This Chain is part of a series on how COVID-19 is affecting agricultural markets and investor flows.

The global biodiesel market has taken major hits from weaker demand, a sharp drop in crude oil prices, and growing palm oil oversupply. The decline in transportation demand as the novel coronavirus has forced global travel to pause has cut into use of biofuels derived from palm oil, a major blow to the industry. At the same time, crude prices in the United States turned negative for the first time in history, making biofuels markets less attractive. This combination has led to a large glut of biofuels, which could amount to a substantial surplus for an extended period of time.

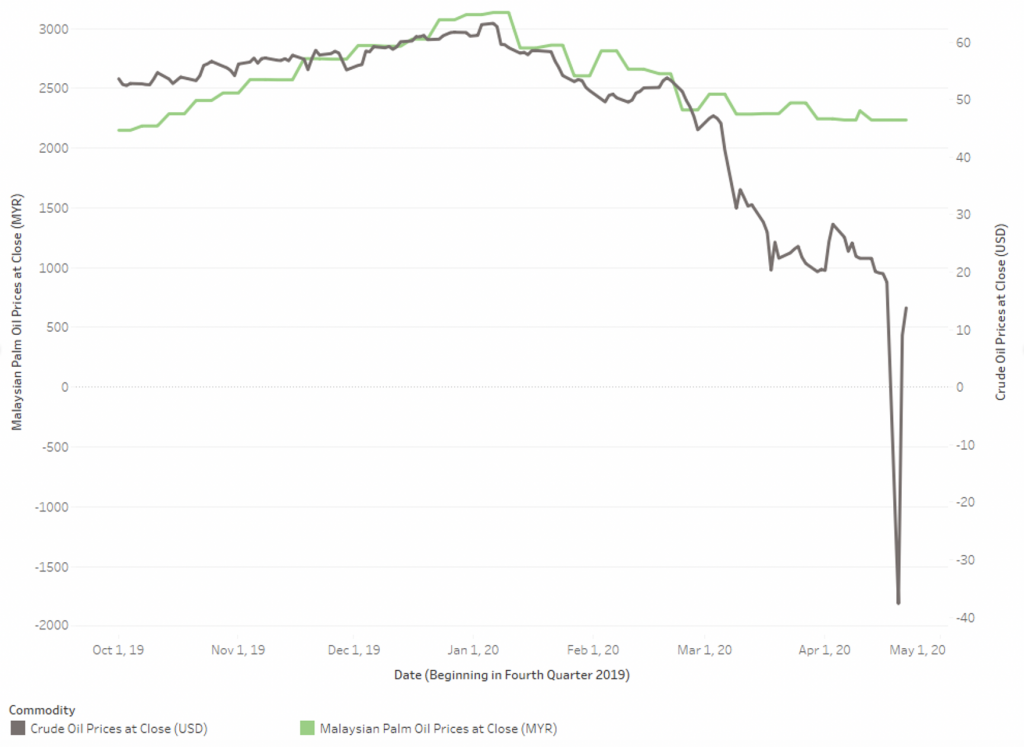

U.S. crude oil benchmark West Texas Intermediate fell to almost USD 40 per barrel below zero on April 20, 2020, pulling down global petroleum and palm oil prices. Though prices have rebounded, they are about 80 percent below year-ago levels. Palm oil futures in Malaysia, meanwhile, fell to their lowest level in nine months and are down by more than 30 percent from their peak earlier this year.

Figure 1: Malaysian Crude Palm Oil Prices and U.S. Crude Prices Since Q4 2019

Sources: Eikon, CME Group, Bursa Malaysia. Note: Crude oil price is per barrel and CPO price is per metric tonne.

The biofuel market was anticipating major shake-ups this year, which were supposed to help the palm oil industry by increasing demand for biodiesel derived from palm oil. Starting in January, Indonesia increased the mandated diesel and crude palm oil blend to 30 percent (B30), up from 20 percent. This was expected to increase consumption of palm-oil based biofuels in Indonesia by 45 percent to as high as 9 million kiloliters. But recent events will instead likely offset efforts by the Indonesian and Malaysian governments to stimulate the use of biodiesel in order to support the palm oil industry at a time when global demand is declining. Sustainability requirements for biofuel production have not been established alongside government moves to increase domestic demand. This could lead to increased pressure on land use for oil palm, while also expanding the leakage market for growers and refiners that do not comply with No Deforestation, No Peat, No Exploitation (NDPE) policies.

Prior to the drop in demand brought on by COVID-19, many major palm oil growers, traders and refiners had seen the Indonesian biofuel market as one of the most significant growth opportunities for the sector. Besides government support, changes in aviation and the shipping industry to shift away from fossil fuels to lower carbon alternatives were expected to increase the use of biodiesel made from palm oil. But higher demand has not been realized due to the economic shock from COVID-19. These market conditions may continue to undermine the government’s efforts to support the industry.

In addition to recent developments, the industry has to contend with longer-term, structural declines in demand in various markets. France will discontinue biofuel tax breaks for palm oil starting January 1, 2020. France’s move has been followed by EU aspirations to reduce palm oil-based biofuels. Not including palm oil in the EU renewable energy target is expected to accelerate phase-out of the fuel’s use in Europe. EU’s target to reduce palm oil exposure will shift Southeast Asian producers to increase reliance on markets which have weaker stringent sustainability standards, such as China and India, the two largest palm oil importers. However, these markets are importing significantly less amid COVID-19. For instance, in January, before the World Health Organization (WHO) labeled the coronavirus a pandemic, China imports from Indonesia were down by 57 percent, while Indian imports are forecast to fall this year.

With the combination of the current price downturn and the enormous impact of COVID-19 on the economies of developing markets like Indonesia, corporate investment strategies may devote fewer resources to reducing deforestation risks, while local governments may turn a blind eye to unsustainable practices. As a consequence, investors in companies active in biofuels could be confronted with increasing deforestation risks and could demand a much stronger verification of the palm oil supply chain. Otherwise, these companies and their investors are likely to be confronted with financial losses, including reputation loss, when markets return to normal.

[…] move would also come at a time when the global biodiesel market has taken major hits from weaker demand, a sharp drop in crude oil prices, and growing palm oil […]