This report discusses the traceability requirement of the new EU regulation on deforestation-free products and the feasibility of its implementation in cattle and soy supply chains in Brazil. Traceability is crucial to ensure that commodity production is not linked to deforestation or forest degradation.

Download the PDF here: EU Deforestation Law_Traceability Viable in Brazilian Beef and Soy Supply Chains

WATCH THE WEBINAR FOR THIS REPORT

Key Findings

- The EU is a significant importer of soy, leather, and beef products, mainly from Brazil, that are covered by the EU Deforestation Regulation. In 2021, the EU imported 32 million metric tons (EUR 13.9 billion) of soy products and 739,000 metric tons (EUR 3.2 billion) of beef and leather products.

- Existing systems and tools provide feasible options to expand traceability in cattle supply chains to include the crucial indirect suppliers. Although the fragmentation of the Brazilian cattle supply chain poses challenges to full traceability, using available systems and tools that can trace cattle beyond slaughterhouses and direct suppliers makes it possible.

- Full traceability of Brazilian soy supply chains is possible and is already part of existing sector agreements. The Amazon Soy Moratorium already lays much of the groundwork required by the EU Regulation in terms of traceability. Nonetheless, challenges still exist, such as coverage of all indirect supply and extension of traceability efforts to other biomes, such as the Cerrado.

- Market leakage and segregation can be avoided while implementation costs will likely become negligible over time. As long as traceability to the plot of land is ensured, segregation is not required. Market players can avoid leakage by making traceability a default component of the management of both cattle and soy supply chains, no matter the destination market.

- Traceability may play a role in supply shortages while also creating legal and reputational risks for operators, traders, and downstream actors. The implementation of the EU Law can hamper operators’ supply capacity. In addition, failing to comply with the EU Regulation’s requirements may lead to legal and reputational damage for operators, FMCG companies, and retailers.

- Costs of compliance are relatively low for downstream actors. They generate high profits on embedded soy and beef and would be able to prevent reputation damage. While still excluded from the Regulation, banks and investors face reputation and investment risk when assets do not comply with the EU Law.

The EU is a significant importer of cattle and soy products from Brazil

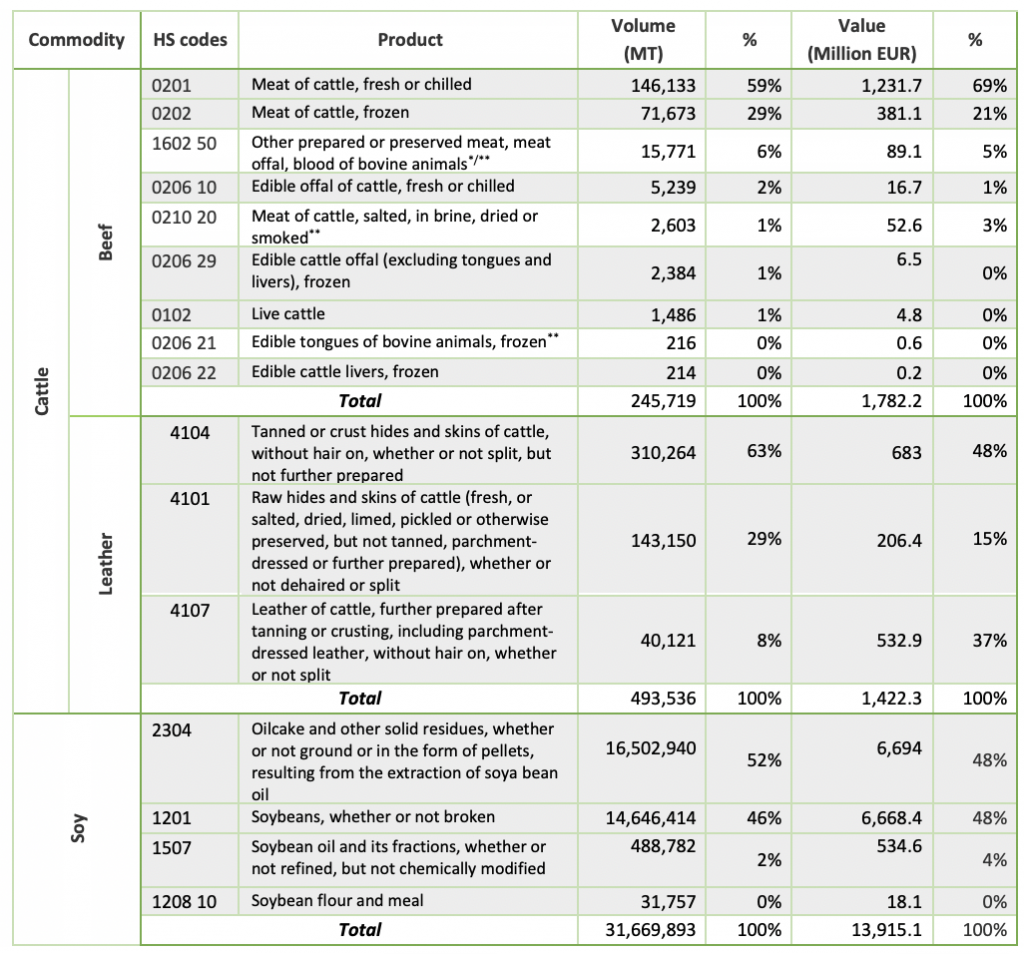

The European Union (EU) imported 739,000 metric tons (MT) of beef and leather products, as well as about 32 million MT of soy and soy derivatives from non-EU countries in 2021. Fresh or chilled meat of cattle represents the largest share of beef products imported in the EU27 while tanned or crust hides and skins were the most imported leather product (Figure 1). As for soy, oilcake and other solid residues is the most imported soy product in the EU27 in terms of volume, closely followed by soybeans.

Figure 1: Total 2021 EU imports of beef and soy products from non-EU countries by volume and value

Source: EU27 trade statistics, 2021 (consulted in August 2022); European Commission’s draft proposal; Council of the EU’s opinion; and European Parliament’s draft report. Notes: These products represent all possible cattle and soy related products under the scope of the EU Deforestation Regulation. In grey, the commodity products from the original proposal by the European Commission, * Suggested addition by the Council; ** Suggested addition by the European Parliament.

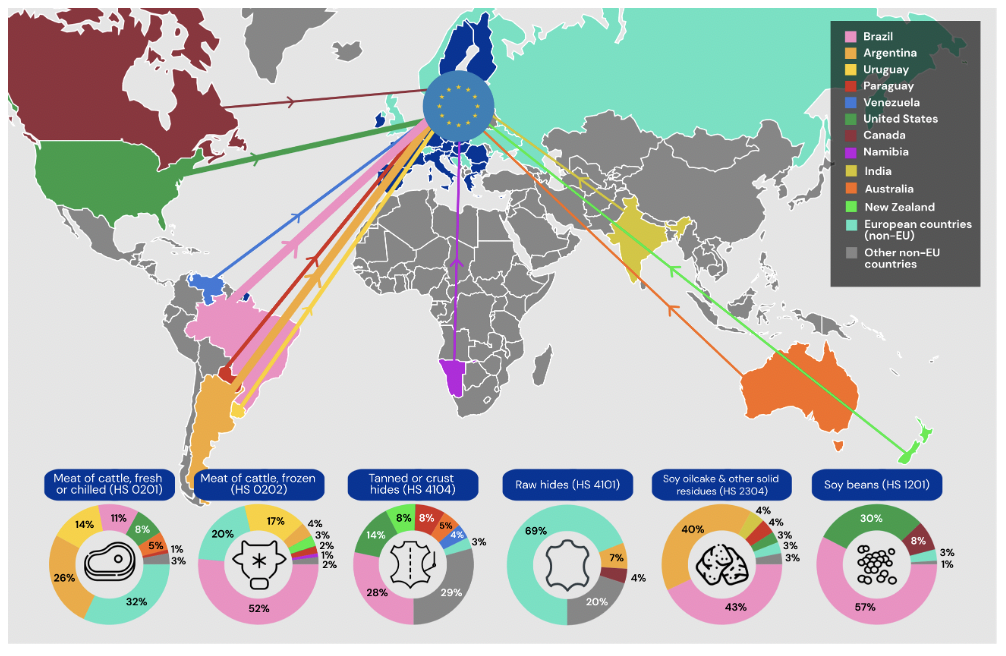

Figure 2: Top-7 non-EU suppliers of the most imported beef, leather, and soy products (by volume) in the EU

Source: AidEnvironment, based on EU27 trade statistics 2021 (consulted in August 2022). The category “European countries (non-EU)” compounds the European countries that were part of the top-7 EU supplier countries for at least one of the products displayed. The countries included here are, specifically, the United Kingdom, Norway, Ukraine, Serbia, Bosnia and Herzegovina, Switzerland, and Russia. The category “Other non-EU countries” includes all the remaining countries that are not part of the EU.

By volume, Brazil, Argentina, Paraguay, and Uruguay are among the largest suppliers of beef, leather, and soy products to the EU. European countries are the largest non-EU exporters of fresh and chilled beef, in volume, to the EU market in 2021 (Fig. 2). They are closely followed by Argentina, which was in fact the largest non-EU exporter of fresh and chilled beef in terms of value in the same period. As for frozen beef, Brazil was, by far, the largest exporter country to the European bloc (Fig. 2), followed by European countries, Uruguay, and Argentina. Tanned or crust bovine hides and skins are the most imported leather product to the EU, the largest share of which came from Brazil (also the largest exporter of bovine leather to the EU), followed by the US, New Zealand, and Paraguay. Concerning soy, Brazil leads the ranking of EU imports for the two most imported soy products (oilcake and soybeans). More than 80 percent of the EU soy oilcake imports came from Brazil, Argentina, and Paraguay.

Brazil will be most affected by stricter EU import restrictions for cattle and soy products under the Deforestation Regulation. In 2021, Brazil was the largest supplier of several of the soy, leather, and beef products that are to be covered by the EU Deforestation Regulation (Figure 2). The production and processing of these commodities and products in Brazil is a known threat to the country’s tropical forest and savannah as it is a leading cause of deforestation, forest degradation, and native vegetation suppression. Soy and beef are two of the commodities with the largest embedded tropical deforestation imported into the EU. In 2016, 77 percent of the deforestation associated with soy imported into the EU originated from Brazil, namely from the Cerrado (70 percent) and the Amazon (7 percent) biomes. As for beef, a similar pattern exists: In 2017, 68 percent of the deforestation associated with EU imports came from the Cerrado (57 percent) and the Amazon (11 percent).

Product scope, country benchmarking, and traceability still under dispute

Full traceability will require operators to provide geographic information linking commodities and products to the plot(s) of land, which has been deemed both unrealistic and crucial. As the cornerstone of the due diligence framework included in the upcoming Regulation, traceability of commodities and products is crucial to ensure that EU consumption is not connected to deforestation and forest degradation globally. According to the draft proposal (Chapter 2, Article 9), operators and traders must collect and provide information on the “geo-localization coordinates, latitude and longitude of all plots of land where the relevant commodities and products were produced.” This means that operators must ensure full traceability of the commodities/products to not be in breach of the Regulation.

Industry groups have raised concerns about the implementation of this requirement and asserted that geo-location to the production area would allow for faster implementation while proving equivalent assurances. Conversely, civil society organizations consider full supply chain traceability essential to guarantee that commodity-driven deforestation is effectively halted. Both the EU Council and the European Parliament have maintained their support for geo-location to all plots of land.

By suggestion of the EU Council or the European Parliament, more products and derivatives might be covered under the Regulation The proposed EU Deforestation Regulation will cover a selected group of soy, beef, and leather products. In the case of beef, the derivatives covered by the Regulation are bound to be expanded due to suggestions from the EU Council and the European Parliament. The inclusion of three extra beef products (Figure 1) has been proposed and, although their imported volumes to the EU from non-EU countries are relatively small, some of them originate from countries where there are significant risks of deforestation and forest degradation. For instance, the non-EU imports of other prepared or preserved meat (HS 1602 50) largely come from Brazil (61 percent of the total EU imported volume), where deforestation or forest degradation risks linked to the cattle supply chains are high. Leather was also added as a co-product of beef, acknowledging that leather production is a relevant contributor to deforestation. The EU is a key importer of leather products, most of which come from Brazil.

The country benchmarking system in the EU Deforestation Regulation may undermine due diligence required from companies and lead to laxer control checks. The due diligence procedures required are adapted to the country benchmarking system, which will classify producing countries in three levels of deforestation and forest degradation risk – low, standard, and high. On the one hand, simplified due diligence is foreseen for operators and traders sourcing from low-risk countries, which has been criticized by civil society organizations since it might enable commodity laundering. On the other hand, the same due diligence measures will be requested for products originating from standard and high-risk countries, which has also raised questions on whether being assessed as a high-risk country will have real consequences. The Commission’s draft proposal also foresaw enhanced scrutiny for products coming from high-risk countries, which the EU Council suggested should be left out of the Regulation. The European Parliament, however, seeks an increase of the checks expected in this situation.

A series of legislative processes still lie ahead of the implementation of the EU Deforestation Regulation. The Council of the EU issued its opinion on the draft proposal of the Regulation at the end of June 2022. In July 2022, the ENVI Committee adopted a set of compromised amendments based on the initial proposal and the draft report presented by the Rapporteur. The Committee’s final report was adopted in the Plenary Session of the European Parliament in September 2022 by a significant majority. Introduced amendments such as the enlargement of the Regulation’s scope, an earlier cut-off date, and the inclusion of financial institutions were approved in the voting. The Regulation is expected to enter into force by the end of 2022 or early 2023, after ongoing negotiations.

Full traceability of Brazilian cattle supply chains is challenging, but possible

There are opportunities and feasible options to expand traceability in the Brazilian cattle supply chain by making use of existing systems and tools. Examples of these systems and tools are Visipec and Selo Verde, as well as SISBOV (Brazilian System for Individual Identification of Bovines and Buffalos), CAR (Rural Environmental Registry), and GTA (Animal Transit Guide). Several operators and traders have already committed to and are working towards full traceability in Brazilian cattle supply chains by making use of such systems and tools. However, significant gaps can still exist, particularly in indirect segments of these chains. Traceability to all plots of land of production, as required by the EU Deforestation Regulation, is not yet a complete process in the Brazilian cattle supply chains. Meat and leather value chains actors consider complying with this requirement a challenging and long-term task.

Fragmentation of Brazilian cattle supply chain poses challenges to full traceability

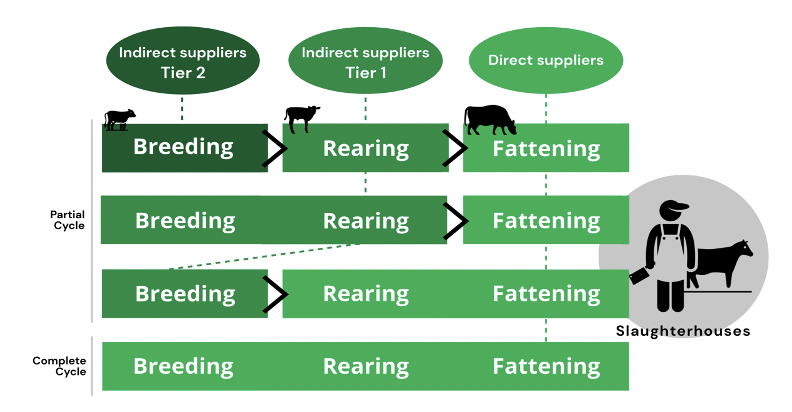

Operators and traders will face challenges providing geographic information on the plot of land from where cattle originate in Brazil, mainly for indirect suppliers. The Brazilian cattle supply chain has a complex architecture characterized by a high-level of fragmentation. Full traceability implies monitoring a wide network of indirect suppliers. For instance, the meatpacker Marfrig works with 1,711 voluntarily registered indirect suppliers, but it potentially has 25,000 indirect suppliers in total in the Amazon biome alone. Indirect suppliers, who sell to other ranches instead of directly to slaughterhouses, can be involved in any of the different stages of the animal life cycle (Fig. 3). These stages can take place exclusively on one farm (complete cycle) or on multiple farms (partial cycles). Therefore, many animals may spend a considerable amount of time in indirect farms and move between several properties before reaching the slaughterhouse.

downstream actors, such as retailers, tanneries, and leather producers, currently use the links to slaughterhouses and its direct suppliers to determine whether the beef and leather products are deforestation-free. However, given the characteristics of the cattle supply chain in Brazil and the lack of implementation of more far-reaching traceability tools, the cattle are likely sourced indirectly from properties tied to deforestation.

Figure 3: Stages in the cattle supply chain until the slaughterhouse (meatpackers)

Source: AidEnvironment, 2022, adapted from Visipec and GTFI.

Traceability gaps in Brazilian cattle supply chains make cattle linked to deforestation harder to identify and create opportunities for cattle laundering. This triangulation strategy, enabled by the lack of traceability to indirect suppliers, is used to avoid connections with non-compliant farms. Laundering cattle implies selling animals to slaughterhouses and meatpackers through “clean properties”, which are compliant with the necessary requirements. These serve as cover for the actual location where animals were raised – a “dirty property” where deforestation and/or human rights violations are likely present. For instance, in 2019, 138 cattle providers of EU-export certified slaughterhouses purchased animals from 301 indirect suppliers which, between 2010 and 2017, compounded a total of 12,907 hectares of deforestation on their farms. Moreover, in 2020, one-third of all direct and indirect suppliers owned more than one property, which facilitates cattle laundering.

CAR and GTA still have limitations that can negatively impact traceability. The existent limitations in these databases might affect the implementation of traceability systems in the sector. CAR has a self-declarative nature which makes it prone to false declarations and fraud. GTAs are used for the sanitary control of animals that are transported between properties. The use of GTAs for traceability purposes is, however, limited by the lack of data integration on all transportations of animals up until the last property and, as a paper-based system, irregularities are facilitated. Moreover, using GTAs to trace animals might also expose the failures of the sanitary control system due to GTA fraud and increase the likelihood of these occurrences. Confidentiality controversies related to the transfer information on the origin of the cattle have also become prominent. The traceability working group of GTPS (Working Group on Sustainable Livestock) says that further analysis is required to ensure data privacy protection and safeguard business strategies.

Despite their limitations, CAR and GTA still constitute important tools for the implementation of traceability systems in Brazilian cattle supply chains. GTPS has stated that integrating these databases can improve traceability and monitoring of cattle supply chains, going beyond slaughterhouses and meatpackers’ direct suppliers. Moreover, big industry players — JBS, Marfrig, and Minerva — have made commitments to adopt comprehensive traceability systems, most of which make use of these databases and tools. This reflects their potential to trace cattle. As for the confidentiality issues, the European Commission has affirmed that no commercially sensitive data, such as the identity or location of operators’ suppliers, will be disclosed publicly.

Synergies between public and private actors are instrumental to cover gaps in the Brazilian cattle supply chains and ensure compliance with EU requirements. Building public-private partnerships (PPPs) and cooperative actions to address current traceability gaps has been deemed an important facilitator in the implementation of the EU Regulation’s due diligence process. There are already multistakeholder forums, such as the Indirect Suppliers Working Group for Brazilian Ranchers (GTFI), working toward increased traceability and monitoring of indirect suppliers. Multistakeholder partnerships and agreements such as the Conduct Adjustment Term (TAC, Portuguese acronym) and the Public Cattle Commitment have contributed to lowering the likelihood of deforestation in properties located in the areas they cover while increasing their chances of enhanced productivity and investment.

Full traceability possible in Brazilian soy supply chains

Traceability in the Brazilian soy supply chain is feasible and is already part of a number of existent agreements. The Amazon Soy Moratorium (ASM), a zero-deforestation agreement that implies monitoring through spatial analysis and independent audits, already lays much of the groundwork required by the EU Regulation in terms of traceability. For instance, the data utilized in ASM’s monitoring system, such as satellite imagery and CAR records, can trace soy to its production site. This data is publicly available and does not create barriers in terms of costs. In addition, a few large traders, such as Bunge, have pledged to share their traceability methodologies and tools with their partners (e.g., aggregators). The ASM monitoring system has also managed to safeguard identities and business strategies, ensuring compliance with existing legislation on privacy and data protection and avoiding business or competitiveness risks.

Industry commitments have led to traceability and monitoring improvements in the Cerrado as well, but gaps remain. The Soft Commodity Forum (SCF), an initiative that unites six of the largest soy traders operating in Brazil – ADM, Bunge, Cargill, Cofco, Louis Dreyfus and Viterra, seeks to reduce deforestation rates linked to soy supply chains in 61 priority municipalities in the Cerrado. SCF members have established a common monitoring and reporting methodology, through which five of them (exception is Louis Dreyfus) have achieved traceability to 100 percent of suppliers to the first point of aggregation. In addition, full traceability commitments have been made. For instance, ADM has committed to achieve full traceability by the end of 2022 while Bunge, Louis Dreyfus, and Viterra have planned to achieve this goal by the end of 2025. However, a time gap for implementation remains, since the EU Regulation is likely to come into force in 2023 and compliance with its traceability requirements will be expected.

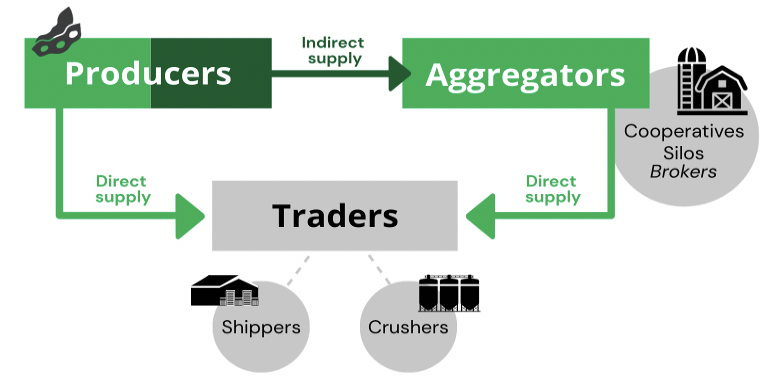

Although improvements in traceability continue, the indirect segment of Brazilian soy supply chains create some barriers. Two different types of relations can be found between producers (farms) and traders in Brazilian soy supply chains (Figure 4). On the one hand, producers may be direct suppliers of traders if the latter obtain their soy and soy products directly from the former. On the other hand, traders may buy from intermediary groups (aggregators) that, in their turn, buy from producers, which become, in this case, indirect suppliers of trader companies. Indirect supply creates more hurdles to traceability up to the plot of land of production, as required by the upcoming EU Regulation. These hurdles to traceability can lead to higher deforestation and human rights’ violation risks. Achieving full traceability will therefore demand increased efforts geared toward soy producers that supply the aggregators from where the soy products are sourced. Currently, for example, indirect supply represents about 22 percent of the collective soy purchases of SCF members in the Cerrado.

Figure 4: Stages of the soy supply chain

Source: AidEnvironment, based on the Proforest soy tool kit.

Reaching full traceability in Brazilian soy supply chains will require targeting biome/region specific issues, as well as improvement of existing systems for traceability purposes. For the Cerrado, implementation of the EU Regulation will be challenging because it is difficult to incentivize farmers to forego the possibility of legally clearing parts of their properties in the Cerrado. According to Brazil’s national forest code, only 20 or 35 percent (depending on location) of the native vegetation in the properties located in Cerrado must be left intact as “legal reserve.” As the EU Regulation will equally cover illegal and legal deforestation, soy produced in farms that deforest legally according to Brazil’s Forest Code will no longer be acceptable in the EU market. The improvement of existing systems appears necessary given the lack of data quality, specifically in the CAR system. As mentioned, as a self-declared document that lacks control checks, CAR declarations are vulnerable to irregularities, which can hamper traceability.

Traceability possible while avoiding supply chain leakage, market segregation, and exclusion of small operators and producers

Market leakage that does not require the same level of socio-environmental compliance can be overcome by promoting traceability independently of the destination market. As a key export market, the EU may provide a strong incentive to implement traceability in these supply chains regardless of the destination of the beef, leather, and soy products. The largest traders in Brazilian beef and soy are strengthening their deforestation-free commitments and improving their traceability systems, which will likely reduce opportunities for leakage. However, market leakage may still occur as an unintended consequence of the EU Regulation. A market bifurcation between clean and dirty supply may come about, and thus products could be diverted to markets that have lower socio-environmental requirements, such as those — like the Chinese market — that are already relevant in terms of trade volumes. Moreover, the largest market for Brazilian beef and an important one for soy is the domestic market. The Brazilian market has been linked to higher deforestation risks as its sustainability standards are relatively low and does not demand traceability to the plot of land.

Since it is not legally required, market segregation can be avoided while traceability implementation costs become negligible over time. Environmental charity Client Earth argues that the EU Regulation does not require market segregation since it does not ban products of mixed origin. It also does not impose a specific supply chain structure or a specific diligence process. The Environment Commissioner has clarified that what needs to be ensured is that “commodities are not mixed at any step of the process with commodities of unknown origin.” Thus, as long as the origin is known, beef, leather, and soy products produced in different areas can be traded in bulk. Furthermore, it is more feasible to avoid segregation altogether by making traceability systems an inherent component of the supply chain management, independent of destination markets. This will not both reduce any additional costs of setting up segregated chains and also make broad traceability implementation costs temporary and negligible with time.

Industry players, however, still argue that this segmentation will occur and have been vocal about the associated burden, considering it “technically and effectively not feasible.” Accordingly, segregation would entail added administrative and financial costs to operators and traders, as well as a possibly creating a shortage of relevant commodities and higher costs for EU consumers. Some soy industry groups have also recommended that a mass balance approach should be allowed under the EU Deforestation Regulation, but, following the OECD and the FAO, mass balance models that allow for mixed batches of grains are not acceptable for zero-deforestation targets. Civil society organizations, meanwhile, state that guaranteeing sustainability along soy supply chains is not possible in mass balance approaches.

Ensuring traceability may be challenging for small and medium-sized companies, but accessible traceability options and support exist. Recent improvements in terms of availability of data, tools, and systems for better traceability in cattle and soy supply chains have allowed for a significant decline in costs. Using these data, tools, and systems can alleviate the financial constraints faced by operators/traders due to compliance with the EU Regulation. High-quality satellite images, CAR registrations, and GTA data, as well as systems such as VISIPEC, allow for tracing of both direct and indirect supply. Nonetheless, for small- and medium-sized operators, implementing traceability methods can be challenging due to lack of familiarity with systems and the associated costs, which are more burdensome in the case of small-scale operations. Marfrig’s Verde+ plan lists access to financial instruments and a technical assistance network as part of its actions toward indirect cattle suppliers. Bunge, a big soy trader, is also open to assisting smaller grain dealers in implementing traceability and monitoring systems as a means to contribute to a more transparent and sustainable soy sector.

Although the EU Regulation has been anticipated to have an exclusionary effect for smallholders, they are not a key group in Brazilian soy production, and assistance is available in the case of cattle. Small producers, with properties between 50 to 100 hectares, are responsible for only 15 percent of the soy produced in Brazil. Soy cultivation in the country is mostly in the hands of large-scale producers, with often thousands of hectares of land for crop production. These producers are responsible for most of the soy linked deforestation. Four hundred large farms in the state of Mato Grosso (only 2 percent of all the soy-producing farms in the state) accounted for about 80 percent of total illegal deforestation linked to soy production between 2012 and 2017. Small producers play a more important role in cattle production than in the case of soy, representing about 30 percent of all Brazilian cattle producers. To incentivize small and medium cattle producers’ adherence to traceability systems, some retailers and meatpacking companies, such as Marfrig, are introducing vertical integration schemes that include long-term contracts and technical assistance.

It is, however, important to reiterate that, according to the draft proposal (Chapter 2, Article 4), due diligence requirements fall upon the operators placing commodities and products in the EU market and not on the producers.

Non-compliance with traceability requirements has legal, reputational risks

There are legal risks for operators and traders that fail to comply with the obligations of the EU Deforestation Regulation. In Brazil, the Conduct Adjustment Term (TAC) for beef and the Amazon Soy Moratorium (ASM) for soy entail a similar legal basis wherein the commitments are enforceable by law. However, not only has TAC not been enforced as it was supposed to, most of the industry commitments currently active in Brazil are voluntary and have not been sufficient to curb deforestation in the country. The EU Deforestation Regulation, on the other hand, includes a due diligence system that can guarantee, by design, the effectiveness of the Regulation and its legal enforcement. As laid out in the Commission’s draft text, this system foresees legal prosecution of those in violation of the Regulation through the application of penalties, namely fines proportional to the environmental damage and temporary exclusion from procurement processes.

Enforcement of the EU Regulation will require breaching operators and traders to take appropriate and corrective action, but the scope of the control is still under discussion. The application of these measures will be in the hands of Member States’ competent authorities who will have to perform annual checks on a given percentage of all operators and traders, as well on the total quantity of each product placed on or exported from the EU market. The EU Council is aiming at simplifying these procedures, by reducing the overall percentage of checks required and eliminating enhanced scrutiny for countries benchmarked as high-risk. The European Parliament has gone, thus far, in the opposite direction, proposing an increase in both regular and enhanced scrutiny checks. Civil society organizations have also been calling for more rigorous measures in cases of repeated offenses and violation of third parties’ rights, particularly rights of Indigenous Peoples and local communities.

Industry groups have warned of supply chain shortages due to difficulties in complying with the Regulation’s requirements. Several factors have led to increasing industry concerns about creating further challenges with stricter due diligence requirements from the upcoming Regulation. Overlapping global crises – COVID-19 pandemic, Russian invasion of Ukraine, and drought in South America (which caused a sharp reduction in soybean yields in Brazil) – have impacted the fundamentals of the global commodity market, increasing prices and creating risks of shortages worldwide. A joint statement by European industry groups has highlighted several ways in which the implementation of the EU Deforestation Regulation can further harm grain and oilseed supplies if it is kept in its current terms. The groups have also suggested the limitation of the Regulation’s scope for the time being, for instance, by introducing a maximum acceptable level of non-compliance (5 percent) to be reduced by 2030.

Reputational risks are also at stake for operators and traders that violate the due diligence requirements. If operators and traders are found to be in breach of the Regulation’s due diligence and traceability requirements, their image with other supply chain actors and consumers may be negatively affected. Further down the supply chain, Fast Moving Consumer Good (FMCG) companies and retailers will also be exposed to reputational risk when sourcing (in)directly from non-compliant operators. Scrutiny efforts on compliance with the EU Deforestation Regulation will increase from civil society organizations (CSOs), which will also target these downstream players since they are better known by the general public.

Sourcing commodities from countries benchmarked as high-risk might lead to reputational damage. According to the Regulation, high-risk countries must comply with the same requirements as standard-risk countries, but will be subject to increased annual checks by Competent Authorities in EU Member States (Chapter 3, Article 20). However, countries classified as high-risk will inevitably be associated with higher chances of non-compliance, especially if the production of relevant commodities and products in high-risk countries has already been linked to deforestation and forest degradation, which is the case of beef, leather, and soy produced in Brazil.

Financial Risk Analysis – Costs of compliance are relatively low for downstream actors

Companies and financers in the beef and soy supply chains face financial costs from compliance with the EU Deforestation Regulation. At the same time, however, expenditures on compliance can prevent financial risks, including reputation damage. Best-in-class compliance will likely avoid financial costs and losses from market access risk, fines, financing risk, and reputation risk. These companies’ financers (banks and investors in shares and bonds) may also face financial impacts, in particular due to reputation risk.

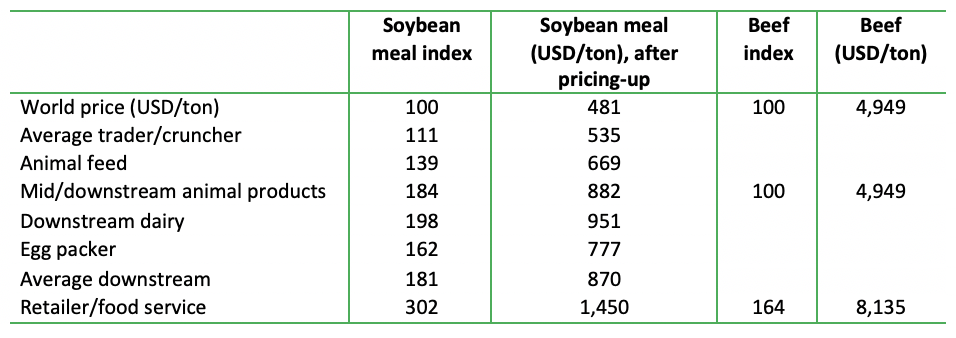

Expenditures by the EU beef and soy industry to comply with the Deforestation Regulation could amount to a relatively low percentage of the total value of embedded beef and soy in the European value chain. When soy, beef, and leather are imported, these products undergo various supply chain processes wherein value is added and the price increases with every step in the supply chain. Embedded soybean meal might face a three-fold increase in value and beef a 64 percent increase (Figure 5).

Figure 5: Pricing up in the supply chains of soy and beef (2021, in USD)

Source: Profundo; USD was used in the analysis. USD is now nearly 1:1 to EUR. The study focused only on soymeal and beef.

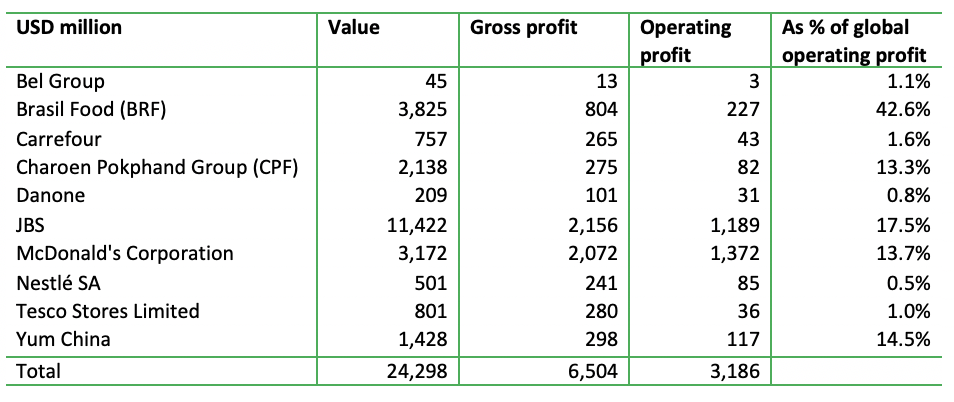

Based on their position in the supply chain, companies are able to generate a gross profit and an operating profit on embedded soy and beef originating from Latin America (LatAm). Figure 6 provides an overview of 10 companies. They generate a total of USD 24.3 billion in value in embedded Latin American soymeal and beef. This group’s gross profit in embedded soymeal and beef totals USD 6.5 billion and the operating profit USD 3.2 billion. Some of these companies are very active in the EU. Their EU activities in embedded soy can, for a material part, be tied to LatAm, which contrasts with their activities in North America wherein soy is sourced locally. A downstream company like McDonald’s earns an operating profit of USD 1.372 billion from embedded LatAm soy and beef, for which a major part of the soy (in feed) is used in the EU.

Figure 6: Summary – Exposure to Latin American soymeal and beef – key numbers

Source: Profundo

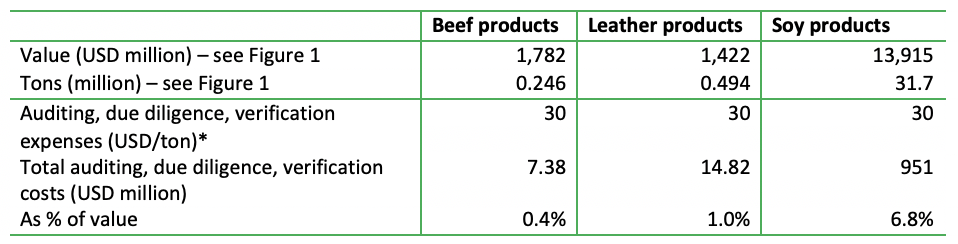

Since traceability systems are already largely present, the implementation of a zero-deforestation policy by beef and soy (sourcing) companies only requires an internal and external auditing system, due diligence process, and verification system like in palm oil. But the costs per ton are probably different and might be lower. That is because the sustainability risk analysis by CRR indicates that the transparency methodology for soy and beef is available but needs to be reinforced and expanded to indirect suppliers. Moreover, segregation streams in the supply chain might not be needed if tracing systems have become a general practice. The expenditures might be 0.4 percent to 6.8 percent versus the value on the embedded material (Figure 7). To keep operating profits intact, a limited price increase might be required (also of 0.4 – 6.8 percent; last row in Figure 7 below). As the EU Deforestation Regulation is heavily focused on importing traders and operators, these expenses could weigh heavily on these actors.

Figure 7: Deforestation-free policy execution and monitoring/verification expenditures

Source: Chain Reaction Research, based on previous report in 2022. *The palm oil per ton policy execution/monitoring/verification costs include around USD 30 for premium pricing of certificated oil; for beef and soy these costs are not included in this calculation, leading to ca USD 30 per ton for policy execution/monitoring/verification.

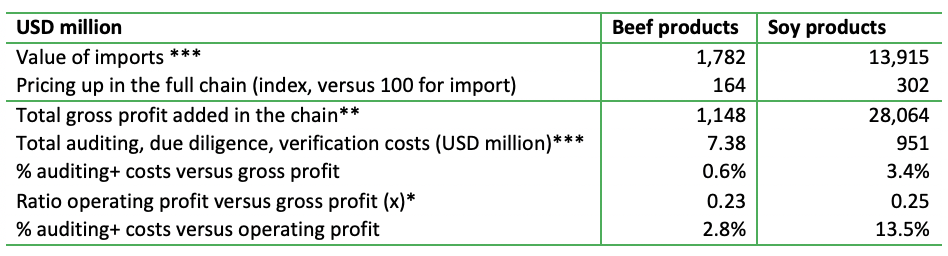

If these costs are spread across the full supply chain, including the downstream segment (Figure 8), the impact on gross profit and operating profit would be in the ranges of 0.6 to 3.4 percent and 1.1 to 10.9 percent, respectively.

Figure 8: Deforestation-free compliance costs relative to value generated in downstream

Source: Chain Reaction Research. *) based on operating profit of group of 10 in Figure 9 versus gross profit of the group of 10 companies (not included but available on request and in Profundo report. **) Based on the pricing up of respectively 64% and 202% for beef resp. soy, and applied to the value of imports from LatAm, respectively USD 1,872 million and 13,915 million.***) from preceding figure.

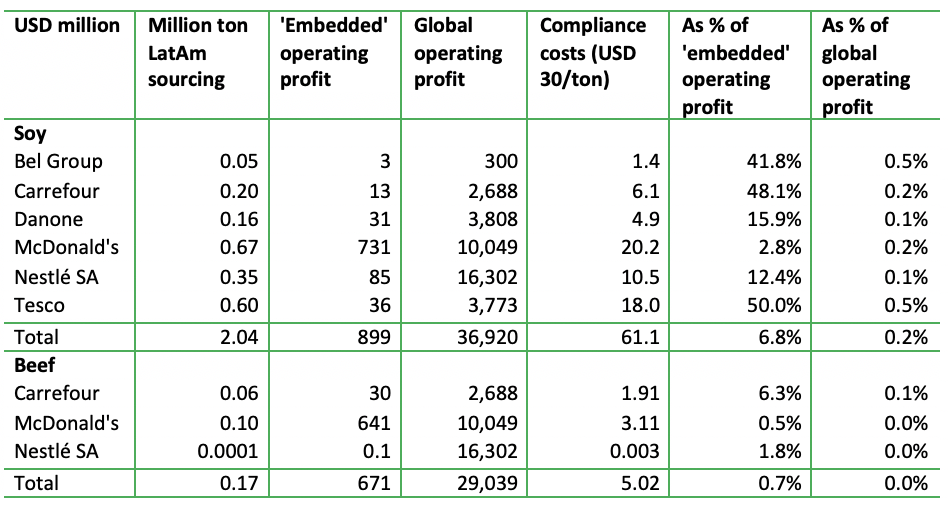

The methodology in Figure 7 is applied to a selection of companies (from Figure 6), in case they would carry all compliance costs (auditing, due diligence, verification). The selected companies are all active in the EU, and the million tons sourcing from LatAm that are shown (first column) are partly for the EU market. By applying a compliance cost of USD 30 per ton (lower than the amount for palm oil due to absence of segregation, and no price premium for certification is assumed), the total compliance cost is 6.8 percent (soy) and 0.7 percent (beef) of the operating profit (on the embedded LatAm material). In relation to the total global operating profit, compliance costs are 0.0 percent to 0.2 percent. These numbers cover all sourcing from LatAm, including supply for markets outside the EU.

Figure 9: Compliance costs Latin American embedded soy and beef

Source: Profundo

A company that does not comply with the upcoming EU Deforestation Regulation could face financial risks. A previous CRR report noted that the reputation value-at-risk is nine to 45 times larger than the present value of future (based on discounted cash flow) compliance costs (present value = discounted future values), calculated for a group of eight publicly listed large FMCG companies. This reputation risk was three to 15 percent of their equity value. The high-end of the reputation risk calculation (15 percent) contains the impact of market access risk, financing risk, and the cost of fines. As the quoted CRR report focused on palm oil compliance costs, estimated at USD 65 per ton (excluding segregation, which would need to be added in the context of the EU Deforestation Regulation), the USD 30 per ton applied to soy and beef in this report would lead to even higher outcomes than the “nine to 45 times” multiple. Thus, compliance would have a very high return on investment.

The EU financial sector is not directly affected by the EU Deforestation Regulation, leading to negative reactions from more than 100 NGOs. The EU Deforestation Regulation proposal says that the present initiative will not specifically target the financial sector and investments (although this might change later on due to amendments). Existing initiatives in the area of sustainable finance — EU Taxonomy Regulation and the future Corporate Sustainability Reporting Directive (CSRD) — are supposed to address the deforestation impacts connected to the finance and investment sectors. These complement and support the legislative initiative on deforestation, the European Commission added. However, civil society (a group of more than 100 NGO/CSOs) stated that the EU Taxonomy Regulation and the CSRD lack obligations for investors and banks to stop investments from going toward harmful activities. The group also argues that there is no mechanisms to hold them accountable. The group of NGOs is asking for equivalent regulation for financial institutions (in line with those demanded for operators and traders importing beef and soy).

Indirectly, financers would likely be affected by financial risks in their shareholding, bonds, and loans. EU financers could face investment risk from the EU Deforestation Regulation. The Regulation could affect the value and dividend streams of companies they finance. These companies could be affected by a reduction in access to the EU market, fines, higher financing costs, and/or reputation damage. These losses would vary per investment and would be related to the exposure of each investment to the EU market. EU financial institutions are large financers of companies active in the global beef and soy value chains: the operating profit on embedded beef and soy are the basis for the financial streams that are reaped by banks (interest on loans) and investors (dividends, share buybacks, interest on bonds).