Palm oil buyers with No Deforestation, No Peat, No Exploitation (NDPE) policies have increasingly removed deforestation-linked palm oil suppliers from their supply chains. However, some palm oil buyers remain linked to deforestation as their palm oil suppliers continue to deforest in other sectors, such as timber and mining. Currently, NDPE policies are still applied to only the palm oil supply chain rather than the entire corporate entity of suppliers. This report analyzes the status of cross-commodity NDPE approaches at every stage of the palm oil supply chain and among financial institutions, how to leverage opportunities for implementation, and key challenges ahead.

Download PDF here: Lack of Cross-Commodity NDPE Implementation Allows for Deforestation

View the recording of our webinar discussing this report

Join our webinar January 26th to discuss the findings of this report.

Key Findings:

- Leading Southeast Asian holding companies are active in palm oil as well as in timber and/or mining. NDPE-compliant palm oil plantations are at risk of having links to timber activities responsible for deforestation and mining operations with a broad set of environmental violations.

- Cross-commodity NDPE risks have been overlooked in regulations, voluntary certification schemes, and supplier codes of conduct. Deforestation regulation and corporate sustainability due diligence proposals, such as those in the EU, are focused on domestic companies and their product streams, instead of the structure of upstream companies. Codes of conduct, RSPO principles, and accountability initiatives also lack explicit criteria for cross-commodity coverage.

- Investigated companies and financial institutions focus only on palm oil in NDPE compliance. Statements on scope prompt confusion about which part of the suppliers’ entity is covered. Refineries, oleochemical suppliers, fast-moving consumer good companies, retailers, fast-food companies, banks, and investors typically never explicitly mention cross-commodity risks. Less than five percent of palm oil-linked debt and less than two percent of shares and bonds are covered by a cross-commodity approach.

- Meanwhile, the palm oil supply chain and its NDPE approach form the best platform to leverage NDPE across all forest-risk commodities. NDPE policy in palm oil is much more advanced than in timber and mining, while identified financing in Southeast Asian palm oil is also much larger than for other sectors which enables engagement by banks and investors.

- Additional costs of a cross-commodity NDPE approach are relatively low. A large part of the policy/monitoring “infrastructure” already exists and companies do not need to pay a price premium for materials that are not in their supply chain. Financial risks will increase for all companies in the palm oil supply chain if there is increasing scrutiny by NGOs and policymakers of cross-commodity violations.

Introduction: Cross-commodity is not a multi-commodity NDPE policy

The absence of a cross-commodity NDPE approach is a policy gap that will not be solved with a multi-commodity NDPE policy. With a cross-commodity NDPE policy approach, a fast-moving consumer good (FMCG) company will not buy palm oil from a plantation company if the holding company that owns the palm oil business deforests in its timber or mining activities, while the FMCG does not buy any timber, coal, or gold from the relevant holding company. The absence of a cross-commodity NDPE approach is a gap in these policies that may move higher on the agenda of policymakers and NGOs in the coming years. Holding companies with an NDPE policy in their palm oil plantation activities might still deforest or breach human rights in their mining or timber activities.

Many large direct and indirect buyers of palm oil, such as refineries, FMCGs, and other downstream companies, have introduced NDPE policies for palm oil. Gradually, many of these companies have extended the NDPE framework to other agricultural commodities that can be linked to deforestation, like timber, soy, and beef. However, these “multi-commodity” NDPE policies are usually only applied to the commodities in the companies’ own supply chains. This means that an NDPE commitment on soy or beef is applied only to soy or beef products directly sourced by the company.

Holding groups active in palm oil might also be active in mining and timber

Since the palm oil plantation sector has strong links with the timber sector, an NDPE-compliant palm oil unit could be confronted with NDPE violations in timber. A 2021 report showed that many of the largest plantation developers in the industrial timber sector also work in the palm oil sector. Nearly all large palm oil refineries were sourcing palm oil from groups that had deforested 133,040 hectares of tropical forests for their industrial timber activities in the period from 2016 to March 2021. These “deforesting” groups were on the palm oil mill list of the refineries and, consequently, many FMCGs. Some of the largest deforesters for industrial timber supplied palm oil to buyers with NDPE policies.

The oil palm and the industrial tree sectors are the two largest plantation sectors in Indonesia and Malaysia. In both countries, it is common for companies to operate plantations in both sectors. In Indonesia, 64 percent of all industrial tree plantation permits are held by company groups that also grow oil palm. In Sarawak, the six largest companies in oil palm plantation development are estimated to hold 69 percent of the state’s industrial tree plantation concessions.

Examples of “successful” cross-commodity implementation by palm oil buyers do exist. Samling has become a showcase of a cross-commodity issue: As an NDPE-compliant palm oil company, it deforested in its timber business group. Several FMCGs suspended the group from their palm oil sourcing lists. United Malaccca is another example. After pressure from palm oil buyers, United Malacca agreed to stop work on the industrial timber concession. However, another company, Djarum, with clearing of 10,833 ha of forest on its industrial timber concessions in Indonesia from January 2016 to March 2021, continues to supply palm oil to many leading refineries and downstream FMCGs.

The palm oil and mining sectors have strong links. Links through holdings can connect an NDPE-compliant palm oil plantation with environmental violations by a sister company engaged in mining. A 2021 Chain Reaction Research (CRR) report proved a substantial overlap in company groups conducting mining and palm oil businesses. Of the ten largest oil palm growing companies in Indonesia, at least six also have mining businesses. And among the ten largest coal mining company groups, at least five also have palm oil businesses. Mining in Indonesia comes with large environmental impacts on forests and communities, which could include deforestation, along with contamination of water resources and other pollution.

Cross-commodity NDPE approach absent in EU regulation and other initiatives

EU deforestation and supply chain regulation proposals, voluntary certification schemes, accountability initiatives, and company supplier codes are currently not covering a cross-commodity NDPE approach, or they lack explicit criteria. The EU Deforestation Regulation proposal agreed in December 2022 does not cover problems related to cross-commodity compliance. The regulation is focused on certain commodities and products associated with deforestation and forest degradation. The regulation requires that EU-based operators and traders should conduct due diligence analysis for all separate commodities they source. The regulation does not discuss the structure of the palm oil groups exporting palm oil products to the EU. Moreover, the EU Corporate Sustainability Due Diligence (CSDD) directive proposal does not cover cross-commodity risks. There are many phrases about “scope,” but these refer to the companies active in the EU. Equivalent deforestation and supply chain proposals in other jurisdictions have similar shortcomings.

The criteria of the Roundtable on Sustainable Palm Oil (RSPO) provide no clarity about its NDPE scope. The RSPO’s definition of “group level” refers to entities “involved in activities related to the palm oil supply chain.”

The Accountability Framework initiative (AFi), advanced through the work of a diverse coalition of organizations dedicated to protecting forests, natural ecosystems, and human rights by making “ethical production and trade” mainstream, expects a broad-scope interpretation of ethical codes in supply chains. This means that buyers could expect that their ethic codes are respected by the suppliers’ entire business. If companies apply this initiative in their supply chains, a cross-commodity NDPE approach could be covered. As a backstop, ethic codes for suppliers, often formulated in codes of conduct, could broaden the responsibility and the scope. Through these codes, buyers could expect NDPE from all the supplier’s activities, although most codes do not provide details on deforestation or NDPE. Overall, these initiatives and codes often lack explicit criteria for cross-commodity coverage of NDPE requirements.

Palm oil sector could play leading role in advancing cross-commodity NDPE commitments

Buying palm oil products from holdings that are active in various forest-risk supply chains affects the entire supply chain. While the risk of cross-commodity deforestation originates with the upstream actors (plantations), the impact is seen further down the chain:

- Midstream companies (trading, processing/refining, oleochemicals) source from plantations owned by holdings

- FMCGs buy palm oil and derivatives from midstream companies

- Supermarkets, food service companies, and fast-food chains buy palm oil products from FMCGs

- Financers (banks, investors) provide loans or invest in companies at various levels of the palm oil supply chain through buying shares and/or bonds

The status of NDPE policies in the palm oil sector makes it logical that it plays a leading role in advancing cross-commodity commitments. Most leading palm oil plantations (16 out of 21) in Indonesia have an NDPE policy, while, for instance, only three of the 21 largest industrial tree growers have one. In mining, NDPE policies are absent. On top of this, downstream actors in the palm oil supply chain are already much further on the path to halting deforestation versus the downstream actors in mining and timber/pulp & paper.

Although palm oil is ahead of other sectors, NDPE policies of nearly all companies in palm oil refer clearly to only palm oil activities of the supplier group and also prompt confusion. The following section investigates whether the NDPE policies of leading companies in the palm oil refining and oleochemical sector, in the FMCG sector, in food retail and fast-food, and in the financial sector contain a clear intention for a cross-commodity NDPE policy approach. In some instances, examples of grievance approaches will be added to illustrate a company’s position.

Refiners and oleochemicals have a crucial position in the palm oil value chain, but lack cross-commodity NDPE policies

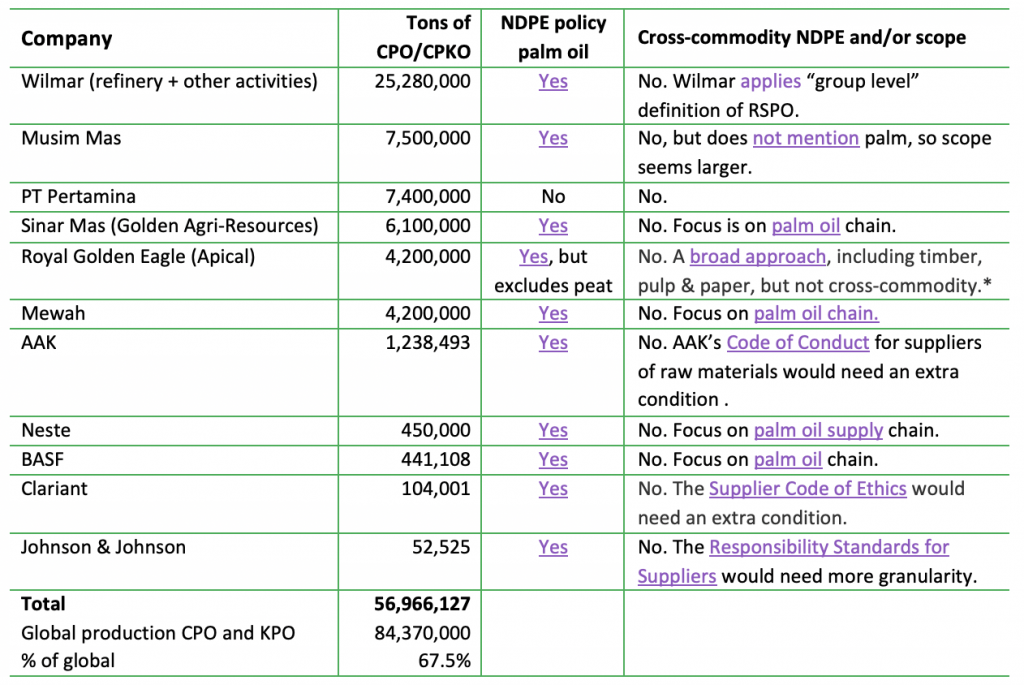

A small group of refiners, biofuel producers, and oleochemical companies have a large market share in sourcing palm oil but lack a cross-commodity approach. Within the palm oil supply chain, refineries have a crucial position as most palm oil flows through this bottleneck, which consists of a limited number of companies. Including oleochemicals, the top 11 in these groups process 68 percent (Figure 1) of the global palm oil production. Excluding oleochemicals, the top seven palm oil refiners account for 59 percent. Thus, the palm oil processing industry could have leverage on the palm oil plantation sector to halt deforestation in its palm oil as well as its non-palm activities.

Palm oil refiners currently apply NDPE policies only to oil palm plantation development, and so far, they have not used extensively their economic leverage on business partners that cut down forests for industrial tree concessions. A report by AidEnvironment, further elaborated on in a webinar, concluded that investigations in response to complaints/grievances by palm oil refineries led to answers that the deforestation/NDPE violations ”did not occur in the palm oil supply chain.”

Wilmar, which has a leading position globally in palm oil, could take the lead in moving forward with an explicit cross-commodity NDPE policy. Until now, Wilmar says that it applies the RSPO definition of “group level” for its suppliers. The RSPO’s definition of “group level” refers to entities “involved in activities related to the palm oil supply chain.” Initially, Wilmar replied that in the Samling and the Rimbunan Hijau Group cases, land clearing was “not related to oil palm development.”

The strong growth of using palm oil in the biofuel sector creates a large risk for zero-deforestation and cross-commodity initiatives. The growing share of biofuels in the palm oil refining sector will not support a quick change to a cross-commodity NDPE approach. Biodiesel refineries already use 23 percent of palm oil production, and this could further increase. Some refinery groups that supply to the FMCG as well as the biofuel market are relatively advanced in their NDPE approaches because of pressure from international FMCGs. However, stand-alone biofuel refineries have no links to FMCGs. The leading Indonesian biofuel producer PT Pertamina, also active in fossil fuels, lacks an NDPE policy. Overall, biofuel produced by Big Oil lacks sourcing transparency and is already a major source of leakage. Neste, another large biofuel refiner, focuses strongly on palm oil and not on cross-commodity risk.

The current lack of refiners’ traction on cross-commodity policies increases risk for downstream actors. Palm oil refineries could play a key role in solving the cross-commodity NDPE problem. Although they have NDPE policies for palm oil, their execution is often via mass balance (MB) and Book & Claim (B&C), with a lack of focus on segregation. The transparency of “derivative” palm oil products is low, while palm oil processors are key sources of transparency and NDPE attainment and progress. Lack of action by refiners and oleochemical companies hinders industry transformation and the ability of retailers and brands to achieve their NDPE commitments faster. Overall, the group’s status on palm oil NDPE execution remains relatively weak, so cross-commodity NDPE policy is not on their radar until it is raised by customers. Leaders in the refinery and oleochemical group continue to defend their position with statements that costs of best-in-class transparency and traceability are too high and that FMCGs do not want to pay premium prices.

Figure 1: Refineries and oleochemicals: Scope of NDPE policies for palm oil

Source: Chain Reaction Research (reports Profit Chain and Wilmar), AidEnvironment, Palm Oil Buyers Scorecard (WWF), company websites; *) a multi-commodity NDPE policy, thus for each commodity it sources, instead of a cross-commodity policy.

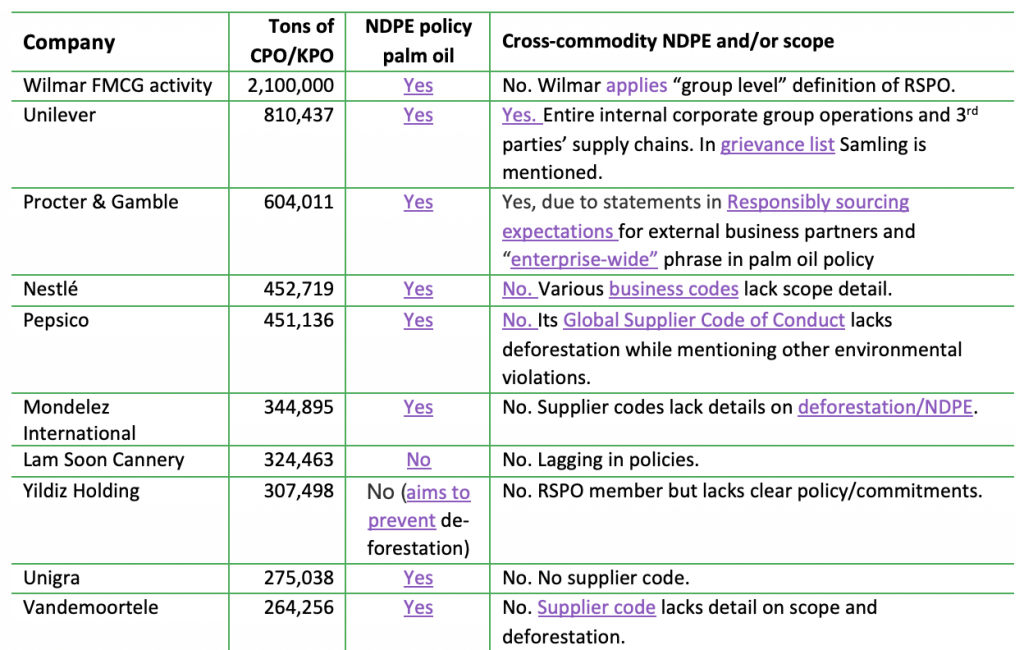

FMCGs lack cross-commodity NDPE approach

FMCGs’ policies focus on their suppliers’ palm oil activity, and in some cases struggle with the definition of “entity” and/or “group level” of its suppliers. The leading companies are the top 30 sourcing FMCG companies in the WWF Palm Oil Buyers Scorecard (POBC), plus Wilmar’s FMCG activity (Figure 2). The top 30 FMCG palm oil buyers source 9.3 percent of the global crude palm oil (CPO) and crude palm kernel oil (CPKO) production. This market power could work as a leverage to develop a cross-commodity NDPE approach. Within the group, Unilever is explicit on a cross-commodity NDPE approach. Also, its grievance list refers to the Samling case. However, most FMCGs are not explicit about a cross-commodity approach. Many FMCG NDPE policies refer to the suppliers’ palm oil activities and palm oil associates, while terms such as “enterprise-wide,” “entire” and “company-wide” are not explained.

Others have a mixed approach. While Hershey’s NDPE policy is unclear in its scope, its reaction on non-palm deforestation complaints at Rimbunan Hijau suggests it has a cross-commodity NDPE approach. Hershey also handled a grievance on deforestation in Agincourt’s gold mining development in North Sumatra. Agincourt is a sister company to palm grower and trader, PT Astra Agro Lestari, through parent company, Astra International (majority-owned by Jardine Matheson). PZ Cussons, which is not in the list, has an NDPE policy and lacks an explicit statement on cross-commodity, but it has evolved its grievance approach for inclusion and engagement with suppliers for cross-commodity cases.

Some FMCGs might turn to a limited number of 100 percent palm oil companies, while others continue to be affected by lack of transparency in the midstream sector. Some companies are not incentivized to introduce a cross-commodity approach and have reduced their suppliers base and only focus on 100 percent palm oil companies, according to one NGO. An example is Mars, which intends to reduce, in two years, the number of supplying palm oil mills from 1,500 to 50 by end of 2022. Another reason for the lack of action in FMCGs cross-commodity approach is that they are very dependent on palm oil refineries and oleochemical companies from which they are sourcing. The refining and oleochemical sectors continue with a low level of transparency in derivatives in particular.

Figure 2: FMCGs: Scope of NDPE policies for palm

Source: Source: Chain Reaction Research (reports Profit Chain and Wilmar), Palm Oil Buyers Scorecard (WWF), company websites

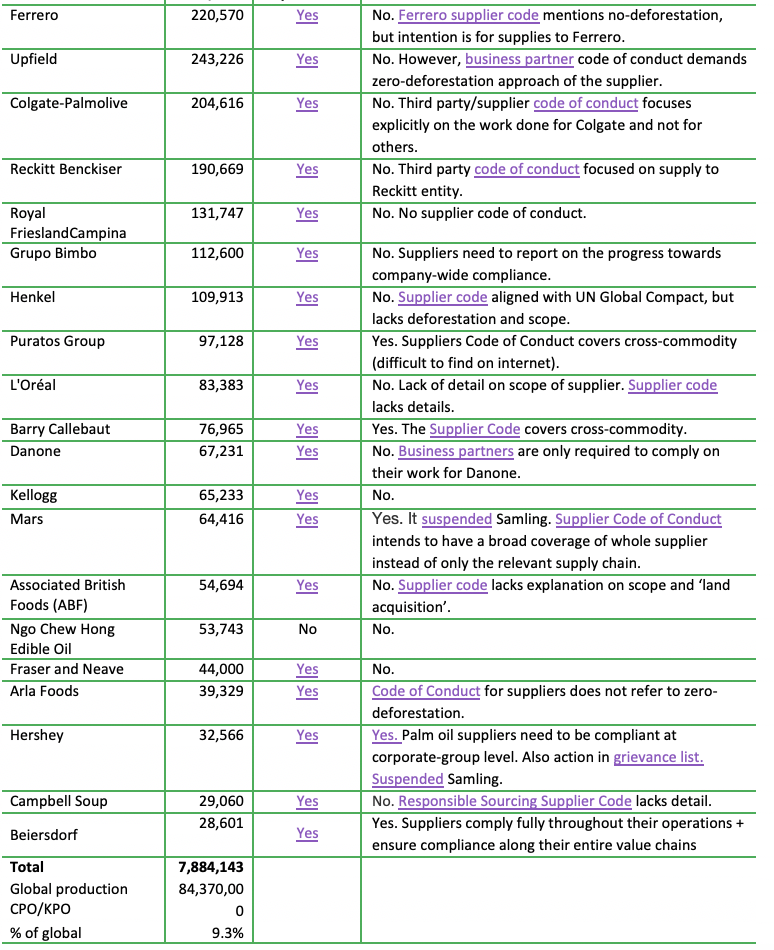

Retailers and fast-food lack cross-commodity policy and individual leverage

Further downstream, food retailers and fast-food companies lack a cross-commodity approach. In the list of leading companies, NDPE policies are relatively weak compared to the sectors further upstream (Figure 3). A reason is the large number of stock-keeping units (SKUs) on their shelf containing (embedded) palm oil. The companies in these sectors tend to shift responsibility for zero-deforestation to their suppliers. When they have an NDPE policy, the focus is often on private label products. The backlog in NDPE policy development and execution versus other levels in the supply chain also leads to the absence of an explicit cross-commodity approach. Codes of conduct for suppliers could form the start of such an approach, but these often lack detail.

The high level of fragmentation in food retail does not enable the leverage or any leadership in the change to a cross-commodity approach. The total palm oil sourced by each of the top 11 supermarkets as well as by this top 11 group in total (the group sources 0.9 percent of global CPO/KPO production) lacks market power to create leverage to upstream companies in the supply chain.

Figure 3: Retailers and fast-food: NDPE policies palm and cross-commodity policies

Source: Chain Reaction Research, AidEnvironment, Palm Oil Buyers Scorecard (WWF), company websites; *) MB = Mass Balance, SG = Segregation, B&C = Book & Claim

Financers lack a cross-commodity approach

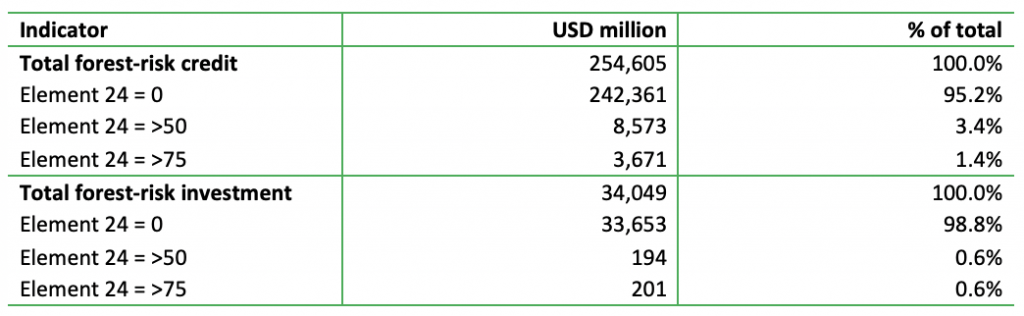

Palm oil financers do not, in general, have NDPE policies that apply to the “entire corporate group.” Forests & Finance’s (F&F) methodology for policy assessment contains “criterium 24,” which investigates whether the financial institution applies its forest-risk policies to the entire corporate group. Of the 3,000 financers identified, 200 have been investigated on criterium 24 and only three of them had a cross-commodity NDPE approach (score = >75). Of the loans, 95.2 percent have been issued by financial institutions lacking the crucial scope addition (score = 0), and for investments (shares, bonds) this number is 98.8 percent.

Figure 4: Selection of financial institutions and scope of forest-risk policy

Source: Chain Reaction Research based on Forests & Finance. Data are segment adjusted, and refer to identified financial relations in 2016-Sep 2022

Figure 5: Top 10 and top 20 palm oil financers

Source: Chain Reaction Research based on Forests & Finance. Data are segment adjusted, and refer to identified financial relations in 2016-2022

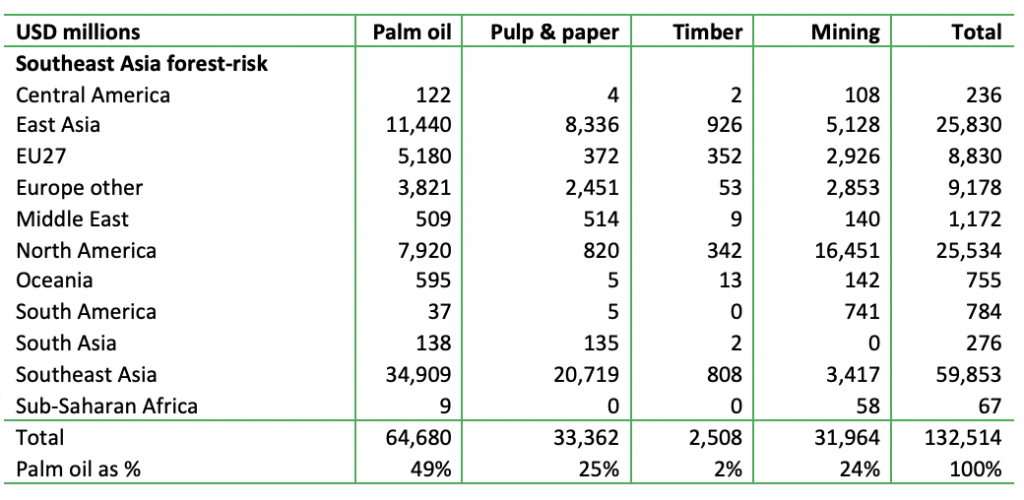

The size of palm oil financing suggests that the sector has potential leverage over others. The identified financing provided to palm oil producers in Southeast Asia (49 percent of the total, see Figure 6) is larger than the identified financing of timber, pulp & paper, and mining, which are other forest-risk product groups. Palm oil producers’ dependence on external financing gives leverage to financial institutions to require more stringent conditions in other companies connected to the palm oil borrower. The data provides no granularity on connections between palm borrowers and borrowers active in other commodities.

Figure 6: Identified financing to forest-risk commodities (tropical areas)

Source: Chain Reaction Research, Forests & Finance

Financial institutions’ introduction of a cross-commodity NDPE approach has ample hurdles. One institutional investor (in an interview by CRR) said that it would be satisfied with a company applying its NDPE policy only in its relevant palm oil supply chain. The interviewee said that the next step in developing cross-commodity policies would be considered too large and/or too expensive. Therefore, support in the asset management industry would be minimal. Another hurdle is palm oil financing shifting to Southeast Asia and East Asia (see Figure 6) where financial institutions are lagging in their approach to NDPE.

Costs of a cross-commodity implementation policy are low

Additional costs of a cross-commodity NDPE policy are relatively low, since a large part of the policy and monitoring “infrastructure” is already in place and a premium price is unlikely for materials that are not in a company’s supply chain. Some FMCGs have introduced a cross-commodity NDPE approach and/or have handled grievances on this subject. Changing policies to be explicitly cross-commodity and handle grievances would lead to a limited increase in costs. The costs of a best-in-class execution of NDPE policy in palm oil, excluding cross-commodity additions, are equal to a low percentage of the revenues in palm oil-containing products. These costs consist of paying for infrastructure (auditing, due diligence, verification, salaries) and a premium pricing for palm oil. Adding timber and mining (or even rubber and cacao) in the scope would not lead to paying a premium price for these products as they are not sourced in a cross-commodity context.

Moreover, as AidEnvironment concludes, there are no practicalities standing in the way for refiners adding industrial tree plantations to their NDPE policies. Deforestation is easily detectable, and responsible traders could already monitor key landscapes in Indonesia and Malaysia. For downstream companies, monitoring would also only require paperwork (adjusting policies) and using current initiatives in verification and landscape monitoring.

However, a cross-commodity approach could have different monitoring costs in different commodity chains, based on the commodity characteristics. For instance, a palm oil buyer would need additional monitoring tools if the group from which it sources palm oil is also active in Latin American beef. In Latin American beef, the supply chain contains many indirect suppliers.

The relative costs of a best-in-class NDPE palm oil policy for refiners and oleochemical companies (the mid-stream) are higher than for downstream (FMCG/retail) companies. This is the result of the FMCG and retail sector generating 66 percent of the added value (gross profits) in the palm oil value chain, versus refiners and oleochemical companies with a total of 21 percent.

In the case of applying a cross-commodity NDPE approach of a palm oil buyer to LatAm beef activities of the same supplier, monitoring costs for FMCGs may still be relatively low. For a palm oil refiner, these costs may be relatively high, but the combination of palm oil supplier and LatAm beef producer is not common, if it even exists.

Currently, industry groups have not reacted enthusiastically to the extra costs that could accompany establishing cross-commodity policies. Several factors have led to increasing industry concerns about creating further challenges with stricter due diligence requirements for EU regulation and/or extra NDPE compliance costs. Commodity supply chain actors regularly use the price increases of overlapping global crises – the COVID-19 pandemic, the Russian invasion of Ukraine, the drought in South America affecting the vegetable oil market – as arguments to delay or postpone extra policy costs. One leading FMCG representative has previously pointed out that at a time of commodity scarcity (after the Russian invasion of Ukraine) the market did not offer the luxury of establishing more policy targets.

Financial risks of lacking cross-commodity NDPE policies

The lack of a transparent cross-commodity NDPE policy may become a risk in the coming years. As the cross-commodity NDPE risk is not in the EU Deforestation Regulation proposal, EU traders and operators involved in the importation of palm oil will not see fines or litigation when the palm oil comes from a corporate group that is deforesting in other supply chains such as timber.

However, if cross-commodity NDPE risk sees wider scrutiny from civil society organizations, companies experiencing cross-commodity deforestation may face reputation risk, market access risk, and financing risk. For FMCGs, reputation risk could become material when palm oil is a relatively large part of their supply, and/or when a large part of their products contains palm oil and their profits are relatively dependent on palm oil-related products. One example is Procter & Gamble (P&G), which indicate that 20-40 percent of its products contain palm oil. Such dependence could lead to reputation risk that is 30 percent of the market value of a company. This type of situation could lead to a shareholders rebellion, such as what occurred with P&G because of its palm oil sourcing execution.

While reputation risk could be material in the palm oil supply chain, CRR concluded that the implementation and monitoring costs of NDPE policies and/or the compliance costs to EU Deforestation regulation are a small part of the reputation value-at-risk. The addition of an explicit cross-commodity NDPE condition and the additional monitoring needed can be embedded in the existing infrastructure of policies and monitoring, requiring nearly no extra expenses.