Wilmar International is a leading company in the palm oil sector. It has 230,000 hectares of planted area and a 10 times greater palm oil footprint through its trading, refining, and fast-moving consumer good activities. Concerns about ESG violations and investor ratings have hampered Wilmar, an early adopter of RSPO certification and a frontrunner in NDPE. This report evaluates financers’ risks and engagement opportunities related to Wilmar.

Download the report here: Wilmar’s Refineries and Brands Lag in Implementation of ESG Policies

Watch our webinar covering this report.

Key Findings

- As the largest company in the palm oil supply chain, Wilmar is highly exposed to China. In 2020, 30 percent of the world’s palm oil and kernel oil moved through Wilmar’s supply chains. Over 50 percent of Wilmar’s sales and more than 40 percent of its profits are generated in China, with a major portion in palm oil. The company’s exposure to Europe has declined to four percent and halved in 10 years.

- Wilmar’s high profile in NDPE and RSPO policies contrasts with its implementation on the ground and in its whole supply chain. In 2004, Wilmar became an RSPO member, and in 2013 it introduced its NDPE policies. In all of Wilmar’s activities, including its consumer brands, 7 percent of embedded palm oil is RSPO certified versus 19 percent in the global market. The company’s data on financial support for smallholders lacks transparency, while Wilmar is linked to many ESG violations.

- Wilmar’s argument that it lacks resources to achieve best-in-class execution is at odd with its annual gross profit on palm oil of USD 1.8 billion. Globally, Wilmar sees the largest earnings from embedded palm oil. Execution of best-in-class NDPE policies and a contribution to re-planting of aging palm trees would require palm oil product prices charged to clients to be 6 percent higher.

- Rating agencies diverge on Wilmar. Although MSCI and DJSI/S&P are positive on Wilmar, Sustainalytics and CSR Hub are less positive. Since agencies have different weighting criteria, social and governance issues have led to Wilmar’s wide rating scores.

- Wilmar’s ESG efforts do not weigh against the global trend of increased regulation. Wilmar’s valuation shows a discount versus peers and its own five-year average, despite high valuation of its Chinese activities. Global adoption of EU regulations on sustainable finance and supply chains may weigh on profits and valuation unless Wilmar increases transparency on NDPE execution and uptake of premium-priced certified palm oil.

Wilmar International: Leading diversified agribusiness

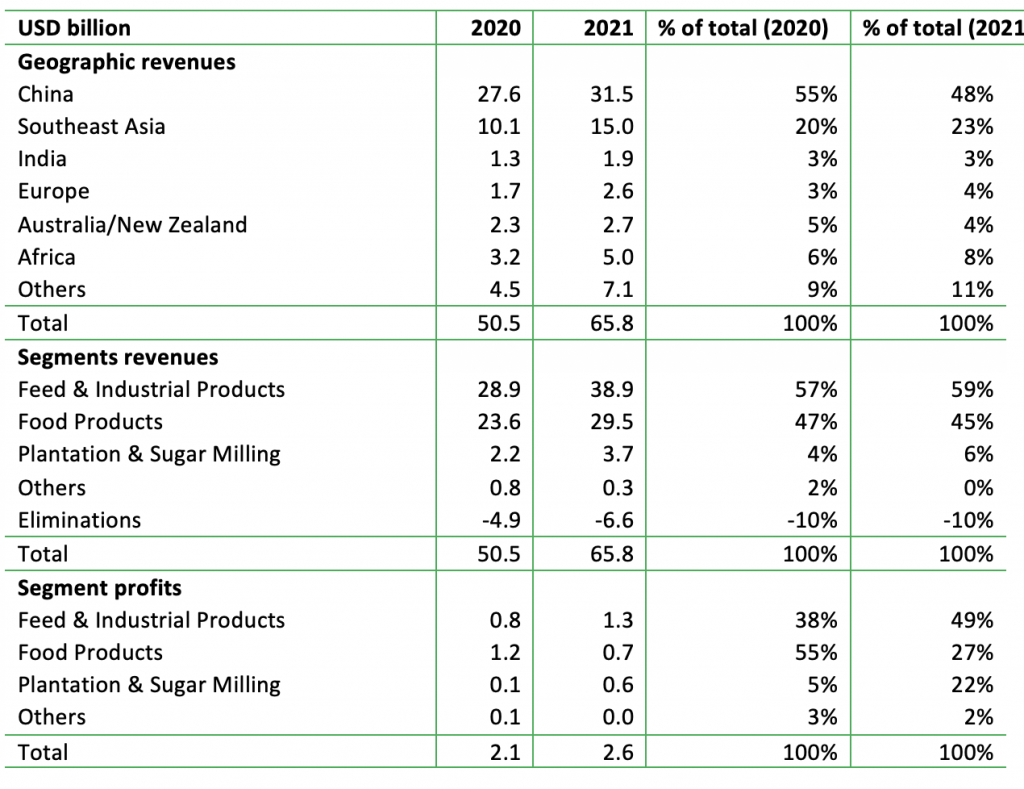

Wilmar, a leading Asian agribusiness group, is active in various agricultural supply chains, with revenues of USD 65.8 billion and net profit of USD 1.89 billion in 2021. Wilmar has an integrated agribusiness model that includes the entire value chain of agricultural commodity business, from farming and milling of palm oil and sugarcane to processing and selling of food products, animal feeds, and industrial agricultural products. Wilmar, which has more than 500 factories, has a large presence in China (2021: 48 percent of revenues), Southeast Asia (23 percent) and more than 50 other countries/regions (See Figure 1). The company has over 100,000 employees. The analysis in this report is based on public sources and discussions with investors, NGOs, and the company. Wilmar did not respond to CRR’s request for comment on the report.

Figure 1: Wilmar International – Geographical and segment division

Source: Wilmar annual reports; * before tax and associate/JV results

Wilmar operates three crucial product groups. Feed & Industrial Products (59 percent of 2021 revenues, 49 percent of profits) consists of processing and selling of animal feeds, non-edible palm and lauric products, other agricultural commodities, oleochemicals, gasoil, and biodiesel. Wilmar is a global leader in oleochemicals as its clients are home and personal care companies (detergents, shampoo, skincare etc.). Wilmar’s biodiesel plants are located in Indonesia and Malaysia. The company is a global leader in crushing of oilseed (various crops) with plants in China, India, Vietnam, Malaysia, Russia, Tanzania, Ukraine, South Africa, Zambia, and Zimbabwe.

The second group, Food Products (45 percent of 2021 revenues, 27 percent of profits), consists of processing and selling of edible food products, including vegetable oils produced from palm and oilseeds, sugar, flour, rice, noodles, specialty fats, margarines, chocolate, snacks, bakery, dairy, soy protein, starch, and sweeteners. Wilmar is a large wheat and rice miller in China and owns flour mills through joint ventures in Malaysia, Indonesia, India, Vietnam, and Thailand. In this group, cacao butter, cooking/margarine ingredients and ice-cream fats are also included. Strategically, Wilmar is moving gradually to the consumer sector, as it wants to become a supplier to the end-consumer.

Finally, Plantation & Sugar Milling (6 percent of 2021 revenues, 22 percent of profits) is Wilmar’s smallest product group. It has a total planted area palm oil of circa 230,000 hectares (ha): 65 percent in Indonesia, 26 percent in East Malaysia, and 9 percent in Africa. When considering smallholder schemes and joint ventures, this group’s area is doubled. This group has milling activities and fertilizer plants. Sugar mill plants are located in Australia, in India, Morocco, China, and Myanmar. These plants also sell electricity, ethanol, liquid fertilizer, and animal feed from byproducts. Wilmar owns 7,000 ha of farmland in Australia.

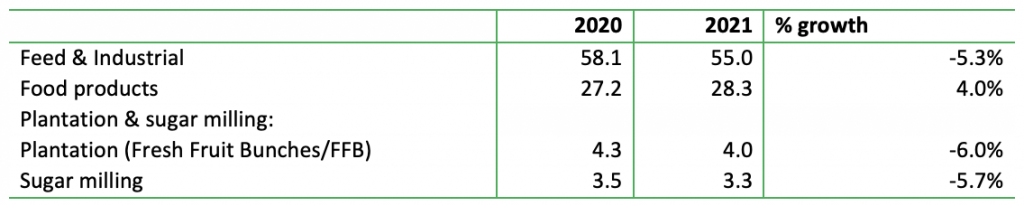

In 2021, revenues and profits rose sharply, which was mainly due to higher commodity prices, but volumes showed mixed results (see Figure 9 in Appendix). There were volume declines in most product groups, while Food Products grew by 4 percent year-on-year. Results benefited, on average, from higher prices.

Archer Daniels Midland (ADM) has a 20 percent stake in Wilmar, down from 24.9 percent in 2020. The China subsidiary, Yihai Kerry Arawana (YKA) Holdings Co. Ltd. was listed in October 2020 and the India joint venture, Adani Wilmar Limited, in February 2022. The Chinese subsidiary, in which Wilmar still holds 90 percent, generates circa 40 percent of Wilmar’s global net profit.

Wilmar International: A large presence in palm oil supply chains

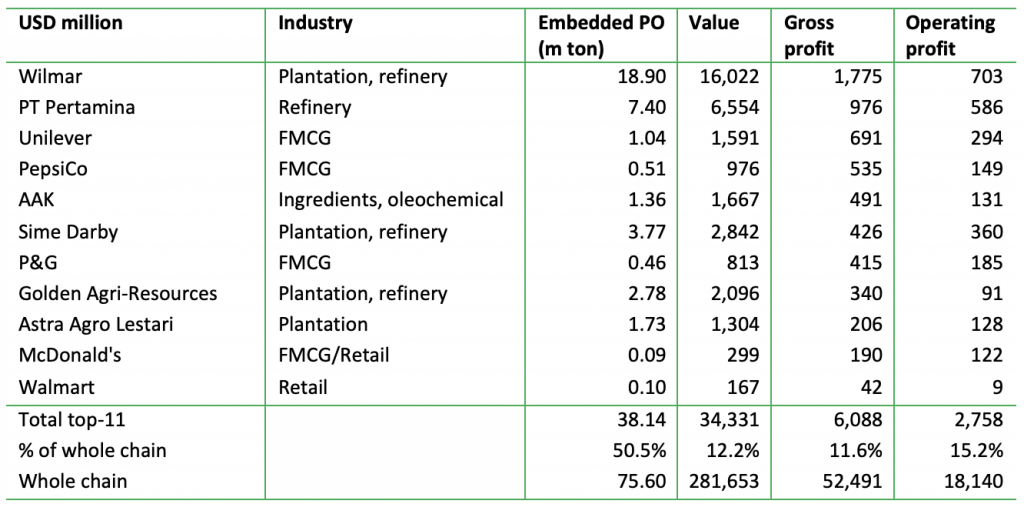

Wilmar is a leader in the palm oil value chain (see Figure 2), according to the CRR report “FMCGs, Retail Earn 66 percent of Gross Profits in Palm Oil Value Chain.” Wilmar’s position is based on its processing activities through refineries, including biodiesel, and to a lesser extent on its plantations. Based on data given by Wilmar to the RSPO (Roundtable of Sustainable Palm Oil), as well as a further increase in palm oil prices, recent volumes and values in palm oil are even larger than presented in Figure 2. When palm kernel oil is included, Wilmar handles 25 million metric tons in all palm-related activities. The company indicates that 41-50 percent of its global revenues is dependent on palm oil: the countries of origin are Ghana, Indonesia, Malaysia, and Nigeria (but appears to exclude Uganda).

Figure 2: Leading companies in palm oil value and profit chain (2020-gross profit ranked)

Source: Chain Reaction Research, mainly based on 2019/20 data and annual reports, Bloomberg. PO = palm oil.

Leading in NDPE policy, but low uptake of certified palm oil in its supply chain

Wilmar was an early adopter of NDPE in 2013, starting a decade of declining deforestation related to palm oil. In 2013, Wilmar stated its commitment to NDPE (No Deforestation, No Peat, No Exploitation) and became the first company to announce an NDPE policy. Wilmar, as a market leader, promised to ban buying from plantation companies involved in deforestation, development of peat lands, or conflicts with local communities from their supply chains. In many cases, Wilmar has kept its promise – sometimes after NGO pressure – by excluding various plantation companies from supplying its refineries. A large number of companies active in the palm oil supply chain have followed Wilmar by introducing NDPE policies or RSPO certification (see next paragraph). Companies adopting these changes has led to a significant decline in deforestation linked to palm oil expansion in Southeast Asia.

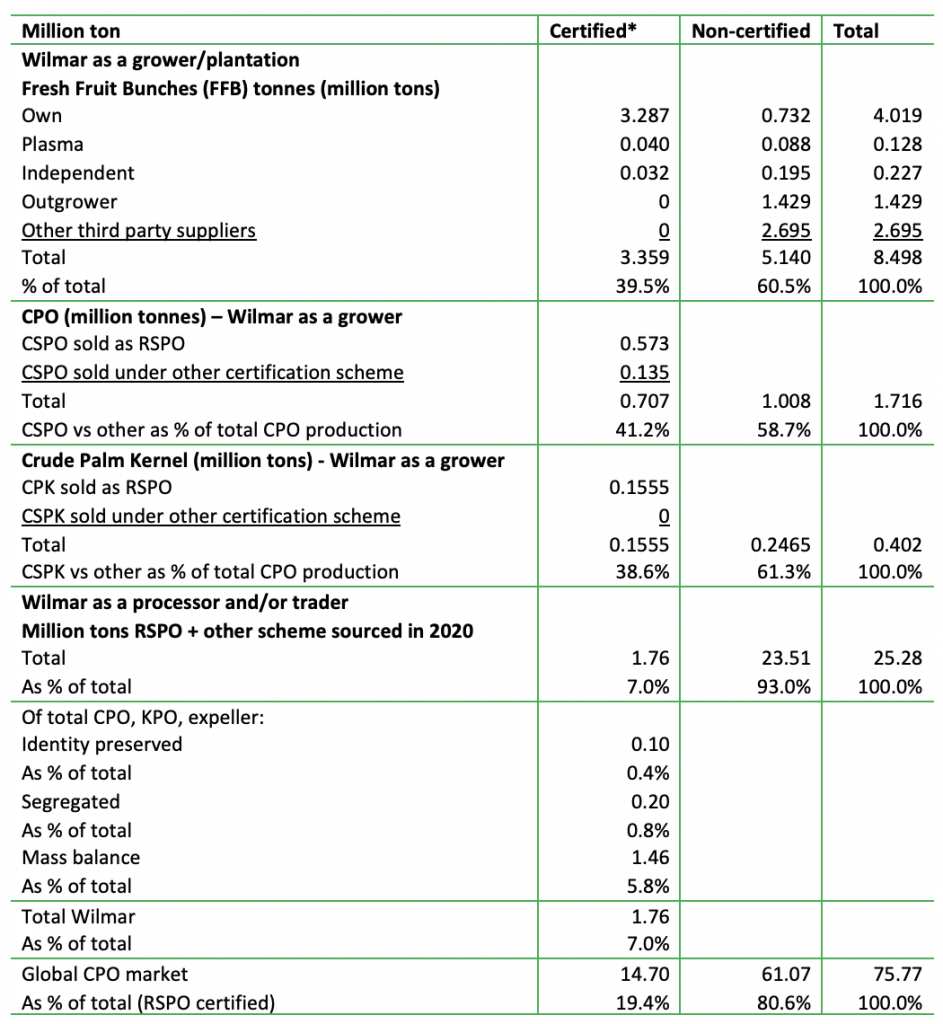

Wilmar provides high traceability, but it has a low level of RSPO-certified palm oil in its system. In 2015, Wilmar published information on all of its 800 palm oil suppliers available through an online dashboard. This spurred an increase in transparency in an industry that for years had operated in secrecy. Wilmar has worked on RSPO certification in own processes, but only sources small volumes of RSPO-certified palm oil in its much larger palm oil supply from third parties. Since 2004, Wilmar has been a member of the RSPO, and the company has been actively involved in various RSPO working groups. Its Malaysian upstream activities (plantations, mills) are fully certified, and the Indonesian and African upstream operations are making progress to the same level. Wilmar plans for its associated/plasma smallholders in Indonesia and Ghana to be RSPO-certified in 2023, and all its mills and plantations in 2025. Wilmar is also working to get the independent smallholders certified, but it has not provided a timeframe. The sale of certified palm oil at higher (premium) prices is an important instrument to increase the income level of smallholders, pay for “sustainable” palm oil, and subsequently reduce deforestation.

Wilmar has 97.7 percent traceability to mill level, but indicates it is facing challenges in promoting certified palm. Only 7 percent of palm oil in Wilmar’s mills and refineries are RSPO-certified or have other certifications (Figure 3). Globally, 19 percent of the palm oil traded is RSPO-certified. As of December 2020, 97.7 percent of CPO and PKO equivalent is traceable to mill level at Wilmar. This translates to about 23.9 million metric tons of palm products traceable to mills across Wilmar’s global operations. Over 90 percent of volumes originate from third-party suppliers in Indonesia and Malaysia. Main challenges cited by the company include difficulties in the certification process, certification of smallholders, high costs in achieving or adhering to certification, reputation of palm oil in the market, supply issues, and traceability issues. Figure 3 elaborates on the RSPO certification and RSPO certified palm oil sold under other certification schemes.

Wilmar claims that the structural problem in accelerating certification is that palm oil is a commodity market and the uptake of certified palm is behind production. The company indicates that the customer decides which type of palm oil is bought, and often customers are focused on price. Globally, the uptake of certified palm oil has therefore been below the level of certified production. As a consequence, a portion of certified palm oil produced has to be sold as conventional palm oil. This generates no premium price and consequently no incentive to accelerate penetration of certified palm oil. The increasing market share of participants from countries still lagging in palm oil policies (China, in the case of Wilmar) worsens the current situation. If Wilmar were to not to sell lower-priced conventional palm oil, it would risk losing clients in China.

Wilmar’s food products division, including its FMCG activity, sources large amounts of palm oil. However, the division lacks transparency about whether it is paying a higher price to smallholders. With 45 percent of 2021 revenues (see Figure 1) and 28.3 million metric tons in sales volume (Figure 9, Appendix), this division includes high activity in Southeast Asia. Within this division, 8.5 million metric tons consist of consumer products, including vegetable oil produced from palm and oilseeds, sugar, flour, rice, noodles, specialty fats, snacks, and bakery and dairy products. Thus, through this division’s consumer products activity, Wilmar is a large branded FMCG company that sources palm oil. Wilmar’s argument that global FMCGs do not buy enough certified palm oil would not apply to this business since Wilmar has full control. Wilmar does not provide data how much palm oil it is sourcing through the food products’ FMCG activity. Also, no data (for instance through CDP) is available on how much Wilmar’s FMCG activity is spending to support smallholders through buying certified palm oil.

CRR estimates that Wilmar’s FMCG activity is sourcing 2.1 million palm oil products, of which a major part is not certified. CRR identified 0.633 million metric tons of imported palm oil from Indonesia (July 2019 to June 2020) through YKA (90 percent owned by Wilmar) into China. YKA’s main activities consist of food product sales. On top of this, YKA imports palm oil from Malaysia, and there have been other non-identified volumes. Finally, Wilmar’s food products division also includes other countries. Wilmar says that this division is “the largest producer of consumer pack edible oils in the world, with leading positions in China, Indonesia, India, Vietnam, Sri Lanka and several African countries.” The other 19.8 million metric tons in the food products division are sold in megapacks, probably to other FMCGs. Wilmar may lack power to “force” these buyers to buy certified palm oil. Assuming a quarter of the volumes of Wilmar’s food products’ consumer activities consist of palm oil, this means 2.1 million metric tons (25 percent of 8.5 million ton) are palm oil.

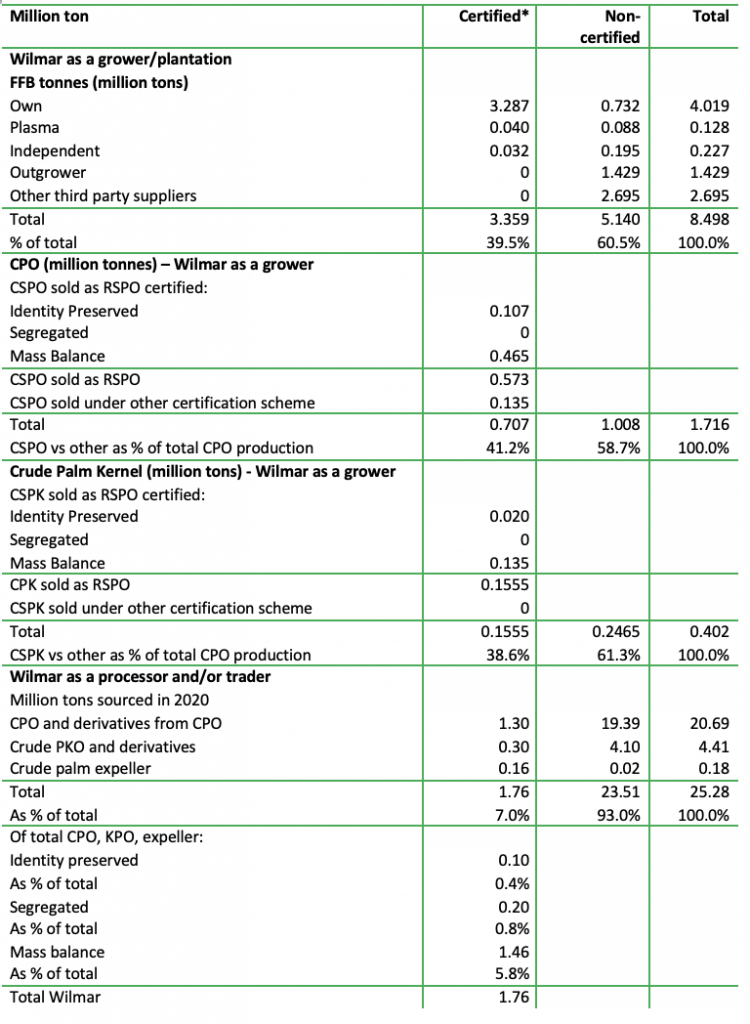

Wilmar has a large gap in the uptake of certified palm oil in its FMCG/branded business, on top of the low uptake in refining. Currently, Wilmar has an uptake of only 1.76 million metric tons of RSPO-certified palm oil and other CSPO (Certified Sustainable Palm Oil) through its trading & processing business (Figure 3). If this whole amount was sold to its food products consumer business, there is still a gap of 0.34 million metric tons that is not covered. Moreover, if all its certified palm was sold internally to its FMCG business, Wilmar would sell zero certified palm oil products to other customers. As many buyers of these products, such as Unilever and PepsiCo, report to have a high uptake of certified palm oil, this appears not to be realistic. Therefore, Wilmar, as a processor and buyer of palm oil, is substantially lagging the global uptake of more expensive certified palm oil. The premium price for certified palm oil is expected to support smallholders. Figure 3 summarizes the main themes of Figure 10 in the Appendix, and shows that in 2020, Wilmar’s 1.76 million metric tons of CSPO uptake, 7 percent of its total, was dramatically behind the global market’s 19 percent.

Figure 3: Wilmar’s grower and processor/trader status in RSPO certification – 2020

Source: RSPO; CSPO = Certified Sustainable Palm Oil: * including volume from an RSPO mill sold under other schemes

Source: RSPO; CSPO = Certified Sustainable Palm Oil: * including volume from an RSPO mill sold under other schemes

Wilmar neglects large downstream activities in its TCFD (Task Force on Climate-Related Financial Disclosures) reporting, but it has promised this will change. In 2018, the Wilmar Group conducted a qualitative scenario analysis to identify the possible impacts that climate change may have on its business. The analysis focused mainly on its upstream operations and supply chain. In a 2 degrees Celsius (2DS) scenario, the analysis revealed a potential reduction of FFB supply due to prolonged droughts and floods. In a 2DS scenario, Wilmar sees opportunities in selling more biofuels. The company promises that in the future it will do a TCFD analysis on its complete downstream activities.

The update of the TCFD analysis might show that by sourcing from plantations that possibly contribute to deforestation and climate change, Wilmar could face financial and reputation risks. The CRR’s report on TCFD implementation mentioned that Wilmar (like Golden Agri-Resources and Indofood) has faced long-standing criticism from international environmental NGOs regarding its contribution to climate change.

Wilmar’s links to deforestation and human rights violations

In many recent CRR studies, Wilmar has been linked to deforestation and social conflicts. This was based on CRR primary research, but also cited in various reports from other civil society organisations. The list below starts with the most recent CRR publications:

- In 2022, CRR listed the top-10 deforesters of 2021, linking Wilmar to the mills of the number 6, PT Permata Sawit Mandiri, with 450 ha of clearing.

- In the 2022 CRR study on African palm oil, Wilmar was linked to numerous social and environmental impacts on its African concessions. These impacts include land-grabbing, loss of social and environmental high conservation values, and violence and intimidation.

- In 2022, Astra International, which is active in palm oil, mining, automotive and heavy equipment, was reported to be linked to deforestation in its mining activities. Since Wilmar lacks a cross-commodity deforestation policy, it still sources Astra’s palm oil.

- In the 2021 CRR report on China’s palm oil supply chain, Wilmar was linked to human right violations in several cases. One of these cases is Wilmar’s palm oil operations in West Sumatra, which has been accused of land grabbing.

- In 2021, Wilmar was visible in the supply chain of PKPS, which planned to develop an agricultural plantation on an 8,000-ha plot of land, which includes 971 ha of peat swamp forest. The scheme is called the Selangor Smart Agro Park project. In the same report, Wilmar was said to be in the palm oil supply chain of Djarum, which cleared 32,000 ha of forest between 2013 and 2017 in timber concessions. This problem was also a result of Wilmar’s lack of a cross-commodity NDPE policy.

- In 2021, CRR cited a Rainforest Action Network report that identified ten companies (one of them was Wilmar) in agribusiness sectors in Indonesia that operate without the Free, Prior and Informed Consent (FPIC) of traditional land users.

- In 2021, CRR’s report on the South Korean palm oil supply chain linked Wilmar to Daseng’s plantation subsidiary PT Sintang Raya. Deasang was involved in clearing peatland, land grabbing, and not allocating plasma plantations for local communities. Labor issues and the risk of child trafficking at the plantations have also been reported.

- In 2020, Wilmar was linked to 700 ha of deforestation of Capitol Group and of companies tied to Indonesia’s Fangiono family, which have been among the largest deforesters in the last few years. Wilmar was also linked to deforestation by TH Plantations. Moreover, deforestation by United Malacca Berhad’s (UMB) industrial tree plantation raised questions about the scope of Wilmar’s cross-commodity NDPE policy status.

- In a 2020 report on the major deforestation footprint of Yum China, Wilmar was listed as a supplier to Yum China predecessor Yum Brands!

- The 2019 CRR report about oil palm growers and their exposure to social compensation risk concluded that Wilmar belonged to the top three companies that have faced the most formal RSPO complaints linked to social issues in Indonesia in the last ten years. Wilmar International received 15 percent (of the 74 complaints filed), Golden Agri Resources (GAR) 12 percent, and Bumitama Agri 9 percent. Considering only the 22 active cases at the time of the writing of the report, Golden Agri-Resources (five cases), PT Pertamina – Persero (four cases), Wilmar International (three cases), and Bumitama (two cases) are on top of the list.

- A 2019 CRR report on future smallholder deforestation and possible palm oil risk pointed out that despite sourcing substantial FFB volumes from independent smallholders, the financial accounts of Wilmar offered no indication of long-term financial support, loans, or guarantees to independent smallholders. Wilmar has explored financing programs with international banks, but these programs did not succeed due to a mismatch in time periods and ticket sizes of loans. Currently, Wilmar gives no direct financial incentive to replant. It mainly requires the smallholders and external suppliers to be NDPE compliant. No long-term loans to independent smallholders could be identified on its balance sheet.

- Wilmar has many supply chain links with shadow companies, as revealed in 2018’s CRR report on shadow companies that present palm oil risks and undermine NDPE efforts. Furthermore, in 2018, CRR noted that Salim Group, related to IndoAgri with various ESG violations, had a joint venture with Wilmar.

- In 2016, CRR concluded that Wilmar’s update on its NDPE policy showed mixed progress on implementation. Some NGOs highlighted the importance of Wilmar’s leadership on transparency, and others criticized its ongoing connection to deforestation, peatland burning, and social conflict.

CRR also reported several positive issues on Wilmar. In June 2018, Wilmar suspended sourcing from 10 Gama companies, after which Gama took measures to remain in the NDPE market. And Wilmar belongs to the minority (nine out of 28) palm oil refiners, which have a no-deforestation policy (CRR report 2021). Wilmar has an active grievance process and reacts on cases, but its name keeps coming up in many reports on violations, which could be related to the low percentages of certified and segregated palm oil streaming through Wilmar’s supply chains, respectively 7 percent and zero percent.

Several ESG conflicts remain under the radar or are upcoming

There are issues on the ground connected to Wilmar that are not captured by mainstream and national media and only appear in local media. One example occurred In 2021, when PT Bumi Pratama Khatulistiwa (PT BPK), a subsidiary of Wilmar, was accused of harvesting their fresh fruit bunch despite expired permits. According to the local community, PT BPK should have ended its operation by 2021 and given the land back to the community, but Wilmar allegedly insisted that the permit allowed for operations to continue until 2026. The company said it held the document from the central government, mentioning that the permit lasts until 2026 and would expire even later. Wilmar added that the land should be returned to the government/country instead of to the local people.

In 2022, Indonesian NGO Ecoton accused PT Bumi Pratama Khatulistiwa and PT Agronusa Investama (both are Wilmar’s subsidiaries) of polluting the rivers near the plantations. In response, Ecoton went on strike in front of PT Wilmar Nabati’s office, protesting the activities of the two companies that allegedly polluted Sambas River and Kapuas River. Samples of wastewater from PT Agronusa Investama had high chlorine content, while samples from PT BPK shows Paraquat, a highly toxic herbicide.

Biofuel companies have benefited from subsidies, with domestic cooking oil market and smallholders being left out. The shortage of cooking oil this year in Indonesia — in which four companies, including two subsidiaries of Wilmar, have been charged by prosecutors — has received broader media coverage. With global CPO prices rising in line with fossil fuel prices increasing and a cap on cooking oil prices imposed in Indonesia, the four leading cooking oil companies appear to have redirected palm oil supplies for biofuels to outside the country. In 2015, Wilmar, with other companies, demanded help from the government – in terms of subsidies amid low palm oil prices. This request occurs in an environment in which rejuvenation subsidies, financed from export of CPO, seem to have been captured by companies (including Wilmar) producing biofuel instead. Instead, these subsidies could have gone to smallholders. The lack of funds for renewal of smallholder plantations combined with smallholders’ poverty increases the risk of deforestation since “income gap” financing is not available.

Friction between Wilmar and NGOs on strengthening cooperation

Wilmar faces more conflicts with some NGOs about the pace of cooperation on achieving zero deforestation. In 2018, Greenpeace said that Wilmar was still sourcing from 18 out of 25 palm oil groups that cleared 130,000 ha of rainforest since 2015. Greenpeace emphasized that only a fraction of the palm oil Wilmar trades comes from its own plantations; more than 80 percent comes from other palm oil producers. Greenpeace listed three specific gaps that need to be filled: mandatory concession maps from suppliers and specific, timebound, and measurable actions to achieve independently verified “100 percent deforestation-free palm oil.” On August 22, 2019 Greenpeace stepped back from an engagement with Wilmar, Unilever, and Mondelez to set up a deforestation monitoring platform amid the companies’ repeated failure to take necessary action to follow through on their commitments to achieve no deforestation.

In 2020, Wilmar quit, after six years, the High Carbon Stock Approach (HCSA). The HCSA is a multi-stakeholder platform made up of NGOs and industry partners that determines which forests should be protected based on conservation value and which lands are suitable for agricultural development. The HCSA distinguishes the vegetation in an area of land into six different classes using analyses of satellite data and ground survey measurements. These six classes are High Density Forest, Medium Density Forest, Low Density Forest, Young Regenerating Forest, Scrub, and Cleared/Open Land. The first four classes are considered potential High Carbon Stock forests. Greenpeace said Wilmar failed to provide evidence that it was actively implementing HCSA. Wilmar cited governance issues and mismanaged budgets for not providing the evidence. Wilmar argues that HCSA did not properly address its internal objections. NGOs accused Wilmar of being directly linked to fires, deforestation, and land conflicts and not fulfilling its information requirements. Wilmar was relatively important in funding the HCSA, which in 2020 saw income sources of USD 1.2 million and expenditures of USD 1.1 million.

Sustainability standards, like the RSPO and company policies, do not reflect results on the ground since Wilmar lacks oversight on plantation-level operations from linked companies, according to some NGOs. In CRR interviews with NGOs (they like to remain anonymous), the narrative is that Wilmar has no oversight on all plantations it sources from. Social violations are insufficiently covered by Wilmar as it lacks a system of local intelligence. Wilmar should increase its due diligence investigations at its suppliers, but according to NGOs, Wilmar says that this would increase costs sharply and that the company prefers to take small steps. Overall, Wilmar benefits from a system in which governments prefer to give land concessions to large-scale companies (like Wilmar) as these promise a secure stream of tax generation. Interviews indicate that these companies tend to have weak grievance mechanisms and lack presence on the ground, which reduces the costs and therefore maximizes short-term profits and corporate tax payments.

Wilmar’s large benefits on palm oil versus a low level of potential costs

Wilmar is globally the number one company in generating gross profits on embedded palm oil in its value chain (see Figure 2) but lacks transparency on support to smallholders. The number one position is based mostly on its refining business and to a lesser extent on its smaller own plantation activity. Wilmar does not disclose how much it spends on “costs of response” to potential risks in its palm oil activities, arguing that the response is an element of running its operations and managing its supply chain, and is therefore considered part of its overall operational costs. “These actions are integrated in (…) operations and costs of operations and is not quantified separately,” Wilmar says. Meanwhile, other large palm oil supply chain participants are specifying their costs, as noted in the CRR report on NDPE execution/verification costs. Wilmar’s financial accounts also offer no indication of long-term financial support, loans, or guarantees to independent smallholders. The section above on certification demonstrates that Wilmar had a low uptake of premium-priced certified palm oil in its refining and its FMCG businesses. The conclusion is that the low uptake and the lack of disclosure do not offer comfort to financial markets and NGOs about Wilmar’s financial support to smallholders.

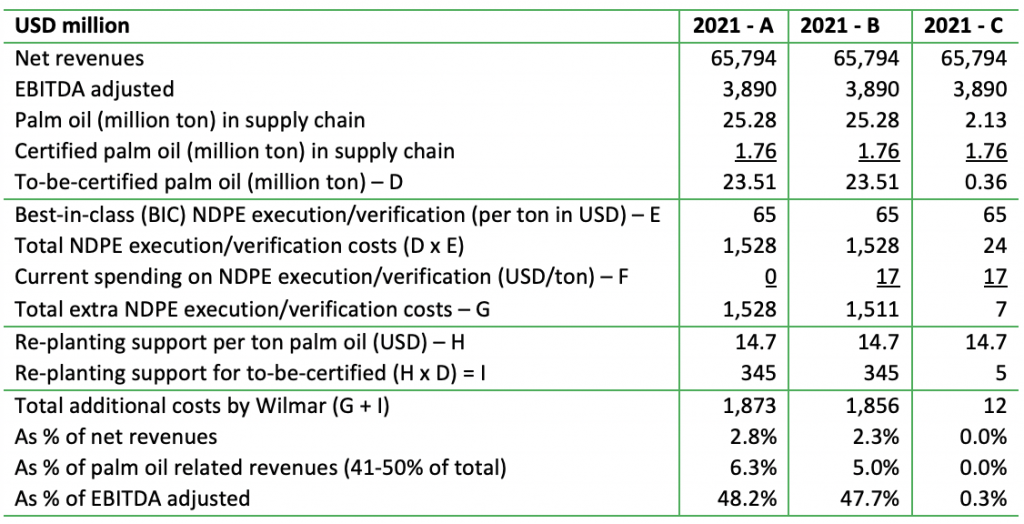

Wilmar’s expenses lag versus a best-in-class execution of NDPE policies. CRR calculated a best-in-class cost per ton of USD 65 for NDPE execution when accounting and monitoring/verification. In the coming years, financiers may ask for more transparency about this cost item as the best-in-class approach may be used to drive the whole palm oil processing and trading sector to a higher ESG level. Figure 4 shows three scenarios for Wilmar. If Wilmar’s current “cost of response” is zero, a USD 65 per ton best-in-class NDPE policy execution, including verification, would need to be applied to the millions of metric tons that are not certified (23.51 million metric tons). In scenario A, the assumption is that this volume would need USD 1,528 million, or USD 1,5 billion, in extra expenses.

On top of this, CRR’s analysis of annual replanting support for smallholders would costs USD 1.1 billion for the whole sector and supply chain. On a per ton basis globally for produced palm oil, this equates to USD 14.7. If this is applied to the non-certified part that Wilmar is sourcing, the company needs to contribute USD 345 million.

In total, Wilmar would need to spend USD 1,873 million (USD 1.9 billion) extra per year to achieve a complete clean, deforestation-free supply chain, including extensive verification. This spending would have been 2.8 percent of total net revenues in 2021 and an estimated 6.3 percent of palm oil-related revenues. A 6.3 percent sales price increase for its palm oil related products could pay for this best-in-class approach. In case of no price increases, EBITDA would decline by 48.2 percent. Passing on the expenses to customers is the most logical path as customers may also desire purchasing from a clean supply chain. The necessary price increases by FMCGs and retailers to pay for the best-in-class NDPE execution are much lower than at Wilmar. CRR calculated these increases to be less than 2 percent.

The scenario B assumes that Wilmar already has a “cost of response” for sustainable palm oil. The company has a 70-FTE department dedicated to sustainability in its supply chains. This department’s activities might cost USD 7 million (70 times 100,000 per FTE). On top of this, training programs for smallholders might costs the company USD 10 million. The outcomes do not differ sharply versus scenario A. Finally, scenario C calculates only the extra costs for all palm oil volume sourced by Wilmar’s own FMCG/brand business, which would have a small impact on Wilmar’s financials. The impact on “sufficient” support for smallholders would also be minimal.

Figure 4: Wilmar’s extra NDPE execution/verification expenses in best-in-class scenario

Source: Profundo

Does Wilmar prioritize profit above ESG? Despite Wilmar’s dominant position in the palm oil chain, the company says that FMCGs do not reward Wilmar for higher spending on NDPE/RSPO supply chain execution/verification. This situation might have led the company to prioritize profitability above sustainability. Interviews with NGOs confirm that Wilmar is much more focused on profit generation and cost savings than several other large companies in the palm oil supply chain. The fact that Wilmar has a stronger position in some ESG ratings (see below) compared to its peers makes sense as other companies might have fewer resources to “tick the boxes” for ESG ratings.

Wilmar’s ESG rating outcomes are mixed

Wilmar has positive ratings, but rating agencies’ outcomes vary. Wilmar said in 2022 that it was upgraded from a BBB to an A rating for its environmental, social and governance (ESG) performance in the 2021 assessment by Morgan Stanley Capital International (MSCI). The high performance was a result of its long-term resilience to ESG risks. In the same publication, Wilmar flagged its other ESG credentials:

- Its inclusion (2021) in the Dow Jones Sustainability Indices (DJSI) World Index for the Food, Beverage and Tobacco sectors was the result of being among the top global companies with the best ESG performance. Wilmar’s 2021 inclusion in this index meant that the company joined a list of 322 global companies on the World Index with the best ESG performance: Wilmar scored 70 points in the S&P Global Corporate Sustainability Assessment (CSA); the industry average was 25 points and the best company in the industry had 88 points. The CSA uses a comprehensive methodology on ESG criteria, with a strong emphasis on long-term shareholder value.

- Wilmar was ranked number one in the 2021 assessment by the Sustainable Palm Oil Transparency Toolkit (SPOTT). While Wilmar scored 3 percent, its 27 percent-owned SIFCA group scored only 16.5 percent. SIFCA’s operations violate Wilmar’s policy to conduct FPIC (Free, prior and informed consent), which is aimed to establish bottom-up participation and consultation of an indigenous population before cultivation. SIFCA did not properly address and mitigate its ongoing conflicts with local communities. Nevertheless, in 2021, the SIFCA group and Satelligence signed a partnership agreementfor satellite monitoring of deforestation on plantations of the group.

- Wilmar said it was included in the FTSE4Good Developed Index and the FTSE4Good ASEAN 5 Index in 2021. The FTSE4Good Index Series is among the world’s first global ESG index families.

Another rating system is developed by World Benchmark Alliance’s Food and Agriculture Benchmark, focusing on system changes based on progress versus SDGs (Sustainable Development Goals). In this group, Wilmar ranks 28 out of 350 with a score of 42.2 out of 100. The company scores below Unilever (position 1, score 71.7). Versus peers, it is in line with Olam but above Sime Darby Plantation (85th position with score of 31.1) and Golden Agri-Resources (111/26.4 score).

Some rating agencies and indices have flagged Wilmar’s ESG risk. Wilmar’s 2021 ESG rating by Sustainalytics of 33.6 out of 100 suggests a “high risk” linked to its non-manageable supply chain. Sustainalytics’ ESG Risk Ratings measure a company’s exposure to industry-specific material ESG risks and how well a company is managing those risks. While Wilmar’s exposure to various ESG risks is labeled as “High” (out of three categories including “Low” and “Medium”), its management of ESG issues is seen as “Strong” (out of three categories including “Weak” and “Average”). The total rating (33.6) combines an assessment of a company’s total exposure to industry-specific material ESG issues with an assessment on how well the company is dealing with manageable risks. For the part that is manageable (as defined by Sustainalytics), Wilmar seems to address the issues well by management structures and policies. Wilmar’s crucial problem appears to be its activity in segments where many ESG issues are difficult to manage. As a consequence, in Sustainalytics’ global universe, Wilmar is ranked at a relatively low level, number 10,713 out of 14,753. Nevertheless, in 2021, United Overseas Bank (UOB) extended a USD 200 million sustainability-linked loan to Wilmar. The interest rate is dependent on achievement of ESG targets/KPIs, as assessed by Sustainalytics.

A downgrade came from the Carbon Disclosure Project (CDP). CDP gives Wilmar a rating of B (A is the highest) in the Forest 2021 appraisal, below the A- in 2020. In Climate Change 2021 and Water Security 2021, Wilmar achieves B and B-, respectively.

With so many ESG score ratings available, CSRHub creates a consensus of rating agencies scores. Based on 36 sources for Wilmar, it has an ESG Ranking of 65 percent compared with 28,662 companies. This means 35 percent of the companies have better ratings.

Rating agencies have different weightings for the three elements in ESG, and they present scores differently. The correlation of various agencies’ rating outcomes is low. Overall, there are large differences in ESG ratings and how the separate Environmental, Social, and Governance factors are weighted. Environment is seen as best/easiest to measure, largely because the most dominant item now is decarbonization. Social factors are much more difficult to measure, as is Governance, which contains the elements like “no bribery” and “checks-and-balances in management.”

Differences in rating methodologies also lead to differences in presentation of the scores. MSCI ESG Research Rating assigns firms ESG scores ranging from best (AAA) to worst (CCC). S&P Global ESG Rank yields a total sustainability percentile rating derived from the total sustainability score and the S&P Global ESG Rank. Sustainalytics Industry Rank provides a percentile rating to companies based on their ESG total score relative to their industry peers. The CDP Score reflects a company’s degree of commitment to climate change mitigation, adaptation, and transparency. At CDP, the firms rated are only those that respond on time to a questionnaire sent in response to an investor request. The Institutional Shareholder Services (ISS) Governance Score assesses a company’s governance practices, while the Bloomberg ESG Disclosure Score is a proprietary rating derived from the extent of a company’s ESG disclosure.

A paper from MIT concluded that ESG ratings from different providers vary substantially. In a dataset, the correlations between the ratings range from 0.38 to 0.71 (which is low), based on ESG ratings from six different raters: KLD, Sustainalytics, Moody’s ESG (previously Vigeo-Eiris), S&P Global (previously RobecoSAM), Refinitiv (previously Asset4), and MSCI. The main conclusions were as follows: 1) it is difficult to evaluate the ESG performance of a company (or a fund), 2) the differences in ratings do impact the incentive for ESG improvement, and 3) the share prices do not reflect ESG performance.

The EU is striving for standardization to support green financing. Since the correlations between the various ESG ratings methodologies are low, the consequential risk is that ESG is seen as a marketing instrument by companies and asset managers. This creates doubts about the usefulness for insights about financial value creation. Therefore, the EU has begun a public consultation aimed at strengthening the reliability and comparability of ESG ratings, which could help grow the sustainable finance market.

EU and US regulation could affect Wilmar’s profits and valuation multiples

EU regulation could impact Wilmar’s profits by much more than the current four percent revenue exposure. Wilmar’s revenues have limited exposure to Europe. In 2020, it was just 3 percent and in 2021 it was 4 percent (2011: 8 percent). In February 2022, the EU adopted a proposal for a Directive on corporate sustainability due diligence. The aim of this Directive is “to foster sustainable and responsible corporate behaviour and to anchor human rights and environmental considerations in companies’ operations and corporate governance. The new rules will ensure that businesses address adverse impacts of their actions, including in their value chains inside and outside Europe.” If Wilmar could no longer export to Europe and would lose four percent of its revenues, this would have a large negative impact on its profits because of operational leverage from fixed costs.

On top of EU regulation, U.S. lawmakers are considering legislation that would halt imports of commodities from deforested land. Wilmar does not report on revenues from the U.S. market separately.

The indirect impact might be larger. Wilmar’s products might be processed by food companies outside of Europe into food products or ingredients, and these products with the embedded palm oil and sugar would then be imported into the EU market. These products would be subject under the EU regulation and could have problems entering the EU market due to the lack of supply chain transparency.

Regulation is expected to impact the composition of investment portfolios, and can lead to Wilmar being placed on “exclusion” lists by EU investors. On top of the impact on profits, EU regulation might also have an impact on the valuation multiples of its shares. The EU Sustainable Finance Disclosure Regulation (SFDR) is a set of EU rules, including taxonomy, which aim to make the sustainable profile of investment funds more comparable and better understood by end investors. More and more funds would like to be presented as “Article 8 or 9″ funds instead of less sustainable “Article 6” funds. Companies with an elevated ESG risk profile would increasingly be excluded from portfolios. Similar initiatives are on the way in the United States and other parts of the world. As a result, Wilmar is on Robeco’s 2021 “exclusion” list for palm oil companies in its sustainability and impact funds. Robeco is engaging Wilmar as the company shows a lack of progress on RSPO certification, as the company is below the 80 percent threshold of its own hectares certified against RSPO standards.

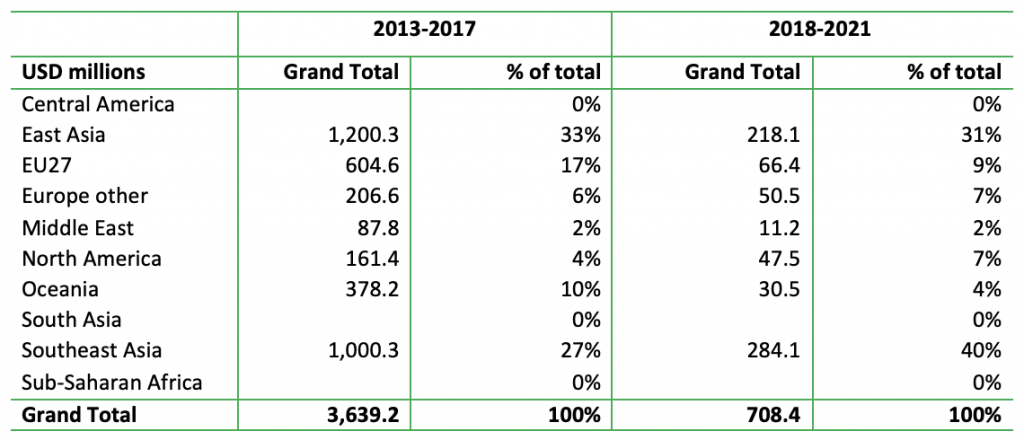

As European financiers have reduced their exposure, Asian investors have become the main financiers of Wilmar. Forests & Finance data show that of the identified financing (forest risk adjusted, see table), the percentage of financing by EU-27 and other European countries has declined from 22 percent of the total in 2013-2017 to 17 percent in 2018-2021. This decline was relatively sharp in the EU-27, from 17 percent to 9 percent. This gap has been filled by Southeast Asian financial institutions, which increased their share of financing from 27 percent to 40 percent. However, a more important conclusion is that the identified financing has declined dramatically from USD 3.64 billion to USD 708 million, excluding shareholdings. This could mean that Wilmar is increasingly financed by bilateral, unidentified loans.

Figure 5: Identified financing, excluding shareholdings

Source: Forests & Finance, includes Bond issuance, Corporate loan, Revolving credit facility, Share issuance; the numbers are forest-risk adjusted (= weighted for the size of activity versus the total company)

Wilmar has a relatively low valuation with a P/E ratio of just above 10X. Its valuation is below that of the peer group.

Figure 6: Wilmar’s valuation versus its peer group

Source: Bloomberg; peer group = Jiangsu Hengshun Vinegar, Sichuan Teway Food Group, Yantai Shuangta Food, Nestle Berhad, Monde Nissin, Three Squirrels, Zhongyin Babi Food, Jiahe Foods Industry, Angel Yeast, Indofood Sukses.

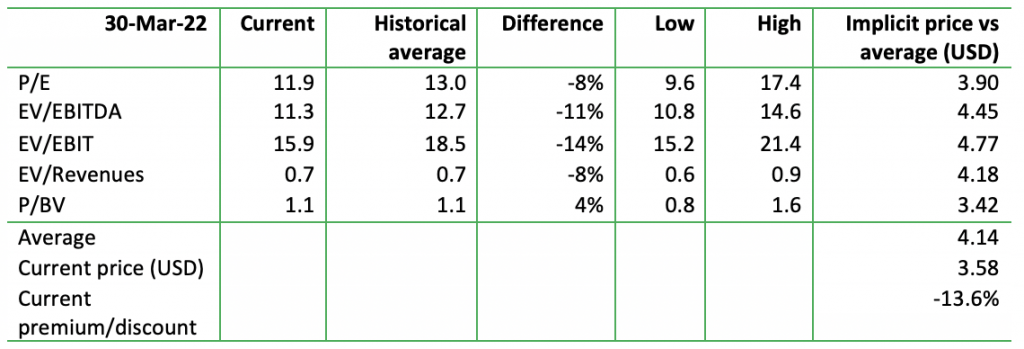

Moreover, Wilmar’s current valuation is below that of its own history. The listing of its large Chinese subsidiary is meant to prop up the value. Its share price performance in the last 10 years has been weak, despite the listing of Chinese and Indian activities.

Figure 7: Wilmar’s valuation multiples (BF = Blended Forward) versus five-year own average

Source: Bloomberg, Profundo

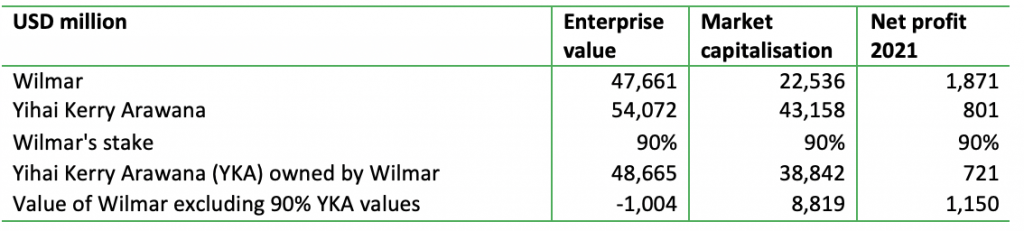

The carve-out of the Chinese YKA led to a high valuation multiple of the listed 10 percent stake, in line with many Chinese stocks in the same sector. As a consequence, the activities excluding the Chinese activities seem to have a low valuation. The enterprise value of Wilmar is USD 1.004 billion lower than the enterprise value of its 90 percent stake in YKA, while Wilmar, excluding YKA, has USD 1.15 billion net profit (EBITDA would be better to compare, but YKA number not available). This low valuation suggests that analysts may become positive on Wilmar.

Figure 8: Wilmar’s valuation versus the value of its listed Chinese subsidiary YKA

Source: Bloomberg, Profundo

After the 2021 result announcement, analysts have become more enthusiastic about Wilmar due to higher CPO prices and processing margins. They recommended accumulating Wilmar shares. Analysts at CGS-CIMB Research, DBS Group Research, Citi Research, and RHB Group Research never referred to any ESG violations. CRR spoke to long-term investors and financiers who are satisfied with Wilmar’s plans on improving sustainability in the palm oil supply chain and believe the company’s culture in this aspect is positive.

Wilmar’s valuation could have a lot to gain from a better reputation. More transparency with regard to its current expenditures to reduce forest and sustainability risks and a much larger uptake of premium-priced certified palm oil in its downstream and FMCG business could have a positive impact on Wilmar’s reputation and its share price. Otherwise, the company may face increasing financial risks from a worldwide adoption of more stringent regulation with regard to sustainable finance as well as supply chain regulation.

Appendix

Figure 9: Wilmar’s volumes sales in million tons

Source: Wilmar Annual Report 2021

Figure 10: Wilmar’s grower and processor/trader status in RSPO certification – 2020

Source: RSPO; CSPO = Certified Sustainable Palm Oi; *) including volume from an RSPO mill sold under another scheme