Shadow Companies Present Palm Oil Investor Risks and Undermine NDPE Efforts

June 21, 2018

Since 2013, companies, governments, investors and civil society have taken steps to stop deforestation, fires, peatland development, and mitigate labor and human rights risks in the palm oil sector. These transformative actions include the adoption of No Deforestation, No Peat, No Exploitation (NDPE) sourcing policies, sustainable management policies, government moratoria, stop work orders, and supply chain transparency. Chain Reaction Research reports that 74 percent of SE Asia’s palm oil refining capacity is now covered by these NDPE policies. However, deforestation continues and unsustainable palm oil continues to be produced, traded and consumed. Ten companies caused 75 percent of all palm oil-related deforestation in Indonesia in 2017. Together, these companies deforested 40,000 hectares (ha). This paper discusses how the use of related corporate entities and opaque ownership structures contributes to the ‘leakage’ of unsustainable palm oil to global markets.

Read More | Download Full Report

Farmland Investments in Brazilian Cerrado: Financial, Environmental and Social Risks

September 20, 2017

Following the financial crisis of 2007-2008, there has been a growing investor interest in farmland around the world. In Brazil, this interest has been most pronounced in the Cerrado, a large tropical savanna biome that covers more than 20 percent of the country. Here, institutional investors such as pension funds and private equity, real estate firms and agribusinesses have adopted business models that aim to produce value from land appreciation by acquiring land, clearing it from its native vegetation and transforming it into farmland. While land prices in the Cerrado have increased nearly fivefold between 2003 and 2016, there are signs that the farmland real estate market is currently overheated.

These large-scale farmland acquisitions have resulted in significant environmental and social impacts. Between 2013 and 2015, 1.9 million hectares (ha) of the Cerrado was cleared of its native vegetation. Cerrado deforestation contributed to 29 percent of Brazil’s carbon emissions. Moreover, land acquisition in Brazil is linked to a process of grilagem, whereby land deeds are falsified and later sold. Traditional communities have been impacted through forced removals, loss of hunting grounds and other livelihood impacts.

Read More | Download Full Report as PDF

SLC Agrícola: Cerrado Deforestation Poses Risks to Revenue and Farmland Assets

SLC Agrícola: Cerrado Deforestation Poses Risks to Revenue and Farmland Assets

September 18, 2017

SLC Agrícola is Brazil’s largest publicly traded farming company, founded in 1977. It operates 15 large farms spread across six Brazilian states, and includes activities in the Matopiba region sometimes referred to as the “newest agricultural frontier” in Brazil. It actively purchases, clears and transforms land in the Cerrado biome for industrialized soy, corn and cotton production. SLC Agrícola owns 323,000 hectares (ha), of which 86,765 ha is held through its real estate joint venture SLC LandC which focuses in part on acquisition and transformation of Cerrado savanna into productive farmland — which involves clearing of Cerrado forests. From 2011 to 2017, SLC Agrícola cleared a total of 39,887 ha of land of its original vegetation, over 30,000 ha of which is classified as Cerrado forest by Brazil’s Ministry of Environment; SLC indicates that another 42,000 ha is still to be developed.

SLC faces potential risk of losing access to clients and half its profits due to an overvaluation of its land portfolio resulting from its sustainability impacts, if its main customers put pressure on deforestation issues; at least 20 percent of the company’s revenue comes from clients with public zero-deforestation commitments. However, SLC Agrícola’s share price, which now has a 49 percent discount versus the Net Asset Value, has upside potential from increasing confidence should the company commit to zero-deforestation.

Read More | Download Full Report as PDF

Report: 2017 Indonesian Palm Oil Sector Benchmark: Revenue at Risk vs. Palm Oil NDPE Sourcing

Report: 2017 Indonesian Palm Oil Sector Benchmark: Revenue at Risk vs. Palm Oil NDPE Sourcing

August 23, 2017

This report analyzes the financial risks for the 10 largest Indonesian listed palm oil companies. The report builds upon the outcomes of the Chain Reaction Research report 2016 Sustainability Benchmark: Indonesian Palm Oil Growers, published in December 2016. It adds a financial risk assessment of each company’s revenues calculating revenue at risk in consideration of its No Deforestation, No Peat, No Exploitation (NDPE) compliance. Analysis shows that an improved sustainability performance might lead to better share price returns and lower valuation risks versus a non-NDPE compliant peer.

Read More | Download Full Report as PDF

Report: Olam International – Deforestation Risks from its Peruvian Coffee Supply Chain

Report: Olam International – Deforestation Risks from its Peruvian Coffee Supply Chain

August 3, 2017

Coffee production has been identified by the Peruvian Agricultural Census of 2012 as one of the major drivers of deforestation in the Peruvian Amazon, making up 25.4 percent of agricultural land in this region. Smallholders with less than 5 hectares (ha) of land produce 62 percent of the coffee grown in the Peruvian Amazon, often applying shade-grown techniques. Smallholder coffee production and the expansion of the agricultural frontier by migrant farmers contribute to deforestation and forest degradation.

In 2016, Olam Peru was the second largest exporter of coffee from Peru with 13 percent volume share. Olam Peru has an important role in the coffee value chain. It purchases 95 percent of its coffee from smallholders through agents and intermediaries. Its parent company Olam International (Olam) has zero-deforestation goals, but policy implementation remains not fully adopted within Olam Peru’s coffee value chain. This exposes Olam to deforestation risks, which could result in reputational damage.

Read More | Download Full Report as PDF

Sustainable Banking Initiatives – Regulators’ Role in Halting Deforestation

July 14, 2017

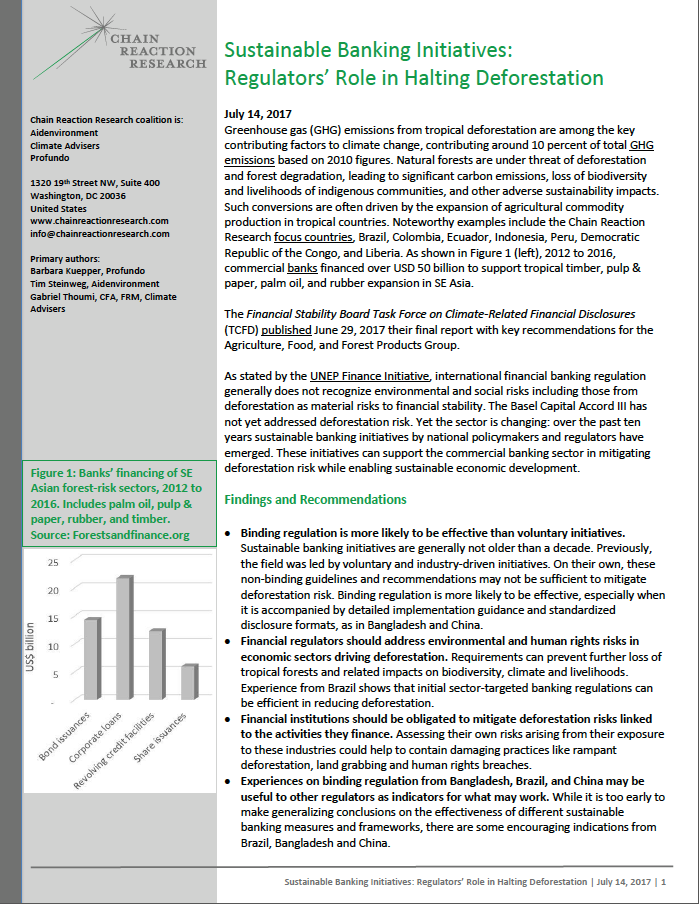

Greenhouse gas (GHG) emissions from tropical deforestation are among the key contributing factors to climate change, contributing around 10 percent of total GHG emissions based on 2010 figures. Natural forests are under threat of deforestation and forest degradation, leading to significant carbon emissions, loss of biodiversity and livelihoods of indigenous communities, and other adverse sustainability impacts. Such conversions are often driven by the expansion of agricultural commodity production in tropical countries. Noteworthy examples include the Chain Reaction Research focus countries, Brazil, Colombia, Ecuador, Indonesia, Peru, Democratic Republic of the Congo, and Liberia. As shown in Figure 1 (left), 2012 to 2016, commercial banks financed over USD 50 billion to support tropical timber, pulp & paper, palm oil, and rubber expansion in SE Asia.

The Financial Stability Board Task Force on Climate-Related Financial Disclosures (TCFD) published June 29, 2017 their final report with key recommendations for the Agriculture, Food, and Forest Products Group.

As stated by the UNEP Finance Initiative, international financial banking regulation generally does not recognize environmental and social risks including those from deforestation as material risks to financial stability. The Basel Capital Accord III has not yet addressed deforestation risk. Yet the sector is changing: over the past ten years sustainable banking initiatives by national policymakers and regulators have emerged. These initiatives can support the commercial banking sector in mitigating deforestation risk while enabling sustainable economic development.

Read More | Download Full Report as PDF

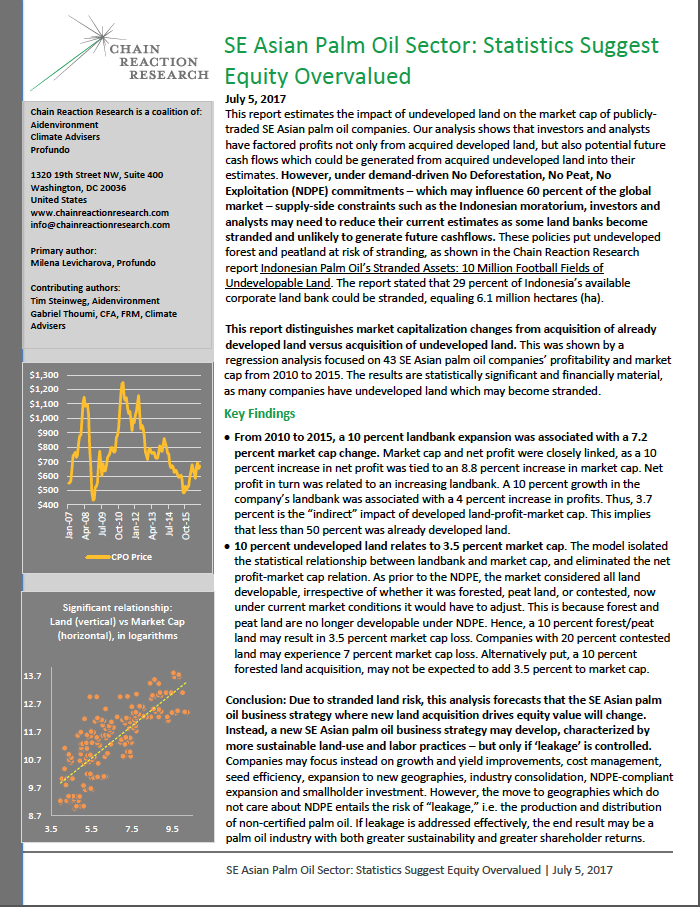

New Report: SE Asian Palm Oil Sector – Statistics Suggest Equity Overvalued

July 5, 2017

This report estimates the impact of undeveloped land on the market cap of publicly-traded SE Asian palm oil companies. Our analysis shows that investors and analysts have factored profits not only from acquired developed land, but also potential future cash flows which could be generated from acquired undeveloped land into their estimates. However, under demand-driven No Deforestation, No Peat, No Exploitation (NDPE) commitments – which may influence 60 percent of the global market – supply-side constraints such as the Indonesian moratorium, investors and analysts may need to reduce their current estimates as some land banks become stranded and unlikely to generate future cashflows. These policies put undeveloped forest and peatland at risk of stranding, as shown in the Chain Reaction Research report Indonesian Palm Oil’s Stranded Assets: 10 Million Football Fields of Undevelopable Land. The report stated that 29 percent of Indonesia’s available corporate land bank could be stranded, equaling 6.1 million hectares (ha).

This report distinguishes market capitalization changes from acquisition of already developed land versus acquisition of undeveloped land. This was shown by a regression analysis focused on 43 SE Asian palm oil companies’ profitability and market cap from 2010 to 2015. The results are statistically significant and financially material, as many companies have undeveloped land which may become stranded.

Read More | Download Full Report as PDF

JBS: Financial Restructuring Could Be Delayed Due to Serious Allegations

JBS: Financial Restructuring Could Be Delayed Due to Serious Allegations

June 28, 2017

JBS is the world’s largest meat company by revenues, capacity, and production including beef, poultry, lamb and pork. It is the largest beef exporter from Brazil. JBS sells its meat products under a range of brands including Swift, Friboi, Seara, Pilgrim’s Pride, Gold Kist Farms, Pierce, 1855, Primo, and Beehive. JBS has executed an aggressive acquisition strategy outside Brazil. As a result, it has high net debt and low equity valuation multiples and now the company lacks room for continued consolidation. Consequently, JBS planned an IPO in May or June 2017 of its activities outside Brazil. This planned IPO of JBS Foods International (JBSFI) represents 85 percent of JBS sales. Barclays PLC is lead underwriter.

In March 2017, allegations of meat contamination, corruption, and deforestation led to a delay of its IPO, which should have generated proceeds of at least USD 1 billion. On May 12, 2017, the Brazilian Federal Audit Court (TCU) released an audit of alleged fraud into Brazilian Development Bank (BNDES) loans used by JBS to finance its Swift & Company acquisition. Because of these allegations, JBS shares dropped. On May 26, 2017, JBS Chairman of the Board resigned. On May 31, 2017, family-controlled J&F Investimentos SA agreed to pay BRL 10.3 billion (USD 3.16 billion) over 25 years as part of a leniency settlement over bribery allegations. On June 6, 2017, JBS announced the sale of its beef operations in Argentina, Paraguay, and Uruguay to Minerva for USD 300 million. Further divestments were announced in June 2017.

Read More | Download Full Report as PDF

Sawit Sumbermas Sarana: Supplying the Palm Oil Leakage Market, Risks for Purchasers

Sawit Sumbermas Sarana: Supplying the Palm Oil Leakage Market, Risks for Purchasers

June 12, 2017

Currently, most large international palm oil traders and refiners have NDPE policies. However, a segment of the market continues to produce or purchase palm oil from recently deforested plantations and cleared peatlands, creating a ‘leakage market’ for unsustainable palm oil. Leakage is defined as any activity in the palm oil industry, production, trade and/or consumption, that is not compliant with NDPE policy requirements. Leakage creates an unlevel playing field and slows and dilutes industry transformation, thereby incurring various financial and reputational risks. The history of Sawit Sumbermas Sarana (SSMS) is instructive.

Due to non-compliance with its buyers’ NDPE policies, SSMS lost 81 percent of its customer base in 2014 to 2015. Nonetheless, it has been able to continue operations and marginal profitability. SSMS restructured contested land bank assets while securing new clients in the ‘leakage market’. Unilever is among SSMS’ new buyers, and its importance of has grown in Q1 2017. Unilever awaits the outcomes of an independent review on sourcing policy compliance to decide on next steps following SSMS’s alleged continuing deforestation and peatland. Next steps could include suspension of sourcing, posing further material risks to SSMS. Unilever’s trading relationship with SSMS commenced after large SE Asian palm oil traders suspended SSMS for non-compliance with their NDPE policies. Notwithstanding the outcomes of the independent review, Unilever’s trading relation might damage its sustainability reputation.

Download as PDF: Sawit Sumbermas Sarana: Supplying the Palm Oil Leakage Market, Risks for Purchasers

BREAKING – Grupo Palmas: First Peruvian NDPE Policy Creates Business Opportunities But Strands Land

April 6, 2017

Grupo Palmas, including Palmas del Espino and subsidiaries, is specialized in the cultivation and processing of palm oil in the Peruvian Amazon. Grupo Palmas is 100 percent owned by the Peruvian conglomerate Grupo Romero. Grupo Palmas is Peru’s largest producer, refiner and exporter of palm oil.

After past controversies, Grupo Palmas is now shifting to a zero-deforestation approach. On April 4, 2017 Grupo Palmas published its No Deforestation, No Peat, No Exploitation (NDPE) policy that covers palm oil and cocoa. This creates new business opportunities, while also stranding its past expansion plans. These undeveloped concessions would be financially risky to develop.

Download as PDF: BREAKING – Grupo Palmas: First Peruvian NDPE Policy Creates Business Opportunities But Strands Land

Alicorp: Peru’s Dominant Palm Oil Player Has NDPE Opportunity

Peru’s Dominant Palm Oil Player Has NDPE Opportunity

March 27, 2017

Alicorp is one of the largest consumer goods companies in Peru, and dominates the Peruvian oils and fats sector. Though the major buyer of palm oil for domestic use in Peru, Alicorp does not yet have a public No Deforestation, No Peat, No Exploitation (NDPE) commitment in place. That poses business risks, as zero-deforestation is rapidly becoming a requirement to access international buyers. Alicorp has an important presence in Latin American countries, and is a domestic market leader in various product categories in the following consumer goods, B2B and aquaculture. Grupo Romero, one of the leading family-owned company groups in Peru, owns 45.7 percent of Alicorp. Between 2000 and 2015, an estimated 40,000 hectares (ha) of primary forest have been cleared for palm oil plantations in Peru. While this represents a minor share of overall deforestation in Peru, it also corresponds to 52 percent of the country’s cultivated area for oil palm.

Download as PDF: Alicorp: Peru’s Dominant Palm Oil Player Has NDPE Opportunity

Indonesia’s Palm Oil Landbank Expansion Limited by Proposed Moratorium and NPDE Policies

February 13, 2017

Indonesia’s proposed palm oil moratorium combined with buyers’ No Deforestation, No Peatland, No Exploitation (NDPE) policies impacts industry growth potential. Within current concession areas, the moratorium adds regulatory risks to market access risks for companies that proceed with developing forests or peatland. Outside these existing concession areas, there is a material loophole in the proposed moratorium for land classified as ‘convertible production forest’ (HPK). However, this loophole is essentially closed by stranded land risks caused by NDPE policies. West Kalimantan has 2.2 million ha of land suitable land for palm oil development outside of its current licensed palm oil concessions. But, because of the moratorium and NDPE policies, at most 6 percent of this land is available for future viable oil palm concessions. Likely responses to NDPE market innovations and the moratorium are an increase in smallholder investments, industry consolidation and vertical integration.

Download as PDF: Indonesia’s Palm Oil Landbank Expansion Limited by Proposed Moratorium and NDPE Policies

Indonesian Palm Oil’s Stranded Assets: 10 Million Football Fields of Undevelopable Land

February 9, 2017

6.1 million ha of forests and peatland are “stranded assets” on the balance sheet of Indonesian palm oil companies and cannot viably be developed. This magnitude is potentially unknown to investors and bankers, and analysts may be mispricing these stranded assets into current financial valuations. Stranded land is a type of stranded asset, “assets that have suffered from unanticipated or premature write-downs, devaluations or conversion to liabilities.” Due to stranded assets, the Indonesian palm oil industry may be facing a trend of lower growth and equity revaluations. Banks may be left with poor loan collateral when the underlying oil palm concession is recognized as stranded land. Risks and costs for companies and credit and equity investors are likely to increase. This means that landbank expansion – regardless of location – is a high-risk financial strategy.

Download as PDF: Indonesian Palm Oil’s Stranded Assets: 10 Million Football Fields of Undevelopable Land

Indofood Sukses Makmur and First Pacific: Financial Risks from Upstream Investments

February 7, 2017

PT Indofood Sukses Makmur Tbk. (Indofood SM), listed on the Indonesia Stock Exchange, is the country’s largest food company. Its largest shareholder is First Pacific Co. Ltd., a Hong Kong-listed conglomerate with interests in food, telecom, construction, and natural resources. Both Indofood SM and First Pacific face financial risks from their upstream investments. These material risks include contested land and labor risks associated with their supply chains and reputation risks from their investments in their Singapore-listed oil palm plantation subsidiary Indofood Agri Resources. A stock price decline of 16 percent could materialize if banks and equity investors with ESG policies avoid Indofood Sukses Makmur because of concerns about deforestation and labor issues at its 74.5 percent controlled subsidiary Indofood Agri. Indofood Agri’s ESG risks could also negatively impact First Pacific’s share price.

Download as PDF: Indofood Sukses Makmur and First Pacific: Financial Risks from Upstream Investments

Indofood Agri Resources: Material Risks from Contested Land and Labor Issues

February 6, 2017

Singapore-listed Indofood Agri Resources (Indofood Agri) is one of the largest oil palm plantation companies in Indonesia. However, 42 percent of the company’s 549,287 ha total landbank is contested. Indofood Agri controls 63 concessions. Of these, six allegedly have community conflicts and labor controversies, and four are located on peat or forest areas and are potentially prohibited from development. Approximately 5,900 ha of peatland burned in 2015 on Indofood Agri’s concessions, and 16 plantation companies — 29 percent of its total landbank — do not publish concession maps. An RSPO complaint was recently filed accusing Indofood Agri of employing child labor and exhibiting poor labor practices, and at least 36 percent of the CPO processed in Indofood Agri’s refineries comes from undisclosed sources. Taken together, these risks could have a 2.5 percent to 20 percent negative impact on Indofood Agri’s share price.

Download as PDF: Indofood Agri Resources: Material Risks from Contested Land and Labor Issues

Banks Finance More Palm Oil Than Investors: Investors Face Indirect Exposure

February 4, 2017

By financing the massive expansion of the palm oil sector, banks are contributing to deforestation, peat development and social conflicts. Analysis of bank financing – both loans and equity and debt underwriting – of 16 major palm oil companies from 2006-2015 shows that banks are more important financiers than equity and debt investors. This means that investors in these banks also are exposed indirectly to sustainability risks. The adoption of no deforestation policies by banks has an impact, but too many banks have not yet adopted such policies.

Download as PDF: Banks Finance More Palm Oil Than Investors: Investors Face Indirect Exposure

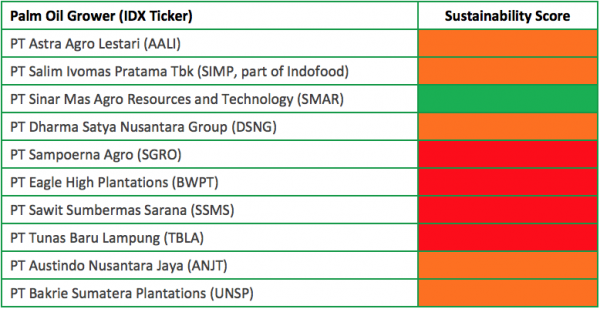

2016 Sustainability Benchmark: Indonesian Palm Oil Growers

December 19, 2016

The sustainability policies and recent practices of 10 largest IDX-listed palm oil growers were analyzed and ranked. Together these companies harvest around 10 percent of the world’s oil palm. Climate change, biodiversity loss and human rights abuses were the key elements of screening. The sustainable purchasing policies of main traders/processors have strengthened the sustainability policies and practices of 4 of the 10 largest palm oil growers listed on the Indonesian stock exchange (IDX). Most of the IDX-listed palm oil growers still have poor sustainability standards. The IDX-listed palm oil growing companies PT Tunas Baru Lampung and PT Sawit Sumbermas Sarana are presently clearing forests and/or peatlands. The world’s top food processing companies Nestlé and Unilever are among their customers.

IDX-listed palm oil growers, sustainability scores:

Download as PDF: 2016 Sustainability Benchmark: Indonesian Palm Oil Growers

Sime Darby: Liberian Crossroads

November 1, 2016

Sime Darby (SIME:MK), a Malaysian conglomerate, signed a 63-year concession agreement in 2009 for 220,000 ha of land to be developed into oil palm and rubber plantations in Liberia. An additional 44,000 ha are to be developed under an outgrower scheme. To date, Sime Darby has planted 10,411 ha palm oil and 107 ha rubber. Our analysis found significant changes in Liberian context since 2009. Customary land rights are entrenched in Liberian legislation and efforts to halt deforestation have increased, heightening risks for Sime Darby’s original aggressive expansion plans. Sime Darby’s undeveloped land bank in Liberia contains high-density forest; thus 45% cannot be developed responsibly. This figure is conservative as it is not adjusted for medium-density forest (an additional 34%) or biodiversity hotspots.

Unresolved issues remain six years after community negotiations started. These long processes create the risk of ‘moving targets’ as previously made agreements can be voided by new developments. Full concession development would require negotiations with an additional 55 communities. This could entail decades of negotiations with uncertain outcomes, and could result in significant delays to project development. Respecting a 2km buffer zone around towns reduces the available area by 20%. Finally, Sime Darby’s share price could devaluate due to restrictions on the concession area. Mainstream investors continue to value Sime Darby’s Liberian project assuming full concession development.

Download as PDF: Sime Darby: Liberian Crossroads

Palm Oil Frontiers: Lessons Learned from SE Asian Corporate Expansion to Africa

October 28, 2016

SE Asian corporations – Golden Agri-Resources, Kuala Lumpur Kepong, Sime Darby, Olam International, Wilmar International, and Felda Global Ventures – are seeking to expand their palm oil business in West and Central Africa. Palm oil has been identified as a driver of both tropical deforestation and climate change, and this expansion also often has financial risks due to concerns about negligence of communities’ rights and environmental impacts. At the same time, countries supporting palm oil expansion are often post-conflict, fragile states seeking development and investments, dealing with weak governance and legal systems and lack instruments to stimulate and regulate responsible management practices.

Chain Reaction Research looked at investments in Africa since 2008, and found that they illustrate both systemic and company-specific material financial risks. For example, the experiences of investors and corporations expanding into Liberia illustrate that it is important to absorb lessons from previous SE Asian investments regarding specific social and environmental risks and opportunities.

Download as PDF: Palm Oil Frontiers: Lessons Learned from SE Asian Corporate Expansion to Africa

Noble Group: Cost of capital and deforestation risks under priced? (Revised)

September 2, 2016

Noble Group Ltd. is a supply chain manager headquartered in Hong Kong, involved in the commodity trading of oil, coal, metals and palm oil. Five years ago, Noble group was among the 100 biggest companies in the world by revenue, generating it by purchasing physical commodities, transforming and then trading them. Since then, its shares value have decreased 90%. For the fiscal year 2015 Noble Group posted its first annual loss in twenty years, losing $1.7 billion due to significant reported impairments. These corresponded to allegations of misleading aggressive accounting overvaluing Noble Group’s commodity contracts.

Chain Reaction Research found that forecast of 2016 revenue is $46 billion, 30% below 2015, due to poor semi-annual performance and asset sell down strategy which may shave 4.5% off expected 2016 operating earnings, 18% annualized. Impairments of palm oil assets and coal receivables may reduce balance sheet equity value by $400 million, or 12%. 33% of Noble’s palm oil landbank is undevelopable as it is primary forest and possibly peat. Coal assets are said to be overvalued by 30%. Syndicate banks have been involved in the recent rights issue and are also involved in the divestment of North America Energy Solutions (NAES), suggesting a conflict of interest coupled with possible mispricing of debt and future increase in borrowing costs. Net profit outlook for 2016 and beyond is below consensus due to divestments and expectations for higher interest rate. Risks for shareholders remain.

Download as PDF: Noble Group: Cost of Capital and Deforestation Risks Under Priced? (Revised)

Economic Drivers of Deforestation: Sectors exposed to sustainability and financial risks

August 3, 2016

The link between deforestation and climate change is increasingly recognized in, for example, the 2015 Framework Convention on Climate Change’s Paris Agreement and elsewhere. This recognition is particularly important, as the planet has lost about 129 million hectares of forest since 1990. As deforestation is largely driven by specific economic activities and is thus a sector-specific risk, investors and banks must now pay far greater attention.

In four Latin American countries (Brazil, Colombia, Ecuador and Peru), over 70% of combined deforestation is linked to cattle ranching. In two African countries (Liberia and DRC), large-scale and subsistence agriculture are the primary drivers. Palm oil and other agricultural commodities, as well as mining and the exploitation of oil and gas are threatening forested areas in various countries. Logging is a recurrent factor in all forests, while infrastructure and hydropower contribute to deforestation in several countries.

Banks and investors can be exposed to deforestation risks directly, by investing in (multinational) companies operating in the identified sectors in these countries. But they can also be exposed indirectly, through downstream companies that buy commodities from these countries, or through governments and public banks that make infrastructure developments possible.

Read the Summary | Download PDF

IOI Corporation: Customers and Investors Want Sustainability

July 18, 2016

IOI’s March 2016 RSPO suspension is likely to result in lost revenue and reduced operating earnings, continued equity price downdrafts and reputational damage. To demonstrate that IOI understands its market and customers’ concerns, the company may want to focus on achieving RSPO compliance and RSPO Next certification and establishing stringent operational risk controls that properly manage its landbank. Yet, questions remain regarding whether RSPO Next is operational. IOI may benefit from employing a robust operational risk management framework built on sustainability, so as to demonstrate to investors the seriousness with which it takes its current RSPO suspension and its possible palm oil revenue at risk. Simply put, IOI cannot move forward without resolving its RSPO cases first.

Read the Summary | Download as PDF

Palm Oil Revenue at Risk: Failure to Meet Buyers’ Procurement Policies Results in Lost Revenue

June 8, 2016

This report applies a Monte Carlo simulation technique to determine 2016 quarterly revenue at risk for three selected palm oil producers: Austindo Nusantara Jaya, Sawit Sumbermas Sarana and Provident Agro. The scenarios are based on a situation where each company has buyers that suspend purchases, from an undiversified buyer base, due to a failure to meet each buyer’s NDPE policies requirements. The scenario is based on actual revenue lost by these three companies in 2015 due to not meeting buyers’ NDPE policy requirements. After running 1,000 iterations, the analysis presents a 5% probability of revenue at risk. All three companies lost revenue due to non-compliance with buyers’ policies, failing either to identify the risk potential of their non-diversified buyer portfolio or to undertake timely action to mitigate, transfer or avoid it.

Read the Summary | Download as PDF

Comprehensive Risk Analysis: Felda Global Ventures – RSPO credentials at risk, immediate cash flow impacts

April 21, 2016

New data shows that Felda Global Ventures Holdings Berhad (FGV:MK) is in breach of Roundtable on Sustainable Palm Oil (RSPO) standards, as its subsidiaries cleared 880 ha of identified High Conservation Value peatlands. RSPO certified sustainable palm oil (CSPO) often sells at a premium to crude palm oil (CPO), which means FGV may lose this premium if temporarily suspended from RSPO. Malaysian palm oil giant IOI Corporation was temporarily suspended from RSPO in March 2016. If FGV follows suit it could loose a CSPO premium of 1% to 2% compared to their average 2015 selling price, resulting in $6 to $12 million in cash-flow-at-risk in 2016, excluding broader market share losses.

Read the Summary | Download as PDF

Comprehensive Risk Analysis: Possible IOI RSPO Suspension

February 16, 2016

The RSPO Complaints Panel’s pending decision on IOI Corporation’s (IOI:MK) operations in Sarawak and West Kalimantan concerns illegal land grabbing, peatland clearing and drainage, loss of High Conservation Value (HCV) forests, and planting palm oil trees illegally inside a forest reserve. RSPO’sRead the Summary |

Download as PDF

Overview Risk Analysis: Fires Burn Southeast Asian Assets

December 11, 2015

From July 1st to October 20th, 2015, 97,000 fires were detected in Indonesia, and over two million hectares of forest caught fire, one-third of which were High Carbon Stock peat forests. Investors may lose money as ineffective oversight and enforcement by plantation companies, as well as local and national government, has allowed fires to burn without proper control measures in place. The resulting haze in Southeast Asia isRead the Summary | Download as PDF

Comprehensive Risk Analysis: Sustainability and Legal Issues Pose Serious Financial Risk for SSMS

September 9, 2015

Sawit Sumbermas Sarana (SSMS), a large Indonesia palm oil producer, is exposed to significant financial risk due to sustainability and legal compliance issues that could prevent its plans for rapid growth in the coming months and years.

Read the Summary | Download as PDF

Overview Risk Analysis: IDX-Listed Palm Oil Growers

June 30, 2015

Six out of ten largest palm oil growers listed on the IndonesianRead the Summary | Download as PDF

Comprehensive Risk Analysis: Triputra Agro Persada

May 21, 2015

Triputra Agro Persada (Triputra/TAP) is a privately owned Indonesian palm oil and rubber plantation company. This Comprehensive Risk Analysis gives anRead the Summary | Download as PDF

Comprehensive Risk Analysis: Kuala Lumpur Kepong (KLK) Bhd.

February 26, 2015

Kuala Lumpur Kepong (KLK) Bhd. is a large Malaysian palm oil company that manages more than 200,000 hectares of palm oil plantations in Indonesia, Malysia and Liberia, and is active in the manufacturing of oleochemicals in Malaysia, China and Europe. This Comprehensive Risk Analysis gives an overview of the company, delves into the environmental and social issues it faces, and presents a financial analysis of how sustainability risks may impact the bottom line.

Read the Summary | Download as PDF

Initial Risk Analysis: Golden Plantation Tbk.

December 11, 2014

From 15 to 17 December 2014, plantation company Golden Plantation Tbk. is making an Initial Public Offering (IPO) on the Indonesian Stock Exchange (IDX), with the aim of raising around IDR 230 billion (USD 15.2 million). The company is currently a full subsidiary of the Indonesian-listed food company PT Tiga Pilar Sejahtera Food Tbk (TPSF), which will still own 78% of the shares after the IPO. This Initial Risk Analysis provides an initial analysis of potential financial, sustainability and governance risks associated with PT Golden Plantation. It is meant to inform investors participating in the IPO, as well as shareholders of the American commodity trader Bunge and investors who have committed funds to the American private equity group KKR – which currently have a stake in PT Golden Plantations.

Read the Summary | Download as PDF

Initial Risk Analysis: BW Plantation Tbk. [Now: PT Eagle High Plantations Tbk.]

November 19, 2014

On 24 November 2014, the shareholders of the Indonesian oil palm plantation company BW Plantation Tbk. will be asked to agree to a new rights issuance to finance the take-over of Green Eagle Holdings. To inform BW Plantation’s present shareholders about several risks associated with the proposal, Chain Reaction Research (CRR) is releasing this Initial Risk Analysis.

Read the Report | Download as PDF

Comprehensive Risk Analysis: Bumitama Agri Ltd.

October 16, 2014

Chain Reaction Research conducted a Comprehensive Risk Analysis of palm oil giant Bumitama Agri Ltd., and found that deforestation and other sustainability issues pose major financial risks. If not resolved, they could affect Bumitama’s access to its primary customers as well as global capital markets. However, the company has recently made serious moves towards addressing these issues, positioning itself to avoid some of the largest risks.

Read the Report | Download as PDF

Initial Risk Analysis: Sawit Sumbermas Sarana Tbk.

December 9, 2013

Chain Reaction Research conducted this Initial Risk Analysis identifying serious undisclosed risks associated with the scheduled December 12 Initial Public Offering of the palm oil company Sawit Subermas Sarana Tbk. on the Jakarta Stock Exchange.

Read the Report | Download as PDF

Comprehensive Risk Analysis: Felda Global Ventures Holdings Bhd (FGVH)

June 12, 2012

Oil palm plantation company Felda Global Ventures Holdings Bhd (FGVH) aims to raise RM 9.95 billion (€ 2.5 billion) from its listing on the Bursa Malaysia, making it the world’s second largest IPO in 2012 after Facebook. We initiate coverage on FGVH with an AVOID recommendation as our analysis shows that an accumulation of environmental, social and governance risks will result in serious financial risks for investors.

Download as PDF