Download Report Here (PDF) | Read TBLA’s response to the report, and our reply

Summary

- An estimated 75 percent of TBLA’s landbank is contested.

- TBLA’s recent peat clearance violates Indonesia’s peat moratorium.

- As a result of non-compliance with clients’ NDPE sourcing policies, 10 percent of TBLA’s revenues are at risk.

Tunas Baru Lampung (TBLA) is an integrated palm oil and sugar cane company established in 1973. It was publicly listed on the Jakarta Stock Exchange in 2000. TBLA is a member of the Sungai Budi Group, which is one of Indonesia’s largest manufacturers and distributers of agricultural consumer products. As of January 2018, 46 percent of the company’s shares were publicly listed. TBLA’s oil palm landbank is estimated at 88,660 hectares (ha), located in South Sumatra and West Kalimantan. In addition, the company converted two plantations – PT Dinamika Graha Sarana and PT Bangun Nusa Indah Lestari – to sugar cane in 2017. TBLA aims to grow its plantations with 2,000- 4,000 ha per year in addition to the 74,060 hectares already developed. The company’s palm oil operations are vertically integrated. Besides its plantations, TBLA possesses three mills, two palm oil refineries, three processing facilities for soap and margarine and one biodiesel plant. Its two refineries are located in Lampung and Sidoarjo. They have processing capacity of 51,000 MT/year and 30,000 MT/year respectively.

|

Key Findings

- An estimated 75 percent of TBLA’s landbank is contested. Since 2014, TBLA has cleared almost 7,000 ha of peatland and forest across its concessions and it has been involved in four reported social conflicts. TBLA’s total oil palm landbank equals 88,660 ha, of which 74,060 ha are already developed and planted with oil palm. The remaining 14,600 ha, 16.5 percent of the total landbank, are still covered with peat, peat forest and forest.

- Several TBLA clients have engaged the company on sustainability issues. The issues raised by TBLA’s clients increase the likelihood of its suspension from the No Deforestation, No Peat, No Exploitation (NDPE) market. As a result, the company could be limited to supplying the ‘palm oil leakage’ market. Whereas its vertically integrated business model allows TBLA to circumvent trader/refiner NDPE policies, its sales to consumer goods companies with zero- deforestation commitments are at risk.

- TBLA’s recent peat clearance violates Indonesia’s peat moratorium. The company faces regulatory risk from these violations at several plantations, in the form of fines, stop-work orders, loss of business permits and operational licenses, and loss of tender eligibility for subsidized biodiesel supply.

- As a result of non-compliance with clients’ NDPE sourcing policies, 10 percent of TBLA’s revenues are at risk. Additionally, TBLA’s violations could result in a 1-year permit freeze resulting in a decrease of eight percent of its revenue. Jointly these negative effects could equal to 26 percent of TBLA’s equity value. The company may also face increased cost of capital in the future.

- To mitigate potential revenue losses, TBLA may opt to restore its peat lands. TBLA might also need to set aside an additional 13 percent of its land for peat restoration. These two changes equals 16 percent of the company’s equity.

Company Profile

Tunas Baru Lampung (TBLA) is an integrated palm oil and sugar cane company that was established in 1973. It was publicly listed on the Jakarta Stock Exchange in 2000. TBLA is a member of the Sungai Budi Group, which is one of Indonesia’s largest manufacturers and distributers of agricultural consumer products. The company’s business activities include manufacturing and distribution of agricultural-based products, such as palm cooking oil, coconut cooking percent derivatives of sugar cane and products.’ The company is vertically integrated with its own plantations, mills and processing/refining capacity.

TBLA has approximately 88,600 ha in its palm oil landbank, located in South Sumatra and West Kalimantan. In addition, the company converted two plantations – PT Dinamika Graha Sarana and PT Bangun Nusa Indah Lestari – to sugar cane in 2017 (24,330 ha).

Besides plantations, TBLA possesses three CPO/PK mills, two palm oil refineries, three processing facilities for soap and margarine and one biodiesel plant. Its two refineries are in Lampung and Sidoarjo with processing capacities of 51,000 MT/year and 30,000 MT/year respectively. TBLA aims to grow its plantations with 2,000-4,000 ha per year in South Sumatra and West Kalimantan.

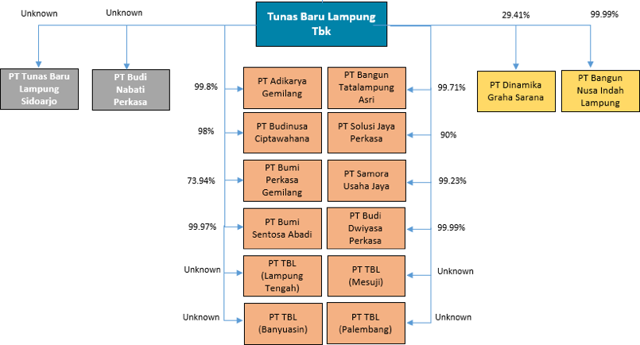

Figure 1: Tunas Baru Lampung corporate structure. Orange = palm oil plantations. Yellow = sugarcane plantations. Grey = refinery. Source: Aidenvironment, TBLA Annual Accounts.

Sustainability Commitments

TBLA has been a member of the RSPO since 2006. Its two refineries are RSPO certified and one CPO mill in Lampung has achieved its initial certification assessment. The company has committed to achieve 100 percent RSPO certification at group level by 2020.

However, TBLA does not have a NDPE policy in place. Its CSR policy commits to the following: ‘we recognize that we must integrate our business values and operations to meet expectations of our stakeholders. They include customers, employees, regulators, investors, suppliers, community and the environment.’ TBLA’s environmental commitments appear to be limited to minimizing its consumption of natural resources and energy, waste reduction and responsible waste management.

TBLA does not have a sustainable sourcing policy. Its two refineries might be a source of non-sustainable palm oil leakage. TBLA’s refinery capacity exceeds that of its three CPO mills. It is likely that the refineries rely on third party CPO supply.

In response to a draft version of this report, TBLA indicated that it operates in accordance with all relevant laws and overall sustainability principles. However, it would not provide further details on these sustainability commitments.

Sustainability Risks

As shown in Table 1 (below), an estimated 75 percent of TBLA’s oil palm landbank is contested because of recent clearings, remaining peat and forest and community land claims. TBLA’s total palm oil landbank amounts to 88,660 ha, of which 74,060 ha have been developed, leaving 16.5 percent undeveloped. All undeveloped land is either peatland, peat forest or forest.

Across its concessions, TBLA has cleared almost 7,000 ha of peatland and forest since 2014. It has been involved in at least four reported social conflicts. Due to ongoing peatland clearing, the company appears to be in breach of Indonesia’s 2016 regulation on the protection of peatland.

|

| PT Tunas Baru Lampung (PKS 2) | Mesuji (Lampung) | N/A | No map available |

| PT Tunas Baru Lampung (PKS 4) | Palembang / Banyuasin (South Sumatra) | 6.985 | Land issues with transmigration communities. |

Table 1: TBLA’s contested landbank. Source: Aidenvironment.

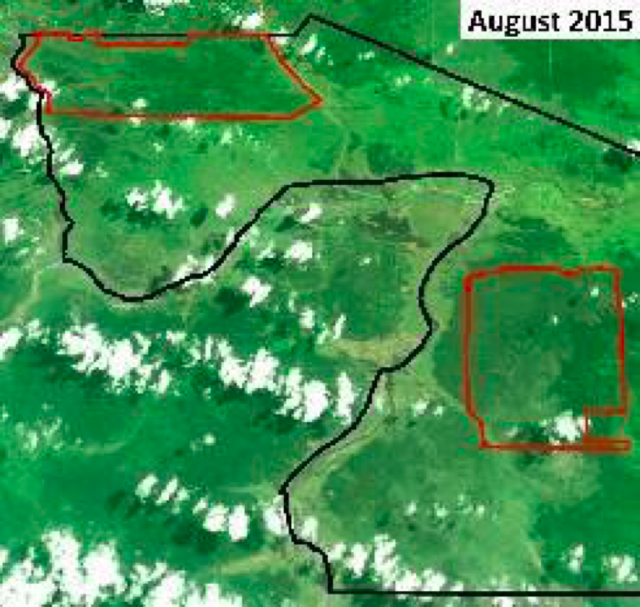

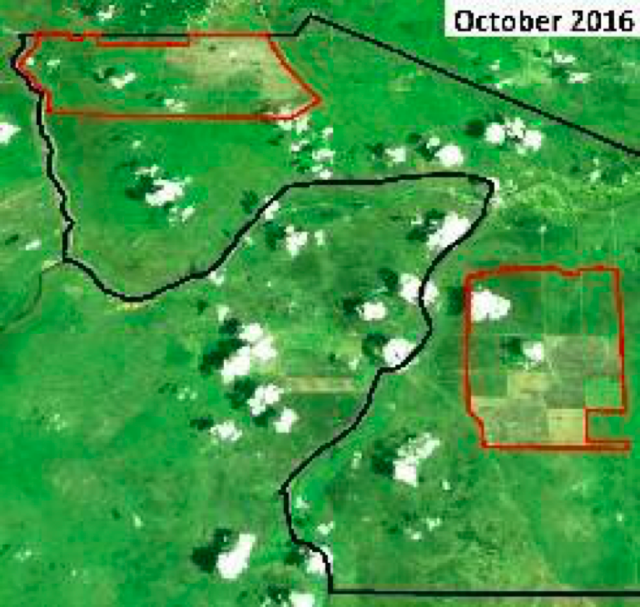

PT Samora Usaha Jaya (SUJ) – peat clearance and ongoing government investigations.

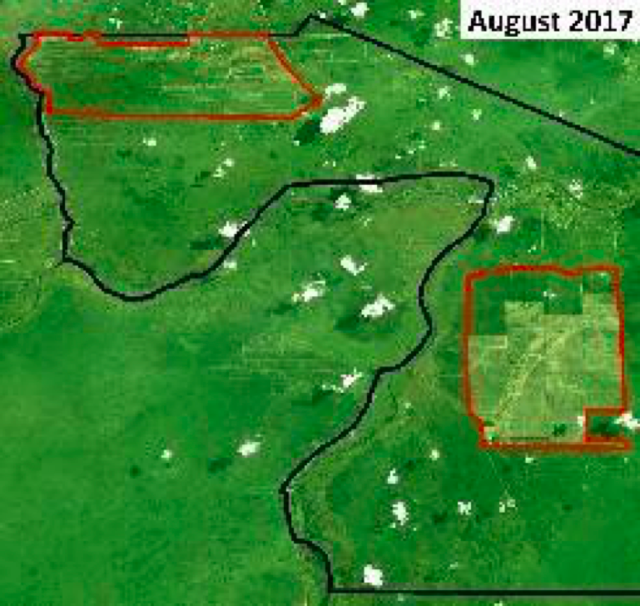

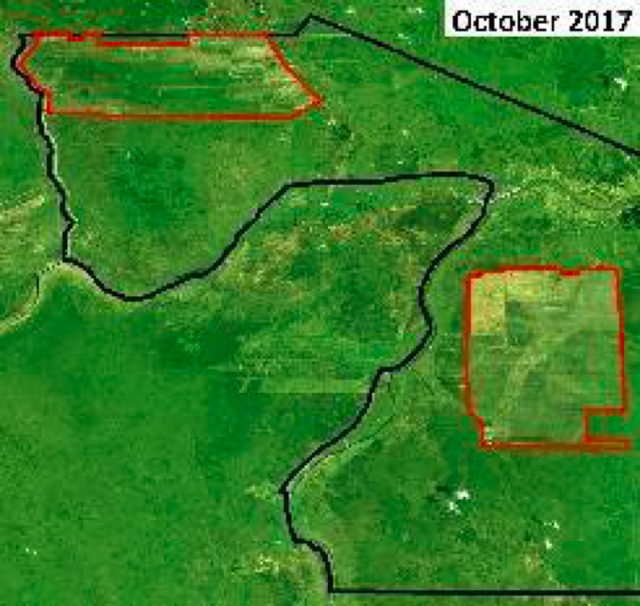

PT SUJ was established in 2013. It is located in three districts in Ogan Komering Ilir Regency, South Sumatra. Based on its location permit, the total area of PT SUJ amounts to 22,565 ha. The entire concession is contested due to ongoing clearings, regulatory issues and social conflicts. As shown in Figure 1 (below), from January 2014 to November 2017, the company cleared 3,200 ha of peat. Since November 2017, no new clearings have been identified. 11,290 ha of peat remain undeveloped.

Figure 2: Peat development in PT SUJ, despite the area being designated as priority for restoration by the Peatland Restoration Agency

PT SUJ is subject to several government investigations:

- In March 2016, the Licensing and Investment Board (BPPM) of Ogan Komering Ilir regency, urged PT SUJ to halt operations. The BBPM’s position was that the company did not have the required Plantation Business Permit (IUP) in place. Further BPPM investigations revealed that the company did not respect the stop-work order.

- In November 2016, the Ministry of Environment and Forestry (KLHK) found that PT SUJ conducted new planting activities in areas that have been designated for restoration by the Peat Restoration Agency (NYSEMKT:BRG), in response to the aftermath of the 2015 fire cases. According to the company, this area does not fall under the peatland moratorium, according to the revised Map for the Deferment of New License Issuance (PIPPIB Map Revision XIII) of the Peat Restoration Agency.

- The original KLHK permit, issued in 2012, designated the concession for the cultivation of sugar cane, yet PT SUJ produces palm oil. According to the company, all planting activities are in accordance with its permits.

In March 2016, local media reported citizen demonstrations against the alleged land grabbing of 800 ha by PT SUJ. According to the article, residents reported the problem to the district’s Land Dispute Settlement officers and the provincial government.

Notwithstanding, PT SUJ continued land development in the contested area. The company states that no grievances over land issues have been filed with the company or the district government.

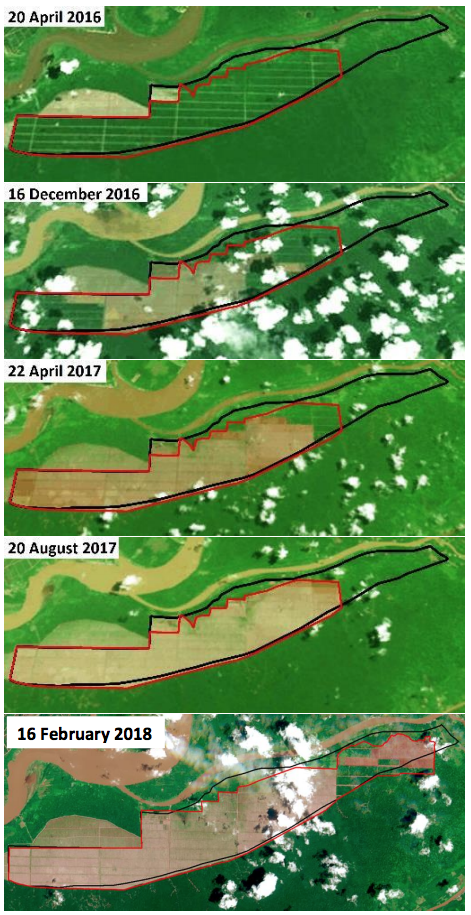

PT Solusi Jaya Perkasa (SJP) – ongoing peat clearing

PT Solusi Jaya Perkasa was incorporated in 2011. It is located in the Kubu Raya district in West Kalimantan. The concession is located east of PT Bumi Perkasa Gemilang and covers an area of 2,940 ha. PT SJP cleared 1,471 ha of peat forest, including 523 ha after December 2016. As shown in Figure 2 and Figure 3 (below), as of January 2018, peat conversion is ongoing. To date, some 787 hectares of peat, peat forest and forest remain. According to the company, this area does not fall under the peatland moratorium for new licenses, as indicated in the revised Map for the Deferment of New License Issuance (PIPPIB Map Revision XIII) of the Peat Restoration Agency. However, the clearings appear to be in violation of the Government of Indonesia’s 2016 peatland regulations.

February 16, 2018

Figure 3: Recent peat forest development in PT SJ

Figure 4: Drone imagery of peat forest development in PT SJP. November 2017.

PT Bumi Perkasa Gemilang (BPG) – peat clearing

PT BPG secured a plantation permit (IUP) in February 2012 for an area of 22,270 ha in Kubu Raya District, West Kalimantan. The PT BPG concession area was predominantly forested peatland. Based on spatial analysis, PT BPG converted approximately 2,000 hectares of peat forest to oil palm estate between early 2014 and September 2017. As shown by the dark lines in Figure 4 (below), high resolution Google Earth imagery suggests that PT BPG drains peatland directly into the Kapuas River, without the legally required dams in place. According to the company, this area does not fall under the peatland moratorium, according to the revised Map for the Deferment of New License Issuance (PIPPIB Map Revision XIII) of the Peat Restoration Agency.

Figure 5: Google Earth imagery of direct peat drainage by PT BPG into Kapuas river, December 2015.

Figure 6: Drone imagery of peat forest development by PT BPG. January 2016. The dark color indicates that the area is made of peat and drained by canals.

PT Adikarya Gemilang (PT AG) – roadblocks by local villagers

PT AG was established in 1995 in Way Kanan Regency, Lampung Province. The plantation covers an area of 2,200 ha. In September 2017, local villagers blocked access to the Adikarya Gemilang plantation for six days to protest their precarious situation. In turn, day laborers protested at the district government, requesting that the issue be solved so that they would be able to go back to work. Their precarious working condition results in income loss for every day that the company does not operate. The road block was lifted in late September 2017.

PT Bangun Tata Lampung Asri (PT BTLA) – land grab accusations

PT BTLA’s concession covers an area of 9,165 ha, located in Mesuji, Lampung, where Dar El Barokah, a local foundation, claims that PT BTLA has grabbed 1,000 ha of land.

According to the foundation’s leader, the land was given to them before the company was established in 1991. A grievance was submitted to the National Land Agency, which confirmed the foundation’s right over the land after a field investigation in March 2017. The conflict has been going on since 1993, and despite the community being in possession of land ownership documents, PT BTLA has not returned the land nor offered compensation. TBLA claims that no legal action has been taken against the company.

PT Tunas Baru Lampung (Banyuasin) – transmigration community complaint

PT Tunas Baru Lampung (Banyuasin; PT TBL)’s total concession area amounts to 6,985 ha. In June 2017, the Transmigration Community Communication Forum (FKTM) argued that PT TBL was in violation of Indonesia’s transmigration law. It filed for a hearing at the Public Accountability Agency (NYSE:BAP) of the Regional Representative Council (DPD),

requesting that PT TBL’s business permit be revised or revoked. The complaint centered around land issues with transmigrant communities, who failed to receive plasma plantations, contrary to agreements with the company. According to the company, this has resulted in a mediation process that has since been concluded. TBL has submitted an official letter to the DPD suggesting that the transmigration community take legal action if there is transmigration land within the plantation.

Business Risks

Market access risks

As reported in its corporate filings, the two largest buyers of TBLA’s palm oil and sugar are its affiliate PT Sungai Budi, and Inter-United Enterprises, a company based in Singapore and owned by the British Virgin Island based Laguna United Ltd. From 2015 to 2017, net sales to PT Sungai Budi almost doubled from 23 percent to 41 percent of TBLA’s revenues and its reliance on external clients decreased from 77 to 59 percent to 43 percent.

| TBLA customers | Parent Company |

| More than 10 percent of TBLA’s total sales | |

| PT Sungai Budi | Sungai Budi |

| Inter United Enterprises | Laguna United Ltd. |

| Less than 10 percent of TBLA’s total sales | |

| PT Perkebunan Nusantara VII | PTPN VII |

| Badan Pengelola Dana

Perkebunan Kelapa Sawit Perkebunan Kelapa Sawit |

|

| PT Harapan Makmur | PT Harapan Makmur |

| PT Sukses Mekar Sawit | PT Sukses Mekar Sawit |

| PT Energi Bahari Lestari | Bumitama Agri Ltd |

| CV Gunung Tambora | CV Gunung Tambora |

| PT Inti Benua Perkasatama | Musim Mas |

| PT Sriwijaya Alam Segar | Wings Group |

| PT Wilmar Nabati Perkasa | Wilmar |

| PT Rezeki Kencana | Tianjin Julong |

| CV Makmur Sentosa | |

| PT Ecogreen Oleo Chemical | Ecogreen Oleochemicals |

| Perum Bulog | Indonesian Bureau of Logistics |

| PT Sintang Raya | Miwon |

| PT Ivomas Tunggal | Sinar Mas |

| PT Aneka Kimia Raya | AKR Corporindo Tbk |

| PT Pundi Lahan Khatulistiwa | Pundi Lahan Khatulistiwa |

| Nestle Oil Singapore Pte. Ltd. | Nestlé |

| Multi Commodity International | Multi Commodity International Ltd |

| Peter Cremer Holdings | Peter Cremer Holdings GmbH & Co |

| Zara General Trading Limitada | Zara General Trading |

| Perissos Development and Investment Lda. | Perissos Development and Investment LDA |

| Franco Asian Enterprises Singapore Ltd | Franco Asian Enterprises Singapore Ltd |

| Aba Corp Ltd | Aba Corp Ltd |

Table 2: TBLA customers. Source: TBLA Q3/2017 financial report.

As shown in Table 2 (above), the company mainly serves the Indonesian market but also exports to African, Asia-Pacific and European destinations.

TBLA’s ongoing peatland and forest clearing at its PT SUJ, PT SJP and PT BPG plantations constitute violations of the NDPE policies of at least 6 of its buyers. At least five identified clients have NDPE policies. Several buyers have already engaged with TBLA in response to Chain Reaction Research’s sustainability benchmark.

|

Table 3: TBLA’s Average Annual Sales by Market. Source: TBLA Q3/2017 financial report.

- Golden Agri-Resources engaged with TBLA in February 2017 and recommended the company conduct a soil study for its PT SUJ concession, offer the results of that study to Indonesia’s Peat Restoration Agency and temporarily halt further development of the concession until the verification process was complete.

- Musim Mas engaged with TBLA in January 2017 and applied ‘controlled purchase’ on the mills that supply Musim Mas. In August 2017, Musim Mas reported that it no longer purchased from TBLA’s mills in South Sumatra nor had a business relation with PT SUJ.

- Wilmar reports engagements with TBLA in October 2016, and January and May 2017.

In addition, TBLA’s customers include a number of other clients with NDPE policies, including ADM, Nestlé and Bumitama. Given the repeat offenses of their NDPE policies, TBLA’s access to these buyers is at significant risk.

Furthermore, the previously discussed media reports about social conflicts at PT SUJ, PT AG and PT BTLA signify that TBLA might also be in violation of the ‘No Exploitation’ provisions of its buyers’ NDPE policies.

Regulatory risks

TBLA’s subsidiaries PT SUJ, PT TBL and possibly PT BTLA are exposed to legal compliance risks and could face sanctions by regulatory agencies. Furthermore, TBLA’s multiple peat clearings constitute a violation of Indonesia’s 2016 regulation on the protection of peatland. This could materialize in fines, stop-work orders and the

revoking of business permits and concession licenses. It could also jeopardize TBLA’s eligibility for tenders to supply subsidized biodiesel to Pertamina, Indonesia’s state- owned oil company. This risk is present for 63,925 ha of TBLA’s landbank.

Operational risks

Finally, the six days strike reported at PT AG could signify underlying tensions that might result in future strikes and blockades. Further obstruction of the company’s operations might be expected.

Financial Analysis

TBLA’s market cap is USD 476 million (IDR 6.4 trillion), which positions it as a medium- sized company. It supplies less than 0.01 percent of the global CPO market.

Tunas Baru Lampung faces four key financial issues

- How would Tunas Baru Lampung be affected if buyers/customers react to Tunas Baru Lampung’s sustainability and deforestation violations?

- Are the potentially-stranded assets substantial in size, and could this impact the value of the company significantly?

- Who is financing Tunas Baru Lampung’s debt and equity, and how will non- compliance related to deforestation impact this?

- How much of the value of debt and equity could be affected by the impacts of deforestation incompliance or by the impact of ‘stranded land’, i.e. land owned by Tunas Baru Lampung that will not be taken into production?

Recent financial performance

As shown in Table 4 (below), the company is experiencing growth. In 2016, total revenue was USD 484 million, up 25 percent vs 2015. Operating profit in 2016 was 87 percent up y-o-y (in USD), reaching USD 82 million. Average selling price increased 17 percent vs 2015. For 2017, (due to lack of published results), the consensus estimated revenue and operating profit are also expected considerably higher than in prior years,

i.e. at USD 637 million and USD 110 million respectively. In Q317, the company’s revenue was 44 percent up vs the same quarter in 2016, while operating profit was up 65 percent. The consensus expected revenue growth for 2017 of 30 percent vs 2016. The projection is more modest for 2018, with expectations for 8 percent revenue growth. This may be considerably reduced if the company losses access to the NDPE market.

| USD million | 2013 | 2014 | 2015 | 2016 | 2017E | 2018E | CAGR

‘17-‘13 |

| Revenue | 304.7 | 511.9 | 386.8 | 483.6 | 637.1 | 685.9 | 20% |

| EBITDA | 54.9 | 82.0 | 59.7 | 103.5 | 150.8 | 165.1 | 29% |

| Operating profit/EBIT | 40.7 | 64.2 | 43.8 | 82.0 | 110.0 | 130.0 | 28% |

| Net Profit | 6.9 | 35.0 | 14.3 | 45.7 | 71.3 | 80.72 | 79% |

| EPS (NYSEARCA:USD) | 0.01 | 0.00 | 0.01 | 0.00 | 0.01 | 0.01 | 0% |

| Free Cash Flow | – | – | -4.7 | -119.1 | -86.4 | 38.2 | 330% |

Table 4: Key TBLA Financial Figures. Source: Thomson Reuters, consensus estimates, Chain Reaction Research.

35 percent of the company’s revenue is generated by its sugar segment, approximately the same by palm cooking oil, and the rest comes mainly from refined palm oil products (and some sugar). 41 percent of TBLA’s sales go to a related party (Sungai Budi). As of Q3 2017, another major buyer with 15 percent of sales is a Singaporean company,

Inter-United Enterprises. On one hand, TBLA has grown increasingly reliant on those two parties. On the other hand, there is little revenue at risk, as it can be assumed that TBLA may find a selling route within the group of companies under Sungai Budi. The lack of transparency on internal pricing, however, is likely one of the drivers of the company’s share price underperformance.

The margins are showing some efficiency gains, but likely to slow down

As shown in Table 5 (below), TBLA’s gross profit margin, which went from 22 percent in 2015 to 25 percent in 2016, remained slightly above 25 percent in the first three quarters of 2017. Both gross and net margin will increase in 2017E, and according to the consensus estimates are likely to be maintained in 2018.

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017E | 2018E | |

| Gross Profit | 27.0% | 25.6% | 20.4% | 22.0% | 25.0% | 24.8% | 27.2% |

| Cost of Revenue | 73.0% | 74.4% | 79.6% | 78.1% | 75.1% | 75.2% | 72.8% |

| SGnA | 13.8% | 12.1% | 7.6% | 10.4% | 7.2% | 6.1% | 8.7% |

| Op. Expense | 86.9% | 86.7% | 87.5% | 88.7% | 83.1% | 81.8% | 81.5% |

| EBITDA Margin | 17.0% | 18.0% | 16.0% | 15.0% | 21.0% | 23.0% | 24.0% |

| O. Income | 13.1% | 13.3% | 12.6% | 11.3% | 17.0% | 18.2% | 18.5% |

| Net Income | 6.4% | 2.3% | 6.8% | 3.7% | 9.5% | 10.7% | 11.8% |

Table 5: Key TBLA Margins. Source: Thomson Reuters, consensus estimates, Chain Reaction Research.

Stock performance and valuation

As shown in Table 6 (below), since reaching an all-time high on May 31, 2017, the stock lost 24 percent till Feb 23, 2018, in line with lower quarterly reported EPS (EPS was declining each quarter, almost at the same pace as the share price). Despite that, the company has received three strong buy recommendations and has a price target mean of IDR 2,033, which is 70 percent higher than its current price.

| 23-02-2018,

USD total return |

1Y return | 2Y return | 31-05-2017 until

23-02-2018 |

| TBLA | 1% | 150% | -24% |

| JKAGRI | -12% | -7% | -12% |

| BB SGG | -11% | 10% | 1% |

Table 6: TBLA Equity Performance. Source: Thomson Reuters.

While EPS was declining (counter to the palm oil production seasonality), the operating profit has been increasing. The discrepancy was caused by increased financing costs related to capex investments. Historically, such trends were followed by a share price increase already a few quarters later, as new assets are anticipated to become productive and cash flow stabilized. Now, however, this may not be the case. An explanation might be that the key business segment of the company, palm oil, is left without any legal growth prospects and may require new capital expenditure to maintain the company’s performance. Lower global sugar prices might also have had an impact.

| Relative valuation using consensus estimates

Share price, Feb 23 2018, USD 0.08 |

P/E (x) | EV/EBITDA

(x) |

EV/Revenue

(x) (select peers) |

Equal weighted fair value USD |

| TBLA as of 18.01.2018 | 5.7 | 6.6 | 1.5 | |

| Own hist avg since Dec 2012 | 12.3 | 7.1 | 1.3 | |

| Peer average forward 2018 | ` 16.2 | 12.0 | 1.4 | |

| Fair value in USD | ||||

| Fair value with own 5Y hist avg | 0.19 | 0.14 | 0.08 | 0.14 |

| Fair value with peer avg | 0.25 | 0.30 | 0.09 | 0.21 |

| Share price vs fair value in % | ||||

| Fair value with own 5Y hist avg | -138% | -75% | 0% | -71% |

| Fair value with peer avg | -213% | -275% | -13% | -167% |

Table 7: TBLA Relative Valuation. Source: Thomson Reuters. Peer group is a mix of palm oil and sugar companies, total number 30; select peer group is 8.

As shown in Table 7 (above), in USD terms, TBLA is currently trading at USD 0.08, while there is a consensus estimate upside of 70 percent. This is predominantly driven by the company’s low relative peer valuation. Its 2018 expected Price/Earnings ratio is 5.7x vs a peer average of 16x. The company is also trading below its own historical average P/E. The same trend is confirmed by the 2018 forward EV/EBITDA of 6.6x vs expected peers’ 7.1x. EV/Revenue is also lagging. The market is substantially discounting TBLA’s share price, for several possible reasons:

- The lack of transparency of internal pricing to its majority shareholder, i.e. is it selling its products at the optimum market price?

- It is majority owned by two individuals

- It has not generated positive free cash flow in 2015-2017E

- It is more leveraged (relatively more debt) than its peers (including sugar peers)

In relation to NDPE, the company may be facing further valuation impairments, which are described in separate scenarios below.

NDPE violations can suppress TBLA’s financial and share price performance

Given the company’s attitude to the near industry-norm NDPE, TBLA is probably exposed to significant risk of lost revenue from unrelated parties. There is also a high chance that TBLA has to regenerate 7,000 ha of peatland recently cleared in violation of NDPE and peat moratorium. The company’s remaining palm oil land of 14,600 ha is likely to become stranded. Its permit on 30,000 ha, more than half its productive land, may be frozen for a year due to regulatory violations. Each of these scenarios/impacts is reviewed in detail below.

Financial risk 1: NDPE driven revenue loss -10 percent, i.e. 24 percent of equity

This is a high likelihood scenario, merited by the fact that several of its customers have committed to NDPE policies. The table on page 9 shows a list of some of TBLA’s direct identified customers, five of which adhere to higher sustainability standards than TBLA itself. No quantitative data was found as to how much each one is purchasing.

However, based on the company’s reported accounts receivable, it can be reasonably assumed that on average each of the unrelated NSPE customers buys around 2 percent of TBLA’s revenue. Thus, based on the identified names, as much as 10 percent of the company’s revenue is at risk. It is possible, that the company loses more than that due to indirect customers have NDPE commitments. Alternatively, it could find replacement buyers without NDPE policies standards and thus supply the shrinking leakage market.

As shown in Table 8 (below)he current consensus estimates for TBLA’s 2018 revenue is at USD 686 million. In the event that it does lose customers and its revenues drops 10 percent to USD 617 million, the company’s EBITDA and net earnings would also be impaired to USD 149 million and USD 72 million. EPS would also decline by 10 percent.

| Basic P&L proforma estimates, USD million | Consensus scenario | Risk 1: Revenue loss 10

percent |

| Revenue | 686 | 617 |

| EBITDA | 165 | 149 |

| Net Income | 81 | 73 |

| Nr shares | 5,342 | 5,342 |

| EPS | 0.02 | 0.01 |

Table 8: Key financial figures; Scenario 1 proforma estimates. Source: Thomson Reuters, Chain Reaction Research.

As shown in Table 9 (below) if the stock price continues to closely follow the EPS as in 2017, a 10 percent decline in profit could ultimately reduce its equity value by 8 to 10 percent. Assuming that the EBITDA loss of USD 16.5 million is a good proxy of free cash flows which will not be recovered in the mid-term, and using a WACC of 10.5 percent, leads to a DCF value of the lost revenue of USD 116 million. This is equal to 24 percent of TBLA’s equity value and to 12 percent of its enterprise value. Even if the stock fails to respond directly, then its relative upside potential will be reduced from 71 percent to 51 percent. Using EV/Revenue as a relative valuation multiple shows that the stock’s upside potential can be even completely destroyed in the event of a 10 percent revenue loss. Nevertheless, valuation in line with peers is highly unlikely as the company has never attained it before.

| Relative valuation in USD using equal weighted fair value estimates of EV/EBITDA, P/E and EV/Revenue | Consensus scenario | Risk 1: Revenue loss 10 percent | Difference with Consensus |

| Own historical fair value premium | 71 % | 51 % | -28 % |

| In line with peers fair value premium | 167 % | 135% | -19% |

| Net debt/EBITDA | 2.5x | 2.7x | 11 % |

| Net debt/EBITDA peers | 1.6x | 1.6x | 0 % |

Table 9: Relative valuation, Scenario 1. Source: Thomson Reuters, Chain Reaction Research.

In either case, however, TBLA remains more leveraged compared to its peers. In the consensus estimates for 2018, its Net Debt / EBITDA is 2.5x, which is 27 percent higher than the peer average. If the company loses 10 percent revenue, this multiple is likely to rise to 2.7x, continuing to suppress the share price.

Financial risk 2: 1Y permit freeze on 27 percent land, equals 2 percent of equity

The regulatory risks which TBLA is facing concern two of its subsidiaries: PT SUJ and PT TBL. They jointly hold 30,000 ha land, of which 18,260 is developed. It is possible that the permits on these concessions could be temporarily suspended while the company resolves the conflicts pertaining to this land. If this freeze lasts for 1 year, the company would not be able to generate any profits from the developed part. Using the same assumptions as above (4.5 CPO tons per ha at USD 650/ton, cost rate at 80%) shows that this permit freeze could cost TBLA USD 11 million in free cash flows, which equals 2% of its equity value.

Financial risk 3: Peat land restoration expense equal to 4 percent of equity value

There is already precedent of companies (Felda and Abdi Budi Mulia) restoring lands in order to keep their market access. Therefore, it is possible that the threat of NDPE- related revenue loss becomes an incentive for TBLA’s to restore the recently cleared 7,000 ha peat land. Using a conservative restoration cost of USD 2,500 per ha, this could cost it USD 17.5 million, or 11 percent off its expected 2018 EBITDA. This would also result in a Net Profit reduction by USD 8 million and it represents 4 percent of equity value.

Financial risk 4: Stranded land equal to 12 percent equity

All the remaining undeveloped oil palm land of TBLA, or 14,600 ha equalling c.13% of the company’s total, would likely become stranded if the company complies with the Indonesian peat moratorium. As for agri-companies like TBLA land assets are

substantial drivers of firm value, writing off this land would lower that value. Assuming that each hectare can produce 4.5 tons CPO per ha at USD 650/ton revenue and apply a cost rate including capex of 80%, then the estimated DCF value of this land is USD 60 million (with WACC assumption at 10.5 percent). This equals 12 percent of the company’s equity value and 6 percent of its enterprise value.

Capital structure

As shown in Table 10 (below), it is noticeable that the company is 53 percent equity funded, the rest being debt. In December 2017 and January 2018, TBLA issued new bonds to refinance bank loans to Maybank Indonesia, Bank CIMB Niaga, Bank OCBC NISP and Bank Rakyat Indonesia. The January-2018- issued bonds USD 200 million were rated BB- and Ba3 by Fitch and Moody’s, considerably lower than previous issuances. 98 percent of the issue was allocated to Asian investors, while only 2 percent were international. Including these latest bond issues, an estimated 50% of total debt is in bonds, the other half being bank credit lines.

|

Table 10: Capital Structure. Source: Thomson Reuters, Chain Reaction Research.

The company’s debt may become more expensive because of poor collateral. More than half of that debt is secured by collateral. 60 percent of TBL’s inventories and more than 50 percent of the oil palm plantations were pledged as security. It is possible that this collateral is even less valuable than expected. The collateral plantations may be either recently deforested, or completely undevelopable because they are covered with peat.

The average interest rate TBLA has managed to secure on its fixed and floating loans has gradually decreased for the past 3 fiscal years, contributing to its stronger net margin performance. TBLA reached levels of 9.5 percent to 12 percent on IDR floating and 4.5 percent – 5.8 percent USD floating rate as of Q3 2017. This, however, may change because of collateral devaluation. It could drive cost of debt higher, which in turn could even reduce the net profit margin.

As shown in Table 11 (below), the poor collateral and worsening leverage metrics together with substantial NDPE violations are likely to impact the financing relations of TBLA with its investors. Almost all of its creditors are scored in the Forest 500 and are aware of the ongoing industry transition towards NDPE. Thus, it is likely that they will engage with TBLA and raise the costs of debt due to the lowered value of their collateral.

| Bank | USD million | Forest 500 (max 5*) |

| PT Bank Rakyat Indonesia | 138.31 | ** |

| PT Bank Maybank Indonesia | 84.48 | * |

| PT Bank Mandiri | 72.55 | * |

| PT Bank OCBC NISP | 29.23 | * |

| PT Bank CIMB Niaga | 21.85 | * |

| PT Bank UOB Indonesia | 20.08 | ** |

| PT Bank Negara Indonesia | 19.17 | * |

| PT Bank Permata | 8.70 |

Table 11: Creditors as of September 2017. Source: TBLA quarterly reports, Forest 500.

As shown in Table 12 (below), TBLA’s equity investors may also be alarmed by the negative financial impacts which the company can suffer. HSBC as its 4thlargest equity holder, with a 1.2 percent stake has achieved 4 stars in the Forest 500 ranking and is thus highly likely to either engage with TBLA or divest. HSBC, together with a few other international investors may exert pressure on the stock regarding its NDPE violations.

| Major Shareholders | As of | %

holdings |

Forest 500 |

| PT Budi Delta Swakarya | 30-09-2017 | 26.21 % | |

| PT Sungai Budi | 30-09-2017 | 25.04 % | |

| Dimensional Fund Advisors, L.P. | 30-11-2017 | 1.39 % | 0 |

| HSBC Global Asset Management (Hong Kong) Limited | 30-11-2017 | 1.20 % | **** |

| FIL Investment Management (Singapore) Ltd. | 30-11-2017 | 0.96 % | |

| Pheim Asset Management (Asia) Pte. Ltd. | 30-09-2016 | 0.31 % | |

| BlackRock Institutional Trust Company, N.A. | 31-12-2017 | 0.21 % | * |

| Daiwa Asset Management Co., Ltd. | 31-08-2017 | 0.08 % | |

| Astmax Asset Management, Inc. | 30-11-2016 | 0.07 % | |

| Widarto | 30-09-2017 | 0.04 % | |

| Winata (Santoso) | 30-09-2017 | 0.04 % | |

| S.E.A. Asset Management Singapore Pte. Ltd. | 30-11-2017 | 0.04 % | |

| Nuveen LLC | 30-11-2017 | 0.04 % | |

| BlackRock Advisors (NASDAQ:UK) Limited | 31-12-2017 | 0.03 % | * |

| Pheim Asset Management Sdn. Bhd. | 30-06-2017 | 0.03 % |

Table 12: Most Recent Equity Holders. Source: Thomson Reuters, Forest 500.

As of 21st of February 2018, the bondholders of the latest bond issuances were unknown (likely because the quarterly holding reports are still upcoming).

Conclusion: Material equity value risk

The company may be facing a trade-off: lose 10 percent of revenue and risk having the permit frozen on the land generating another 8 percent, both totaling 26 percent of equity value; or to recognize stranded assets and restore land, jointly equal to 16 percent of equity value. The first scenario is very destructive to equity price, while the second could let TBLA regain access to the NDPE market and help avoid prolonged revenue loss.

[…] are three other notable deforesters. All three have recently been covered in CRR reports due to deforestation on their plantations or the methods they have used to publicly disassociate themselves from […]

[…] Austindo Nusantara Jaya and Sawit Sumbermas Sarana. CRR has previously covered deforestation and peat clearance issues on their plantations. Austindo Nusantara Jaya was the first company known to have violated […]

[…] has previously covered deforestation on Tunas Baru Lampung’s concessions. In 2019, approximately 1,500 ha have […]

[…] has previously covered Tunas Baru Lampung because of widespread peat and forest clearance. After being suspended by […]