In the last decade, there have been large strides made in tackling commodity-driven deforestation: Awareness of the impacts of forest loss and degradation on climate change has grown; deforestation rates in Southeast Asia have declined; and corporate accountability and (financial) transparency in supply chains have improved. This report looks back at ten years of Chain Reaction Research (CRR), drawing lessons for the financial sector and other stakeholders.

Please download the PDF here: Financial Risks of Commodity-Driven Deforestation: Lessons from 10 Years of CRR

Key Findings

- The financial sector increasingly recognizes that deforestation constitutes an important part of climate change. CRR supported this shift by translating sustainability risks into material business risks, monitoring deforestation, shaping policy debates, and developing methodologies.

- Southeast Asia has seen a drop in deforestation over the past decade, but leakage risks remain. Since 2014, NDPE policies have become the strongest private sector instrument to cut the direct link between deforestation and palm oil in Asia. However, there are still leakage markets. Oil palm expansion in Africa and Latin America shows that environmental and social sustainability concerns are also prominent in these geographies.

- As NDPE implementation in soy and beef industries in Latin America lags Southeast Asia, pressure to further increase transparency is mounting. Voluntary commitments have been insufficient, with key soy traders and meatpackers continuously delaying zero-deforestation target dates. Complex, non-transparent cattle and soy supply chains and local politics have driven forest loss in Latin America. However, binding legislative initiatives, such as the EU Deforestation Regulation, may accelerate the transition to deforestation-free supply chains.

- Companies and financiers are increasingly aware of the value of their risk and accountability in deforestation-linked supply chains. CRR has valued risks from loss of market access, stranded assets, regulation, operations, and financing in upstream companies. Valuation of reputation risk is crucial for downstream companies. The profit distribution model showed that downstream actors earn the most on palm oil, soy, and beef. Financiers and CSOs now have arguments to hold fast-moving consumer goods companies accountable for their role in supply chains.

- Despite progress in the last ten years, significant work is still needed. Areas of concern include critical global ecosystems not sufficiently protected under national and international laws; the lack of cross-commodity policies; emerging threats linked to palm oil that may increase deforestation; limited attention to social issues and exploitation in supply chains; and unintended negative impacts on climate and livelihoods from the transition of fossil fuels to biofuels.

REDD+ objectives are increasingly integrated in investment decisions

An increasing number of institutional investors and other financial actors now recognize that forest loss and degradation constitute an important part of climate change. CRR, since its inception ten years ago, has supported the integration of REDD+ (Reducing Emissions from Deforestation and Forest Degradation) objectives in investment decisions of institutional investors exposed to sectors that affect tropical forests. Since the start of CRR in 2013, deforestation as a major contributor of greenhouse gas (GHG) emissions has moved much higher on the political agenda and is now understood as a major contributor to climate change. Globally, land use change, primarily deforestation, is estimated to contribute 12-20 percent of total GHG emissions.

Awareness has grown because of the understanding that tropical deforestation is driven by commodity agriculture and poses a material financial risk to investors and financiers. It is now widely recognized that deforestation and other unsustainable business practices can result in the loss of market access, more expensive financing, stranded assets, regulatory costs, and reputation risk. CRR and others contributed in the following ways:

- Adding financial analysis to tangible and intangible sustainability risks

- Developing innovative and tested methodologies that supported (financial) transparency in international supply chains

- Engaging noncompliant companies through institutional investors (e.g., Green Century, IPOs, shareholder resolutions)

- Shaping policy and corporate debates in Latin America, North America, Europe, such as those linked to the EU Deforestation Regulation (EUDR) and Corporate Sustainability Due Diligence Directive (CSDDD).

Educating investors through translation of sustainability risks into financial risks

CRR has translated tangible and intangible sustainability risks into financial risks, including market access risk, legal risk, financing risk, stranded asset risk, and reputation risk. This analysis has helped asset managers’ sustainability officers engage fund managers about the various risks they were taking. Based on analyses in numerous CRR Reports (Figure 1), financial institutions could assess material risks of their clients, based on individual companies’ actions that are linked to deforestation, degradation, and wider environmental and social issues. This includes, but is not limited to, the loss of clients with No Deforestation, No Peat, No Exploitation (NDPE) policies; legal fees, fines, suspensions, and stop-work orders; operational risks such as strikes, property damage, and reduced yields (due to climate impacts); stranded assets, as recent or planned infrastructure or land acquisitions are no longer viable; and reputational damage.

Other than tangible sustainability risks, such as deforestation in hectares, CRR also quantified intangible risks, such as social compensation risk and lack of conflict mitigation. CRR projected the hidden risk of social conflict in the Indonesian palm oil industry at USD 0.4-5.9B. Inadequately mitigating social and cultural loss due to oil palm expansion can result in complaints and conflicts, leading to operational, stranded land, and market access risks for oil palm growers.

Figure 1: Top 20 most viewed CRR reports since October 2018

Source: Chain Reaction Research, analyzed in March 2023. Note: CRR was not able to monitor pageviews between 2013 and October 2018. *While this report was published in 2016, it has been one of the top-20 read reports on the CRR website since Oct. 1st, 2018.

Innovative and tested methodologies improved transparency in supply chains

CRR developed innovative and tested methodologies to improve transparency in supply chains. CRR highlighted who is financing actors in palm oil, beef, and soy supply chains, and supported analysis on which mechanisms contribute to deforestation. CRR analyses also revealed which companies are behind deforestation and which finanicers funded these companies. For instance, the “mystery shopping” research in 2018 allowed for tracing a sample of randomly selected 480 frozen beef and processed products in 48 Carrefour-owned supermarkets in Brazil to the originating slaughterhouses. CRR found 11 products on Carrefour’s shelves that originated from slaughterhouses within the Amazon with high deforestation risks. Carrefour Brasil sourced these products from JBS, Marfrig Global Foods, and Mercúrio, all of which signed agreements (TACs) with the Brazilian governments to refrain purchasing from recently deforested farms. A similar investigation into the Casino Group, in collaboration with investigative journalists and civil society groups, led to a lawsuit filed against the group and its Latin American subsidiaries, claiming that the company’s supply chain practices in Brazilian and Colombian cattle were in violation of France’s Duty of Vigilance law of 2017.

CRR introduced innovative financial methodologies such as the “valuation of reputation risk” and the “profit chain distribution analysis.” The latter made transparent which companies and which sectors are earning the most in the supply chains of tropical commodities. Civil Society Organizations (CSOs) and other entities have used this methodology to focus on the responsibility of the downstream sector to pay for more “sustainable” supply chains. CRR has shown that the necessary price increases for the end-product are only minimal in cases of a segregated supply chain or in scenarios of best-in-class NDPE implementation and verification. For instance, Procter & Gamble would need to raise the consumer retail price of a bottle of Head & Shoulders shampoo by only 0.11 percent to pay for a “best-in-class” NDPE policy execution and verification. The reputation value methodology demonstrates that fast-moving consumer goods companies face material value risk if they do not act proactively on deforestation risks. In a later section of this report (page 12), the Financial Analysis section provides more details, including the impact on financiers.

Pressure on noncompliant companies through direct engagement with investors and companies

CRR, in collaboration with activist investors such as Green Century, has directly engaged noncompliant companies. The collaboration partners filed, or announced to file, shareholder resolutions when they were strategically necessary, prompting key changes at major companies. For instance, CRR published several research reports and Chains (news items) on Bunge between 2017-2018, reporting on how legal deforestation was not covered in Bunge’s NDPE policy and how this posed a major threat to financial investors. Stemming from these reports, CRR and Green Century, together with the New York State Common Retirement Fund (NYSCRF), filed a shareholder resolution proposal, pressing Bunge to address its deforestation risks. In April 2018, Bunge committed to a more stringent zero-deforestation policy, also covering “legal” deforestation and greater traceability in its supply chains.

Investors and funds have divested from several companies repeatedly covered in the CRR portfolio of companies. These include JBS, Marfrig, SLC Agrícola, Olam International, and Sime Darby. Certain financial institutions may have acted on CRR’s analysis and constrained capital availability for companies engaged in deforestation. While this information is often considered confidential and therefore undisclosed, investors may have halted Initial Public Offerings (IPOs), divested their equity, or threatened to do so via proposed shareholder resolutions.

Shaping policy and corporate debates in Europe, Latin America, and North America

CRR has contributed to priority policy and corporate debates relevant for the palm oil, beef, and soy sectors linked to European legislative initiatives such as the EUDR and CSDDD. CRR reports and related CRR webinars have demonstrated how the upcoming EU Deforestation Regulation will impact the palm oil beef, and soy industries and their financiers, including key implications linked to traceability, smallholder exclusion, leakage, and the law’s cut-off date (December 31, 2020). CRR found that compliance costs to the EUDR are relatively low and protect reputation value. Webinars on the EU legislative initiatives are among CRR’s most watched, with respectively over 700 and 450 online views. In addition, CRR outlined how EU corporations and investors face sustainability due diligence obligations from the Corporate Sustainability Due Diligence Directive, for which the European Parliament adopted its negotiation position on June 1, 2023. Companies and financiers will have to prepare for these changes, or they could face financial risks if they default on implementation and compliance efforts. These risks could consist of loss of revenues, loss of EBITDA, financing risks, and reputation value loss.

Trends in Southeast Asia: Drop in deforestation, leakage risks remain

Steep decline in palm-oil driven deforestation in Southeast Asia, NDPE policies as a catalyst

Since 2013, CRR’s education and engagement on deforestation risks contributed to curbing forest loss in Southeast Asia, where deforestation rates, particularly linked to palm oil, have declined in recent years. The largest palm oil refiners and traders have adopted NDPE policies since 2014, the strongest private instrument to cut the direct link between deforestation and palm oil. The sector has seen significant changes during this time span, with an acceleration of the implementation of NDPE policies in recent years. The adoption of NDPE policies by a handful of refiners and traders appears to have catalyzed sustainability improvements in palm oil supply chains. In 2020, CRR reported that NDPE policies cover 83 percent of palm oil refining capacity in Indonesia and Malaysia. Because several refiners, such as the Salim Group, fall short in their NDPE implementation, effective NDPE coverage in 2020 was approximately 78 percent.

CRR has continuously monitored NDPE coverage and engaged commodity traders and producers to adopt NDPE policies. CRR’s Chains in 2018, 2019, 2020, 2021, and 2022 highlighting the top deforesters for oil palm in Southeast Asia that did not implement effective NDPE policies were consistently some of the most viewed CRR Chains (Figure 2 below). From the continuous monitoring of deforestation in Indonesia, Malaysia, and Papua New Guinea, several trends became apparent. While 10 years ago deforestation-linked palm oil still ended up in NDPE supply chains, the largest Southeast Asian deforesters are no longer linked to NDPE markets. Moreover, several longstanding, mostly Indonesian, deforesters continue to be the main culprits. Most deforesters featured in the recent top 10 list also appeared in earlier top deforesters lists, highlighting both the failure of many buyers with NDPE policies to adequately implement their policies and the risk of leakage markets.

Figure 2: Top 20 most viewed CRR Chains since October 2018

Source: Chain Reaction Research. Analyzed in March 2023. Note: CRR was not able to monitor pageviews between 2013 and October 2018.

Government policies, palm oil prices, and wet seasons also linked to declining deforestation rates

NDPE policies, along with government measures, very wet seasons, and low prices for palm oil, have contributed to lower deforestation for palm oil. The Indonesian government attributes the sharp decline of forest loss solely to its forest and peat moratoria policies, but CRR points to several gaps in the government’s policies. First, while Indonesian moratoria are indispensable, loopholes and lack of sanctions fail to stop all palm-oil linked deforestation. The moratoria are considered weak in protecting primary forests and peatlands since they are not legally binding. Moreover, supervision and effective penalties for non-compliance are lacking. Additionally, unusually wet weather and fluctuating palm oil prices likely slowed the rates of deforestation and fires. Since 2020, Indonesia has seen very wet seasons, and oil palm growers could not develop concessions that flooded. Due to climate change, these wet seasons will likely occur more frequently. Also, unstable palm oil prices, with a sharp fall after 2020, may have contributed to the decline, as plantation expansion and forest loss correlate with palm oil prices. By contrast, the sector has seen price increases since the Russian war on Ukraine began in 2022 amid the global surge in demand for edible oils. Finally, the fact that there is simply little remaining forest left in some areas to clear is another explanatory factor for the declining forest rates.

Leakage market shrunk, but risks remain

The snowball effect triggered by NDPE policies has resulted in a recent reduction of the number of actors involved in the leakage market. This decline in leakage market actors has led to reduced volumes of palm oil produced, traded, and consumed without being subject to sustainability criteria. Partially because of these market developments, deforestation in Indonesia has declined significantly in recent years. The trend of decreasing deforestation rates and increasing uptake of NDPE policies reflect the success of CRR and other initiatives.

There is, however, a need for sustained focus on leakage actors and markets. Despite the adoption of zero-deforestation policies across the palm oil industry, a segment of the market continues to produce, trade, and consume palm oil without meaningful sustainability requirements. This “leakage market” has reduced in size in recent years, but the following recent market developments point to several emerging risks that may continue to drive land clearing for palm oil and wood in Indonesia, Malaysia, and Papua New Guinea:

- The increased global demand for palm oil-based biofuels

- The Indonesian and Malaysian governments prioritizing domestic biofuel use, providing a leakage market for plantation developers suspended by NDPE companies

- Continued slow take-up of NDPE policies in regions in East Asia, including China, Japan, and South Korea

CRR has shed light on these risks and encouraged financial institutions and industry actors to take meaningful and coordinated action against leakage companies and markets. CRR reports on leakage markets in Japan, China, South Korea, and Indonesia’s domestic biofuel market are among the most read CRR reports (Figure 1). CRR found that Japan, a large buyer of palm oil and timber products from Indonesia and Malaysia, is a leakage market for both commodities. China is a key market for palm oil and derivatives from Indonesia and Malaysia. Leakage refiners without an NDPE policy or those lagging in their implementation accounted for at least 12 percent of Indonesian palm oil supplies to China. South Korean companies are significant leakage players as both developers of plantations in Indonesia and buyers of palm oil products. On January 1, 2020, Indonesia increased the mandated diesel and crude palm oil (CPO) blend to 30 percent (B30). As a result, the Indonesian government offered local leakage refiners an escape from NDPE market requirements through the palm oil diesel market, since no sustainability requirements were set for biofuel production. Finally, CRR revealed how so-called shadow companies use related corporate entities and opaque ownership structures that contribute to leakage of unsustainable palm oil to world markets.

Palm oil trends in Africa and Latin America: Environmental and social sustainability concerns

In addition to palm oil sustainability and financial risks in Southeast Asia, CRR has also shed light on palm oil trends and lessons learned in Africa and Latin America (LatAm), with one report specifically about Brazil. Environmental and social sustainability concerns are also prominent in these geographies.

Although West and Central Africa have been promising regions for large-scale palm oil production, expansion has not gone as planned. CRR revealed how only a handful of companies control industrial palm oil production and will likely drive expansion in West and Central Africa, but on a smaller scale and at a slower pace than originally anticipated. Nevertheless, these companies have been linked to numerous social and environmental impacts, violating their buyers’ NDPE commitments.

The slowdown of oil palm expansion in the African context is due to the materialization of stranded land risks linked to land acquisition and community resistance. Planned oil palm plantations of at least 27 projects, covering 1.37 million hectares, failed negotiations or were abandoned between 2008-2019. Reasons for delayed, failed, or dropped expansion plans vary and include civil society pressure and community resistance to expansion on their traditional lands. Oil palm growers experience considerable operational risks and costs from violent community conflicts, and many African communities have been successful in their resistance to oil palm development.

In Latin America, palm oil is linked to social risks and local deforestation. CRR analyzed palm oil market developments and connected sustainability issues in Colombia, Guatemala, Brazil, Ecuador, Honduras, Costa Rica, Mexico, and Peru. In the light of environmental and social sustainability concerns in relation to palm oil from Southeast Asia, several Latin American countries have seized on the opportunity to open export markets as they present palm oil from the region as a more sustainable option. However, there are still social and environmental sustainability concerns prominent in the Latin American sector, requiring continued due diligence.

Oil palm growers in Brazil have argued that palm oil production is a “green solution” to safeguard the Amazon as a result of planting on only areas already degraded and cleared before 2008. While palm oil production in the Brazilian Amazon has relatively lower environmental impacts than soy and beef, CRR also revealed how palm oil expansion in Brazil is linked to deforestation, fires, exploitive labor conditions, and land disputes, even in the Amazon biome.

Trends in Latin America: Critical mass of NDPE activity not reached for soy and beef

Voluntary commitments insufficient: Continuous delay on target zero-deforestation deadlines

A major lesson learned is that voluntary zero deforestation commitments in the soy and cattle sectors have been insufficient and not at the pace necessary to halt global warming. Non-legally binding zero-deforestation commitments and certification schemes in soy and beef sectors have been insufficient to halt native vegetation conversion. While the implementation of the voluntary Amazon Soy Moratorium (ASM) has been mostly successful, it has had significant unintended negative side effects. The ASM has shifted clearing for agricultural production and linked vegetation to other vulnerable ecosystems, such as the Brazilian Cerrado.

There is evidence that international companies in the soy and beef supply chains are starting to commit to NDPEs, but progress is slow and a chain reaction, as in the palm oil sector, did not occur. In 2015, Forest500 assessed that less than 20 percent of soy companies had mentioned commodity-specific policies, and in 2023, 43 percent of assessed soy companies have a deforestation commitment in place. For beef, the share is even lower: In 2015, only 26 percent of companies involved in the supply chains of beef and leather were found to have specific commodity policies, compared to 30 percent having a deforestation commitment for beef in 2023. By contrast, in 2020, CRR estimated effective NDPE policies of palm oil refineries cover 78 percent.

Grains and beef companies have continuously delayed their target zero-deforestation deadlines. The 2020 target deadlines of the New York Declaration on Forests (NYDF) and the Consumer Goods Forum (CGF) were not met. Endorsers of the NYDF, a non-binding political declaration initiated in 2014, had committed collectively to remove deforestation from agricultural supply chains by 2020. Also, the Consumer Goods Forum, a coalition of around 400 companies and other stakeholders in 70 countries that sell goods and services worth more than EUR 4.6 trillion, had initially set 2020 to achieve net zero deforestation in supply chains. Instead, the target is now 2030 or later for zero deforestation in the direct and indirect supplier base of many major deforestation-risk companies, such as Cargill, JBS, and Minerva. By 2030, a material part of the remaining native vegetation in the world’s global critical ecosystems may already be gone. Of the 350 companies assessed in the Forest 500, only 55 percent have set a target date of 2025 or earlier.

Neither did certification schemes deliver on their promises: The Roundtable on Responsible Soy (RTRS) and ProTerra Standard for soy did not effectively contribute to a sustainable transformation of the entire sector. In 2021, just over 1 percent (4.6 million MT) of global soy production (371 million MT) was estimated to be certified under the RTRS standard. Moreover, most RTRS-certified soy continues to be sold under a credit system, meaning that physical soy supplies to credit buyers may still be linked to deforestation.

Legally binding initiatives to curb deforestation and human rights violations in supply chains may accelerate the transition to zero deforestation. Besides the EU (EUDR and CSDDD), laws have been proposed or passed in the United States (The U.S. FOREST Act) and the United Kingdom (the UK Environment Act) in 2021 that aim to regulate (illegal) deforestation linked to global commodity production. The laws, along with the EU Regulation, would have an impact on the imports of palm oil, soy, beef, leather, cocoa, coffee, rubber, wood, and maize in the Global North. In October 2021, the Fostering Overseas Rule of Law and Environmentally Sound Trade (FOREST) Act of 2021, in an effort to “deter commodity-driven illegal deforestation around the world,” was introduced in the U.S. Congress. In the UK, the Primary Legislation Environment Act was passed on November 9, 2021, also with the goal of curbing illegal deforestation. In December 2022, the European Commission adopted a regulation on deforestation-free products (EUDR), that covers both legal as well as illegal deforestation. Finally, on June 1, 2023, the European Parliament adopted its negotiating position on the Corporate Sustainability Due Diligence Directive (CSDDD). Under the CSDDD, companies — potentially including those in financial services — will be obligated to demonstrate what action they are taking to protect not only the environment, but also human rights.

Due diligence legislation for companies is a key step to reduce deforestation and human rights violations in supply chains, but it could be strengthened and include financial institutions. The EUDR will initially not directly affect the EU financial sector. As a result, more than 100 CSOs have reacted negatively to this lack of inclusion of the financial sector in the legislation. Moreover, the current deadlines for achieving full supply chain transparency are not in line with the target dates for the implementation of the EU Deforestation Law. For numerous companies, zero-deforestation target deadlines, including that of indirect supply chains, are earliest in 2025, but mostly in 2030 or later. As of December 30, 2024, the key articles of the EUDR will apply. With an ever-increasing market share in the global grains market of Asian banks and investors that do not need to comply with the EUDR, the potential for leakage markets for unsustainable soy and beef is increasing.

Nontransparent, complex cattle and soy supply chains; politics dictate forest loss

While CRR predicted the NDPE model could also work in Latin America, the complex and nontransparent nature of soy and cattle supply chains remains a bottleneck, as are political movements. In Brazil, government policies and politics rather than international action appear to dictate the magnitude of forest loss. Sharp reduction of deforestation rates in Brazil starting in 2004 under the Lula presidency and the record deforestation and fire rates under President Bolsonaro starting in 2019 point to the importance of political will to halt deforestation. Moreover, supply chain transparency and traceability are a major bottleneck in the proper implementation of sustainability commitments, and the soy and cattle supply chains have been lagging in these areas. This situation is aggravated by the Brazilian cattle supply chain having a complex architecture characterized by a high level of fragmentation and tens of thousands of direct and indirect suppliers to meatpackers.

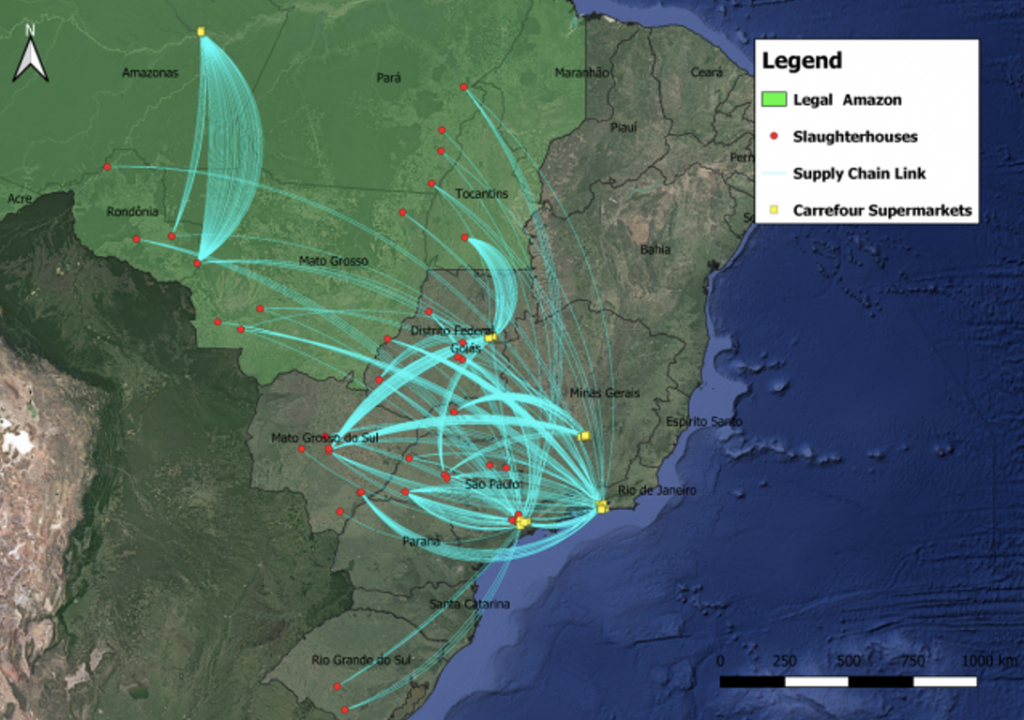

The push for transparency and traceability in the soy and beef supply chains is nevertheless mounting, and the trend is toward more pressure on meatpackers and soy traders to adopt and implement zero-deforestation policies. CRR and others (e.g. Trase, Carbon Disclosure Project, Rota do Gado) are contributing to improved transparency and traceability in beef and soy supply chains. CRR uncovered direct and indirect suppliers of major deforestation-risk companies linked to soy and beef sectors, highlighted the geographies of risk in their supplier base (Figure 3), and revealed insights on who is financing them. CRR has put pressure on key actors to adopt and implement zero-deforestation policies, by means of company risk profiles and continuous monitoring of the major meatpackers (e.g. JBS, Marfrig and Minerva); soy producers, land investors, and traders (e.g. ADM, Amaggi, BrasilAgro, Bunge, Cargill, Cofco, Glencore/Viterra, JJF Holding, Louis Dreyfus, SLC Agrícola, Sodrugestvo); retailers (Carrefour, Casino, Cencosud); and FMCG companies (e.g. Yum China, Mondelēz, Unilever, Procter & Gamble, Neste).

Figure 3: Uncovering supply chain linkages in the beef sector

Source: Chain Reaction Research, based on AidEnvironment data. Figure visualizes the supply chain linkages of Brazilian slaughterhouses and Carrefour supermarkets identified through the analysis of 480 Carrefour beef products.

Private sector initiatives, such as the Soft Commodities Forum (SFC), have united the largest soy traders including Cargill, Bunge, Louis Dreyfus Company, Glencore Agriculture (rebranded as Viterra in 2020), and COFCO International, in developing a common framework for supplier traceability in high deforestation and fire-risk regions. However, this initiative and soy trader’s zero-deforestation pledges are not yet adequate to prevent the conversion of natural habitats. Moreover, soy traders still do not publicly disclose their suppliers. The focus lies mostly on eliminating illegal deforestation from supply chains. As the Brazilian Forest Code permits extensive legal deforestation in the Cerrado, soy traders are still not incentivized to publicize sourcing records, thus inhibiting more granular analysis and mitigation of fire risk.

CRR’s financial analysis provides tools for investors

CRR’s financial analysis provided five important tools to financial institutions (FIs) and CSOs to improve respectively their risk assessment and their campaigning:

- Sustainability officers, investors, and account managers with banks have improved the evaluation of their investments by calculating the total financial risk of assets linked to deforestation.

- A valuation methodology on reputation risk helps to expand the universe of forest-risk sectors from upstream to downstream. Downstream refers to FMCGs and food retailers.

- By linking financial flows with financial institutions’ deforestation policies, banks and pension funds along with their asset managers became aware of potential conflicts and reputation risk.

- A methodology to calculate the profit distribution in a supply chain raises transparency of “who is earning what.” This supports discussions on accountability for all damage done and future costs.

- The assessment of the costs of creating a sustainable supply chain, combined with the profit distribution model, gives insight into the relative costs of a “best-in-class” NDPE approach for downstream companies. The confrontation with the risk of reputation value distortion enables decisions on the question accountability.

The value numbers linked to financial risks raised transparency for financiers

Value numbers linked to financial risks have spurred companies and financiers to take action. In 2016, CRR analyzed that IOI Group could face a suspension from Roundtable on Sustainable Palm Oil (RSPO) certification, leading to market access risk and a sharp share price decline. This was an example of a business risk to financiers. The concepts of stranded asset risk, revenue risk (or market access risk), regulation risk, operational risk, and financing risk are very well applicable to upstream companies like IOI. The annualized values can be related to annual profits, while the values translated to a discounted cash flow (DCF) value can be compared to the current market/equity value or the enterprise value. The financial markets might already have discounted it as a material client of Sawit Sumbermas Sarana (SSMS), a relevant example is how Unilever discounted a part of these value risks in the existing valuation, but the size is difficult to assess. However, if financial risks become a major part of the enterprise value, management, owners, and financiers may be concerned. Next to financiers, buyers/sourcing companies of palm oil have acted when they became aware of their leverage opportunity in a palm oil plantation. A relevant example is how Unilever, as a material client of Sawit Sumbermas Sarana (SSMS), pressed the plantation company to change its policies.

The calculation of reputation risk: A new methodology

Reputation risk can be material for downstream companies/FMCGs. For downstream actors, such as FMCGs, food retailers, food service companies and (fast-food) restaurants, CRR investigated the value of reputation risk. This study pointed to value risks of up to 30 percent in case a company structurally lacked to act on sustainability events, while companies with a proactive approach can gain 20 percent in valuation. As a result, the difference in share price performance might be 70 percent between companies which structurally neglected to act (from an index of 100 to 70) and companies with a pro-active approach (from 100 to 120). Social media attention has widened this reputation risk valuation gap further during the last 20 years. In various follow-up studies, further refinements have been made, including applying adjustment factors: Each new case requires in-depth research as a company’s business model and is not always 100 percent dependent. For instance, palm oil, and thus reputation risk, is not 30 percent of the whole companies’ value but only for the relevant part.

Financial flows might conflict with a financial institution’s deforestation policy

Financiers’ deforestation policies sometimes conflict with their clients’ conduct. Based on financial relation analysis and a database like Forests & Finance, CRR has identified financiers of forest-risk sectors and companies. Financiers’ zero deforestation policies sometimes conflict with clients that they finance: While various FIs have made investments in JBS or Cargill, for example, these FIs, or their holdings, have zero deforestation policies. Consequently, FIs will be confronted with a reputation risk. On many occasions, CRR has communicated these inconsistencies to FIs. The next step for a FI can be to engage with the company linked to deforestation, or to divest. Financiers do not often publicly communicate about their engagement and/or divestment and have not provided feedback to CRR.

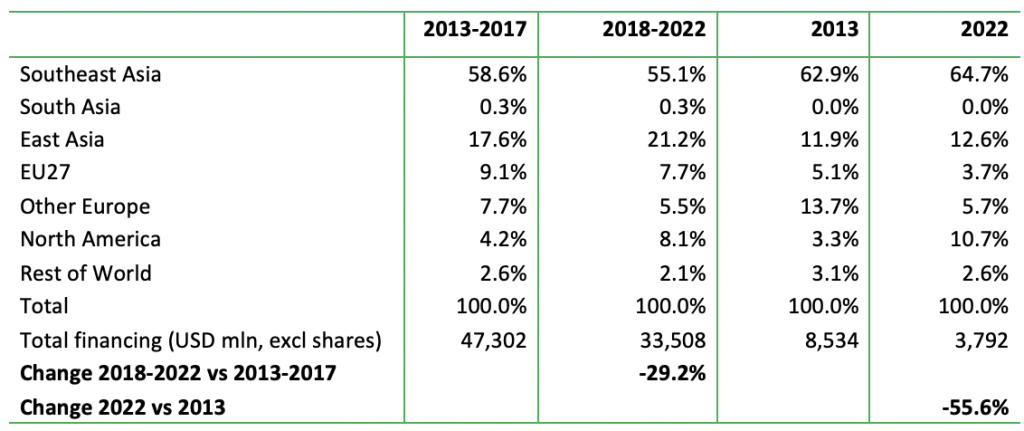

Financiers, particularly those in Europe, have reduced their exposure to forest-risk activities. An important consequence of a sharp increase in attention to deforestation reduction and the establishment of deforestation policies is FIs having materially reduced their exposure to activities that could be linked to commodities with a high deforestation risk. For instance, from 2013 to 2022, the identified financial flows to the Indonesian palm oil sector declined by 56 percent (Figure 4 below). In a five-year period, financial flows declined by 29 percent. The relative position of European FIs has declined, while North American and East Asian (mostly Japanese) FIs saw an increase in its relative position.

However, most regions reduced their absolute financial flows. This is an indication that the availability of capital has contracted, or that financing instruments that are more difficult to identify — or more obscure or nontransparent — have filled the gap. An effect of these developments is that the capital costs of this forest-risk activity (palm oil) could face an increase (due to less supply). Higher costs for capital increase the total costs of projects, and this impacts further expansion of deforestation-linked investments. In 2022, the identified shareholdings in forest-risk activities in palm oil were worth USD 15,257 million, or USD 15.3 billion (Forests & Finance), which was 46 percent of the non-shareholding financial flows in 2018-2022. Important shareholders’ jurisdictions are Southeast Asia (51 percent) and North America (29 percent).

Figure 4: Changes in financing to Indonesian palm oil sector (excluding shares)

Source: Forests & Finance

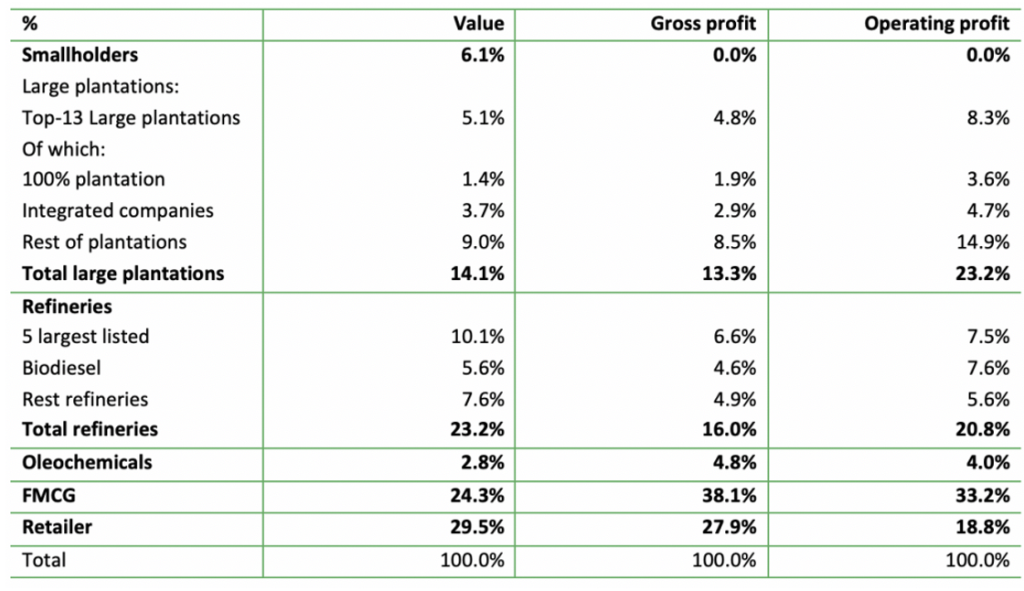

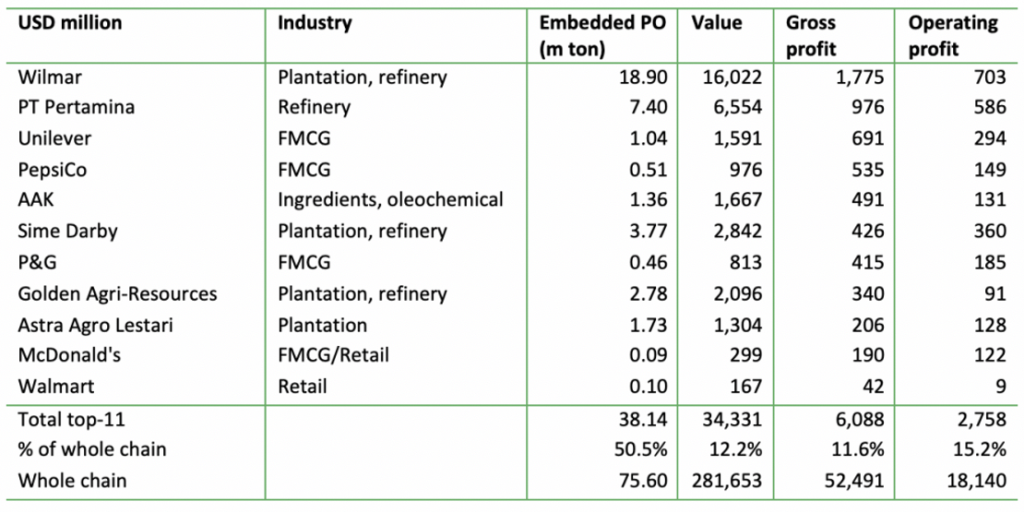

The profit distribution model adds to transparency of beneficiaries and accountability regarding deforestation

The profit chain analysis of palm oil revealed that 66 percent of gross profits and 52 percent of operating profits on embedded palm oil are earned by FMCGs and food retailers (Figure 5). This methodology has been regularly quoted by CSOs. For example, Solidaridad has used this methodology in its Palm Oil Barometer. In 2023, Nestlé took action to increase its accountability for a sustainable palm oil chain with more support to smallholders.

Figure 5: Percentage distribution of value and profit generated in the palm oil chain

Source: Chain Reaction Research, annual reports, Bloomberg; 2020 data

Wilmar, PT Pertamina, Unilever, and PepsiCo earn most from palm oil embedded in their products (Figure 6). PT Pertamina is Indonesia’s state-owned oil company, which is also a major biofuel producer. Unilever and PepsiCo are large FMCGs, while Wilmar is the world’s leading palm oil trader. Wilmar also has the world’s largest consumer food product franchise with branded products based on palm oil. The company is lagging materially in sourcing sustainable palm oil for its own consumer brands.

Figure 6: Top 11 companies in the palm oil value and profit chain, ranked by gross profit

Source: Chain Reaction Research, annual reports, Bloomberg. PO = palm oil. 2020 data

Assessment of deforestation-free sourcing costs showed doable and mitigated relative impacts

The execution and verification costs of NDPE policies are dwarfed by potential risks. For instance, a “best-in-class” NDPE policy execution in palm oil requires extra costs for those companies that are under-investing. These extra costs include a premium price for sustainable palm oil and, when necessary, for segregated supply chains and due diligence and verification process. Crucially, the costs of these necessary actions are dwarfed by the potential reputation risk losses in the event of no action. Moreover, the costs of execution and verification will be subject to economies of scale and further digitalization. Therefore, the relative costs will decline in the coming years. According to a case study on Procter & Gamble, a best-in-class palm oil policy execution and verification would cost 0.15 percent of net revenues of palm oil containing products. The cost would be 0.11 percent of consumer prices (on the retail level including VAT).

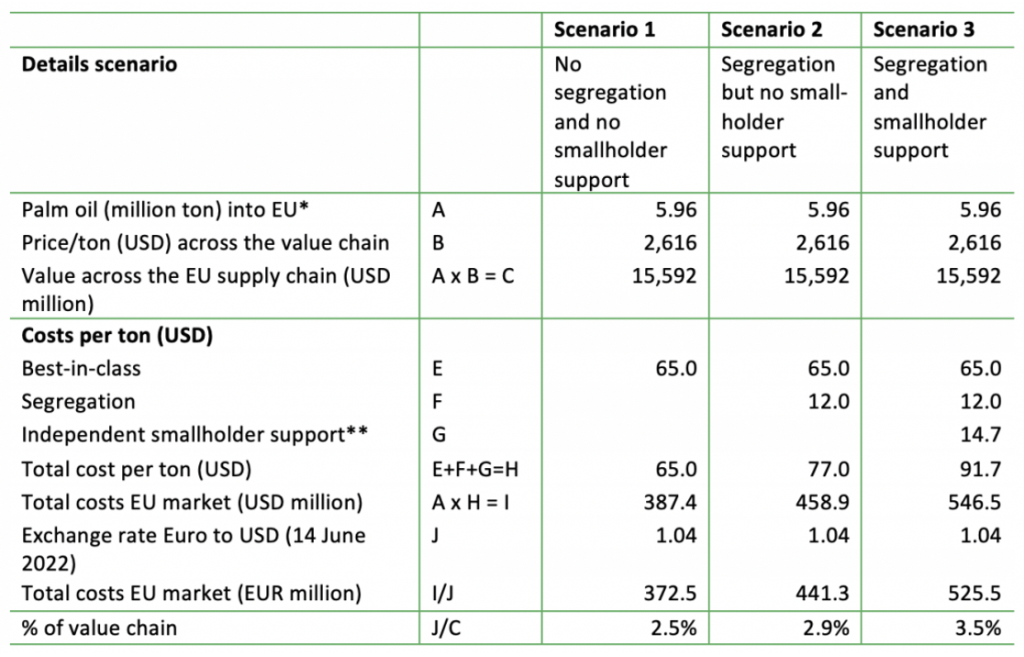

In a CRR report on the implications of the EU Deforestation Regulation, a similar methodology was applied. In various scenarios excluding and including extra costs for segregated supply chains and smallholder support, the total costs would amount to 2.5 to 3.5 percent versus the end value in the supply chain of the embedded palm oil (Figure 7).

Figure 7: Three scenarios: Annual expenditures by EU palm oil-sourcing actors on compliance with EU Deforestation Regulation’s traceability requirement

Source: Profundo, based on previous CRR reports (see web links in text); Indexmundi: *Based on the total of 5.96 million MT of palm oil that was imported in the EU in 2021. **USD 1.1 billion divided by 75m global production.

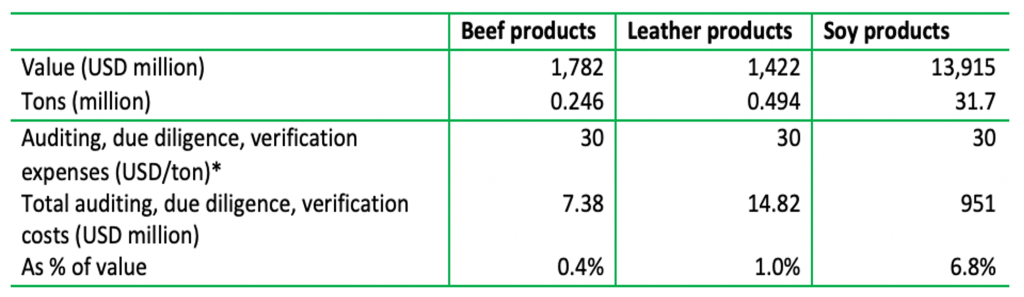

For beef, leather, and soy products, CRR conducted a similar analysis related to the introduction of the EU Deforestation Regulation and the implication for the value chain actors. The necessary price increases in the chain necessary to pay for a best-in-class execution and verification are respectively 0.4 percent, 1.0 percent, and 6.8 percent.

Figure 8: Deforestation-free policy execution and monitoring/verification expenditures

Source: Chain Reaction Research, based on previous report in 2022. *The palm oil per ton policy execution/monitoring/verification costs include around USD 30 for premium pricing of certificated oil; for beef and soy these costs are not included in this calculation, leading to ca USD 30 per ton for policy execution/monitoring/verification.

Despite progress, the work is far from completed

Despite progress in the last ten years, the work is far from complete. A company such as Wilmar, the largest company and biggest earner active in the palm oil supply chain, sources only 7 percent of its palm oil as certified sustainable palm oil (RSPO), while in the global market, 19 percent of production is certified. With just more than 1 percent coverage of RTRS certified soy worldwide, voluntary soy certification schemes have not delivered a broad sustainability shift in soy production. Zero- deforestation commitments of some of the largest global meatpackers and soy traders have targets for 2030, or even later. In Indonesia, there is a rise in deforestation linked to the industrial forest plantation sector. Key areas of concern include the scope of ecosystems protected under national and international laws, the lack of cross-commodity policies, several emerging threats that may increase palm oil-linked deforestation in the near future, the fact that social issues and exploitation in supply chains are still overlooked, and the risk of unintended negative impacts on the climate and livelihoods from the transition from fossil fuels to biofuels.

National and international laws are needed to protect remaining critical ecosystems

While CRR and others have contributed to more attention to global ecosystems at risk, there remains a lack of political support for developing more stringent deforestation laws in several critical ecosystems. This applies, for instance, to Brazil’s Cerrado and Pantanal, and Indonesia’s peatland. Since the launch of the Cerrado Manifesto in September 2017, 160 global FMCG companies and institutional investors have endorsed it. In this manifesto, civil society groups urged immediate action by companies that purchase soy and beef to eliminate deforestation and conversion of native vegetation in the Cerrado. This is necessary since even though Brazil’s Amazon Soy Moratorium was successfully implemented, it has had the unintended consequence of pushing soy production into the Cerrado. Depending on the location, 65 to 80 percent of the properties in the Cerrado can be developed and cleared from native vegetation with approved environmental licenses under Brazil’s Forest Code.

Under current legislation, not all critical ecosystems and native vegetation types are protected. For instance, the EUDR’s scope includes only forest and woodland ecosystems, excluding critical ecosystems such as grasslands (e.g., Cerrado), wetlands (e.g., Pantanal), and peatlands. In 2021, land use in the Cerrado biome showed 14 percent of the native vegetation was forest, 30 percent wooded savannah, and 9 percent other non-forest (i.e., grassland) vegetation. The latter would not be under the scope of the EUDR. In Indonesia, only 30 percent of peat needs to be protected under the peatland regulation. This implies a potential risk of drainage and degradation for the remaining 70 percent of cultivable peatland, which is also not protected under the EUDR. Moreover, permit holders can continue to drain protected peat areas.

Cross-commodity policies are needed

The lack of cross-commodity NDPE implementation involves deforestation risk. CRR revealed how cross-commodity NDPE risks have been overlooked in regulations, voluntary certification schemes, and supplier codes of conduct. Cross-commodity refers to NDPE policies being applied to the entire corporate entity of suppliers in different supply chains rather than just one commodity supply chain, such as palm oil. Some palm oil buyers with NDPE policies who have increasingly removed deforestation-linked palm oil suppliers from their supply chains remain linked to deforestation as a result of their palm oil suppliers continuing to deforest in other sectors, such as timber and mining. Moreover, deforestation regulation and corporate sustainability due diligence proposals, such as those in the EU, are focused on domestic companies and their product streams, instead of the structure of upstream companies. Codes of conduct, RSPO principles, and accountability initiatives also lack explicit criteria for cross-commodity coverage. CRR’s project partner Green Century has been engaging with companies to establish cross-commodity zero deforestation agreements.

Palm oil sector’s emerging threats that may increase deforestation

There are several emerging threats that may increase palm oil-linked deforestation in the near future. Specifically, regarding the world’s largest palm oil producer Indonesia, these threats include the country’s Omnibus Law, the failure to extend the palm oil permit moratorium, the revocation of agricultural, forestry, and mining permits, the revised mining law, and continued logging in Indonesia’s industrial tree sector, coupled with rising global palm oil prices. The Omnibus Law, passed in October 2022, encourages economic investment, and critics fear it will weaken environmental and labor safeguards. For instance, it removes a stipulation that each province in Indonesia must maintain 30 percent forest cover. The Law also makes it easier for exploitative businesses to operate in protected forest areas and simplifies procedures to turn a piece of land from forest to non-forest area.

It remains unclear what the long-term effects of the failure to extend the palm oil permit moratorium will be, bringing about a risk of new oil palm permits being issued. The palm oil moratorium, which involves a ban on issuing new oil palm licenses, has not been extended since September 2021. While it does not apply to forest and peatland within existing palm oil concessions or to natural forests controlled by local government, it did (partly) protect forests and peatlands outside concessions. This is currently no longer the case.

Another threat is the growing risk of independent smallholder deforestation that is linked to the lifecycle of oil palm trees. Oil palm trees have a lifecycle of approximately 25 years, and it has now been 25 years since the start of strong growth in the Southeast Asian palm oil industry. Replacing old trees with new ones might be too costly for many independent smallholders. These smallholders, which have a crucial position in the Indonesian upstream sector, might replace forest for oil palm trees, as it takes three to four years before trees bear fruit.

Finally, there is evidence that palm oil, mining, and industrial tree companies, which had their licenses revoked in January 2022, have actively started clearing forests in their concessions. On January 6, 2022, the President of Indonesia announced that the government would revoke the licenses of more than 2,000 companies since their concessions are considered “stranded land.” What will happen to the revoked concession permits is not yet clear, but the government said it would offer them to farmers and civil society organizations, but critics are challenging this approach.

In the first half of 2023, the industrial forest plantation sector in Indonesia was responsible for significant deforestation, with ten companies collectively contributing to the clearance of 10,000 hectares of forest.

Social issues and exploitation in supply chains are overlooked, particularly in beef and leather

While companies have increasingly adopted NDPE policies to prevent deforestation and peatland degradation, the “No Exploitation” part of the NDPE policies has not yet been standardized. Therefore, the scope and strength of these policies may vary depending on how much weight a commodity company places on social issues. Next to the protection of human and labor rights of workers and local communities, “No Exploitation” may cover a range of social issues. Wilmar International’s NDPE policy, for instance, includes the facilitation of smallholder inclusion into the supply chain, respect for land tenure rights; communities’ free, prior and informed consent (FPIC) to operations on their lands, and the resolution of complaints and conflicts through an open, transparent, and consultative process. Currently, there is no standardization of which social issues exactly fall under the “No Exploitation” part of NDPE policies.

Addressing the “No Exploitation” part of NDPE policies is falling behind in beef and leather supply chains. Forest 500 reveals that in 2023, 72 percent of companies assessed with a deforestation commitment for palm oil also had an FPIC policy. For beef and leather, the percentages were respectively only 45 percent and 20 percent. Since commodity-linked expansion, deforestation, and exploitation issues often go hand in hand, an effective approach to ending deforestation must include inclusive action on human rights abuses in supply chains. In particular, beef and leather industries, major drivers of deforestation, require a comprehensive NDPE policy. The clearing of land, and linked to it land dispossession, can lead to community-company conflicts that can cause serious investment risks for companies and investors, if not addressed properly.

Transition from fossil fuels to biofuels may have unintended negative impacts on climate, livelihoods

The transition from fossil fuels to biofuels may have unintended negative impacts on climate and rural livelihoods. New government regulations in Indonesia, Malaysia, Brazil, Colombia, and other countries that mandate increased biodiesel blends have increased demand for edible oils such as palm oil and soybean oil that are used as feedstock. For instance, Brazil’s RenovaBio policy, implemented in 2020 and formalized as Brazil’s National Biofuels Policy, has revitalized demand for edible oils-based feedstocks, including palm oil. In Indonesia, the government is targeting 100 percent biodiesel (B100). Despite concerns over the impact of demand for palm oil as biofuel on Indonesia’s forests, the government has defended its plan as way to reduce dependency on fossil fuels. In the longer term, efforts to decarbonize the global marine fuel and jet fuel markets may add additional pressure. For instance, civil society organizations have raised concerns that the shift to palm oil- and soy-based biofuels could result in 3.2 million hectares of additional deforestation by 2030.

Biofuel expansion therefore requires the same strict sourcing requirements that are in the most established palm oil markets, but limited transparency and the lack of deforestation policies are the norm in most biofuel and energy companies. Energy and biofuel refineries have become a large client group of palm oil producers, taking up 23 percent of global production of palm oil. However, in general, they lack transparency from which companies they are sourcing: Most of the biofuel/energy companies do not publish a palm oil mill list. In addition, most of them lack a zero-deforestation policy, and thus potentially create a large leakage market for palm oil from deforested land. Globally, 2020’s gross profits on embedded palm oil in biofuels are estimated at USD 2.4 billion and operating profit at USD 1.4 billion. The implementation of zero-deforestation policies plus a best-in-class monitoring/verification system would cost key players in biofuels only a fraction of their profits. Banks and investors that are financing the expanding supply chain in biofuels through plantations and refineries, or through financing Big Oil and other palm oil-using energy companies, should be aware of this new investment risk, including “material” reputation risk.