The Brazilian company JBS SA is the largest meat processor in the world based on sales. The company operates five main business units: JBS Brazil, Seara, JBS USA Beef, JBS USA Pork, and Pilgrim’s Pride. This paper assesses the deforestation exposure and the physical and transition risks from JBS’ operations in Brazil. CRR has located and monitored 983 direct suppliers and 1,874 indirect suppliers to JBS in six Amazon states. In addition, CRR calculates the revenue and EBITDA impact of deforestation, Chinese demand, and COVID-19 in three forward-looking scenarios.

Download the PDF here: JBS: Outsized Deforestation in Supply Chain, COVID-19 Pose Fundamental Business Risks

Report Webinar Recording:

Key Findings:

- JBS has a growing presence in the Chinese market. China accounted for 26.1 percent of JBS’ global exports in 1Q20 and 33.4 percent in 2Q20. The company has benefited from the growing Chinese reliance on meat imports after the African Swine Fever reduced the country’s pig herd.

- Since 2016, JBS has expressed intentions to list its international assets in the United States. The U.S. listing would consist of a spin-off of JBS’ international operations into a separate company with the same shareholders. Simultaneous to the U.S. listing plans, JBS’ second-largest shareholder BNDESPar announced its intention to sell half its shares.

- JBS’ beef operations in Brazil have an outsized deforestation risk exposure. JBS operates 20 slaughterhouses within the Legal Amazon. The company’s monitoring of supplier compliance is limited to its direct supply. Its indirect supply chain risks remain unmitigated.

- Since 2008, 20,296 ha have been deforested in the sample of JBS’ direct supply chain, and 56,421 ha in its indirect supply chain. CRR conservatively estimates that JBS’ total deforestation footprint may be as high as 200,000 ha in its direct supply chain and 1.5 million ha in its indirect supply chain.

- Both deforestation and COVID-19 may impact the company’s revenues, cost structure, and asset value. Business risks include COVID-19 plant closures; shareholder action; restrictions on export markets and supply chain exclusions; growing Chinese consumer weariness for imported meat; and availability of plant-based substitutions.

- In a “high-impact” scenario, JBS’ EBITDA could be negatively impacted by 26 percent or USD 1.3 billion, leading to increasing financing costs. JBS’ cost of capital might rise as almost a third of its financing is through European investors and banks that are adopting stricter ESG policies.

JBS increasingly reliant on U.S. revenues and Chinese export markets

Largest meat processor in the world headquartered in Brazil but with global operations

JBS SA is a Brazilian company primarily engaged in meat processing. JBS’ activities focus on the production of a range of beef, pork, and poultry products. Its products are distributed under various brand names, such as Friboi, Swift, Bertin, Pilgrim’s, and others. The company also operates related businesses, such as leather, biodiesel, personal care and cleaning, solid waste management, and metal packaging. JBS operates in 15 different countries.

JBS is the largest meat processor in the world by sales. It has 400 production units, facilities and offices, of which 230 are used for the production of beef, pork, lamb, and poultry products. The company has been listed on the São Paulo stock exchange since 2007 and has received significant financial support from Brazil’s development bank BNDES. With this public funding, JBS has made a range of domestic and international acquisitions. The founding Batista family maintains a 39.8 percent stake.

The company operates five main business units:

- JBS Brazil comprises the company’s Brazilian beef and leather production. It manages 37 meatpacking plants throughout Brazil and 24 leather production facilities around the world. It furthermore holds 18 distribution centers and five beef cattle feedlots. JBS Brazil generated BRL 16.9 billion revenues (USD 3.1 billion) in 1H20, (14.0 percent of consolidated revenues adjusted for intercompany eliminations), up 21.1 percent from 1H19. The share of export market revenues increased from 40 percent in 1Q20 to 51 percent in 2Q20.

- Seara is the company’s chicken and pork producing and exporting unit. The unit produces meat for the domestic Brazilian market and exports to over 100 different countries. It has 30 poultry processing units, eight hog processing units, 20 prepared food facilities, and 18 distribution centers located throughout Brazil. Seara accounted for 1 percent of JBS’ revenues in 1H20, of which 54.7 percent came from export markets in 2Q20.

- JBS USA Beef, JBS USA Pork, and Pilgrim’s Pride control the company’s operations in North America, Europe, and Australia. Among other facilities these three business units operate 18 beef slaughterhouses, five hog slaughterhouses and 36 poultry plants. JBS USA accounted for 1 percent of revenues in 1H20.

JBS has a growing presence in the Chinese market, which is the largest export destination for the company. China accounted for 26.1 percent of JBS’ global exports in 1Q20 and 33.4 percent in 2Q20. The company has benefited in recent years from the growing Chinese reliance on meat imports after the African Swine Fever reduced the country’s pig herd. In January 2020, JBS signed a memorandum of understanding with WH Group, a large Hong Kong-based meatpacker, to supply up to BRL 3 billion (reported as USD 717 million at the time) of beef, poultry, and pork products to the Chinese market annually. This partnership followed a November 2018 deal with Alibaba worth USD 1.5 billion.

U.S. listing, BNDES divestment not before 2021

IPO was delayed in 2017 due to investigations targeting owners

Since 2016, JBS has repeatedly expressed its intentions to restructure its business with a listing of its international assets in the United States. The core factor behind these restructuring plans is a mismatch between the company’s capital structure and its operational structure. A U.S. listing would unlock shareholder value from a business model that relies primarily on USD transactions but that reports its finances in Brazilian Real. Signals that the company was moving ahead with this listing resurfaced in November 2019.

The U.S. listing would result in a spin-off of JBS’ international operations into a separate company with the same shareholders. Operations in Brazil would continue under JBS SA, the entity currently listed on the São Paulo stock exchange. Whereas the company was ready to move ahead in March 2020, the impacts of the COVID-19 outbreak shifted the company’s focus away from the listing. In August 2020, CEO Gilberto Tomazoni indicated that the company has revived plans for the listing, but it “cannot happen this year.”

Simultaneous to the U.S. listing plans, JBS’ second largest shareholder BNDESPar announced in November 2019 its intention to sell half its JBS shares. BNDESPar, the equity investment arm of Brazil’s development bank BNDES, holds a 21.3 percent stake in JBS. JBS accounts for 20 percent of BDNESPar’s portfolio. BNDES had hired various investment banks and planned a roadshow to sell its stake following the release of JBS’ 4Q19 results. The sale would be made in a single tranche and was planned for June 2020, but the COVID-19 pandemic interrupted this process. In July 2020, reports said that BNDESPar would commence with other divestments first, and that more complex sales, such as its JBS stake, would take place at a later, undisclosed date.

As a result of the repeated delays of its corporate restructuring, JBS remains in a continuous state of uncertainty. Plans for the U.S. listing have repeatedly been sidetracked due to criminal investigations in 2017 and pandemic outbreaks at its facilities in 2020.

JBS has an outsized deforestation exposure in its Brazilian beef supply chain

JBS’ cattle operations in Brazil have long been associated with Amazon deforestation. Following intensive civil society campaigns, JBS was among the major beef producers in Brazil to sign multilateral Cattle Agreements with civil society organizations in 2009 to increase sustainability in the sector. The company also signed legally binding Terms of Adjustment of Conduct (TACs) with Brazil’s Federal Prosecutors Office. JBS has a zero-deforestation target and publicly commits to refrain from sourcing raw materials from farms that are:

- involved with deforestation in the Amazon biome after 2009;

- facing environmental embargoes;

- linked to any kind of forced labor;

- located on indigenous land or in environmental conservation areas.

JBS is also involved in various multi-stakeholder initiatives, including the Brazilian Coalition on Climate, Forest and Agriculture, the Tropical Forest Alliance (TFA), and the Supply Chain Protocol.

JBS tracks supplier compliance through a social and environmental monitoring system that uses satellite imagery and data georeferencing to analyze 50,000 cattle suppliers in the Amazon daily. Through this system, the company monitors an area of 45 million hectares (ha). The company will block suppliers found to be in non-compliance with JBS’ policies from future purchases. JBS indicated to CRR that over 9,000 farms have been blocked to date. Independent auditors found a 99.9 percent compliance rate with these policies.

JBS’ monitoring system is limited to its direct cattle suppliers, and the company does not yet have systems in place to systematically monitor its indirect suppliers. The company has stated publicly that “the traceability of the entire beef supply chain is an industry-wide challenge and a complex task.” The company indicated to CRR that it is in active discussions with Brazil’s Ministry of Agriculture to explore the possibility of creating so-called “Green GTAs” – animal transportation records that would include information about environmental and slave labor embargoes. Such discussions have been ongoing since at least 2013, and independent audit reports from 2019 described these efforts as “not yet successful.” In addition, JBS is piloting blockchain technologies and theoretical productivity indices as measures to address indirect supply chain exposure. The theoretical productivity index is intended to address the risk of “cattle laundering” by assessing the size of a property and the number of cattle it supplies.

Despite its measures, JBS continues to be linked to illegal deforestation in its supply chain, and an unspecified proportion of JBS’ supply chain deforestation footprint may be in violation of Brazil’s Forest Code. Various media outlets have reportedly found that JBS purchased cattle from illegally cleared farms in Rondônia and Pará. According to a March 2020 report from the Guardian, JBS indirectly sourced from a Rondônia farm whose owner was implicated in the murder of nine people in Mato Grosso. JBS denies that a link exists between the company and the farm owner. As reported in July 2020, in Mato Grosso, JBS transported cows from embargoed farms to “clean” farms that met JBS’ sourcing protocols. In 2017, JBS was fined BRL 24 million (USD 4.3 million) for buying cattle from illegally deforested areas in Pará. JBS indicated to CRR that it appealed this fine.

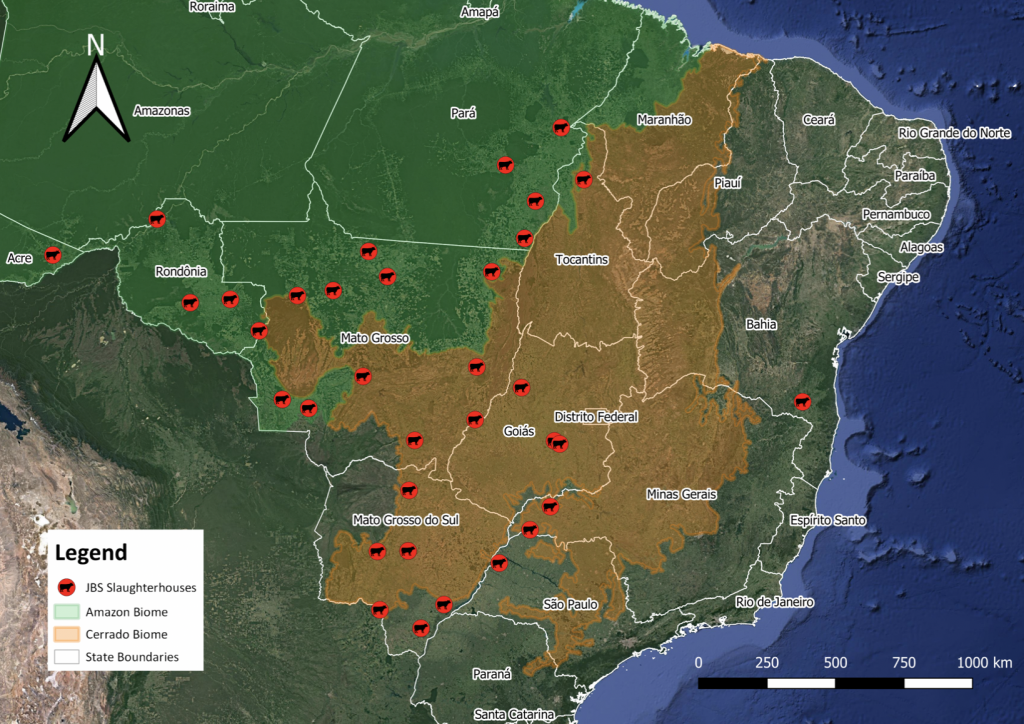

JBS operates a total of 37 cattle slaughterhouses in Brazil, of which 20 are located within the Legal Amazon. An earlier study that assessed meatpackers’ deforestation risks based on projected buying zones concluded that JBS had the highest exposure of all meatpackers active in the Amazon. Based on their locations, eight JBS slaughterhouses had projected deforestation risks of 600,000 ha each.

Figure 1: Location of JBS Cattle Slaughterhouses in Brazil

Source: Chain Reaction Research, based on Ministry of Agriculture and JBS.

75,000 ha of deforestation detected in sample of JBS’ direct and indirect supply chain

Based on animal transportation and rural cadaster data, CRR has located 983 direct suppliers and 1,874 indirect suppliers (see Figure 2) to JBS in the states of Goiás, Minas Gerais, Mato Grosso do Sul, Mato Grosso, Pará and Tocantins (see Annex for CRR’s methodology). These farms have either sent one or more batches of cattle directly to a JBS slaughterhouse or to another farm that then sold cattle to JBS at a later moment in time. Based on JBS’ reported 90,000 suppliers, CRR’s dataset constitutes approximately 1.1 percent of JBS’ direct supply chain in all of Brazil. The sample represents an estimated 10 percent of the direct supply chain in the six above-mentioned states.

Figure 2: Sample of 983 direct JBS suppliers and 1,874 indirect JBS suppliers

Source: Chain Reaction Research, based on Ministry of Agriculture, JBS and animal transportation permits (GTA).

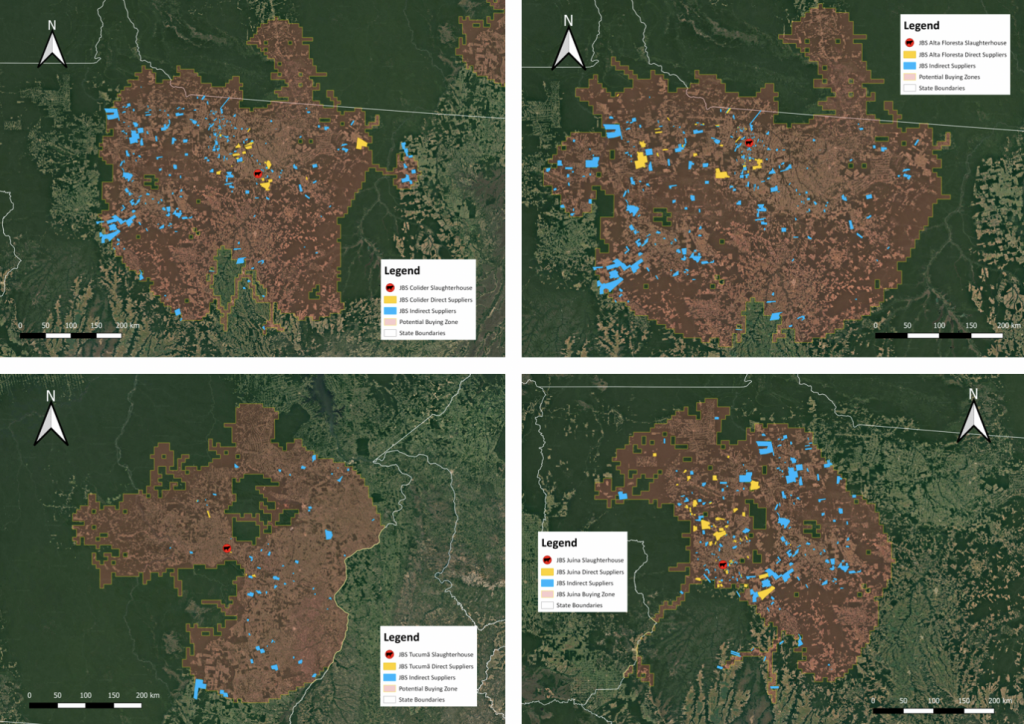

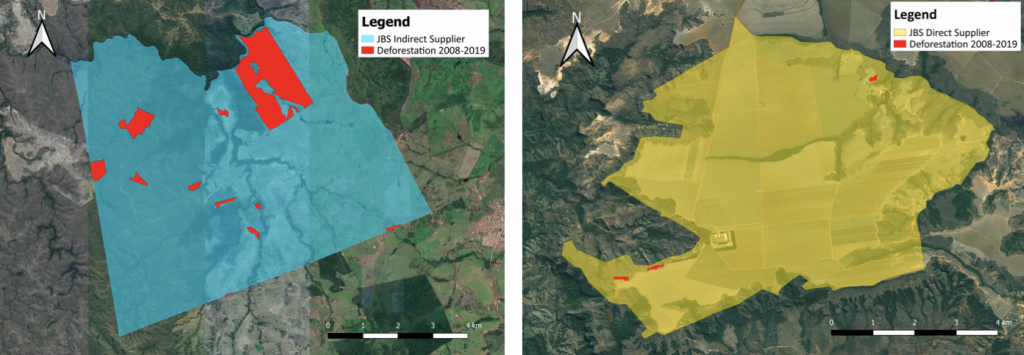

The dataset provides a granular sample of the origin of cattle slaughtered at JBS facilities, and allows for a targeted assessments of deforestation risks in both the direct and indirect supply chains. Figure 4 illustrates the confirmed locations of the direct and indirect suppliers to JBS’ facilities in the municipalities of Colider (MT), Alta Floresta (MT), Tucumã (PA), and Juína (MT). These properties fall within the potential buying zone of the same slaughterhouse identified in earlier studies.

Figure 3: Location of sample of direct and indirect suppliers of JBS’ meat plants in Colider (MT), Alta Floresta (MT), Tucumã (PA) and Juína (MT)

Source: Chain Reaction Research, based on Ministry of Agriculture, JBS, Imazon and animal transportation permits (GTA).

Figure 4: Deforestation at sample of direct and indirect suppliers of JBS’ meat plants in Colider (MT), Alta Floresta (MT), Tucumã (PA) and Juína (MT)

Source: Chain Reaction Research

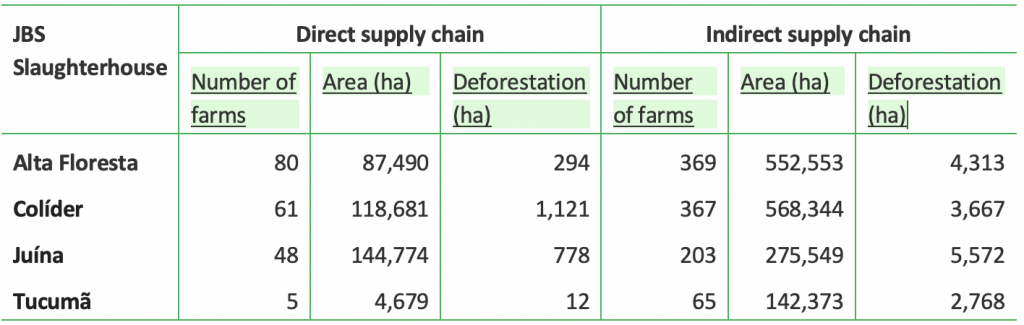

Since 2008, confirmed deforestation of 20,296 ha has been detected on the 983 identified properties in JBS’ direct supply chain. This land use change represents 0.85 percent of the cumulative land area of the identified farms, with an average deforestation of 20.65 ha per farm. Approximately 70 percent (14,655 ha) of detected land clearing occurred in the Cerrado Biome, in some cases without the required environmental licenses. JBS’ monitoring systems for its direct supply chain are less developed in the Cerrado biome than in the Amazon, as satellite data for Cerrado deforestation is not integrated into JBS’ internal systems.

Both absolute and relative deforestation figures confirm that JBS’ exposure is higher in its indirect supply chain than in its direct supply chain. CRR identified 50,852 ha of deforestation on the 1,874 identified farms within JBS’ indirect supply chain after the 2008 cut-off date of Brazil’s Forest Code. This represents 1.44 percent of the cumulative land area of these properties, with an average of 27.13 ha per farm. Despite company efforts to address the issue, deforestation in the indirect supply chain still falls outside of the scope of its zero-deforestation policy. Thus, the associated deforestation risk exposure remains fully unmitigated. The lack of mitigation allows for so-called “cattle laundering,” whereby cattle are moved from non-compliant farms to compliant farms in order for farmers to maintain market access to slaughterhouses.

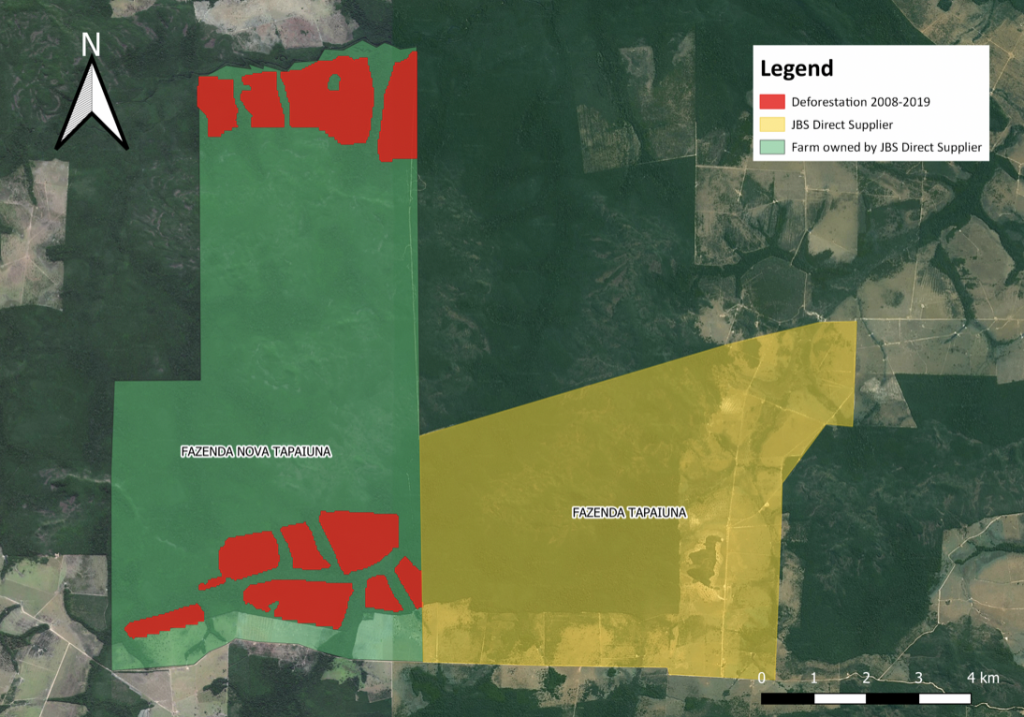

Figure 5: Example of a farm in Novo São Joaquim, Mato Grosso with 371 ha deforestation (on the left) that supplied cattle to a direct supplier of JBS in Tesouro, Mato Grosso with minimal deforestation (on the right)

Additional deforestation exposure may be present in farms adjacent to the identified direct suppliers. Fraudulent land titling and self-declarations to the Environmental Rural Cadaster (CAR) may result in farms fragmenting into separate administrative entities owned by the same companies or individuals. In several known examples, deforestation took place on one part of the farm while cattle were supplied from another part that was registered separately. In reality, these parts belong to a single farm with a single owner. This exposure is not captured in the figures presented in this report, but it may constitute an additional unmitigated deforestation risk. JBS indicated to CRR that the responsibility to assess the CAR data lies with the competent official agencies.

Figure 6: Example of deforestation at a farm in Nova Canaã do Norte, Mato Grosso adjacent to a direct JBS supplier. Both properties are registered under the same owner

Estimated deforestation footprint of 1.7 million ha to date, with 64 million ha of forest at risk

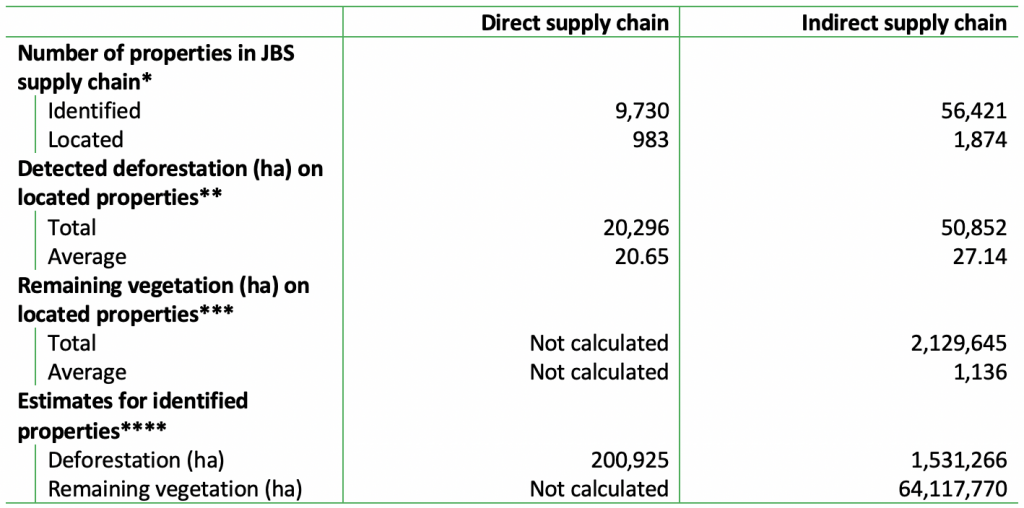

CRR conservatively estimates that JBS’ total deforestation footprint since 2008 may be as high as 200,000 ha in its direct supply chain, and 1.5 million ha in its indirect supply chain. These figures are extrapolations of the average deforestation per farm to the total number of farms for which supply chain records exists (see Figure 7), and they only include the states of Goiás, Minas Gerais, Mato Grosso do Sul, Mato Grosso, Pará, and Tocantins. Among others, the data excludes figures from the Amazon states of Rondônia (four JBS slaughterhouses) and Acre (one JBS slaughterhouse).

2.1 million ha of native vegetation remains on the 1,874 identified properties within JBS’ indirect supply chain. Extrapolating this figure, CRR projects a staggering 64 million ha of remaining forests within JBS’ indirect supply chain. That is roughly the equivalent of the island of Sri Lanka or the U.S. state of West Virginia. The above-mentioned absence of mitigation measures may jeopardize these forests in the coming years.

Figure 7: Estimates of JBS’ deforestation risk exposure in direct and indirect supply chains in GO, MG, MS, MT, PA, and TO

*Properties were identified in 2019 GTA records. Properties were located through matching with rural cadaster data (SIGEF and SNCI) **Deforestation calculated on the basis of annual confirmed PRODES data since 2008 ***Remaining vegetation calculated on the basis of data from INPE and FREL.**** Calculated on the basis of averages for located properties multiplied by total number of identified properties. Remaining vegetation only calculated for the indirect supply chain due to lack of mitigation measures. Source: Chain Reaction Research

COVID-19, deforestation pose fundamental threats to JBS SA’s business model

Scenario analysis shows how physical and transition risks may impact revenues and asset value

In addition to the longer standing deforestation exposure, JBS has been heavily affected by this year’s COVID-19 outbreak, both in the United States and in Brazil. In the US, outbreaks at its plants in Colorado, Utah, Michigan, Wisconsin, Texas, Nebraska, Minnesota and Pennsylvania have affected thousands of workers. In response, JBS has committed USD 120 million to funds aimed to combat the pandemic and has put a range of preventive safety measures in place.

On April 24 2020, a COVID-19 outbreak at a JBS’ poultry plant in the Brazilian state of Rio Grande do Sul marked the first large-scale outbreak at a Brazilian meat plant. This case marked the beginning of a wider outbreak at meat plants in the southern states of Brazil, where most of the country’s poultry and pork production facilities are located. As of late June, 32 plants operated by various companies in the state of Rio Grande do Sul had workers infected with COVID-19. According to state labor prosecutors, meat workers represent more than 25 percent of the 19,710 confirmed cases of infection in the state. At least five meat-workers in Rio Grande do Sul and 12 relatives or friends have died from the disease. Positive tests have also been reported for workers at JBS facilities in Goiás and eight JBS plants in Mato Grosso.

Both the growing concern over Amazon deforestation and the global responses to COVID-19 may have long-term impacts on JBS’ business and pose a range of different business risks. Notwithstanding the strong financial performance of JBS in recent quarters, these risks may adversely impact the company’s business model. This section analyzes various scenarios for each of the identified risks, in line with methodologies developed within the context of the Task Force for Climate Related Disclosures (TCFD).

1. Physical Risk: COVID-19 plant closures

After COVID-19 outbreaks were detected, JBS temporarily closed down several of its meat plants in the U.S. and in Brazil, either voluntarily or after legal orders. As reported in media articles, closures included;

- Souderton, Pennsylvania (beef) as reported on April 9

- Greeley, Colorado (beef) as reported on April 10

- Worthington, Minnesota (pork) as reported on April 20

- Green Bay, Wisconsin (beef) as reported on April 26

- Passo Fundo (RS) (poultry) as reported on May 9

- Ipumirim (SC) (poultry) as reported on May 18

- São Miguel do Guaporé (RO) (beef) as reported on May 27

- Caxias do Sul (RS) (poultry) as reported on June 6

- Trindade do Sul (RS) (poultry) as reported on June 12

Most of these closures were temporary and production restarted within a matter of weeks. In some cases, closures resulted in significant supply chain disruptions, with farm animals killed at supplying farms but not processed into meat products. At the other end of the chain, the closures led to empty meat shelves at retail facilities. In Rio Grande do Sul, a spokesperson for the meat producers’ association indicated that the shutdowns had not yet impacted production figures. However, at the time of this report, Brazil had the second most cases of COVID-19 globally and continued elevated daily rates of new infections. Meat plants continue to be COVID-19 hotspots, and it is probable that more closures will follow in spite of the prevention and control measures taken. In addition to plant closures, strikes, worker protests, and staff shortages as a result of COVID-19 outbreaks may also affect productivity.

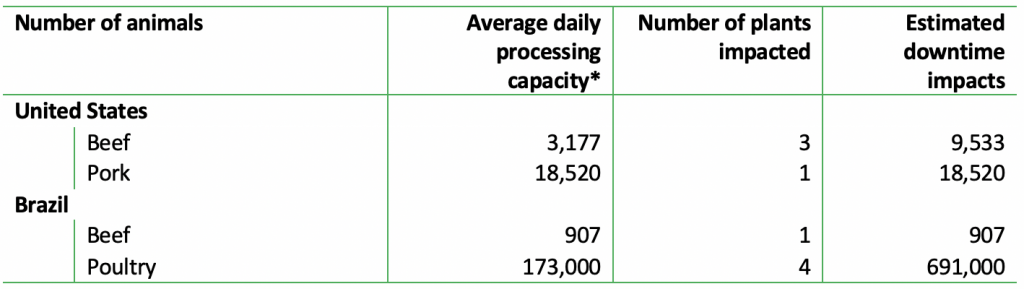

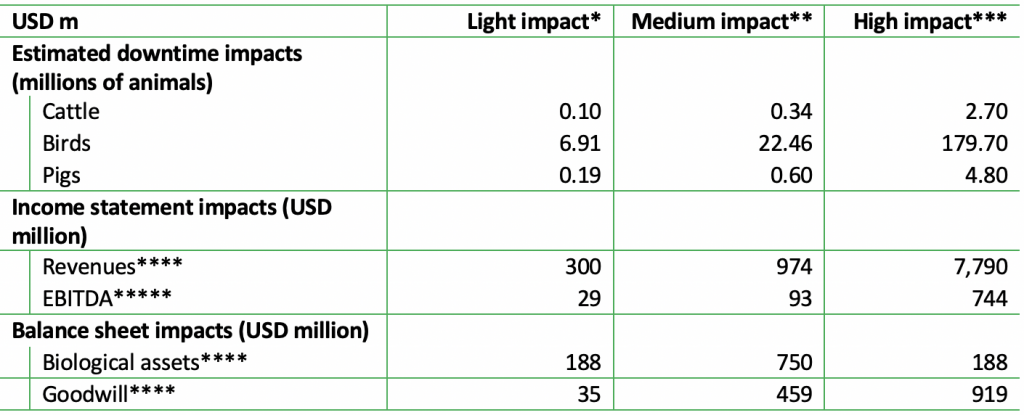

JBS has not disclosed the cumulative impacts of the closures on its production figures. Based on the reported average daily processing capacities in Brazil and the U.S., the impacts of downtime for the nine abovementioned plants are estimated to be 10,439 heads of cattle (13.9 percent of installed capacity), 691,000 chickens (16.1 percent of installed capacity) and 18,520 pigs (4.9 percent of installed capacity) per day. Closures have affected circa 4 percent of all JBS meat processing facilities.

Figure 8: Calculations for estimated daily downtime impacts due to COVID-19 plant closures

*Calculated on the basis of the reported daily aggregated capacity, divided by the number of plants per country (JBS Formulário de Referência, p.164-166).

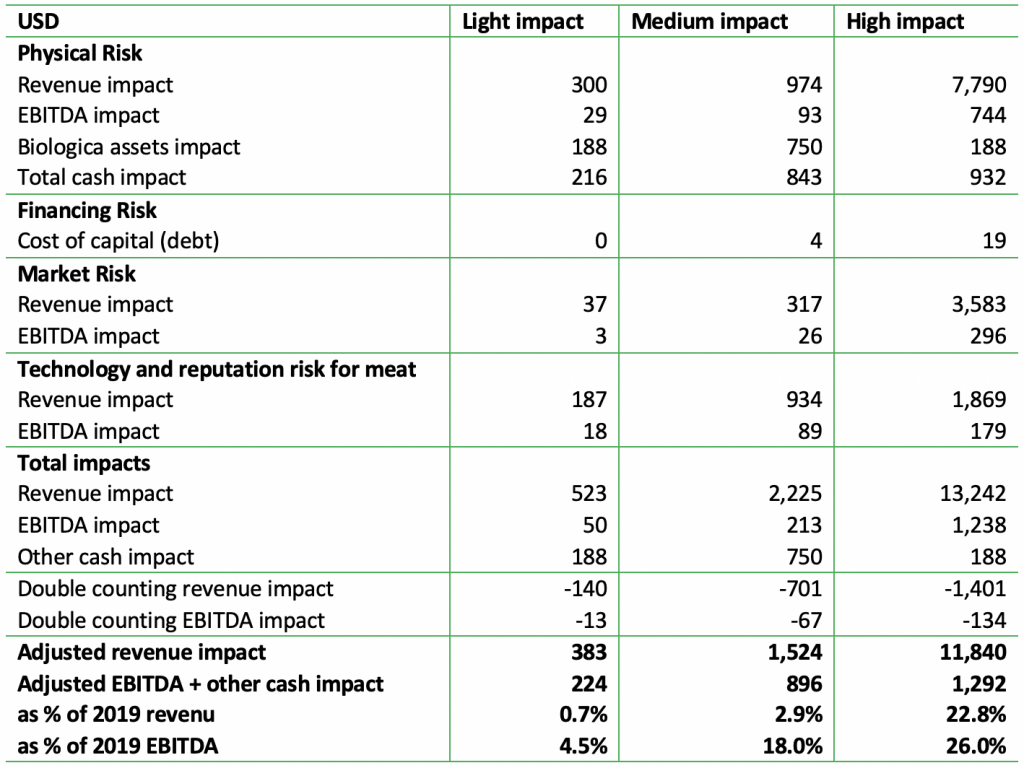

Temporary plant closures may impact both JBS’ revenues as well as its biological and intangible assets. Each day of a plant closure is assumed to have a linear negative impact on sales and gross profits. Repeated intermittent closures may have the largest impacts on JBS’ biological assets (2019: BRL 5 billion/USD 1.25 billion), whereas annual impairment tests may affect the goodwill of subsidiaries (2019: BRL 24.5 billion/USD 6.1 billion) on JBS’ balance sheet. Figure 8 shows projected impacts on revenues and assets under three forward-looking scenario’s: a light-impact scenario without further plant closures; a medium-impact scenario with intermittent plant closures during 2H20; and a high-impact scenario with full plant closures for the next 12 months.

Figure 9: Estimated financial impacts of COVID-19 related plant closures under three forward-looking scenarios

* Assumptions include average plant closures of 2 weeks for each of the nine reported plants and no additional closures in the future. **Assumptions include average plant closures of 2 weeks for each of the nine reported plants and future intermittent closures during 2H20. Calculations are based on one-week closures every month for a six month period. ***Assumptions include average plant closures of 2 weeks for each of the nine reported plants and future permanent closures for a 12 month period. ****Calculations based on assumed 15% impacts of events on revenues and asset values. *****EBITDA calculations do not include asset write-offs. Source: Chain Reaction Research

2. Reputation risk: increased investor concerns and shareholder action

International financial institutions are increasingly wary of Brazilian investments, in particular in the meatpacking sector. In June 2020, a group of 30 institutional investors from Europe and Asia called on the Brazilian government to curb environmental destruction. In a public letter, these investors signaled their intent to divest from Brazilian assets – corporate as well as sovereign – and highlighted their concern for Brazil’s meatpacking industry and its role in driving deforestation. Investor signatories represented USD 3.7 trillion assets under management. At least one investor, Nordea Asset Management, has followed through and announced that it excluded JBS from all assets it sells. In August 2020, it was reported that HSBC “sounded alarms” over its JBS investment due to deforestation inaction. These actions follow a string of shareholder action and engagement toward JBS in recent years:

- In March 2020, 95 current and past shareholders initiated legal arbitration, seeking BRL 1.4 billion (USD 280 million) in compensation for damages caused by JBS illegal practices. The shareholders’ claims are based on false and misleading statements made by JBS and its executive officers since its IPO in 2007.

- The Council of Ethics of the Swedish National Government Pension Funds reported on its engagement with JBS in its 2019 annual report: “The Amazon is once again in focus with an increase in illegal wildfires during the autumn of 2019. The Council on Ethics has strengthened its focus on soy production and cattle farming with the aim to ensure that companies like JBS, Bunge and Archer Daniel Midlands are sourcing their products from legally deforested parts of the Amazon.”

- In July 2018, Norges Bank officially placed JBS on its exclusion list, following a recommendation of its Council of Ethics. Norges owned USD 143 million in JBS shares at the time and cited “gross corruption” as the exclusion criterion. JBS remains this list as of March 2020.

- In April 2018, Dutch asset manager APG voted against the re-election of three of JBS’ directors. APG ranks among the ten largest JBS shareholders.

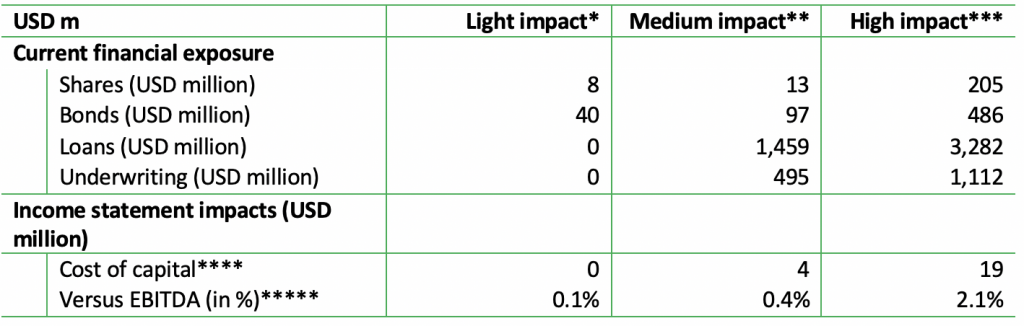

As investors grow weary of Brazil’s political and economic climate and concerns around deforestation increase, JBS SA may see an outflow of current investors and significantly reduced interest from potential investors. Reduced investor appetite could also significantly complicate the sale process of BNDES shares. Most investor action is currently coming from European financial institutions, which constituted the majority of the signatories of the June 2020 letter and have taken the lead in earlier engagement processes. Currently, 32 percent of JBS’ total financing comes from European investors.

Divestments, exclusions, refusal to extend loans, and other actions from financial institutions would affect JBS’ cost structure, and thus its net profits. In particular, its cost of debt may rise if banks refuse to extend loans and the company is forced to seek new financiers during difficult circumstances. Figure 9 projects the financial impacts of actions by financial institutions under three scenarios: a low-impact scenario with divestment from the signatories of the June 2020 letter; a medium-impact scenario with divestment from the signatories and their parent companies; and a high-impact scenario in which half of all European financial institutions withdraw.

Figure 10: Estimated financial impacts of deforestation-related financier action under three forward-looking scenarios

* Assumptions include divestment from the 30 signatories of the June 2020 public letter to the Brazilian government. ** Assumptions include divestment from the 30 signatories of the June 2020 public letter to the Brazilian government and their parent companies. *** Assumptions include divestment and refusal to extend loans from half of all current European investors. **** Calculated on the basis of a 25 base point increase in interest costs in the medium impact scenario and a 50 base point increase in the high impact scenario. ***** Calculated as percentage relative to EBITDA 2019. Source: Chain Reaction Research

* Assumptions include divestment from the 30 signatories of the June 2020 public letter to the Brazilian government. ** Assumptions include divestment from the 30 signatories of the June 2020 public letter to the Brazilian government and their parent companies. *** Assumptions include divestment and refusal to extend loans from half of all current European investors. **** Calculated on the basis of a 25 base point increase in interest costs in the medium impact scenario and a 50 base point increase in the high impact scenario. ***** Calculated as percentage relative to EBITDA 2019. Source: Chain Reaction Research

3. Market Risk: Restrictions to export markets and supply chain exclusions

COVID-19 may result in restrictions to export markets for JBS’ meat products produced in plants with virus outbreaks. In June 2020, China announced that it increased its inspections of imported meat products after a second wave of COVID-19 infections began due to an outbreak at a wholesale market in Beijing. Chinese customs no longer accept import licenses from 15 meat plants. The four suspended plants in Brazil include one JBS poultry plant. This move followed an earlier suspension of beef imports from Australia, possibly in retribution to Australia’s criticism over China’s handling of the COVID-19 outbreak. The four Australian meat plants subject to this suspension included two JBS-owned plants. The more restrictive Chinese approach to imported meat products may particularly affect JBS SA’s Brazilian exports to China, which has been a notable growth market for the company in recent years.

Concerns over wildfires and deforestation may also result in further exclusions from corporate supply chains for non-compliance with responsible sourcing policies. In the aftermath of the 2019 wildfires in the Amazon, global fashion brands H&M and VF Corporation suspended all use of leather originating from Brazil because of the cattle industry’s role in the fires. In May 2020, a group of more than 40 British supermarkets warned the Brazilian government that it may boycott Brazilian products if legislation that allowed for faster Amazon deforestation passes. In August 2020, a Greenpeace UK campaign called on retailer Tesco to cut all ties with JBS. With higher deforestation rates in the first months of 2020 and indications of another intense fire season, more boycotts, exclusions, and suspensions may occur.

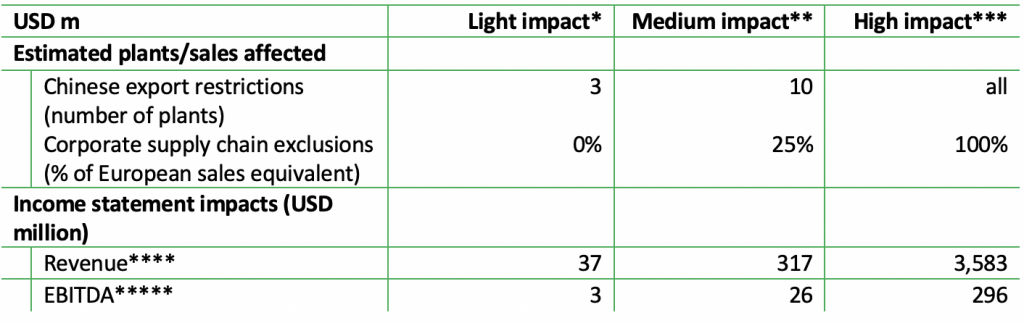

Further export restrictions to China and loss of corporate customers would impact JBS’ revenues and EBITDA margins. China has become an increasingly important sales market, and JBS is investing in partnerships for direct-to-consumer sales. Corporate clients with zero-deforestation commitments are likely present in both its leather and beef sales channels. Figure 10 shows the financial impacts under three forward-looking scenarios: a light-impact scenario with no further export restrictions or supply chain exclusions; a medium-impact scenario with a limited number of future export restrictions and supply chain exclusions; and a high-impact scenario in which access to Chinese and European markets is significantly restrained.

Figure 11: Estimated financial impacts of deforestation and COVID-19 related export restrictions and supply chain exclusions under three forward-looking scenarios

* Assumptions include no further export restrictions or supply chain exclusions other than already reported on. **Assumptions include seven additional plants with future export restrictions to China, and future supply chain exclusions representing the equivalent of 25 percent of EU sales. ***Assumptions include future fully restricted access to the Chinese and European markets **** Calculations based on total number of meat plants (230), reported sales in China (USD 2,803 million) and reported sales in Europe (USD780 million). ***** Calculations based on revenue impacts and EBITDA margins of JBS Brasil (5.4%) and Seara (11.1%). Underlying assumptions include a 75% share of Brazilian facilities to total JBS export figures. Source: Chain Reaction Research

4. Reputation and Technology Risk: Growing Chinese consumer weariness for imported meat products and substitution threats by plant-based proteins

In addition to the restrictions by Chinese customs, trends in Chinese consumer preferences may also negatively impact JBS’ meat export potential. Both the outbreak of the African Swine Fever and the outbreak of COVID-19 have raised questions among Chinese consumers about the safety and sustainability of animal proteins. Market research firms project that interest in plant-based protein and lab-grown meat will grow among consumers in China in the next ten years. As plant-based proteins are not new to Chinese consumers, market acceptance of alternative meat products is likely if consumers are educated about the nutritional, health, and safety benefits.

The World Economic Forum also notes that demand for plant-based protein is surging in Asia as a result of consumer suspicions over possible links between animal meat and COVID-19. This change in demand is most notable in Hong Kong and mainland China. The virus outbreak has accelerated an ongoing trend that already caught the attention of JBS’ plant-based rivals Beyond Meat and Impossible Foods. Both international and local companies are producing alternative meats used in dumplings, noodles, rice, and fast-food products.

Plant-based proteins are rapidly becoming a viable and economic substitute product to animal proteins amid a rapid decline in production costs. In May 2020, Beyond Meat’s CEO indicated that the company is ready to compete directly with real beef on price terms in supermarkets. The surge in beef prices caused by the COVID-19 triggered supply chain disruptions has narrowed the gap in relative prices. Beyond Burger’s gross margins provide room for the company to lower retail prices in order to capture market share from real meat products. In March 2020, Impossible Foods made a similar move when it cut its vegan product prices by 15 percent. Both Beyond Meat and Impossible Foods have entered the Chinese market.

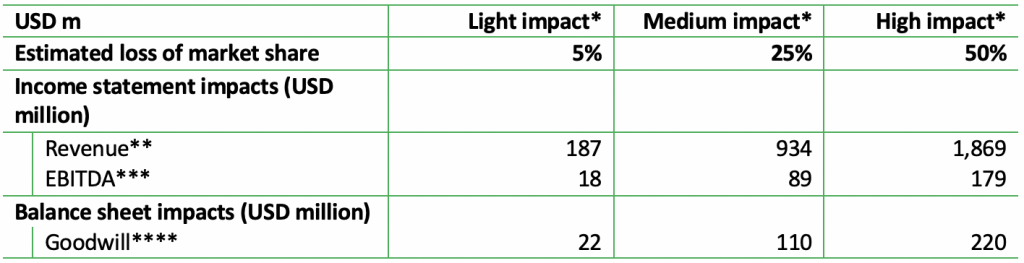

Plant-based meat alternatives may cut into JBS’ Chinese meat market share and its revenues. With JBS’ recent partnerships with WH Group and Alibaba, direct sales to Chinese consumers have become an important and growing revenue stream that may be at risk from this development. Figure 11 illustrates the financial impacts of losing market share to plant-based proteins under three forward-looking scenarios: a light-impact scenario in which JBS loses 5 percent of its Chinese market share to plant-based alternatives; a medium impact scenario in which it loses 25 percent of its Chinese market share; and a high-impact scenario with a 50 percent market share loss. The company may be able to mitigate these risks through increased investments in the plant-based alternatives that the company has already introduced in various markets.

Figure 12: Estimated financial impacts of loss of Chinese market share to plant-based proteins under three forward-looking scenarios

* Assumptions include loss of market shares to competitors and does not take into account new plant-based product lines that JBS may introduce. ** Based on net revenues in China of USD 3,737 million in 2019. *** Based on EBITDA margin of 9.6 percent in 2019. **** Based on JBS goodwill multiplied by Chinese share in 2019 sales and multiplied by resp. 5%, 25% and 50%. Source: Chain Reaction Research

Summary of the four financial impacts and the three scenarios

The sum of the four impacts, after deduction of double counting, may impact revenues by 22 percent and EBITDA by 26 percent in the “high-impact” scenario. The double counting refers to the reduction in Chinese revenues which is calculated twice in the market risk impact and in the technology impact.

Figure 13: Summary of four financial impacts in three scenarios

Source: Chain Reaction Research

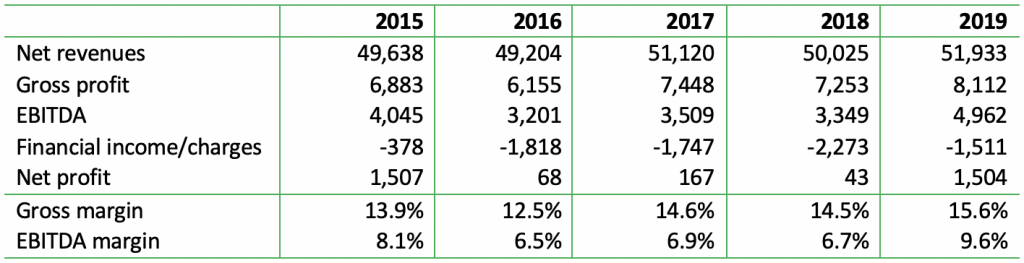

2Q20 EBITDA higher than expected due to imbalance between demand and supply

2Q20 results surprised analysts mainly because of relatively high margins in the U.S. and Brazilian Beef operations, but the quarter was clearly an outlier. In the JBS Brazil unit (mainly beef), the animals “processed” declined by 15 percent, but exports to China increased by 53 percent in USD. The EBITDA margin increased from 4.7 percent in 2Q19 to 12.4 percent in 2Q20. JBS USA Beef (including Australia and Canada) saw an 18 percent decline in volume due to capacity closure related to COVID-19. But amid higher prices as demand continued to be strong, the EBITDA margin grew from 8.9 percent in 2Q19 to 20.4 percent in 2Q20. For the whole company, the 2Q20 EBITDA margin was 15.5 percent versus 6.9 percent in 1Q20 and 10.0 percent in 2Q19. Figure 13 shows that 2Q20 is an outlier as the EBITDA margin develops in a range of 6.5-9.6 percent on an annual basis between 2015 and 2019.

Figure 14: Summary of Profit & Loss JBS SA in USD million

Source: Chain Reaction Research, Bloomberg, July 6, 2020

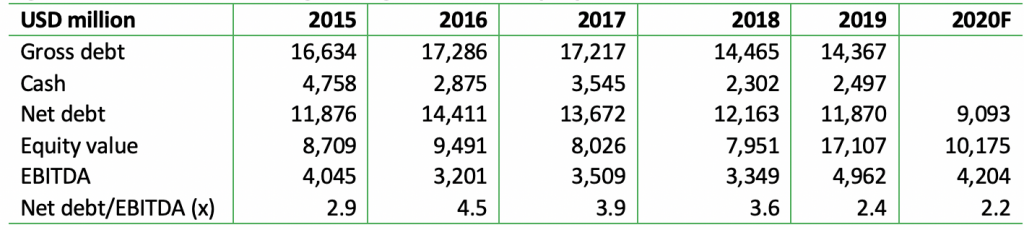

USD 10 billion financing may be in conflict with forest policies

JBS highly depends on debt financing and net-debt/EBITDA would deteriorate materially in a high-impact scenario. Since banks and bondholders have the most impact on the cost of capital of a company, JBS’ high debt level could become an important ESG issue for financers that engage the company. More and more, leading banks are issuing loans linked to ESG targets. At the end of 2Q20, JBS’ debt consisted of 66.5 percent bonds and 33.5 percent bank loans. Just under 94 percent of debt is denominated in USD and 6.1 percent in Brazilian Real. At the end of 2Q20, net debt stood at USD 10.0 billion, which is higher than the Bloomberg consensus estimate of USD 9.1 billion for end 2020. Although the net-debt/EBITDA has improved recently, the high-impact scenario would pro forma shave off USD 1.3 billion of the USD 4,962 million (2019) and lead to a net-debt/EBITDA of 3.2X.

Figure 15: JBS SA’s Financing through Debt and Equity

Source: Chain Reaction Research, Bloomberg, July 6, 2020; F = forecast based on consensus.

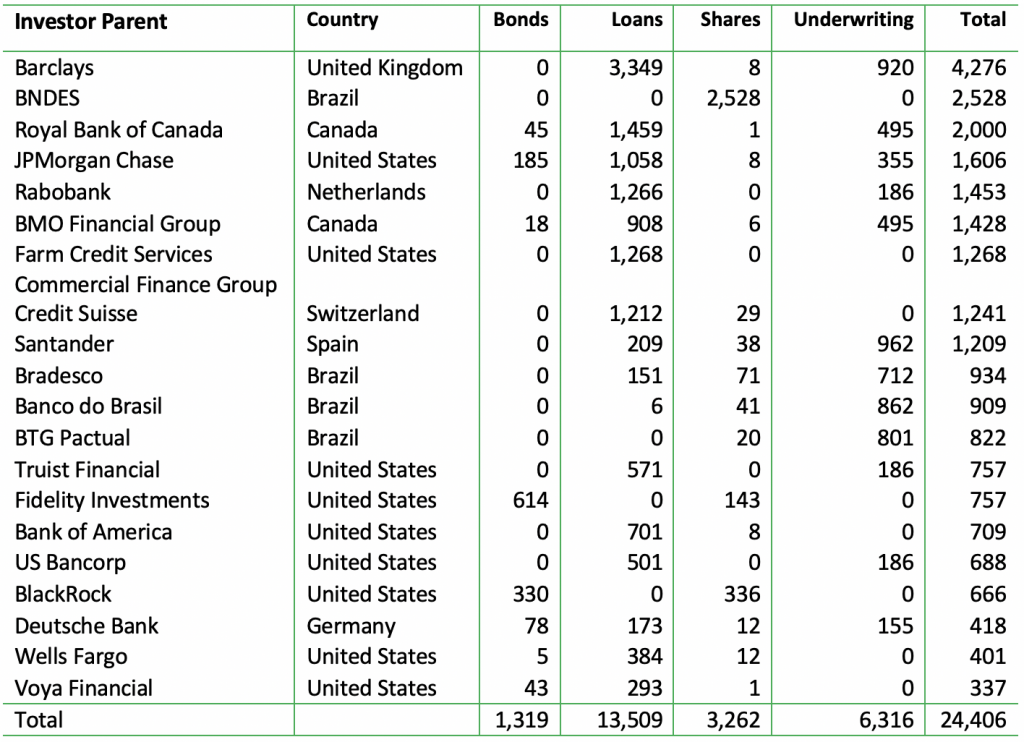

Of the top-20 financers, half of them — with USD 10 billion exposure to JBS — have deforestation policies or policies that are gradually adapting zero-deforestation. Figure 15 summarizes the top-20 financers (excluding the family holdings) of JBS and its affiliates, including JBS USA and Pilgrim’s Pride. In total, these financers have provided USD 24.4 billion of financial services to JBS and its affiliates: USD 13.5 billion in loans, USD 1.3 billion in bond holdings, and USD 3.3 billion in shareholdings. And through underwriting services, JBS has been offered USD 6.3 billion.

In 2019, JPMorgan Chase (exposure USD 1.6 billion), the group company of JPMorgan Asset Management, released its first climate report based on recommendations by TCFD (Task Force on Climate-related Financial Disclosures). JPMorgan Chase’s policies cover all group activities. The group is also signatory or member of many other initiatives, including the Consumer Goods Forum (CGF), which strives for zero-deforestation. Rabobank (exposure USD 1.5 billion) is an active member of the Round Table on Responsible Soy (RTRS), with a seat on the executive board. Rabobank is also a member of the CGF. Credit Suisse (exposure USD 1.2 billion) sees the protection of biodiversity as an integral part of its sustainability commitments. Its policies are aligned with RSPO and Forest Stewardship Council (FSC), but the bank does not mention explicitly zero-deforestation targets. Santander participates in the RTRS, and through the Banking Environment Initiative (BEI) it participates in the Soft Commodity Compact. Barclays is a signatory to the New York Declaration on Forests (NYDF) of the United Nations, which aims to cut natural forest loss in half by 2020, and to end it by 2030, and adopted the Banking Environment Initiative’s Soft Commodities Compact. This initiative, according to Barclays, commits the bank to zero-deforestation in forestry, pulp and paper, and palm oil. Deutsche Bank has also signed the NYDF.

Some other financers are taking steps to developing a policy on deforestation. Bank of America and Bancorp say they will not engage in business contacts with companies active in illegal logging or uncontrolled fire. There is, however, a large group of top-20 financers which have no forest policies. BNDES and other Brazilian banks have no concrete zero-deforestation commitments. Royal Bank of Canada has no policies on deforestation, similar to BMO Financial Group (exposure USD 1.4 billion). Farm Credit Services (exposure USD 1.3 billion) has no material environmental policy, while BlackRock and Fidelity have no forest policies.

Figure 16: Investors’ and banks’ exposure to JBS and its affiliates in US Dollars (million)

Source: Chain Reaction Research, Thomson-Eikon, Bloomberg; data June 3, 2020

Annex 1: Methodological notes for deforestation analysis

This company profile includes a deforestation analysis of JBS’ direct and indirect supply chains. This annex describes the methodological notes of the approach used. It describes the following:

- The main sources of data used

- A description of the data processing and database development

- A description of the data analysis and quality checks

- The limitations to the methodology

1. Data sources

The main sources of data include:

- Animal transportation permits (GTAs). These permits are mandatory sanitary documents required when transporting cattle between two properties. CRR used 2019 GTA records from the states of Minas Gerais, Goías, Mato Grosso, Mato Grosso do Sul, Pará, and Tocantins to identify the names of the farms that directly and indirectly supply JBS.

- Rural cadasters and property registries. CRR used the SIGEF (Sistema de Gestão Fundiária) and SNCI cadasters and property registries obtained from Brazil’s National Institute for Colonization and Agricultural Reform (INCRA).

- Annual confirmed deforestation data. CRR used the official annual data from the Brazilian government’s Program to Calculate Deforestation in the Amazon (PRODES) as the basis for the deforestation calculations in both the Amazon and the Cerrado.

- Remaining vegetation data. CRR used maps from Brazil’s space agency INPE (for the Amazon) and the FREL data from the Ministry of Environment (for the Cerrado) to assess remaining native vegetation.

2. Data processing and database construction

Three following steps were taken to construct the database for this report:

- Clean and prepare GTA information. Using R studio, a script was written to clean text within both our GTA dataset and the SIGEF and SNCI land registries to ensure the highest possible success of string matching. Examples of this cleaning include the conversion of Portuguese characters to English (ã to a), standardizing the spacing between words, and standardizing the name of companies (i.e. JBS exportaçãoto JBS).

- Identify direct and indirect suppliers of JBS.A script was written to search through the GTA dataset and extract all entries that had a JBS slaughterhouse as the final destination. Filtering was applied for “abate” (slaughter) and “bovinos” (cattle), to limit data to the beef supply chain of JBS and to ensure the slaughterhouse was the end destination. To identify indirect suppliers, CRR repeated this process with JBS’ direct suppliers as the registered destination of the cattle transport. In order to avoid false positives, we only included records whereby the owner name, farm name, and municipality matched. We applied the filters of engorda (fattening) or reprodução (reproduction) as the purpose for transportation. Through this method, a total of 9,730 direct supply farms and 56,421 indirect supply farms to JBS were identified. These suppliers each supplied one or more batches of cattle. An excel sheet with the details of these suppliers was created (“JBS identified suppliers”).

- Geographically locate suppliers. Using R studio, string matching was performed to match the “JBS identified supplier” dataset to the SIGEF and SNCI cadaster and property registries for the six states within the scope of this analysis. In order to avoid false positives, records were only included if a match was found between datasets on; a) the name of the landowner; b) the name of the farm; and c) the municipality of the farm. If two or less of these metric matches, suppliers were excluded from further analysis. Through this method, a total of 983 direct supply farms and 1,874 indirect supply farms were located. Two shapefiles with georeferenced data were created in QGIS (“JBS located direct supplying farms” and “JBS located indirect supplying farms”).

3. Data analysis and quality checks

The “JBS located direct supplying farms” and “JBS located indirect supplying farms” shapefiles were subsequently used as the basemap for analysis of deforestation and remaining vegetation, through the following steps:

Overlay PRODES deforestation data. CRR used confirmed PRODES deforestation alerts from Instituto Nacional de Pesquisas Espaciais (INPE) for the years 2008-2019. CRR chose 2008 as the cut-off year as it is in line with Brazil’s Forest Code. Deforestation data was intersected with the two shapefiles to calculate deforestation at each located property, resulting in a total of 20,296 ha for the 983 direct supply farms and 50,852 ha for the 1,874 indirect supply farms.

Overlay remaining vegetation data. CRR used historical deforestation data from INPE for the Amazon going back to 1988, and the 2000 FREL native vegetation basemap for the Cerrado. CRR calculated the total land area for the indirect supply farms and detracted all changes in native vegetation since the beginning of these timelines. However, CRR did not conduct this calculation for the direct supply chain, under the assumption that JBS’ own monitoring systems would mitigate the risk of future clearing of native vegetation on these properties. The calculations resulted in a projection of 2.1 million ha of forest and other types of native vegetation remaining within the located indirect supply farms.

Projections of deforestation footprint in direct and indirect supply chain. In order to extrapolate the findings in our sample, CRR calculated averages for the deforestation per property. For the located direct supply farms, CRR calculated an average of 20.65 ha per property (20,296 ha of deforestation divided by 983 located properties). CRR multiplied this average by the total of 9,730 identified direct supply farms to come to the estimated projection of 200,000 ha of deforestation in JBS’ direct supply chain since 2008. This calculation was repeated for the indirect supply farms, resulting in a higher average deforestation per farm of 27.14 ha per property. The extrapolated estimation to the 56,421 identified indirect supply farms resulted in a figure of 1.5 million ha deforested since 2008.

Quality checks. CRR conducted a number of quality checks during various phases of the data analysis. These include:

- Confirming that the slaughterhouses listed as the destination in the GTA records are still owned by JBS by matching record with the list of assets included in JBS’ corporate reference document.

- Removing the duplicate records of located properties that have both SIGEF and SNCI registrations in order to avoid double counting.

- Intersecting deforestation alerts with property boundaries to exclude deforested areas that spill over farm boundaries.

- Conducting, at each stage of the analysis, sample quality checks to ensure proper functioning of the applied scripts.

- Calculating the average deforestation per farm for both properties with and without deforestation in order to balance projected estimates for JBS’ full deforestation risk exposure and account for the reality that not all supplying farms have deforestation.

- Using Cochrane’s equation for choosing a sample size for a large population (Equation 1), to ensure the representativeness of our sample. With this formula, it can be determined that using data for 384 farms would have been sufficient for a representative sample. We used 983 farms, which is approximately 10 percent of the 9,730 direct supply farms identified in the GTAs.

Equation 1: Cochrane’s equation:

n0

is the required sample size, Z is the z-value (found in a z-table), p is the estimation of how many farms have deforestation (0.5 assumes maximum variability; that half the farms contain deforestation and half do not), e is the desired level of precision (in this case 95%) and q is 1-p.

n0= Z2pqe2

n0= (1.96)2(0.5)(0.5)0.052

n0= 384.16 farms

- Methodological limitations

CRR’s data and analytical methods pose a number of limitations that merit caution in interpretation of the presented findings. They include:

- Conservative estimates and projections. We have made a number of choices that resulted in more cautious estimates and potential underreporting of totals. These include:

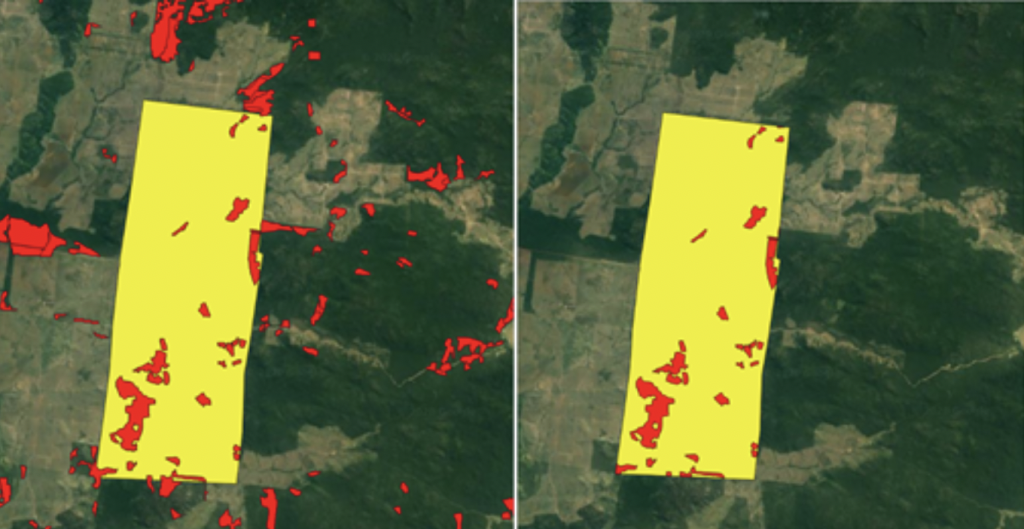

- Not attributing deforestation adjacent to but outside farm boundaries.In several cases, deforestation alerts transgress farm boundaries. CRR excluded all deforestation that took place outside of farm boundaries from our calculations, despite the likelihood that they are part of a single deforestation event. See Figure 1a below for an example.

- Projections based on 2019 GTA records. CRR projects the total deforestation footprint on the number of properties included in our 2019 GTA records. As a result, it excludes JBS suppliers that did not supply the company in 2019, but did so in other years. It also excludes any suppliers with faulty, fraudulent, or absent GTA records.

- Data does not cover the Amazon states of Rondônia and Acre.The GTA dataset did not include data for these two Amazon states. These are states with significant deforestation in recent years, and where JBS has a presence. The direct and indirect supply chains for its two slaughterhouses in Rondônia and one slaughterhouse in Acre are not included in our calculations.

- Analysis does not cover third-tier supply chain and beyond.The analysis is based on identified suppliers in the first and second tier of JBS’ supply chain. It excludes any farms that may be further removed from the slaughterhouse. Cattle typically move from property to property multiple times during its lifetime and any deforestation risks in these tiers are also fully unmitigated.

- No distinction between legal and illegal deforestation. This analysis does not make a distinction between legal and illegal deforestation and does not make any claims of illegal practices by JBS or any of its suppliers, other than referring to third party reports. In particular in the Cerrado biome, the majority of deforestation falls within the scope of Brazil’s Forest Code.

Figure 1a: Demonstration of the clipping tool in QGIS

Note: The deforestation is indicated in red and a JBS direct supply farm in yellow. The deforestation events at the bottom of the farm are all part of the one event although only part of it will count as this farm’s deforestation