was submitted for 2,428 ha. In the EIA, THP Agro Management Sdn Bhd described the area as a “mixed flat, rolling and hilly area…Other than forest, the land use surrounds the Project site is agriculture, which (sic) mainly rubber and oil palm plantations.” Satellite analysis by CRR indicates the concessions are within the Yong Forest Reserve.

Although EIAs are expected to be submitted and approved before any development, approximately 1,600 ha of forest have been cleared in the two concessions since February 2017. As of August 2019, the concession has been completely cleared of vegetation.

P&G indicated that TH Plantations has been removed from its supply chain in 2018, but the company did not provide any further details. As both P&G’s direct suppliers Wilmar and Musim Mas continue to source from TH Plantations, its supplies could continue to enter P&G’s supply chain inadvertently.

Figure 5: Deforestation on THP Agro Management Sdn Bhd concession in Pahang between January 2016 and August 2019

Supply chain deforestation may expose P&G to reputational risks

As an end-user of palm oil and well-known brand company, P&G is exposed to reputational risks as a result of the continued presence of deforestation and peatland clearing in its supply chain. P&G has acknowledged that it will fall short of its goal of zero deforestation by 2020. Failing to meet a publicly stated objective could undermine the company’s reputation, as companies may become targets of civil society campaigns and negative media attention. Moreover, P&G could score below its peers in sustainability benchmarks. In 2014, prior to committing to zero-deforestation, P&G was subject to a Greenpeace campaign, and the campaign group engaged the company again in 2017. The company is also the focus of a recent civil society campaign around the threat of its pulp and paper use to Canada’s boreal forests.

P&G’s reliance on actions taken by its direct suppliers in cases of non-compliance may be inadequate to fully mitigate this risk. Following best practices by downstream companies, P&G could improve its own monitoring and due diligence to ensure that non-compliance is adequately acted upon. This point is further illustrated by the recent reappearance of Double Dynasty in Wilmar’s supply chain, despite Wilmar’s grievance list saying that it stopped purchasing from Double Dynasty in April 2019. Double Dynasty’s owners have been accused of illegal land clearing as recent as October 2019.

Financial Risk Analysis: Valuing remedies and risks

The potential value impact of deforestation-related risks is relatively large versus the costs of measures to improve execution and the costs of stranded assets. This is the conclusion of the value analysis in the following section. Currently, after a long period of stagnant growth, recent quarters have shown accelerating revenues. As a consequence, the share price has moved up and the relative valuation versus peers now shows a high premium.

Investors have been focused on operational improvements

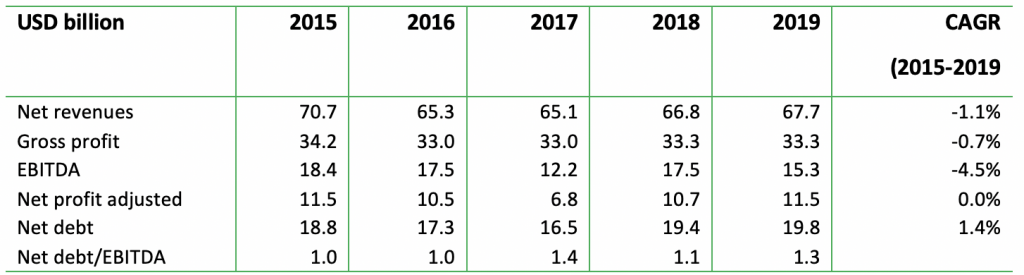

P&G’s financial performance has remained stable over the past five years (2015-2019). In 2019, organic revenue growth was 5 percent with 2 percent volume growth, as compared to FY2018. Meantime, EBITDA declined by 12 percent, primarily due to the accounting adjustments to the Gillette Shave Care business. The five-year CAGR shows a slight negative return for revenues, gross profit, and EBITDA. Net profit CAGR stands at zero percent.

In recent quarters, P&G showed accelerating revenue growth. P&G reported Q1 2020 (July-Sep 2019) net revenues of USD 17.8 billion, an organic increase of 7 percent versus the prior year. The Q1 organic growth was a continuation of a strong 4Q18, when P&G started to outperform its competition. The company paid USD 1.9 billion of dividends and repurchased USD 3 billion of common stocks. The dividends and buybacks followed a USD 12.5 billion return to shareholders in FY 2019 through USD 7.5 billion of dividend payments and USD 5 billion of direct share repurchases. Despite these programs, P&G’s net debt/EBITDA ratio has stabilized for the past five years at around 1x. This multiple is safe for P&G creditors.

Figure 6: Key financial figures (as of June 30)

Source: P&G AR 2019, Bloomberg

Solutions would have a low cost

The measures to improve implementation of responsible sourcing policies carry a relatively low cost of 0.06 percent of the current equity value. Since, P&G is a downstream purchaser of palm oil, the company does not face stranded asset risk. P&G sources palm oil and kernel from various suppliers and could shift its purchasing to other suppliers. The company sources circa 0.3 million ton palm oil and kernel, which is valued by CRR at circa USD 200 million. The low level of certification (10 percent) is mainly related to the low availability of certified palm kernel oil. P&G could partially substitute kernel oil, or incentivize certification in kernel. Extra costs could amount to at least USD 5 million, or 0.01 percent of gross profit. The DCF value would total USD 50 million (or 0.02 percent equity value).

An improvement in the monitoring and implementation phase could lead to extra costs. In an earlier report on AAK’s lagging implementation of NDPE best practices, CRR reported that the company could spend USD 5-10 million annually for improvement. For P&G, with its six “independent” SBUs, costs may be higher and could amount to USD 10-15 million annually if each SBU establishes its own organizations, or USD 125 million in a DCF value (0.04 percent versus the equity value at 4 November 2019).

Market access risk: P&G’s European revenue could hurt as retailers move away from unsustainable palm oil

European revenue of approximately USD 10 billion could be at risk, as well as USD 2.4 billion EBITDA, translating into USD 24 billion DCF value. P&G sells its products mainly through supermarket retailers, drug stores, and beauty stores. Retailers that are members of the Consumer Goods Forum (CGF) and/or signatories of the New York Declaration of Forest (NYDF) could move away from P&G to ensure deforestation-free supply chains. As retailers, particularly those based in Western Europe, strengthen their policies and processes to end deforestation in their product portfolio, P&G’s products with palm oil may lose shelf space at retail outlets. At the same time, consumers are becoming increasingly aware of the potential negative effects of non-certified palm oil.

Most of the P&G products contain palm oil. As globally circa 64 percent of P&G’s product sales do contain palm oil (segments Beauty, Health care, Fabric and Home Care), circa USD 10 billion revenues in Western Europe could be at risk. This would translate into USD 2.4 billion EBITDA (applying the five-years average of 24 percent for the global EBITDA margin). The DCF value of this would be USD 24 billion. In a longer-term (5-10 year) perspective, the revenue-at-risk could be larger, as outside Europe consumer and company awareness is on the rise.

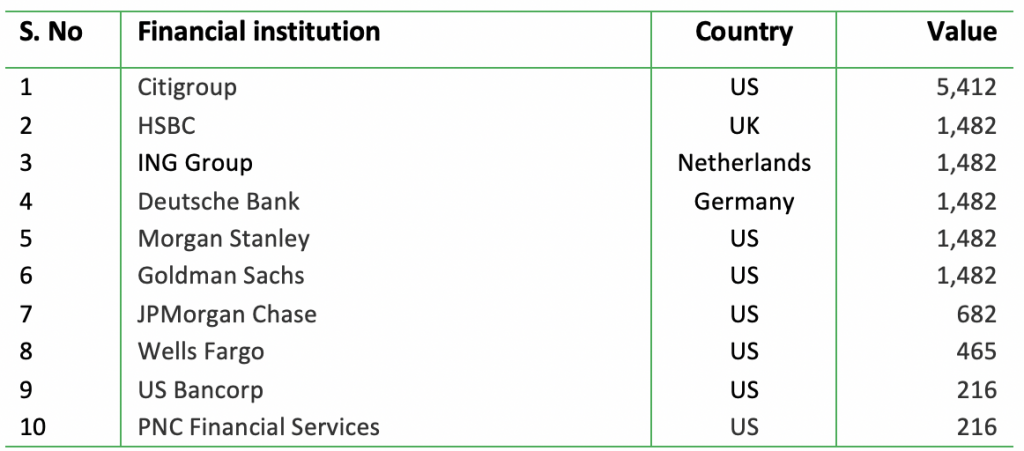

Financing risk is limited, but it might pass a green interest cost opportunity

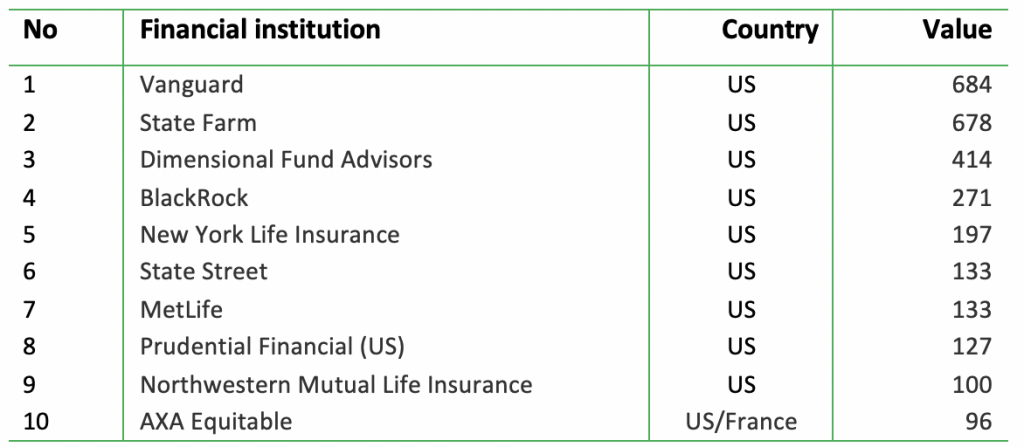

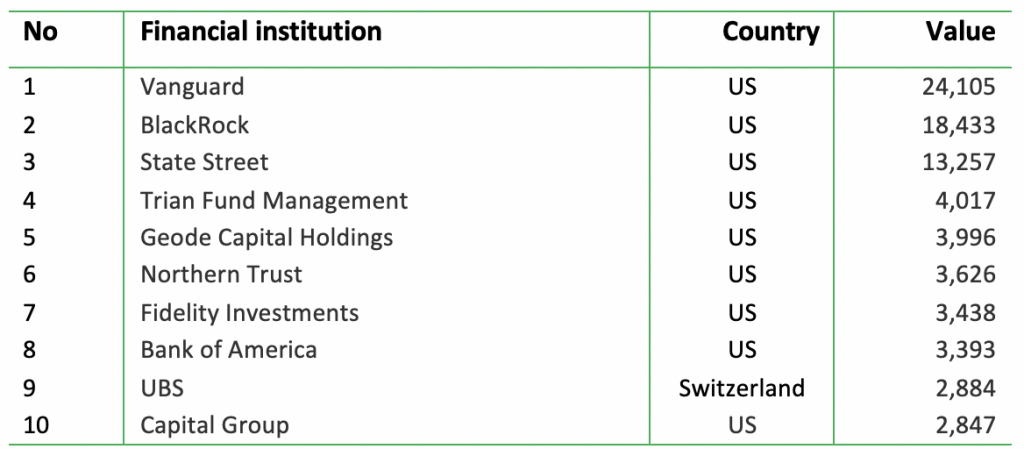

P&G’s top-10 bondholders and shareholders lack adequate deforestation policies and commitments. Most of the P&G’s USD 30 billion debt comes from bonds and only a minor part (ca 12 percent) from loans. As shown in Figure 8, all of the top-10 bondholders of P&G are from the United States, except for Axa. They do not have deforestation-related commitments. As a result, the company may not face financing risk from bondholders. Similarly, the top-10 shareholders are all from the United States, except for UBS, which is based in Switzerland (see Figure 9). U.S. shareholders do not have adequate deforestation-related commitments. UBS has a commitment to zero deforestation, and in 2014, it joined the Soft Commodities Compact. It is also a member of the Roundtable on Sustainable Palm Oil (RSPO).

Figure 7: Bondholders of P&G, based on most recent filing date (in USD million)

Source: Thomson EMAXX (2019), ‘Bondholdings of P&G, latest filing date’, retrieved on 28 October 2019

Figure 8: Shareholding of P&G, at most recent filing date (in USD million)

Source: Thomson Eikon (2019), ‘Shareholders report P&G, latest filing date,’retrieved on 28 October 2019

P&G also has revolving credit facilities worth USD 14.5 billion. A number of banks, such as Citigroup, HSBC, ING and Deutsche Bank, have extended revolving credit facilities to P&G. But the company has not fully used them. Citibank is a signatory to the RSPO and HSBC has a NDPE policy for palm oil. ING’s palm oil policy states that it does not finance palm oil plantations. With Deutsche Bank and JP Morgan Chase signatories to the New York Declaration on forests and Soft Commodities Compact, they are committed to zero net deforestation by 2020.

Figure 9: Revolving credit facility not yet matured as of December 31, 2018 (January 2015 – October 2019, Value in USD million)

Source: Thomson Eikon (2019), ‘Loans to P&G 2015-2019,’ retrieved on November 1, 2019

P&G is typically overlooked by investors, as their deforestation-related commitments often focus on exposure through upstream companies, food companies, and active investing. BlackRock holds both bonds and shares in P&G. The asset manager acknowledged that companies, including consumer goods firms, that fail to address deforestation risks in their supply chains may face financial risks from climate change. In one of its reports “Adapting portfolios to climate change,” BlackRock explained its engagement policy for the palm oil sector. Since its policy focuses on upstream palm oil producers, P&G is not assumed to be a part of this engagement program. A Chain from CRR highlighted another limitation of BlackRock’s palm oil engagements: The policy only focuses on actively managed funds and ignores most of the BlackRock’s investments in the palm oil sector through passive investing. Moreover, since palm oil is mostly linked to food companies, Home and Personal as well as biofuel sectors are over-looked. If financial institutions expand their policies and/or raise awareness about deforestation, P&G could face the risk of higher cost of capital and/or it may not benefit from green financing.

Financing costs for P&G, which has gross debt of USD 30 billion, could decline if the company “greens” its finance. This opportunity could add USD 1.5 billion to P&G’s enterprise value. Currently, a growing trend of green/climate financing rewards companies for reaching certain ESG targets. As a result, loans and bonds with green criteria and/or less ESG violations tend to show lower yields, up to 50 basis-points lower interest rates. For P&G’s USD 30 billion gross debt, this could translate into USD 150 million lower interest costs annually. The DCF value of this is USD 1.5 billion.

Reputation-at-risk could be valued up to USD 41 billion

P&G is a Fast-Moving Consumer Good (FMCG) company in the Home and Personal Care segment that potentially faces significant reputation risk, which is valued at USD 41 billion. A previous CRR report concluded that FMCGs may face reputation risks when sourcing from deforested land. The difference between a company that executes ESG policies in a structurally correct way and another company that lags in implementation could total 70 percent in share price returns.

As P&G lags in its NDPE policy execution, its earnings capacity could be affected by lower brand loyalty by consumers and a qualitative decline in long-term contracts with retailers. These developments may occur not only for the products containing palm oil; they may also have a ripple effect by damaging the overall brand and motivating consumers to reduce purchases of any P&G products across all categories, not only the ones containing palm oil. Moreover, P&G may face problems in retaining and attracting talent for its workforce. Finally, a damaged reputation could also impact P&G’s investor base and/or hinder inroads in the strongly growing ESG investment niche.

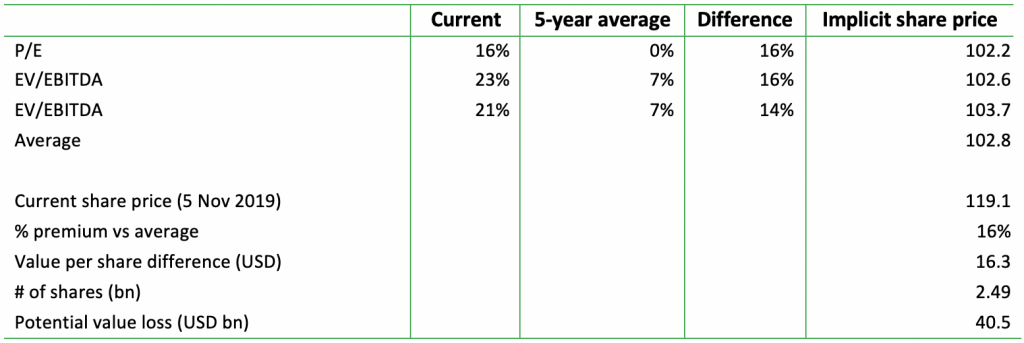

In recent quarters, P&G’s share price benefited from the acceleration in top-line growth and its continued shareholders’ friendly approach through its program of returning money to shareholders. As a consequence, the company’s P/E ratio has moved from a discount to a premium compared to its peers. These premiums are now 16 percent in P/E terms (see Figure 11), 23 percent in EV/EBITDA and 21 percent in EV/EBIT. The five-year averages are much lower. The current negative ESG event on palm oil sourcing could negatively impact P&G’s premium valuation multiples. In the case of a string of negative events, valuation premiums could decline to the averages of the past five years. This setback would result in a USD 16 share price decline, or USD 41 billion in total equity value.

Figure 10: P&G valuation multiple premium, implicit share price and potential value loss

Source: Chain Reaction Research, Bloomberg