The upcoming EU Deforestation Regulation will have an impact on JBS, Minerva and Marfrig. A sample of 12,461 direct and 26,572 indirect suppliers of these key meatpackers shows recent deforestation that may end up in the European Union’s (EU) beef and leather consumption markets. Any deforestation after the proposed December 31, 2020 cut-off date would be non-compliant with the upcoming law.

Download the PDF here: JBS, Marfrig, and Minerva Unlikely Compliant with Upcoming EU Deforestation Law

WATCH THE WEBINAR FOR THIS REPORT

Key Findings

- Meatpackers JBS, Marfrig, and Minerva will need to comply with the upcoming EU Deforestation Regulation once it is passed and implemented. These meatpackers dominate the Brazilian cattle industry and are major exporters of frozen beef and leather products to the EU. To export to the EU, their direct and indirect cattle supply chains cannot be associated with either legal or illegal deforestation, after the December 2020 cut-off date.

- A sample of their suppliers provides information on Brazilian beef production hotspots linked to the EU market. JBS is the dominant buyer of cattle in all seven Brazilian states included in the sample, while buying zones of Marfrig and Minerva are concentrated in fewer states. For all three meatpackers, their indirect supplier base in high-deforestation risk state Pará is nearly double compared to the direct supplier base.

- CRR found conversion of 72,663 hectares (ha) in the sample since the cut-off date. Potentially 65,969 ha of Amazon and 6,694 ha of Cerrado deforestation alerts linked to the suppliers of the three meatpackers may be non-compliant with the upcoming EU law.

- Deforestation linked to indirect suppliers is highly prevalent. Indirect suppliers are a risk since meatpackers’ monitoring of their indirect supply chains shows gaps and delays, and they are unlikely to be ready for the expected EU law implementation starting in 2023.

- Since the meatpackers do not monitor all indirect supply, they cannot guarantee compliance with the upcoming EU Deforestation law. Thus, meatpackers, leather operators, and FMCGs may face legal and reputational risks. Meatpackers JBS and Minerva monitor only illegal deforestation linked to their suppliers, while the upcoming Law will also consider Brazilian legal deforestation as non-compliant. Marfrig has committed to zero deforestation, including legal.

- Due diligence expenses in EU beef and leather chains are relatively low in the context of mitigated financial risks for the relevant sectors. In contrast, financers of JBS, Marfrig, and Minerva may face the most value risks (9.5-19 percent).

EU Deforestation Regulation will affect cattle imports from Brazil

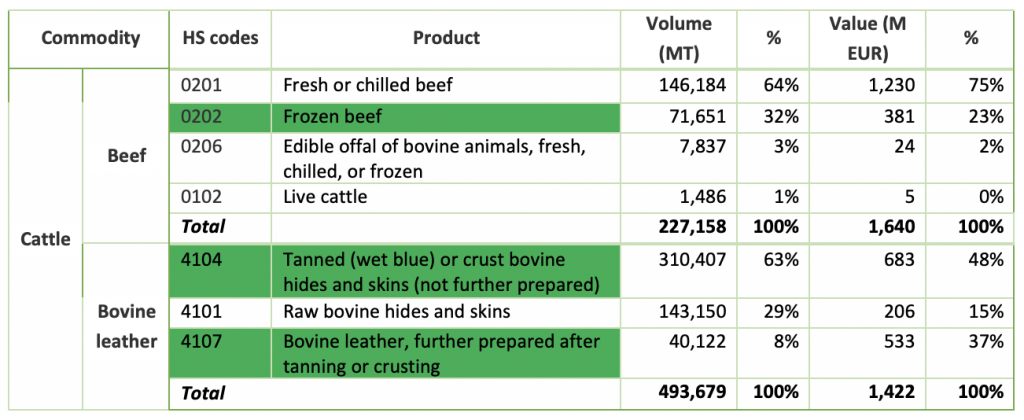

EU mainly imports frozen beef and leather products from Brazil

Among non-EU countries, Brazil, a high deforestation-risk country, is the main supplier of frozen beef, tanned or crust bovine hides and skins, and prepared bovine leather to the EU. Imports of beef and beef-related products from non-EU origins account only for a small share of European consumption. But among those, Brazil plays a principal role as a supplier of frozen beef, and even more for bovine leather products to the EU (Figure 1). Both beef and leather production are key drivers of deforestation in Brazil. Cattle raising is causing the most deforestation in the Brazilian Amazon, an area that has seen a new record of forest loss during the first half of 2022. In 2021, the EU sourced 52 percent (37,147 metric tons, MT) of its total imports of frozen beef from Brazil, as well as 28 percent (87,344 MT) of its total imports of tanned (wet blue) or crust hides and skins, and 30 percent (12,029 MT) of its total imports of prepared leather.

Figure 1: Total 2021 EU imports of cattle products from non-EU countries by volume and value in green predominantly originating from Brazil

Source: EU27 trade statistics, 2021, assessed in October 2022; European Commission’s draft proposal. Notes: These products represent cattle-related products under the scope of the EU Deforestation Regulation. Highlighted products in green are predominately originating from Brazil. Edible offal of bovine animals includes Harmonized System (HS) codes 020610, 020629, and 020622.

JBS, Marfrig, and Minerva most impacted by EU Deforestation Law

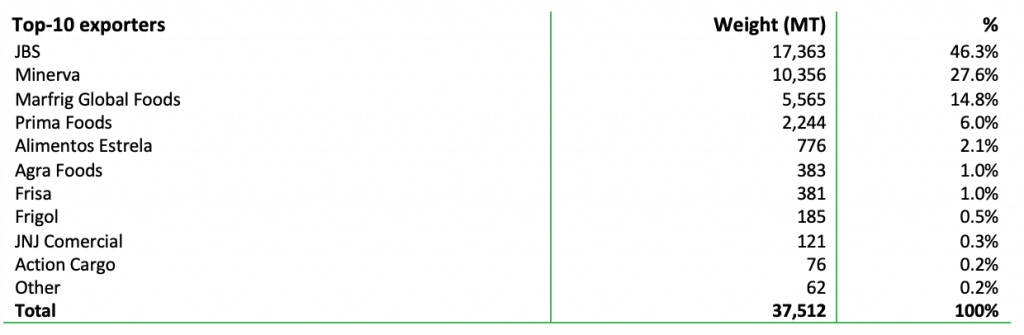

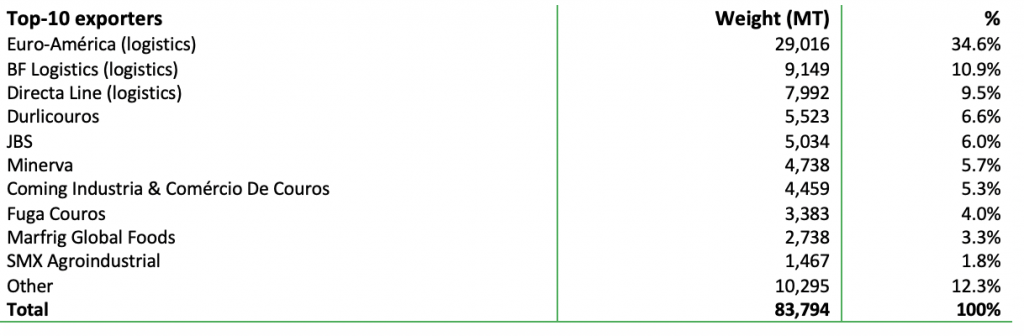

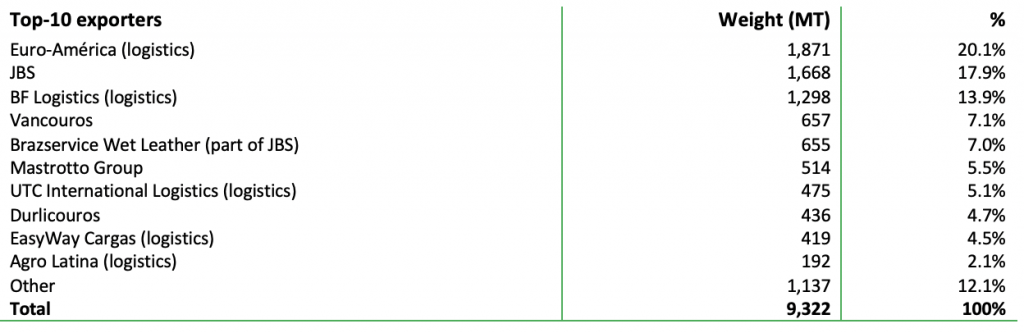

Three key meatpackers, JBS, Marfrig, and Minerva, are major exporters to the EU and dominate the Brazilian cattle industry and the production of beef and bovine leather products. JBS is the largest animal protein company and the second-largest food company in the world. Marfrig is the world’s second-largest beef company by production capacity, while Minerva is an export-oriented beef company. JBS, Minerva, and Marfrig are the largest Brazilian exporters of frozen beef to the EU (Figure 2) and are among the largest Brazilian tanneries supplying tanned (wet blue) or crust hides and skins to the EU market (Figure 3). For prepared leather, only JBS plays a direct role as a top exporter to the EU (Figure 4). Also, other meatpackers’ slaughterhouses indirectly provide hides and skins to leather producers that export prepared leather to the EU. For instance, tanneries of leather producers Durlicouros and Viposa likely source raw materials from Marfrig’s nearby slaughterhouses.

With 63.7 percent of all EU imports of frozen beef in 2020, Italy represents the largest recipient of Brazilian frozen beef followed by the Netherlands (22.1 percent), Spain (8.6 percent), and Germany (4.6 percent). The major European destination country for tanned (wet blue) or crust bovine hides and skins from Brazil in 2020 is Italy (97.7 percent), which has a large leather processing industry. Europe’s main destination countries for further prepared bovine leather from Brazil in 2020 include Italy (45.7 percent), Germany (29.9 percent), the Netherlands (9.1 percent), and Hungary (8.4 percent).

Figure 2: Top-10 Brazilian exporters of frozen beef to the EU (2020)

Source: Shipping data 2020, based on HS code 0202. Prima Foods includes exports under Mataboi.

Figure 3: Top-10 Brazilian exporters of tanned or crust bovine hides & skins to the EU (2020)

Source: Shipping data 2020, based on HS code 4104.

Figure 4: Top-10 Brazilian exporters of prepared bovine leather to the EU (2020)

Source: Shipping data 2020, based on HS code 4107.

The three meatpackers will need to comply with the upcoming EU Deforestation Regulation, that aims to curb both legal and illegal deforestation and forest degradation resulting from EU consumption and production. The European Commission’s proposed Regulation defines “deforestation-free” as relevant commodities and products that were produced on land that has not been subject to deforestation since December 31, 2020, and wood that has been harvested from forests without inducing “forest degradation” after December 31, 2020. This cut-off date is still under debate. Beef and leather products fall under the scope of the Regulation. One of the Regulation’s central points is full supply chain traceability of the listed deforestation-risk commodities and products, requiring beef and leather operators to provide geographic information linking commodities and products to the exact location of production. A recent CRR report concluded that, while some challenges remain, the traceability requirement of the EU Deforestation Regulation is viable in Brazilian cattle supply chains by using existing systems and tools.

Meatpackers’ beef production hotspots

New data on direct and indirect suppliers of the three meatpackers gives information on the exact locations of beef production hotspots in Brazil, as visualized in Figure 5. This is relevant under the traceability requirement of the EU Deforestation Regulation. To create the sample of 12,461 direct and 26,572 indirect suppliers of the three meatpackers, CRR used a similar methodology, with some adjustments, as we used in our 2020 paper on the three meatpackers. The main changes include 1) increasing the sample significantly by using new analyzing techniques and 2) using deforestation alerts (DETER), including deforestation by fire, in this analysis, as opposed to yearly processed deforestation data (Prodes), generally resulting in larger areas detected with clearing. Consequently, the deforestation data from the December 2020 report and the current analysis are not comparable, since the sample is different and deforestation rates are calculated differently.

Figure 5: Locations of direct (left) and indirect suppliers (right) to JBS, Minerva, and Marfrig

![]()

Source: AidEnvironment, heatmaps are created with QGIS, and based on data from the Ministry of Agriculture and animal transportation permits (GTA). The brighter the colors, the higher the concentration of direct and indirect suppliers in the sample.

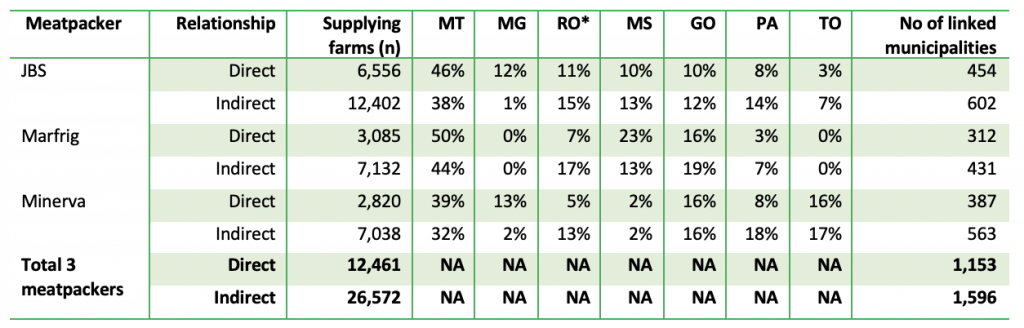

Based on animal transportation and rural cadaster data, CRR has located and monitored 12,461 direct and 26,572 indirect suppliers connected to the top three meatpackers in seven states in Brazil’s Amazon and Cerrado biomes. These numbers represent a partial sample of the total suppliers to JBS, Minerva, and Marfrig. For instance, the sample with 6,556 direct suppliers to JBS’s slaughterhouses (Figure 6) covers only 13 percent of the company’s total estimated supply base of 50,000 direct suppliers. Minerva says it has 6,000+ suppliers in Brazil; the sample of 2,820 would cover 47 percent of its direct suppliers. In 2020, Marfrig says it has 15,000 direct suppliers registered in the Amazon Biome and estimates to have potentially 25,000 indirect suppliers in total in the Amazon biome alone. The sample of 3,085 direct suppliers and 7,132 indirect suppliers would then respectively cover 21 and 29 percent. None of the three meatpackers publishes clear information on the total amounts of their direct and indirect suppliers. One reason for not publishing the information may be that these numbers are not known to them.

Figure 6: Sample characteristics: buying zones of JBS, Marfrig, and Minerva per Brazilian state

Source: AidEnvironment, based on rural cadaster data (SIGEF and SNCI), Ministry of Agriculture, animal transportation permits (GTA). MT = Mato Grosso; MG = Minas Gerais; RO = Rondônia; MS = Mato Grosso do Sul; GO = Goiás; PA = Pará; TO = Tocantins. *For Rondônia, the numbers may represent a slight overestimation due to some data limitations. For more explanation, CRR authors can be approached.

JBS is the dominant buyer of cattle in all seven Brazilian states included in the sample, while buying zones of Marfrig and Minerva are concentrated in fewer states. Most of JBS’s direct suppliers are in Mato Grosso (46 percent of the total sample), but overall, the company has direct suppliers spread over all seven Brazilian states (Figures 5 and 6). By contrast, Minerva and Marfrig seem to have their buying zones more concentrated in certain states. Marfrig has relatively little (or no) direct suppliers in Pará, Minas Gerais, and Tocantins in the sample, while Minerva has a direct supplier base in these states. Compared to Minerva and JBS, meatpacker Marfrig has a larger direct supplier base in Mato Grosso do Sul (Figures 5 and 6).

Deforestation risks linked to the meatpackers’ indirect supply base are most relevant in Pará, a state in the Brazilian Amazon. The sample reveals that for all three meatpackers, their indirect supply base in Pará is in most cases more than double their direct supplier base (Figure 6). The larger indirect supplier base is a risk, since the meatpackers’ monitoring of their indirect supply chains shows significant gaps and delays. Similarly in Rondônia, the indirect supplier bases of Marfrig and Minerva are at least double the number of their direct suppliers. By contrast, all three meatpackers have relatively few indirect suppliers located in Minas Gerais (Figures 5 and 6). A potential explanation is that Minas Gerais mostly operates in the final step of the chain (slaughter) rather than the fattening stage, which is characterized by the involvement of many indirect supplier properties. This explanation is supported by the concentration of slaughterhouses of the three meatpackers in the triangle of Minas Gerais, São Paulo, and Mato Grosso do Sul (Figure 5).

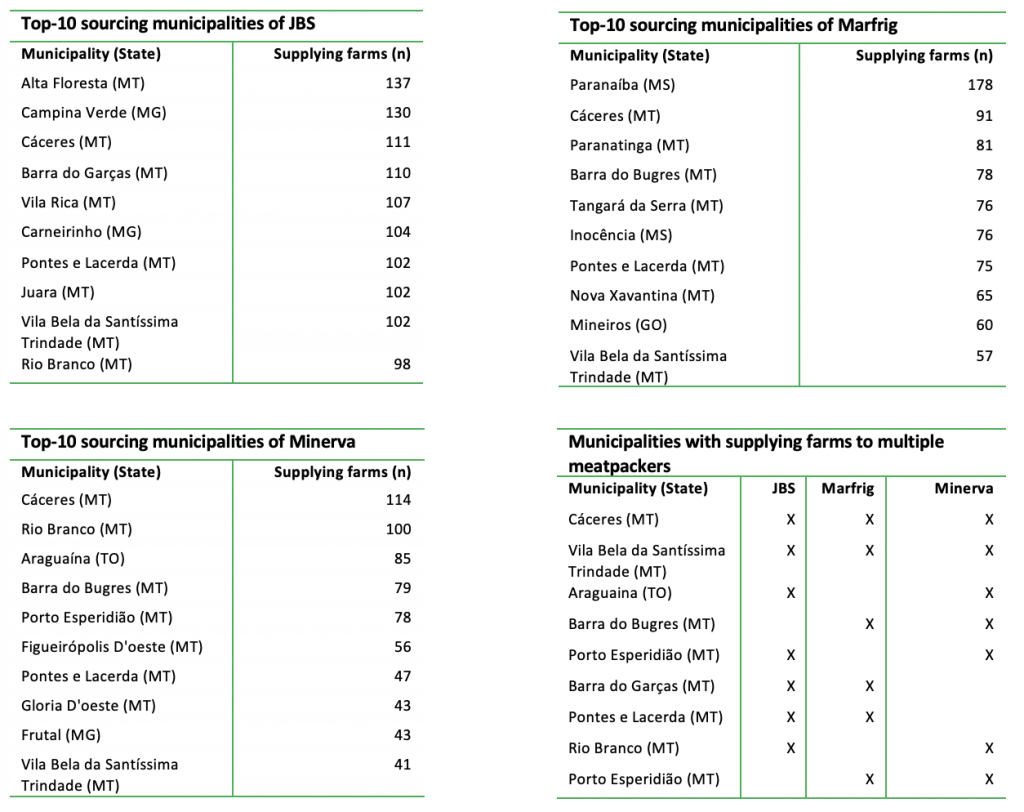

The sample also reveals production hotspots and meatpacker dominance in Brazilian municipalities. These municipalities may become a priority for demonstrating compliance with the upcoming EU Deforestation Law. The sample shows, for example, that all three meatpackers source beef from a significant number of farms in Cáceres in Mato Grosso (Figure 7). While part of this municipality is already developed, the southeastern part is still covered with native vegetation and therefore at risk of deforestation. Moreover, Parnaíba in Mato Grosso do Sul accommodates most supplying farms of Marfrig in the sample, while Minerva, apart from Cáceres, mainly sources from Rio Branco in Mato Grosso and Araguaína in Tocantins. Finally, Vila Bela da Santíssima Trindade in Mato Grosso accommodates large numbers of direct suppliers to all three meatpackers.

Figure 7: Top-10 municipalities in the sample with most direct suppliers to JBS, Marfrig, and Minerva

Source: AidEnvironment, based on rural cadaster data (SIGEF and SNCI), Ministry of Agriculture, animal transportation permits (GTA), and based on the sample. Note: the table “Municipalities with supplying farms to multiple meatpackers” is based on the top-20 sourcing municipalities of each meatpacker.

While nearly 80 percent of the direct suppliers in the sample supply only one of the three meatpackers, indirect suppliers more regularly tend to supply all three meatpackers at once (Figure 8 below). Of the 12,461 direct suppliers in the sample, 79 percent sold to only one of the three meatpackers, 19 percent supplied two meatpackers, and only 2 percent to all three meatpackers. Of the indirect suppliers in the sample, 37 percent sold to only one of the three meatpackers, 53 percent supplied two meatpackers, and 10 percent to all three meatpackers.

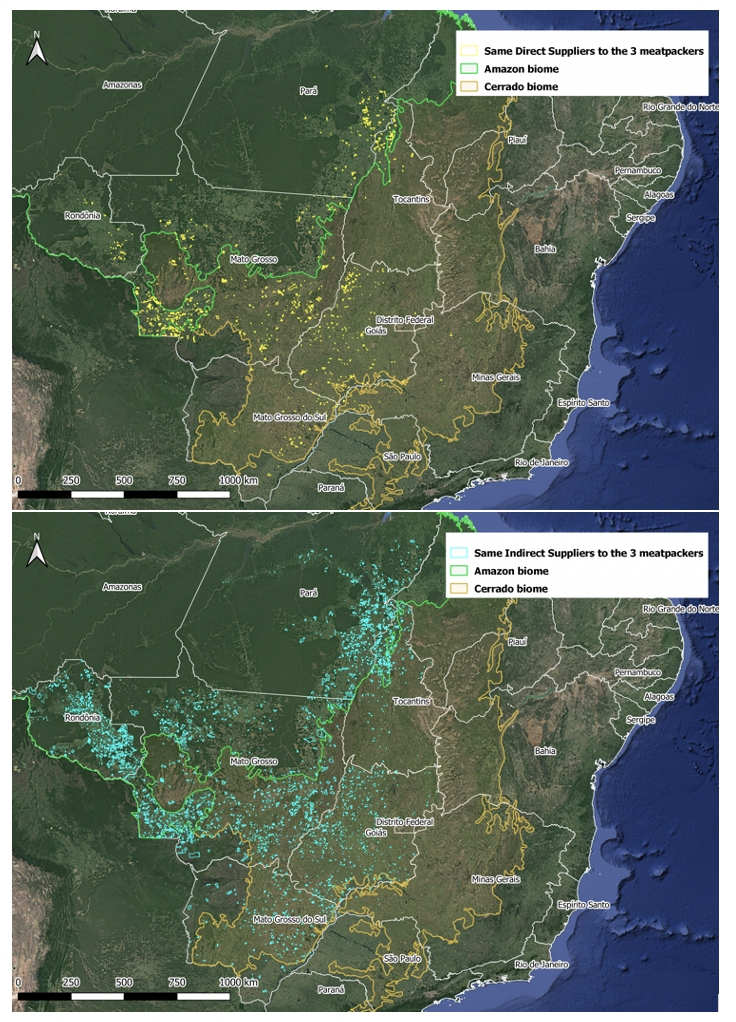

Figure 8: Locations of direct and indirect suppliers serving all three meatpackers

Source: AidEnvironment, based on rural cadaster data (SIGEF and SNCI), Ministry of Agriculture, animal transportation permits (GTA).

Significant conversion since 2020 cut-off date of EU Deforestation Regulation

Potentially 65,969 ha of Amazon and 6,694 ha of Cerrado vegetation clearing non-compliant

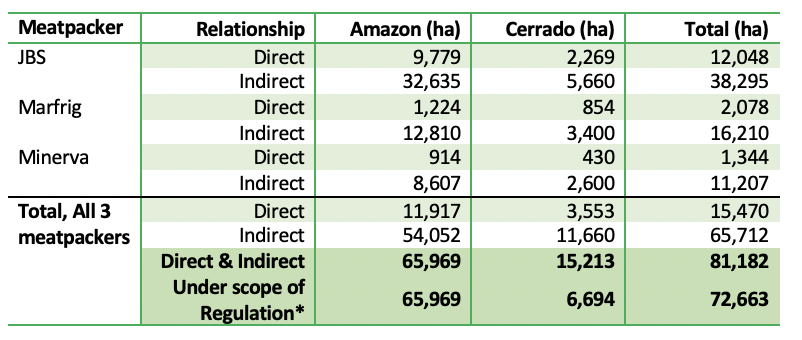

Considering the proposed cut-off date of December 31, 2020, CRR analysis reveals that potentially 65,969 ha of Amazon deforestation and fire alerts linked to suppliers of the three meatpackers in the sample may be non-compliant with the upcoming EU Deforestation Law. The Amazon vegetation loss is connected to both direct and indirect suppliers of all three meatpackers since the proposed cut-off date of the EU Deforestation Regulation (December 31, 2020) (Figure 9). The deforestation detected corroborates other studies showing that Amazon clearing is on the rise and that beef-linked deforestation continues to originate from protected areas in the Amazon.

The identified deforestation area covers legal and illegal deforestation under Brazilian law, both of which will be non-compliant under the EU Deforestation Regulation. Deforestation that is legal under Brazilian law will become non-compliant under the EU Deforestation Regulation. The deforestation area of 65,969 ha may be an overestimation since it is based on still unconfirmed (DETER) deforestation alerts. On the other hand, the estimated deforestation area is conservative since CRR’s sample covers only a small proportion of all direct and indirect suppliers linked to the three meatpackers. When considering the full supply base of the three main meatpackers, CRR estimates that deforestation rates linked to suppliers of JBS, Marfrig, and Minerva slaughterhouses will increase. This estimation does not make claims of illegal practices by the three meatpackers, since a portion of the deforestation, particularly in the Cerrado biome, would be legal under the scope of Brazil’s Forest Code.

Figure 9: Deforestation alerts (ha) in sample linked to suppliers of JBS, Marfrig, and Minerva slaughterhouses from December 31, 2020 to July 2022

Source: AidEnvironment, based on 2022 DETER deforestation alerts; SIGEF, SNCI, 2022 GTA records. Note: Deforestation alerts from DETER 2022 are not yet confirmed, therefore, the deforestation rates linked to this sample may be overestimated. *Not all Cerrado native vegetation (e.g. grasslands) is under the scope of the proposed EU Deforestation Regulation.

The sample demonstrates that Amazon-based suppliers to the three meatpackers are responsible for more land clearing since December 31, 2020 than Cerrado-based suppliers. Multiple explanations exist for an increase in Amazon deforestation. First, observed deforestation rates in the Amazon biome have increased since 2019, as a result of a new Brazilian governance mandate and actions not favorable to tackle deforestation or enhance forest conservation. Second, the new analysis in this report includes deforestation by fires, with peak fire seasons increasing considerably in the Amazon the last three years. Areas cleared by fires in the peak fire season (roughly from early August to the end of October) are not always picked up through satellite analysis in the subsequent year, as vegetation has already regrown at the time of confirmation of deforestation alerts by Prodes.

In the Cerrado, removal of 6,694 ha of forest and wooded savannah may be non-compliant with upcoming EU legislation. Of the total of 15,213 ha Cerrado vegetation cleared on properties of both direct and indirect suppliers to the three meatpackers (Figure 9), an estimated 44 percent (6,694 ha) may be non-compliant under the EU Deforestation Regulation. The Regulation’s scope includes forest and woodland ecosystems. In 2021, land use in the Cerrado biome showed 14 percent of the native vegetation was forest, 30 percent wooded savannah, and 9 percent other non-forest (i.e., grassland) vegetation.

Deforestation linked to indirect suppliers of JBS, Minerva, and Marfrig most prevalent

Most of the calculated deforestation can be attributed to the indirect supplier base of the three meatpackers. In the sample, deforestation alerts are at least four times larger in the indirect supplier base of all three meatpackers combined (65,712 ha) compared to the direct suppliers (15,470 ha) (Figure 9). Moreover, 19 percent (15,255 ha) of the deforestation alerts can be attributed to indirect suppliers that supply to all three meatpackers, compared to only 1.5 percent (1,000 ha) of the deforestation alerts in the suppliers’ sample that could be linked to direct suppliers that serve all three meatpackers simultaneously. This discrepancy confirms that deforestation risks in indirect supply chains are higher, and adds that indirect suppliers tied to deforestation more regularly tend to supply all three meatpackers at once.

Within the sample, JBS is most exposed to deforestation both in absolute and relative numbers, compared to the rates linked to Marfrig and Minerva. But the lower number of suppliers to Minerva and Marfrig covered in the sample may explain part of this difference. Deforestation alerts in JBS’s indirect supplier base are more than three times the size of its direct supplier base, but for Marfrig this number is more than seven times higher, and for Minerva more than eight times higher (Figure 9).

Legal and reputational risks for breaching EU Deforestation Regulation

Since meatpackers do not monitor all their indirect suppliers, they cannot guarantee compliance with the upcoming EU Deforestation Regulation. In particular, high deforestation alerts since the December 2020 cut-off date in the indirect supply chains of JBS, Marfrig, and Minerva raise concern about compliance with the EU Law and forest conservation in general. While meatpackers have made progress on compliance in direct supply chains, they have shown little progress on indirect supply chain monitoring. The deadlines for achieving full supply chain transparency, including that of indirect supply chains — earliest in 2025 or latest in 2035 — are out of pace with the implementation of the EU Deforestation Law. The Law will likely enter into force in 2023, with most requirements applicable one or two years later.

Meatpackers JBS and Minerva monitor only illegal deforestation linked to their suppliers, while the upcoming EU Law will also consider legal deforestation as non-compliant. This part of the Law is particularly relevant in Brazil’s Cerrado, where, depending on the location, 65 to 80 percent of the properties can be developed and cleared from native vegetation. With approved environmental license, clearing of these properties is considered legal under the Brazilian Forest CodeIn response to a draft version of this report, Minerva says that it monitors illegal deforestation for 100 percent of its direct suppliers and confirms its compliance with Brazilian environmental regulations. However, this would not meet the upcoming EU import restrictions that forbid both legal and illegal deforestation-linked beef and leather imports, for both direct and indirect cattle supply chains.

Marfrig is the only meatpacker company that is committed to zero deforestation by 2025 (for the Amazon, 2030 for the Cerrado), both for legal and illegal deforestation. This commitment increases the company’s likelihood to eventually comply with the upcoming Regulation. However, Marfrig’s incapability to currently monitor all its indirect suppliers shows a gap in compliance with the Regulation’s expected requirements.

JBS has committed to achieving zero deforestation across its full global supply chain only by 2035.

Breaching the upcoming EU Law may imply legal risks for the three meatpackers. The Regulation foresees legal prosecution of those in violation of the Regulation through the application of penalties, namely fines proportional to the environmental damage caused and temporary exclusion from procurement processes. While JBS, Marfrig, and Minerva are large suppliers to the European market, it remains unclear what proportion of the non-compliant produced beef and leather eventually ends up in European supply chains.

Breaching the Regulation may also involve reputational risks for meatpackers, leather operators, and fast-moving consumer goods companies (FMCGs). The European Parliament has proposed to publish a list of operators and traders that are non-compliant with the EU Deforestation Regulation. If adopted in the final voting rounds, the list will be made available by the European Commission, and will unquestionably be used in advocacy and potentially litigation by civil society organizations (CSOs) and law charities, which have been strongly in favor of the inclusion of this list of non-compliant companies.

Reputational risks for downstream players will increase from CSOs that mainly target well-known downstream companies and retailers that use beef and leather. In December 2021, European supermarket chains J Sainsbury, Lidl, Auchan, Ahold Delhaize, and Carrefour dropped beef products originating from JBS in Brazil after CSOs’ allegations of links to deforestation. Others have targeted European car manufacturers Volkswagen, BMW, Daimler, and Renault for using leather linked to deforestation and originating from JBS, Marfrig, and Minerva. Increased scrutiny of downstream suppliers’ compliance with the EU Deforestation Regulation has been reflected in the many calls for an ambitious EU law on deforestation.

Mitigated financial risks for meatpackers, FMCGs, and financial institutions

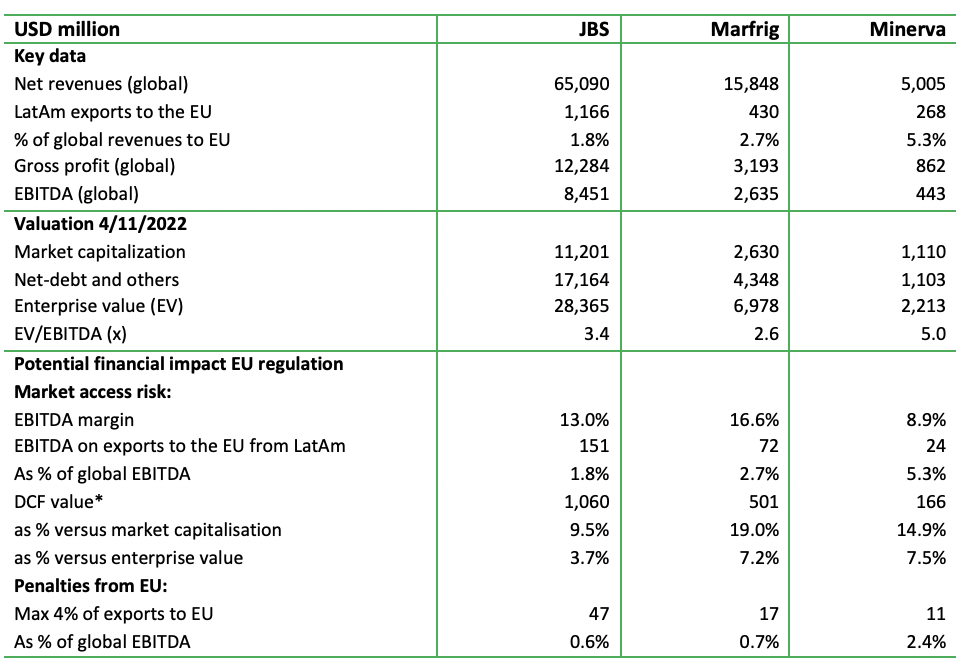

JBS, Marfrig and Minerva may face market access risk, fines, and financing risk. EU-based consumer facing companies and EU-based financial institutions could see value risk and reputation risk. Due to the upcoming EU Deforestation Regulation, the meatpackers may face difficulty in exporting beef and leather to the EU market. Being cut off from the EU market would impact net revenues, gross profit, EBITDA, and net profit. If companies continue to export, they might face fines. Reputation value is the risk category that dominates the EU-consumer facing downstream industry that sources beef and/or leather from Latin American (LatAm) meatpackers, and indirectly for their financers.

Meatpackers’ exports to the EU are a small part of their total revenues (Figure 10), resulting in a value risk for their shares. Maximum penalties are a low percentage of global profits. The meatpackers do not provide detailed numbers for beef and leather products’ exports, and export numbers occasionally refer to other areas besides LatAm. As a result, beef and leather product exports from LatAm may be a lower value number than calculated in line 3 of Figure 10. Marfrig is a large exporter to the EU. Of its South American revenues, 58 percent is exported. Of these exports, 18 percent is sent to the EU. JBS’s export exposure to the EU is much smaller, seven percent. However, this number includes exports to the EU from other JBS units, like its US business which has no deforestation issues. Because of these two companies’ large activity in the U.S. market, the percentage of revenues from LatAm exports to the EU is relatively low. Minerva’s global business mainly originates in LatAm, and its total exposure to EU exports relative to global revenues is the highest of the three meatpackers.

If companies face restrictions to export beef and leather products to the EU, they may lose profits. Based on EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization) margins, the loss of annual EBITDA (1.8 to 5.3 percent) is the basis of a calculation of a value number for an infinite period, based on discounted cash flow methodology. This value would be relatively high for Marfrig when compared to its current market capitalization (19.0 percent), but much lower for JBS (9.5 percent). Moreover, for JBS, this number also includes exports to the EU from other regions and products other than LatAm beef and leather. Thus, JBS’s comparable number versus Marfrig and Minerva may be even lower.

Penalties for operators and traders in case of non-compliance could be a maximum of at least four percent of turnover in EU member states. For the meatpackers, this amount would be relatively low, at 0.6-2.4 percent of global EBITDA (Figure 10).

Investors seem skeptical about the future cash flow of the current meat profits of JBS, Marfrig, and Minerva and may already discount “sustainability” headwinds. This skepticism can be concluded from the low valuation of the meatpackers: the EV/EBITDA multiple is in a 3.4-5X range (Figure 10) versus >10 for most fast-moving consumer good companies. No investor surveys are available to explain the reason for the lack of confidence in future cash flow streams. Reasons might include emerging market exposure, links to deforestation and lack of animal welfare, the volatile profit environment, human right violations (indigenous people rights, workers’ rights), and a lack of good governance within the companies.

Figure 10: Meatpackers’ exposure to the EU market and financial risk

Source: Profundo, companies’ result presentations 2021, Bloomberg; *DCF = Discounted Cash Flow, assuming 10% discount rate and 0% growth rate.

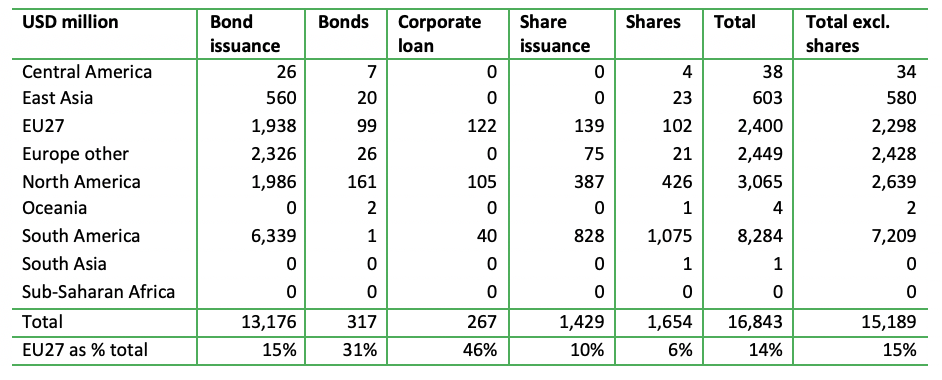

Meatpackers face financing risk, while EU financial institutions may be confronted with reputation risk. EU financial institutions are not yet directly affected by the EU Deforestation Regulation, and they might continue to finance meatpackers’ beef and leather operations. However, they could face conflict with their own ESG policies and commitments. Moreover, civil society campaigning could lead to reputation risk. Consequently, EU financial institutions would become increasingly hesitant to continue financing meatpackers, and capital costs may increase for JBS, Marfrig, and Minerva, impacting their value. EU financers contributed approximately 15 percent to financing the three meatpackers in 2013-2022. In bonds and corporate loans, the EU financers provide 31-46 percent of the total. As percentage of their total assets, the identified total in Figure 11 (USD 2.4 billion) is a very small part of all assets of EU financers (bank assets only are already USD 27 trillion and exclude shares and bonds).

Figure 11: Financing of JBS, Marfrig and Minerva (region-based)

Source: Profundo, based on Forests & Finance; all data based on identified financial relations in 2013-2022. Bilateral financial relations can often not be identified.

FMCGs, retailers, and fast-food companies may face mitigated reputation value risk. The reputation value of a company is based on interactions with all stakeholders, including suppliers, customers, employees, financers, and investors. They may disengage from consumer-facing companies that are not proactive on eliminating sourcing products linked to deforestation. A recent study on the materiality of profits linked to (embedded) LatAm beef and soy concluded that the exposure to LatAm beef, which is sourced by FMCGs for a part for their EU activities, is high for McDonald’s (6.4 percent) but relatively low for Nestlé (0.001 percent) and Carrefour (1.1 percent). For Carrefour, the major portion of its Brazilian-sourced beef products is sold in LatAm. Translating these embedded LatAm beef exposure numbers into a value of reputation risk could mean that up to one-third of the exposure (for McDonald’s one-third of 6.4 percent = 2.1 percent) may be lost in the share price due to reputation risk. As a result, reputation risk values will be relatively small for beef only (if sourcing of LatAm embedded soymeal is included, the numbers will be higher). As a result, reputation risk values will be relatively small for beef only (if sourcing of LatAm (embedded) soymeal is included, the numbers will be higher).

Figure 12: Selection of companies with LatAm beef sourcing (2021)

Source: Profundo, based on the report “Financial Materiality in Latin American Soy and Beef Supply,” July 2022.

Downstream sectors in the EU leather chain face reputation value risk, but it could be relatively small compared to total value in the supply chain. For leather, no comparable study is available (like the one for beef mentioned in the preceding paragraph). The EU import value amounts to EUR 1,422 million, mainly from LatAm leather (Figure 1). Globally, around half of the leather exported from Brazil is used in the automotive sector, while the other half is distributed, for a large part, in the footwear and upholstery sectors.

EU-based sectors active in the leather supply chain are financially exposed to Brazilian leather and could be subject to reputation risk. The financial exposure can be material, and the value can be estimated by calculating the price elevation in every step of the supply chain in imported leather. For instance, leather used in cars first goes from an Italian leather company to a Czech seat company, and these seats are sold to a car manufacturer, and then car dealers sell the cars to consumers/customers. All these steps lead to an accumulation of gross profits and operating profits on the embedded Brazilian leather. Financers (investors and banks) could disengage, employees could become more reluctant to work for the companies, and consumers less eager to buy the products. The EU automotive sector, including suppliers, represents currently 7 percent of the EU GDP (2021, EUR 14.5 trillion), or EUR 1.02 trillion. Assuming that half of the imported Brazilian leather (EUR 711 million) is used in the EU automotive chain, this totals just 0.07 percent of the automotive’s GDP contribution. Similar to beef, the value of Brazilian leather imports for the EU automotive sector is a relatively small amount of the end product bought by consumers.

Leather is probably a relatively larger input for other industries (shoes, upholstery) than for the EUR 1.02 trillion automotive sector. For instance, the EU shoe industry generated EUR 28 billion turnover. Assuming 25 percent of EU Brazilian leather import is used for shoes (EUR 356 million), the financial materiality of this leather (1.3 percent of USD 28 billion revenues) in the shoe industry is larger than in automotive (0.07 percent; see above). More than 100 fashion brands could be linked to Brazilian leather. For individual companies in the leather supply chain, the financial exposure to embedded Brazilian leather might be material but needs additional research.

Financial risks can be avoided by “doable” due diligence expenditures. In various reports, CRR has calculated the costs of an investment in a best-in-class zero-deforestation policy execution for palm oil, beef, and soy, including auditing, monitoring, and verification. Potential benefits (for instance reputation value protection) exceed these costs significantly. CRR analysis has shown that it would take a low, single-digit price increase to pass on these costs to customers and keep profits for shareholders intact. Also in leather, the large size of the automotive and shoe industry versus the imported value of Brazilian leather supports such an analysis.