Coffee production has been identified by the Peruvian Agricultural Census of 2012 as one of the major drivers of deforestation in the Peruvian Amazon, making up 25.4 percent of agricultural land in this region. Smallholders with less than 5 hectares (ha) of land produce 62 percent of the coffee grown in the Peruvian Amazon, often applying shade-grown techniques. Smallholder coffee production and the expansion of the agricultural frontier by migrant farmers contribute to deforestation and forest degradation.

In 2016, Olam Peru was the second largest exporter of coffee from Peru with 13 percent volume share. Olam Peru has an important role in the coffee value chain. It purchases 95 percent of its coffee from smallholders through agents and intermediaries. Its parent company Olam International (Olam) has zero-deforestation goals, but policy implementation remains not fully adopted within Olam Peru’s coffee value chain. This exposes Olam to deforestation risks, which could result in reputational damage.

Key Findings

- Olam International has extensive environmental sustainability policies. Olam’s upcoming Global Forest Policy, will have a cross-commodity scope and may apply to Olam Peru’s coffee supply chain.

- Olam Peru is one of the largest coffee traders in Peru. In 2016, it accounted for 13 percent of Peruvian coffee exports. As most Peruvian coffee is produced for sale to export markets, Olam Peru has an important position in the coffee value chain. Olam Peru sources 95 percent of its coffee through a network of licensed agents, intermediaries and traders. Suppliers are selected on a day-to-day basis.

- Government institutions, research agencies and civil society have identified coffee as a major driver of deforestation in the Peruvian Amazon. Coffee has the highest land coverage and highest expansion rates of all commodities produced in the Peruvian Amazon. Small-scale coffee production and the expansion of the agricultural frontier by migrant farmers contribute to forest loss.

- Olam Peru uses certification schemes for parts of its supply chain. It applies its Livelihood Charter and Supplier Code to smallholders and intermediaries, but Olam Peru is unable to guarantee a zero-deforestation supply chain. Olam Peru does not suspend trading relations in response to non-compliance with its sourcing policies.

- Olam International faces reputational risk because of deforestation in Olam Peru’s coffee supply chain. It is unlikely that Olam faces possible loss of clients or regulatory sanctions because of Peruvian deforestation in its supply chain. If Olam Peru lost all its Peruvian coffee sales due to deforestation risks, it would have a negative impact of 0.5 percent on Olam’s enterprise value. Because of Olam’s high debt level, this would trigger a negative 1.6 percent impact of 1.6 percent on its equity valuation. This USD 60 million annual loss of client revenue would exceed the estimated USD 10 million financial gain from extra coffee sales by Olam Peru from deforested land.

Olam International: The World’s Largest Farmer

Figure 1: Olam segment revenue, 2016 (Source: Olam International, Annual Report 2016)

Olam International is one of the ten largest agri-commodity companies globally. Since its founding in 1989 and currently headquartered in Singapore, it has grown from a commodity trader to a vertically integrated player with assets throughout the supply chains and across various products. Its 18 product platforms source from 4.33 million farmers. Olam International (Olam) has 2.4 million hectares (HA) under direct management. Olam sources from an additional 7.1 million ha. In FY2016, Olam reported revenues of USD 14.9 billion, resulting in a net profit of USD 225.0 million.

As shown in Figure 1 (right), Olam has five business segments:

- Edible Nuts, Spices and Vegetable Ingredients

- Confectionery and Beverage Ingredients (cocoa and coffee)

- Food Staples and Packaged Foods

- Industrial Raw Materials, Ag Logistics and Infrastructure

- Commodity Financial Services

37 percent of Olam’s 2016 revenue was from its coffee and cocoa business segment. It operates single-estate coffee plantations in Brazil, Zambia, Tanzania, and Laos. Olam is one of the world’s leading coffee traders. It sources from Africa, Asia, Central America and Latin America. Olam is Peru’s second largest coffee exporter by volume and value.

Olam’s Sustainability Policies Include Suppliers and Smallholders

Olam applies its Olam Sustainability Standard Framework (OSSF) to its business activities across its supply chains. It has seven focus areas:

- Labor

- Land

- Water

- Climate Change

- Livelihoods

- Food Security

- Food Safety

Olam sources from 4.33 million farmers globally. Its Supplier Code last updated October 17, 2014, addresses responsible business practices in its supply chain. The Code was implemented in 2013 in priority products in key countries, including coffee in Peru. By 2016, 58 percent of all tonnage from priority product volumes was covered under its Supplier Code. Olam defines priority products as having high risk of social and environmental impacts.

These products include:

- Cashew

- Coffee

- Cocoa

- Cotton

- Hazelnut

- Palm oil

- Rubber

By signing the Supplier Code, suppliers are expected to commit to the following:

- Commit to corporate governance and integrity

- Guarantee the quality of goods and services they supply

- Uphold labor standards and human rights within their operations

- Respect the natural environment

- Conduct their business in a way that honors the local community

- Ensure compliance.

In 2016, the Olam Livelihood Charter (OLC) reached 302,552 smallholder farmers in 19 countries including Peru, and in key value chains, including coffee. Olam uses the OLC to reduce its smallholders’ environmental footprint. The company organizes trainings for smallholders it sources from on climate smart agricultural practices to increase productivity and to improve soil, water, and forest management.

Olam says it cannot monitor land management processes for all its suppliers, as it cannot physically reach all the supplying farms. As a result, the company prioritizes the high-risk products cashew, cocoa, coffee, palm oil and rubber. The OLC and its Supplier Code are also used to extend influence on its indirect suppliers.

Zero Deforestation Commitments for Palm Oil

Olam has deforestation policies for its palm oil supply chains. Its specific palm oil No Deforestation, No Peat, No Exploitation (NDPE) policy extends to all Olam owned and managed plantations, outgrowers in Gabon, and third-party suppliers who have specific commitments. For palm and rubber plantation activities, Olam applies Free, Prior and Informed Consent (FPIC), Environmental and Social Impact Assessment (ESIA), participatory mapping, and the Roundtable on Sustainable Palm Oil (RSPO) Principles and Criteria. All palm oil suppliers have signed the Olam Supplier Code.

In December 2016, the Mighty Earth forest campaign alleged that Olam caused deforestation in Gabon. The forest campaign alleged that Olam created a market for deforestation-linked palm oil. It criticized the company for giving its suppliers until 2020 to comply with its sustainability requirements. These organizations alleged that Olam violated its FSC commitments, and that the company did not use a proper High Carbon Stock Approach (HSCA) methodology to identify forest areas suitable for clearing. In response, Olam indicated that it could not sign onto the HCSA approach on the basis of available land in Gabon and that most development took place in degraded forests.

In February 2017, Olam pledged to stop clearing forest in Gabon for one year. In response, the forest campaign dropped its FSC complaint. Olam updated its palm oil policy and made a commitment to publish more information about its supply chain. This agreement applies to Olam’s palm oil and rubber suppliers. The forest campaign announced it will further investigate Olam’s social and environmental impacts specifically targeting its coffee and cocoa supply chains.

Olam was one of twelve cocoa and chocolate companies that committed in March 2017 to zero-deforestation and forest degradation in their global cocoa supply chains. This commitment initially focuses on Côte d’Ivoire and Ghana. The 12 companies will announce the framework at COP 23 in Berlin in November 2017.

Cross-commodity Forest Policy Forthcoming

In its 2016 Annual Report, Olam announced it will launch a cross-commodity Global Forest Policy in 2017. Olam stated this policy will strengthen and clarify its OLC and Supplier Code-deforestation related requirements for all third-party suppliers and smallholders. The policy will become part of Olam’s sourcing policy. Suppliers will be required to sign deforestation supply chains. It does not make clear if, how often or by whom third-party audits are required. It does not discuss the consequences of non-compliance.

Once adopted, Olam’s cross-commodity policy might commit the company to addressing deforestation issues in a range of sectors and countries including Peruvian coffee.

Olam Peru Has a Key Position in the Coffee Value Chain in Peru

Figure 2: Peru coffee estate 2014 to 2017 (Source: USDA, 2017)

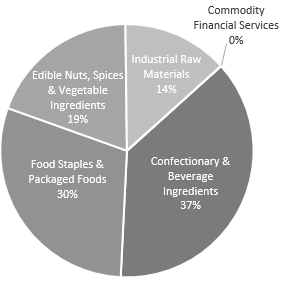

Peru’s total coffee production for the year 2015/16 was 183,000 metric tons (3.05 million 60 kg bags). U.S. Department of Agriculture (USDA) estimates that 2016/17 coffee production will increase 37 percent, reflecting recovery from leaf rust. As shown in Figure 2 (left), the harvested area equals 355,000 ha.

The Peruvian Government has made international coffee promotion a national priority. Peru’s coffee production is 90 percent Arabica coffee, with greater than 70 percent of the typica variety and 20 percent the caturra variety. The USDA calculates Peru’s average cost of production at USD 1.75 per kg, 86 cents of which is labor. Conventional fields yield on average 2,025 to 2,250 kg per ha per year, while organic fields yield 540 to 675 kg per ha per year in Peru. The price premium of USD 40 per bag does not compensate organic farmers for their lower yields.

Figure 3: Olam Peru’s coffee operations in Peru (Source: Olam Peru).

In 2016, Olam Peru accounted for 13 percent of Peru’s total coffee exports. Olam Peru was a separate company registered under the name of Outspan Peru S.A.C. In 2006, Olam International Limited incorporated Outspan Peru S.A.C. as its wholly-owned subsidiary. Olam Peru main products are Arabica coffee, oregano and paprika. As shown in Figure 3 (above), its coffee operations operate two dry mills, six warehouses, six buying units and four cupping labs.

Olam Peru sources its coffee from Peru’s core coffee growing regions. It manages the coffee value chain from origination to sale and delivery. 95 percent of its procurement of smallholder-grown coffee goes through intermediaries and agents. The remaining 5 percent of annual volumes is sourced directly from around 1,000 smallholders.

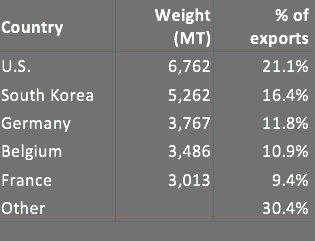

Figure 4: Olam Peru’s annual coffee exports percent of total Peruvian exports. Source: Olam International.

Olam Peru markets 14 different types of Peruvian coffees. In FY2016, Olam Peru exported 31,887 metric tons of coffee with a value of USD 89,886,205. As shown in Figure 4 (right), this equals 13 percent of Peru’s total coffee

exports. Olam Peru is Peru’s second largest exporter. In Figure 5 (below), Olam Peru’s exports are compared versus its competitors.

In FY2016, the United States was Olam Peru’s largest importer purchasing 21.1 percent of its coffee. Consignees in the U.S. are mostly other subsidiaries of Olam, which then often sell to other buyers.

Exports are the Most Concentrated Node in the Peruvian Coffee Supply Chain

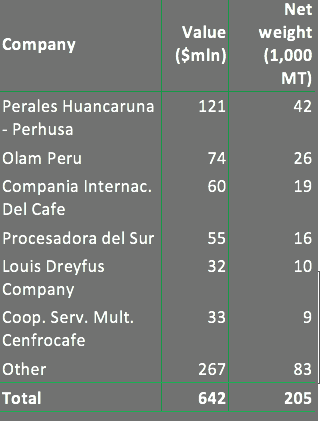

Figure 5: Olam Peru’s coffee exports compared to is competitors, Jan to Nov 2016. Source: Junta del Cafe.

As shown in Figure 5 (left), Olam Peru and five other firms account for 60 percent of the USD 642 million coffee export market. In 2016, Perales Huancaruna (Perhusa) was the largest exporter at 20 percent followed by Olam Peru at 13 percent. The largest importers for coffee from Peru are the US and Germany.

In 2015, 106 cooperatives and associations shipped 35,000 metric tons of coffee or 20 percent of total exports, valued at USD 144 million. An important main umbrella organization was created in 1993, when 5 of the major coffee cooperatives merged into the Junta Nacional del Cafe (JNC), the National Coffee Board. It functions as a platform for farmer organizations. It represents 56 coffee cooperatives and associations.

90 percent of Peruvian coffee is exported. Peru’s domestic consumption has doubled over the last five years to 10 percent of total production and nearing 1 kg per capita. In comparison, coffee consumption in Brazil exceeds 4 kg per capita.

Figure 6: Top destinations for Olam Peru’s coffee exports, 2016. Source: SICEX.

Exports are expected to continue increasing. In calendar year 2016, Peru exported 240,220 metric tons. Export prices for Peruvian coffee averaged USD 3,164 per metric ton in 2016, 5 percent lower than in 2015. USDA forecasts exports to continue increasing, driven by progress in combating the effects of the coffee leaf rust outbreak, and an expansion of coffee planted area resulting from the Peruvian government program to renew 80,000 ha of coffee land.

Associations might provide technical assistance and finance during the pre-harvest, harvest and post-harvest phases, and focus on meeting the quality standards of importers. However, most cooperatives face currency risks from fluctuating international prices, constraints to obtaining credit, lack of technological innovation, and other economic difficulties

Coffee Production Causes Peruvian Deforestation

Peru is globally the 8th largest producer and 7th largest exporter of coffee by volume in 2016/17. Peru has perfect growing conditions for the Arabica variety. Coffee is traditionally produced in agroforestry systems with shade-grown techniques. Forest cover does not always remain. It is common practice to clear land and replant some trees to provide necessary shade. In some areas shade-grown coffee has been replaced by higher productivity Arabica variety and high-input sun-grown coffee.

In 2016/17, 380,000 ha of land was under coffee cultivation in Peru. Since 2001/02, Peruvian coffee cultivation has increased by 110,000 ha. Peruvian Ministry of Agriculture SERFOR’s 2015 study showed that coffee was the permanent crop with the highest expansion rates from 2004 to 2010, followed by cocoa and oil palm trees. Coffee is produced throughout the eastern slope of the Andes, which is part of the Amazon. Chanchamayo province (Junín region) accounts for 28 percent of national coffee production, while combined Amazonas and San Martín regions account for 49 percent. The latest Peruvian Agricultural Census of 2012 identified coffee as the crop with the highest land coverage in the Peruvian Amazon, totaling 25.4 percent of cultivated area. The northern region, bordering Ecuador, has seen most recent growth in coffee production.

The Amazon region of Peru is home to 10 percent of Peru’s 31 million citizens. Most of them are involved in agricultural activities at the forest margin. The livelihood strategies of these farmers have a significant impact on shaping a landscape mosaic of forest and non-forest land, fallow, and agricultural land.

Peru is the world’s leading exporter of organic coffee with 90,000 ha certified organic. This represents 25 percent of Peru’s total harvested area in 2016/17. For a large part, this can be explained by smallholders’ inability to pay for costly chemical fertilizers and pesticides. However, rising foreign demand for specialty coffee is motivating some of the smaller growers to seek out specialized certification.

Coffee Production Drives Deforestation

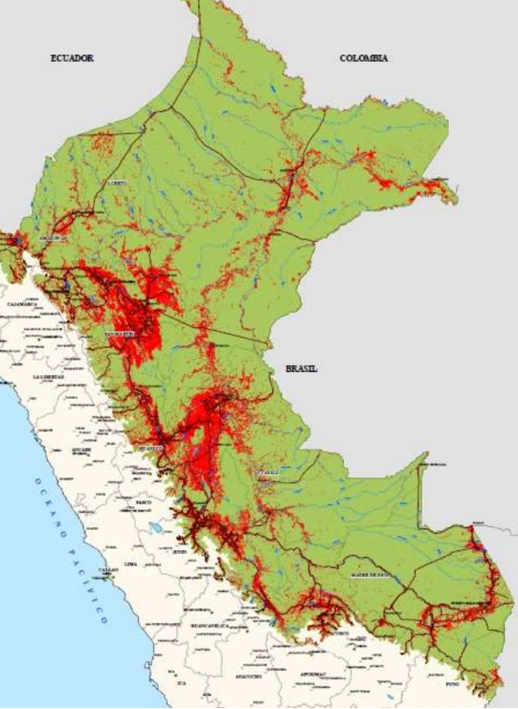

Figure 7: Deforestation in Peru, 2000 to 2014. Source: Ministry of the Environment, Peru.

As shown in Figure 7 (right), from 2000 to 2014, Peru’s deforestation was 1.32 million ha equaling 2 percent of Peru’s total forests. Half of Peru’s total land area or 69 million ha is forested. 92 percent of these forests are in the Amazon region. Peru estimated its deforestation in its 2016 report on its proposed Forest Reference Emission Level to the UNFCCC equaled 61 percent of the country’s total GHG emissions. Deforestation is Peru’s single largest source of GHG emissions, greater than GHG emissions from its transportation and energy sectors.

Peru’s coffee production deforestation is driven by:

- Migration to the Peruvian Amazon is a key factor in the expansion of the agricultural frontier and a key cause of deforestation. Deforesting and planting crops is a strategy to claim legal ownership over land as agricultural development is a condition for the formalization of land titles. At the same time, migrant workers tend to have little or no connection to the land, forests or ecosystems. New farmers often cultivate coffee in a manner that requires less shade, and therefore tend to cut down more trees.

- Road development increases the accessibility of remote areas. From 1999 to 2005, 75 percent of deforestation and degradation in the Amazon was located within 20 km of a road, a pattern that continues today with the road expansion.

- Local smallholders that increase their area of production through slash-and-burn and other forest clearing techniques add further pressures on the landscape. According to a 2015 study by Hivos, an international NGO, the expansion and intensification of coffee plantations is contributing to deforestation, particularly in the Region of San Martín. From 2000 to 2009, the opening of areas equal to half a hectare accounted for 75 percent of Peru’s national deforestation.

- The majority of the soils farmed in the Amazon are nutrient-poor and unsuited for permanent agricultural use in the absence of input use. This forces farmers to clear more forest. Increasingly, expansion and intensification to meet growing demand are also sought through the use of agricultural chemicals to augment production, while at the same time relying less on shade-grown practice.

- Peruvian analyses suggest that climate change will make some regions unsuitable for coffee production in 20 years’ time. Consequently, production moves up to higher elevations where temperatures are lower. These highlands are now more vulnerable to deforestation. Climate change and the creation of micro-climates also foster the occurrence of natural pests that specifically target coffee plants. From 2013 to 2014, 40 percent of Peru’s total coffee estate suffered an outbreak of the fungus Hemileia vastatrix which causes coffee leaf rust disease, leading to yield losses.

However, according to comments from the Global Coffee Platform, a global facilitator for sustainability in the coffee sector, the root cause of deforestation practices in the sector is economic adversity and poverty. Therefore, cutting off smallholders for non-compliance with Olam Peru’s sustainability standards would not address the fundamental issues. It is also noted that most smallholders are unaware of common sustainability standards and practices, according to comments from the Global Coffee Platform.

The cooperatives of coffee smallholders pay little attention to sustainability and deforestation issues yet, according to comments from Cooperativa Agraria Cafetalera Divisoria Peru. Training would be required as well as funding to make necessary investments to comply with sustainability standards.

In 2013, the Ministry of Agriculture and Irrigation introduced the National Plan for the Renovation of Coffee Farms, a 4-year program to renew 80,000 ha of coffee land. Meanwhile, local government agencies and NGOs focus on promoting organic coffee production to increase farmers’ income. According to development NGO Solidaridad, technical assistance from government institutions to smallholders has been cancelled 5 years ago. Only a few NGOs and companies continue to cooperate with smallholders to provide technical assistance. Comments from Cooperativa Agraria Cafetalera Divisoria Peru indicates this is rather geared towards improving productivity than addressing environmental impacts.

Olam’s Approach to Deforestation in Peru

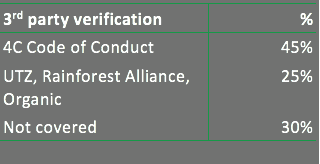

Figure 8: Third-Party Verification Totals, Coffee Exports, Peru. Source: Olam International.

Olam Peru aims to address environmental risks through farmer trainings and the roll-out of the Supplier Code. In instances where the company buys coffee via buying agents, which is the case for 95 percent of the coffee it sources in Peru, the agents need to sign its Supplier Code to ensure Olam’s standards are met. In case of non-compliance, these suppliers are not cut off. Olam states that it believes it is through continuous engagement with these suppliers that change and improvement takes place. Audit processes are currently still under development.

In 2016, 45 percent of the coffee volume sourced by Olam Peru was covered under the 4C Code of Conduct of the Global Coffee Platform, which is an entry-level standard for sustainable production, processing and trade of coffee. 25 percent is certified under UTZ, Rainforest Alliance or Organic programs. The UTZ and Rainforest Alliance certification systems announced their intention to merge in June 2017. Although these voluntary codes and certifications promote sustainability and address deforestation in protected areas, being certified is no guarantee for a deforestation-free supply chain. As shown in Figure 8 (above), the remaining 30 percent of Olam Peru’s coffee volume is not covered by third-party verification schemes. Olam requires all intermediaries to sign its Supplier Code. To achieve third-party certification, Olam Peru employs 11 agronomists and field staff who train smallholders on Good Agricultural Practices. Suppliers trade on a day to day basis, but Olam Peru also has a set of regular suppliers, according to comments by Olam.

The company provides smallholder training but does not suspend trading relations in case of non-compliance. Comments by Olam stated that the 1,000 Peruvian smallholders from whom it directly purchases coffee are all enrolled in Olam sustainability programs. Since 2015, Olam indicated that it has implemented two coffee farmer programs in Peru. Both are focused on reforestation. These programs reached 1,500 smallholder farmers in 2016, according to commentary by Olam. This represents 5 percent of the total volume that Olam Peru sources.

The company states that many smallholders lack education on environmental impacts from deforestation, water pollution or biodiversity loss. Olam Peru’s farmer training sessions use pictorial aids to help them understand this. Field staff also try to identify poor practices on their visits. It remains unclear what Olam Peru’s coffee supply chain smallholders know of its policies. Olam Peru says it is difficult to hold smallholders accountable to policies and codes with regards to deforestation since these smallholders are critically dependent on companies to buy their products. Therefore, Olam applies a training-based approach to improve agricultural practices so that they meet is OLC, instead of ceasing purchase agreements in cases of non-compliance.

Olam International Financial Analysis

As shown in Figure 9 (below), in 2016, Olam International adjusted revenue was USD 14.9 billion, a 7.5 percent increase year-over-year. Over the same period, the company’s EBITDA was USD 964 million, 0.5 percent increase year-over-year resulting in an EBITDA margin of 6.5 percent. In 2016, 37 percent of its revenue was generated in the Confectionery and Beverage Ingredients (cocoa and coffee) segment. Over the same period, this segment generated only 12 percent of the company’s total volume. The EBITDA margin of this segment was 5.2 percent, which was below the company’s average and therefore its EBITDA contribution to company’s total was above 30 percent.

Figure 9: Key Olam International Financial Data, 2012-2017E (Source: Bloomberg, Profundo).

| USD million | 2012 | 2013 | 2014 | 2015 | 2016 | 2017E |

| Net sales | 13,574 | 16,793 | 15,607 | 13,865 | 14,918 | 15,113 |

| EBITDA | 744 | 902 | 939 | 959 | 964 | 933 |

| EBITDA margin | 5.5% | 5.4% | 6.0% | 6.9% | 6.5% | 6.2% |

| Net debt | 5,032 | 5,720 | 6,035 | 7,163 | 7,967 | 8,346 |

| Net debt/EBITDA (X) | 6.8 | 6.3 | 6.4 | 7.5 | 8.3 | 8.9 |

Olam Peru Coffee Segment Generates 0.7 Percent Net Sales for Olam International

Olam’s Confectionery and Beverage Ingredients segment, whose 2016 net sales was USD 5.5 billion, is only active in cacao and coffee. In this segment, an estimated USD 100 million comes from coffee sourced from Peru based on USD 90 million revenues from exports and 10 percent domestic consumption. The estimated USD 100 million is 1.8 percent of the segment’s sales. As shown in Figure 10 (below), this means that Olam Peru’s coffee sales are a small contributor to Olam’s sales at 0.7 percent. Olam Peru’s EBITDA contribution is slightly lower at 0.5 percent.

Figure 10: Olam Peru’s Coffee Sales Estimates (Source: Profundo).

| USD million | 2016E | Assumptions |

| Based on Olam Peru’s coffee export value | 99.9 | USD 90 million export value in 2016 and 90 percent in sector Peru is exported |

| % of total net sales | 0.7% |

Does the Potential Impact on Shareholders Exceed the Financial Benefit from Deforestation?

Coffee has been identified as a major driver of deforestation in the Peruvian Amazon. No direct link between Olam Peru and deforestation in the Peruvian coffee sector could be identified though. There is a low likelihood of an imminent loss of customers and financiers. Therefore, the negative financial impacts on sales and EBITDA might be limited and only come from reputational risk for the sector as a whole. As we have no exact data on the size of deforestation by Olam Peru’s (independent) suppliers specifically, we cannot calculate the financial benefit that Olam has from coffee sourced from deforested sites. We conclude that a confrontation of the potential financial losses from reputation versus financial benefits from deforested area is not possible.

There is increased scrutiny by forest campaigns of Olam’s role in coffee-related deforestation. In a worst-case scenario in which Olam Peru would lose all its Peruvian coffee sales due to broad action to tackle deforestation in the sector and a subsequent reputation damage to the sector. For example, a 100 percent boycott could cost Olam 0.7 percent in net sales and 0.5 percent in EBITDA. This equals to a 0.5 percent discounted cash flow (DCF) of future operations and a negative 0.5 percent in enterprise value.

To calculate the impact of deforestation on Olam’s equity value, its net debt and preference shares need to be deducted from its enterprise value. As shown in Figure 11 (below), given that Olam is financed for 70 percent by debt, the impact on the equity value is relatively high, 1.6 percent (0.5 percent / 30 percent).

Figure 11: Olam International’s Enterprise Value, July 17, 2017 (Source: Bloomberg, Profundo).

| USD million | July 17, 2017 | % |

| Enterprise Value | $12,951 | 100.0% |

| Net debt, preference shares and other | $9,031 | 69.7% |

| Market Capitalization | $3,920 | 30.3% |

For Olam, this 1.6 percent equals USD 60 million equity value – 1.5 percent its July 28, 2017 market cap. If 25 percent of Olam Peru’s coffee production has taken place on deforested area, then USD 25 million of Olam Peru coffee sales would have come from deforested areas. At a 5 percent EBITDA margin, this equals an EBITDA of USD 1 million and a DCF value of USD 10 million. This means that the financial benefit from contested area at USD 10 million is below its USD 60 million potential loss of equity value due to loss of revenue and EBITDA related to reputational risk.

Institutional Shareholders might start engagement

For a further analysis, we focus on the financing structure of Olam International in order to understand if investors with a deforestation policy might act.

As mentioned above (see table in introduction) and in Figure 12 (below), Temasek, (part of) a sovereign wealth fund owned by the Government of Singapore, is the controlling shareholder with 50.3 percent of the shares. Another key shareholder with 20 percent is Mitsubishi Corporation. Next to several local shareholders, Norges Bank and the State of California have stakes that are less than one percent. In particular, the smaller shareholders from Europe and North America have policies on deforestation and might start engagement.

Figure 12: Olam International’s Gross Debt Composition, 2016 (Source: Annual Report Olam 2016, Profundo).

| SGD million | 2015 | 2016 | 2015% | 2016% |

| Bank | 8,558 | 9,486 | 70% | 69% |

| Bonds | 2,947 | 3,704 | 24% | 27% |

| Other | 789 | 481 | 6% | 4% |

| Total | 12,294 | 13,671 | 100% | 100% |

Olam is Highly Levered

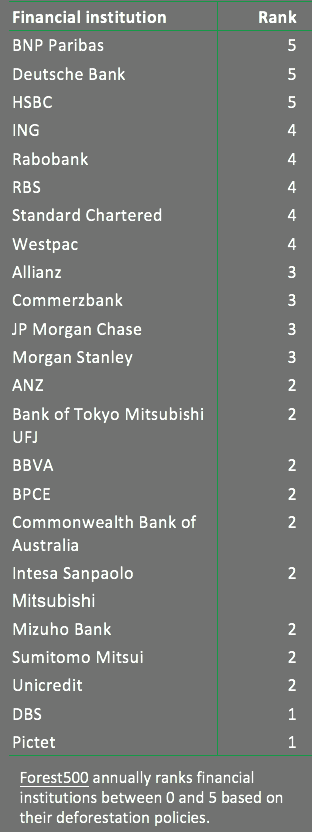

Figure 13: Financial Institution’s Forest500 Score.

As of July 17, 2017, its USD 13 billion enterprise value, 70 percent existed of net debt and preference shares, and only 30 percent was equity value. As shown in Figure 9 (above), the company’s financing is dependent on debt. From 2012 to 2017E, its net debt/EBITDA ratio increased from 6.8X to 8.9X. The interest coverage (operating income divided by interest costs) is low at 2.2x.Olam’s debt is 70 percent bank debt. 25 percent is from bonds while the rest is from other instruments.

For its bank debt, Olam has access to a wide-range of banks from Europe, US, Japan and Asia.

- Olam arranged a USD 1 billion loan facility to fund its USD 1.3 billion December 2014 purchase of ADM’s cacao business. The syndicate included: ANZ, Banco Bilbao Vizcaya Argentaria SA’s Singapore branch, The Bank of Nova Scotia Asia, The Bank of Tokyo-Mitsubishi UFJ, BNP Paribas, Commerzbank AG, Commonwealth Bank of Australia, Rabobank, DBS Bank, HSBC, Intesa Sanpaolo SpA, JPMorgan Chase Bank, The Korea Development Bank, Mizuho Bank, National Australia Bank Limited, Natixis, Standard Chartered Bank, Sumitomo Mitsui Banking Corporation and Westpac Banking Corporation.

- In 2014, Olam concluded an AUD 350 million 5-year facility from a syndicate including HSBC, ING Bank, DBS banks and several Australian banks.

- In 2014, Olam was able to arrange a large USD 2,475 million facility up to 3-years with a syndicate including many of the banks mentioned above.

As shown in Figure 13 (right), most of these banks have deforestation policies in place and could engage with Olam to redefine its policies on deforestation for coffee.

The Olam International bonds are held by various investment funds and banks in Europe and in the US. Institutions like Allianz, Deutsche Bank, Pictet, RBS, Morgan Stanley, JP Morgan and Unicredit hold millions USD in these bonds. Also, several of these actors have deforestation policies in place.

Financial Risk Assessment: Conclusions

- Olam’s Confectionary and Beverage Ingredient segment contributed respectively 37 percent and 30 percent to its 2016 net sales and adjusted EBITDA. Olam should focus on managing the reputational risk of this important segment.

- Olam Peru’s coffee business generated about USD 100 million in sales in 2016, which is 2 percent of the Confectionery and Beverage segment and 0.7 percent of Olam’s sales. As the Confectionary and Beverage segment has a relatively low margin, its estimated EBITDA contribution from Peruvian coffee is 0.5 percent.

- Olam Peru’s deforestation risk will probably not lead to a loss of clients. However, if Olam Peru would lose all its Peruvian coffee sales this equals a negative 0.5 percent impact on their enterprise value. As Olam International is leveraged with a high level of debt, this would trigger a negative impact of 1.6 percent on the equity valuation. This worst case USD 60 million negative impact from a loss of clients would substantially exceed the estimated financials benefits of USD 10 million from the extra coffee sales from deforested land.

- Minority shareholders might be successful when engaging with Olam. As the Confectionery and Beverage segment is important to Olam, the company and its dominant shareholders could be willing to adjust their Peruvian policy.

- Olam has a high net debt/EBITDA. Of its gross debt, 70 percent is from bank credits and 25 percent from bonds. In credits, leading banks are in the syndicates. In bonds, leading asset managers hold stakes. As a majority of banks/investors have high scores on their deforestation policies, we should expect engagement about the Peruvian deforestation related to coffee production.