This Chain is part of a series on how the COVID-19 crisis is affecting agricultural markets and investor flows.

Amid widespread outbreaks in crowded meat processing facilities and a major decline in restaurant demand, innovative solutions for those operating along agricultural supply chains are accelerating during the era of COVID-19. International megatrends that were disrupting industries before the pandemic have been magnified, both posing significant risk to traditional business models and providing opportunity for creative destruction. In 2019, the National Association of Corporate Directors called on members to recognize existential threats to existing business models posed by growing megatrends like climate change, rising activism, geographical instability, expectations of responsible investors, and digitization. Such disruptive risks have been magnified by lockdowns, social distancing, unemployment, and social unrest in recent months, leaving an opening for companies that adapt and develop sustainable business models. Two trends have emerged as a result: Industry disruptors are introducing creative, small-scale solutions to major sustainability problems, while industry giants rush to invest in innovation to avoid being left behind.

Disruptive business models: Using technological innovations to solve supply chain problems

Technological advances and creative solutions to food waste are quickly disrupting agricultural supply chains. COVID-19 has underlined the vulnerability of farmers that rely solely on few, large-scale customers in the hospitality industry. Without the time or resources to package produce for a different customer base, entire yields have been wasted, exacerbating food shortages. Emerging AgriTech companies are working to reduce unsustainable practices that result from inflexible, opaque supply chains, while major industry players, such as Covantis, are investing in technological innovations to optimize supply chains. As such, the success of technological platforms that directly connect suppliers to customers rests largely on their ability to provide a competitive, transparent, and adaptable marketplace. Increasingly transparent agricultural markets also represent an opportunity to use data to mitigate deforestation risk in supply chains.

Pinduoduo, a USD 50 billion Chinese e-commerce platform that connects millions of consumers directly with producers and reduces costs through economies of scale, represents a company taking advantage of shifting dynamics. The Pinduoduo stock price almost doubled in April and May amid its efforts to create connections in a decentralized COVID-19 landscape, as farmers benefit from increased negotiating power and access to customers. Meicai, a large AgriTech startup in Beijing, targets producers and restaurants, boasting a farmer to business model. While relatively low labor costs in China have contributed to achieving the logistical capabilities required to quickly scale solutions, similar models in developed, Western nations remain largely at the startup phase. Labor costs, regulation, and efficient distributor supply chains often lead to liquidity challenges, due to the high upfront investment and over time returns.

As global hunger spikes amidst economic pressures and supply chain disruptions, business models that aim to reduce food waste are gaining momentum. By the end of 2020, the United Nations has predicted that hunger will impact up to 265 million people globally, driven primarily by income loss, unemployment, a tourism downturn, sinking oil prices, lower funds from overseas workers, and 369 million students missing daily school meals. An estimated one-third of food produced for human consumption is wasted globally, which means about 1.3 billion tons of food loss or waste across supply chains annually. U.S. estimates are even higher, with about 30 to 40 percent of food supply being wasted. As such, reducing food waste will likely be a valuable part of the solution to the supply chain disruptions experienced during COVID-19. Initiatives like Imperfect Foods and Misfits Market are facing unprecedented demand through creating value from products that are often wasted, due to nonstandard sizing, cosmetic blemishes, labelling errors, and surplus inventory issues. Delivery boxes with limited packaging enable farmers to increase revenue and quickly pivot to new customer groups, while allowing for collaboration across partners. These examples, along with similar initiatives around the world, represent solutions to one component of a large, complex problem. Outside of developed countries, the main challenge to solving hunger is distribution rather than food waste.

Disruptive business models: Meat substitutes gain market share

Employee safety concerns during COVID-19 have accelerated disruptions to the meat industry. Chain Reaction Research recently described criticism directed toward meat processing plants due to a lack of social distancing measures, resulting in closures, productivity losses, and reverberating supply chain impacts. Meanwhile, a quickly evolving meat substitute industry is designed for a higher degree of automation and sanitation, allowing facilities to ramp up production to meet demand while largely adhering to social distancing.

The meat industry has long grappled with a host of Environmental, Social, and Governance (ESG) issues. Cattle ranching is a key driver of deforestation, which is a major climate risk and has also received growing attention recently during COVID-19 for its role in increasing the risk of future infectious diseases. Accelerated adoption of meat substitutes, especially in Brazil and Colombia, could change land use dynamics longer term and reduce greenhouse gas emissions. Reputation risks have been particularly elevated for the meat industry during the pandemic. As meatpackers have become an epicenter for COVID-19 infections, plant closures have disrupted supply chains and led to high meat prices, low variety, and quantity limits in many grocery stores.

Supply chain disruptions have provided an opening for meat substitutes to access new markets. Beyond Meat Inc. and Impossible Foods Inc. are both expanding beyond traditional vegetarian consumers as a result of their focus on achieving a similar look, sound, texture, and taste as real meat. Beyond Meat Inc., valued at USD 8.3 billion, has expanded plant-based burger sales to Sam’s Club and BJ’s, in order to become more competitive with beef through higher sales quantities at discounted prices. In April, Beyond Meat Inc. entered the Chinese market through a collaboration with Starbucks in 4,000 locations. As industry giants looked to hedge the growing risks associated with meat supply chains, the Beyond Meat Inc. stock price increased by 80 percent since the start of 2020. Impossible Foods Inc., valued at USD 1.3 billion, has experienced similar success. A USD 500 million funding round in March allowed it to scale up during COVID-19, including a partnership to stock 1,700 Kroger stores.

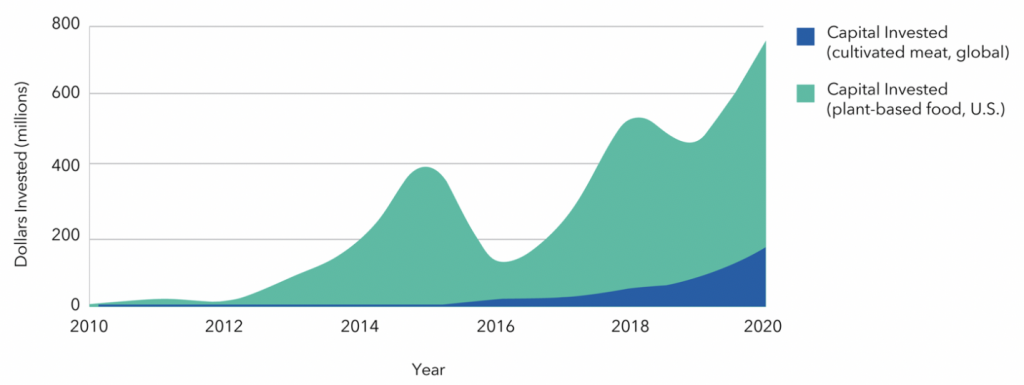

Industry disrupters, however, face competition from the very companies they aim to disrupt. In recent years, giants like Tyson Foods, Perdue, Smithfield, and Hormel have entered the meat substitutes market. Former Tyson CEO underlined that the business’ strategy was to actively disrupt itself. In fact, nine of the top ten meat companies in the United States have launched, bought, or collaborated on meat substitutes. Major players often use venture capital investments to hedge disruption risk, resulting in exponential growth of money flowing into companies making cell-based or plant-based proteins.

Figure 1: Venture capital investments in meat substitutes between 2010 and Q1 2020

Source: The Global Food Institute

Source: The Global Food Institute

As the leading meat exporter in the world, Brazil is in the spotlight for plant-based investments. In May, two major stakeholders in the Brazilian protein supply chain, ADM and Marfrig, announced the launch of a 70/30 plant-based protein joint venture. PlantPlus Foods will leverage the ingredients of ADM, while benefitting from the scale of manufacturing and distribution at Marfrig. A shifting focus to less land-intensive activities for meatpackers in Brazil could have lasting impacts on the Amazon, if sustained.

In the eight weeks leading up to mid-April, U.S. sales of meat substitute sales ballooned by 265 percent, compared to the 39 percent growth in fresh meat sales. Volume increases are contributing to a rapidly decreasing price gap between fresh meat and meat substitutes, and both start-ups and large industry players are leveraging expansion opportunities during COVID-19. If the meat substitutes market grows to USD 85 billion by 2030, as predicted by UBS, innovation, industry knowledge, and logistics will likely all be a part of scaling solutions.