Summary

- Financial regulators should address environmental and human rights risks in economic sectors driving deforestation.

- Financial regulators should address environmental and human rights risks in economic sectors driving deforestation.

- Binding regulation may be more effective than voluntary initiatives.

- Chinese, Brazilian, and Bangladeshi experiences may be useful for regulators.

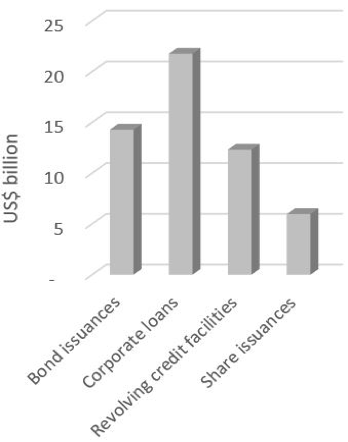

As published by Chain Reaction Research and written by Barbara Kuepper, Profundo, Tim Steinweg, Aidenvironment, and Gabriel Thoumi, CFA, FRM, Climate Advisers, greenhouse gas (GHG) emissions from tropical deforestation are among the key contributing factors to climate change, contributing around 10 percent of total GHG emissions based on 2010 figures. Natural forests are under threat of deforestation and forest degradation, leading to significant carbon emissions, loss of biodiversity and livelihoods of indigenous communities, and other adverse sustainability impacts. Such conversions are often driven by the expansion of agricultural commodity production in tropical countries. Noteworthy examples include the Chain Reaction Research focus countries, Brazil, Colombia, Ecuador, Indonesia, Peru, Democratic Republic of the Congo, and Liberia. As shown in Figure 1 (below), 2012 to 2016, commercial banks financed over USD 50 billion to support tropical timber, pulp & paper, palm oil, and rubber expansion in SE Asia.

The Financial Stability Board Task Force on Climate-Related Financial Disclosures (TCFD) published June 29, 2017 their final report with key recommendations for the Agriculture, Food, and Forest Products Group.

Figure 1: Banks’ financing of SE Asian forest-risk sectors, 2012 to 2016. Includes palm oil, pulp & paper, rubber, and timber. Source: Forestsandfinance.org

As stated by the UNEP Finance Initiative, international financial banking regulation generally does not recognize environmental and social risks including those from deforestation as material risks to financial stability. The Basel Capital Accord III has not yet addressed deforestation risk. Yet the sector is changing: over the past ten years sustainable banking initiatives by national policymakers and regulators have emerged. These initiatives can support the commercial banking sector in mitigating deforestation risk while enabling sustainable economic development.

Findings and Recommendations

- Binding regulation may be more effective than voluntary initiatives. Sustainable banking initiatives are generally not older than a decade. Previously, the field was led by voluntary and industry-driven initiatives. On their own, these non-binding guidelines and recommendations may not be sufficient to mitigate deforestation risk. Binding regulation is more likely to be effective, especially when it is accompanied by detailed implementation guidance and standardized disclosure formats, as in Bangladesh and China.

- Financial regulators should address environmental and human rights risks in economic sectors driving deforestation. Requirements can prevent further loss of tropical forests and related impacts on biodiversity, climate and livelihoods. Experience from Brazil shows that initial sector-targeted banking regulations can be efficient in reducing deforestation.

- Financial institutions should be obligated to mitigate deforestation risks linked to the activities they finance. Assessing their own risks arising from their exposure to these industries could help to contain damaging practices like rampant deforestation, land grabbing and human rights breaches.

- Experiences on binding regulation from Bangladesh, Brazil, and China may be useful to other regulators as indicators for what may work. While it is too early to make generalizing conclusions on the effectiveness of different sustainable banking measures and frameworks, there are some encouraging indications from Brazil, Bangladesh and China.

Framework for Sustainable Banking Initiatives: Sustainable Banking Definition

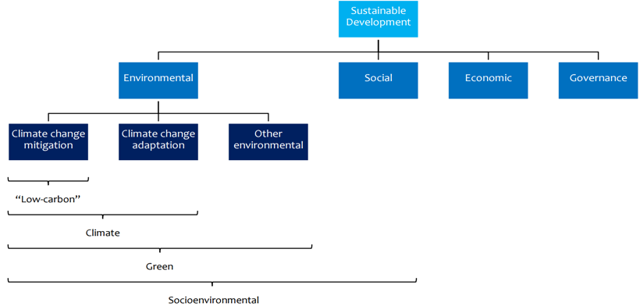

As shown in Figure 2 (below), the concept of sustainable finance contains a group of overlapping terms that includes green finance and climate finance. A broad definition of sustainable banking includes all aspects of sustainable development: environmental, social, economic, and government. In this paper, the term ‘sustainable finance / banking’ is used in this comprehensive sense as illustrated in Figure 2. Deforestation as a major contributor to climate change as well as other detrimental effects is covered by the broader socio-environmental aspects.

Figure 2: Dimensions of sustainability in financial decision-making. Source: UNEP (2016).

Sustainable Banking Distinctions and Categories

Various initiatives to improve banks sustainability must be distinguished both in their institutional and technical features. Institutional differences include:

- Their nature: are they voluntary or binding?

- Which actor or organization proposes or mandates them: is a particular sustainable banking framework promoted by statute law, a country’s central bank or banking supervisor or by the financial sector itself (the country’s banking association)?

- Which financial institutions are covered by it: does the framework in question only cover banks or also other financial actors?

Technical differences arise because regulators and supervisors have many tools to assess sustainability of a bank’s organizational structures and operations. Each framework uses different tools and target distinct aspects of a bank’s operations. For example:

- Minimum capital requirements including regulatory capital

- Internal risk management

- Governance

- Disclosure

- Sustainable (or green) lending

- Sustainable (or green) financial products for retail investors

- Net interest margin, duration, and banks’ refinancing operations

- Physical operations

Numbers one to four in the list above belong to prudential and supervisory regulation. The purpose of this is to make sure that banks do not take on too much risk because bank failures do not just endanger the financial system, but entire economies. Apart from prudential and supervisory regulation, there is also monetary policy. This affects how commercial banks refinance themselves by borrowing from central banks and correspondent banks. The latter can use monetary policy to create incentives for commercial banks to lend more to sustainable industries or businesses by making cheaper refinancing options available for banks that lend sustainably, and/or by accepting assets such as green bonds as collateral for central bank borrowing and separately as pledged collateral to ensure public deposit accounts against default risk by the bank holding company who manages these deposits.

Risk management and sustainable lending/financial products are the two broad fields into which most of the aspects of banking activity and regulation can be grouped. Sustainable banking activities and regulation can be broadly grouped into the fields of risk management and sustainable lending/financial products.

- Risk Management: Risk management primarily refers to the processes by which banks assess and monitor the credit risk associated with individual loans or entire loan portfolios, but also with other activities such as securities underwriting. Most sustainable banking initiatives focus on the risk management aspect of banking by suggesting, or requiring, banks to incorporate environmental and social risks in lending decisions in order to avoid or mitigate financial losses, reputational risk, or environment or social damage caused by projects banks finance. This is based on what could be called an avoidance logic, the idea being that banks should be forced or given incentives to avoid exposure to unsustainable projects, businesses or industries.

- Sustainable lending / financial products: Sustainable banking initiatives try to encourage sustainable lending and the sale of sustainable financial products, going beyond an avoidance logic. Rather than merely avoiding the financing of undesirable activities, banks are being encouraged or required to make capital flow to industries whose activities are desirable from a sustainability point of view. They can do so through their own lending or through the investment products they sell to their retail customers.

Regulatory Pioneers of Sustainable Banking

Figures 6 and 7 (below) in the appendix include a comprehensive list of sustainable banking initiatives that have been put into practice. Profiled below, Bangladesh, Brazil and China are three leading pioneers of sustainable banking regulation and implementation.

Bangladesh

Bangladesh has pioneered a systematic and comprehensive approach to sustainable banking. Bangladesh Bank, the country’s central bank and financial sector regulator and supervisor, is the key factor behind the country’s sustainable finance initiatives. It combines monetary policy and regulatory tools to make banks avoid unsustainable lending and increase their lending to sustainable businesses and industries. It has devised three policies: a green banking and finance framework, a monetary policy facility for cheaper loan refinancing and a green lending target.

- In 2011, Bangladesh Bank published its Environmental Risk Management Guidelines for banks and financial institutions. It defines the concepts of environmental risks and environmental risk management, provides detailed technical guidance, including sector-specific Environmental Due Diligence Checklists and describe the organizational requirements for effective environmental risk management. The Policy Guidelines for Green Banking prescribed a phased introduction of green banking practices over three years (2011 to 2013), covering many different aspects of banks’ day-to-day business operations, from governance and disclosure of green banking activities to eco-efficient buildings and employee training.

- Monetary policy incentives, specifically cheaper and easier refinancing, are used to direct commercial bank lending to priority areas of the economy including agriculture, the garment sector and small enterprises. In 2009, Bangladesh Bank used its fund for solar energy, biogas and waste treatment plants to create a refinancing facility for lending to renewable energy and other environmentally friendly industries. USD 25 million (BDT 2 billion) was made available to support bank lending to green industries. Initially restricted to only five, the list of industries and activities that qualify as green has been expanded to 50 different activities grouped under eleven categories. This includes renewable energy, solid and liquid waste management or recycling.

- The 2014 Annual Target for Direct Green Finance decreed that a minimum of five percent of total commercial bank lending from January 2016 must go towards directly financing green industries and activities. Non-bank financial institutions are also covered. In their case the five percent target refers to their investment portfolio.

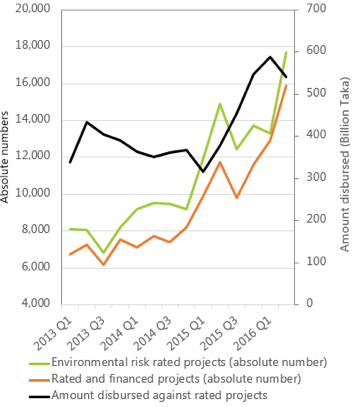

Figure 3: Number of / amounts disbursed to environmentally risk-rated loan applications (2013 to 2016).

Bangladesh Bank required banks to report to it on their progress in implementing the above program on a quarterly basis and to put up-to-date information on their green banking activities on their websites. It also introduced an incentive element by granting preferential treatment to compliant banks, such as favorable mention on the Bangladesh Bank website or having this fact taken into consideration when applying for permission to open new bank branches. All banks have now created green banking units and policies, and the number of loan applications that are screened for environmental risks increases continuously. ‘Green’ loans constitute a very small, but increasing, share of banks’ total loan portfolios.

Bangladesh: Results

At the institutional level, the green banking framework appears to be successful. As of June 2016, all of the 56 banks under the regulatory purview of Bangladesh Bank have established green banking units and defined green banking policies. Foreign banks with operations in Bangladesh are also under the purview of Bangladesh Bank. This includes Standard Chartered and Citibank. These policies “tend to be a direct replication of the Bangladesh Bank guidance”.

The Bangladesh Bank also asks commercial banks to carry out environmental due diligence on individual projects whenever loan applications are made to ecologically sensitive industries. The number of projects that have undergone environmental risk rating has risen steadily over the past three to four years, as has the number of rated projects that received financing. In Figure 3 (above), in the last twelve months, the amount disbursed to these projects has also increased. Additional research is required to ascertain whether these environmental risk ratings, which are based on the described avoidance logic, have mitigated socially and/or ecologically harmful activities.

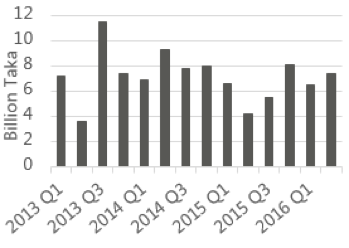

As shown in Figure 4 (below), from 2013 to Q1 2016, the amounts disbursed directly to environmentally important industries have fluctuated, but not grown. The percentage share of financing to sectors such as renewable energy or green construction in total funded loan disbursements by commercial banks has remained at or around 0.5 percent over the last 24 months (the time for which this data is available), below Bangladesh Bank’s 5 percent target.

Figure 4: Direct green finance disbursement by banks, 2013 to 2016. Source: Sustainable Finance Department at Bangladesh Bank.

Indirect green finance, which refers to financing for projects with end-of-pipe effluent treatment, is much larger than direct green finance disbursements. In FY2015, banks disbursed a total of USD 5.6 billion (BDT 442.1 billion) in green finance. Indirect finance was the majority at 94 percent.

|

Figure 5: Disbursements Green Refinancing Scheme Source: Sustainable Finance Department at Bangladesh Bank (2013 to 2016).

As shown in Figure 5 (above), disbursements suggest that Bangladesh Bank’s green refinancing facility has grown. However, the key question is whether this growth is because it is a subsidy that makes borrowing to environmentally friendly industries temporarily more profitable or less risky for banks, or whether it has the potential to shift lending patterns in the long run by establishing a new segment in financial markets. The latter is the goal of the Bangladesh Bank. They want to build a business case for sustainable lending. This raises the question whether the banks’ green lending would continue to grow or decrease if the refinancing facilities were phased out.

Brazil

Brazil Private Sector Banks

Brazil’s Banco Central do Brasil (BCB), like Bangladesh Bank, is responsible for monetary policy authority and financial sector regulation and supervision. It has played a crucial role in advancing the sustainable finance agenda in Brazil. Unlike Bangladesh Bank, Banco Central do Brasil does not use monetary policy to promote sustainable banking practices among commercial banks. However, Banco Central do Brasil has used the Basel III framework as a vehicle for prescribing sustainable banking practices among commercial banks.

Sustainable banking regulation in Brazil began as a series of industry-specific green banking regulations related to the agriculture commodity sector. In 2008, Resolution 3,545 made the granting of subsidized rural credit to agricultural activities in the Amazon Biome conditional upon the provision of proof of compliance with legal and environmental requirements. In 2009, Resolution 3,813 imposed certain conditions on the granting of credit to the cultivation and processing of sugarcane. In 2010, Resolution 3,876 prohibited lending to entities or individuals associated with the employment of slave labor.

In 2011, the BCB began implementing sustainability criteria into the day-to-day practices of commercial banks through Circular 3,547. This provided banks with guidance on how to implement the Internal Capital Adequacy Assessment Process in Pillar 2 of Basel III. This is the process through which banks assess the level of risk their lending and other investments expose them to so that they can determine the amount of equity capital needed to support their business activities. Article 1 requires each bank to “demonstrate […] how it evaluates the risk arising from exposure to social and environmental damage caused by its activities” when assessing how much capital it needs to cover a range of operational and financial risks.

Specifically, Article 1 requires:

1. An evaluation and calculation of the institution’s capital needs to cover

- credit risk,

- market risk,

- operational risk,

- interest rate risk in the banking book,

- counterparty credit risk,

- concentration risk.

2. An assessment of capital needs to cover other relevant risks to which the institution is exposed, considering, at a minimum

- liquidity risk,

- strategic risk,

- reputational risk.

3. Stress testing and the assessment of its impact on capital.

4. Description of the methods used to estimate capital needs and the stress tests referred to in item 3.

In 2014, Resolution 4,327 required financial institutions to have a Social and Environmental Responsibility Policy (PRSA). It provides implementation guidelines on social and ecological risk management. Specifically, it requires:

- Suitable governance structures: the governance body should monitor implementation of and compliance with the PRSA and evaluate the effectiveness of the actions. It should check the adequacy of managing social and environmental risk established in the PRSA. It should identify any shortcomings in the implementation of actions.

- A system for social and ecological risk management: social and environmental risks are defined as the possibility of financial losses resulting from environmental damage. Such risks should be identified and systems and procedures should be implemented that make it possible to identify, classify, assess, monitor, mitigate, and control the environmental risk present in the activities and the operations of the institution, including prior assessment of the potential negative social and environmental impacts of new types of products and services, including reputational risk.

- It also required a plan for implementing the PRSA by February 2015 for financial institutions subject to the ICAAP, and by July 2015 for all other financial institutions.

Brazil: Public and Development Banks

Brazil’s Banco Nacional de Desenvolvimento Econômico e Social (BNDES) is the main institution driving finance to socially and ecologically desirable activities and industries in Brazil. The BCB restricts its supervisory role to private banking practices focusing on influencing risk management procedures or imposing conditions on lending to environmentally sensitive activities. It applies an avoidance logic with regard to private banks, unlike the Bangladesh Bank. Starting in 1995 with the voluntary Green Protocol, revised in 2008, state-owned and development banks have played an important role in advancing sustainable banking. The protocol sets out broad principles for socially and environmentally responsible banking. It was initiated by the Ministry of the Environment, BNDES, and five state-owned banks.

The National Fund for Climate Change (Fundo Nacional sobre Mudança do Clima (FNMC)) also involves BNDES. Established by federal law in 2009 and administered by the Ministry of the Environment, FNMC uses public funds from a variety of sources to finance projects or studies that aim to mitigate or adapt to climate change. It disburses non-refundable grants and makes refundable loans at low interest rates. The latter are administered by BNDES. BNDES also finances the Programa ABC, established in 2010 to fund investments that reduce greenhouse gas emissions in the agricultural sector.

Brazilian Lender Liability: Law and the Environment in Brazil

Brazilian law has established the principle lender environmental liability. Brazil’s legal system allows non-affected parties to file civil lawsuits against those who are responsible for environmental damage. There have been several lawsuits over the past ten to fifteen years that have made environmental damage costly to those directly responsible. They’ve also established the principle of lender environmental liability on the grounds that the activities that caused damage could not have taken place without financing. Lenders can now be held liable for the damages caused by the activities of borrowers.

For example, in a 2006 lawsuit against the mining company Companhia Mineira de Metais, Brazil’s Superior Tribunal de Justiça – Brazil’s superior court of justice – decided that the financing institution was jointly liable with the other defendants for environmental damages, provided that there was proof that it disbursed money to the mining company despite being aware of the existence or imminent danger of such damages.

These developments are not directly related to the sustainable banking initiatives discussed in this report because they do not involve banking regulators and supervisors using their prudential or monetary policy tools. However, establishing lender liability as a normal part of the operations risk management in which banks do business strengthens regulatory frameworks that require banks to assess the financial risk to them from exposure to environmentally sensitive businesses and industries.

Brazil: Results

Unlike in Bangladesh, in Brazil there is no centralized and standardized gathering of data related to sustainable banking. Greater systematic data collection by the banking supervisors and more research may improve analysis of Brazil’s sustainable banking framework.

The BCB’s early green banking regulations were not yet concerned with incorporating attention to sustainability in a broad sense into banking operations but were specific to a geography or industry sector. Resolution 3,813 (2009) and 3,876 (2010) were targeted at lending to specific activities, such as sugar cane cultivation, or particular aspects of general business activity, such as the employment of slave-like labor. Resolution 3,545 (2008) focused on the Amazon Biome.

In the years following its adoption, Resolution 3,545 had a positive effect on reducing deforestation in the Amazon. It made the granting of rural credit contingent upon the ability of prospective borrowers to demonstrate compliance with environmental regulations. Rural credit is a much-used type of government-subsidized loans to agricultural producers. Does Credit Affect Deforestation? Evidence from a Rural Credit Policy in the Brazilian Amazon by Assunção, Gandour, Rocha and Rocha shows that Resolution 3,545 had the effect of reducing the flow of rural credit in the Amazon and that this significantly reduced deforestation. Their modeling suggests that about 2,800 square kilometers of forest would have been cleared from 2008 through 2011 had Resolution 3,545 not been passed.

Similarly, Climate Policy Initiative (CPI)’s 2013 analysis stated:

In 2008, Brazil introduced Resolution 3,545. The law tied credit, an important source of financing for rural producers, to proof of compliance with environmental regulations. Climate Policy Initiative’s study estimates that approximately BRL 2.9 billion (USD 1.4 billion) in rural credit was not contracted in the 2008 through 2011 period due to restrictions imposed by Resolution 3,545. This reduction in credit prevented over 2,700 km2 of forest area from being cleared, which represents a 15% decrease in deforestation during the period.

The Assunção study also shows that this result depended on two other conditions beyond the control of regulators:

- Are producers able to obtain alternative financing sources when the flow of subsidized rural credit is reduced by the Resolution 3,545, e.g. loans at normal market interest rates? Availability of alternative financing sources would allow producers to maintain activity levels, including deforestation.

- Which production technologies are available to agricultural producers? If, for instance, rural credit is used not to expand the area used for agricultural production but to invest in productivity-enhancing technologies, a reduction in rural credit might leave deforestation rates unchanged.

Differentiating between crop production and cattle farming, the Assunção study found that the reduction in the flow of rural credit did not significantly reduce deforestation activities of the crop sector, but that it did reduce deforestation activities in the cattle sector. It appears that the latter is more credit constrained than the former. Moreover, the absence of options for productivity-enhancing investment in the cattle sector means that the only option for expansion is to increase grazing area. Under these conditions, tightening the credit supply can have a direct effect on the activity levels and thus reduce deforestation.

In the last two years, deforestation rates in the Brazilian Amazon Biome have been found to increase again. The causation is not yet clear, the impacts of the resolution cannot be singled out.

China

The China Banking Regulatory Commission (CBRC) drives China’s sustainable banking initiatives. While it is an independent state agency, it follows the political direction determined by the Chinese Communist Party. The Chinese Communist Party and CBRC share staff.

Green Banking Framework

Like Brazil, China green banking framework includes management of social and environmental risks, green lending criteria and environmental requirements regarding each banks’ operations. The green banking framework does not use monetary policy or mandatory credit quotas. The framework’s development started in the 1990s. In 2007, its first implementable guidance, the Green Credit Policy, was launched. In 2012, the Green Credit Policy was superseded by the Green Credit Guidelines issued by the CBRC. These Guidelines provided more detailed guidance than the Green Credit Policy. The Guidelines specify:

- Boards and senior managers of banks take the lead in developing and implementing green credit concepts and objectives at the level of individual institutions (Chapter 2).

- Banks create environmental and social risk management systems (Chapter 3).

- Banks can engage in green credit innovation (Article 12).

- Banks can improve their ecological footprint of their buildings and operations (Article 13).

- Banks can strengthen due diligence before granting credit (Article 15).

- Banks can monitor and promote borrowers’ compliance with current rules and clients’ environmental and social performance. Granting loans can be made conditional upon such compliance. Banks can employ punitive measures against non-compliant borrowers. (Articles 16 to 19)

- Banks are required to institute internal control mechanisms regarding their green lending business and disclose relevant policies and data, including their exposure to environmental and social risks (Chapter 5).

These Guidelines require banks to take an active role in supervising, monitoring, measuring, and reporting certain environmental and social risks within the loans they issue before, during and after the granting of a loan. The Green Credit Guidelines refer to environmental and social risks that banks must be aware of.

The Guidelines are supported by additional standardized assessment and reporting formats issued by the CBRC from 2013 and 2015. In 2013, the CBRC issued instructions on the submission of green credit statistics by individual banks. These instructions include classification of green loans into twelve categories that are subdivided further. It also includes instructions on how to calculate environmental benefits from green lending as well as a standardized reporting format. The 2014 Key Performance Indicators of Green Credit Implementation provide a checklist that banks must use to assess and report how far they have come in implementing the requirements set out in the Green Credit Guidelines. The 2015 Energy Efficiency Credit Guidelines, jointly issued by CBRC and the National Development and Reform Commission, provide banks with definitions of energy efficiency lending as well as operational guidance.

China: Results

Not enough data is currently available to assess the success of China’s green banking framework. According to a joint report by the International Finance Corporation and the Sustainable Banking Network, “the majority of the top 21 banks have adopted E&S risk management practices at different levels”. There are also reports that lending to environmentally desirable activities has increased over the last decade, both in absolute terms and as a percentage of banks’ loan portfolio, and that such lending has grown at a faster rate than overall lending. However, it is currently not possible to assess whether this growth is causally related to the Green Credit Guidelines, or whether commercial banks are meeting market demand for loans that would have taken place anyway.

Greening China’s Financial System, published in 2015, cast doubt on the effectiveness of China’s policies in their present form. The authors point out that the supply of capital from private sources of investment finance, including commercial loans, is inadequate to meet the demand for green fixed capital investments. Such lending is often commercially unattractive and may be challenging for banks due to lack of guidance or experience with this type of lending.

Conclusions

- Encouraging indicators of sustainable banking initiatives include a reduction in deforestation in Brazil and the increase in loans subject to environmental risk rating in Bangladesh. Regulatory sustainable banking frameworks and guidelines that are detailed and sophisticated enough to be implementable are relatively recent. The three case studies of Bangladesh, Brazil, and China began implementation within the last half a decade. Further research is necessary to confirm their effectiveness. There are also challenges, such as making it interesting for Chinese private banks to provide loans to green projects.

- Banking regulators introducing sustainable banking frameworks in their own countries are unable to copy best practices from elsewhere. They need to pick from existing tools and create new tools relevant to their respective contexts. National contexts may depend on specific financial systems, economic structures, and political and institutional environments.

- More innovation is required to shift financial flows via sustainable banking frameworks away destructive activities. Voluntary commitments in the financial industry and other sectors may not be rigorous enough to shift capital. Regulation may be more effective at shifting capital, when accompanied by implementation guidance and standardized disclosure formats, as in Bangladesh and China.

- Brazil’s Resolution 3,545 could inform forest-rich countries’ approaches to sustainable banking. Beyond sustainable banking initiatives, targeted regulatory approaches have shown positive results. For example, Resolution 3,545 helped to reduce deforestation in the Brazilian Amazon. However, this success also depended on specific local conditions. Regulators in other countries could access whether a similar policy might work in their countries, given their specific local conditions.

Forest-rich countries such as Liberia and Democratic Republic of the Congo may want to join Brazil, Colombia, Ecuador, and Peru and participate in the International Finance Corporation’s Sustainable Banking Network (SBN). Joining the SBN offers regulators and officials a forum to share experiences and learn from other members.

Appendix: Overview of Existing Sustainable Banking Initiatives

Figure 6 (below) presents existing sustainable banking initiative frameworks developed by an official regulatory or supervisory body. Figure 7 (below) shows industry-led, voluntary sustainable banking initiative frameworks. Not all regulatory frameworks for sustainable banking in Figure 1 may be technically mandatory. For example, the Chinese Green Credit Guidelines, while voluntary, are de facto mandatory and are supported by detailed guidelines. Where applicable and available, Figures 6 and 7 include information about whether a) risk management (internal risk management; market, credit, operational risks; regulatory capital; bank governance) or b) sustainable lending / financial products are covered by the framework.

Not included in the Figures 6 and 7 is the “Roadmap for Sustainable Finance” in Indonesia because it has not yet led to implementable rules or guidelines for banks.

Figures 6 and 7 also do not included data from the “Dutch Banking Sector Agreement on international responsible business conduct regarding human rights”. This agreement was signed in November 2016 between the Dutch government, the Dutch Banking Association (NBV), Dutch trade unions and Dutch non-governmental organizations. Through this agreement, 13 Dutch banks, including ABN AMRO, ING Group and Rabobank, confirm their responsibility to respect human rights, including labor rights, in their daily business practices.

Note: Also, not included is the G20 Green Finance Study Group (GFSG), which the Bank of England co-chairs with the People’s Bank of China, and the UN Environment (UNEP) Inquiry as secretariat. The Study Group published its synthesis report in September 2016. Recognizing the need to significantly scale up green finance, the GFSG aims to identify institutional and market barriers to achieving this goal. Based on country experiences, options will be developed to enhance the ability of the financial system to mobilize private capital for green investment. During 2017, the GFSG aims to advance the integration of environmental risk analysis into the financial system, as well as identifying publicly available environmental data that can be applied within risk analysis models.

| Framework | Regulation and Scope | Risk Management | Lending and Financial Products |

| Bangladesh | |||

| BRPD Circular No. 1: Environmental Risk Management Guidelines (2011)Aims to encourage and enable financial institutions to take environmental risks into account in credit risk assessment. |

Central Bank regulation: Applicable to banks and non-bank financial institutions. |

X | |

| BRPD Circular No. 2: Policy Guidelines for Green Banking (2011)Guidelines for moving towards green banking practices, e.g. in credit appraisal process, reporting, banks’ own operations, lending etc. |

Central Bank regulation: Initially banks only; extended to non-bank financial institutions 2013 (GBCSRD Circular No. 4). |

X | X |

| Cheaper refinancing for commercial loans to ‘priority areas’, such as agriculture or renewable energy. E.g. GBCSRD Circular No. 2: Refinancing Scheme for Renewable Energy and Green Financing (2013). | Central Bank: Monetary policy incentives for commercial banks. |

X | |

| GBCSRD Circular No. 4: Annual Target for Direct Green Finance (2014): Mandatory 5% allocation of loan/investment portfolio to green finance. |

Central Bank regulation Applicable to banks and non-bank financial institutions. |

X | |

| Brazil | |||

| Resolution No. 3545 (2008):

Makes rural credit to agricultural producers in the Amazon contingent on compliance with environmental regulation. |

Central Bank regulations:

Applicable to financial institutions / other entities authorized by the Central Bank. |

X | |

| Resolution No. 3813 (2009):

Conditions for loans for sugar cane cultivation |

X | ||

| Resolution No. 3876 (2010):

Prohibits granting loans to entities or individuals associated with employment of slave-like labor. |

X | ||

| Circular No. 3547 (2011):

Internal Capital Adequacy and Assessment Process (ICAAP, Pillar 2 of Basel III). Banks to demonstrate how they take social and environmental risks into account in calculating risk exposure; also requires disclosure of ICAAP to central bank. |

X | ||

| Resolution No. 4327 (2014):

Guidelines on how to implement Social and Environmental Responsibility Policies. Includes guidance on social and ecological risk management. |

X | ||

| China | |||

| Green Credit Guidelines, CBRC (2012), No. 4:

Operational guidance to implement green banking in environmental and social risk management, green lending, and greening banks’ own operations. |

China Banking Regulatory Commission:

Applicable to banks. |

X | X |

| Green Credit Statistics, CBRC General Office (2013) No. 185:

Green loans classified into 12 categories with sub-categories. Includes tool for banks to calculate environmental benefits from green lending. Standardized format for green credit reporting. |

X | ||

| Green Key Performance Indicators (2014):

Banks to assess themselves against these indicators and report to CBRC. |

China Banking Regulatory Commission:

Applicable to banks. |

X | X |

| Energy Efficiency Credit Guidelines, CBRC (2015) No. 2: Defines “energy efficiency credit” and applicable areas; operational guidance to banks extending such credit. Banks called on to increase lending to energy efficiency projects and develop innovative lending products, but no targets formulated. |

X | ||

| India | |||

| Priority Sector Lending (PLS) targets (2015):

Renewable energy included in PSL categories; sets 40% target of bank credit that must go to priority areas. |

Reserve Bank of India:

Applicable to commercial banks. |

X | |

| Lebanon | |||

| Circular No. 84, Decision No. 7835, Reserve Requirements:

Cheaper funding to commercial banks for lending to environmentally sustainable projects. |

Central Bank of Lebanon:

Monetary policy incentives for commercial banks. |

X | |

| Peru | |||

| Resolution SBS No. 1928-2015 for Social and Environmental Risk Management (2015):

Flanked by guidance on “Role of Enhanced Due Diligence in the Regulation of Socioenvironmental Risk Management for Financial Firms.”. |

Superintendency of Banking, Insurance and Private Pension Fund Administrators (SBS)

Applicable to banks and non-bank financial institutions. |

X | |

| Vietnam | |||

| Directive on Promoting Green Credit Growth and Environmental and Social Risks Management in Credit Granting Activities, No.: 03/CT-NHNN (2015):

Requires lenders to promote ‘green’ credit growth and introduce procedures for social and environmental risk managements. |

State Bank of Vietnam:

Applicable to all financial institutions operating in Vietnam. |

X | X |

Figure 6: Regulatory sustainable banking initiatives, including monetary policy tools.

| Industry-led, Voluntary | Binding | Risk Management | Lending and Financial Products |

| Brazil | |||

| Green Protocol: Initiated in 1995 by the Ministry of Environment and five state-owned banks; revised in 2008. |

X | X | |

| Colombia | |||

| Colombia Green Protocol (2012):

Adopted by major commercial and development banks. |

|||

| India | |||

| National Voluntary Guidelines for Responsible Financing (2015):

Issued by Indian Banking Association. |

X | X | |

| Kenya | |||

| Sustainable Finance Initiative Guiding Principles (2015):

Developed by Kenya Bankers Association (KBA). |

X | X | |

| Mexico | |||

| Sustainability Protocol (2016):

Developed by Mexican Banking Association (ABM); provides guidance on risk management and sustainable lending. |

X | X | |

| Mongolia | |||

| Mongolian Sustainable Finance Principles (2014):

Developed by Mongolian Bankers Association; implemented by all Mongolian banks from 2015. Also issued sector-specific guidelines for agriculture, mining etc. |

X | X | X |

| Nigeria | |||

| Nigerian Sustainable Banking Principles (2012):

Originally developed by the Nigerian Banker’s Committee, their implementation was later made mandatory by the Central bank of Nigeria. |

X | X | X |

| Singapore | |||

| Guidelines on Responsible Financing (2015):

Issued by Association of Banks in Singapore; define minimum standards for responsible financing. |

|||

| Turkey | |||

| Sustainability Guidelines for the Banking Sector (2014):

Issued by Banks Association of Turkey. |

X | X |

Figure 7: Industry-led sustainable banking initiatives.