This report discusses the role of Japan in the worldwide palm oil and timber market, looking particularly at the country’s position as a buyer and financier of unsustainable palm oil and plywood.

Download the PDF here: Japan: Major Financier and Buyer of Leakage Palm Oil and Plywood

Download the Indonesian version here: Japan: Major Financier and Buyer of Leakage Palm Oil and Plywood-Indonesia Version

Watch webinar recording

Key Findings:

- Japan, a large buyer of palm oil and timber products from Indonesia and Malaysia, is a leakage market for both commodities. Major trading corporations ITOCHU, Mitsubishi, Mitsui & Co., Sojitz, and Sumitomo, are buyers and financiers of unsustainable palm oil and/or plywood. While ITOCHU, Mitsui, and Mitsubishi make purchases based on NDPE, none are compliant to date. In 2020, 4,538 hectares were cleared in ITOCHU’s palm oil supply chain.

- The Japanese government’s biomass policies incentivize palm oil and wood products imports. While demand for palm products for food consumption remains relatively stable, demand for palm kernel shells and palm oil for power generation has risen amid the Japanese FIT program.

- While the 2021 Tokyo Olympics has promoted sustainability and spurred RSPO membership, the sourcing policies are inadequate. Imports of RSPO certified palm oil are small and mixed with uncertified volumes. Korindo has supplied deforestation-linked plywood for the construction of one of the Games’ venues through Japanese importer Sumitomo

- Japan’s large demand for Indonesian plywood is linked to deforestation and leakage palm oil. The largest ten exporters of Indonesian plywood to Japan cleared 15,340 ha of land for oil palm operations between 2016-2020. Sojitz, Sumitomo, and ITOCHU are among their major receivers. Only ITOCHU has a group-level NDPE policy, but its subsidiary ITOCHU Kenzai received plywood from companies that cleared land for palm oil.

- Japan is the fourth largest financier of oil palm concessions after Indonesia, Malaysia, and Singapore. Japanese financial institutions provided USD 6.2 billion in financing to the Southeast Asia palm oil sector between 2013-2019. Mitsubishi UFJ Financial, Mizuho Financial, and SMBC Group accounted for 96 percent. They also provided 63 percent of financing to companies active in the timber sector.

- Japanese trader Fuji Oil and downstream company Kao Corporation are exposed to reputation risks. Fuji Oil was exposed to 4,732 ha of deforestation and peat development in its palm oil supply chain in 2020, while Kao had 9,523 ha. Fuji Oil and Kao anticipate value losses due to deforestation risk at USD 1.6 billion and USD 60 million respectively based on current valuation multiples. Financiers and investors could engage on extra spending on monitoring/verification to avoid reputation value loss at Kao and Fuji Oil.

Japan plays a key role as importer and financier of palm and timber operations

Japan, a major buyer of palm oil and timber products from Indonesia and Malaysia, is a leakage market for both commodities. While Japan is not a grower of palm oil, a handful of general trading companies (sogo shosha) trade and finance a wide range of products including palm and timber. Five of the major Japanese sogo shosha appear in this report as buyers and financiers of unsustainable, or so-called leakage palm oil and timber. These companies are ITOCHU Corporation (“ITOCHU”), Mitsubishi Corporation (“Mitsubishi”), Mitsui & Co., Sojitz Corporation (“Sojitz”), and Sumitomo Corporation (“Sumitomo”).

Japanese palm oil imports for food and biomass power plant demand continue to grow

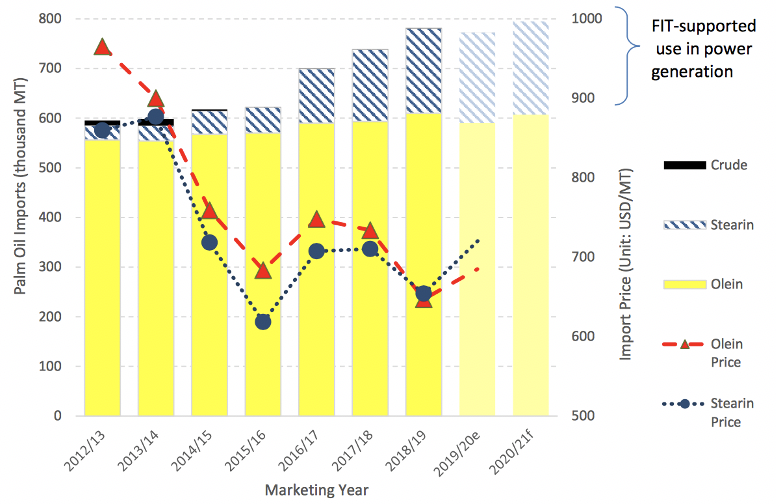

Japan is among the largest importers of palm oil from the East Asia region, primarily for food processing and biomass power plant demand. In 2018/19, Japan imported 781,758 metric tons (MT) of palm oil, of which 62 percent originated from Malaysia and 38 percent from Indonesia. Seventy-eight percent (610,428 MT) of the 2018/19 imports was palm olein oil, primarily for food processing and chemical manufacturing; 22 percent (170,741 MT) was palm stearin oil for power generation and use in food products (mainly margarine); less than 1 percent (589 MT) was crude palm oil (CPO).

Palm olein demand, primarily driven by food consumption, is relatively stable (Figure 1 below). Other industrial use of palm olein (15 percent) includes chemical manufacturing into soap, detergents, and cosmetics. For 2020/21, total palm oil imports are estimated at 795,000 MT. Also, palm kernel oil (PKO) imports have remained constant between 72,000-80,000 MT in the last five years.

Continued growth of demand for palm stearin is likely, which has been primarily driven by biomass power generation since the first palm oil power plants became operational in Japan in 2014.

Figure 1: Japan’s annual palm olein, palm stearin, and crude oil imports

Source: Figure derived from Japan Oilseeds and Products Annual, April 2020. FIT refers to the ‘feed-in tariff’ (FIT) system, a Japanese government renewable energy support scheme.

Japan is the top destination of Indonesian plywood, primarily used in construction

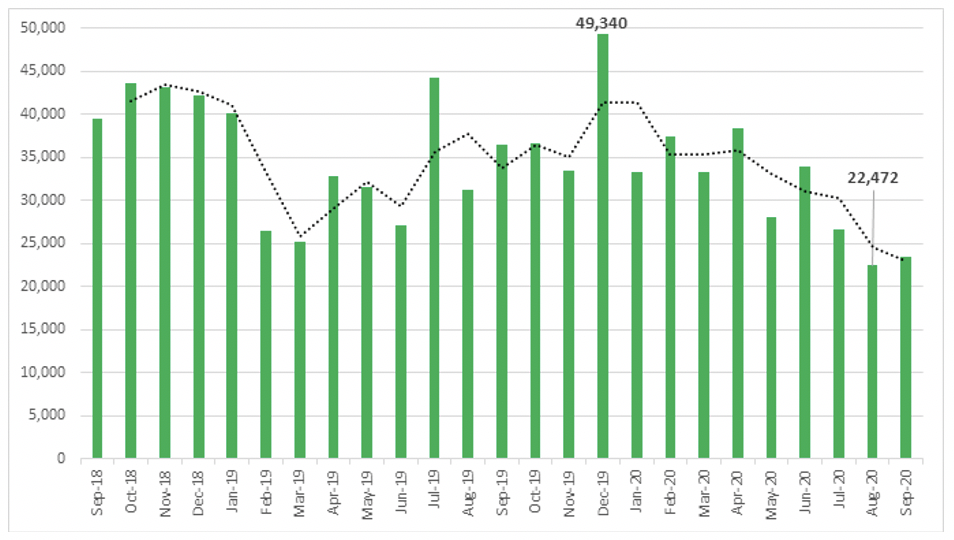

Japan is Indonesia’s largest buyer of plywood. Between September 2018 and September 2020, 8.6 million MT of plywood were exported from Indonesia to Japan. Over this period, Japan was Indonesia’s largest buyer and received 31 percent of the country’s exports of plywood, importing from 73 different companies. Average monthly plywood exports to Japan were 34,393 MT, with outliers in December 2019 (49,340 MT) and August 2020 (22,472 MT) (Figure 2).

Figure 2: Indonesian plywood exports to Japan between Sep 2018-Sep 2020 (in MT)

Source: Compiled by Chain Reaction Research, based on tradedata.net.

Japan’s imports of softwood and engineered wood products, including plywood, appear to have slowed. Trade data and sector analysis confirm this decline and recent shift in Japan’s wood market. Underlying factors are most recently linked to the COVID-19 pandemic, as imports and exports of raw materials have been affected by an overall downturn in global economic activity. More structurally, the decrease is linked to a decline in demand from the construction sector and the growth of domestic wood products.

In Japan, plywood is widely used for housing construction and flooring. With the Japanese population declining, the family housing units now being constructed are smaller. As a consequence, the principal consumer of softwood, the Japanese construction sector, has reduced its demand for overseas plywood.

Finally, Japan has increasingly relied on domestic wood products since the early 2000s. The country’s Forestry Agency (FA) aims for a surge of domestic wood consumption from 30 million m³ to 40 million m³ by 2025. Growing domestic production has gradually displaced imports of wood products from Indonesia, Malaysia, and China. To boost the consumption of wood, against the backdrop of reduced demand for housing, the government has promoted non-traditional markets for softwood products such as non-residential and high-rise buildings. Last year, the FA developed a USD 22 million support program intended at facilitating the use of structural lumber and engineered wood products in multi-story buildings.

Japan’s biomass policies incentivize imports of palm oil and wood products

Japanese government incentives for the use of renewable energy have spurred the use of palm oil, palm kernel shells, and wood pellets for power generation. The use of palm oil as a primary source of fuel by power plants is controversial due to its links to deforestation. Since 2012, Japan implemented the feed-in-tariff (FIT) Act, a renewable energy support scheme that guarantees utilities will purchase electricity generated from renewable energy at a fixed price (i.e. tariff). In 2020, the FIT system had the largest incentive in the world for biomass power at 21-24 yen/kWh. Starting in April 2022, Japan aims to introduce the feed-in-premium (FIP) scheme for large-scale biomass power plants while maintaining the FIT system for smaller plants. The FIP scheme is dependent on the market price of electricity, while FIT is based on a fixed electricity price. Both schemes will continue to rely on biomass, contrary to what was earlier expected.

Japan has delayed the requirement for palm oil and its derivates used in biomass power plants to be certified by the Roundtable on Sustainable Palm Oil (RSPO) until April 2022. The Japanese Ministry of Economy, Trade, and Industry (METI) originally planned this requirement under the FIT system from March 2019, but it was delayed until 2021, after bilateral cooperation negotiations between Japan and Indonesia in 2019. Indonesia is the largest exporter of oil palm kernel shells used in biomass power plants in Japan. Moreover, it was negotiated that Japan would also accept other certification schemes, such as the Indonesian Sustainable Palm Oil (ISPO) scheme. METI has recently delayed certification under FIT for a second time until April 2022. METI’s FIT guidelines for implementation in 2022 require “identity preserved” (IP) or “segregation” (SG) procurement of palm oil, meaning that the oil can be traced back to certified supply bases.

Meanwhile, joint civil society efforts and resident opposition have resulted in halting one existing and one newly planned palm oil-burning power plant in Japan in 2020. The largest cancelled project for a liquid palm oil plant was the 66-MW power plant in Maizuru City, Kyoto Prefecture, Japan. It had been planned to operate for 20 years and consume approximately 120,000 MT of palm oil annually. In May 2019, Golden Agri-Resources (GAR) disposed its entire shareholding in the Maizuru Green Initiatives GK, which was responsible for the planning the development of the power plant. The withdrawal of the leading company AMP Group from the Maizuru Biodiesel Electric Power Plant project ultimately kept the project from progressing. Following the cancellation of the new palm oil plant, travel agency H.I.S. in Miyagi and Sankei Energy in Kyoto were targeted by civil society campaigns to end involvements with palm oil power plants.

Steep rise of non-certified palm kernel shell imports for power generation

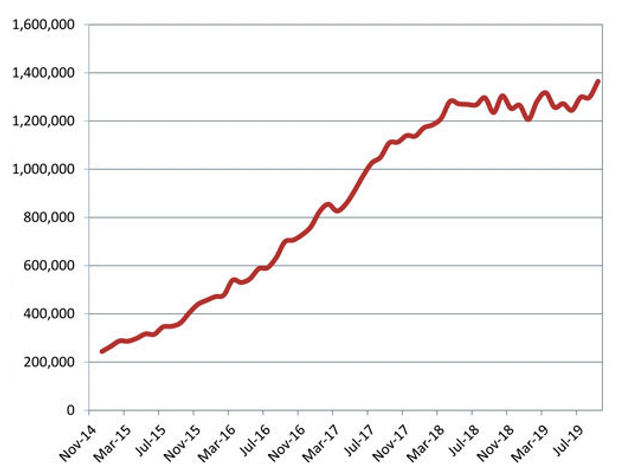

Japan has been a significant importer of palm kernel shells (PKS) since this palm oil by-product became authorized as biomass for the FIT system in 2012. Estimates point to imports of 2.5 million MT of PKS and other palm residues in 2019, which is primarily used as feedstock by medium and large (over 20 MW) FIT-eligible biomass power plants. By contrast, in fiscal year 2014-2015, Japan imported only 287,000 MT of palm kernel shells, highlighting the significant increase (Figure 3) since the first biomass power plants became operational in Japan in 2014. By 2025, Japanese PKS imports are expected to reach 5 million MT, due to an increasing number of biomass power plants that require “reliable and inexpensive feedstock.”

The majority of PKS originates from Indonesia. In 2018, Indonesia reportedly exported 1.1 million MT of PKS. Indonesia meets approximately 70 percent of Japan’s palm kernel residue demand, while the remaining 30 percent comes from Malaysia. PKS is considered the “most cost-effective biomass feedstock in terms of energy content.”

Figure 3: Steep rise in Japanese PKS imports between 2014-2019 (in MT)

Source: Biomass Magazine, January 02, 2020

The main Japanese importers of Indonesian PKS between June and November 2020 include Hanwa, Erex, Toyota Tsusho Corporation, Sumitomo Forestry, ITOCHU Corporation, and Inabata (part of Sumitomo Chemical). The latter three companies are featured as palm oil and plywood leakage players in other parts of this report. In February 2021, Tokyo-listed trading firm Hanwa was the first company to receive a so-called RSB Japan FIT Certification. The certification is for companies producing, procuring, and importing biomass into Japan under Japan’s FIT system, requiring them to follow 12 sustainability principles. In 2019, Hanwa engaged in a 15-year contract with its Indonesian-based supplier and an unidentified Japanese power plant. Only Indonesian company Jatim Propertindo Jaya is listed as a supplier of Hanwa, according to shipping data. The Riau-based company is reportedly the largest national PKS exporter that supplied 205,564 MT of PKS to Hanwa between June and November 2020. Also, renewable power producer Erex has secured fuel with Indonesian PKS suppliers for its new PKS-power plants in Japan: the 50-MW Uruma plant in Okinawa (planned for July 2021) and the 75-MW Sakaide plant in Kagawa (planned for 2025-2026). Inabata & Co. is a specialized trading group that is affiliated to Sumitomo Chemical.

Palm kernel shells are a by-product of palm oil crushing. Environmental certification schemes have not included PKS to date. Between July 2018 and June 2019, only one-fifth of the PKS produced in Indonesia and Malaysia was assessed to derive from RSPO-certified oil palm plantations. Nevertheless, several global and European certification programs, such as the Roundtable on Sustainable Biomaterials (RSB), the International Sustainability and Carbon Certification (ISCC), and the Green Gold Label (GGL), have indicated their intent to certify PKS.

METI will likely advise for the inclusion of stricter sustainability measures in the near future, such as only including certified PKS as FIT-eligible. In response, increased imports of alternative biomass fuel sources, such as wood pellets, is likely, despite the higher costs of the latter. Nevertheless, PKS sustainability certification may prove difficult to realize. Tracing a waste product that originates from numerous individual mills is not straightforward.

Tokyo Olympics accelerated sustainability performance in Japan but leakage remains likely

Japan promotes Tokyo Olympics as Sustainable Games

The Tokyo 2020 Olympic and Paralympic Games have adopted sustainable sourcing policies for palm oil, timber, paper, and other agricultural and fishery products. The procurement standards for palm oil require that all palm oil sourced is certified under one of the following approved certification schemes: RSPO, MSPO, or ISPO. According to the Sourcing Code for the Promotion of Sustainable Palm Oil, “People in Japan have so far paid very little attention to the sustainability of palm oil. Tokyo 2020, through business operators’ and consumers’ awareness of sustainable palm oil raised by formulating and implementing this Sourcing Code, aims to contribute to the long-term expansion of a movement on sustainable palm oil, which leads to the improvement at palm oil production sites.”

NGOs have flagged that the Tokyo 2020 sourcing policies do not fully address environmental concerns, such as the lack of disclosure of procurement results and the lack of an external review of the sourcing code.

Malaysia has successfully pushed for the adoption of MSPO certification in the Games’ sourcing policies next to RSPO and ISPO. The Minister of Primary Industries Malaysia, Teresa Kok, noted in 2018 that her Ministry, its agencies, and the industry were collaborating to ensure that MSPO certification is recognized by importing countries. The Malaysian government regards this action as a significant step toward globally accepted Malaysian palm oil that “enhance the branding and image of Malaysian palm oil.” The MSPO and ISPO standards generally score low on sustainable and social requirements compared to the more internationally accepted RSPO standard. But also this latter standard is being criticized for failing to deliver on environmental and social sustainability.

Plywood manufacturers under higher scrutiny from NGOs for unstainable practices ahead of Tokyo Olympics

With the Tokyo Olympics approaching, timber exporters to Japan are seeing greater scrutiny from NGOs for unsustainable practices. In November 2018, Rainforest Action Network, WALHI, TUK Indonesia, and Profundo revealed how Korindo, as an exporter, and Sumitomo Forestry, as an importer, have provided plywood for the construction of the Ariake Arena, the volleyball venue of the 2020 Tokyo Olympics. Despite the requirements of legality, sustainability, workers safety, and respect of Indigenous and community rights embodied in the Tokyo 2020’s Sustainable Sourcing Code for Timber, Sumitomo Forestry indirectly supplied plywood from a plantation company, PT Tunas Alam Nusantara (PT TAN), which had cleared an Orangutan habitat in East Kalimantan. Between 2016 and 2017, Korindo’s plywood mill received materials from PT TAN while manufacturing and exporting plywood to Sumitomo Forestry in Japan.

Similar to the RSPO, the FSC trademark for sustainable wood products has been condemned by environmental NGOs for allowing certified companies to engage in deforestation and human rights abuses. The Japanese Clean Wood Act regulation requires Japanese wood importers to verify the origin of their wood products. This can be done through industry certification schemes run by forestry and forest products associations or through third-party forest certification schemes/chain of custody (CoC) forest certification systems such as the Forest Stewardship Council (FSC) or the Programme for the Endorsement of Forest Certification (PEFC). Many companies opt for FSC certification to guarantee that the timber entering their supply chain has been sustainably produced. However, several Indonesian plywood suppliers such as Hardaya are currently FSC and PEFC certified and yet CRR partner Aidenvironment detected deforestation in their operations between 2016 and 2020.

Olympics spurred Japanese membership in RSPO but sustainability remains an issue

The Tokyo Olympics procurements standards, which include certified palm oil, caused Japanese companies to intensify sustainability activities through RSPO membership. The USDA GAIN report says, “While the use of palm oil from tropical nations has long been a controversial issue in the West, the Tokyo 2020 Olympic Games introduced the issue to Japan.” Japanese companies using RSPO-certified palm oil jumped from 37 companies in 2015 to 221 members in December 2020.

While the Olympics appear to have catalyzed sustainability issues in Japan, widespread impact has yet to be seen. Companies’ strategies to fulfill sustainability requirements seem to be mainly relying on voluntary certification schemes. The requirements under the Olympics’ sourcing code have therefore increased RSPO membership. However, in 2019, of the palm oil imported to Japan, only 2 percent was RSPO certified, in contrast to Belgium and German companies, which stood at 84 and 47 percent respectively.

While companies have promoted sustainability, for instance through RSPO membership, in practice the ‘mixed’ RSPO label on numerous Japanese products is not yet sufficient evidence of improved sustainability practices.

RSPO labels on numerous Japanese products show “mixed,” meaning that unsustainable palm oil is included in certified palm oil. While Japanese companies have attempted to move forward on sustainability issues, the certified oil so far is often a blend with non-certified oil. When Japanese companies import certified palm oil, 98 percent of their certified oil is RSPO classified as “mass balance” (MB) and “book and claim” (BC). MB refers to certified palm oil blended with untraceable, conventional palm oil at some point in the supply chain. The BC classification refers to palm oil originating from unmonitored supply chains, but that product originates from producers that purchase RSPO-certified palm oil “volume credits” as a first step toward achieving certification.

Finally, the Olympics’ sourcing codes for the promotion of sustainable palm oil remain weak as they allow for the inclusion of RSPO’s mass balance labeled palm oil. As such, uncertified, unsustainable palm oil may continue to be used for the Games.

Japan’s indirect buyers of palm oil may be a greater leakage risk than direct buyers

Japanese importers source 97 percent of its Indonesian palm oil from NDPE traders

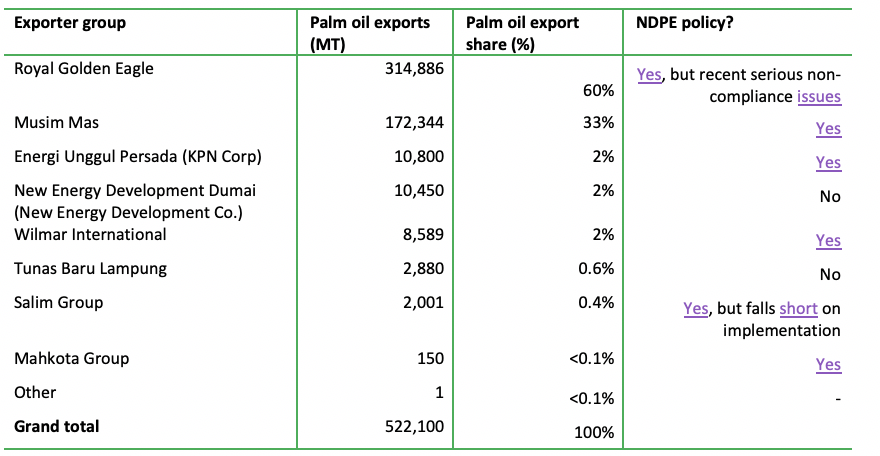

The top seven Japanese importers of palm oil sourced 93 percent of their Indonesian palm oil volumes in 2019-2020 from NDPE exporters Royal Golden Eagle (RGE) and Musim Mas. The latter two palm oil traders respectively supplied 60 percent (314,866 MT) and 33 percent (172,344 MT) of Indonesian palm oil exports to Japan from 2019 to November 2020 (Figure 4 below). Also, Wilmar International and Energi Unggul Persada both supplied 2 percent under an NDPE commitment. The latter company, which is part of KPN Corporation Group (formerly GAMA), had to adopt and commit to KPN Corps’ NDPE policies by the end of 2019. The remaining 3 percent (13,331 MT) originated from leakage refiners and traders, including New Energy Development Dumai (10,450), Tunas Baru Lampung (2,880 MT), and Salim Group (2,001 MT). The latter company does have an NDPE policy, but falls short on implementation. New Energy Development Dumai is part of the Japanese company New Energy Development Co., which has significant expansion plans for its biomass power plants, using palm oil and kernels as the main source of fuel. The company has no public NDPE policy.

There has recently been controversy over RGE Group’s compliance with its NDPE policies, particularly in its palm oil trading and processing arm APICAL and in its pulp and paper business APRIL. Aidenvironment-Earthqualizer’s most recent footage links RGE to Nusantara Fiber Group’s subsidiary PT Industrial Forest Plantation, which has already deforested over 10,000 ha in Kalimantan, Indonesia. Another 50,000 ha are at immediate risk of being cleared in the near future. RGE denies any connection with Nusantara Fiber Group, which has a secret ownership structure, but they are connected in various ways to the Nusantara Fiber group. RGE Group receives loans from the Japanese bank Mitsubishi UFJ Financial Group (MUFG) and the Dutch bank ABN AMRO, among others.

Moreover, reportedly “over 100 communities are, or have been in active conflict with RGE and its suppliers” and linked to RGE’s pulp and paper operations’ subsidiary APRIL. The company was highlighted as one of the largest corporate groups whose policies and standard operations procedures fail to respect local communities’ free, prior, and informed consent (FPIC).

Figure 4: Key suppliers of Indonesian palm oil to Japan (2019-2020)

Source: Compiled by Chain Reaction Research, based on Indonesian export data. Trade data 2020 only covers till November 2020. Since the data only covers Indonesian export data to Japan, and not Malaysian export data, the list of palm oil exporters to Japan is not exhaustive.

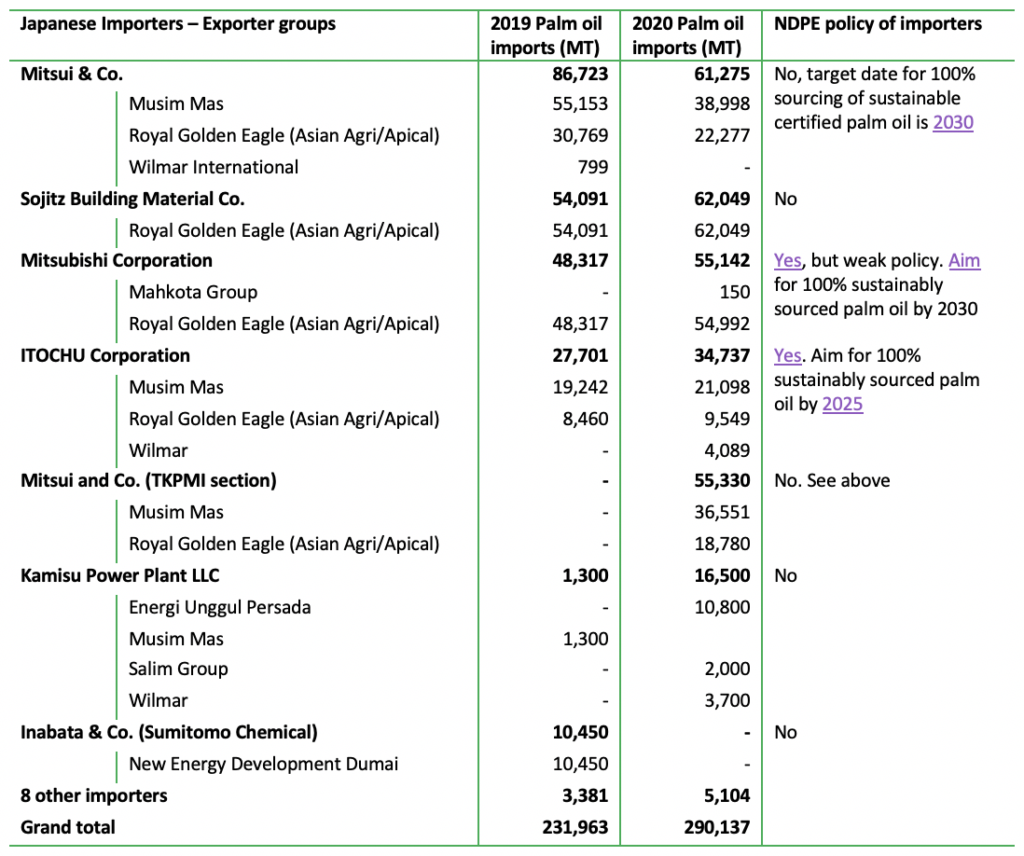

Leakage is likely, given that only ITOCHU has a group-level NDPE policy among the Japanese top seven importers of Indonesian palm oil. Traders Mitsui & Co. and Mitsubishi Corporation have 2030 as their target dates for 100 percent sustainably procured palm oil (Figure 5). While Mitsubishi has an NDPE policy, it is considered weak since it does not reference FPIC and no burning. Combined with compliance issues in their suppliers’ base (e.g. Royal Golden Eagle), the weak policy makes uptake of leakage palm oil in their supply chains more likely.

Figure 5: Top 7 Japanese importers of Indonesian palm oil in 2019 and 2020, including exporter groups

Source: Compiled by Chain Reaction Research, based on trade data. Data 2020 only covers till November 2020. Moreover, trade data only covers Indonesian export data to Japan, not Malaysian export data. This could partly explain why one of the largest Japanese palm oil users who mainly sources in Malaysia, Fuji Oil Holdings, does not appear in this Figure.

Largest user of palm oil, Fuji Oil, and shareholder ITOCHU, linked to a combined 9,270 ha of clearing in 2020

Stock-listed trader Fuji Oil Holdings is the largest Japanese user of palm oil products. The company consumed 776,000 MT of CPO, CPKO, and refined palm oil in 2019. It sources the majority of its volumes from Malaysia (58 percent), while the rest originates from Indonesia (38 percent), Papua New Guinea (3 percent), and Thailand (1 percent). In 2019, the company spent 11-20 percent of its procurement on these palm oil products. Fuji Oil’s palm oil products represent 21-30 percent of the company’s net revenues. Japanese trading company and sogo shosha ITOCHU Corporation is Fuji Oil’s largest shareholder and one of the seven major buyers of Indonesian palm oil (Figure 5 above).

Fuji Oil has set a 2030 target to improve its sustainability performance, partly through entering a supply chain relationship with Mars through UniFuji, a partnership between Fuji Oil and United Plantations. Fuji Oil, which promotes an NDPE policy within its group, has had a responsible palm oil sourcing policy since 2016. The company also has a public grievance mechanism, and it aims to reach 100 percent sustainably sourced palm oil by 2030.

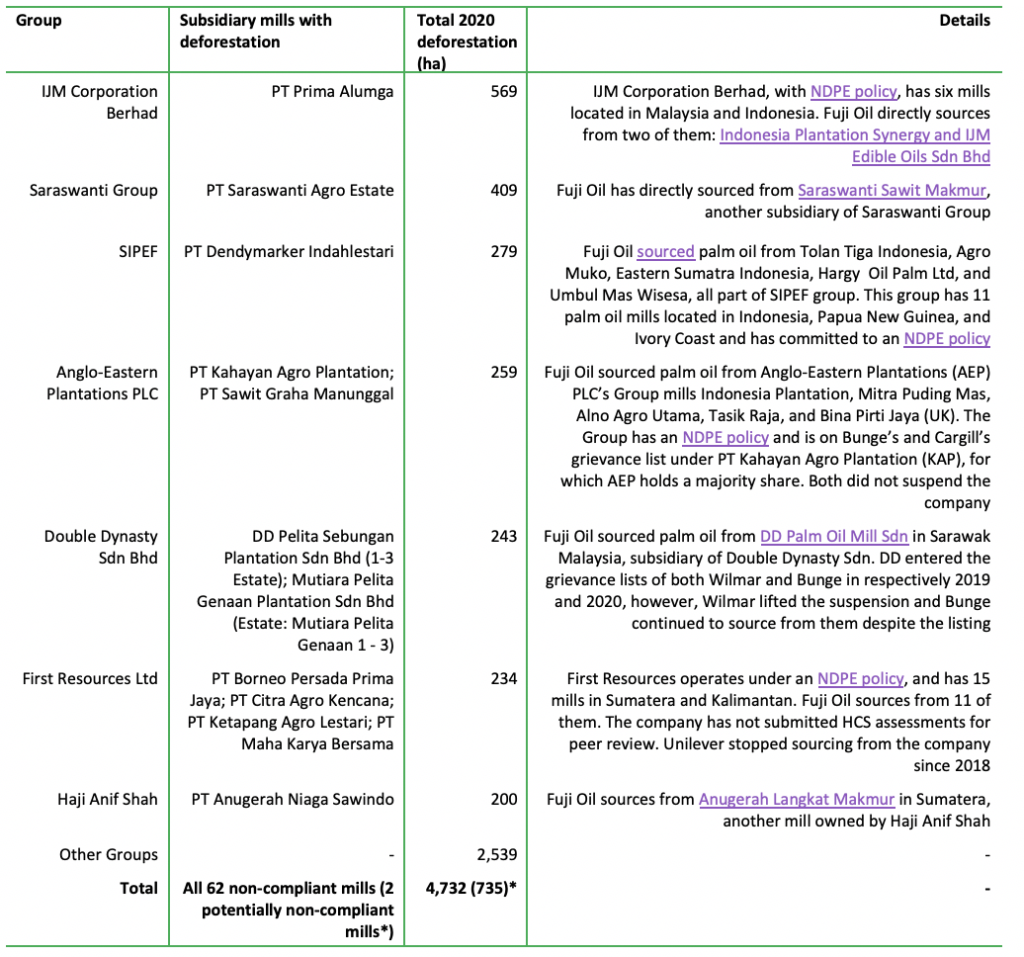

Aidenvironment-Earthqualizer identified 4,732 ha of removal of forest, peat forest, and peat in Fuji Oil Holdings’ palm oil supply’s base in 2020. Of the company’s 1,395 supplier mills, 62 were found to be NDPE non-compliant, along with two potentially non-compliant (Figure 6 below). These seven supplier groups were responsible for 46 percent (2,193 ha) of the non-compliant palm oil that entered Fuji Oil’s supply base in 2020. Moreover, two groups listed as the largest deforesters within oil palm concessions in Indonesia, Malaysia, and Papua New Guinea in 2020, Capital Group and Jhonlin Group, operate mills that appear in the supply chains of a number of traders and brands with NDPE policies, including Fuji Oil.

Moreover, Aidenvironment-Earthqualizer detected 4,538 ha of deforestation in 2020 in the palm oil supply chain of Fuji Oils’ main shareholder ITOCHU Corporation. ITOCHU, a Japanese trader without palm oil mills and refineries, sourced 308,000 MT of palm oil and palm oil products in 2019, of which 91 percent of its CPO volumes were reportedly from 688 mills. Of these mills, 40 were found to be non-compliant and removed 4,538 ha of forest and peat in 2020. The largest deforesters in its supply chain are mostly similar to the suppliers of Fuji Oil (Figure 6). ITOCHU has an NDPE policy that applies to its sourcing of timber, pulp & paper, rubber, and palm oil and aims for 100 percent sustainably sourced palm oil by 2025.

Figure 6: Fuji Oil Holdings suppliers with over 200 ha of deforestation in 2020

Source: Aidenvironment/Earthqualizer. *Also mills YP Plantation Holdings Sdn Bhd (Pekan Timur Estate) of Yayasan Pahang Group and PT Arjuna Utama Sawit, owned by Mr. Alexander Thaslim were among the highest deforesting suppliers, linked to respectively 417 ha and 318 ha (total 735 ha) of deforestation. While potentially connected To Fuji Oil Holdings, the linkages could not be confirmed.

Japanese FMCG companies procure significant volumes of palm; leakage risks more likely

Japanese fast moving consumer goods (FMCG) companies, including Nissin Foods Group, Calbee, Lion, Moringa Milk Industry, and Kao, buy significant amounts of palm oil and palm oil products. In particular, Kao Corporation sources considerable amounts, with 11-20 percent of its procurement spent on palm oil and palm oil products, while Calbee Inc., Moringa Milk Industry, and Lion Corporation disclosed that they spend about 1-5 percent of their procurement on palm oil. Nissin Foods Group did not respond to a request for data on its palm oil business. Other FMCG companies, such as Ajinomoto Group, spend less than 1 percent of their procurement on palm oil.

Only Kao Corporation and Nissin Foods Group have NDPE commitments. Kao Corporation seems most advanced in its commitments, with a 2020 zero-deforestation target and public disclosure of its palm oil mills. Nissin Foods Group’s NDPE policy was revised in 2020 to include the procurement of sustainable and conflict-free palm oil, although the target date for 100 percent sustainable procurement is not until 2031. The company does not publish its list of palm oil mill suppliers. Consumer goods manufacturers Moringa Milk Industry, Calbee Inc., and Lion Corporation have no NDPE policies, nor do they publish their mill suppliers. While they are all RSPO members, they typically source BC and MB-classified palm oil.

The leakage of unsustainable palm through FMCGs is likely due to the limited NDPE group level commitments and implementation of most buyers, the lack of screening of suppliers, and non-transparent supply chains.

Despite leading in sustainability reporting and disclosure, Kao suppliers link to 9,523 ha of deforestation

Japanese FMCG company Kao Corporation sources significant volumes of palm oil and palm oil products from Indonesia, Malaysia, and Thailand. The company spends 11-20 percent of its procurement on purchasing CPO, crude palm kernel oil (PKO), and its derivatives for use in its consumer goods business, and fatty acid for use in their chemical business. In 2020, Kao consumed 446,000 MT of palm oil products. Moreover, the company states that 81-90 percent of its total revenue is dependent on products containing palm and palm (kernel) oil derivatives.

Kao Corporation, founded in 1887, reported JPY 1,382 billion (USD 12 million) in revenues and 33,603 permanent employees as of December 31, 2020. The company’s consumer products business includes cosmetics (20.1 percent consolidated net sales in FY2019), skin and hair care (22.7 percent), human health care (17 percent) and fabric and home car (23.9 percent). The chemical business segment accounts for 16.3 percent. Kao Corporation jointly operates PT Apical Kao Chemicals with Royal Golden Eagle’s subsidiary Apical. This joint venture supports Kao with securing sufficient raw materials for its chemical business unit.

Kao Corporation has included the responsible sourcing of palm oil and timber products on its agenda. It seems to be the only Japanese FMCG company that has disclosed its 2019 palm oil mill list. The three other Japanese companies disclosing their palm oil mills lists are traders Fuji Oil, ITOCHU Corporation, and Nisshin Oillio (with main shareholder Marubeni). Kao has sourcing guidelines for palm oil and paper, committing to zero-deforestation and abstaining from buying palm oil linked to development of forest and peatland. In February 2021, the company was recognized as a supplier engagement leader for the fourth consecutive year by CDP, a nonprofit that focuses on global disclosure system on environmental impacts, for its efforts in reducing carbon emissions and tackling climate change across its supply chain. Kao has been a RSPO member since April 2007. While the company originally planned to reach 100 percent traceable palm oil in 2020 through RSPO-certified palm oil, it reportedly decided to “verify ourselves that the palm oil we use is traceable and leads to zero-deforestation. The reason for this decision is that the supply of certified oil to the market is insufficient, and some environmental NGOs have pointed out that certified oil does not necessarily lead to zero-deforestation, or fully protect human rights.”

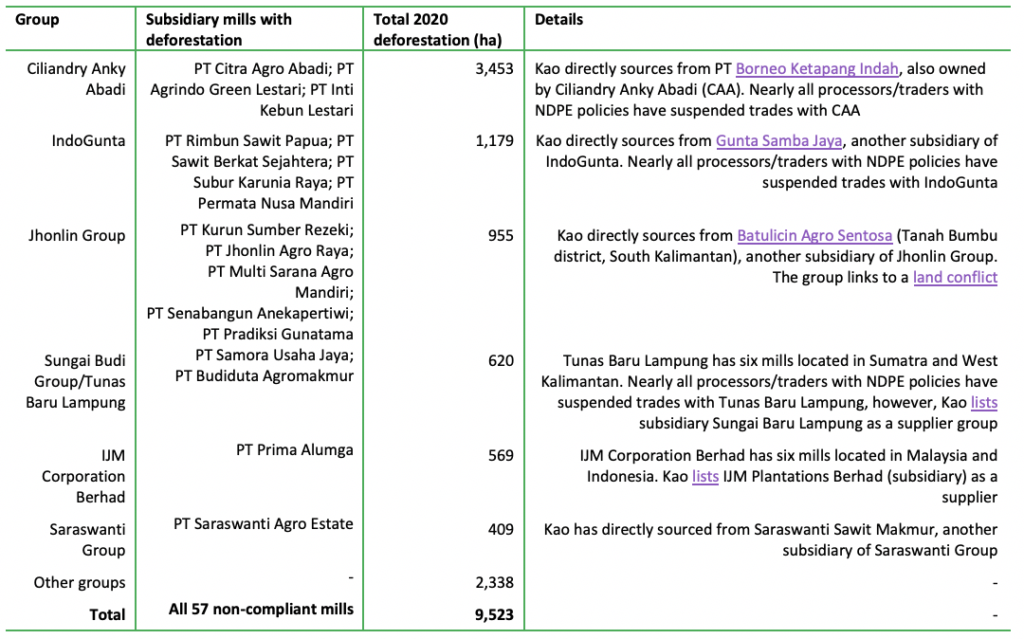

Aidenvironment-Earthqualizer’s 2020 deforestation monitoring of Kao’s suppliers, however, reveals that the company’s verification systems have been insufficient. As such, the FMCG company has become an important leakage buyer of unsustainable palm oil and palm oil products. Of its 1,027 supplier mills, 57 non-compliant mills deforested 9,523 ha of forest, peat forest, or peat in 2020 in Indonesia and Malaysia. Figure 7 below highlights the largest 2020 deforesters linked to Kao Corporation. These six company groups were responsible for 75 percent (7,185 ha) of all deforestation on palm oil and palm oil concessions that supplied to Kao Corporation in 2020. Ciliandry Anky Abadi (CAA), IndoGunta, and Jhonlin Group also appear on the 2020 top 10 deforesters of Southeast Asia.

Figure 7: Kao suppliers with most deforestation in 2020

Source: Aidenvironment/Earthqualizer, based on deforestation data (Sentinel Satellites 1 and 2)

Japan’s demand for plywood linked to deforestation and leakage palm oil

Top exporters of Indonesian plywood to Japan linked to leakage palm oil

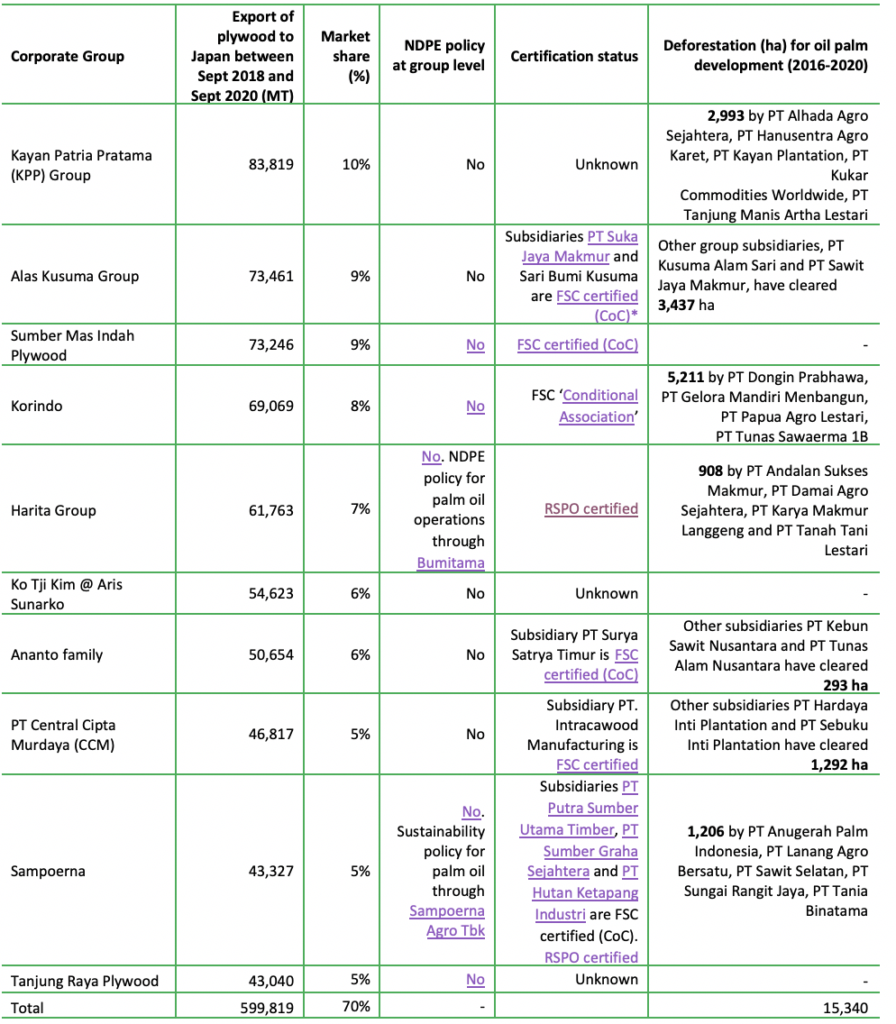

The top 10 largest exporters of Indonesian plywood to Japan cleared 15,340 ha of land for oil palm between 2016 and 2020 (Figure 8). Between 2018-2020, they exported 599,819 MT of plywood to Japan, representing 70 percent of the total export volume. Seven out of the 10 corporate groups also grow oil palm, but none have adopted a group NDPE policy covering all their plantation operations.

Figure 8: Top 10 exporters of Indonesian plywood to Japan between Sep 2018 and Sep 2020

Source: Compiled by Chain Reaction Research, based on trade data, corporate websites, and Aidenvironment-Earthqualizer deforestation data (Sentinel Satellites 1 and 2). *CoC stands for Chain of Custody Certification, i.e., FSC-certified material has been identified and separated from non-certified and non-controlled materials.

The majority of these Indonesian plywood exporters have unknown ownership structures, do not have public websites, and are not transparent about their suppliers, buyers, and palm oil operations. The most opaque groups include Kayan Patria Pratama (KPP), Alas Kusuma Group, Sumber Mas Indah Plywood, Ko Tji Kim @ Aris Sunarko, the Ananto family, and Tanjung Raya Plywood:

- KPP exported plywood through two subsidiaries, Idec Abadi Wood Industries (81,169 MT) and Kayan Wood Industries (2,650 tons). The first is located in Kota Tarakan, North Kalimantan and produces plywood and sawn timber. Little is known about the second subsidiary;

- Alas Kusuma Group exported plywood to Japan through Sari Bumi Kusuma (64,997 MT) and Harjohn Timber (8,463 MT), both located in West Kalimantan;

- Sumber Mas Indah Plywood is a processing company located in Gresik, East Java which produces plywood, woodworking, and secondary process products, with a 12,000 m³ monthly capacity. It exports to different regions, including Asia, North America, and Europe;

- Ko Tji Kim @ Aris Sunarko owns two processing companies, PT Wijaya Triutama Plywood and PT Wijaya Cahaya Timber;

- The Ananto family’s operations are opaque as neither PT Surya Satrya Timur nor Wana Cahaya Nugraha owns a website;

- Tanjung Raya Plywood produces 6,600 m³ of wood products per month and exports to different markets, but primarily Japan and India. It is not known whether the company has any connection with the palm oil sector.

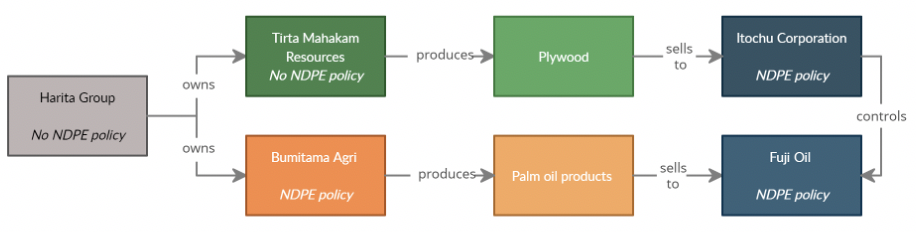

Plywood exporters with more transparency and with known links to palm oil NDPE buyers include the Harita Group, PT Central Cipta Murdaya (CCM), and Sampoerna. CCM’s NDPE buyers are the most exposed to deforestation risks as CCM does not have any NDPE policies, in contrast to the Harita Group and Sampoerna, both of which have NDPE policies for their palm oil divisions. The Harita Group exported plywood through Tirta Mahakam Resources. The company, located in Gresik, East Java, manufactures and sells plywood and related wood products. It has factories in East Kalimantan. The Harita Group is an Indonesian conglomerate with business in natural resource industries. Its main businesses include palm oil plantations, mining, and smelters. Most NDPE buyers of the palm oil sector source from Bumitama, Harita’s palm oil division (Figure 9).

Figure 9: Harita Group linkages to NDPE buyers

Source: Compiled by Chain Reaction Research, based on trade data, public palm oil mill list and corporate websites.

PT Intracawood Manufacturing is part of the Central Corporate Management Group (CCM), which operates in a number of businesses, including property, manufacturing, retail, IT, construction, and natural resources in Indonesia and overseas. CCM is allegedly owned by husband-and-wife Murdaya Widjawimarta Poo and Siti Hartati Murdaya, who ranked 14th on the Forbes list of the richest Indonesians in 2011. CCM Group sells palm oil to most NDPE buyers through Hardaya Inti Plantations, including Unilever, AAK, Cargill, Ferrero, GAR, Nestlé, and P&G.

Sampoerna operates in many different sectors including banking, transportation, property, and plantation (forestry, rubber and oil palm). The group exported plywood to Japan through three different subsidiaries, including PT Sejahtera Usaha Bersama (32,558 MT). The oil palm division, Sampoerna Agro Tbk, has been listed on the Indonesian Stock Exchange since 2007. Thirty-seven NDPE buyers source palm oil from the group as of February 2021.

Korinodo is likely the best-known exporter of plywood and palm oil linked to compliance issues. The company is accused of unsustainable oil palm and plywood operations. Korindo’s subsidiaries, Korindo Aria Bima Sari and Balikpapan Forest Industries, respectively, exported 40,762 MT and 28,306 MT of plywood. Korindo operates four logging companies and seven processing facilities, mainly in Papua and Kalimantan. Avon, Kellogg’s, and Mondelez buy palm oil from Korindo as of February 2021.

Only two out of the top 10 exporters of Indonesian plywood to Japan have adopted NDPE policies that cover their palm oil operations. They include Harita Group (through Bumitama) and Sampoerna (through Sampoerna Agro Tbk). None of them have adopted sustainability policies that apply to their full plantation business even though several also operate timber plantations in Indonesia.

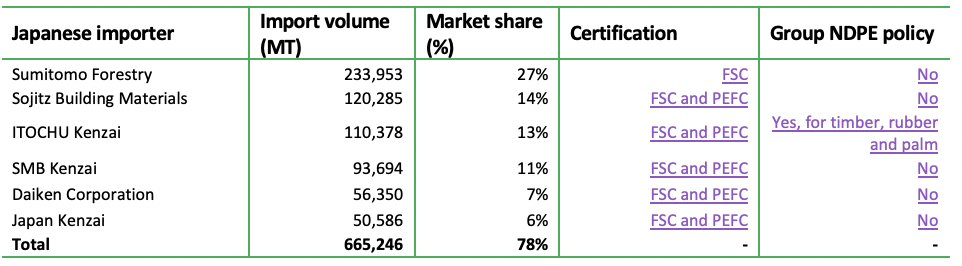

Top 6 Japanese importers of Indonesian plywood linked to palm oil growers without NDPE

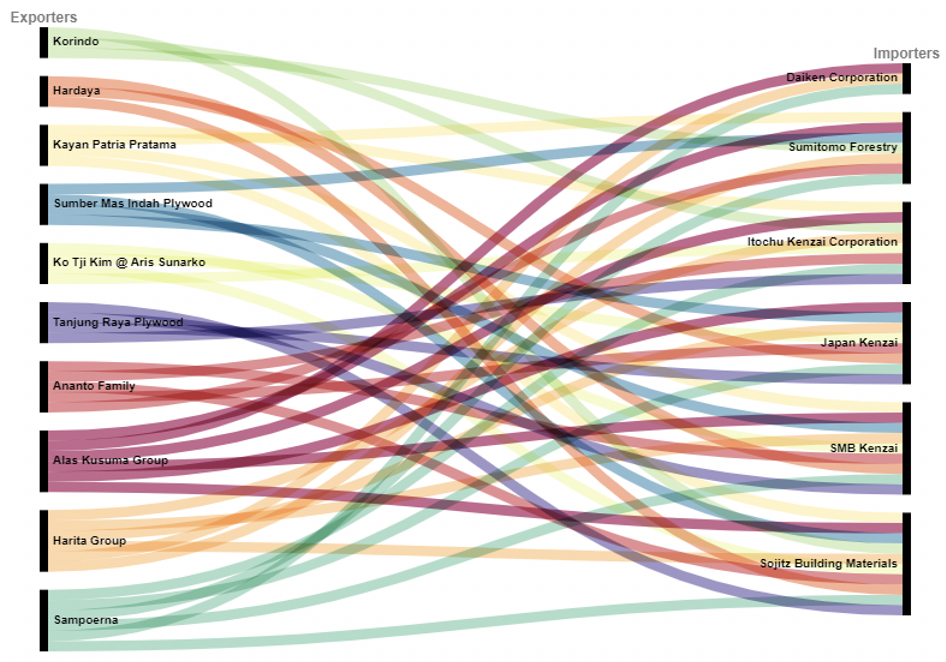

The 10 Indonesian groups primarily exported to six Japanese companies that received 78 percent, or 665,246 MT, of plywood between 2018-2020. The alluvial diagram below (Figure 10) shows how the top exporters and top importers of Indonesian plywood to Japan are connected. While these importers are all FSC certified, they source plywood from companies running palm oil activities not covered by NDPE policies. These Japanese companies have yet to adopt cross-commodities group level NDPE commitments (Figure 11).

Figure 10: Supply relationships between Top 10 exporters of Indonesian plywood and top 6 Japanese importers of Indonesian plywood (Sep. 2018 – Sep. 2020)

Source: Compiled by Chain Reaction Research, based on trade data

Figure 11: Top 6 Japanese importers of Indonesian plywood between Sep 2018 and Sep 2020

Source: Compiled by Chain Reaction Research, based on trade data, corporate websites, FSC and PEFC websites

The main Japanese importer linked to leakage plywood and palm oil is Sumitomo Forestry. Sumitomo Forestry is listed on the Tokyo Stock Exchange and specializes in natural resources management and the material and construction business. Sumitomo Forestry owns approximately 48,000 ha of forest and plantation in Japan and 231,000 ha overseas, in Indonesia, Papua New Guinea, and New Zealand. The company’s operations have already been reported by several NGOs as it was linked to companies (Shin Yang, Samling, and WTK) operating illegal and unsustainable logging in Sarawak. More recently, the company was exposed for purchasing tainted timber from Korindo. Between September 2018 and September 2020, Sumitomo Forestry also received plywood from Alas Kusuma Group, which operates oil palm plantations without an NDPE policy.

Other Japanese importers receiving plywood from companies without group NDPE policies include Sojitz Building Materials, ITOCHU Kenzai Corporation, SMB Kenzai, Daiken Corporation, and Japan Kenzai. Sojitz Building Materials is 100 percent owned by the Japanese conglomerate Sojitz Corporation. Sojitz Building Materials is involved in construction materials trading, construction, and real estate, while Sojitz Corporation is a conglomerate listed on the Tokyo Stock Exchange. Sojitz Building Materials sourced plywood from nine out of 10 of the top exporting groups, including Korindo, Kayan Patria Pratama, and Hardaya. Five of Sojitz Building Materials’ suppliers, including PT Kayu Lapis Asli Murni, which belongs to the Salim Group, run palm oil activities without an NDPE policy.

ITOCHU Kenzai Corporation, a subsidiary of ITOCHU Corporation, runs its business in the construction sector through many branches. It owns a policy for wood procurement, mainly focused on legality aspects. In 2017, the Rainforest Action Network reported how ITOCHU was linked to unsustainable companies operating plantations in different forest-risk commodity sector (pulp and paper, timber, palm oil, rubber). ITOCHU has also been exposed through its import of plywood, as four of its plywood suppliers operate in the palm oil sector without any NDPE policy. While ITOCHU’s palm oil business is covered by a Responsible Palm Oil Sourcing Policy, adopted by Fuji Oil, it continues to source from several plantation companies where forest clearance was recently found. The companies include IJM Corporation, Genting, and Sumber Tani Agung Resources.

SMB Kenzai is owned by three parent companies: Sumitomo Corporation (36.25 percent), Mitsui & Co Ltd (36.25 percent) and Marubeni Corporation (27.5 percent). Its activities include import/export, real estate, services, and sales. PT SMB Gobel Indonesia and PT Indonesia Fibreboard Industrya Tbk are two companies affiliated with SMB Kenzai that are conducting business in Indonesia. SMB Kenzai follows the requirements of Sumitomo’s environmental policy, which requires legal compliance for wood products handled by the group. Since none of the two companies’ operations are covered by NDPE commitments, SMB Kenzai is exposed to the same risks as Sumitomo. The company sourced from nine out of 10 top supplier groups of Indonesian plywood between September 2018 and September 2020 (Figure 10), many of them showing deforestation in their palm oil operations. Five out of its 26 plywood suppliers are also operating oil palm plantations not yet covered by NDPE commitments.

Daiken Corporation imported 56,330 MT of plywood to Japan between September 2018 and September 2020. The company is listed on the Tokyo Stock Exchange and specializes in the production of various wood materials and furniture for housing and construction. Daiken’s top shareholder is ITOCHU Corporation (35 percent). It conducts activities in Indonesia through PT Daiken Dharma Indonesia which is both a production center and a representative office. Two plywood suppliers of Daiken grow oil palms in Indonesia without an NDPE policy.

Japan Kenzai produces building materials. It is owned by JK Holdings and listed on the Tokyo Stock Exchange. In Indonesia, Japan Kenzai has one representative office and one subsidiary company. Japan Kenzai sources from seven out of the 10 biggest Indonesian plywood exporters. Among its 18 suppliers, three are not covered by NDPE commitments.

Japan is the 4th largest financier of the Southeast Asia palm oil sector

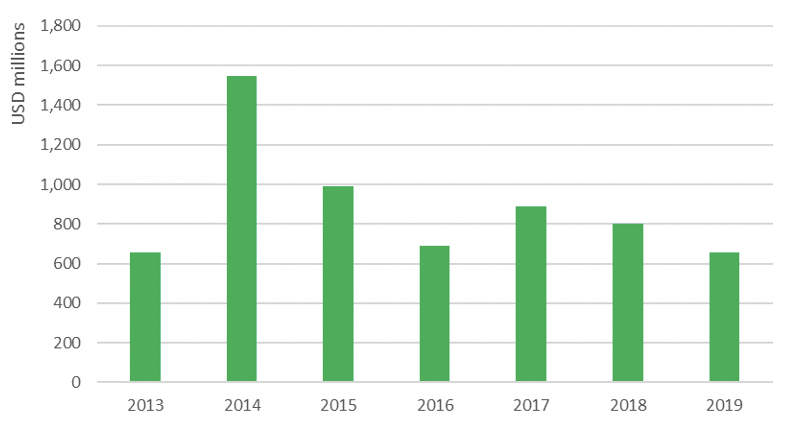

Japanese financial institutions provided USD 6.2 billion in financing to Southeast Asia palm oil

Between 2013 and 2019, Japanese financial institutions provided 11 percent of the total identified financing to companies in the Southeast Asia palm oil sector. In the form of loans and underwriting services, Japanese financial institutions provided USD 6.2 billion in financing to the palm sector. As the fourth largest financier, Japan follows Malaysia, Indonesia, and Singapore.

Figure 12: Loans and underwriting to Southeast Asia palm oil from Japanese financial institutions

Note: All amounts are adjusted for palm oil attributable value. Source: Forests & Finance (2020).

Annual financing provided by Japanese financial institutions averaged USD 890 million between 2013 and 2019, while the rise in the 2014 figure was mainly the result of the USD 405 million in financing provided by Mitsubishi UFJ Financial and Mizuho Financial to Sime Darby for the acquisition of New Britain Palm Oil Limited (NBPOL).

Of the total identified financing by Japanese financial institutions, 96 percent originated from Mitsubishi UFJ Financial, Mizuho Financial, and SMBC Group. Between 2013 and 2019, these three financial institutions provided USD 2.3 billion, USD 2.0 billion, and USD 1.7 billion respectively worth of loans and underwriting services to Southeast Asia palm oil sector.

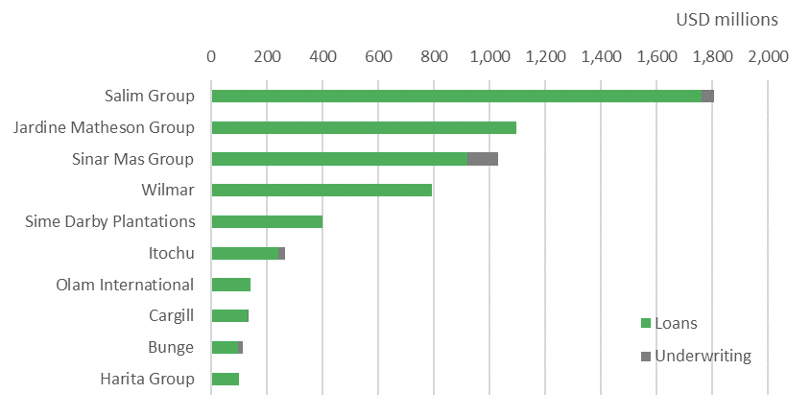

The Salim Group received the largest identified financing from Japanese financial institutions with a total of USD 1.8 billion from 2013-2019. The Salim Group was the only major Indonesian palm oil exporter to receive a substantial amount of financing. During the same period, Jardine Matheson Group and Sinar Mas Group received USD 1.1 billion and USD 1.0 billion, respectively. Along with the Salim Group, Wilmar International with USD 792 million and ITOCHU Corporation with USD 265 million were also in the top 10 list of clients of Japanese financiers. Despite having an NDPE policy, Salim Group falls short on its implementation.

Figure 13: Top 10 palm oil clients of Japanese financial institutions (2013-2019)

Note: All amounts are adjusted for palm oil attributable value. Source: Forests & Finance (2020).

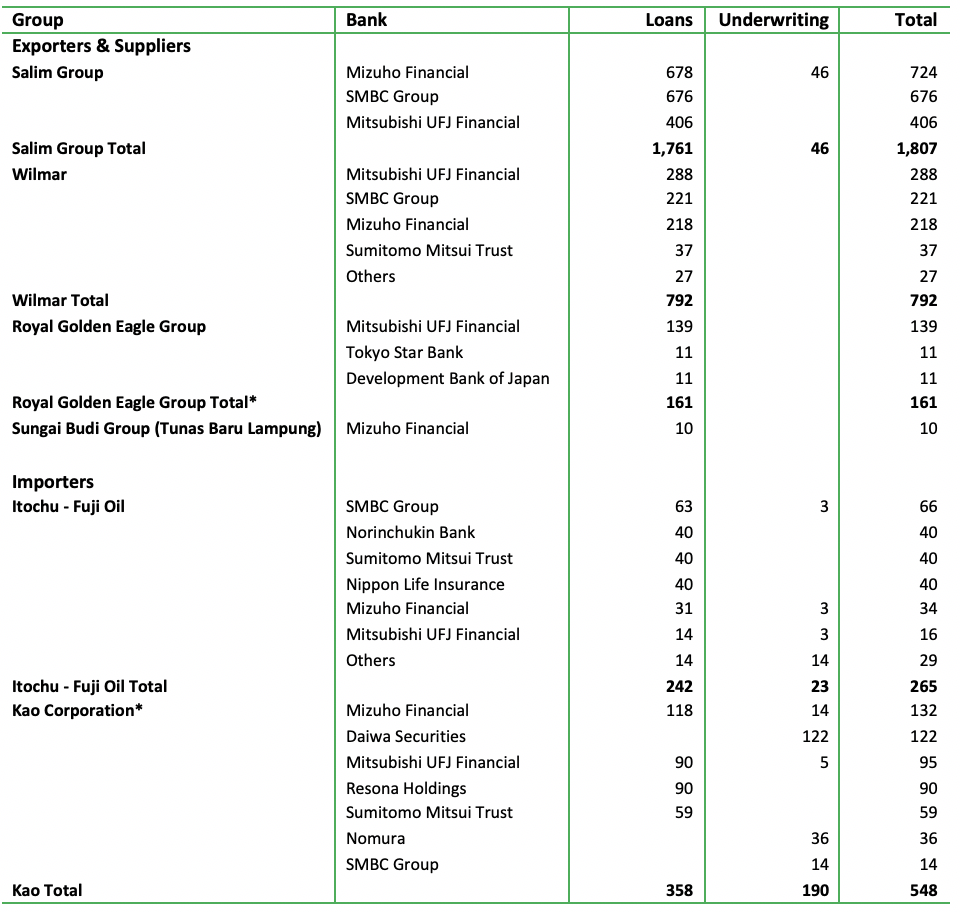

Trader Fuji Oil and downstream company Kao Corporation received respectively USD 265 million and USD 548 million financing from Japanese financial institutions. Royal Golden Eagle Group, the largest exporter of palm oil from Indonesia to Japan, received a limited USD 161 million from Japanese institutions. This amount corresponds to only two percent of the USD 7.1 billion total identified financing received by the company. For the two large Japanese industrial groups, Mitsui and Mitsubishi’s financing data was not included as palm oil operations represent a very small portion of their business activities. For the other names mentioned in the report, no financial links to Japanese financial institutions were identified by the Forests & Finance database.

Figure 14: Selected palm oil exporter/importers with identified financing from Japan (2013-2019, USD millions)

Note: All amounts are adjusted for palm oil attributable value, except for Royal Golden Eagle Group and Kao (*) for which the financing amount is for the whole company. Source: Forests & Finance (2020). Chain Reaction Research (2020).

Japanese financiers of palm oil sector also financing companies active in timber sector

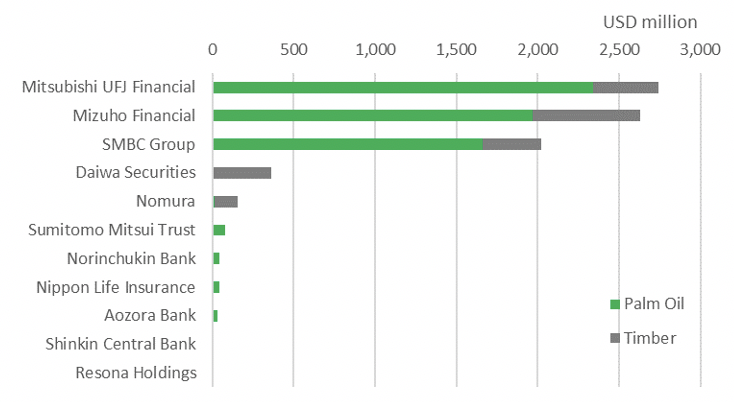

Mitsubishi UFJ Financial, Mizuho Financial, and SMBC Group are also among the top five Japanese financial institutions that finance wood manufacturers for the construction sector. They provide 63 percent of financing. Out of the USD 2.3 billion total identified loans and underwriting services provided by Japanese financial institutions, Mizuho accounts for 29 percent (USD 662 million), Mitsubishi UFJ for 18 percent (USD 400 million), and SMBC Group for 16 percent (USD 361 million).

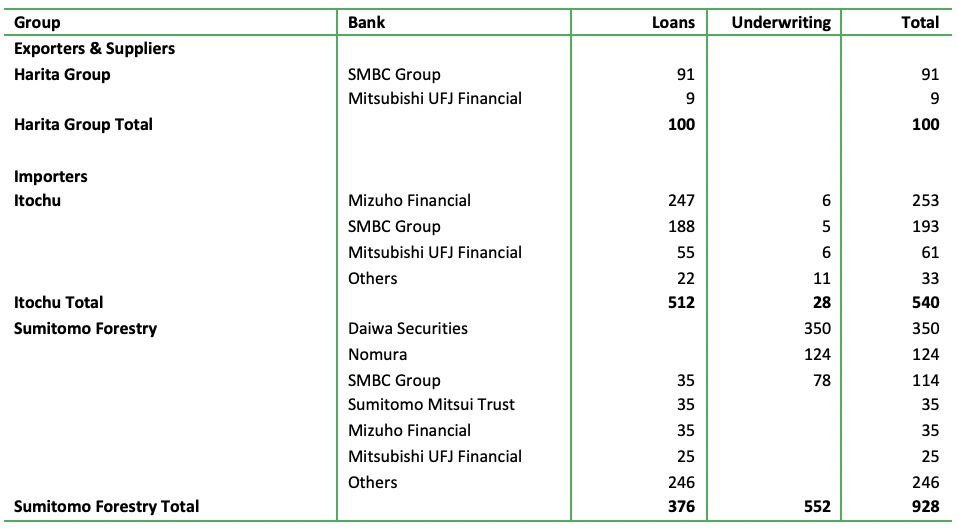

Figure 15: Selected timber exporter/importers with identified financing from Japanese institutions (USD millions)

Note: Amounts for Sumitomo Forestry and Itochu are adjusted for timber attributable value, while for Harita Group (*) the financing amount is for the whole company. Source: Forests & Finance (2020).

The combined total amount of financing provided to the palm oil and timber sectors by the Mitsubishi UFJ Financial, Mizuho Financial, and SMBC Group was USD 7.4 billion between 2013 and 2019. Following the top three, Daiwa Securities and Nomura provided USD 364 million and USD 155 million to the timber sector during the same period.

Figure 16: Top 10 Japanese creditors of palm oil and timber (2013-2019)

Note: All amounts are adjusted for palm oil and timber attributable value. Source: Forests & Finance (2020).

Forest-risk sector policies of Mitsubishi UFJ Financial, Mizuho Financial, and SMBC Group remain inadequate

According to 2018 policy assessments by Forests & Finance, all three financial institutions are weak on environmental standards, despite having publicly available forest-risk commodity sector policies.

Mitsubishi UFJ Financial: The bank scored 18 out of 50 on Forests & Finance 2018 policy assessment, as its policies were labeled as “bad” on prohibiting deforestation by clients except for High Conservation Value areas. Regarding its palm oil sector policy, MUFJ states clients are encouraged to become members of the RSPO, and the company requests clients to submit action plans to achieve certification when relevant operations are not certified. As a recent development, Japanese NGO Kiko Network, with the support of Rainforest Action Network (RAN), 350.org Japan, and Market Forces filed a climate resolution on Mitsubishi UFJ Financial in March 2021, calling on Mitsubishi UFJ to adopt and disclose a plan to align its financing and investments with the Paris Climate Agreement. The bank is also being questioned for its decision to exclude its Indonesian subsidiary, Bank Danamon, from its global ESG policies. Bank Danamon is one of the sources of finance to the Sinar Mas Group’s palm oil division led by Golden Agri-Resources.

Mizuho Financial: The bank scored 16 out of 50 on Forests & Finance 2018 policy assessment, as it lacks policies to prohibit clients from violating environmental standards. However, in its updated palm oil, lumber and pulp sector policy in May 2020, the bank states that it takes into consideration whether the client/project has received certification for the production of sustainable palm oil or whether they have been certified for responsible forest management. Strengthening its older policy, the bank added that “In the event that we identify any unlawful act during the term of a transaction, we urge the client to take immediate remedial measures. In the event that the client has not taken appropriate measures to address social issues, we undertake engagement with the client to promote remedial measures and, if the client’s remedial measures are unsatisfactory, we suspend new financing and investment. Further, we urge our clients in these sectors to formulate sustainable environmental policy, such as No Deforestation, No Peat, and No Exploitation (NDPE), and to respect Free, Prior, and Informed Consent (FPIC) in relation to local communities.”

SMBC Group: SMBC Group scored 22 out of 50 on Forests & Finance 2018 policy assessment, as its environmental standards were labeled as reasonable. The bank’s palm oil policy states that support is only provided after confirming certification by the RSPO or an equivalent certifying body. It also requires that forest resources and biodiversity are protected when new plantations are developed and that there are no human rights violations, such as child labor. Regarding deforestation, only illegal deforestation is mentioned, while for large-scale projects, environmental impacts are evaluated in accordance with the Equator Principles when it considers lending.

Kao Corporation and Fuji Oil’s large palm oil purchases expose them to reputation risks

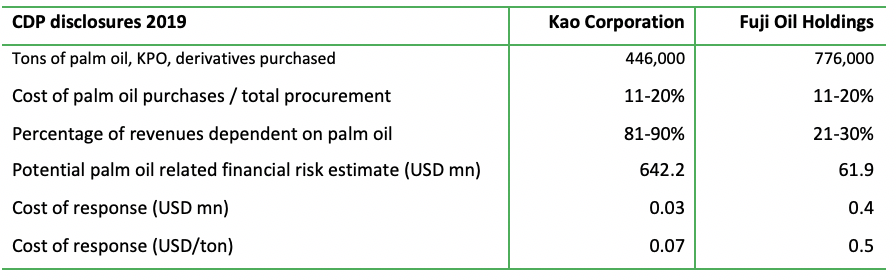

Based on self-reported CDP disclosures for 2019, Kao Corporation and Fuji Oil Holdings’ palm oil purchases were in the range of 11-20 percent of each company’s total procurement, exposing their investors to financial risks in the case of a reputation-damaging event.

Kao Corporation estimates that reputation and market risks stemming from its palm oil supply chain can have a financial impact of JPY 70 billion (approximately USD 642.2 million). The company attaches a high likelihood to such an event. The cost that Kao discloses as a response to this financial risk is JPY 3.6 million (approximately USD 33,000), corresponding to 10 percent of three employees per annum as cost of management work. However, the majority of the cost of response may already be included in the cost of palm oil procurement for Kao since the cost of palm oil (and derivatives) at USD 2,700 per metric ton (calculated based on the information on CDP disclosure for 2019). This is substantially higher than the 2019 market average price of USD 600 per metric ton.

Fuji Oil Holdings sees the risk of a JPY 6.75 billion (approximately USD 61.9 million) financial impact in case of a reputation-damaging event stemming from its palm oil supply chain. Fuji Oil reported JPY 40 million (approximately USD 0.4 million) as cost of response. This includes 1) joint program costs with NGOs, 2) information gathering cost from outside consulting company, and 3) costs for promoting a sustainable palm oil procurement policy, such as supply chain improvement activities and engagement with suppliers. Unlike Kao, Fuji Oil’s calculated palm oil cost for 2019 was lower than the market average at USD 539 per metric ton.

Figure 17: CDP disclosures of Kao and Fuji Oil on palm oil for 2019

Source: CDP Forest disclosures

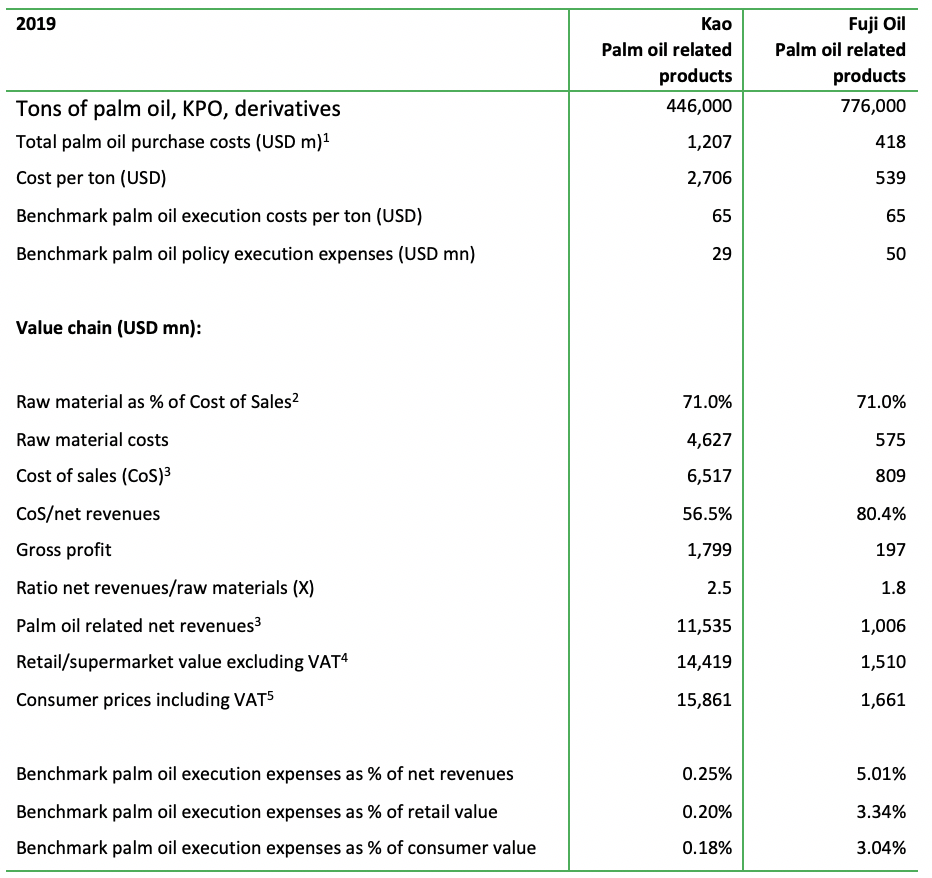

Reputation risk can be minimized with a benchmark execution cost of USD 65/MT

Financiers could focus on engagement on extra spending for monitoring/verification to avoid reputation value loss at Kao and Fuji Oil. Based on the USD 65 per MT benchmark palm oil execution cost and the value chain analysis from CRR’s July 2020 report, the benchmark palm oil policy execution expenses as a percentage of consumer value of palm oil products were 0.18 percent for Kao and 3.04 percent for Fuji Oil. The relatively small extra cost can easily be added to the retail and consumer prices for Kao’s products. With Fuji Oil a comparatively lower-margin B2B business, its business customers would need to increase their product prices by about 3 percent to compensate the extra execution costs. Considering Fuji Oil’s high-margin FMCG, retail, and restaurant customer base and specifically its supply chain relationship with Mars through UniFuji, the extra cost can be distributed in the next two steps of the value chain.

Figure 18: Value chain analysis for Kao and Fuji Oil

Source: Chain Reaction Research, 1CDP 2020, mid-point of 11-20% range of total procurement,2Unilever Annual report FY2019, 3 Annual Report for total company, and CDP for palm oil related sales, 4assuming 20% gross margin supermarkets/food retail for Kao, and 50% gross margin for FMCGs for Fuji Oil, 5assuming 9% VAT food channel

Kao and Fuji Oil may be underestimating financial risks, investors have room to engage

Both Kao Corporation and Fuji Oil Holdings base their financial impact estimates on potential lost revenues from a portion of their clients in case of a reputation-damaging event. Kao estimates that half of its total revenues could be affected and that 10 percent of its customers could change their purchasing behavior over the period of a year, putting approximately 5 percent of revenues at risk. Meanwhile, Fuji Oil assumes 10 percent of total sales could be affected for six months from 45 percent of its clients, amounting to approximately 2 percent of total revenues at risk. For their investors, this market access risk is a direct risk to the value of their investments. Isolating the impact of the lost revenues on the company valuations, Kao and Fuji Oil stocks could lose 5.2 percent and 2.4 percent value, respectively, assuming the same level of profit margins and using current valuation multiples.

However, a May 2019 study by CRR on valuing reputation risks shows that reputation-damaging events can have far more negative effects on company valuations than lost revenues. The methodology from the report suggests that such an event can have anywhere from a 20 percent positive impact to a 29 percent negative impact on company valuations, depending on the success (or lack thereof) of the response. Applying to Kao Corporation and Fuji Oil Holdings, the value at risk from reputation is as high as USD 9.6 billion and USD 0.75 billion, respectively, for the companies’ investors.

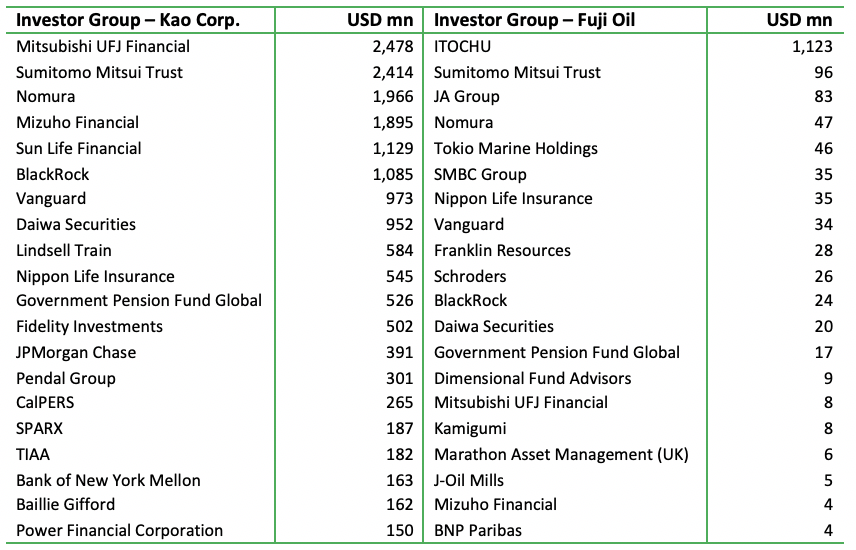

According to most recent filings, 41 percent of Fuji Oil Holdings is owned by ITOCHU and its group companies while Sumitomo Mitsui Trust and JA Group own 4 percent and 3 percent of Fuji Oil, corresponding to USD 96 million and USD 83 million, respectively. Although many international institutions such as Vanguard, Schroders, and BlackRock are also invested in the company, investors have more room for engagement with the controlling shareholder company ITOCHU Corporation. Foreign investors own 35 percent of ITOCHU, according to its website.

Kao Corporation, however, does not have a parent company, and foreign investors own 44.4 percent of the company. On the top investors list, Japanese Banks Mitsubishi UFJ Financial, Sumitomo Mitsui Trust, and Nomura are the largest three investors with USD 2.5 billion, USD 2.4 billion, and USD 2.0 billion, respectively.

Figure 19: Top 20 shareholders of Kao Corporation and Fuji Oil Holdings (USD millions)

Source: Refinitiv (viewed in March 2021), Profundo calculations.