The expansion of the palm oil industry in the last ten years was partially in response to the anticipated demand for biofuels worldwide. The expected EU biodiesel boom did not materialize, resulting in a systemic oversupply of palm oil in Southeast Asia. A number of recent policy initiatives may bring about significant shifts in the end-user markets of palm oil-based biodiesel starting January 1, 2020. The geographical markets and the sectors with growing biodiesel demand are not traditionally known for their strict sustainability demands, and therefore may pose new leakage market risks.

Download the PDF here: Palm Oil Biofuels Market May See Shake-Up in 2020, Heightening Leakage Risks

Download the Bahasa translated version here: Pasar Bahan Bakar Nabati Berbaham Dasar Minyak Kelapa Sawit Dapat Mengalami Guncangan pada Tahun 2020 sehingga Meningkatkan Risiko Leakage

Key Findings:

- On January 1, 2020, Indonesia will increase the mandated diesel and crude palm oil (CPO) blend to 30 percent (B30). This change may increase Indonesian consumption of palm oil for biofuels to 7.8 million (metric) tons. The Indonesian government will unlikely set sustainability requirements for biofuel production.

- France will discontinue biofuel tax breaks for palm oil starting January 1, 2020. France’s move comes in the context of wider EU action on palm oil-based biofuels. Not including palm oil in the EU renewable energy target is expected to help phase-out of the fuel’s use in Europe. In 2018, nearly two-thirds of the 7.7 million tons of palm oil imports into the EU were used for biodiesel.

- In the medium to long term, the decarbonization of the shipping industry may rely on biofuels. The International Maritime Organization (IMO) has set new regulations on sulphur content of fuel oil for ships, starting January 1, 2020. The new regulations are expected to stimulate unprecedented demand for alternative low-sulphur fuels. Under current market prices, the sulphur cap is unlikely to increase maritime demand for palm-based biofuels in the short term.

- The aviation industry has committed to carbon neutral growth from 2020 onwards. Civil society organizations have raised concerns that the shift to palm oil- and soy-based biofuels could result in 3.2 million hectares of additional deforestation.

- China is increasing its use of palm oil-based biofuels as a cheap alternative to crude oil. In August 2019, Beijing announced it would remove import quotas on crude palm oil. China’s imports may jump to 7 million tons in market year 2019/20.

Five trends will alter palm-based biodiesel market in 2020

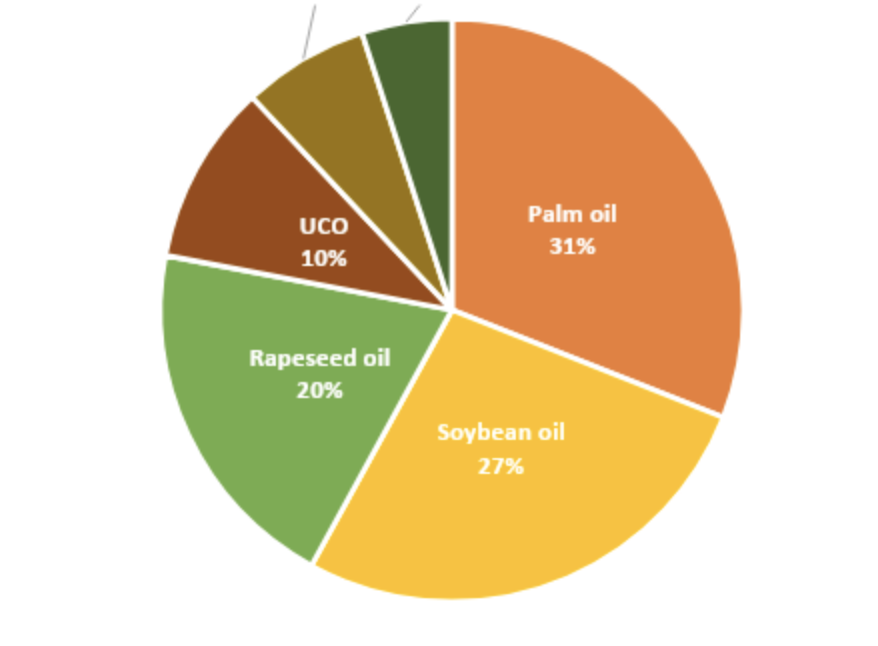

The expansion of the palm oil industry in the last ten years was partially in response to the anticipated growing demand for biofuels worldwide. In 2010, the EU drafted its Renewable Energy Directive, setting targets for member states and providing incentives to switch to palm oil-based biodiesel. This Directive contributed to the increase in EU palm oil imports by 40 percent between 2010 and 2017. Globally, biodiesel consumption grew from 1.1 million kiloliters (0.3 billion gallons) in 2001 to 35.2 million kiloliters (9.3 billion gallons) in 2016. Fifty-eight percent of all biofuels were consumed in the United States (22 percent), Brazil (10 percent), France (10 percent), Indonesia (9 percent), and Germany (7 percent). In 2017, palm oil accounted for 31 percent of global feedstock use for biodiesel.

Figure 1: Feedstock Use in Biodiesel Production (2017)

Source: UFOP

However, the appetite for palm oil-based biofuels has weakened significantly in recent years in Europe. Palm oil is no longer considered a sustainable biofuel due to its contribution to deforestation and indirect land use change, and the EU has announced plans to phase out palm oil-based biodiesel by 2030. Oil palms planted five to ten years ago in anticipation of the biofuel boom in Europe have now reached maturity. As the biofuel boom has failed to materialize, the palm oil industry is facing structural oversupply.

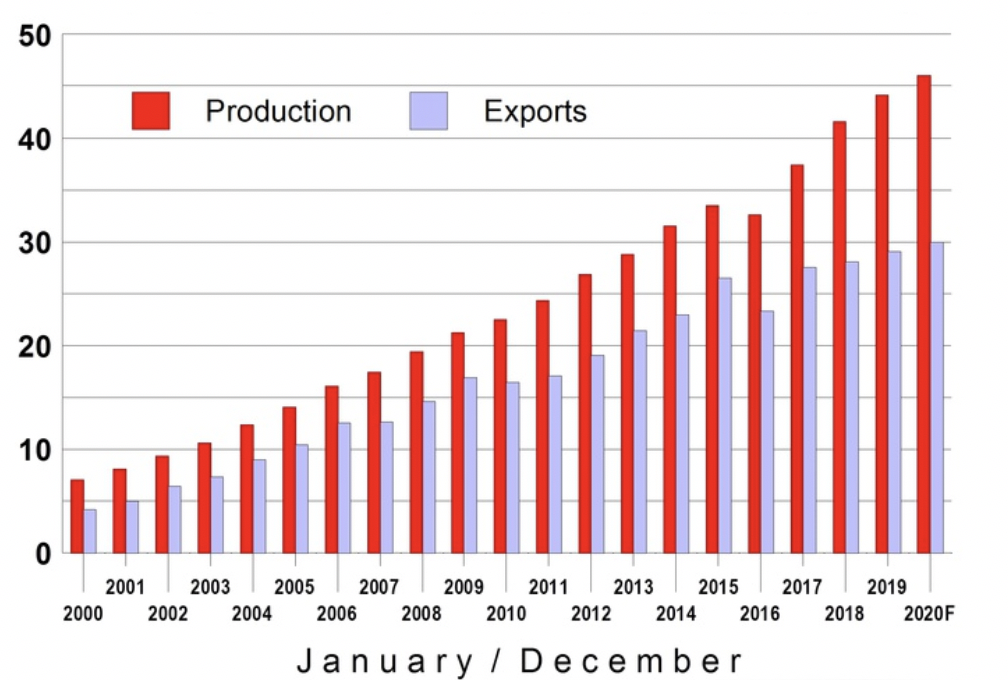

Figure 2: Indonesian palm oil production and exports (million tons)

Source: Oil World

Recent policy initiatives have changed the global biofuels outlook for 2020 and beyond. Several policies announced in the last ten years will come into effect in the coming months, leading to shifts in end-user markets for palm oil-based biofuels. Unless end-user markets implement effective safeguards to ensure sustainable production, these shifts may create new and additional leakage markets for unsustainable palm oil.

Trend 1: Indonesia and Malaysia increase biofuel blend mandates

On January 1, 2020, Indonesia will increase the mandated portion of diesel blended with crude palm oil (CPO) to 30 percent (B30). This expansion represents the next step in a gradual increase of biodiesel blending from the current B20 mandate. This political move is intended to support the domestic palm oil industry by creating more domestic demand for CPO and also reducing Indonesia’s imports of oil by an expected 8.7 million kiloliters (55 million barrels) annually.

The Ministry of Energy and Mineral Resources plans to use the B30 blend in automobiles, ships, and trains. The Ministry began tests on automotive engines in June 2019, to ensure that B30 use would not result in any safety issues. Shipowners have opposed the higher blend, citing increased operating costs and poor performance in ship engines. The River, Lake and Water Transportation Operators Association (Gapasdap) said the government should not mandate B30 by 2020 since it has only tested automotive engines.

The higher biodiesel blend may push consumption of palm oil-based biofuels in Indonesia from 6.2 million kiloliters per year in 2019 to as much as 9.6 million kiloliters in 2020The gradual increase of mandatory biofuel blends has already created a growing domestic market for palm oil producers and biodiesel refiners at a time when global demand for the oil has been in decline. Over the past five years, domestic biodiesel demand has grown by 35 percent. Many major palm oil traders and refiners recognize the Indonesian biofuel market as one of the most significant growth opportunities for the sector (e.g. Golden Agri-Resources, Wilmar, IOI).

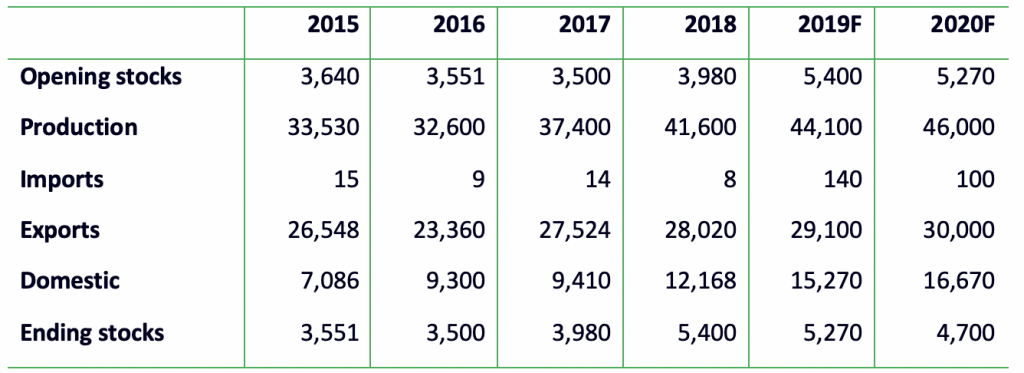

Figure 3: Palm oil production, exports and stocks in Indonesia (1,000T)

Source: Oil World

The Indonesian government is unlikely to set sustainability requirements for biodiesel production in the coming years. As such, increased end-user demand from domestic biodiesel mandates will likely create both an upward pressure on land use for oil palm, as well as a potential leakage market for growers and producers that are not compliant with No Deforestation, No Peat, No Exploitation (NDPE) policies.

Malaysia also intends to raise its blending mandate for the transportation sector from B10 to B20 in 2020. In addition, it plans to expand the mandate for the industrial sector from B7 to B10. The move is expected to increase Malaysian palm oil demand to 1.3 million tons of CPO annually, up from 761,000 tons. Like Indonesia, the Malaysian government is seeking to reverse the reduction of palm oil demand and the increase in Malaysian palm oil stocks. The move is seen as a boost to the domestic palm oil industry. Malaysia will implement the B20 measure in stages, starting with Langkawi (Kedah archipelago) early in 2020.

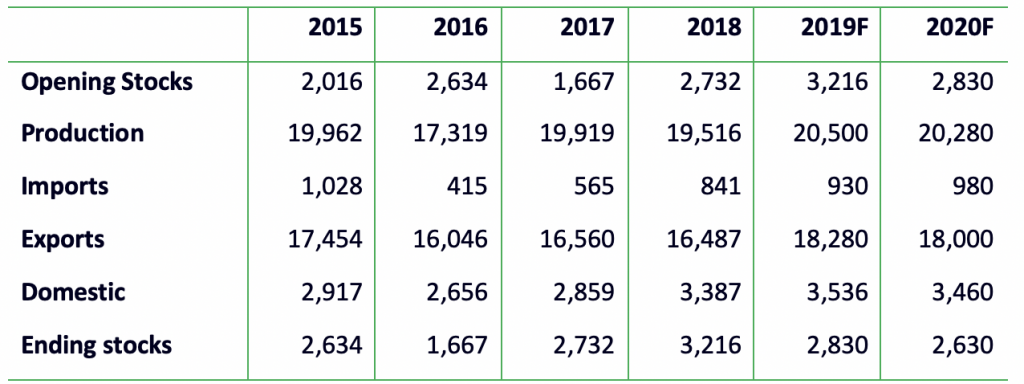

Figure 4: Palm oil production, exports and stocks in Malaysia (1,000T)

Source: Oil World

Trend 2: France ends tax exemptions while EU Renewable Energy Directive phases out palm oil

In January 2019, the French National Assembly passed a bill that disallows palm oil for any biofuel tax as of January 1, 2020. France is the largest biodiesel consumer in Europe, and the third largest in the world. As part of the French finance bill for 2019, French MPs voted to end all reductions on general tax for polluting activities (TGAP) for palm oil-based biofuels. The MPs cite deforestation and indirect land use change (ILUC) as their main concerns. The elimination of this tax break significantly affects French oil company Total’s biorefinery at La Mede, which was recently converted to process up to 300,000 ton of palm oil per year. France’s constitutional court rejected Total’s appeal against the measure in October 2019.

In November 2019, France’s National Assembly adopted an amendment that would delay the end of the palm oil tax breaks until 2026. However, that decision was overturned one day later by France’s parliament, which upheld the tax break termination date of January 1, 2020.

France’s move comes in the context of wider EU action on palm oil-based biofuels. In December 2018, the European Commission announced its plans to phase out palm oil-based biofuels by 2030. The plans are part of the revised Renewable Energy Directive (RED II) that sets new targets for renewable energy use within the EU. This directive contains sustainability criteria for bioenergy, including the negative impact that biofuel production may have due to indirect land use change. The EC argues that biofuel production usually takes place on cropland previously used for the cultivation of food crops. In turn, this activity may extend agricultural land use into high carbon stock areas such as forests, wetlands, and peatlands.

The RED II sets limits on the volumes of biofuels with high risks of indirect land use change that count towards national targets of EU Member States. These targets are initially frozen at 2019 levels for the period 2021-2023. They will gradually reduce to zero by 2030. The EC has qualified palm oil as a high-ILUC risk commodity for which these limits apply, as 45 percent of palm oil expansion has taken place on land that was forested in 1989. As a result, palm oil can no longer be counted towards the new renewable energy targets from 2030 onwards. Palm oil is also no longer eligible for related subsidies. The Directive offers a loophole for smallholder-produced palm oil, which will remain eligible for renewable energy targets.

Figure 5: EU28 Imports of Palm Oil from 3rd Countries (1,000T)

Source: Oil World

In 2018, nearly two-thirds of all palm oil imports into the EU were used for biodiesel. The ban on counting towards the renewable energy target is expected to result in a complete phase-out of the fuel’s use in Europe. In direct response to the announcement of RED II, the governments of Malaysia and Indonesia voiced their opposition to the move, calling it a discriminatory act against palm oil producers, for the benefit of domestic EU vegetable oil producers. Both countries have threatened to take their grievances to the World Trade Organisation. Scientists also raised concerns that the move may contribute to leakage in the global palm oil market. Indonesian exporters may offset the loss of EU sales by supplying other end-user markets, such as China and India, that do not place meaningful sustainability requirements on palm oil production.

Figure 6: EU Palm Oil Consumption by End Use

Source: Transport & Environment

Trend 3: International Maritime Organization implements global sulphur cap for marine fuels

The volume of conventional oil affected by this new regulation is significant. In 2018, the shipping industry used about 556,000 kiloliters (3.5 million barrels) of high-sulphur fuel per day, accounting for . Marine fuel or bunkering fuel is traditionally produced from residues from oil refineries. But most refineries are not yet equipped to produce the volumes in demand for the lower sulphur standard. Oil refiners will see disruptive changes, including wider price differentials between high-sulphur and low-sulphur fuels. Refineries that are able to produce compliant fuels are expected to see higher margins, whereas simple refineries that mostly produce high-sulphur fuel oil will face difficult adjustments. Large oil majors, including Shell and BP, are already offering compliant marine fuels.

The new regulations are expected to have disruptive effects on the marine fuel industry and create an unprecedented demand for alternative low-sulphur fuels. They will impact approximately 75 percent of the global marine fuel market that now has to meet the lower standard. In the short term, shipping companies are expected to seek out the alternative low-sulphur fuel options, amounting to an estimated additional fuel cost of USD 60 billion. Alternative fuel options include Very Low Sulphur Fuel Oil (VLSFO), marine diesel, methanol, LNG, biofuels, solar power, and fuel cells.

The IMO sulphur cap is unlikely to increase maritime demand for palm based-biofuels in the short term. Biofuels are for the maritime industry, despite technological possibilities to do so. Experts told Chain Reaction Research that the industry will likely seek out the fuel option legally allowed, and that biofuels would not be among the most sought-after options in the short term.

In the medium to long term, the decarbonization of the shipping industry may nonetheless rely in part on biofuels. As biofuels do not contain sulphur, stricter environmental regulations for maritime fuels may tip the economic scale in the longer term. Several companies are currently conducting tests with biofuel bunkers, including dredging company Van Oord, shipping company Maersk, furniture retailer IKEA, and the Japan Engine Corporation.

A 2040 scenario analysis conducted for the Sustainable Shipping Initiative in May 2018 concluded that biofuels may be the most economically feasible zero-emission alternative for the shipping industry. Biodiesel, for instance, can be used through internal combustion engines and does not require large technological adaptations. The study recognizes that certified biofuels are required to ensure full decarbonization, which may affect supply and price levels. As constraints may affect the available volume of certified biodiesel, uncertified palm oil-based biodiesel demand may increase in such a scenario.

Korindo Group, the private Indonesian palm oil, rubber and timber company, is already looking at business opportunities in the regional bunkering market. Korindo was suspended by multiple NDPE traders between 2016 and 2018 after evidence of deforestation and illegal burning on its concessions. In March 2019, Korindo was reportedly working with the South Korean companies GF Oil and Sejong Technology to establish a biofuel plant on the Indonesian island of Bintan. The plant would use Korindo’s palm oil, aiming to produce approximately 3 million kiloliters of biofuel — although the timeframe for this production has not been publicly specified. The announcement followed reports that GF Oil, established in 2012 to market biofuel to industries as a way of reducing GHG emissions, was promoting palm oil-based biofuel as compliant with the International Maritime Organization’s (IMO’s) global sulphur cap.

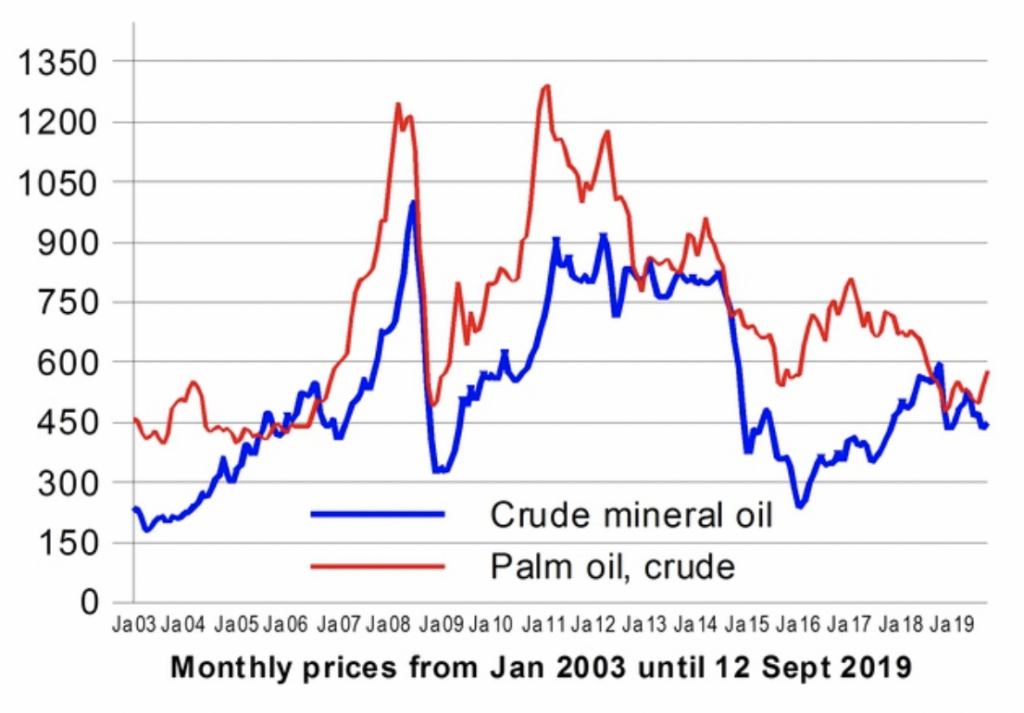

Trend 4: Aviation committed to carbon neutral growth from 2020 onwards

The IMO-triggered change in demand for low sulphur fuels is also expected to have spill-over effects in other sectors, including aviation. The demand for low-sulphur fuel from the shipping industry may impact prices and availability of low-sulphur jet fuel and diesel. Prices for jet fuel are expected to rise due to the new IMO rules, posing a threat to airline profitability. Jet fuel price hikes may give a boost to palm oil jet fuels and other alternative aviation fuels.

Figure 7: Monthly Prices of Palm Oil & Crude Mineral Oil (USD/T)

Source: Oil World

These projected price developments come in parallel to the aviation industry’s own commitment to carbon neutral growth from 2020 onwards. Airline companies aim to use more fuel-efficient aircrafts, fly more direct paths, and offset emissions by purchasing carbon credits. The use of alternative aviation fuels is seen by the industry as a critical tool towards meeting this commitment.

Civil society organizations have raised concerns that the shift to palm oil- and soy-based biofuels could result in 3.2 million hectares of additional deforestation. With current technologies, palm oil- or soy-based HEFA (Hydroprocessed esters and fatty acids) are the only economically viable options. To meet the industry aim of 100 percent alternative fuel use, demand for palm oil and soy may reach 140 million tons per year, double current palm oil production rates.

Meanwhile, Norway’s announced quota requirement of 0.5 percent advanced biofuels in aviation will come into effect on January 1, 2020. This requirement stipulates the use of Sustainable Aviation Fuel (SAF), while market actors can decide themselves where and when to mix the biofuel. Biofuels from “problematic feedstocks such as palm oil” are ineligible to count against this quota. The government’s goal aims for 30 percent of aviation fuel to be “sustainable” by 2030.

Trend 5: China turns to palm oil biofuels amid U.S. trade war

In August 2019, China announced it would remove import quotas on crude palm oil. The move came at the height of the U.S.-China trade war, when the United States announced plans to impose additional 10 percent tariffs on Chinese imports. In a series of retaliatory moves, China reduced its consumption of U.S. soybeans and soy oils. China has moved to Brazilian soy oil, palm oil, and rapeseed oil as alternatives.

The implications of this shift in agricultural trade was already seen in 2019, with China’s palm oil imports in August reaching their highest level in six years at 590,000 tons. At current pace, China’s 2019 imports of palm oil are set to be the highest annual rate ever. Further increase in Chinese consumption is projected for 2020 and beyond. As the trade war between Beijing and Washington has affected China’s soy volumes from the United States, China has looked for alternatives elsewhere, particularly soy from Brazil.

China, Indonesia’s second largest buyer of palm oil, is expected to import 6.7 million tons of palm oil in 2019, a 6.3 percent increase versus last year and triple levels seen in the early 2000s. China National Grain and Oils Information Center says that imports will jump to 7 million tons for the market year starting in October. Over the summer, China’s imports from Indonesia rose by 30 percent year-on-year. Imports from Malaysia have also increased significantly. China has so far imported mostly refined products, which have been covered by refiner NDPE policies despite the lack of sustainability demands from Chinese end-users. If China now starts importing significant crude palm oil volumes, that could be a major factor in the leakage market.

China is also increasing its use of palm oil for biofuels. China’s palm oil-based biofuel imports grew almost 50-fold to 811,000 kiloliters (751,056 tons) last year. This increase is driven by China’s intention to reduce its fossil fuel use and increase its use of alternative energy. The increased imports mostly originate from Malaysia, as Indonesia’s biodiesel capacity is primarily used to meet domestic demand.

Shift in end-user biodiesel markets may accelerate leakage of unsustainable palm oil

Significant shifts in the end-user markets of palm oil-based biodiesel are expected in 2020. Expanded policy mandates and shifts in global commodity trade may spur growing biodiesel demand from Asian countries, particularly Indonesia, Malaysia and China, while Europe will move to phase out palm oil as a biofuel. Simultaneously, demand from the maritime and aviation sectors may increase as a result of new international standards and sustainability commitments.

Neither the geographies nor the sectors with growing biodiesel demand are traditionally known for their strict sustainability demands. This dynamic may lead to the creation of new “leakage” markets that fail to set meaningful conditions on the sustainable production of palm oil. As a result, actors facing restricted NDPE market access may increasingly turn to these end-user markets, unless these markets set similar sustainability criteria as seen in the food supply chains.

In addition, an absence of sustainability demands from these end-user markets may weaken the current transformation of the palm oil industry. Even actors that currently have NDPE policies may be less inclined to forcefully implement these policies without a clear signal from their clients. This situation could result in more “paper policies” that are not implemented, greenwashing efforts, and unsustainable supply “seeping through the cracks.”