In the light of environmental and social sustainability concerns in relation to palm oil from Southeast Asia, several Latin American countries see an opportunity to open export markets as they present palm oil from the region as a more sustainable option. However, social and environmental sustainability concerns are also prominent in the Latin American sector and require continued due diligence. This report looks at the palm oil market developments and connected sustainability issues in Colombia, Guatemala, Brazil, Ecuador, Honduras, Costa Rica, Mexico, and Peru.

Download the report here: Latin American Palm Oil Linked to Social Issues, Local Deforestation

Key Findings

- Palm oil production in Latin America has increased by almost 60 percent during since 2011/12, reaching a total of 4.6 million tons in 2020/21. Due to Southeast Asia’s dominance, this amount represents only 6.4 percent of global production but could become more material in coming years.

- A further production increase is forecasted, with export markets in the Latin American region as well as in Europe as important drivers. Some of the leading exporters are Colombia, Guatemala, and Honduras. Brazil and Mexico cannot meet domestic demand and therefore import large volumes from the region as well as Southeast Asia.

- The Latin American region consumes three-quarters of its own production. Food products account for around 45 percent for the largest share, energy accounts for 20 percent, and other consumer products for 35 percent. Demand for food uses, as well as biodiesel programs in several national markets, is expected to further drive regional consumption.

- The direct link between deforestation and oil palm expansion is overall weaker than in Southeast Asia, but it still threatens valuable forest ecosystems. Oil palm may also displace other land uses in several countries, pushing cattle and crop production further into forested areas.

- The dispute for land and the recognition of the rights of indigenous and afro-descendant communities is a common issue in several countries. Moreover, breaches of labor rights in the palm oil industry are widespread. The lack of decent wages and food sovereignty are also migration factors.

- Financiers’ risks linked to social and environmental impacts from palm oil are prevalent for plantations, traders, and FMCGs, as well as energy companies. Investments in the Latin American palm oil chain could face stranded asset, market access, financing, legal and reputation risk due to ESG issues. The biofuel expansion also adds these risks amid limited transparency and deforestation policies.

Latin America supplies 6.4 percent of global palm oil, regional markets are key

Further regional production growth expected as Southeast Asia sees slowing expansion

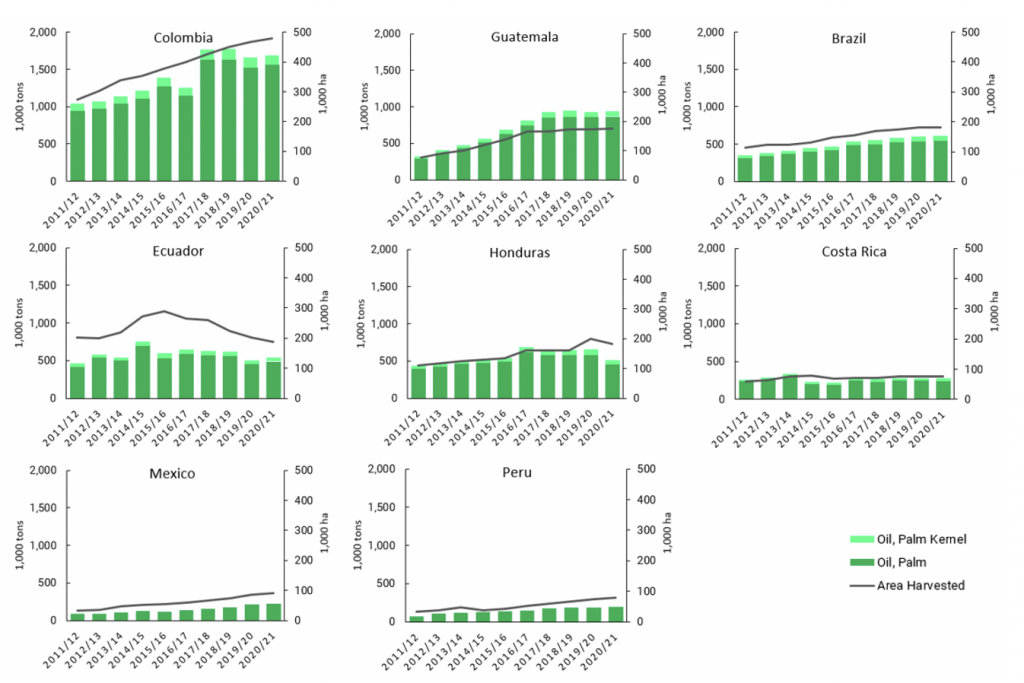

Latin American countries have increased output by almost 60 percent during the last ten years, reaching a total of 4.6 million metric tons (MT) in 2020/21. The Latin American region is currently the second largest palm oil producing region behind Southeast Asia. However, due to the dominant role of Southeast Asian producers with 89 percent of global output, Latin America in its entirety only accounts for 6.4 percent. For 2021/22, a further increase to almost 5 million MT is expected. Five Latin American countries were among the world’s top ten palm oil producers in 2020/21, with Colombia at number four, and Guatemala, Brazil, and Ecuador in places sixth, eighth, and tenth, respectively.

Production areas and levels as well as growth rates differ across Latin American countries. Strong growth rates during the analyzed ten years can be observed for Guatemala, Colombia, and Brazil. Mexico and Peru also increased their production significantly, albeit coming from a much lower level (Figure 1). Production in Honduras, Ecuador, and Costa Rica stagnated or decreased in recent years, with adverse weather conditions and plant diseases as key reasons.

Figure 1: Development of Latin American palm oil production and harvested area

Source: USDA FAS (2021), PSDonline.

The different Latin American countries show considerable variations in palm oil productivity. Yield is highest in Guatemala, with an average of 5.0 MT/hectare (ha) across the last three years. In the middle of the range, Colombia, Costa Rica, Brazil, and Honduras have average yields between 3.4 and 3.0 MT/ha. The yields in Mexico, Peru, and Ecuador were considerably lower at 2.6 to 2.5 MT/ha. In comparison, Indonesia and Malaysia reached average yields of 3.6 MT/ha. Yields are influenced by internal factors such as the quality of seedlings, the age of the trees, fertilization, proper tree maintenance, while external factors like climatic and weather conditions are outside the control of the planter. Yields tend to be lower in countries with large numbers of smallholders.

Production forecasts suggest a continuous growth in the region

Palm oil production in several Latin American countries has further growth potential, for domestic and regional consumption, as well as export markets. Global production of palm oil is expected to further increase, from around 80 million MT in 2021 to 90 million tons in 2030. Besides productivity increases, further expansion prospects for palm oil plantations in Southeast Asia are nearing a limit, constrained by increasingly stringent sustainability requirements and concerns of importers. Therefore, analysts expect growth to take place in other regions, particularly in Latin America. The potential to tap into export markets – both in the region and in Europe – is one driver of cultivation expansion. Moreover, government subsidy programs encouraging the substitution of illicit crops in some countries contribute to an increase in oil palm cultivation in the region.

75 percent of Latin American production is consumed in regional markets

Despite a growing importance of export markets, the Latin American region consumes on average 75 percent of its own palm oil production. Across the region, food products account for an estimated 45 percent of palm oil consumption, energy uses for around 20 percent and other consumer products for around 35 percent. A projected increase in food consumption in the region is one of the drivers of increasing demand for edible oils expected in future years. Frying is an important part of Latin America’s cooking culture, and palm oil is very suited for it. Moreover, several countries, including Brazil and Colombia, are promoting the use of biodiesel as part of CO2 emission reduction goals and aims to reduce dependency on fossil fuel imports.

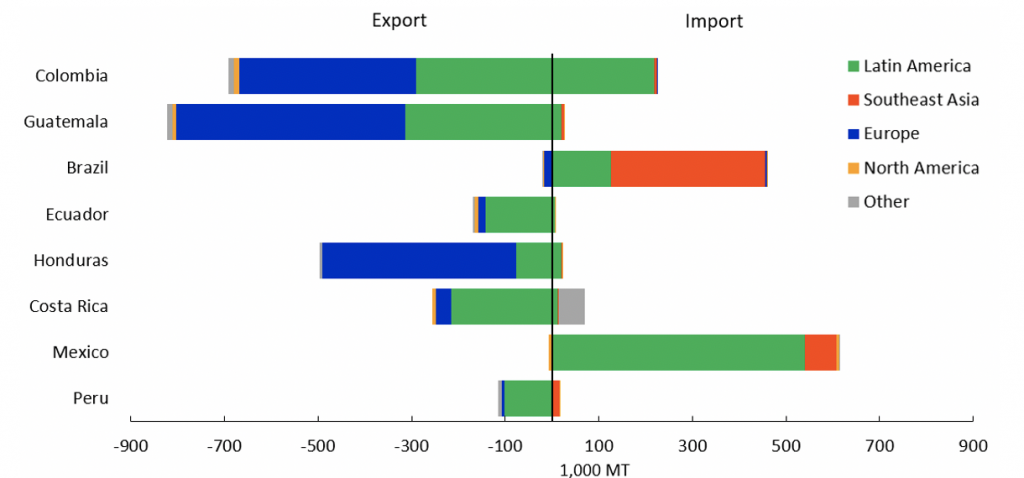

Figure 2: Palm oil trade patterns from Latin American producer countries

Source: Trademap (2021).

Next to regional destinations, Europe is the most important export market. Mexico and Brazil are net importing countries, while Guatemala, Colombia, Honduras, Costa Rica, Ecuador, and Peru are net exporters. The leading exporter in 2020/21 was Guatemala, followed by Colombia and Honduras (Figure 2). During this period, Mexico and Brazil imported palm oil from neighboring countries as well as from Southeast Asia.

Environmental and social impacts of oil palm expansion in Latin America

Voluntary measures, often in the form of public-private partnerships, have been implemented in recent years in several Latin American countries to promote oil palm cultivation, aiming for a more sustainable expansion. These aim to spare forests and promote economic development. However, similar to Southeast Asia, Latin America’s rapid expansion of oil palm continues to be connected to a range of environmental and social sustainability issues.

Oil palm in Latin America mostly expands on non-forested land but deforestation still occurs

Due to the dominant expansion on already deforested land, the land use trajectory in Latin America shows a different pattern than in Southeast Asia. However, while being less prevalent than in the large palm oil-producing countries, habitat loss through deforestation remains a problematic issue in several Latin American countries. Looking at land use change until 2014, a study sample of around 340,000 ha of oil palm plantation across the continent found that 79 percent took place on already deforested land, including pastures (51 percent), croplands, and banana plantations. The remaining 21 percent was converted from forested areas, with most forest conversion observed in the Amazon and the Petén province in Guatemala.

Palm oil driven conversion of natural forests is marked by local hotspots. In the Peruvian Amazon, considerable forest loss for oil palm was linked to a few companies. Between 2000 and 2010, an estimated 72 percent of palm oil in the Peruvian Amazon was expanded on forested lands. In Guatemala, the northern provinces of Petén and Quiché experienced respectively 17 percent and 12 percent of oil palm expansion displacing tropical forests between 2010 and 2019. In the Brazilian Amazon state Pará, around 8 percent of palm oil expansion replaced natural vegetation between 2006-2014, including intact and secondary forests. These analyses of land use change do not yet consider the potential indirect effect caused by the displacement of cattle or crops into still forested areas, especially in agricultural frontier areas.

Being home to a range of highly biodiverse and threatened ecosystems, expansion of agricultural production remains a serious threat to natural ecosystems in Latin America. Severing the link between forest conversion and oil palm expansion may require financial incentives and strengthened land use governance in areas like the Amazon Rainforest, the Chocó-Darién moist forest, and the tropical Maya Forest. Despite the abundant availability of already deforested and degraded land, forested land remains cheaper. According to estimates for Peru, costs for clearing primary forest are around USD 2,000 per ha lower than developing plantations on already cleared land.

In recent years, voluntary sustainability agreements have been agreed in several of the palm oil producing countries, but social and environmental issues are still a concern. The agreements involve a range of stakeholders from industry, government, and civil society. At the same time, many of the large plantation companies claim to bring development and employment opportunities to remote areas while limiting expansion to only previously deforested lands. However, evidence from various countries and instances shows that the Latin American industry has repeatedly breached its sustainability promises. The industry is linked to deforestation, pollution, encroachment on indigenous and traditional communities, land grabbing, and exploitive labor relations.

Colombia is the leading producer and consumer of palm oil in Latin America

Considering domestic production as well as trade, Colombia saw 2020 consumption of palm oil and palm kernel oil in various products reach around 1 million MT. Cultivation on 480,000 ha of land resulted in almost 1.6 million MT of palm oil. The cultivated area increased by 75 percent during the last ten years. More than 80 percent of the over 6,000 producers in Colombia are smallholders.

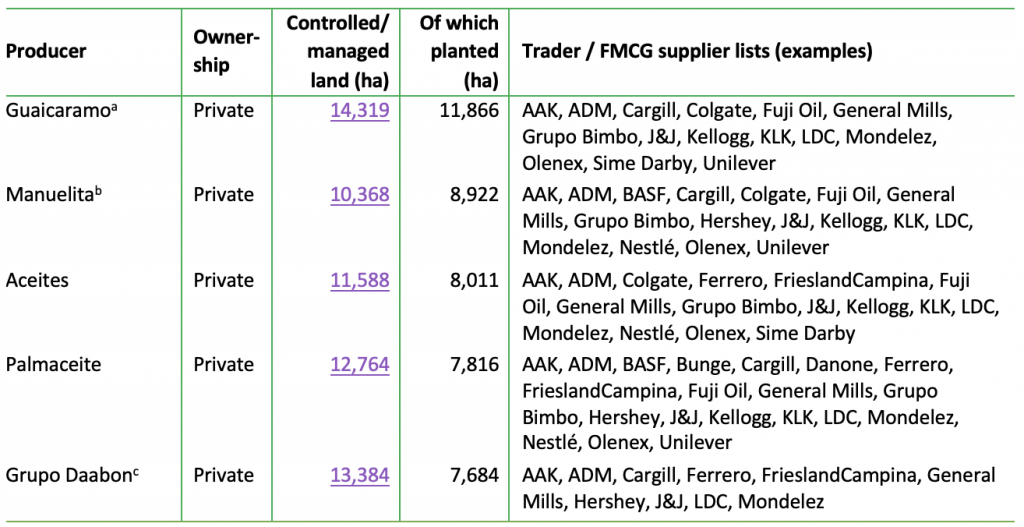

Figure 3: Large palm oil producers Colombia, links with selected traders and FMCGs

Note: The included companies are large domestic actors, but due to limited data availability it is difficult to ascertain whether these are indeed the largest. Not considering biodiesel trade as no relevant palm oil mill lists are available. aincl. Agropecuaria la Tagua, Guantanos; bincl. Palma de Altamira; cincl. Tenquendama, Oleaginosas del Yuma.Source: RSPO ACOP (2021); Palm Oil Mill Lists of Traders / FMCGs (latest available date).

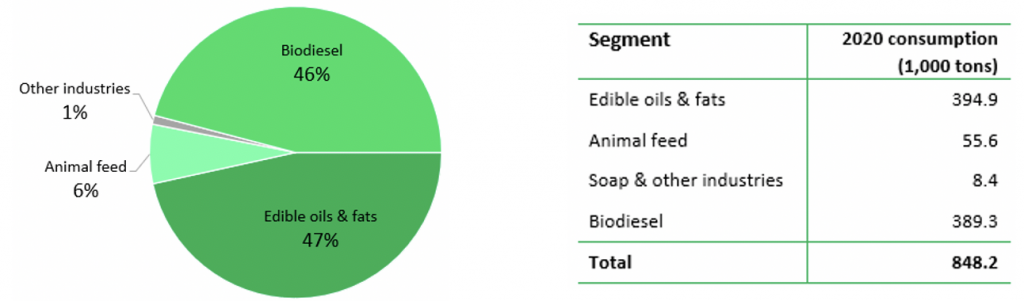

Domestic crude palm oil sales totaled 848,200 MT in 2020, an increase of 3 percent compared to 2019 despite the COVID-19-related contraction for edible and inedible uses in part of the year. Sales to the edible oils and fats segment reached 395,000 MT in 2020, a year-on-year (y-o-y) increase of 14 percent, representing 47 percent of total sales to the local market. Similar to the regional level, palm oil accounts for around two-thirds of Colombia’s edible oils and fats consumption.

Biodiesel is an important economic factor influencing the palm oil sector development

In the biofuel segment, crude palm oil sales contracted by 7 percent to 389,000 MT and accounted for 46 percent of domestic sales. Lower fuel consumption caused by Covid-19 lockdown measures significantly reduced demand for palm oil from the biodiesel industry in 2Q20, despite the mandatory 10 percent blending level. The animal feed segment accounted for 6 percent of total domestic sales (Figure 4).

Figure 4: Key crude palm oil consuming sectors in Colombia, 2020

Source: Fedepalma (2021)

Colombia is projected to produce 2 million MT of palm oil by 2030, increasing by around 25 percent versus current levels, with palm oil-based biodiesel as an important and growing market. After a number of years of stagnation or temporary decreases, the average biodiesel blend is expected to reach 11 percent in 2021. The mandate in most of the country was increased from a B10 to a B12 blend in April 2021.

With a third of its production capacity not utilized, the local biodiesel industry aims to increase output for export. However, opportunities for palm oil-based biodiesel are weak in the EU and the United States, the two largest biodiesel markets. The EU member states are gradually phasing out palm oil-based biodiesel, while in the United States, Colombian palm oil biodiesel is not yet approved under the Renewable Fuel Standard (RFS). In the large Brazilian market, an auction system excludes foreign biodiesel suppliers.

Palm oil industry is not a key driver of deforestation, but illegal expansion into forests observed

Colombia has seen high rates of primary forest loss during the last 20 years, primarily caused by cattle ranching. Colombia, home to some of the most biodiverse forest ecosystems in the world, has been consistently among the countries with the highest tree cover loss in primary forests in recent years. Since 2001, the country lost 4.66 million ha of tree cover. Deforestation occurs in the Amazon Biome in the eastern part of the country and at the Chocó-Darién deforestation front stretching along the Colombian Pacific coast in the western part. On both fronts, cattle ranching has been identified as the primary cause of deforestation. Oil palm expansion mainly has been associated with the conversion of scrublands, croplands, and savannas in Colombia.

Members of Colombia’s association of palm oil producers, Fedepalma, signed a zero-deforestation agreement in 2017. The commitment was signed by producers, processors, and civil society organizations with several ministries. The association aims to increase production of certified palm oil under RSPO (Roundtable for Responsible Palm Oil) or equivalent schemes from 28 percent in 2020 to 75 percent by 2023. The palm oil industry stresses that it plays a minimal role in contributing to forest loss, including in the Amazon. According to government figures for the period 2011-2017, 4,455 ha have been deforested to cultivate oil palm. This comparatively small share of less than 1 percent in overall forest loss is explained by the dominant expansion of oil palm into low productivity pasture lands. Further oil palm expansion is also aimed to focus on degraded pasture land. However, considering the important role of cattle ranching as a driver of deforestation in Colombia, this dynamic raises the question of whether the expansion of palm oil onto pastures is pushing cattle into untouched areas and acts as an indirect driver of deforestation. Moreover, it leaves aside the question of how far degraded areas should be prioritized for restoration instead of being turned into monocultures that lack biodiversity.

Illegal expansion of palm oil plantations has nonetheless been documented in recent years in the Colombian Amazon. This expansion by unknown actors is observed primarily in southwest Meta and northern Guaviare. Research in 2020 found that cattle ranching and mechanized agriculture of palm oil and other crops along with illegal roads and illicit coca crops are increasingly spreading in the Amazon state of Guaviare. Criminal armed groups may be paying peasants to cut down forest and plant coca. Analysis by the Foundation for Conservation and Sustainable Development (FCDS) found at least 250 ha of oil palm planted in forested areas in Guaviare. In the absence of effective law enforcement, oil palm plantations have also started to encroach illegally, yet unhindered into the reservation of the Nukak indigenous people.

In the Chocó Forest, indiscriminate logging and smallholder cultivation of coca, palm oil, and bananas are causes of primary forest loss. Deforestation fragmentation in the forest edges is also linked to large-scale palm oil production. The Colombian government is working on a roadmap to tackle these deforestation drivers and bring net deforestation to zero by 2030, including developing strategies to prevent illicit activities.

Palm oil expansion since the 1990s was linked to internal conflicts and displacements

The expansion of oil palm cultivation in Colombia since the 1990s has coincided with periods of internal conflict, displacement, and unequal land distribution. Several previous governments followed pro-palm oil policies. The ensuing consolidation and legitimization of the legal and commercial control of land resulted in exclusion from land and high rates of displacement and dispossession of local communities. After the peace agreement with the FARC guerilla in 2016, access to land in the light of millions of displaced people remains critical to the lack of a comprehensive rural reform and also affects indigenous and forest reserves.

Researchers found a direct spatial relationship between oil palm expansion and displacement in various municipalities in the 2000s. Expanding oil palm cultivation on dispossessed land contributes to the comparatively small deforestation footprint of palm oil. Large palm oil producers benefit from widespread enforced land acquisitions and violent evictions of Afro-descendant communities in various documented cases. While they might not have been involved in violence themselves, alliances with paramilitaries led to imprisonments of some palm businessmen in the Pacific coast region. In other parts of the country, similar dynamics had no legal consequences.

After the peace agreement, violence by new paramilitary groups against land defenders who call for land restitution and oppose the expansion of agribusiness continued. Such events have especially been observed in Western Colombia’s highly biodiverse tropical forests of the Chocó-Darién region.

Oil palm cultivation has also been linked to socio-environmental problems in other regions. Communities in different parts of the country have been impacted by land dispossession linked to large-scale palm oil developments and the resulting pollution from agrochemicals, water scarcity, restrictions on movement, and constraints on the traditional use of forests and savannahs.

Guatemala shows high productivity and strong export orientation

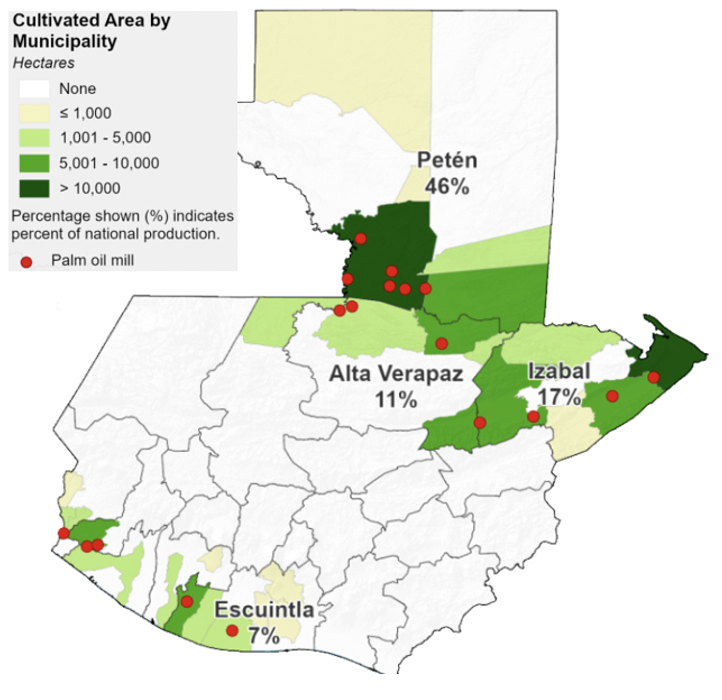

Guatemala is the second largest palm oil producer in Latin America, with the sector contributing 1.13 percent to the country’s GDP in 2020. At almost 20 percent, the GDP share in the main production region, Petén, is much higher. Production is approximately 180,000 ha, with the largest share (59 percent) concentrated in the North of the country (Figure 5). The remainder is split between the South (22 percent) and the Northeast (19 percent). The cultivated area increased by about 130 percent during the last ten years. Of the 235 oil palm growers in the country, smallholders account for 55 percent, while one third are medium-sized producers and 12 percent large producers. However, the large producers are likely to produce a larger share of the volume.

Figure 5: Palm oil planted area in Guatemala by province

Source: USDA FAS (2021)

Strong export orientation of palm oil sector

In Guatemala, palm oil production is export–oriented, making the country the world’s third largest exporter among producing countries. The trade generated USD 461.6 million in export revenues in 2020. However, due to the dominance of Indonesia and Malaysia, the country contributed a share of less than 2 percent to the global palm oil trade. In line with increasing production, Guatemala’s palm oil exports also increased continuously in recent years.

Of a production of 865,000 MT of palm oil and 69,000 MT of palm kernel oil in 2020/21, domestic consumption totaled just 70,000 MT. Most of this consumption is presumably going into food and other consumer products. Biodiesel is currently not produced on an industrial level in Guatemala. Meanwhile, palm oil exports, with a total of 853,000 MT in 2020, have become much more important. Key destinations are the EU with a share of 60 percent in 2020/21, and neighboring Central American countries, including Mexico, El Salvador, Nicaragua, and Honduras, receiving 37 percent. According to Guatemala’s producer association GREPALMA, 64 percent of total production in 2020 was certified under international schemes like the RSPO and ISCC (International Sustainability and Carbon Certification).

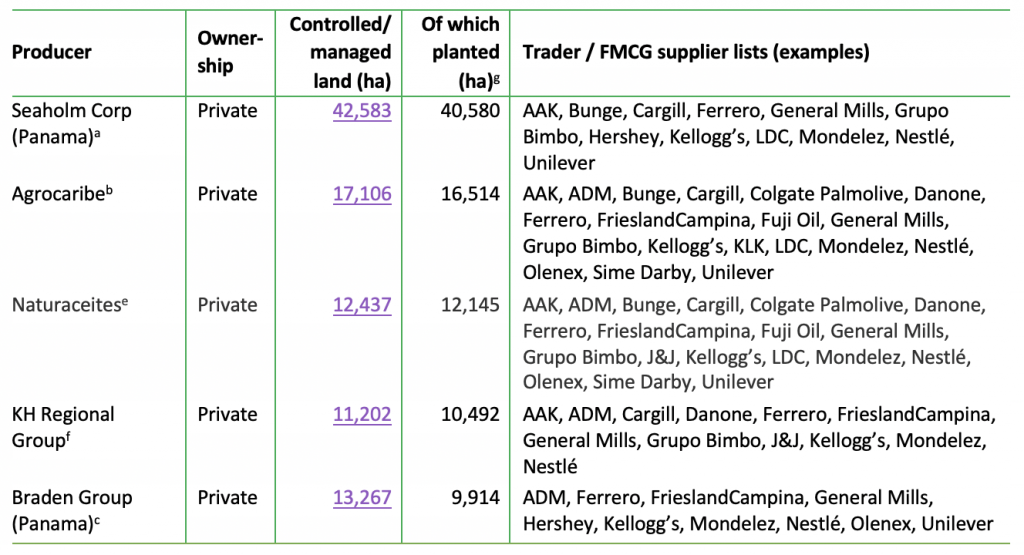

Figure 6: Large palm oil producers in Guatemala, links with selected traders and FMCGs

Note: The included companies are large actors, but due to limited data availability it is difficult to ascertain whether these are indeed the largest. aincl. Grupo Hame, Santa Rosa, Olmeca, Reforestadora de Palmas de el Peten (REPSA), Atlantida; bincl. Extractora Atlantico, Extractora La Francia cincl. Palmas del Ixcán, Agroindustria Palmera San Román; eincl. Exportadora de Grasas y Aceites Vegetales, Tanques Del Atlántico; fincl. Procesadora Quirigua, Nacional Agro Industrial, Alimentos Ideal. Source: RSPO ACOP (2021); Palm Oil Mill Lists of Traders / FMCGs (latest available date).

Palm oil-driven deforestation in Northern Provinces, zero-deforestation agreement since 2019

The expansion of oil palm cultivation in Guatemala since the early 2000s has been one of the drivers of rapid forest loss in the country. In combination with expanding sugar and cattle farming and illicit activities, this has led to one of the highest country-level deforestation rates in natural forests in the world. Between 2010 and 2019, respectively 17 percent and 12 percent of palm oil expansion displaced tropical forests in the northern provinces of Petén and Quiché. In the same decade, more than 1,500 ha of forest were converted to oil palm in Alta Verapaz.

In 2019, the palm grower association GREPALMA went public with a zero-deforestation commitment, but the effectiveness cannot be assessed yet. In 2020, 77 percent of the area managed by its members had exceeded the commitment. In 2020, 64 percent of production was certified under the RSPO or ISCC. GREPALMA members also adopted commitments in relation to human rights and labor conditions.

Breaches of labor and human rights in the palm oil supply chain

Palm oil cultivation is increasingly taking over land from subsistence farmers in Guatemala. Industry supporters are heralded for creating jobs and investments in a region marked by poverty and violence. However, critics point to farmers being forced to sell their land, leading to loss of food sovereignty and co-dependency with companies that have become major employers but pay too little to keep people from migrating. Investigations in recent years found that companies, including Grupo Hame and Industría Chiquibul, paid plantation workers below the daily minimum wage and living cost. Moreover, various palm oil companies, including Naturaceites, Palmas del Ixcán, and Grupo Hame, have been linked to serious labor and community rights violations in recent years.

Indigenous people continue to fight for land rights in the face of an expanding palm oil industry, leading to sometimes violent conflicts. Particularly in the north and northeast of the country, oil palm plantations overlap with the indigenous Maya Q’eqchi’ territory. Leading companies Naturaceites, Palmas del Ixcán, and Grupo Hame are among the companies involved in conflicts with indigenous or local communities over land rights and more economic benefits for the local population.

Brazil increases palm oil production in Amazonian states, remains net importer

Brazil produced 550,000 MT of palm oil in 2020/21, just 0.7 percent of the worldwide production. The cultivated area increased by around 60 percent during the last ten years, albeit coming from a comparatively low level. Most of the expansion is concentrated in the Amazonian state Pará. According to forecasts, the market was projected to show a compound annual growth rate (CAGR) of 13.6 percent from 2019 to 2025.

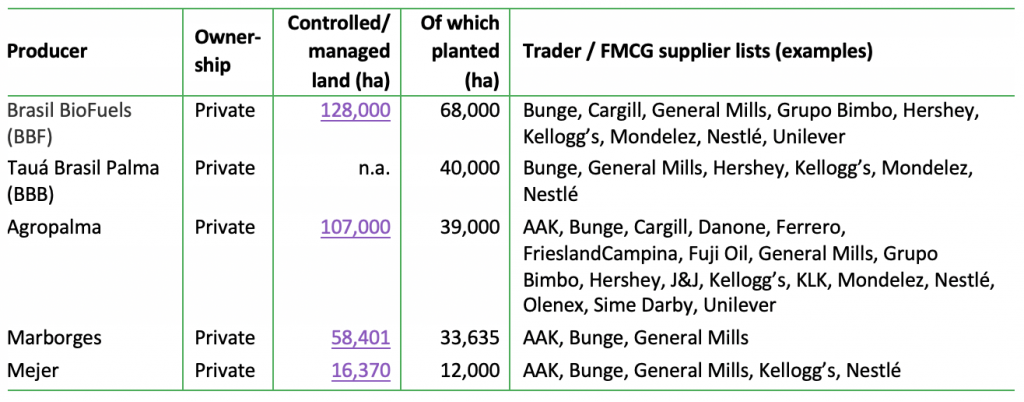

Figure 7: Large palm oil producers Brazil, links with selected traders and FMCGs

Note: The included companies are large actors, but due to limited data availability it is difficult to ascertain whether these are indeed the largest. Source: Company websites; Palm Oil Mill Lists of Traders / FMCGs (latest available date).

Brazil is a net importer, sourcing from Southeast Asia and regionally

In 2020, Brazil imported 460,000 MT of palm oil and palm kernel oil. Contrary to other Latin American countries, Brazil sources most of its palm oil imports from Southeast Asia. In 2020, Indonesia and Malaysia accounted, with a combined 327,000 MT, for more than 70 percent of the country’s imports. Neighboring Colombia was, with 25 percent, another important source.

Since 2010, the Brazilian government has aimed to establish enabling conditions for an expansion of palm oil production and industrial processing capacity in the Amazon. The Sustainable Palm Oil Production Program (SPOPP) stipulated expansion restricted to degraded areas to avoid deforestation and restore degraded lands. It also advocates for social inclusion by incentivizing companies to involve smallholder farmers in their supply chains through contract farming. The program saw the potential for oil palm development without deforestation on up to 30 million ha. The current cultivated area remains far below this level. The Brazilian agricultural research organization, Embrapa, concluded in 2018 that socio-economic constraints, including high relative production costs and the lack of expertise, were among the key reasons for the large discrepancy between estimated potential suitable areas and realized oil palm development.

Policy changes encourage palm oil cultivation for biofuels

Brazil’s RenovaBio policy, implemented in 2020 and formalized as Brazil’s National Biofuels Policy, has revitalized demand for edible oils-based feedstocks, including palm oil. Brazil primarily uses palm oil as an edible oil and for the production of lubricants and greases, while palm kernel oil is used for cosmetics, confectionary fats, and detergents. After a wave of oil palm investments in Pará state for biofuels production in 2005, several companies divested from biofuels when oil prices collapsed in 2014-2016. With RenovaBio, the government is increasingly promoting oil palm cultivation for use as biodiesel feedstock. As part of the program, biofuel production can be certified based on pre-defined GHG emission reduction rates. “Decarbonization credits” (CBios) can be sold and traded to increase compensation for producers enrolled in the program. By end of 2020, 22 out of 241 CBios-certified plants were biodiesel plants, while sugarcane-based ethanol producers remained dominant.

Overall biodiesel production increased by 50 percent between 2017-2020 to almost 6 million MT, with the role of palm oil increasing slowly. Soybean oil remained the dominant feedstock with 71.5 percent in 2020, followed by beef fat with 8.7 percent and other oils and fats with 17.3 percent. However, the role of palm oil has risen continuously in recent years, from 0.8 percent in 2017 to 2.6 percent in 2020, and saw an almost five-fold increase in volume to 160,000 MT.

Recently adopted incentives by the Brazilian government for renewable energy have spurred the use of sugarcane and increasingly palm oil, for power generation. In 2019, President Jair Bolsonaro lifted a ban on sugarcane cultivation in the Amazon to boost Brazil’s biofuel production. Moreover, the government invested in several thermoelectric power plants in the Amazon state of Roraima, which use palm oil as a primary feedstock. In other countries with a longer history of palm oil production for biofuels, palm oil as a primary feedstock for power plants has been controversial due to its links to deforestation. Also in Brazil, environmentalists fear that recent measures to promote biofuels will drive deforestation, adding to the already large pressure on the Amazon rainforest.

Oil palm expansion in Brazilian Amazon linked to deforestation and community rights breaches

A recent CRR analysis found 1,224 ha of deforestation on oil palm plantations of nine key palm growers between 2008-2021. While this total area is relatively small in comparison to the conversion driven by the expansion of cattle ranching and soy cultivation, it happened despite commitments by industry and officials to expand oil palm only on areas deforested before 2008. Of this total, 74 percent occurred in areas designated as legal reserves and/or in permanent preservation areas in frontier areas of agricultural development, meaning that it was likely illegal. Brasil Biofuels (BBF), the largest Brazilian producer of palm oil (formerly Biopalma) was found responsible for 667 ha, of which the majority was cleared in 2019 and 2020. A peak of 165 fire alerts was detected in BBF’s oil palm plantations in 2020. According to CRR, deforestation on Agropalma’s farms, the largest exporter of Brazilian palm oil, was negligible after 2008, with no new plantings observed. Also, CRR found indications of indirect deforestation around oil palm plantations, adding to the existing pressure on the Amazon rainforest from cattle production, soy cultivation, hydroelectric dams, and mining. According to other estimates, 4 percent of the area used to grow oil palm in the deforestation frontier area of Roraima was newly cleared between 2008-2019.

Oil palm expansion in the Brazilian Amazon by companies like BBF has been linked to a disregard for indigenous people’s rights and traditional communities. Recent allegations include the contamination of rivers and soils, and harm to the livelihoods and health of Indigenous peoples and traditional communities. Numerous land rights conflicts with former smallholder farmers and local communities have been documented. Palmaplan has deforested 58 ha in 2018 in close distance to two indigenous territories in Roraima, including isolated groups, despite claims of keeping more distance. Moreover, several reports documented poor working and labor rights conditions on palm oil plantations of Agropalma and BBF in Pará.

Ecuador’s production lowered by disease, mostly consumed in domestic market

While still the fourth largest palm oil producer in Latin America, Ecuador has experienced a decline in harvested area and production since 2015 due to bud rot disease. Palm oil is cultivated by some 6,600 producers in Ecuador. In 2020, it contributed 4.5 percent to the country’s agricultural GDP. With a share of 96 percent, production is dominated by small- and medium-sized growers with less than 50 ha. According to the latest agricultural census, only nine of the farmers produced on more than 1,000 ha.

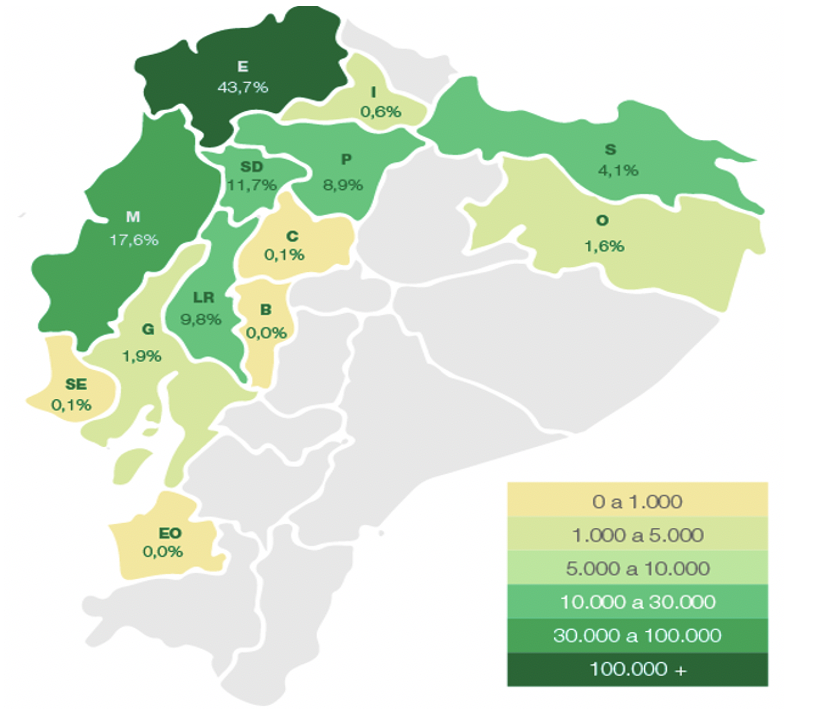

Figure 8: Palm oil planted area in Ecuador

Source: ProPalma Ecuador (2021)

Production is most prominent in the northwestern province of Esmeraldas, stretching along the coast to the South (Figure 8). Production is also found in the Amazon states Orellana and Sucumbios. Production decreased by around 15 percent over the last five years, to 540,000 tons in 2020/21. The reason for the decline in productive area and output is the impact of bud rot disease (Phytophthora palmivora). It is estimated that the disease has damaged some 90,000 ha, with Esmeraldas province most affected.

In 2020/21, around three-quarters of palm oil and palm kernel oil output was consumed domestically, while one quarter was exported. Oils and fats accounted for 69 percent of palm oil consumption in the domestic market, while soaps made up another 8 percent. Regional Latin American markets were the main destinations of Ecuadorian exports, accounting for 83 percent. By far the most important export market is Colombia, making up 75 percent in 2020, followed by Europe with 9 percent. The top five exporters of palm oil products in 2020 – Queve Palma, La Fabril, Grupo Danec, Aexpalma and Fronex – accounted for a combined 56 percent of the total export volume.

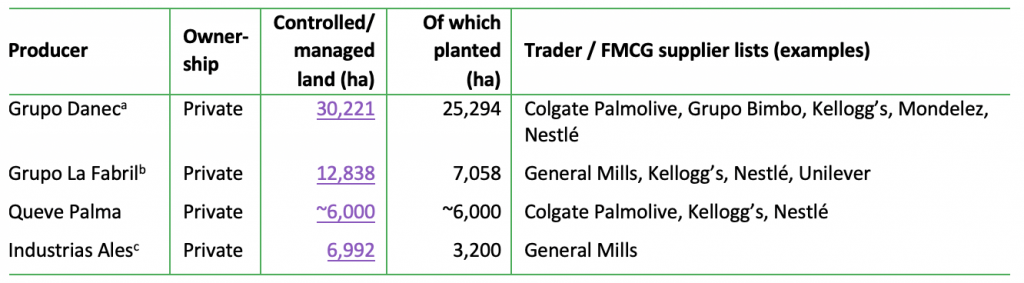

Figure 9: Large palm oil producers Ecuador, links with selected traders and FMCGs

Note: The included companies are large actors, but due to limited data availability it is difficult to ascertain whether these are indeed the largest. aincl. Palmeras de las Andes – Quininde, Palmeras del Ecuador, Palmeras de los Andes – San Lorenzo; bincl. Energy & Palma, La Fabril, Extractora Agrícola Rio Manso; cincl. Agrisanlo. Source: RSPO ACOP (2021); Palm Oil Mill Lists of Traders / FMCGs (latest available date).

Palm oil-based biodiesel is currently not playing an important role in the Ecuadorian market. The country has a biofuels program that aims to reduce the generation of greenhouse gases as well as the dependence on fossil fuels. Presently it consists of ethanol. The high cost of current first-generation biodiesel means that it is only produced in one pilot plant. However, the Oil Palm Law, which was approved in July 2020 and seeks to regulate the economic activities around palm oil production, includes provisions for the promotion of palm oil-based biodiesel, allowing for a B2 blend to cut diesel imports.

Afro-Ecuadoran communities lack land rights and are losing ancestral land to palm oil companies

Afro-Ecuadoran communities are particularly affected by land conflicts that stem from oil palm cultivation. They often lack the land rights necessary to keep palm oil companies from seizing the land while the economic benefits for the communities are lacking. The communities have lost an estimated 30,000 ha of ancestral land since the 1990s, much of it to palm oil production. A land conflict involving Energy & Palma, part of Grupo La Fabril, and Wimbi village in the main producing province Esmeraldas has been ongoing since 2000.

Ecuadorian actors agreed on the introduction of a jurisdictional certification approach for the responsible cultivation of palm oil in a collaboration between the government, the RSPO, and civil society in 2017. In 2018, the government and major supply chain actors agreed a five-year plan to increase sustainability, including investments of USD 1.2 billion. Tax breaks for palm oil exporters are supposed to feed money into a dedicated fund to support smallholders obtaining RSPO or organic certification. However, there are concerns among civil society that the Palm Oil Law focuses only on promoting expansion of planted area, ignoring the impact on communities through the violation of environmental, territorial, and human rights. This system may also exacerbate deforestation in Esmeraldas, the province with the highest deforestation rates in the country.

Honduras uses palm oil exports as important foreign exchange generator

Honduras produced 450,000 MT of palm oil in 2020/21, a decrease of around 22 percent in comparison with the previous year caused by unfavorable weather conditions. It is expected that production will rebound to 600,000 MT in 2021/22. Production is concentrated along the Atlantic Coast in the eastern part of the country. Approximately half of the oil palm cultivated area is in the hands of small producers with surfaces between 5 and 25 ha. During the last two decades, the overall increase in output has been stimulated by economic policies, including targeted subsidies, tax breaks, and funds for small-scale farmers to incentivize palm oil production.

Domestic consumption is estimated at around one-third of production in recent years, while two-thirds are exported. The most important destination is the EU, receiving 83 percent of exports in 2020, while neighboring Central American countries accounted for the remainder. At an export value of USD 357 million, the oil crop is an essential generator of foreign exchange for Honduras, second only to coffee.

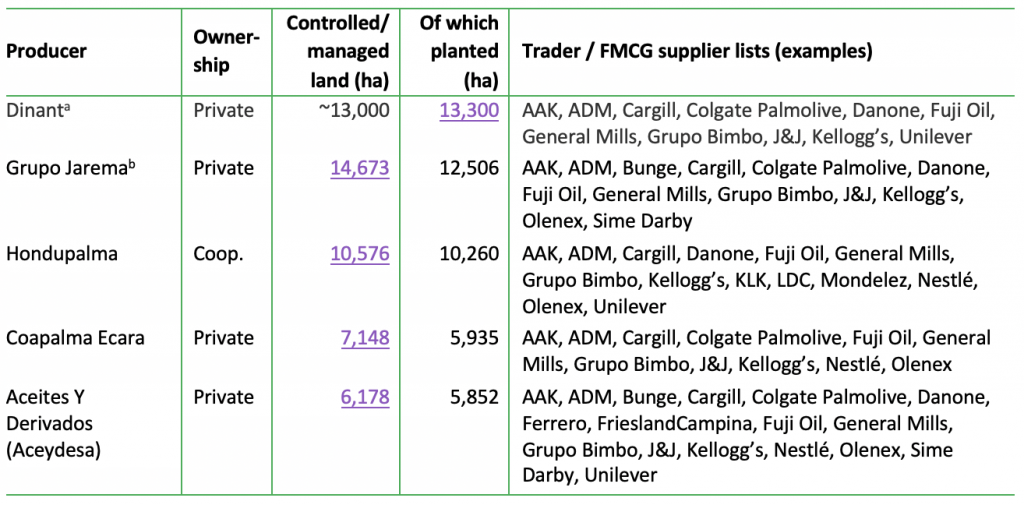

Figure 10: Large palm oil producers Honduras, links with selected traders and FMCGs

Note: The included companies are large actors, but due to limited data availability it is difficult to ascertain whether these are indeed the largest. aincl. Exportadora del Atlántico; bincl. Palmas de San Alejo; Agroindustrial Guaymas; Agricola Tornabe; Agroindustrial Valle Aguan; Agroindustrial Sava; Agroindustrial Mezapa; Agricola Industrial Ceibena; Agroindustrial El Faro. Source: RSPO ACOP (2021); Palm Oil Mill Lists of Traders / FMCGs (latest available date).

Palm oil-driven deforestation in local hotspots, linked to land conflicts

In Honduras, oil palm cultivation has led to less direct deforestation than in other countries as it often replaced banana plantations. However, local deforestation events have been documented, as in the encroachment into national parks in biodiversity hotspots on the northern coast. The oil crop has reportedly replaced between 20 and 30 percent of Punta Izopo and Jeanette Kawas national parks. Fires near oil palm plantations and attributed to logging and agriculture caused further damage. Small-scale farmers, of which some live legally within park borders, clear continuously deeper sections of forest and have become off-the-record suppliers for palm oil companies in the area.

An Agreement for Zero Deforestation in the Palm Oil Chain (Acuerdo para la Cero Deforestación en la Cadena de Aceite de Palma en Honduras) was agreed by a public-private partnership in 2019.

Honduras is among the countries where the dispute for land is also linked to oil palm expanding into areas linked to drug trafficking. Palm oil becomes a factor that exacerbates violence and internal armed conflict. In this context, the repression and intimidation of local communities and the presence of paramilitaries have been reported in Honduras, Guatemala, and Colombia.

Costa Rica, Mexico, and Peru are small producers, experience local illegal deforestation

Palm oil and palm kernel oil production in Costa Rica, Mexico and Peru remained below 300,000 MT per year in 2020/21, but the countries show different patterns.

In Costa Rica, 20 percent of palm oil and palm kernel oil is consumed domestically, while 80 percent, or 255,000 MT, went into export in 2020/21. Imports are negligible. As observed in the larger producing countries, most exports (84 percent) go to other Latin American countries, while Europe received 13 percent. In terms of planted area, oil palm is the second most important crop after coffee. The largest industrial actor is Palma Tica, part of Grupo Numar, which controls a total of 26,465 ha and plants oil palm on 25,141 ha of land. This surface equals almost one-third of Costa Rica’s oil palm cultivation area. Around 70 percent of the oil palm area is planted by 3,200 small- and medium-sized producers, organized in the Agroindustrial Cooperative of Oil Palm Producers (Coopeagropal). Production remained at 280,000 MT in the last two years.

Output by the Costa Rican sector, especially among smaller producers, has been negatively affected since 2013 by bud rot disease, which is aided by poor soil health and a lack of drainage and fertilization. As in other Central American countries, the oil palm is not a significant driver of direct forest conversion, but it may lead to an indirect expansion of the agricultural frontier through displacement of other crops.

In contrast to Costa Rica, Mexico’s production of around 220,000 MT is by far not fulfilling demand, despite an output increase of 164 percent over ten years. Production is dominated by smallholder farmers, accounting for about 90 percent of Mexico’s 8,000 growers. The observed oil palm oil expansion was driven largely by government programs encouraging the planting of oil palm in the states of Veracruz, Tabasco, Campeche, and Chiapas. In 2016, a previous government still had plans to plant an additional 100,000 ha of oil palm in the following years. However, since then the incentive programs favored by the previous government were canceled, encouraging now rather the planting of fruit trees and hardwoods in the same states. Meanwhile, to fulfil growing demand, especially from the food industry, a total of 524,000 MT of palm oil was imported in 2020 from Costa Rica, Guatemala, Colombia, and Southeast Asia.

The increase in planted area since 2016 has reached about 31,000 ha in 2021. Most of this growth has taken place in Chiapas state, where about 70 percent of all oil palm plantations are found. Palm oil companies have reportedly appropriated more than 35,000 ha of land in Chiapas. This expansion has been accompanied by an increased presence of military and paramilitary control forces, which generates violence and dispossession and especially affects women. Many of the plantations are located near natural protected areas and national parks. Smallholders who grow traditional food crops that sustain entire communities are coerced into selling or renting their lands to palm oil companies.

Peru’s palm oil production reached 190,000 tons in 2020/21, with 52 percent of planted area in the hands of small- and medium-sized farmers. Though remaining a small player, this output represented a 140 percent increase over a ten-year period. Net exports totaled around 80,000 tons, with 95 percent staying in the region. The year 2020 saw a first export of about 6,000 tons to Europe. Domestic consumption accounted for approximately 60 percent of output, with food as the key use. Biodiesel production had been halted between 2014 and 2016 due to strong competition from cheaper imports from Argentina but resumed in 2017. Since then, palm oil-based biodiesel has seen a steady output increase to 195 million liters in 2021, driven by antidumping duties on Argentinean biodiesel as well as a biofuel law (Law 28054) promoting domestic production and procurement. As palm oil biodiesel quickly solidifies at higher altitudes due to lower temperatures, it is unlikely that the blend rate will be raised above B5.

The expansion of palm oil production and cattle grazing has been one of the key drivers of the wide-spread deforestation in the Peruvian Amazon since the early 2000s. After previously being linked to deforestation and land disputes in the Peruvian Amazon, the largest palm oil producer, Grupo Palmas (part of Grupo Romero), adopted a zero-deforestation policy in 2017, which was seen as an important steps towards severing the link between palm oil and deforestation.

In Ucayali department, plantations by Plantaciones de Pucallpa (PdP) and Plantaciones de Ucayali (PdU) (part of United Oils (Cayman Islands)) were established since 2012. They were linked to contentious land deals, deforestation on community lands, and other negative impacts on the lives of the indigenous Santa Clara de Uchunya community. In 2015, Peru’s Ministry of Agriculture ordered the suspension of the plantation operations due to illegal deforestation. In 2016, the RSPO issued a preliminary stop-work order against PdP, however, shortly afterwards PdP withdrew from the RSPO and divested from palm oil activities. The RSPO in 2017 nonetheless confirmed a breach of its criteria by PdP. The investigations for irregular land acquisition and deforestation were still ongoing and the call by the Santa Clara community for the restitution of ancestral lands remained unresolved when the Ocho Sur group of companies acquired PdP and PdU palm oil plantations in a public auction in 2016. Peru’s environmental regulation agency, OEFA, revoked previously imposed sanctions and granted Ocho Sur in April 2021 the opportunity to correct its Environmental Adaptation and Management Program (PAMA). Meanwhile, a case at the Constitutional Court filed by the Santa Clara community seeking restitution, titling, and remediation of the land previously acquired by PdP and now controlled by Ocho Sur is pending since 2018. In communication with CRR, Ocho Sur stressed its adherence to all legal requirements and its good relationship with local communities.

The Peruvian palm oil producer association, Junpalma, committed to a sustainable and deforestation-free palm oil supply chain in 2019, aiming for a deforestation free supply chain in 2021. Before that, the Peruvian government adopted a National Plan for Sustainable Development of Oil Palm 2016 to 2025, stating the aim to improve the competitiveness of the oil palm production chain while making it economically, socially, and environmentally sustainable. The Plan strives for more inclusion of smallholder producers, avoiding deforestation, and promoting competitiveness and technical assistance. Critics have pointed to a stagnant implementation of the plan.

Traders, FMCGs, and energy companies linked to Latin American palm oil at risk

Traders and FMCGs sourcing from Latin American palm oil producers risk being linked to environmental and social conflicts. While the deforestation footprint in the Latin American industry is less prominent than in Southeast Asia, local hotspots like the Brazilian Amazon and Peruvian Amazon or the Chocó Forest remain in important forest ecosystems across the continent. Moreover, widespread breaches of human and labor rights form a risk for traders and FMCGs with no deforestation, no peat, and no exploitation (NDPE) policies.

Complaints and conflicts around social and cultural loss from oil palm expansion can lead to operational, stranded land, and market access risks. Conflicts around the expansion of oil palm cultivation are widespread in Latin American countries, aggravated by the commonly observed insecure land rights situation. As demonstrated in a previous CRR paper on the Southeast Asian situation, a lack of effective mitigation of social risks and compensation for losses can cause high costs for companies and their financers.

Financers’ focus should not only be on plantations, traders and global FMCGs for palm oil risk, but also on biofuel companies. With ESG (environmental, social, governance) risks linked to Latin America palm oil, all companies involved in this supply chain face risks. Plantations could face stranded asset, market access, and financing risk. Traders might be most exposed to market access risk, financing risk as well as reputation risk. A large risk for FMCGs is reputation risk, which could have a significant impact on their share price. Finally, legal risk is also increasing in the light of upcoming EU regulation on deforestation and due diligence of supply chains.

The financiers of all these participants in the supply chain could be confronted with a loss in the value of their investment or the repayment of a loan might be delayed. Banks and investors may also be confronted with reputation risk.

Energy and biofuel refineries have become a large client group of palm oil producers. However, in general they lack transparency from which companies they are sourcing: most of the biofuel/energy companies do not publish a mill list. In addition, most of them lack a zero-deforestation policy, and thus potentially create a large leakage market for palm oil from deforested land. Globally, 2020’s gross profits on embedded palm oil in biofuels are estimated at USD 2.4 billion and operating profit at USD 1.4 billion. The implementation of zero-deforestation policies plus a best-in-class monitoring/verification system would cost key players in biofuels only a fraction of their profits. Banks and investors that are financing the expanding chain in biofuels through plantations and refineries, or through financing Big Oil and other palm oil-using energy companies, should be aware of this new investment risk including “material” reputation risk.

Editor’s Note: The report has been updated from its original version to include comments from Ocho Sur.