This report discusses the EU’s regulation on deforestation-free products and how its requirements will affect the palm oil industry, one of the key commodities driving deforestation. The upcoming law, expected to be implemented in 2023, will have implications for palm oil supply chain actors and their financers.

Watch our webinar covering the findings of this report

Download the PDF here: EU Deforestation Regulation Implications for the Palm Oil Industry and Its Financers

Key Findings:

- The EU is a significant importer of palm oil. In 2021, the EU imported 8 million metric tons (EUR 6.3 billion) of palm oil and palm oil products. The majority is currently used for biodiesel and energy, but the EU’s dependence will likely decline due to the Renewable Energy Directive II that requires a gradual phase out of palm oil-based fuels by 2030.

- The Regulation will largely affect imports originating from Indonesia and Malaysia, the largest suppliers to the EU. It would require a mandatory due diligence system for operators and traders. Next to Indonesia and Malaysia, other palm oil-producing countries impacted include Guatemala, Papua New Guinea, Honduras, Colombia, Côte d’Ivoire, Cameroon, and Thailand.

- Besides the EU, the US and UK are also developing laws to regulate commodity-linked deforestation, imposing increased restrictions on palm oil imports. The EU law is the most comprehensive, since it also includes legal deforestation.

- Key implications for the palm oil industry are linked to traceability, smallholder exclusion, leakage, and the cut-off date. The traceability requirement may lead to exclusion of smallholders and costly segregated supply chains, but it could also improve smallholders’ positions in the global marketplace. The law may increase leakage of unsustainable palm oil in Indonesia’s domestic biofuel market and in countries with less strict import requirements. There is also risk of leakage from not including all palm-oil related products, such as PFAD. The 2020 cut-off date could undermine existing industry NDPE commitments that use 2015 as the cut-off.

- The Regulation may impact palm oil supply to the EU and bring about legal and reputational risks for operators and traders that are in breach of the new rules. In contrast to voluntary industry commitments, the law provides a stronger legal basis for enforcing zero- deforestation commitments. In anticipation of the upcoming law, EU member states have started cleaning their countries’ supply chains.

- Compliance costs are relatively low and protect reputation value. Even in a scenario of segregated supply and inclusion of smallholders, EU operators’ compliance costs would be at most 3.5 percent of revenues on embedded palm oil. Proper compliance could protect USD 14.3 billion in reputation value.

EU is a significant importer of palm oil, mainly from Indonesia and Malaysia

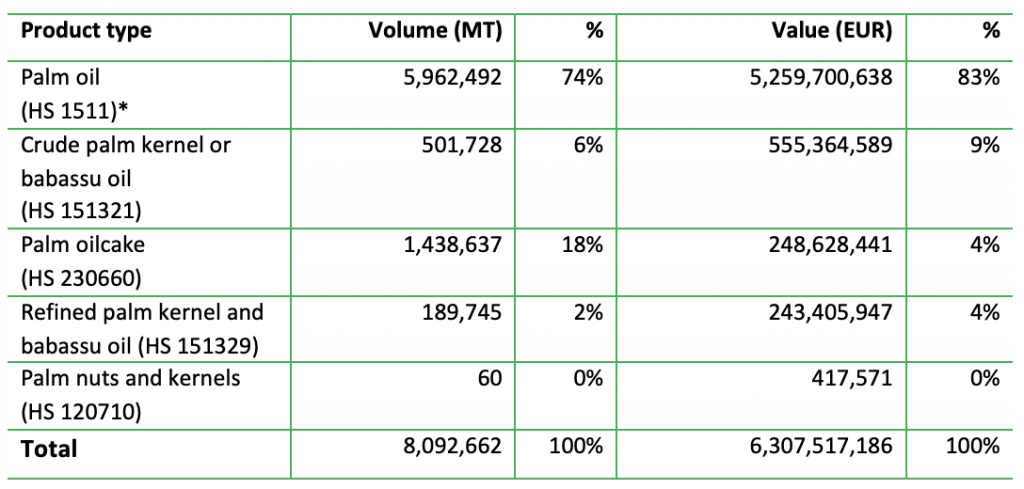

The European Union (EU) imported 8 million metric tons (MT) of palm oil and palm oil products from non-EU countries in 2021. Within the category of palm oil-related products, palm oil represents the largest share of both imported volumes and values in the EU27, accounting for 74 percent (5.9 million MT) of the total imported volumes and 83 percent (EUR 5 billion) of the total imported value (Figure 1). Palm oilcake, a residual product resulting from the extraction of palm nuts or kernels and the second largest imported palm oil product by volume, represents 18 percent (1.4 million MT) of imported volumes, but only 4 percent (EUR 248 million) of the total imported value.

Figure 1: Total EU imports of palm oil related products in 2021 by volume and value

Source: EU27 trade statistics, 2021 (excluding the UK). *Harmonized System (HS) codes and linked palm oil products are derived from Annexes to the EU proposal for a regulation on deforestation-free products. Babassu oil is extracted from the nuts of wild babassu palm trees, that grow in the Amazon region of South America.

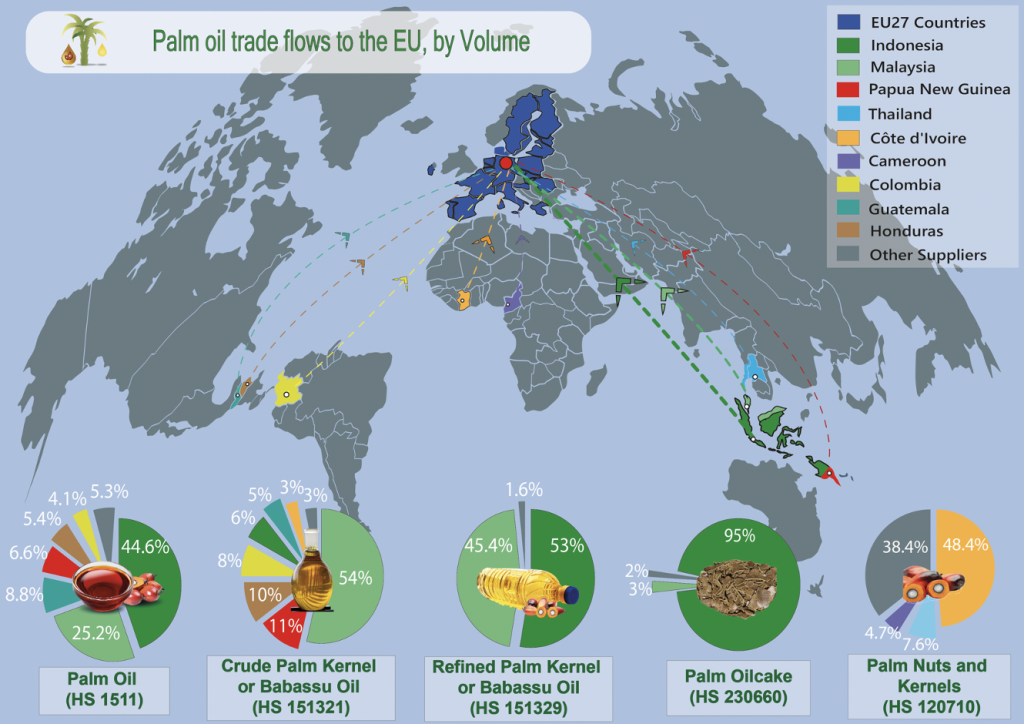

Indonesia and Malaysia are the largest suppliers of palm oil to the EU. The EU27 received respectively 44.6 and 25.2 percent of its palm oil import volumes in 2021 from these two producer countries, followed by Guatemala (8.8 percent), Papua New Guinea (6.6 percent), Honduras (5.4 percent), and Colombia (4.1 percent) (see Figure 2 below). Also, the total EU imported volumes of palm oilcake and refined palm kernel or babassu oil originate mainly in Indonesia and Malaysia, with 95 percent of the oilcake imported from Indonesia and 3 percent from Malaysia. For refined palm kernel or babassu oil, 53 percent comes from Indonesia and 45 percent from Malaysia. Crude palm kernel or babassu oil largely originates from Malaysia (54 percent), Papua New Guinea (11 percent), Honduras (10 percent), and Colombia (8 percent). Finally, in 2021, the EU imported palm nuts and kernels mostly from Côte d’Ivoire (48 percent), Thailand (8 percent), and Cameroon (5 percent), but these numbers are negligible in terms of volume and value, as seen in Figure 1.

Figure 2: Top 10 non-EU suppliers of palm oil products to the EU, by volume

Source: AidEnvironment, based on EU27 trade statistics 2021; FAO’s Global Forest Recourses Assessment 2020; and FAOSTAT 2020. Notes: FAO’s report on Global Forest Resources was used to only include non-EU ‘forest risk’ countries that still have intact forests and showed net forest loss between 2010-2020. FAOSTAT 2020 data was used to verify whether the palm oil (product) was also produced in the country of origin. While Malaysia self-reported no net forest loss in the 2010-2020 period, the country was still included considering its relevance in the palm oil industry, and its remaining forest cover of 19 million hectares in 2020.

Majority of EU imported palm oil is used for biodiesel and energy

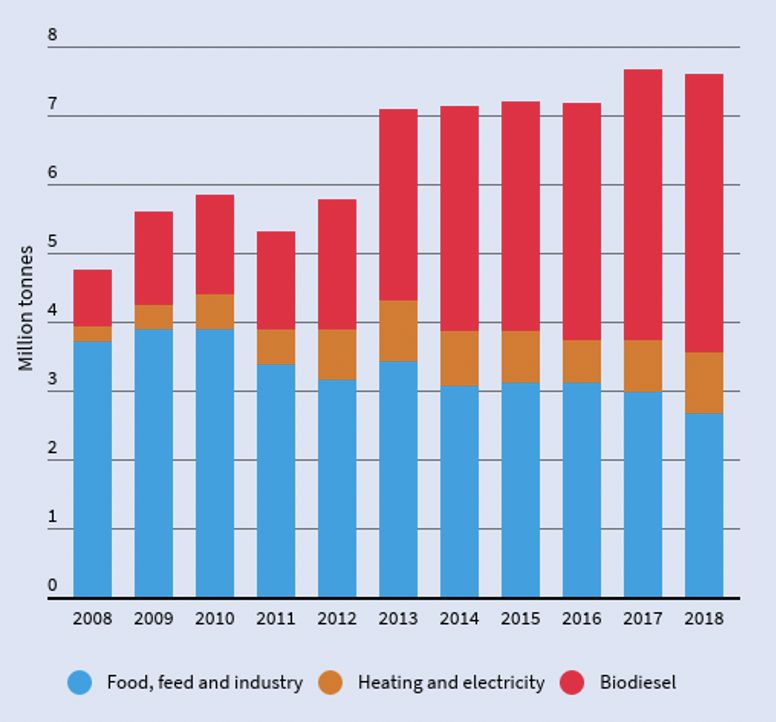

While the food and feed sectors and industry were initially the largest users of palm oil in the EU, the demand for palm oil as a feedstock for biodiesel increased between 2008-2018. In 2018, the EU used more than 4 million MT of crude palm oil (CPO) for biofuel production in European biorefineries (Figure 3 below). In that year, the EU imported an additional 1.2 million MT of palm oil biodiesel. In 2018, an estimated 65 percent of all imported palm oil was used for energy, of which 53 percent for biodiesel production for cars and trucks and 12 percent to generate electricity and heating. About one-third of the palm oil was used to produce food, animal feed, and other industrial products such as detergents and soaps. The continuous growth in the use of palm for biodiesel production was linked to a weak EU biofuels policy, which has allowed, since 2009, using palm oil, a key driver of deforestation, as a feedstock for the production of biodiesel and energy.

Figure 3: EU palm consumption by end use (2008-2018)

Source: Transport & Environment, 2019, derived from OILWORLD.

Since 2021, EU use of palm oil for biofuel production has been on the decline and is expected to drop further. In 2021, biofuels use was estimated at 2.63 million MT, in 2022 at 2.31 million MT, and in 2023 at 2.17 million MT. The decrease is attributed to an anticipated fall in demand for biodiesel linked to the EU’s renewable energy directive (RED II), which requires a gradual phase out of palm oil-based fuels by 2030. The European Commission expects that, as a result of RED II, the overall demand for palm oil will decline to 4 million MT by 2031, down from 6.5 million MT in 2021.

EU, US, and UK plan to strengthen anti-deforestation regulation

EU most extensive in its palm oil import restrictions

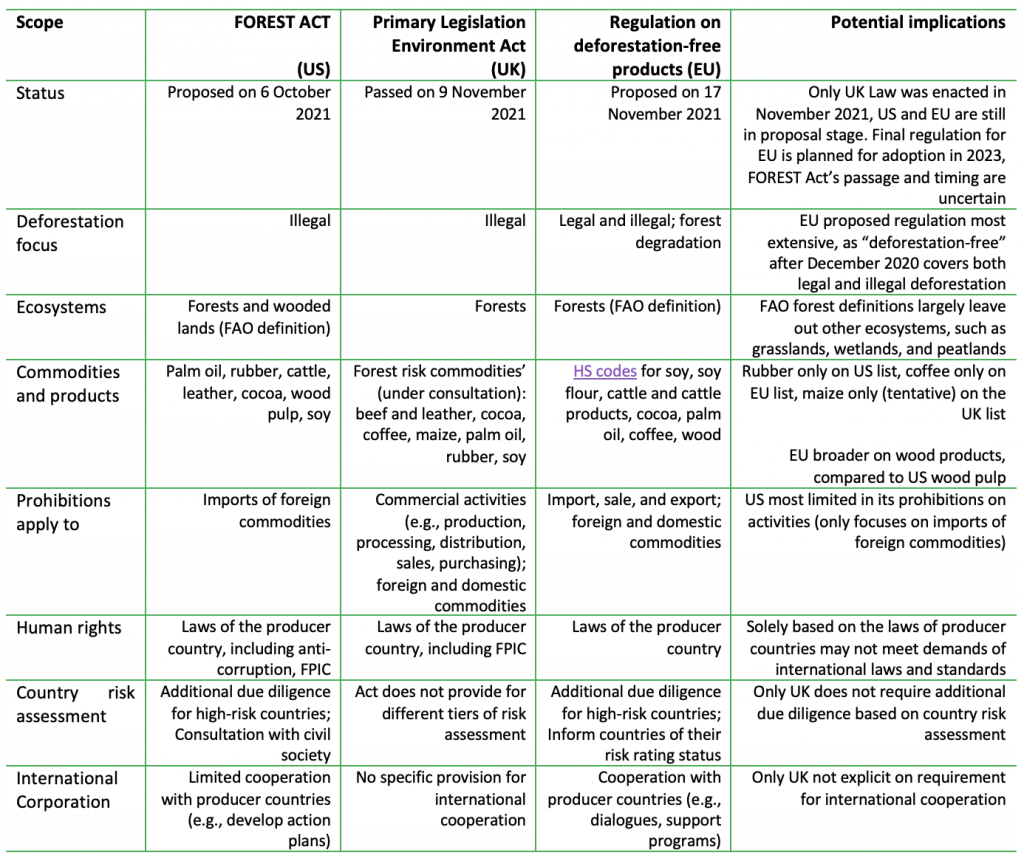

Besides the EU, laws have been proposed or passed in the United States (US) and the United Kingdom (UK) in the past year that aim to regulate (illegal) deforestation linked to global commodity production. The laws, along with the EU Regulation, would have an impact on the imports of palm oil in the Global North. In October 2021, the United States proposed the Fostering Overseas Rule of Law and Environmentally Sound Trade (“FOREST”) Act of 2021 in an effort to “deter commodity-driven illegal deforestation around the world.” In the UK, the Primary Legislation Environment Act was passed on November 9, 2021, also with the goal of curbing illegal deforestation. And then on November 2021, the European Commission released a proposal for a regulation on deforestation-free products (“Deforestation Regulation”). Figure 4 below summarizes key similarities and differences between these anti-deforestation regulations, including their potential implications.

Figure 4: Key similarities and differences between (upcoming) US, UK, and EU anti-deforestation regulation

Source: AidEnvironment, based on Brazil Climate Action Hub, Presentation at COP26, 10/11/2021; Steptoe Global Trade Policy Blog, January 2022. Free, prior, and informed consent, or FPIC, refers to engagement of indigenous and other local communities, specially through being consulted prior to any land conversion.

The proposed EU Deforestation Regulation aims to curb both legal and illegal deforestation and forest degradation that is the result of EU consumption and production. As noted above, of the three pieces of legislation, it is most comprehensive in its definition of deforestation-free. Compared to the UK and US regulations, the EU proposed regulation on deforestation-free products is the most far-reaching since it also includes the prohibition of legal deforestation that would have been allowed under local laws of the country of production. The Regulation defines “deforestation-free” as relevant commodities and products that were produced on land that has not been subject to deforestation since December 31, 2020, and wood that has been harvested from forests without inducing “forest degradation” after December 31, 2020. The deforestation law includes six commodities that reportedly represent “the largest share of EU-driven deforestation: palm oil (33.95 percent), soy (32.83 percent), wood (8.62 percent), cocoa (7.54 percent), coffee (7.01 percent), and beef (5.01 percent).”

A mandatory due diligence system for operators and traders, combined with a system to benchmark risk for producing countries, forms the basis of the EU Deforestation Regulation. Operators (those who place commodities on the EU market for the first time) and large traders will need to meet several requirements (gathering information, risk assessment, and, if necessary, risk mitigation) and submit a due diligence statement on compliance. Small and medium-sized enterprises (SMEs) are exempted from these obligations. Article 27 of the Deforestation Regulation stipulates that the European Commission will develop a classification of producer countries into low, standard, and high-risk countries. The high-risk countries will require stricter due diligence measures, based on the deforestation-free definition.

At the time of this report’s publication, the draft Deforestation Regulation is being further discussed in the European Parliament and the Council (EU Member States), with several upcoming voting rounds expected. Implementation is planned for mid-2023. The European Parliament is expected to adopt its position in the plenary session of 12 September 2022. A rapporteur proposed various amendments in March 2022, based on the inputs from at least 70 entities, including commodity traders, civil society organizations, and research institutes. One of the proposed adjustments is removing the proposed three-tier classification of countries into low, standard, or high risk. Other suggestions include putting rubber on the list of commodities in the current scope of the proposed Regulation and adding “other wooded land” next to the definition of “forests” to include forest-mosaic ecosystems, tropical woodlands, and savannas. See the next section for other proposed changes.

Further EU palm oil imports scrutiny under RED II and the SCG legislative initiative

Next to the Deforestation Regulation, the EU Renewable Energy Directive II imposes further restrictions on EU palm oil imports. RED II sets rules for the EU to achieve its 32 percent renewable energy target by 2030, with one of its rules being the gradual phaseout of crop-based biofuels by 2030. So far, phasing out biofuel feedstock applies only to palm oil since palm oil has a high indirect land-use change (ILUC) risk. This phaseout also applies to palm oil derivates such as palm oil mill effluent and empty palm fruit bunches. Critics fear that the gradual phaseout of only palm oil will result in an increase in the use of soy, another deforestation-linked commodity, in the EU’s biofuels mix.

Although the EU wants to align the Deforestation Regulation and RED II, there are substantial differences between both, potentially causing problems with practical implementation. The European Commission requires the Deforestation Regulation to be applied together with the EU RED II for biofuel-linked commodities such as wood pellets or derivatives of soy and palm oil. A RED II expert highlights the different cut-off dates of both (2020 for the EU Deforestation Regulation, 2008 for RED II); different definitions of forest types and different scopes (RED II also includes peatlands, wetlands and biodiverse grasslands); the way of proving compliance (a due diligence obligation for the Deforestation Regulation versus voluntary certification schemes for RED II); and different traceability requirements (RED II can be based on mass balance, while the Deforestation Regulation requires full traceability to the plot of land including geolocation).

The deforestation law also needs to complement the legislative initiative on Sustainable Corporate Governance (SCG), which is aimed at improving company law and corporate governance. Under the SCG initiative, which has been under proposal status since February 2022, palm oil companies, and explicitly corporate directors, are subjected to mandatory due diligence on addressing adverse human rights and environmental impacts in their global value chain. While both pieces of legislation will have a due diligence requirement, the SCG legislative initiative will target a wider range of companies, including also SMEs and non-EU companies. While the requirements of the SCG initiative “go beyond the requirements of the deforestation regulation, they apply in conjunction.”

Potential implications of EU Deforestation Regulation for the palm oil sector

Key discussions about the upcoming EU Deforestation Regulation relevant for the palm oil industry center around the law’s traceability requirements, exclusion of smallholders, potential leakage risks, and the implication of the 2020 cut-off date. Since the proposal is still under discussion, both industry and civil society are lobbying for their own and their members’ interests. Other discussions relevant for the palm oil industry are the inclusion of different types of ecosystems (e.g. inclusion of peatlands next to forests), the Regulation’s human rights-based approach, the reliance on certification schemes as evidence of zero-deforestation compliance, and the risk benchmarking system for producing countries.

Traceability requirement may lead to exclusion of smallholders

One of the Regulation’s central points is the proposed full supply chain traceability of the listed deforestation-risk commodities, which has caused concerns on its feasibility by both industry and civil society. The traceability requirement includes the geolocation with coordinates of the “plots of land” where the commodities are produced (Article 9, paragraph 1, point d). Both private companies and civil society organizations (CSOs) have expressed concerns about the feasibility of this requirement, for various reasons. For instance, some fear that smallholder producers may be excluded from global supply chains resulting from the traceability requirement, and others worry about who would need to carry the additional costs for the implementation of the traceability requirement.

Once the Regulation is implemented, European purchasers may buy from only large-scale oil palm plantations and “scheme smallholders” that can comply with stringent traceability criteria. This could potentially exclude the so-called independent palm oil smallholders which lack contracts to a particular mill or company. Typically, palm oil companies are supplied by two mechanisms: they receive palm oil fruits from their own company plantations or from contracted (scheme) smallholders; or they receive palm oil fruits from third-party suppliers. Particularly traceability to this latter supplier group is complex and tricky, as typically three types of third-party suppliers exist, with a significant role for middlemen in the palm oil supply chain. The transactions between palm oil smallholders and middlemen are unregulated and unregistered. Moreover, before supplying the palm oil fruits to the mill, middlemen commonly mix the palm oil fruits from various independent palm oil smallholders and sort them based on quality. These factors make tracing to the independent smallholder “plot of land” challenging.

A traceability obligation to a single plot of land may further disadvantage smallholders as they often face land tenure issues. The reality is that palm oil smallholders often lack legal entitlements to land, multiple land claims on one property can occur, and different land and crop sharing arrangements exist. For instance, in Honduras, many palm oil smallholders manage land held under a communal title. Under the current draft text of the EU Deforestation Regulation, operators or large palm oil traders are required to not only show exactly from which plot of land the palm oil comes from (Article 9, point d), but they are also required to get the full contact details of any business or person from whom they have been supplied (Article 9, point e). While this latter requirement would be practically infeasible for all indirect, third party-suppliers, it will likely refer to only an operator’s direct suppliers and buyers.

It is worth noting that the rapporteur to the European Parliament proposed the following amendments on the draft EU Deforestation Regulation, which reduces the need for plot geolocation. The new draft text of the Regulation is changed from “including geo-location coordinates of relevant plots of land” to “including geo-location coordinates of relevant production areas,” wherein production areas refer to an “area of land delineated for traceability and monitoring purposes, including a plot of land, farm, plantation, cooperative or village.” At the time of this publication, it is not yet known whether these amendments will be approved, nor how this will be implemented on the ground.

Traceability may require costly, segregated supply chains

The costs of compliance with segregated supply chains may be considerable for palm oil companies, but it remains questionable whether segregated supply chains are truly required. Segregation is not mentioned, nor is it legally required under the Deforestation Regulation proposal. However, the rapporteur who suggested amendments on the Deforestation Regulation noted that “making sure that a commodity is deforestation-free inevitably means that segregated supply chains will have to be set up.” Moreover, he proposed a 24-month period, instead of 12 months after the enforcement of the Regulation to become compliant with “setting up segregated supply chains.” In contrast, environmental charity Client Earth points out that “mixed supply chains are permissible and segregated supply chains are not necessary, provided that the due diligence requirements can be completed for all the Covered Products supplied through the relevant supply chain.” In order words, supply chains need to be only traceable, not necessarily segregated.

Moreover, an expensive market segregation strategy would be redundant if commodity traders invest in and implement traceability and monitoring strategies that cover the companies’ entire operations instead of creating segregated markets. Indeed, if the traceability and monitoring systems already being implemented by major forest-risk commodity traders can remove deforestation from their supply chains at the point of origin, there would not be any additional costs for segregated storage or logistics.

Nonetheless, while the Deforestation proposal does not require it, segregation may be a practical result under the Regulation, increasing compliance costs, potentially for smallholders. The experience from existing certification schemes, such as RSPO’s “Identity Preserved” and “Segregated” supply chain models or genetically modified organism (GMO)-free products, demonstrate that a segregation strategy to farm level would have high implementation costs, especially when applied on a small scale. Separating sustainable palm oil from ordinary palm oil involves high adaptation costs of additional storage facilities and logistics, since for many commodities, operators currently share supply chain infrastructures (e.g., warehouses, trucks, tanks). In response, Client Earth reiterates that “while the relevant supply chain must be traceable, it is not necessary that each individual product is traceable to its point of origin as it moves through the supply chain,” such as in trucks, or in containers.

Some NGOs worry that these potential costs of compliance of segregated supply chains will be put (partly) on palm oil smallholders. An Indonesian palm oil expert indicated to CRR this may be a major concern as currently similar dynamics occur in partnerships between palm oil companies and scheme smallholders. In such partnerships, palm oil companies must take care of the legal ownership documentation. But according to the palm oil expert, they often put the burden (charge of fees) to the scheme smallholders.

Traceability requirement may also empower smallholders, shorten supply chains

Contrary to the statements above, smallholder representatives in the palm oil industry stated their support in favor of a strong traceability requirement in the EU Deforestation Regulation. Smallholder associations in palm oil and cocoa say a strong traceability system is both feasible and needed to improve smallholders’ positions in the global marketplace. Contrary to industry statements, a palm oil smallholder representative organization has stated that traceability is feasible, is not expensive, and that smallholders are used as an excuse by commodity traders to say the EU Deforestation Regulation traceability requirement is not feasible. Instead, the traceability requirement will promote shorter supply chains and a direct link between independent palm oil smallholders and mills. As such, it may decrease smallholders’ dependence on middlemen, reducing the risk of non- or unfair payments, and make smallholders more visible in the value chain.

The traceability requirement could be disadvantageous for smallholders if EU commodity traders and operators use the Regulation to exclude smallholders from their global supply chains to minimize the cost of compliance.

Stricter EU import requirements may not address global leakage problem

The stricter EU import requirements may lead to leakage of unsustainable palm oil in Indonesia’s domestic biofuel market and in countries with less strict environmental regulations. Indonesia’s government mandated that biodiesel sold in the country must be mixed with 30 percent of palm-based biodiesel (B30). The goals of this policy are to cut its energy imports, meet green energy targets, and increase the consumption of palm oil — the feedstock to the fuel. The Indonesian government is ultimately targeting a 100 percent biodiesel (B100) market. There is currently no domestic sustainability or traceability standard for biodiesel, providing an alternative market for palm oil producers that may not be (or willing to be) eligible under new sustainability and traceability EU import requirements. For instance, known deforester Jhonlin Group turned to the Indonesian domestic biofuel market in 2021.

Indonesia’s domestic biofuel market may also provide independent smallholders with an alternative market if the EU import traceability requirements eventually exclude them from the EU market. For several Latin American countries exporting palm oil to the EU, such as Honduras and Guatemala, there may be fewer markets to send their palm oil.

Leakage of unsustainable Indonesian palm oil to countries with weaker environmental regulations is also a major concern. Earlier CRR studies on palm oil leakage markets in South Korea, India, Japan, and China have demonstrated that unsustainably produced palm oil in Indonesia was bought and financed by South Korean, Indian, Japanese, and Chinese buyers and financers. Unsustainable palm oil can still be processed through so-called “leakage refiners,” refineries that source palm oil without placing meaningful sustainability criteria on the suppliers from which they source.

Leakage also occurs through so-called “shadow companies,” companies that (often purposely) have complex and opaque ownership structures. Deforestation occurs at related parties that belong to the same ultimate owners as NDPE committed entities. For some palm oil mills, it remains unclear who is the ultimate owner.

Finally, the EU Regulation risks leakage from not including all deforestation-linked palm oil products. Other palm oil derivatives like oleochemicals are not included in the scope of products under the Deforestation Regulation. One such product is Palm Fatty Acid Distillate (PFAD, HS 38231930), a palm oil processing residue that is largely used for the production of biodiesel, animal feed, candles, and soap. In 2021, the EU imported over 1 million MT of fatty acids from refining (palm oil, palm kernel and coconuts) from Indonesia alone. The Regulation does not explain whether PFAD would fall under the Regulation’s notion that it shall not apply to goods that “are produced entirely from material that has completed its lifecycle and would otherwise have been discarded as waste.”

Just before the publication of this CRR report, the EU Environment Ministers proposed to include PFAD under the palm oil products that should fall under the EU Deforestation Regulation.

2020 cut-off date could undermine 2015 NDPE commitments

The cut-off date proposed by the EU deforestation law forbids any commodity-linked deforestation from December 31, 2020, potentially undermining 2015 palm oil industry NDPE commitments. In the palm oil sector, it is common to rely on the voluntary cut-off date of December 31, 2015 for compliance with so-called No Deforestation, No Peat, No Exploitation (NDPE) commitments. A public Indonesian CSO statement argued that with the EU law’s December 2020 cut-off date, “massive forest destruction in the period before the cut-off date will be whitewashed.” This would reward companies that have continued sourcing from deforested areas after the NDPE December 2015 cut-off date. It would also allow for the placing on the EU market of commodities and products that originate from land that has been illegally deforested but whose status has been or could be retroactively legalized. In short, it would undermine existing palm oil industry NDPE commitments.

A Southeast Asian palm oil expert told CRR that there is currently confusion on how the more recent threshold date for due diligence will apply to the “recovery methodology.” The methodology is currently being developed and liability is being calculated from the cut-off date of December 31, 2015. Any change to the cut-off date and a move way from December 31, 2015, which is now largely accepted by the industry, risks undermining efforts to hold companies liable for previous deforestation. It also risks a two-tier system developing, with some companies operating in compliance of industry NDPE policies and some in compliance with the EU.

A new cut-off date of December 31, 2021 was proposed by the EU Council just before the publication of this CRR report. The new proposed cut-off date is part of an opinion piece from the EU Environment Ministers on the Regulation, who is aiming for “the right balance” between ambition and realism. The new proposed cut-off date would not solve the concerns addressed above.

Other discussions include the scope of protected vegetation, human rights approach, and compliance through certification schemes

While the above elements of the EU Deforestation Regulation are key features of the upcoming law, there are other ongoing discussions that are relevant for the palm oil industry. These include the coverage of different ecosystems and the inclusion of peatlands, the regulation’s human rights-based approach, and the reliance on certification schemes as evidence for no-deforestation compliance.

The EU regulation uses the 2000 FAO definition of forests, leaving out due diligence requirements for many other crucial biomes and ecosystems, such as Indonesia’s peatlands. The FAO definition of forests includes natural forests and forest plantations and refers to land with a tree canopy cover of more than 10 percent and area of more than 0.5 hectare. This would exclude other non-forested ecosystems. Environmentalists are alarmed that a focus on dense forests will further push deforestation into grasslands, savannas, wetlands, and peatlands, which are also critical for mitigation of climate change due to their ability to store carbon and for being home to numerous species, i.e., promote biodiversity. This is a real risk, illustrated by the Soy Moratorium, which was largely successful in limiting soy as a direct driver of deforestation in the Brazilian Amazon, but caused an immediate expansion of the soy industry in other ecologically important areas across South America, including the nearby savanna Cerrado, where such an initiative was absent.

As currently framed, the EU Deforestation Regulation’s human rights approach is based solely on the laws of producer countries and will not meet demands of international declarations and conventions on human and labor rights. The draft Deforestation Regulation also does not explicitly include the active engagement of indigenous and other local communities, specially through being consulted prior to any land conversion (the so called free, prior, and informed consent, or FPIC). This may also undermine palm oil industry NDPE commitments that have already integrated FPIC principles. Nonetheless, the amended draft Deforestation Regulation, which still requires several voting rounds, has now expressly included international laws and standards on the rights of indigenous people and tenure rights of local communities, including the UN Declaration on the Rights of Indigenous People, the UN Declaration on the rights of Peasants and other People working in rural Areas, the International Labor Organization Convention 169, and the OECD guideline on human rights and businesses.

There is ongoing discussion about whether the due diligence requirement of the Regulation could be fulfilled with reliance on existing certification schemes, such as RSPO and FSC. CSOs argue that such a preferential treatment or so-called “green lane” for certification systems or third-party verification systems is undesirable and that the obligation for all operators and large traders to carry out due diligence should be maintained. The draft EU Deforestation Regulation asserts that certification can be used as a source of complementary information for risk assessment but that it is not sufficient for replacing palm oil companies’ due diligence obligations. This is based on the European Commission’s impact assessment of existing voluntary certification systems that revealed its shortcomings, particularly linked to certification system’s effectiveness, reliability, integrity, and vulnerability to fraud.

EU deforestation law may impact supply, cause legal and reputational risks

The EU Deforestation Regulation has implications for palm oil actors in various stages of the supply chain, as well as for its financers. There is a risk that supply will decline if the requirements are not met, while companies may face legal and reputational risks if they breach the regulation.

Regulation risks declining supply, intensified by climate change and global crises

The effects of the EU’s Deforestation Regulation will not occur in isolation, but will take place in global commodity markets at a time of conflict and climate change. Current global crises, such as Russia’s invasion of Ukraine and the blocking of export routes, increased export levies on soybean oils in Argentina, and drought in Canada, have increased the need for crude palm oil (CPO) as an alternative source of oils. Ukraine and Russia are the most important sunflower seed producers, while drought in Canada contributed to reduced supply of canola oil for 2022. China has been looking into alternatives for soybean oil, and palm oil is one of the preferred replacements. Moreover, Indonesia’s cooking oil crisis has further pushed up global demand for palm oil, resulting in high CPO prices.

This global commodity context may amplify the risk of supply chain shortages in the EU if commodity operators and traders will not be able to comply with the Regulation’s requirements. Food and feed industry sectors with palm oil uptake are alarmed that the strict EU import requirements from the upcoming Regulation will further increase palm oil prices and reduce resilience and competitiveness of the sector. A group of eight leading industry associations suggested in May 2022 to delay the Regulation’s application on palm oil products until 2030, to avoid the impacts of global supply chain disruptions such as the Ukraine war. To prevent supply chain shortages, the rapporteur on the Deforestation Regulation proposed that products that have already been produced can still be placed on the market until one year following the implementation of the regulation.

Palm oil operators in breach of the Regulation face legal and reputational risks

The Deforestation Regulation provides a stronger binding legal basis for enforcing zero-deforestation commitments, and palm oil operators and traders in breach of the Regulation face legal risks. Voluntary industry commitments, such as NDPE commitments, have been effective but not sufficient in halting palm oil-linked deforestation. In contrast, the EU Deforestation Regulation has a binding legal requirement to ban imports of palm oil connected to deforestation. European palm oil operators and traders must demonstrate under the Deforestation Regulation that they can hold their global suppliers accountable for not being linked to deforestation and human rights violations. Those who cannot would be in violation of the Regulation and can be legally prosecuted and receive penalties if they do not eliminate these risks.

How implementation and enforcement of the Deforestation Regulation will develop, in practice, remains to be seen. There are indications that the enforcement mechanisms of the Regulation, among others based on the previous framework for a regulation on timber imports (EUTR), are not yet sufficient. First, there are minimum requirements for compliance checks. The draft Deforestation Regulation requires member states to check compliance with only 5 percent of the operators and their producers annually. The amended text of the Regulation suggests changing the requirement to 15 percent as an annual standard check, and 5 percent for low-risk countries. Second, the proposed Regulation lacks an obligation for a public list of operators and traders found in breach of the Regulation. If a public list would be there, it would allow for easier legal prosecution. Such a list would provide a strong incentive for compliance, since it would detach prosecution measures from national enforcement agencies’ willingness to apply penalties, increase transparency, and may serve as a deterrent to non-compliant companies.

In anticipation of the upcoming EU Deforestation Regulation, EU Member States have started cleaning their countries’ supply chains, increasing reputational risks for traders linked to high-risk areas. Exposing the names of operators and traders linked to high-risk deforestation areas would likely increase reputational risks for concerning companies. For instance, the French government identified soy traders Bunge and Cargill as the leading soybeans importers in France from high-risk deforestation areas in Brazil. Germany is also commissioning research and models to assess its association with tropical and subtropical deforestation via its consumption of imported agricultural commodities. For instance, a study by Trase on behalf of the German Federal Ministry for Economic Cooperation and Development (BMZ) reveals names of high-risk operators and traders. Other EU countries will likely follow with monitoring systems to identify and expose high-risk operators and traders of palm oil.

Immediate risks and the need for due diligence will mainly lie with palm oil traders, and less with European downstream players. However, reputational risks for downstream players will particularly increase from CSOs that will mainly target palm oil-using downstream companies that are better known to the general public, such as Unilever, PepsiCo, Procter & Gamble, and Nestlé. Increased scrutiny efforts on downstream suppliers’ compliance with the EU Deforestation Regulation are reflected in the many calls for an ambitious EU law on deforestation.

EU Deforestation proposal: Compliance costs and the value-at-risk

Companies and financers in the palm oil supply chain face direct financial costs from compliance with the EU Deforestation Regulation. However, these investments in compliance can also prevent financial risks, including reputation loss. The EU deforestation proposal will confront companies active in the EU market that source palm oil products with additional compliance costs. Best-in-class compliance will likely avoid financial costs and losses from market access risk, fines, financing risk, and reputation risk. Financers of these companies (banks and investors in shares and bonds) may also face financial impacts.

Compliance costs for palm oil sourcing companies in the EU are relatively low

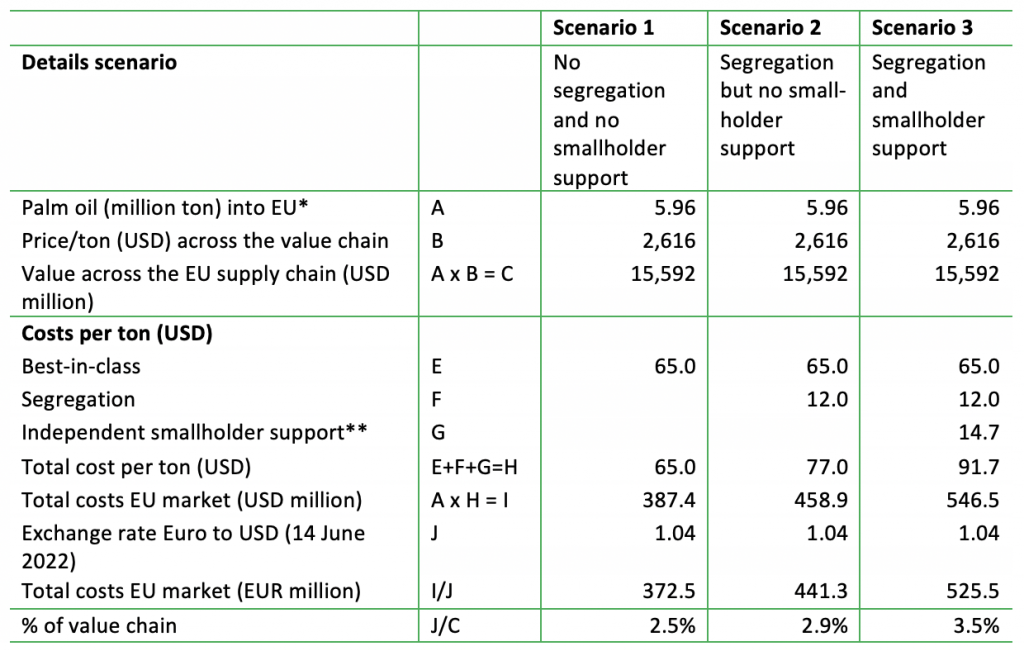

CRR sketched out three scenarios regarding compliance with the EU Deforestation Regulation’s traceability requirement and related costs for companies active in the EU that buy palm oil (products). They include: 1) compliance without segregation of supply chains; 2) compliance including segregation; 3) compliance with segregation and inclusion of smallholders’ support. Under the EU Deforestation Regulation, a key action for palm oil companies active in the EU is reaching 100 percent traceability. As a starting point for most relevant commodities, Identity Preserved (IP) or Segregation (SG) is not required. Internal and external auditing, on-site investigation, installing a due diligence process and buying certified palm might need thousands or millions of USD per company, depending on the total tons that are sourced, according to a CRR report (Scenario 1). However, as analyzed above, the palm oil supply chain complexity may entail segregated supply chains, which would involve additional costs (Scenario 2). A further expansion might consist of extra attention for palm oil smallholders so that they are incentivized to be involved in a segregated supply chain instead of being left out (Scenario 3).

Scenario 1: Regarding the costs of compliance without segregation, the main costs would consist of the establishment of an NDPE and traceability policy, including internal and external auditing, a due diligence framework and, because of the complexity of the palm oil supply chain, monitoring and verification. Companies might need to pay a premium for the certified palm oil product. A CRR report calculated a best-in-class NDPE execution-verification-monitoring approach of USD 65 per ton of CPO. This blend is CSPO (Certified Sustainable Palm Oil) and CSPKO (Certified Sustainable Palm Kernel Oil), and contains auditing, due diligence, verification costs as well as premium prices that needs to be paid by FMCGs.

Scenario 2: A study by Proforest and WWF (World Wildlife Foundation) estimated the costs per ton of segregated palm oil. This study was a follow-up of the European Commission/LMC report. The costs of segregation of palm oil would be between USD 9 and USD 15 per ton (Figure 5). These costs would be five times higher for palm stearin per ton. For CSPKO, there is no estimate. In all cases, the compliance costs for segregation are higher than for Book & Claim and Mass Balance, but the price premiums for certification are also higher for segregation.

Including the best-in-class of USD 65 per ton, the total costs would be USD 77 per ton (in Figure 6 the average of USD 12 per ton for segregation is applied).

Figure 5: Segregation and Identity Preserved: Indicators for price premium for certified sustainable palm products and segregation costs

Source: Proforest, WWF. IP/SG cost includes higher FFB transport cost, tank washing, transport in small vessels, new tanks; *low-end and high-end are market outcomes and/or or estimates for segregation costs.

In scenario 3, the costs for smallholders’ support are included. These costs are financial support for re-planting and to overcome the income/cash flow gap from waiting for new trees to bear fruit (3-4 years). Although this is not part of the EU Deforestation Regulation proposal, these extra costs might be needed to incentivize smallholders. Also, sustainable palm oil customers and investors will feel pressed to add this smallholder component for social reasons (within ESG policies) and to reduce the risk of deforestation because of “poverty” reasons. Smallholders may deforest an area for planting new trees in order to keep the cash flow from aging trees intact. CRR’s analysis of annual replanting and cash flow support for smallholders calculates that the costs could amount to USD 1.1 billion for all the independent smallholders in the global palm oil supply chain. On a per ton basis for produced palm oil, this equates to USD 14.7 (see Figure 6, last column). The largest part is for bridging the cash flow gap for smallholders when they replace old trees with new ones.

Costs for the EU palm oil industry to comply with the Deforestation Regulation are equal to 2.5-3.5 percent of the value chain of embedded palm oil. In the three scenarios, the EU palm oil sourcing sector would need to spend between EUR 373 million to EUR 526 million for 5.96 million MT of palm oil (see Figure 6). The current analysis is limited to CPO as this is the largest part of EU imports. Palm oil represent 73 of volume and 83 percent of the value of all palm related imports into the EU (see Figure 1).

Although USD 547 million (EUR 526 million) seems a material annual expenditure, the relative size is limited. A CRR report showed that the pricing up of embedded palm oil in the whole value chain is 1.94X. This factor is applied to the June 15, 2022 CPO price per ton of USD 1,349. The total value across the EU palm oil supply chain calculates to USD 15.5 billion. The extra compliance costs versus the value of the total palm oil chain is 2.5-3.5 percent. This percentage number is likely an overestimate as compliance costs could gain from economies of scale.

Figure 6: Three scenarios: Annual expenditures by EU palm oil-sourcing actors on compliance with EU Deforestation Regulation’s traceability requirement

Source: Profundo, based on previous CRR reports (see web links in text); Indexmundi: *Based on the total of 5.96 million MT of palm oil that was imported in the EU in 2021. **USD 1.1 billion divided by 75m global production.

Best-in-class compliance could avoid high financial risks, including reputation loss

A company that does not comply with the upcoming EU Deforestation Regulation could face financial risks. A CRR report cited that the reputation value-at-risk is nine to 45 times larger than the present value of future compliance costs (present value = discounted future values), calculated for a group of eight publicly listed large FMCG companies. This reputation risk was three to 15 percent of their equity value. The high end of reputation risk calculation (15 percent) contains the impact of market access risk, financing risk, and the cost of fines. Fines could amount to at least 4 percent of the annual turnover in relevant EU Member States.

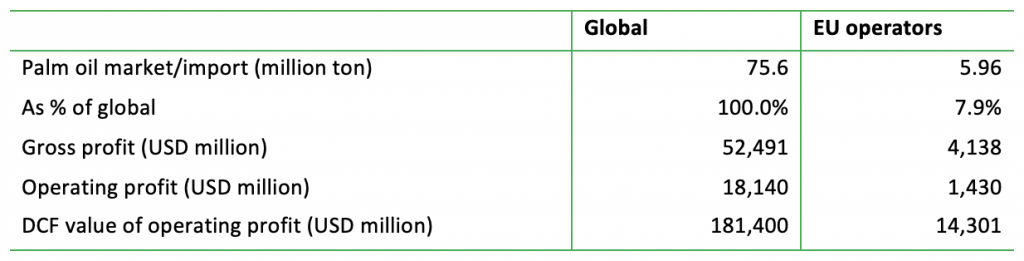

EU actors in the palm oil value chain could lose USD 14.3 billion in case of no compliance (Figure 7). Another way of calculating the financial exposure and risk of a company or sector active in the palm oil supply chain is the Profit Chain Analysis. Operators and traders active in this supply chain generate high operating and gross profits on embedded palm oil. The discounted cash flow of the current and future embedded profits form a proxy for reputation value-at-stake of no compliance to the Deforestation Regulation. EU imports of palm oil (5.96 million MT excluding other palm oil products in 2021) account for 7.9 percent of global production (2020). Based on the Profit Chain Analysis by CRR, global gross profits on embedded palm oil amount to USD 52.49 billion and operating profit USD 18.14 billion. Assuming that EU operators have a 7.9 percent share in the global operating profit on embedded palm oil, the EU sector generates USD 1.43 billion in operating profit for embedded palm oil. The DCF (Discounted Cash Flow) value is USD 14.30 billion, which is a proxy for reputation value that could be lost if all companies do not structurally comply with EU Deforestation Regulation.

Figure 7: EU operators’ reputation value related to palm oil (USD million)

Source: Profundo

Source: Profundo

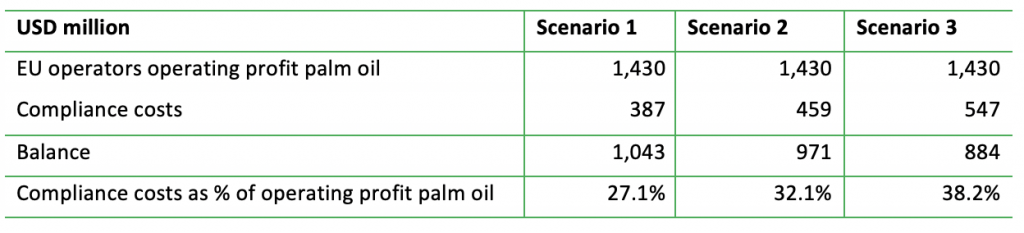

In the EU, compliance costs are significantly lower than profits on embedded palm oil. The EU says that the minimum monetized global benefits of EU Deforestation Regulation clearly offset the costs, referring to the EU budget, not to the corporate sector. Figure 8 shows the operating profits from embedded palm oil of EU operators (USD 1.43 billion, based on Figure 7). The compliance costs in the three compliance scenarios (Figure 6) are substantially below the profits that are generated from embedded palm oil. The positive balance, even with a strict compliance including support to independent smallholders, would be USD 884 million.

Figure 8: EU operators’ benefits and costs (USD million)

Source: Profundo

Implications for financers

The EU financial sector is not directly affected by the EU Deforestation Regulation, leading to negative reactions from more than 100 NGOs. The EU Deforestation Regulation proposal says that the present initiative will not specifically target the financial sector and investments. The reason is that existing initiatives in the area of sustainable finance — EU Taxonomy Regulation and the future Corporate Sustainability Reporting Directive (CSRD) — are well suited to address the deforestation impacts of the finance and investment sectors. These complement and support the legislative initiative on deforestation, the European Commission added. However, civil society (a group of more than 100 NGOs) stated that the EU Taxonomy Regulation and the CSRD lack obligations for investors and banks to stop investments going toward harmful activities and provide no mechanisms to hold them accountable. The group of NGOs is asking for equivalent regulation for financial institutions (in line with those for companies sourcing palm oil).

An equivalent to the Deforestation Regulation for financial institutions may lead to a further shift of palm oil financing to Asian banks and investors. If the above-mentioned proposal of the NGOs were adopted by the EU, the compliance costs of EU financial institutions would sharply increase. This could lead to a further reduction in financing of palm oil-related companies, or a limitation of financing only to larger corporates that work along the lines of scenario 3. These corporations have the resources to spend on certification, accounting, due diligence, segregation and smallholder support (see Figure 6). Like palm oil-related companies in the EU, financial institutions could also face reputation value-at-risk. Asian financial institutions will become increasingly involved in the financing of global palm oil activities, creating leakage risk, as they lack obligations to promote a scenario 2 or 3.

Indirectly, financers would likely be affected by financial risks in their shareholding, bonds, and loans. EU financers could face investment risk from the EU Deforestation Regulation. The Regulation could affect the value and dividend streams of the companies they finance. These companies could be affected by a reduction of access to the EU market, fines, higher financing costs, and/or reputation loss. These losses would vary per investment and would be related to the exposure of each investment to the EU market. It should be noted that EU financial institutions are large financers of companies active in the global palm oil value chain: The above-calculated operating profit on embedded palm oil forms the financial streams that are reaped by banks (interest on loans) and investors (dividends, share buybacks, interest on bonds). A part of the USD 1.43 billion (Figure 8) flows to EU financial institutions and owners, and a portion flows to non-EU institutions/owners. EU financial institutions benefit from palm oil-related activities which are not affected by EU regulation, such as Indonesian palm oil companies exporting to China.